25

NEW ZEALAND ENERGY CORP. Corporate Presentation August 2011 NEW ZEALAND ENERGY CORP.

NEW ZEALAND ENERGY CORP.

Corporate Presentation August 2011

NEW ZEALAND ENERGY CORP.

New Zealand Energy Corp.

2

Introduction

New Zealand

• 130,000 boe/d and growing

• Proven hydrocarbon system with multiple basins and numerous prospective formations

• 5% revenue royalty attracting significant investment from quality players

Properties

• 5 permits >>> 2 permits focused on large conventional targets (West Coast) and 3 permits focused on two unconventional targets (East Coast)

- West Coast: Discovery in Feb 2011 and conventional exposure to 729.5 mmboe of OOIP(1) and 66.6 mmboe prospective resource(2) >>> Focus for 2011

- East Coast: Basin provides exposure to international size unconventional play potential >>> 22.3 billion barrels OOIP(1) >>> Option Value

Team

• Western Canadian Sedimentary Basin (“WCSB”) leadership with proven track record of value creation

• In-country expertise involved in 100 million bbls of reserve accumulations

• Proprietary technical database key to NZEC Exploration / Exploitation Model

Production, Cashflow, Resource to Reserves

• Exploit Conventional Discovery and Area Surrounding >>> West Coast

• Unlock World Class Resource Play >>> Evaluate 200+ metres of pay in East Coast Basin well controlled by NZEC

(1) Net Undiscovered Petroleum Initially In Place (OOIP) as identified by AJM Petroleum Consultants

(2) AJM Petroleum Consultants Net Prospective Resource (best estimate)

New Zealand Energy Corp.

3

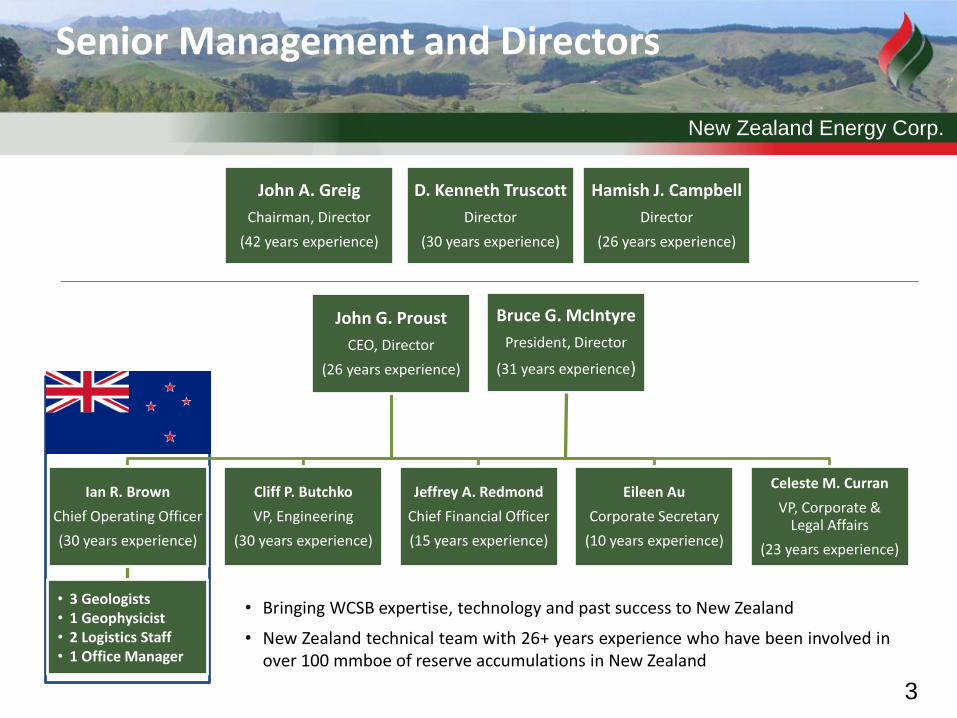

John A. Greig

Chairman, Director

(42 years experience)

Hamish J. Campbell

Director

(26 years experience)

D. Kenneth Truscott

Director

(30 years experience)

John G. Proust

CEO, Director

(26 years experience)

Ian R. Brown

Chief Operating Officer

(30 years experience)

Cliff P. Butchko

VP, Engineering

(30 years experience)

Jeffrey A. Redmond

Chief Financial Officer

(15 years experience)

Eileen Au

Corporate Secretary

(10 years experience)

Celeste M. Curran

VP, Corporate & Legal Affairs

(23 years experience)

Bruce G. McIntyre

President, Director

(31 years experience)

Senior Management and Directors

• 3 Geologists • 1 Geophysicist • 2 Logistics Staff • 1 Office Manager

• Bringing WCSB expertise, technology and past success to New Zealand

• New Zealand technical team with 26+ years experience who have been involved in over 100 mmboe of reserve accumulations in New Zealand

New Zealand Energy Corp.

4

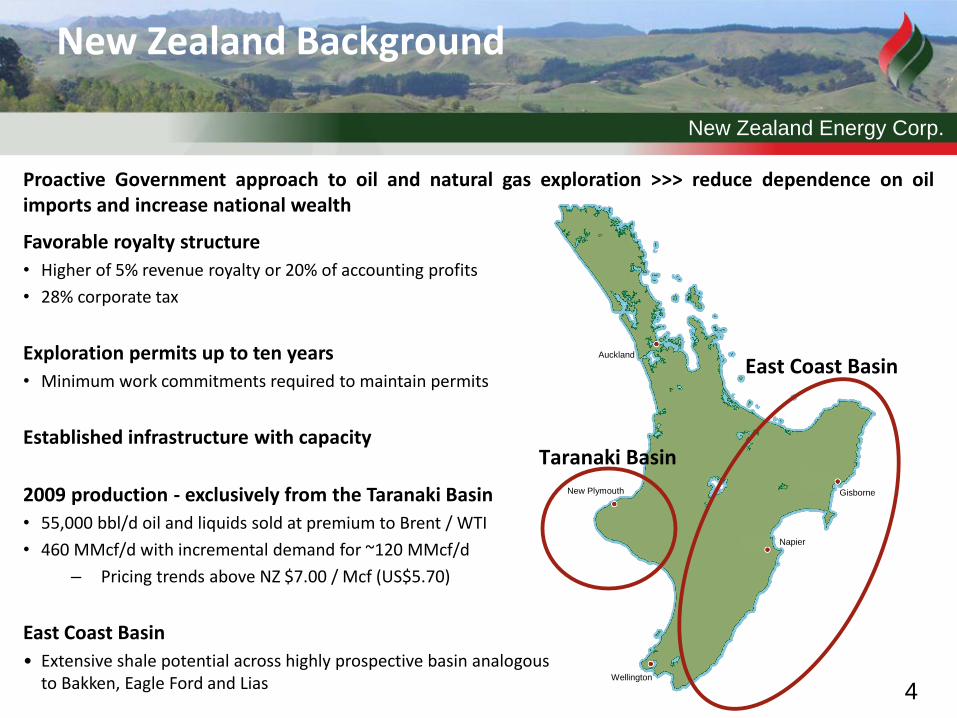

New Zealand Background

Favorable royalty structure

• Higher of 5% revenue royalty or 20% of accounting profits

• 28% corporate tax

Exploration permits up to ten years

• Minimum work commitments required to maintain permits

Established infrastructure with capacity

2009 production - exclusively from the Taranaki Basin

• 55,000 bbl/d oil and liquids sold at premium to Brent / WTI

• 460 MMcf/d with incremental demand for ~120 MMcf/d

– Pricing trends above NZ $7.00 / Mcf (US$5.70)

East Coast Basin

• Extensive shale potential across highly prospective basin analogous to Bakken, Eagle Ford and Lias

Proactive Government approach to oil and natural gas exploration >>> reduce dependence on oil imports and increase national wealth

New Plymouth Gisborne

Napier

Wellington

Auckland

East Coast Basin

Taranaki Basin

New Zealand Energy Corp.

5

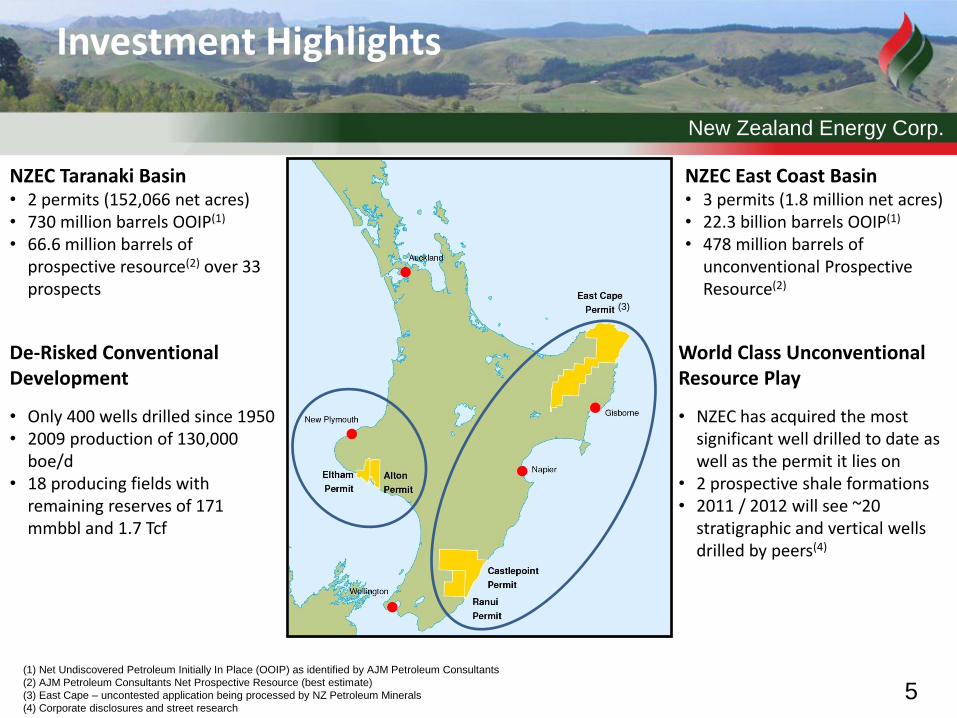

Investment Highlights

NZEC Taranaki Basin • 2 permits (152,066 net acres) • 730 million barrels OOIP(1)

• 66.6 million barrels of prospective resource(2) over 33 prospects

(1) Net Undiscovered Petroleum Initially In Place (OOIP) as identified by AJM Petroleum Consultants

(2) AJM Petroleum Consultants Net Prospective Resource (best estimate)

(3) East Cape – uncontested application being processed by NZ Petroleum Minerals

(4) Corporate disclosures and street research

NZEC East Coast Basin • 3 permits (1.8 million net acres) • 22.3 billion barrels OOIP(1)

• 478 million barrels of unconventional Prospective Resource(2)

2011 Focus (cont.) 3. Advance unconventional

resource through exploration of the most significant well drilled to date

• Re-entry and evaluate 200+ metres of prospective unconventional pay

2011 Focus 1. Copper Moki discovery >>>

“Greater Cheal Area” • Convert discovery to production

immediately • Convert resource to reserves by

year end 2. Repeat Copper Moki exploration

model in new area and formation

(3)

• Only 400 wells drilled since 1950 • 2009 production of 130,000

boe/d • 18 producing fields with

remaining reserves of 171 mmbbl and 1.7 Tcf

• NZEC has acquired the most significant well drilled to date as well as the permit it lies on

• 2 prospective shale formations • 2011 / 2012 will see ~20

stratigraphic and vertical wells drilled by peers(4)

World Class Unconventional Resource Play

De-Risked Conventional Development

New Zealand Energy Corp.

6

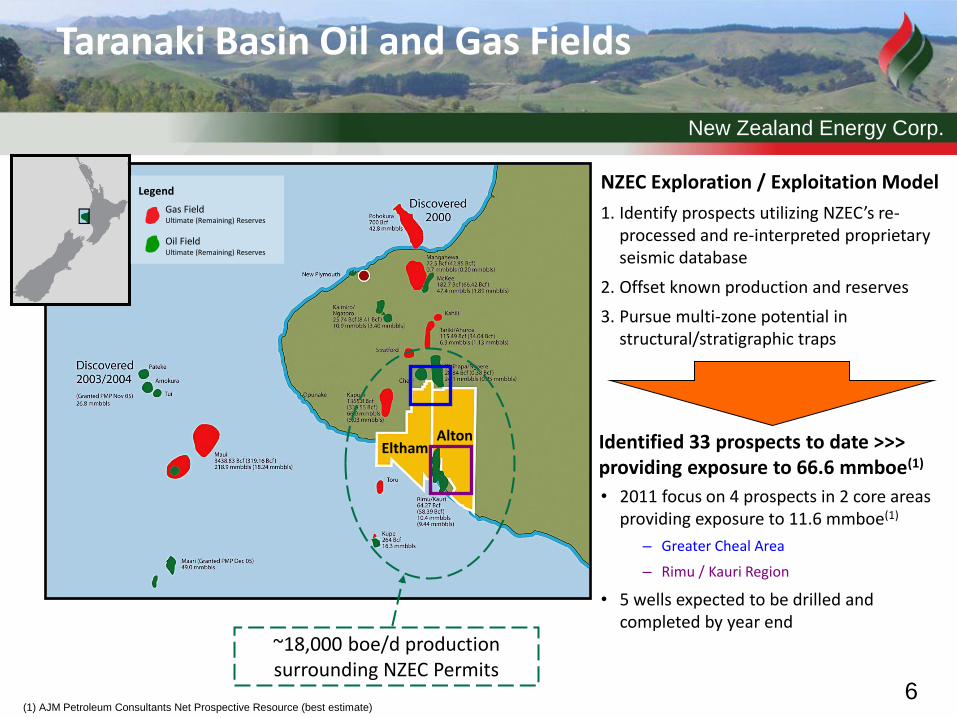

Identified 33 prospects to date >>> providing exposure to 66.6 mmboe(1)

NZEC Exploration / Exploitation Model

1. Identify prospects utilizing NZEC’s re-processed and re-interpreted proprietary seismic database

2. Offset known production and reserves

3. Pursue multi-zone potential in structural/stratigraphic traps

Taranaki Basin Oil and Gas Fields

Legend

Gas Field Ultimate (Remaining) Reserves

Oil Field Ultimate (Remaining) Reserves

~18,000 boe/d production surrounding NZEC Permits

Alton Eltham

• 2011 focus on 4 prospects in 2 core areas providing exposure to 11.6 mmboe(1)

– Greater Cheal Area

– Rimu / Kauri Region

• 5 wells expected to be drilled and completed by year end

(1) AJM Petroleum Consultants Net Prospective Resource (best estimate)

New Zealand Energy Corp.

7

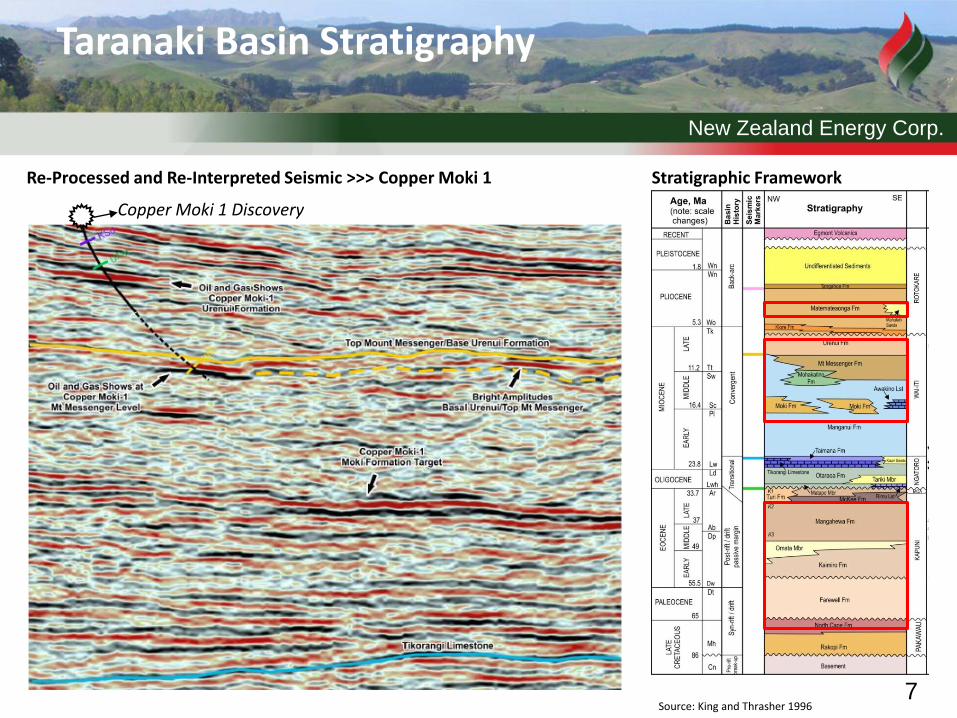

Taranaki Basin Stratigraphy

Source: King and Thrasher 1996

Stratigraphic Framework Re-Processed and Re-Interpreted Seismic >>> Copper Moki 1

Copper Moki 1 Discovery

New Zealand Energy Corp.

8

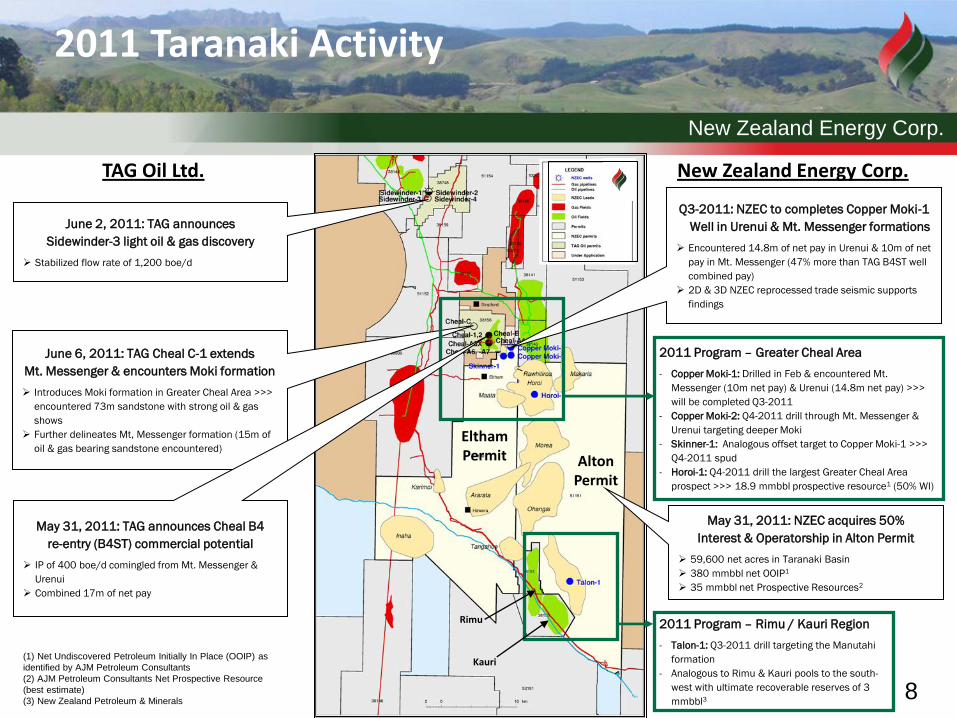

2011 Taranaki Activity

(1) Net Undiscovered Petroleum Initially In Place (OOIP) as

identified by AJM Petroleum Consultants

(2) AJM Petroleum Consultants Net Prospective Resource

(best estimate)

(3) New Zealand Petroleum & Minerals

June 2, 2011: TAG announces

Sidewinder-3 light oil & gas discovery

Stabilized flow rate of 1,200 boe/d

May 31, 2011: NZEC acquires 50%

Interest & Operatorship in Alton Permit

59,600 net acres in Taranaki Basin

380 mmbbl net OOIP1

35 mmbbl net Prospective Resources2

Q3-2011: NZEC to completes Copper Moki-1

Well in Urenui & Mt. Messenger formations

Encountered 14.8m of net pay in Urenui & 10m of net

pay in Mt. Messenger (47% more than TAG B4ST well

combined pay)

2D & 3D NZEC reprocessed trade seismic supports

findings

June 6, 2011: TAG Cheal C-1 extends

Mt. Messenger & encounters Moki formation

Introduces Moki formation in Greater Cheal Area >>>

encountered 73m sandstone with strong oil & gas

shows

Further delineates Mt, Messenger formation (15m of

oil & gas bearing sandstone encountered)

2011 Program – Rimu / Kauri Region

- Talon-1: Q3-2011 drill targeting the Manutahi

formation

- Analogous to Rimu & Kauri pools to the south-

west with ultimate recoverable reserves of 3

mmbbl3

Alton Permit

Eltham Permit

2011 Program – Greater Cheal Area

- Copper Moki-1: Drilled in Feb & encountered Mt.

Messenger (10m net pay) & Urenui (14.8m net pay) >>>

will be completed Q3-2011

- Copper Moki-2: Q4-2011 drill through Mt. Messenger &

Urenui targeting deeper Moki

- Skinner-1: Analogous offset target to Copper Moki-1 >>>

Q4-2011 spud

- Horoi-1: Q4-2011 drill the largest Greater Cheal Area

prospect >>> 18.9 mmbbl prospective resource1 (50% WI)

Rimu

Kauri

May 31, 2011: TAG announces Cheal B4

re-entry (B4ST) commercial potential

IP of 400 boe/d comingled from Mt. Messenger &

Urenui

Combined 17m of net pay

TAG Oil Ltd. New Zealand Energy Corp.

New Zealand Energy Corp.

9

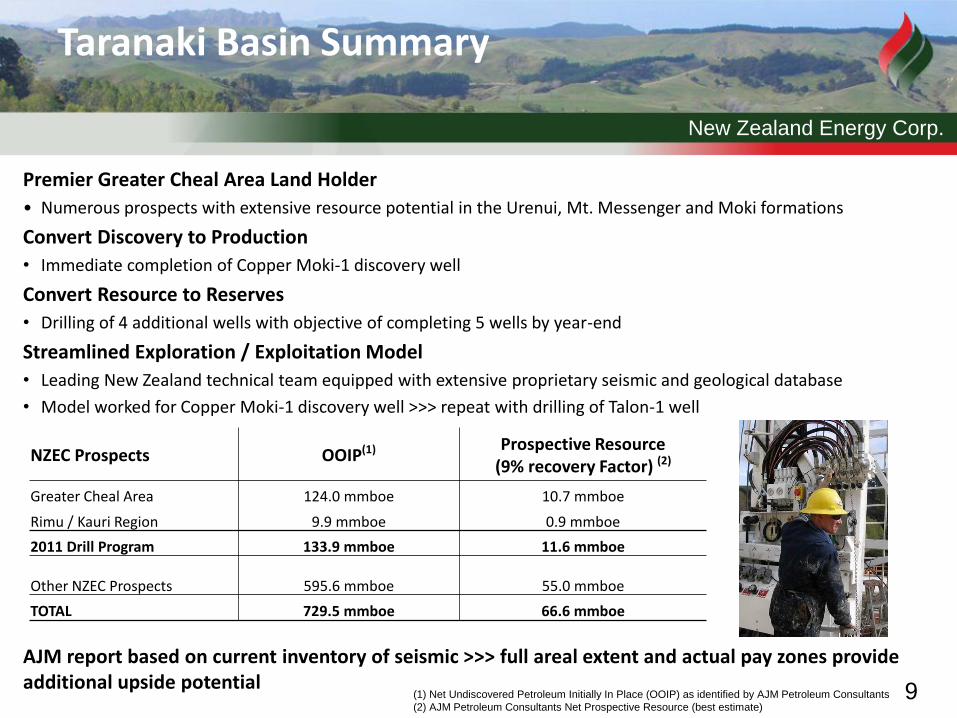

Taranaki Basin Summary

Premier Greater Cheal Area Land Holder

• Numerous prospects with extensive resource potential in the Urenui, Mt. Messenger and Moki formations

Convert Discovery to Production

• Immediate completion of Copper Moki-1 discovery well

Convert Resource to Reserves

• Drilling of 4 additional wells with objective of completing 5 wells by year-end

Streamlined Exploration / Exploitation Model

• Leading New Zealand technical team equipped with extensive proprietary seismic and geological database

• Model worked for Copper Moki-1 discovery well >>> repeat with drilling of Talon-1 well

AJM report based on current inventory of seismic >>> full areal extent and actual pay zones provide additional upside potential

(1) Net Undiscovered Petroleum Initially In Place (OOIP) as identified by AJM Petroleum Consultants

(2) AJM Petroleum Consultants Net Prospective Resource (best estimate)

NZEC Prospects OOIP(1) Prospective Resource

(9% recovery Factor) (2)

Greater Cheal Area 124.0 mmboe 10.7 mmboe

Rimu / Kauri Region 9.9 mmboe 0.9 mmboe

2011 Drill Program 133.9 mmboe 11.6 mmboe

Other NZEC Prospects 595.6 mmboe 55.0 mmboe

TOTAL 729.5 mmboe 66.6 mmboe

New Zealand Energy Corp.

10

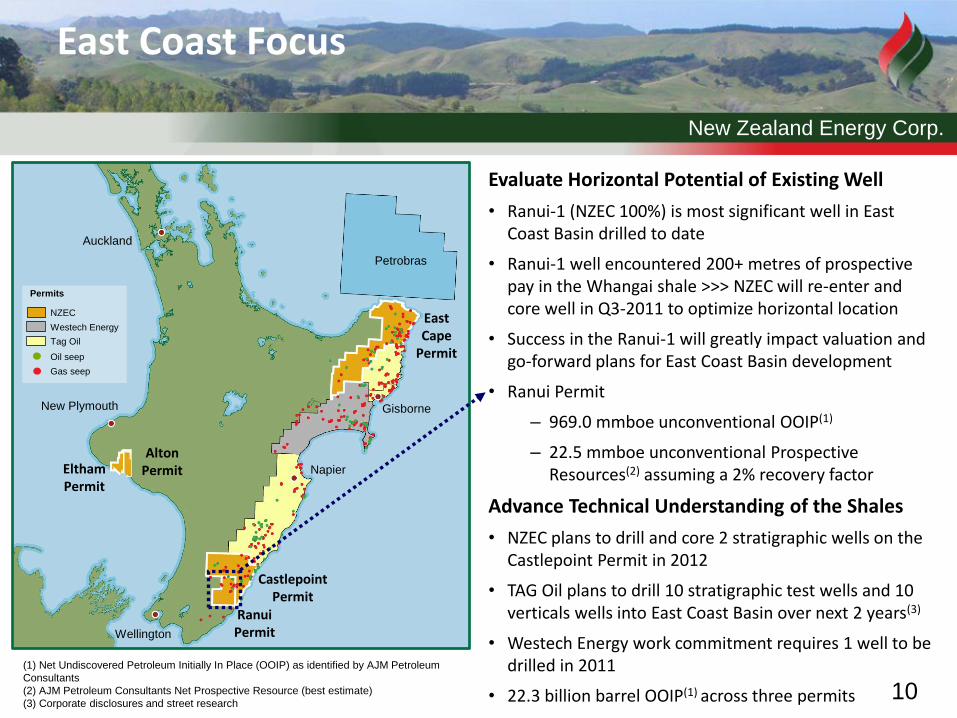

East Coast Focus

Petrobras

Permits

NZEC

Westech Energy

Tag Oil

Oil seep

Gas seep

Castlepoint Permit

Gisborne

Napier

Wellington

Auckland

New Plymouth

East Cape

Permit

Ranui Permit

Eltham Permit

Advance Technical Understanding of the Shales

• NZEC plans to drill and core 2 stratigraphic wells on the Castlepoint Permit in 2012

• TAG Oil plans to drill 10 stratigraphic test wells and 10 verticals wells into East Coast Basin over next 2 years(3)

• Westech Energy work commitment requires 1 well to be drilled in 2011

• 22.3 billion barrel OOIP(1) across three permits

Evaluate Horizontal Potential of Existing Well

• Ranui-1 (NZEC 100%) is most significant well in East Coast Basin drilled to date

• Ranui-1 well encountered 200+ metres of prospective pay in the Whangai shale >>> NZEC will re-enter and core well in Q3-2011 to optimize horizontal location

• Success in the Ranui-1 will greatly impact valuation and go-forward plans for East Coast Basin development

• Ranui Permit

– 969.0 mmboe unconventional OOIP(1)

– 22.5 mmboe unconventional Prospective Resources(2) assuming a 2% recovery factor

(1) Net Undiscovered Petroleum Initially In Place (OOIP) as identified by AJM Petroleum

Consultants

(2) AJM Petroleum Consultants Net Prospective Resource (best estimate)

(3) Corporate disclosures and street research

Alton Permit

New Zealand Energy Corp.

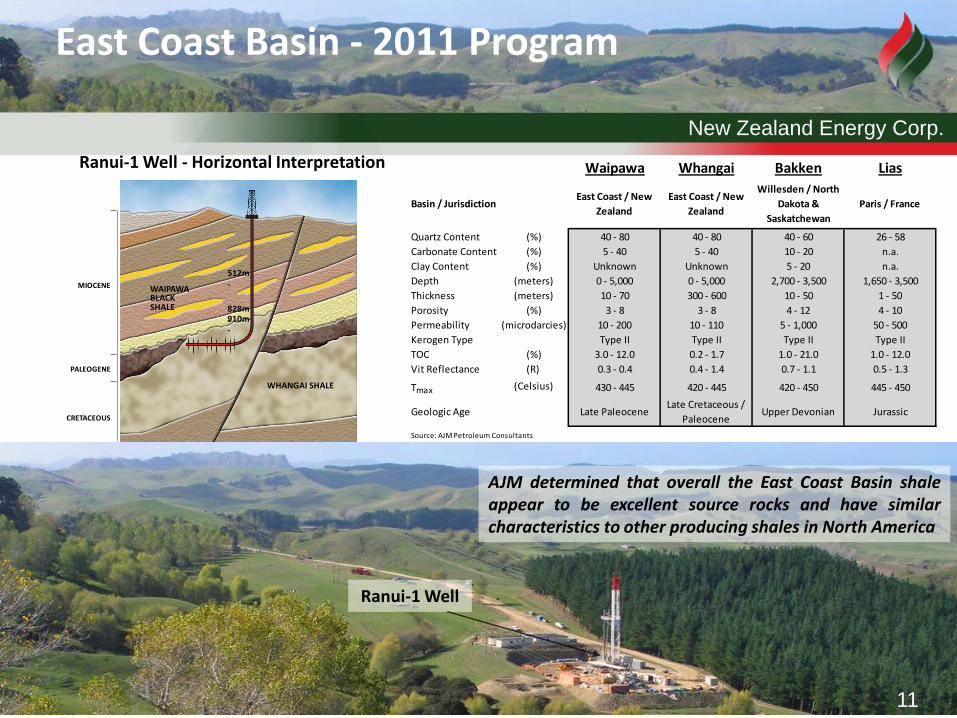

11

PALEOGENE

CRETACEOUS

WAIPAWA BLACK SHALE

512m-

828m-910m-

MIOCENE

WHANGAI SHALE

East Coast Basin - 2011 Program

Waipawa Whangai Bakken Lias

Basin / JurisdictionEast Coast / New

Zealand

East Coast / New

Zealand

Willesden / North

Dakota &

Saskatchewan

Paris / France

Quartz Content (%) 40 - 80 40 - 80 40 - 60 26 - 58

Carbonate Content (%) 5 - 40 5 - 40 10 - 20 n.a.

Clay Content (%) Unknown Unknown 5 - 20 n.a.

Depth (meters) 0 - 5,000 0 - 5,000 2,700 - 3,500 1,650 - 3,500

Thickness (meters) 10 - 70 300 - 600 10 - 50 1 - 50

Porosity (%) 3 - 8 3 - 8 4 - 12 4 - 10

Permeability (microdarcies) 10 - 200 10 - 110 5 - 1,000 50 - 500

Kerogen Type Type II Type II Type II Type II

TOC (%) 3.0 - 12.0 0.2 - 1.7 1.0 - 21.0 1.0 - 12.0

Vit Reflectance (R) 0.3 - 0.4 0.4 - 1.4 0.7 - 1.1 0.5 - 1.3

Tmax (Celsius) 430 - 445 420 - 445 420 - 450 445 - 450

Geologic Age Late PaleoceneLate Cretaceous /

PaleoceneUpper Devonian Jurassic

Source: AJM Petroleum Consultants

AJM determined that overall the East Coast Basin shale appear to be excellent source rocks and have similar characteristics to other producing shales in North America

Ranui-1 Well - Horizontal Interpretation

Ranui-1 Well

11

New Zealand Energy Corp.

12

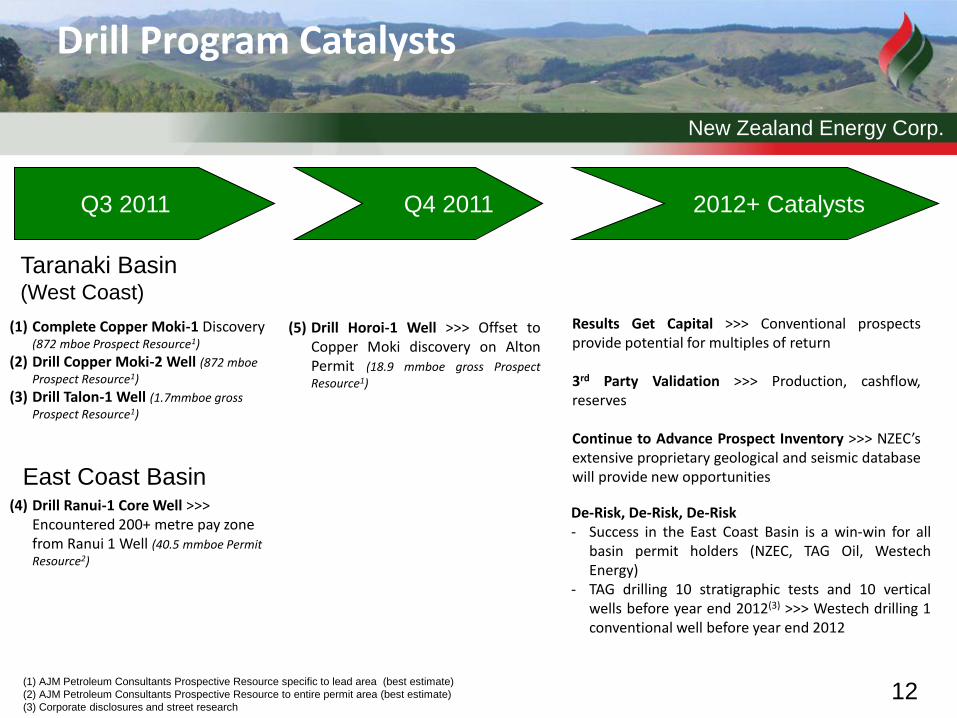

(1) Complete Copper Moki-1 Discovery (872 mboe Prospect Resource1)

(2) Drill Copper Moki-2 Well (872 mboe

Prospect Resource1)

(3) Drill Talon-1 Well (1.7mmboe gross Prospect Resource1)

Q3 2011

Taranaki Basin (West Coast)

East Coast Basin (4) Drill Ranui-1 Core Well >>>

Encountered 200+ metre pay zone from Ranui 1 Well (40.5 mmboe Permit

Resource2)

(5) Drill Horoi-1 Well >>> Offset to Copper Moki discovery on Alton Permit (18.9 mmboe gross Prospect Resource1)

Q4 2011

(1) AJM Petroleum Consultants Prospective Resource specific to lead area (best estimate)

(2) AJM Petroleum Consultants Prospective Resource to entire permit area (best estimate)

(3) Corporate disclosures and street research

2012+ Catalysts

Results Get Capital >>> Conventional prospects provide potential for multiples of return 3rd Party Validation >>> Production, cashflow, reserves Continue to Advance Prospect Inventory >>> NZEC’s extensive proprietary geological and seismic database will provide new opportunities

De-Risk, De-Risk, De-Risk - Success in the East Coast Basin is a win-win for all

basin permit holders (NZEC, TAG Oil, Westech Energy)

- TAG drilling 10 stratigraphic tests and 10 vertical wells before year end 2012(3) >>> Westech drilling 1 conventional well before year end 2012

Drill Program Catalysts

New Zealand Energy Corp.

13

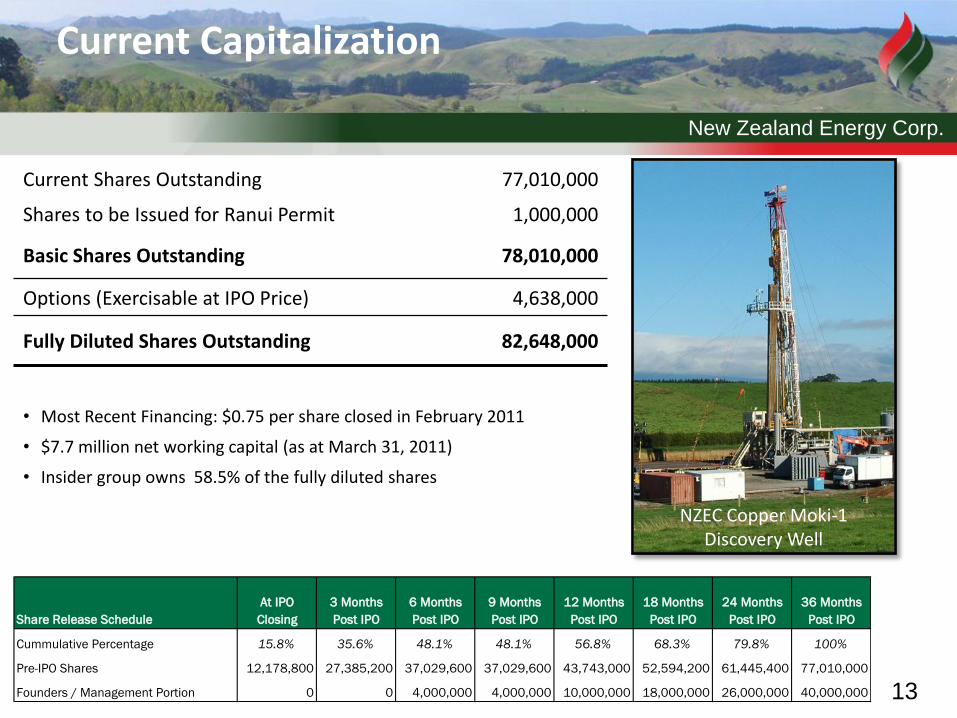

• Most Recent Financing: $0.75 per share closed in February 2011

• $7.7 million net working capital (as at March 31, 2011)

• Insider group owns 58.5% of the fully diluted shares

Current Capitalization

NZEC Copper Moki-1 Discovery Well

Current Shares Outstanding 77,010,000

Shares to be Issued for Ranui Permit 1,000,000

Basic Shares Outstanding 78,010,000

Options (Exercisable at IPO Price) 4,638,000

Fully Diluted Shares Outstanding 82,648,000

Share Release Schedule

At IPO

Closing

3 Months

Post IPO

6 Months

Post IPO

9 Months

Post IPO

12 Months

Post IPO

18 Months

Post IPO

24 Months

Post IPO

36 Months

Post IPO

Cummulative Percentage 15.8% 35.6% 48.1% 48.1% 56.8% 68.3% 79.8% 100%

Pre-IPO Shares 12,178,800 27,385,200 37,029,600 37,029,600 43,743,000 52,594,200 61,445,400 77,010,000

Founders / Management Portion 0 0 4,000,000 4,000,000 10,000,000 18,000,000 26,000,000 40,000,000

New Zealand Energy Corp.

14

Production and Cashflow 2011

1. Greater Cheal Area

• Complete Copper Moki-1 >>> 24.8 metres pay thickness

• Drill and test Horoi-1, Copper Moki-2, and Skinner-1 wells

2. Rimu / Kauri Region

• Repeat NZEC Exploration / Exploitation Model >>> Drill and test Talon-1 well

Reserves

• Focus on converting resource to reserves

• Enhance recovery factor

World Class Upside………..exposure to 22.3 billion barrel OOIP(1)

• Exploit Conventional Discovery and Area Surrounding >>> West Coast

• Unlock World Class Resource Play >>> Evaluate >200 metres of pay in East Coast Basin well controlled by NZEC

Conclusion

(1) Net Undiscovered Petroleum Initially In Place (OOIP) as identified by AJM Petroleum Consultants

New Zealand Energy Corp.

15

Appendix

New Zealand Energy Corp.

16

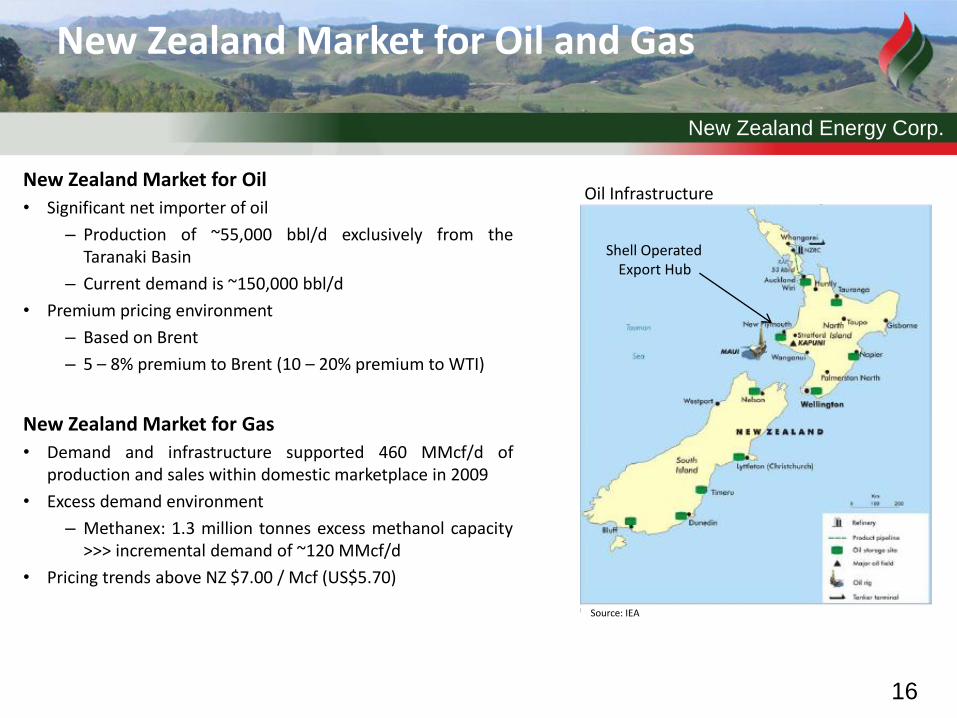

New Zealand Market for Oil

• Significant net importer of oil

– Production of ~55,000 bbl/d exclusively from the Taranaki Basin

– Current demand is ~150,000 bbl/d

• Premium pricing environment

– Based on Brent

– 5 – 8% premium to Brent (10 – 20% premium to WTI)

New Zealand Market for Gas

• Demand and infrastructure supported 460 MMcf/d of production and sales within domestic marketplace in 2009

• Excess demand environment

– Methanex: 1.3 million tonnes excess methanol capacity >>> incremental demand of ~120 MMcf/d

• Pricing trends above NZ $7.00 / Mcf (US$5.70)

New Zealand Market for Oil and Gas

Oil Infrastructure

Shell Operated Export Hub

Source: IEA

New Zealand Energy Corp.

17

New Zealand North Island Access to Market

Castlepoint Permit

Gisborne

Hastings

Wellington

Auckland

New Plymouth

East Cape Permit

Ranui Permit

Eltham Permit

Alton Permit

New Zealand Energy Corp.

18

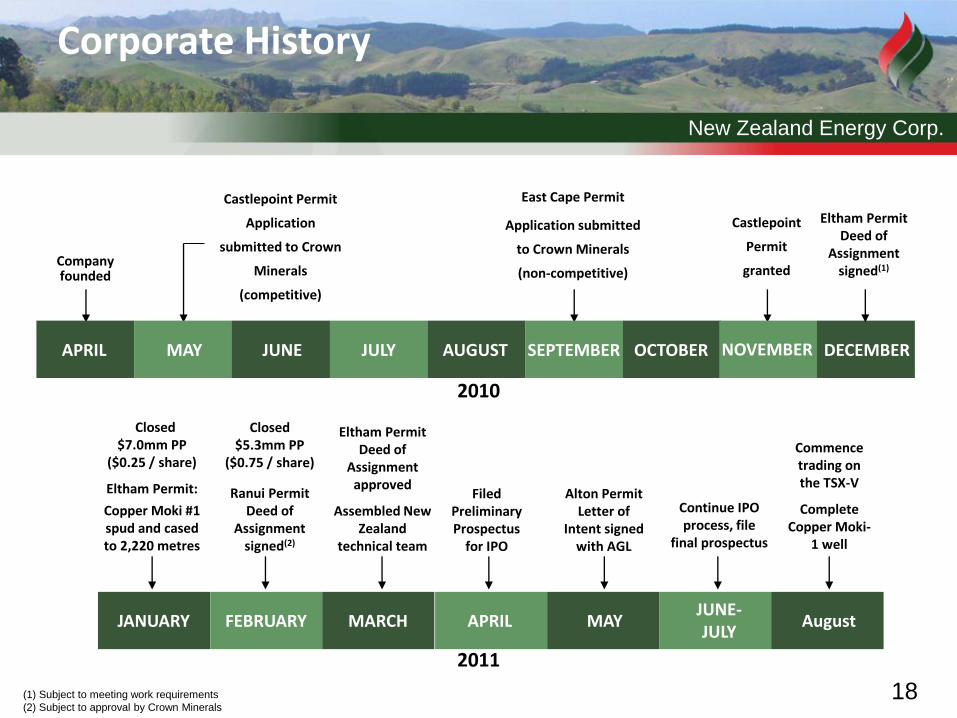

Corporate History

2010

Company founded

Castlepoint Permit

Application

submitted to Crown

Minerals

(competitive)

East Cape Permit

Application submitted

to Crown Minerals

(non-competitive)

Castlepoint

Permit

granted

APRIL MAY JUNE JULY AUGUST SEPTEMBER OCTOBER NOVEMBER DECEMBER

Eltham Permit Deed of

Assignment signed(1)

2011

Closed $7.0mm PP

($0.25 / share)

Eltham Permit:

Copper Moki #1 spud and cased to 2,220 metres

Closed $5.3mm PP

($0.75 / share)

Ranui Permit Deed of

Assignment signed(2)

Eltham Permit Deed of

Assignment approved

Assembled New Zealand

technical team

Filed Preliminary Prospectus

for IPO

(1) Subject to meeting work requirements

(2) Subject to approval by Crown Minerals

Alton Permit Letter of

Intent signed with AGL

Continue IPO process, file

final prospectus

JANUARY FEBRUARY MARCH APRIL MAY JUNE-JULY

August

Commence trading on the TSX-V

Complete Copper Moki-

1 well

New Zealand Energy Corp.

19

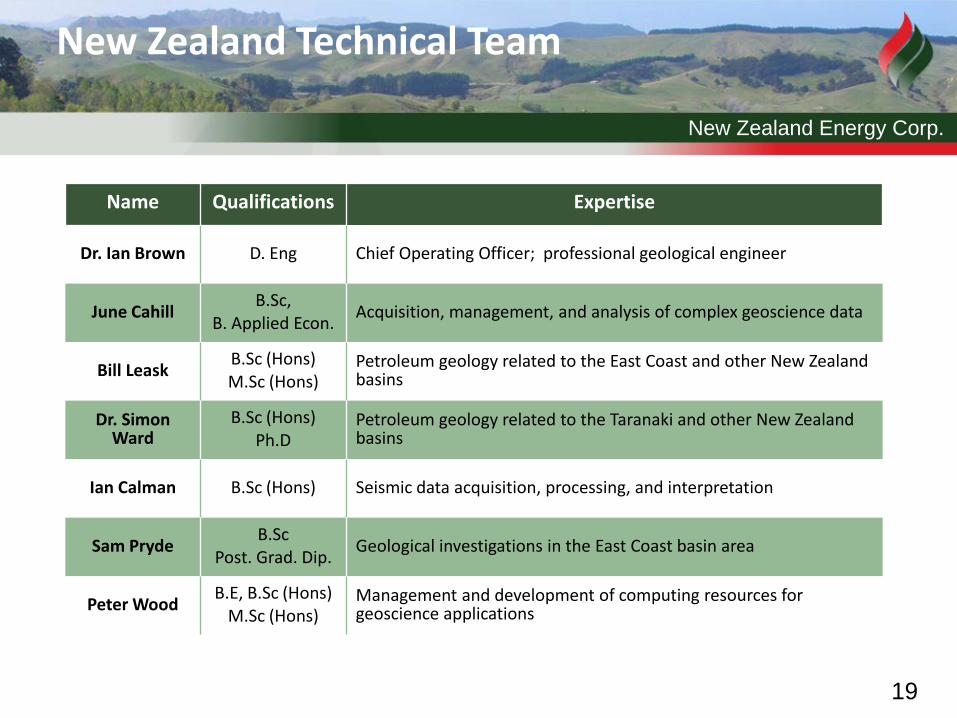

New Zealand Technical Team

Name Qualifications Expertise

Dr. Ian Brown D. Eng Chief Operating Officer; professional geological engineer

June Cahill B.Sc,

B. Applied Econ. Acquisition, management, and analysis of complex geoscience data

Bill Leask B.Sc (Hons) M.Sc (Hons)

Petroleum geology related to the East Coast and other New Zealand basins

Dr. Simon Ward

B.Sc (Hons) Ph.D

Petroleum geology related to the Taranaki and other New Zealand basins

Ian Calman B.Sc (Hons) Seismic data acquisition, processing, and interpretation

Sam Pryde B.Sc

Post. Grad. Dip. Geological investigations in the East Coast basin area

Peter Wood B.E, B.Sc (Hons)

M.Sc (Hons) Management and development of computing resources for geoscience applications

New Zealand Energy Corp.

20

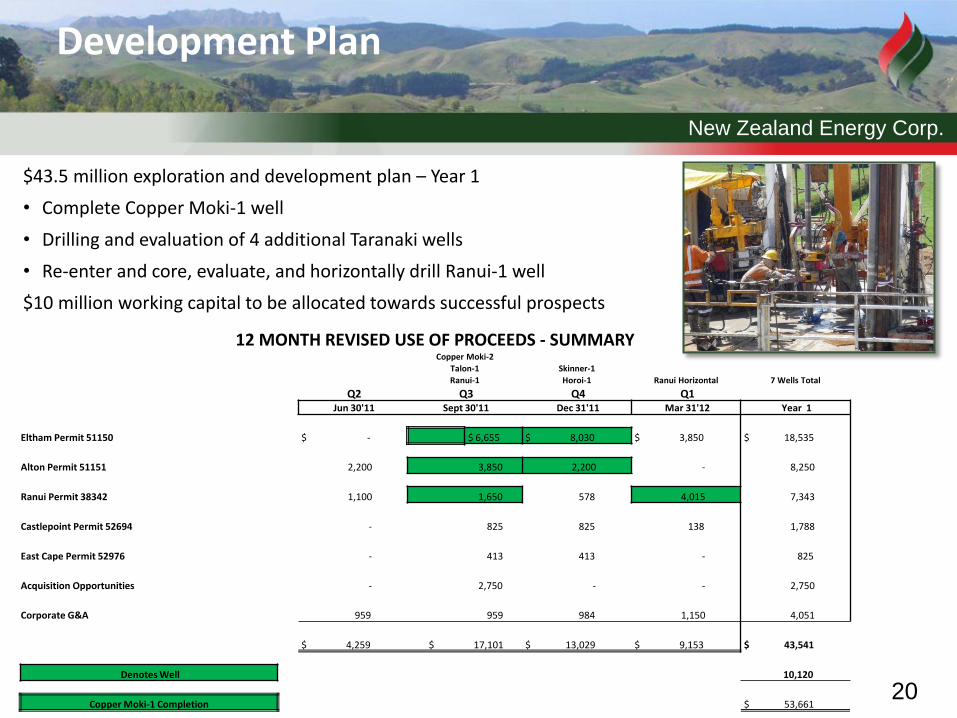

Development Plan

$43.5 million exploration and development plan – Year 1

• Complete Copper Moki-1 well

• Drilling and evaluation of 4 additional Taranaki wells

• Re-enter and core, evaluate, and horizontally drill Ranui-1 well

$10 million working capital to be allocated towards successful prospects

12 MONTH REVISED USE OF PROCEEDS - SUMMARY Copper Moki-2

Talon-1 Skinner-1

Ranui-1 Horoi-1 Ranui Horizontal 7 Wells Total

Q2 Q3 Q4 Q1 Jun 30'11 Sept 30'11 Dec 31'11 Mar 31'12 Year 1

Eltham Permit 51150 $ - $ 6,655 $ 8,030 $ 3,850 $ 18,535

Alton Permit 51151 2,200 3,850 2,200 - 8,250

Ranui Permit 38342 1,100 1,650 578 4,015 7,343

Castlepoint Permit 52694 - 825 825 138 1,788

East Cape Permit 52976 - 413 413 - 825

Acquisition Opportunities - 2,750 - - 2,750

Corporate G&A 959 959 984 1,150 4,051

$ 4,259 $ 17,101 $ 13,029 $ 9,153 $ 43,541

Denotes Well 10,120

Copper Moki-1 Completion $ 53,661

New Zealand Energy Corp.

21

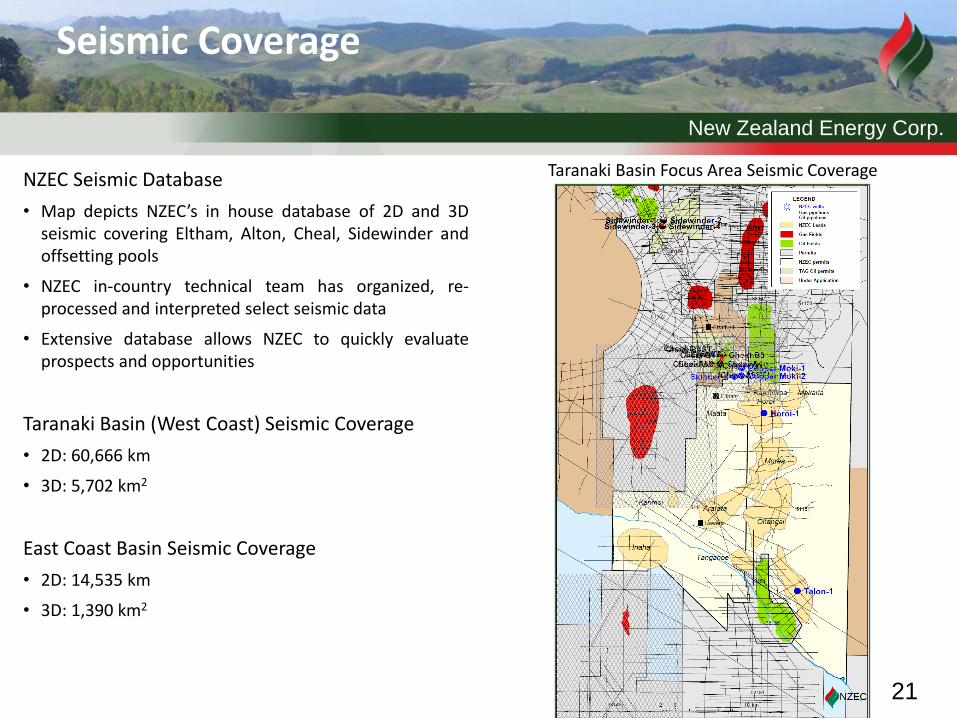

Seismic Coverage

Taranaki Basin Focus Area Seismic Coverage

NZEC Seismic Database

• Map depicts NZEC’s in house database of 2D and 3D seismic covering Eltham, Alton, Cheal, Sidewinder and offsetting pools

• NZEC in-country technical team has organized, re-processed and interpreted select seismic data

• Extensive database allows NZEC to quickly evaluate prospects and opportunities

Taranaki Basin (West Coast) Seismic Coverage

• 2D: 60,666 km

• 3D: 5,702 km2

East Coast Basin Seismic Coverage

• 2D: 14,535 km

• 3D: 1,390 km2

New Zealand Energy Corp.

22

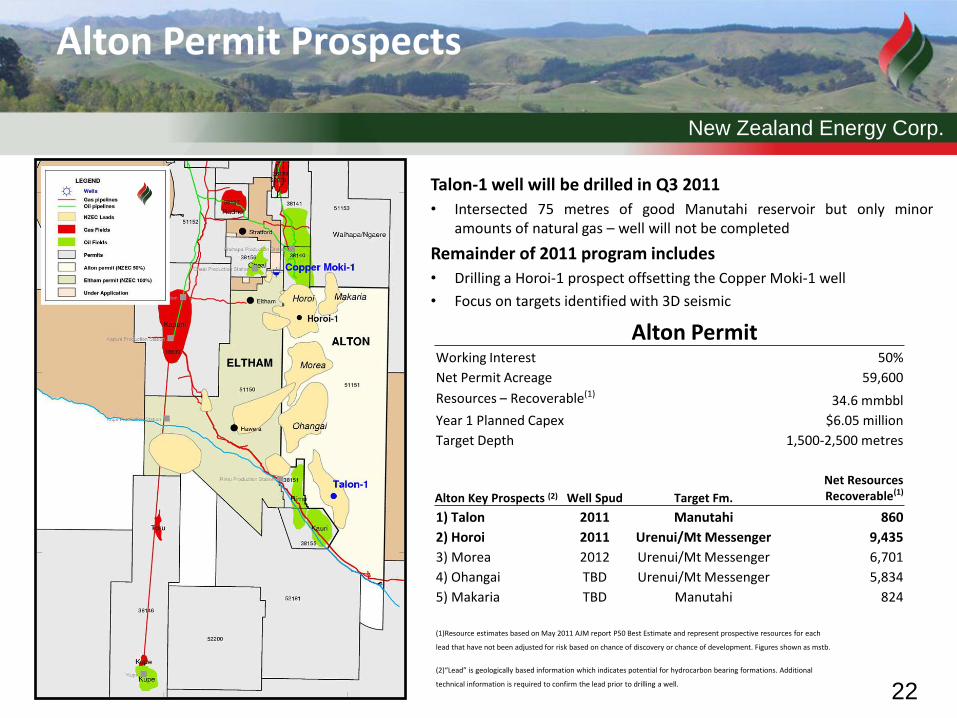

Alton Permit Prospects

Talon-1 well will be drilled in Q3 2011

• Intersected 75 metres of good Manutahi reservoir but only minor amounts of natural gas – well will not be completed

Remainder of 2011 program includes

• Drilling a Horoi-1 prospect offsetting the Copper Moki-1 well

• Focus on targets identified with 3D seismic

Alton Permit

Working Interest 50%

Net Permit Acreage 59,600

Resources – Recoverable(1) 34.6 mmbbl

Year 1 Planned Capex $6.05 million

Target Depth 1,500-2,500 metres

Alton Key Prospects (2) Well Spud Target Fm.

Net Resources Recoverable(1)

1) Talon 2011 Manutahi 860

2) Horoi 2011 Urenui/Mt Messenger 9,435

3) Morea 2012 Urenui/Mt Messenger 6,701

4) Ohangai TBD Urenui/Mt Messenger 5,834

5) Makaria TBD Manutahi 824

(1)Resource estimates based on May 2011 AJM report P50 Best Estimate and represent prospective resources for each

lead that have not been adjusted for risk based on chance of discovery or chance of development. Figures shown as mstb.

(2)“Lead” is geologically based information which indicates potential for hydrocarbon bearing formations. Additional

technical information is required to confirm the lead prior to drilling a well.

New Zealand Energy Corp.

23

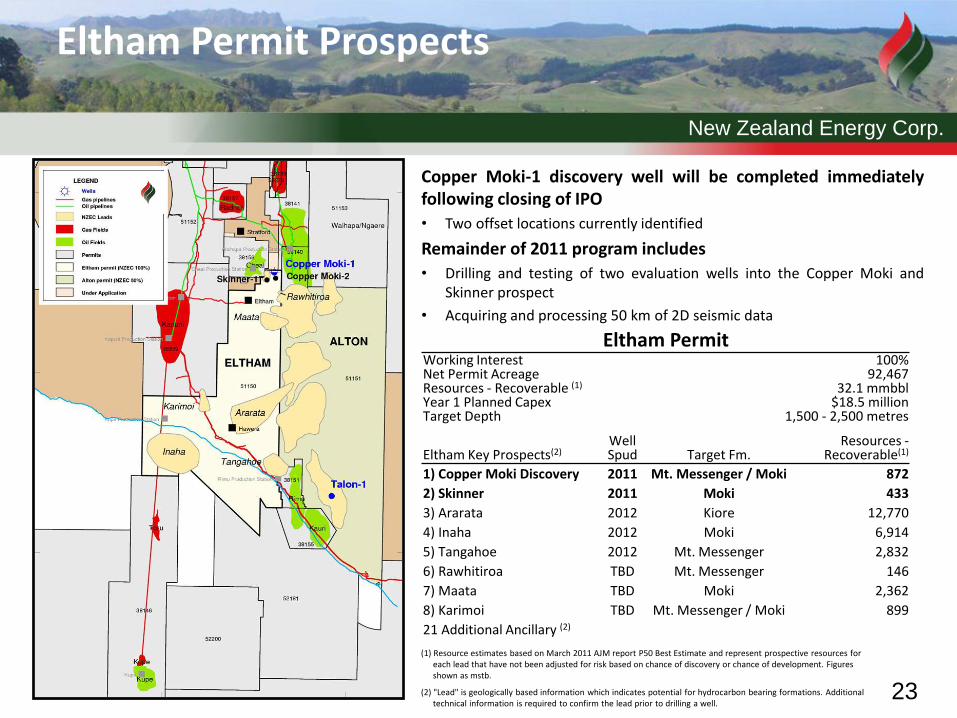

Eltham Permit Prospects

Copper Moki-1 discovery well will be completed immediately following closing of IPO

• Two offset locations currently identified

Remainder of 2011 program includes

• Drilling and testing of two evaluation wells into the Copper Moki and Skinner prospect

• Acquiring and processing 50 km of 2D seismic data

Eltham Permit Working Interest Net Permit Acreage Resources - Recoverable (1)

Year 1 Planned Capex Target Depth

100% 92,467

32.1 mmbbl $18.5 million

1,500 - 2,500 metres

Eltham Key Prospects(2) Well Spud Target Fm.

Resources - Recoverable(1)

1) Copper Moki Discovery 2011 Mt. Messenger / Moki 872

2) Skinner 2011 Moki 433

3) Ararata 2012 Kiore 12,770

4) Inaha 2012 Moki 6,914

5) Tangahoe 2012 Mt. Messenger 2,832

6) Rawhitiroa TBD Mt. Messenger 146

7) Maata TBD Moki 2,362

8) Karimoi TBD Mt. Messenger / Moki 899

21 Additional Ancillary (2)

(1) Resource estimates based on March 2011 AJM report P50 Best Estimate and represent prospective resources for each lead that have not been adjusted for risk based on chance of discovery or chance of development. Figures shown as mstb.

(2) "Lead" is geologically based information which indicates potential for hydrocarbon bearing formations. Additional technical information is required to confirm the lead prior to drilling a well.

New Zealand Energy Corp.

24

Forward-Looking Statements

This presentation and the Company’s preliminary prospectus dated April 29, 2010 (collectively the presentation and the preliminary prospectus referred to as the “Prospectus”) contain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). The use of any of the words “anticipate”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “propose”, “should”, “believe” and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. The Corporation believes the expectations reflected in those forward-looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct. Such forward-looking statements included in the Prospectus should not be unduly relied upon. These statements speak only as of the date of the Prospectus. In addition, the Prospectus may contain forward-looking statements attributed to third party industry sources.

In particular, the Prospectus contains forward-looking statements pertaining to the following:

• business strategy, strength and focus;

• proposed expenditures under “Use of Proceeds”;

• the granting of regulatory approvals;

• the timing for receipt of regulatory approvals;

• the resource potential of the Properties;

• the estimated quantity and quality of the Corporation’s oil and natural gas resources;

• projections of market prices and costs and the related sensitivity of distributions;

• supply and demand for oil and natural gas;

• expectations regarding the ability to raise capital and to continually add to resources through acquisitions and development;

• treatment under governmental regulatory regimes and tax laws, and capital expenditure programs;

• expectations with respect to the Corporation’s future working capital position;

• capital expenditure programs; and

• abandonment and reclamation costs.

Statements relating to “resources” are deemed to be forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the resources described can be profitably produced in the future.

With respect to forward-looking statements contained in the Prospectus, assumptions have been made regarding, among other things:

• future commodity prices;

• the Corporation’s ability to obtain qualified staff and equipment in a timely and cost-efficient manner;

• the impact of any changes in New Zealand law;

• the regulatory framework governing royalties, taxes and environmental matters in New Zealand and any other jurisdictions in which the Corporation may conduct its business in the future;

• the ability of the Corporation's subsidiaries to obtain subsequent mining permits, access rights in respect of land and resource and environmental consents;

• the recoverability of the Corporation’s crude oil, natural gas and natural gas liquids resources;

• the applicability of technologies for recovery and production of the Corporation’s oil, natural gas and natural gas liquids resources;

• the Corporation’s future production levels;

• the Corporation’s ability to market crude oil, natural gas and natural gas liquids production;

• future development plans for the Corporation’s assets unfolding as currently envisioned;

• future capital expenditures to be made by the Corporation;

• future cash flows from production meeting the expectations stated herein;

• future sources of funding for the Corporation’s capital program;

• the Corporation’s future debt levels;

• geological and engineering estimates in respect of the Corporation’s resources;

• the geography of the areas in which the Corporation is exploring;

• the intentions of the Corporation’s board with respect to the executive compensation plans and corporate governance programs described herein;

• the impact of increasing competition on the Corporation; and

• the Corporation’s ability to obtain financing on acceptable terms, or at all.

New Zealand Energy Corp.

25

Forward-Looking Statements

Actual results could differ materially from those anticipated in these forward-looking statements as a result of the risk factors set forth below and elsewhere in the Prospectus:

• the speculative nature of exploration, appraisal and development of oil and natural gas properties;

• uncertainties associated with estimating oil and natural gas resources;

• changes in the cost of operations, including cots of extracting and delivering oil and natural gas to market, that affect potential profitability of oil and natural gas exploration;

• operating hazards and risks inherent in oil and natural gas operations;

• volatility in market prices for oil and natural gas;

• market conditions that prevent the Corporation from raising the funds necessary for exploration and development on acceptable terms or at all;

• global financial market events that cause significant volatility in commodity prices;

• unexpected costs or liabilities for environmental matters;

• competition for, among other things, capital, acquisitions of resources, skilled personnel, and access to equipment and services required for exploration, development and production;

• changes in exchange rates, laws of New Zealand or laws of Canada affecting foreign trade, taxation and investment;

• failure to realize the anticipated benefits of acquisitions; and

• the other factors discussed under “Risk Factors”.

Readers are cautioned that the foregoing lists of factors are not exhaustive.

The material factors and assumptions used in developing the forward-looking statements are based on the assumptions contained in the Eltham Report, Castlepoint Report, Ranui Report and East Cape Report (as those terms are defined in the preliminary prospectus), including future commodity prices, costs and expected inflation, as well as the Corporation’s planned capital expenditure program, estimated drilling success rates and other prospects. Due to the nature of the oil and natural gas industry, budgets are regularly reviewed in light of the success of the expenditures and other opportunities, which may become available to the Corporation. Accordingly, while the Corporation anticipates that it will have the ability to spend the funds available to it as stated in the Prospectus, there may be circumstances where, for sound business reasons, a reallocation of funds may be prudent. The Corporation’s business objectives and other factors that management will consider in assessing the Corporation’s participation in acquisition or development opportunities are described under “General Development of the Business”.

The forward-looking statements contained in the Prospectus are expressly qualified by this cautionary statement. Except as required under applicable securities laws, the Corporation does not undertake or assume any obligation to publicly update or revise any forward-looking statements. Subscribers should read the entire Prospectus and consult their own professional advisors to assess the income tax, legal, risk factors and other aspects of their investment in the Shares.

None of the Corporation’s securities have been or will be registered under the United States Securities Act of 1933, as amended (the "U.S. Securities Act"), or any state securities laws, and the Corporation’s securities may not be offered or sold in the United States unless registered or exempt from such registration requirements. This presentation does not constitute an offer of securities in the United States or in any jurisdiction in which such an offer would be unlawful.

(cont.)