26

March 17, 2008 New requirements to file material contracts entered into “in the ordinary course of business”

March 17, 2008

New requirements to file material contracts entered into “in the ordinary course of business”

2

I. Introduction

• Amendments to National Instrument 51-102 —Continuous Disclosure Obligations:

Reporting issuers will be required to file certain material contracts entered into in the ordinary course of businessunder section 12.2 of NI 51-102.

• Amendments come into force today in all provinces and territories in Canada.

3

I. Introduction (continued)

• The presentation will be divided into two parts:• the previous regulatory requirements; and• the new requirements.

• We will attempt to answer the following questions:• What constitutes a material contract?• Must all material contracts entered into in the ordinary course

of business be filed?• What information can be omitted or redacted?• What are the applicable delays?• What should I do following the new rules coming into force?

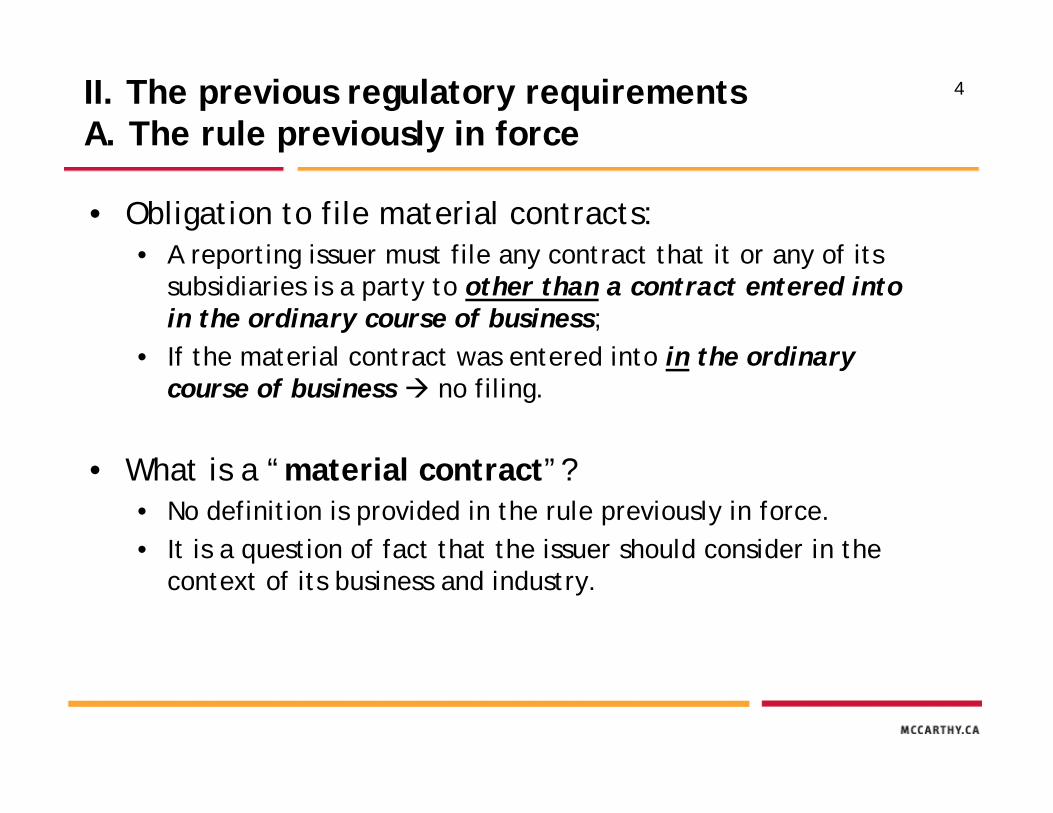

4II. The previous regulatory requirementsA. The rule previously in force

• Obligation to file material contracts:• A reporting issuer must file any contract that it or any of its

subsidiaries is a party to other than a contract entered into in the ordinary course of business;

• If the material contract was entered into in the ordinary course of business no filing.

• What is a “material contract”?• No definition is provided in the rule previously in force.• It is a question of fact that the issuer should consider in the

context of its business and industry.

5B. Filing of a material contract under the previous rules

Material fact or material change

• Procedure• Immediately after entering into a material contract which

constituted a material fact or a material change, the reporting issuer had to issue and file a news release on SEDAR disclosing the nature and substance of the contract.

• The reporting issuer had to also file a material change report on SEDAR, along with the material contract if it is entered into outside the ordinary course of business.

• Delay• A material contract entered into outside the ordinary course of

business had to be filed on SEDAR at the same time the material change report was filed within 10 days of the execution of the contract.

6B. Filing of a material contract under the previous rules (continued)

Not a material fact or material change

• A material contract entered into outside the ordinary course of business which did not constitute a material fact or a material change also had to be filed on SEDAR: • at the time the annual information form (AIF) was filed, if the

contract is entered into before the date of the AIF; or• if the issuer was not required to file an AIF, no later than 120

day after the end of the last financial year, if the contract isentered into before the end of the financial year.

7III. The new regulatory requirementsA. What is a “material contract”?

• Definition of “material contract”:“any contract that the reporting issuer or any of its subsidiaries is a party to, that is material to the issuer”

• The addition of this definition does not change existing practices. A contract which was previously “material”remains a material contract.

• The question of whether a reporting issuer has entered into a material contract should still be interpreted in the context of the issuer’s business and industry.

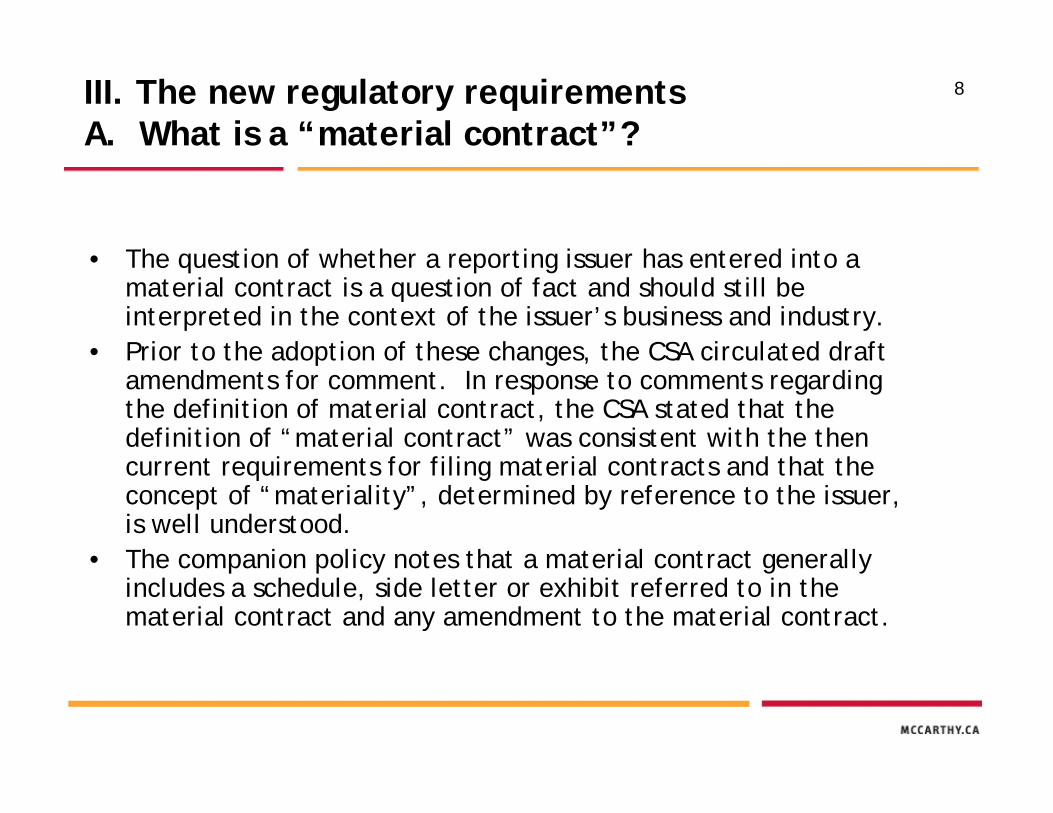

8III. The new regulatory requirementsA. What is a “material contract”?

• The question of whether a reporting issuer has entered into a material contract is a question of fact and should still be interpreted in the context of the issuer’s business and industry.

• Prior to the adoption of these changes, the CSA circulated draftamendments for comment. In response to comments regarding the definition of material contract, the CSA stated that the definition of “material contract” was consistent with the then current requirements for filing material contracts and that the concept of “materiality”, determined by reference to the issuer, is well understood.

• The companion policy notes that a material contract generally includes a schedule, side letter or exhibit referred to in the material contract and any amendment to the material contract.

9B. What material contracts must be disclosedand filed?

• For contracts entered into outside the ordinary course of business no change.

• For contracts entered into in the ordinary course of business The reporting issuer is not required to file the material contract, unless the material contract is:• any contract to which directors, officers or promoters are

parties, other than an employment contract;

To determine whether it is dealing with an employment contract, the reporting issuer may consider whether it contains payment or other provisions that are required to be disclosed as executive compensation in a management information circular (under Schedule 51-102F6).

10

• any continuing contract to sell the majority of the reporting issuer’s products or services or to purchase the majority of the reporting issuer’s requirements for goods, services or raw materials;

• any franchise, license or other agreement to use a patent, formula, trade secret, process or trade name;

• any financing or credit agreement, with terms that have a direct correlation with anticipated cash distribution;

• any external management or external administrationcontract; or

• any contract upon which the reporting issuer’s business is substantially dependent.

B. What material contracts must be disclosed and filed? (continued)

11What material contracts must be disclosed and filed? (continued)

• What does “substantially dependent” mean under the U.S. securities rules?• The new Canadian requirements very closely follow the approach of

the U.S. rules contained in s. 601(b)(10) of Regulation S-K.• The SEC has not issued any official statement; the following

constitutes the SEC’s unofficial position and accepted practices.• The analysis depends on circumstances and facts. For example:

• a patent licensing agreement on which the issuer’s activities are dependent to a material extent;

• a distribution contract which represents over 25% of the revenue of a senior issuer.

• Senior issuers very rarely file contracts under this category.

12

• What does “substantially dependent” mean in the Canadian regulatory context?• It is more precise than the meaning contained in the U.S. rules.• It is a contract that is so material that the issuer’s business is

dependent on its continuation.• The companion policy provides a few examples of this type of

contract, all of which refer to “the majority”. The CSA, in responding to comments, explicitly stated that “majority” means greater than 50%.

B. What material contracts must be disclosed and filed? (continued)

13

• Examples of material contracts on which the reporting issuer’s business is substantially dependent:• A financing or credit agreement providing a majority of the

reporting issuer’s capital requirements for which alternative financing is not readily available at comparable terms.

• A contract for the acquisition or sale of all or substantially all of the reporting issuer’s property, plant and equipment or assets.

• An option, joint venture, purchase or other agreement relating to a mining or oil and gas property that represents a majority of the reporting issuer’s business.

B. What material contracts must be disclosed and filed? (continued)

14

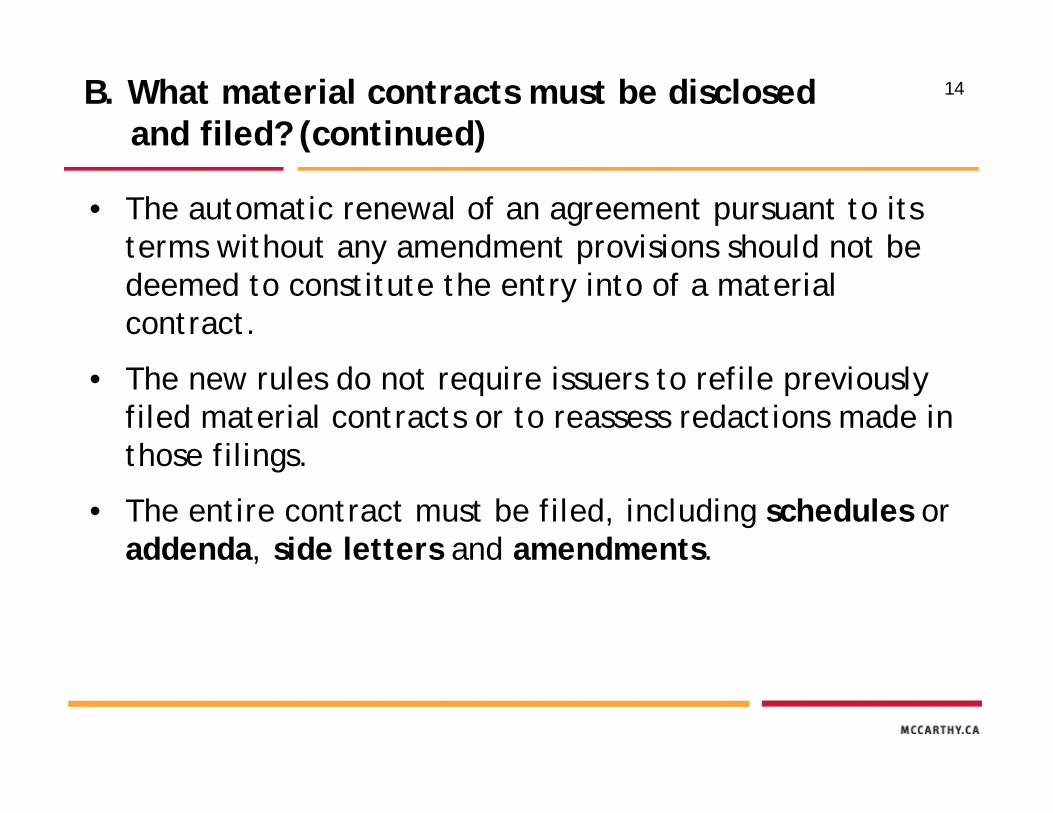

• The automatic renewal of an agreement pursuant to its terms without any amendment provisions should not be deemed to constitute the entry into of a material contract.

• The new rules do not require issuers to refile previously filed material contracts or to reassess redactions made in those filings.

• The entire contract must be filed, including schedules or addenda, side letters and amendments.

B. What material contracts must be disclosed and filed? (continued)

15C. Can certain information be omitted or redacted?

• Certain provisions of a material contract may be omitted or redacted if an executive officer has reasonable grounds to believe that its disclosure:• would be seriously prejudicial to the interests of the reporting

issuer; or• would violate confidentiality provisions.

• An issuer who omits or deletes a provision must include, immediately after the omission or deletion, in the filed copy, a description of the type of information that has been omitted or redacted. A brief one-sentence description is generally sufficient.

16C. Can certain information be omitted or redacted? (continued)

• What constitutes disclosure seriously prejudicial to the interests of the reporting issuer?• We expect the exceptions to be interpreted restrictively.• The American experience:

• in general, only manufacturing secrets and pricing information may be omitted; and

• a “word by word” approach to redaction is preferred, rather than redaction of entire sections.

• Disclosure contrary to Canadian privacy laws, for example, namesof employees, salaries and other confidential details regarding employees, could be viewed as seriously prejudicial (except if the disclosure is specifically required by the regulations).

17C. Can certain information be omitted or redacted? (continued)

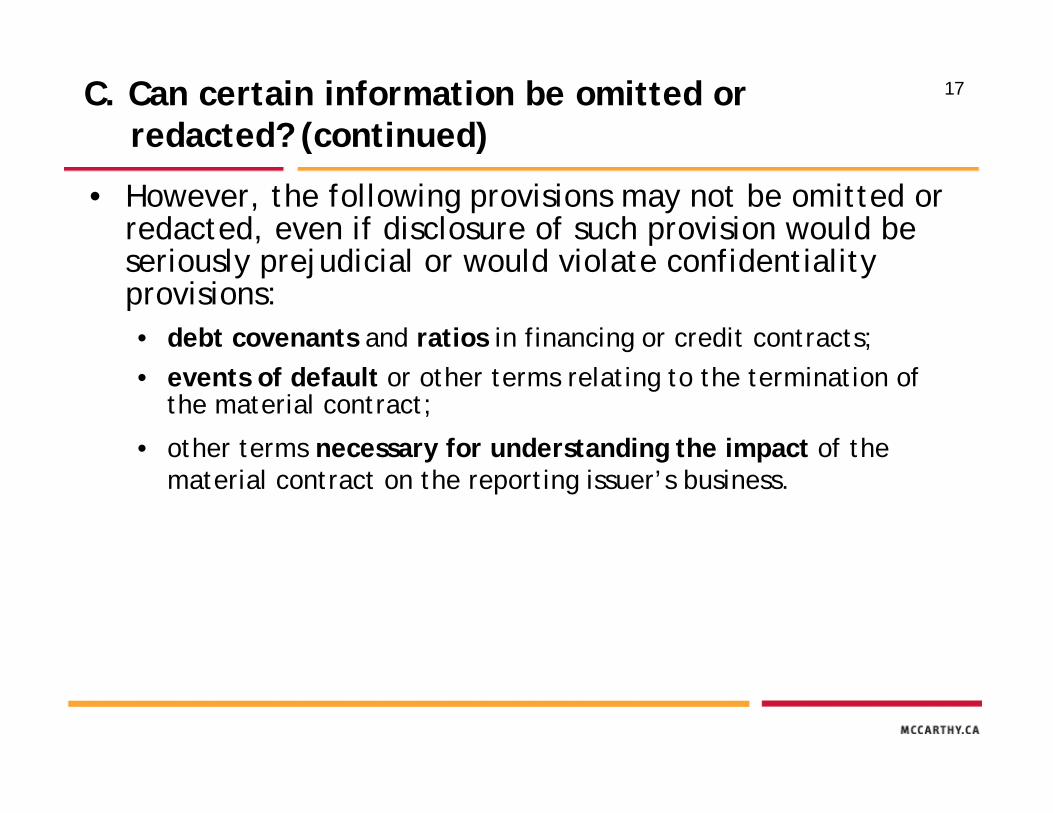

• However, the following provisions may not be omitted or redacted, even if disclosure of such provision would be seriously prejudicial or would violate confidentiality provisions:• debt covenants and ratios in financing or credit contracts;• events of default or other terms relating to the termination of

the material contract;

• other terms necessary for understanding the impact of the material contract on the reporting issuer’s business.

18C. Can certain information be omitted or redacted? (continued)

• What are the terms “necessary to understand the impact” of a material contract:• the duration and nature of a patent, trademark, license,

franchise or concession;

• disclosure regarding related party transactions; and

• contingency, indemnification, anti-assignability, take-or-pay clauses or change-of-control clauses.

19C. Can certain information be omitted or redacted? (continued)

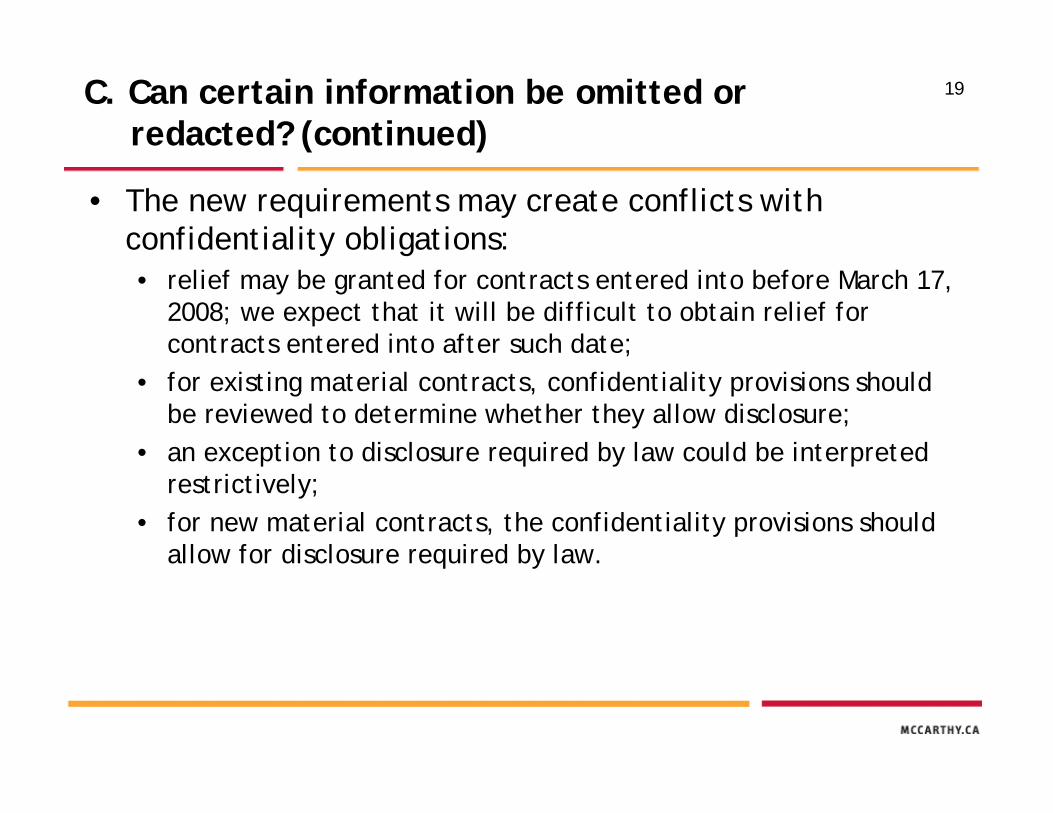

• The new requirements may create conflicts with confidentiality obligations:• relief may be granted for contracts entered into before March 17,

2008; we expect that it will be difficult to obtain relief for contracts entered into after such date;

• for existing material contracts, confidentiality provisions should be reviewed to determine whether they allow disclosure;

• an exception to disclosure required by law could be interpreted restrictively;

• for new material contracts, the confidentiality provisions should allow for disclosure required by law.

20

D. Planning

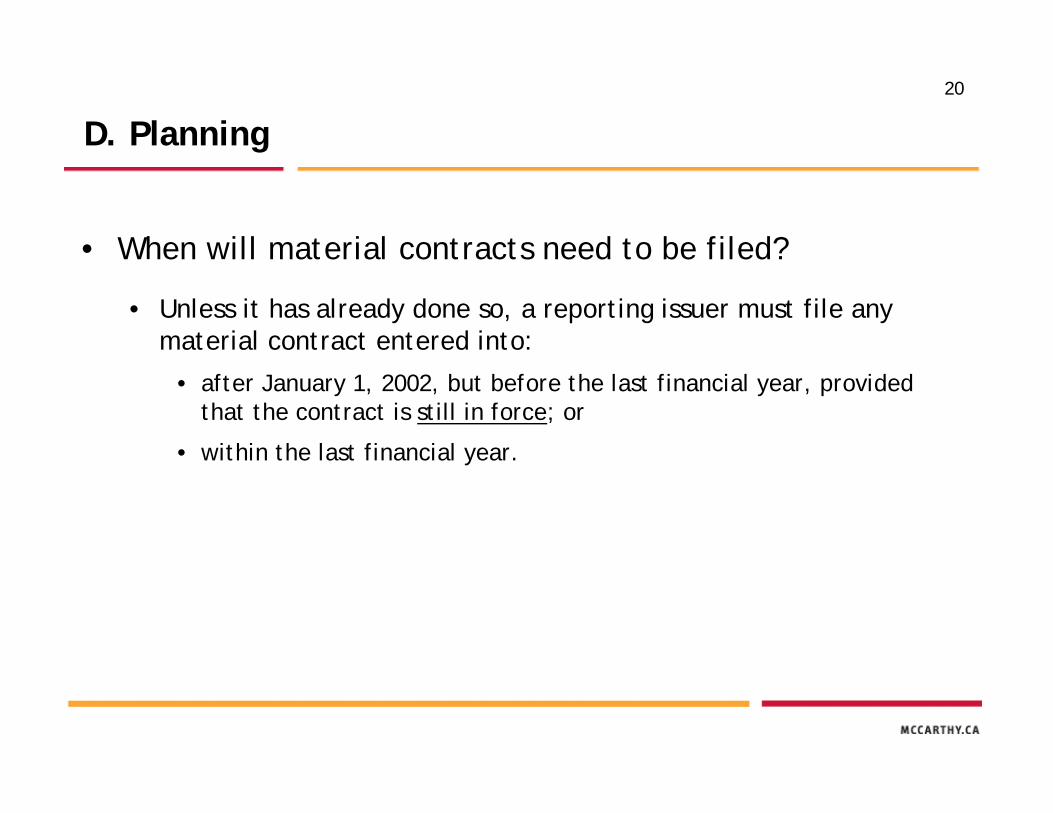

• When will material contracts need to be filed?

• Unless it has already done so, a reporting issuer must file any material contract entered into:

• after January 1, 2002, but before the last financial year, provided that the contract is still in force; or

• within the last financial year.

21

D. Planning (continued)

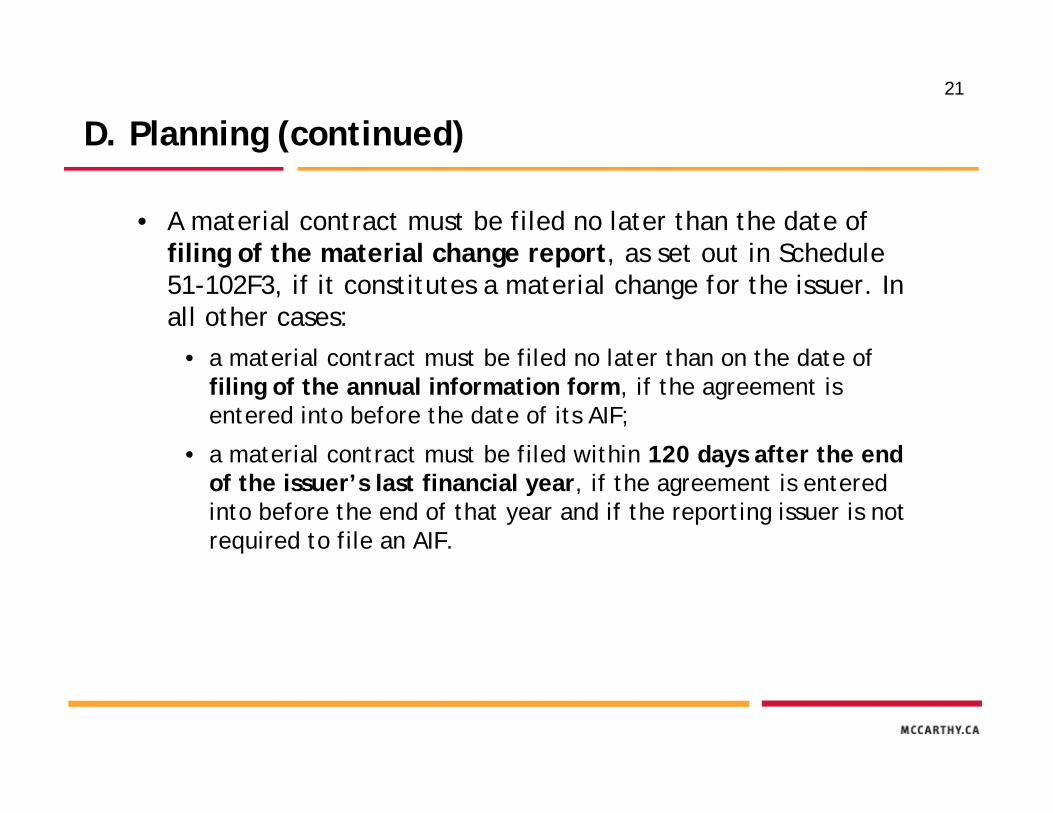

• A material contract must be filed no later than the date of filing of the material change report, as set out in Schedule 51-102F3, if it constitutes a material change for the issuer. In all other cases:

• a material contract must be filed no later than on the date of filing of the annual information form, if the agreement is entered into before the date of its AIF;

• a material contract must be filed within 120 days after the end of the issuer’s last financial year, if the agreement is entered into before the end of that year and if the reporting issuer is not required to file an AIF.

22

D. Planning (continued)

• Reporting issuers whose financial year ended on December 31, 2007 and who filed their AIF prior to March 17, 2008, will not be required to meet the new filing requirements until the reporting issuer files for the financial year ended December 31, 2008 in 2009.

• These previous material contracts must nonetheless be disclosed and filed in 2009 if they are still in force.

• There is no transition period.

23

E. Practical considerations

• Bear these new requirements in mind when negotiating new contracts, particularly for issuers who have a low materiality threshold.

• Ensure that the confidentiality clauses of the contract allow filing on SEDAR.

• We recommend that you identify those standard form contracts likely to constitute material contracts and establish a systematic review process.

24

E. Practical considerations (continued)

• Establish guidelines, particularly for the benefit of persons in your organization who are involved in drafting and negotiating contracts.

• Upon renewal of a contract which has not been filed, consider whether the contract has become “material”.

• Be careful not to disclose personal information in contravention of privacy legislation.

25

IV. Conclusion

• The new requirements will come into force this March 17.

• Question period.

VancouverP.O. Box 10424, Pacific CentreSuite 1300 777 Dunsmuir Street Vancouver BC V7Y 1K2Tel: 604-643-7100 Fax: 604-643-7900

CalgarySuite 3300 421 – 7th Avenue SWCalgary AB T2P 4K9Tel: 403-260-3500 Fax: 403-260-3501

TorontoBox 48, Suite 5300 Toronto Dominion Bank TowerToronto ON M5K 1E6Tel: 416-362-1812 Fax: 416-868-0673

OttawaThe ChambersSuite 1400 40 Elgin StreetOttawa ON K1P 5K6Tel: 613-238-2000 Fax: 613-563-9386

MontréalSuite 25001000 De La Gauchetière Street WestMontréal QC H3B 0A2Tel: 514-397-4100 Fax: 514-875-6246

QuébecLe Complexe St-Amable1150, rue de Claire-Fontaine, 7e étageQuébec QC G1R 5G4Tel: 418-521-3000 Fax: 418-521-3099

United Kingdom & Europe5 Old Bailey, 2nd FloorLondon, England EC4M 7BATel: +44 (0)20 7489 5700 Fax: +44 (0)20 7489 5777