VOL. 26 | APR - JUN 2016 | USD 30 NGV TRANSPORTATION MAGAZINE NGV Transportation DIVERSIFYING PAKISTAN’S ENERGY NEEDS - A CASE OF NATURAL GAS & LNG FMECA AND HAZOP: INTEGRATED METHODOLOGY TO SUPPORT SAFETY ANALYSIS IN LNG FMECA AND HAZOP: INTEGRATED METHODOLOGY TO SUPPORT SAFETY ANALYSIS IN LNG FLOATING REGASIFICATION - A REALITY CHECK FLOATING REGASIFICATION - A REALITY CHECK FEATURES: FEATURES: SPECIAL REPORT: SPECIAL REPORT: LNGgc EVENT REPORT EVENT & EXHIBITION:

Transcript

VOL. 26 | APR - JUN 2016 | USD 30

NGVTRANSPORTATION

MAGAZINE

NGV Transportation

DIVERSIFYING PAKISTAN’SENERGY NEEDS - A CASE OF NATURAL GAS & LNG

FMECA AND HAZOP:INTEGRATED METHODOLOGY TO

SUPPORT SAFETY ANALYSIS IN LNG

FMECA AND HAZOP:INTEGRATED METHODOLOGY TO

SUPPORT SAFETY ANALYSIS IN LNG

FLOATING REGASIFICATION- A REALITY CHECK

FLOATING REGASIFICATION- A REALITY CHECK

FEATURES:FEATURES:

SPECIAL REPORT:SPECIAL REPORT:

LNGgc EVENT REPORTEVENT & EXHIBITION:

1 Vol.26 Apr - Jun 2016 NGV Transportation

EDITOR’S TWO CENTS

The year seems to be zipping right by us, we are well into 2016 already and the energy markets seem to be adapting to the cheap oil environment. The conglomerates are still making investments in natural gas projects as the line between LNG buyers and sellers slowly fades. They are increasingly making spot trading of LNG a part of their business for some extra revenue.

LNG is going through a real period of change and it is necessary that the industry bends and forms to accommodate the latest trends in the market so that it can move towards the next stage in its evolutionary journey. I personally believe that natural gas is just too dynamic a fuel to ever face obstacles that cannot be overcome. Like I’ve mentioned on numerous occasions, markets a cyclical and the energy industry is very volatile – the upswings and downswings can be immense but they rarely last for very long. This is not to say that there will not be huge obstacles to overcome – there very well will be and the current slump in oil prices has certainly put doubts in those who have recently entered or are not familiar with the industry.

In this issue we’ve prepared for you some interesting technical articles for you once more – researchers in Italy proide an analysis on FMECA and HAZOP integrated methodology for LNG support with regards to LNG transport and terminal operations. There is also a very nice study detailing the safety risks associated with a dual fuel LNG/diesel heavy duty trucks.

We also delve into the complicated natural gas industry in Pakistan and look into the situation from the perspective of the Assistant Executive Director of LNG; Rahil Pitafi of OGRA in Pakistan. Furthermore, the pit bull of LNG; Rudolf Huber continues to give his insights on all things LNG and speaks extensively on the unsettling reality of FSRUs in the current market.

As always we hope this issue intrigues you and we welcome any feedback that you might have. Keep fighting the good fight and plan for the future! There’s an old saying that goes, ‘Failing to plan is planning to fail’ and it resonates close to those involved in the LNG business – it’s time to be prepared or be left behind.

Ryan PasupathyEditor

Greetings all!NATURAL GAS GLOBAL

Published by:

Our Address:

Natural Gas Global52 Foch Road, #02-02Singapore 209274

PT Olifen Global Indonesia20th Floor, Wisma KEIAIJl. Jend. Surdirman Kav 3-4Central Jakarta - Indonesia

All rights reserved. No portion of this publication covered by the copyright herein may be reproduced in any form or means – graphic, electronic, mechanical, photocopying, recording, taping, etc – without the written consent of the publisher. Opinions expressed by contributors and advertisers are not necessarily those of the publisher and editor.

Follow us on our social media platforms to receive the latest natural gas news from around the world!

www.facebook.com/NGVTMag

www.linkedin.com/company/NGV-Transportation

@NGVTmag

NGVTRANSPORTATION

MAGAZINE

CONTENT

03

SPECIAL REPORT: SAFETY AND RISKS OF A DUAL FUEL SYSTEM WITH LNG AND DIESEL

29ANALYSIS OF NATIONAL POLICIES AND ITS IMPACT ON NGV

GROWTH IN MALAYSIA

24

NEWS AROUND THE WORLD

FMECA AND HAZOP: INTEGRATED METHODOLOGY TO SUPPORT SAFETY

ANALYSIS IN LNG TRANSPORT AND TERMINAL OPERATIONS

EDITOR’S TWO CENTS

DIVERSIFYING PAKISTAN’S ENERGY NEEDS - A CASE OF

NATURAL GAS & LNG

LNGgc EVENT REPORT

11

3901

19

34

FEATURES:

SPECIAL REPORT:

EVENT& EXHIBITION:

FLOATING REGASIFICATION - A REALITY CHECK

3 Vol.26 Apr - Jun 2016 NGV Transportation

NEWS AROUND THE WORLD

ABU DHABIJanuary 2016: Abu Dhabi Taxi Drivers Forced to Queue 40 Minutes for CNG

CNG terminals at petrol stations across the country are causing taxi drivers much grief when trying to fill up their cabs. The cities taxi force have said that they can only make a full tank of gas last 90 km and as such have to refill their cars 3-4 times a day. As there few petrol stations with CNG pumps, they end up having to wait up to 40 minutes just to get one refill.

The feeling is that they lose a lot of their actual earning time filling up their tanks with fuel. The cab drivers feel that all petrol stations should have CNG pumps as if this was so, it would allow them to operate without this huge problem of extended downtime. At the moment there are only 17 CNG filling stations in the country. There are plans however to equip 8 more by the end of the year.

- The National

SapuraKencana GE Oil & Gas Services (SKGE) has secured a long term service contract to provide maintenance services for Petronas’ two forthcoming floating LNG vessels. SapuraKencana is to provide Petronas with complete maintenance services for their fleet of 12 gas turbines and their fleet of GE compressors, generators and electric motors to be installed on their floating LNG vessels. SKGE is a joint venture between SapuraKencana Services Sdn Bhd and GE Power Systems (M) Sdn Bhd. The contract was awarded by Petronas Floating LNG1 (L) Ltd (PFLNG).

- The Star

INDIA MALAYSIAFebruary 2016: Australia Keen to Invest in India’s LNG, Health, Financial Sectors

March 2016: SapuraKencana GE JV Gets Petronas LNG Vessels Job

India is looking like a favourable investment destination for Australia who is interested in investing in LNG financial services, education and healthcare sectors of the country. It is felt that India presents a lot of good prospects for Australian businesses.

Australia’s Minister for Trade & Investment Andrew Robb told reporters, “We expect the opportunity for those things that we are good at. We expect the opportunity to be able to come in and compete and to offer. In a lot of cases that would involve doing Joint Ventures (JVs) as there are a lot of local issues that need to be understood and the best way to do that is to

find a good and trustworthy JV partner.”

He added that, Prime Minister Narendra Modi has transformed India’s image and made it a “favourable” investment destination. He also said that, “We want the opportunity to invest in a way which is not fraught with long delays, approvals and endless red tape.(We want to) invest in an efficient way and also be able to offer, after investing, a fair opportunity to compete with other service offerings.”

- The Economic Times

4NGV Transportation Vol. 26 Apr - Jun 2016

NEWS AROUND THE WORLD

Oil & Gas Africa 2016 – Trade Exhibition will bring together leading Oil and Gas industry players from across the globe to confront and overcome current industry issues. This premier event will explore critical topics and trends, including, but not limited to, exploration technologies, reservoir characterization,

The Arctic LNG project includes the construction of a new LNG plant in the port of Sabetta, where a plant for Yamal LNG project is already under construction. Japanese companies show interest in the new LNG projects of Novatek.

The Arctic LNG project includes the construction of a new LNG plant in the port of Sabetta, where a plant for Yamal LNG project is already under construction. Gas will be supplied from Salmanovskoye (Utrenneye) and Geofizicheskoye oil and gas fields that are located on the Gydan Peninsula. The construction of the plant is scheduled for 2018.

- TASS

Africa has experienced massive internal growth in major areas within the last 20 years which have contributed greatly to investors’ assets and one area in particular is in particularly high demand and continuously predicting huge returns – the energy market.

It has already had an impact in creating greater well-being to the people of Africa whilst boosting profits for shareholders involved. Due to this massive interest in the African power sector which includes the UN’s 2014 ‘Sustainable Energy for All’ programme and highlights Africa as one of the main areas of focus, Expogroup is organizing The 5th Power & Energy Exhibition & Conference 2016 from the 12th to the 14th of May, 2016 at Kenya’s prime international venue; the Kenyatta International Conference Centre in Nairobi and the 2nd edition from the 03rd to the 05th of June 2016 at Tanzania’s international venue; the Mlimani Conference Centre in Dar-es-Salaam.

The premier conference and exhibition dedicated to the power generation, renewable and alternative energy & distribution industries attracted delegates and attendees from over 22 countries across Africa and around the world.

- Expogroup E-newsletters

KENYA

RUSSIA

February 2016: Oil & Gas Africa 2016 Announced

February 2016: Japanese Companies Show Interest in New LNG Projects by Novatek

February 2016: Africa’s Power & Energy Exhibition & Conference Announced

production optimization, deep-water drilling, heavy oil, enhanced oil recovery, cost containment, acquiring skilled workers and health, safety and environmental risks.

Exhibiting at the largest oil and gas event in the industry will allow you to showcase your products and services to the industry’s largest gathering of

qualified decision-makers., the Oil & Gas Africa 2016 will kick-start the entry of international support services into the local oil and gas industry. The exhibition will play host to a multitude of international companies looking to introduce and expand their operations, products and services in Africa. Attendees will meet one-on-one with solution providers throughout the event to learn about critical products and services capable of solving organizational challenges.

- Expogroup E-newsletters

E X P L O R E T H E V A S T E M E R G I N G M A R K E T O F

Exhibitors from 24 Countries | Visitors from all over Africa

6NGV Transportation Vol. 26 Apr - Jun 2016

NEWS AROUND THE WORLD

CNPC Chairman Wang Yilin has said that his company is looking for opportunities to rework the pricing method on its LNG supply contract with Qatar. Wang’s comments follow Petronet’s successful renegotiation of its long-term (25-

Papua New Guinea is rapidly becoming one of the more prosperous countries when it comes to LNG production. Their biggest obstacle at the moment however, is dealing with the challenging terrain where deposits are located. The challenging terrain requires an experienced operator to properly capitalize on the potential of LNG that the country has to offer.

ExxonMobil PNG Limited has won the 2015 Asia-Pacific Midstream/LNG Company of the Year Award, highlighting the potential of a country that isn’t usually on the tips of tongues

CHINA

PAPUA NEW GUINEA

March 2016: LNG Shake-Up Ahead As China Pushes To Renegotiate Pricing On Qatar Gas

February 2016: LNG Puts PNG on the Map

waxing lyrical about industrial opportunity.

The likes of InterOil Corporation and High Arctic Energy Services have staked their claim as international success stories in Papua New Guinea over the past decade, having realised the future potential that the country will hold. Subsequently, oil majors such as Total SA and the award-winning ExxonMobil have joined the party, capitalising on the formers’ growing experience to carry out some of the most substantial LNG projects in the world.

Significant and lauded in its

own right of course, the PNG LNG project didn’t take long to prove itself as a trailblazer in the region, immediately paving the way for a second significant project to get underway as the strive for liquefied natural gas resources intensified.

A partnership between Total and InterOil Corporation - as well as international player, Oil Search - saw attentions turn to the Elk-Antelope gas field in the country’s Gulf province; essentially confirming the country’s position as a low-risk investment hub for the industry.

-Asia Outlook Magazine

year) LNG contract with Qatar’s RasGas in December.

Wang’s comments seem to offer growing evidence that LNG markets are in a state of change for which there will be no turning back. These changes come amid two important developments. First, the plunge in global oil prices of around 70% since June 2014. Since most LNG in the Asia-Pacific region is linked to the price of oil, the bloodbath in global oil markets have hit LNG hard. Spot LNG prices in Asia have plunged from just over $20 per million British thermal units (MMBtu) in February 2014, to around $4.50/MMBtu for cargoes to be delivered in April.

The other major driver is the ever-increasing LNG supply glut. Global LNG output last year reached 250 mtpa and is projected to reach 330 mtpa by 2018, mostly from new projects coming on-stream in Australia and the U.S.

- Forbes

7 Vol.26 Apr - Jun 2016 NGV Transportation

Hoegh LNG is putting its FLNG development activities on hold while it plans to allocate its funds elsewhere into its core business – FSRUs. The company sees this as being their highest return on capital investment and also having the most promising market prospects.

The company has made this decision based on the current market scenario of an oversupplied LNG market and falling energy and financial markets. The market conditions for FSRUs however, continue to be favourable as the demand is driven by strong

The German Federal Ministry of Transport has just awarded a grant of more than 1 million Euros for deployment of containerized LNG fuelled generators for cold-ironing. These systems are the first of their kind and will be lifted aboard container ships upon their arrival at the port and then removed when the ship leaves again. Each of these generators can provide 1.5 megawatts of power, for up to 30 hours of operation per separate, containerized tank of fuel.

Henning Kuhlmann, managing director at Becker Marine Systems, the generators’ developer, said that, “During layovers at port the power for container ships is currently being supplied by on-board auxiliary diesel engines. By doing so, ships account for the majority of harmful emissions at ports.”

The generator and tank, each equivalent to standard container sizes, will be the first container crane lift onto the vessel upon its arrival and then the last off before its departure, eliminating a cabled shore power connection while greatly reducing emissions. As an added bonus, no changes to harbour infrastructure are required. If more than 1.5 megawatts of power is needed, additional generators can be lifted aboard. Each system is designed to be stackable so that it occupies the footprint of one 40-foot container.

- Maritime Executive

NORWAY

GERMANY

February 2016: Hoegh LNG Pulls Out of FLNG

February 2016: LNG Cold-Ironing Gets Government Support

PAKISTANFebruary 2016: Centre Decides on Higher Rates of LNG, Ignores OGRA

The Federal Government in Pakistan has strangely decided to ignore the LNG price set by it’s Oil and Gas Regulatory Authority and decided on higher rates depending on the type of consumer.

The development has caused some unrest among followers who blame the centre for bypassing the regulator and taking the decision into their own hands. After conducting public hearings and taking input from stakeholders, Ogra had determined a provisional price of $8.60 per million British thermal units (mmbtu). However, the government has allowed Sui Northern Gas Pipelines Limited (SNGPL) to charge up to $12 per mmbtu.

Among other sectors, the federal government decided on higher prices for CNG stations, meaning that it would be difficult for them to maintain the 30% price parity with petrol directed by the Economic Coordination Committee (ECC).

Officials familiar with the development said that the gas utility was charging a higher price at a time when LNG prices had witnessed a decline in global market. In addition, the gas utility was charging three prices for each category of consumers.

- The Tribune

growth in new LNG supplies at competitive prices.

The company sees a large amount of new FSRU projects coming underway, being promoted by LNG producers and importers as well as downstream gas consumers. According to Hoegh LNG’s latest statement they will not engage in any further new FLNG developments but will continue to complete its obligations for existing projects. All of its FLNG staff will be transferred to its FSRU side of the business.

- Marine Link.com

8NGV Transportation Vol. 26 Apr - Jun 2016

NEWS AROUND THE WORLD

March 2016: Chance to Supply LNG to Japan Fading Fast: Ambassador

After years of preparation, Cheniere Energy has completed loading its first tanker with liquefied natural gas for export. The occasion was extremely significant as the company has Over the last several years, the company has spent billions building terminals such as the Louisiana facility so it can export LNG.

Cheniere’s interim CEO, Neal Shear, has said that, “Cheniere is in fabulous shape, we’ve secured contracts for 87% of its LNG from export terminals.” He added that, “We (Cheniere) are not like other companies in the energy patch, and people should really think of us in that sense. When you build projects like this, you’re not worried about the next 36 months — you’re really worried about 20 years.”

- CNBC

Russian energy giant Gazprom has received word from the government of Jordan that it was interested in buying LNG from them. The Jordanian side asked the Russian side to consider the possibility of LNG supplies to Jordan at preferential prices. Jordan has struggled in the past to find a reliable source of natural gas in part because of downstream problems in Egypt.

Jordanian companies Arab Potash and Jordan Bromine have secured a total of 66 billion cubic feet of natural gas from the Tamar field, located off the Israeli coast, in 2014. The partners managing Tamar estimate the field holds up to 10 trillion cubic feet of natural gas.

- UPI

JORDANMarch 2016: Russia Sees Jordanian Interest in LNG

UNITED STATESFebruary 2016: In a First, Cheniere to Export US LNG

Qatargas, Maersk Group and Shell announced that they have signed an MOU to work toward the development of LNG as a marine fuel. The signing of the MOU signifies that the partners will “explore the development of new markets for LNG to be used as propulsion fuel for merchant vessels” as a way of replacing heavier fuel oils, and helping to lower emissions “before the end of the current decade.”

The MOU sees LNG supplies coming from the Qatargas 4 gas project, which is a joint venture between Qatar Petroleum and Shell Gas and could potentially be used by Maersk Line for its merchant vessels.

Saad Sherida Al-Kaabi, Chairman of Qatargas, said that, “We are very proud to continue to pioneer new and novel opportunities to utilize Qatar’s LNG. We are also proud to partner with industry leaders such as Maersk and Shell to create potential new market opportunities for Qatar’s LNG and, at the same time, provide ship operators around the globe with a cleaner fuel alternative to the heavy fuel oils currently in use.”

- Ship & Bunker

QATARFebruary 2016: Qatargas, Maersk Group and Shell Sign Agreement on LNG Bunkers

JAPAN

Delays in approving the $36 billion Pacific NorthWest LNG project are putting Canada at risk of missing out on the biggest market in the world, warns Japan’s ambassador to Canada. Petronas’ multibillion-dollar LNG project in Prince Rupert – already past the 750-day mark of what was supposed to be a one-year review – experienced yet another setback in mid-March, when the federal environment minister pushed back a final decision by another three months.

In a letter to the Canadian Environmental Assessment Agency (CEAA), Kenjiro Monji, Japan’s ambassador to Canada, warned that the LNG market opportunity in his country is closing fast.

Kenjiro Monji wrote that, “If the approval of the environmental assessment is delayed further, Canada may run the risk of missing the chance to export LNG to the growing Asian market for a long time,”

- TASS

9 Vol.26 Apr - Jun 2016 NGV Transportation

NEWS AROUND THE WORLD

Kuwait has inked a $2.93 billion contract with three South Korean firms for the construction of the largest Liquefied Natural Gas import facility in the oil-rich country. The project, to be built at the Al-Zour refinery near the border with Saudi Arabia, was awarded to Hyundai Engineering Co, Hyundai Engineering & Construction Co and Korea Gas Corporation.

CEO of national refiner Kuwait National Petroleum Co Mohammad Al-Mutairi, who signed the contract, said the project is slated to be completed in the first quarter of 2021. OPEC member Kuwait is rich with crude oil but its natural gas production is too small to meet its needs. Every year it imports large LNG quantities to supply power plants, especially during the summer, and for use in the petrochemicals industry.

- Kuwait Times

Singapore is looking at allowing its gas customers to import up to 10% of their annual LNG intake from the international spot market for domestic use. Singapore’s Energy Market Authority plans to allow the import of spot LNG for domestic use after the conclusion of UK-based BG’s exclusive franchise to provide buyers with more supply options.

Singaporean Minister for Trade and Industry, S. Iswaran said that, “Under the spot LNG Import Policy, a gas buyer would be given annual credits to import up to 10% of its total long-term contracted quantities in the form of spot cargoes.” He added that, “This will also encourage price discovery, which would complement Singapore’s efforts to develop into a hub for gas trading activities.”

-Platts

Indonesian President Joko Widodo decided that the Masela LNG plant will be constructed onshore. Masela, located in the Arafura Sea (Moluccas), is Indonesia’s largest deep-water gas project. Previously, Japan-based oil company Inpex Corp and Netherlands-based Royal Dutch Shell proposed to construct the LNG plant offshore, which would have made it the world’s largest floating LNG plant.

KUWAIT SINGAPORE

INDONESIA

March 2016: Kuwait and Korean Firms Seal $2.9 billion LNG deal

March 2016: LNG Buyers to be Allowed to Import Up to 10% From Spot Market

March 2016: Masela Gas Project Indonesia: Widodo Opts for Onshore LNG Plant

President Widodo rejected the proposal after months of mulling over the project. Contractors Inpex and Shell are not expected to withdraw from the project but will need time to adjust plans. Widodo said it was a difficult decision but in the end calculations and considerations suggested an onshore plant would have more economic benefits for the country. The main considerations were related to the optimization of multiplier effects for the benefit of local communities and the national economy as a whole.

Several analysts claim, however, that this decision is based on nationalistic sentiments as onshore development will actually raise investment costs by approximately USD $7.5 billion (due to an additional 600 kilometers of pipelines that are required). As such, one analyst stated that nationalist (and political) interests are priority for Indonesian decision-makers rather than rational economic considerations. Meanwhile, an analyst of the Eurasia Group said this case shows that Widodo is constrained by politics and vested interests of people that were behind his ascent to the presidential drivers’ seat.

- Indonesia-Investments

E X P L O R E T H E V A S T E M E R G I N G M A R K E T O F

07 - 09 July 2016, Mlimani Conference Centre,Dar-es-Salaam, Tanzania

Exhibitors from 22 Countries | Visitors from all over Africa

11 Vol.26 Apr - Jun 2016 NGV Transportation

FEATURE ARTICLE

LNG TRANSPORT AND TERMINAL OPERATIONS

INTEGRATED METHODOLOGY TO SUPPORT SAFETY ANALYSIS IN

FMECA and HAZOP

M. Giardina, M. MoraleDepartment of Energy, Information Engineering and Mathematical Models (DEIM), University of Palermo, Viale delle Scienze, 90128 Palermo, Italy

12NGV Transportation Vol. 26 Apr - Jun 2016

FEATURE ARTICLE

IntroductionThe development of the liquefied natural gas (LNG) industry has been viewed by many countries as a major improvement in the utilization of the energy resources, so it is expected that increasing need for natural gas demand, especially in the electricity sector.

However, the societal acceptability of LNG technologies largely depends on safety standards which should result in low risk for both the population and the environment. That is why it is important to perform appropriate and in-depth safety analyses to be able to take into account the risks connected to new technologies and/or human factors considering that operator errors are the most commonly identified causes of accidents (Castiglia and Giardina 2013), especially when complex procedures are used (human error is the primary causal factor in industrial and transport accidents, typically range is between 50% and 90%).

The risks should include all operational activities arising from terminal operations involving transfer and storage of LNG. This issue should cover also the management of LNG shipping operations, a matter of some importance that needs further and deeper discussions respect to safety.

Detailed descriptions of the possible accident scenarios and component failures can be attained by applying well-known methods - Hazard and Operability Analysis (HAZOP) or Failure Modes, Effects and Criticality Analysis (FMECA).

Taking into account these concerns, the proposed FMECA and HAZOP integrated analysis (FHIA) has been designed by researchers at Department of Energy, Information Engineering and Mathematical Models (DEIM), University of

Palermo, Italy, as tool to develop specific criteria for reliability and risk data organisation and to gain additional recommendations, beyond those typically provided by applications of a single method.

A typical HAZOP provides an identification of accidental events (top events, TEs) and operability problems by using logical sequences of cause-deviation-consequence of process parameters. However, it doesn’t lend itself to quantitative analysis, to rank the effects of failures and to study the relative effectiveness of the proposed

corrective actions. The FMECA method focuses on individual components and their failure modes. Thus, each failure mode is only considered once, and all of its effects and controls are listed together. The criticality analysis is based on the risk priority number (RPN), a useful method for ranking the importance of each potential failure according to the failure rate, the severity of the failure consequence and the detection, which defines if the failure can be detected by the design controls or inspection procedures (Casamirra et al. 2009). However, it can be

13 Vol.26 Apr - Jun 2016 NGV Transportation

FEATURE ARTICLE

Occurrence probability of component failure (operating day)

Occurrence probability of human error Rank

<1/20,000 Less than every 5 years 1

1/20,000÷1/10 ,000 Every 2÷5 years 2

1/10,000÷1/2000 Once a year 3

1/2000÷1/ 1000 Several times a year 4

1/ 1000÷1/200 Once a month 5

1/200÷1/100 Several times a month 6

1/100÷1/20 Once a week 7

1/20÷1/10 Several times a week 8

1/10÷1/2 Once a day 9

>1/2 Several times a day 10

Table 1 : FMECA scale for probability of component failure and human errors, O.

difficult for this technique to identify accident sequences and dependencies between equipment and human actions (Giardina et al. 2014).

FHIA approach allows for a systematic methodology that provides more logical reasons for component failures/human erros and undesirable consequences (i.e. TE). This is done under different operating conditions and during the various steps of the examined process, a very difficult task, especially in those technologies characterised by a large number of processes for the same subsystem.

Moreover this tool provides an exhaustive list of events or combinations of events that affect the same or different TEs. This allows to focus on the critical points of a hazard before making a quantitative assessment of the occurrence probability. For example, this data can be very useful if risk assessments are performed by using Layers Of Protection Analysis (LOPA) method (CCPS, 2001), a powerful analytical tool for assessing the adequacy of protection layers used to mitigate process risk.

Finally, because human errors are the most commonly identified causes of accidents, evaluation of the Risk Priority Number (RPN) index is proposed to rank both component failures and human errors.

A more extended discussion of the FHIA methodology as well as its application to a case study is reported in (Giardina and Morale 2015).

To support the safety analysis, a new software, called risk analysis database (RAD), has been developed at DEIM, Italy, with the objective to standardise the application of FHIA as described in detail below.

Finding other sources of funding to improve the RAD tool as well as to verify the effectiveness of the proposed methodology, considering other case studies in LNG industrial

systems, is among the initiatives supported by DEIM researchers.

Description of the FHIA approachTo enhance the distinctive

Severity of component failure or human error Rank

No reason to expect failure to have any effect on safety performance or health. 1

Very minor effect on system performance to have any effect on safety or health and the system does not require repair. 2

Minor effect on system performance to have any effect on safety or health and the system can require repair. 3

A failure is not serious enough to cause injury, property damage, or system damage, but can result in unscheduled maintenance or repair. 4

The system requires repair. A failure which may cause moderate injury, moderate property damage, or moderate system damage which will result in delay or loss of system availability.

5

System performance is degraded. A failure causes injury, property damage, or system damage. Some portion of mission is lost. 6

System performance is severely affected but functions. The system may not operate. Failure does not involve noncompliance with government regulations or standards.

7

System is inoperable with loss of primary function. Failure can involve hazardous outcomes and/or noncompliance with government regulations or standards.

8

Failure involves hazardous outcomes and/or noncompliance with government regulations or standards. Failure will occur with warning. 9

A failure is serious enough to cause injury, property damage, or system damage. Failure will occur without warning. 10

Table 2: FMECA scale for severity index, S.

14NGV Transportation Vol. 26 Apr - Jun 2016

FEATURE ARTICLE

features of HAZOP and FMECA methodologies, the FHIA approach has been divided into three main steps.

In the first step (see Fig. 1), the safety analysts and design experts must have an accurate description of the facility and the process (Baybutt, 2012b): process flow diagrams; piping

Table 3: FMECA scale for detection index, D.

and instrumentation diagrams (P&IDs); components reliability data; safety instrumented systems; operating instructions; safety shutdown procedures; process limits. The operational tasks (operating and maintenance procedures, inspection, etc..) that meet the operating goals and subgoals

should also be examined. This scheme should allow the team to break up the system into a number of subsystems and to describe the various operational conditions for each subsystem.

In the second step, the team compiles the FMECA worksheets for the components installed in each subsystem. This task should take into account the different operating conditions of the subsystem, which was previously examined in step 1. The team may also rank each failure according to the criticality of the failure effect and its probability of occurring using risk priority number (RPN). This amount of work isn’t a long-term commitment, but an initial workload that should be revised only if system repairs, equipment installations or changes are performed.

RPN uses three numerical values to describe each failure mode: occurrence index (O), which describes the probability that a particular accidental event will occur; severity index (S), which is a measure of the severity of consequences resulting from the undetected failure mode; and detection index (D), which describes the probability that the failure will be detected before the failure occurs.

The product of these three numbers yields the RPN as follows:

RPN = O × S × D (1)

Generally, the parameters O, S, and D are estimated by expert judgment. The specific rating descriptions and criteria can be defined by the organization or the analysis team to fit the products or processes that are being analyzed. The failures modes with higher RPN should be corrected with a higher priority than those with lower RPN.

The O, S, and D used in the FHIA analysis are based on

Likelihood of detection of failure or errorProbability of failure detection

Rank

Current control almost certainly will detect component failure/task error. <0.05 1

Current control will detect component failures/task error. Controls are able to detect within the same machine/module (almost always preceded by a warning).

0.05÷-0.15 2

The design control will almost certainly detect a component failure/task error. Controls are able to detect within the same function area.

0.15÷0.25 3

Moderately high likelihood current control will detect component failures/task error. 0.25÷0.35 4

Moderate chance that the design control will detect a potential component failure/task error, or the defect will remain undetected until the system performance is affected.

0.35÷0.45 5

Low likelihood current control will detect component failures/task error (program or operator is not likely to detect the potential design weaknesses).

0.45÷0.55 6

Very low likelihood current control will detect component failures/task error (program or operator will not to detect the potential design weaknesses).

0.55÷0.65 7

Remote chance that the design control will detect a potential component failure/task error, or the defect will remain undetected until an inspection/test is carried out.

0.75÷0.85 8

Defect most likely remains undetected (very remote chance that the design control will detect a potential cause/mechanism and subsequent failure modes). The operation will be performed in the presence of the defect.

0.85÷0.95 9

System failures are not detect (design control will not and/or cannot detect a potential cause/mechanism and subsequent failure modes). There is no design verification or the operation will certainly be performed in the presence of the defect.

>0.90 10

15 Vol.26 Apr - Jun 2016 NGV Transportation

FEATURE ARTICLE

the ranking scales presented in Tables 1 through 3, which summarise some evaluation criteria used in many hazardous industrial processes (Giardina et al., 2014).

The RPN rank is between 1 and 1000, and some users define priorities in the FMECA procedure as follows:• Very low if RPN<5 (almost

unnecessary to take the follow-up actions),

• Low if 5< RPN<20 (minor priority to take the follow-up actions),

• Medium if 20< RPN<200 (moderately priority to take the follow-up actions),

• High if 200< RPN<500 (high priority to take the follow-up actions),

• Very high if RPN>500 (absolute necessary to take the follow-up actions, unacceptable).

Obviously, the threshold value at which the risk is acceptable can be modified taking into account the assigning value by experts on the basis of criticism collected against the severity levels.

It should be noted that, in traditional FMECA applications, the human error is not adequately addressed in RPN evaluation; therefore, it is proposed the incorporation of human error into the occurrence parameter, O, as reported in Table 1.

In this step the collection of the data necessary for the analysis can be performed by using existing failure data (from a reliability database, e.g. OREDA Offshore Reliability Data Handbook, European Industry Reliability Data Bank EIReDA, etc ..). Moreover, a lot of data can be available as the baseline for maintenance plan analysis, operating instructions, operating history, for failure detection and isolation subsystem design, etc. Note that

the detection ranking, D, starts by identifying current controls that may detect a failure or effect of a failure (if there are no current controls, the likelihood of detection will be low, and the item would receive a high ranking). Obviously, the current controls should be listed for all failure modes and then the detection rankings assigned.

In the third step, the team focuses on the specific points of each subsystem, called internal and external nodes. At each of these nodes, deviations in the process parameters are examined using the guide words (Dunjó et al., 2011a; Dunjó et al., 2011b). To perform this task, the main causes that produce the performance deviations (i.e., failures or human errors), identified in step 2, can be easily used and added to the HAZOP worksheets (Fig. 1).

For each TE, identified via the HAZOP procedure, the critical causes can be ranked using the RPN index.

Advantages of the proposed methodologyVarious methodologies have been developed and reported in literature to predict potential hazards associated with LNG on-shore and off-shore terminal processes and progress has been made in the development of specific hazard identification techniques.

Nevertheless, today there are some basic issues to resolve as lack of a methodology that has been proven to be simple and versatile to support safety professionals in all steps of the risk assessment (often the choice of a particular hazard identification technique depends on the purpose for which the study is performed). A further problem is the development of analysis techniques that more consistently assess the critical safety points, such as human error, failure modes, multiple or common

cause failures, and correlation of the causes and consequences for each process unit and operation mode. This data is necessary for quantitative assessments of the occurrence probability of hazards, the characterisation of their consequences and the inclusion of these consequences in other units of the plant, if necessary.

The proposed approach can significantly reduce the subjective factors that arise from a lack of information that forces analysts to make many simplifications.

FHIA becomes possible:• to count how many

times the failure modes (cause of deviation), examined using the FMECA method, can produce accidental events (consequence) identified using the HAZOP analysis. This can be done for each operational condition;

• to identify multiple failures affecting each system or neighbouring systems;

• to rank the critical failure modes for each TE;

• to group the worksheets for each node, physical parameter (e.g. flow, pressure, temperature, level, etc.), type of deviation (e.g. “more than”, “less than”, etc.), cause of deviation (failure modes or human errors) and TEs;

• to support the analysts in the revision and revalidation of the safety analysis (for example, to study different nodes for similar processes in different subsystems, to upload safety data for same components used in different configurations, to perform Management of Change, MoC, procedure), and to help the decision makers in choosing appropriate safety controls and plan maintenance procedures;

• to collect a significant amount of information regarding the processes and safety data.

16NGV Transportation Vol. 26 Apr - Jun 2016

FEATURE ARTICLE

efforts required at company level for building brainstorming procedure, time requested for worksheet compilation, and staff training costs. However, this task entails a reasonable initial workload because tools scuh as an RAD database allow to support further and deeper safety analyses. Moreover the description of the type of severity reported in tables 1 through 3 supports the team in the choice of the suitable value.

ReferencesBaybutt P., (2012a) Conducting Process Hazard Analysis to Facilitate Layers of Protection Analysis Process Safety Progress, 31 (3), 282-286.Baybutt P. (2012b). Prework and Precompletion of Worksheets for Process Hazard Analysis. Process Safety Progress, 31 (3), 275-278.Casamirra M., Castiglia F., Giardina M., Lombardo C. (2009) Safety studies of a hydrogen refuelling station: Determination of the occurrence frequency of the accidental scenarios, International Journal of Hydrogen Energy, ISSN: 0360-3199, vol. 34, Issue 14.Castiglia F, Giardina M. Analysis of operator human errors in hydrogen refuelling stations: Comparison between human rate assessment techniques, International Journal of Hydrogen Energy, 38, pp 1166-76; 2013.CCPS. (2001) Layer of Protection Analysis: Simplified Process Risk Assessment. AIChE, Center for Chemical Process Safety (CCPS), Wiley, New York, New York,Dunjó J. , Fthenakis V. M., Darbra R. M., Vílchez J. A., Arnaldos J. (2011a) Conducting HAZOPs in continuous chemical processes: Part I. Criteria, tools and guidelines for selecting nodes. Process Safety and Environmental Protection, 89 (4), 214-22.Dunjó J. , Fthenakis V.M., Darbra R.M., Vílchez J. A., Arnaldos J. (2011b) Conducting HAZOPs in continuous chemical processes: Part II. A new model for estimating HAZOP time and a standardized approach for examining nodes. Process Safety and Environmental Protection, 89 (4), 224-233.Giardina M., Castiglia F., Tomarchio E., (2014) Risk assessment of component failure modes and human errors using a new FMECA approach: application in the safety analysis of HDR brachytherapy J. Radiol. Prot. 34, 891-914Giardina M., Morale M. (2015) Safety study of an LNG regasification plant using an FMECA and HAZOP integrated methodology. Journal of Loss Prevention in the Process Industries, 35, pp 35-45.

NTM By M. Giardina & M. Morale

The software package RAD was designed to standardise the above procedure. It allows, for example, the use of graphical interfaces to retrieve tables or to store data relevant to the component failures modes, to compile FMECA or HAZOP worksheets, to evaluate the RPN index, to choose the nodes in the P&ID of the system and to classify the TEs, etc...

It is worth noting that another advantage is the collection of a significant amount of information regarding the processes, particularly important when a company operates a similar process in several different locations and it is necessary to improve organisational memory,

communication and exchange of useful safety data, to provide information useful in developing further safety analysis or test programs, to develop monitoring criteria, to provide new ideas for safety improvements in similar designs or processes. It is important that the know-how of the plant design and of the process becomes more and more company-owned (not the prerogative of experts whose plans can fail). An important question to be addressed in this context is whether having so many severity levels, as reported in tables 1 through 3, this makes the task of the team very time consuming. Some problems in development and management of FMECA analyses are the

MASSIMO MORALE

MARIAROSA GIARDINA

Graduated with academic distinction in Mechanical Engineering at University of Palermo (1992). PhD degree in Energy Engineering, “La Sapienza”, University of Rome (2000). In December 2004 he became first Assistant Professor and then, in June 2008, Associate Professor in Technical Physics at the Department of Energy, Information Engineering and Mathematical Models, University of Palermo, Italy. Research activities mainly concern: improvement of power generation systems, refrigerating

plants working also with new fluids, optimization of thermoelectric systems for power generation, safety and risk analysis of systems for power generation, ORC, Fuel Cells, energy planning, heat transfer and energy saving.

Graduated with academic distinction in Nuclear Engineering at University of Palermo, Italy (1994). PhD degree in Energy Engineering, “La Sapienza”, University of Rome, Italy (2003). In January 2004, she became Assistant Professor in Nuclear Power Plants at the Nuclear Engineering Department, Palermo University. Research activities mainly concern Safety and Risk analysis of hazard industrial plants, Human Rate Assessment techniques, development of soft computing techniques

for safety and reliability applications (fuzzy logic), nuclear thermal-hydraulics analysis, improvement of power generation systems.

Exhibit in the LNG Facilities & Infrastructure Zone

600+Regional and International Exhibitors

54,000Square Metres Exhibition Space

25,000+International Attendees

GLOBAL REACHDelivering projects, connecting suppliers with procurement teams

Gastech provides international energy companies who operate across the up, mid and downstream sectors of the gas & LNG supply chain with a B2B platform to meet and influence highly-focused International decision-makers and buyers.

Who exhibits?Who will you meet?

Exhibiting companies represent the following sectors: IOC, NOC, EPC & FEED, Shipbuilders, Marine Engineering, Gas Processing and LNG Technology & Service Providers

EXHIBIT IN YOUR SECTOR OF EXPERTISECreating business opportunities across industry sectors

If you supply products or services within any of the sectors highlighted below then you need to reserve your stand at the GAS exhibition.

Other industry sectors expected to exhibit include:

Integrated Energy Company, Industry Associations, Extraction, Production & Processing, Health, Safety, Security & Environment, Human Resources, Information Technology, Media, Natural Gas Vehicles, Government, Explorations, Alternative Energy, Education, Embassies

Engineering Procurement

Construction & Management

Marine Shipping and Storage

Contracting, Commercial, Investment &

Trading

Petrochemicals RegasificationTransmission and

Distribution & PowerGeneration

Exhibit at Gas Asia Summit

PROJECTED DEMOGRAPHICS FOR GAS 2016

TargetedAudience

TechnicalAudience

CommercialAudience

Senior & C-levelManagement

35%30%

35%

Attendeesby job

function*

55%Asia & Oceania

10%Middle East

20%Europe

5%Africa

10%The Americas

AttendeesBY REGION

For more details about exhibiting or participating, please call +65 6422 1475, email [email protected] or visit www.gasasiasummit.com/ngvtransportation1

4th EDITION

Powered by

INCORPORATING:ORGANISED BY: SUPPORTED BY: PART OF: HELD IN:

Commercial Audience: Business Development Manager, Sales & Marketing Manager, Purchasing Manager, Country Manager, Purchasing Director, Trader, Operations Manager, Financier & Lawyer, Analyst/Business Advisor/Consultant

Senior & C-level Management: General Manager, Head of Dept & Directors, Chairmen, Presidents, CEO, COO, Vice Presidents, Commercial/Business Development Director & Sales/Marketing Director

GAS A4 Advert v2.indd 1 04/04/2016 15:10

19 Vol.26 Apr - Jun 2016 NGV Transportation

SPECIAL REPORT

DIVERSIFYING PAKISTAN’S ENERGY NEEDS – A Case of Natural Gas & LNG

E nergy availability has become one of the most significant needs of the developing

economies and Pakistan is no exception. Pakistan has been facing perpetual energy crises. The energy mix of the country is not fairly balanced as it is dominated by traditional fossil fuels like oil and natural gas with a little to minute role of hydel, coal, nuclear and modern day alternate fuel sources of wind, bio-gas and solar.

Pakistan’s economic growth demands higher energy inputs whereas indigenous oil and gas production is not sufficient

enough to quench energy thirsty economy of the country. Besides other factors like international economic crises and pressures of war on terrorism, energy shortages have also played a vital role in decline in country’s GDP growth during last few years.

Pakistan’s primary energy supply mix clearly shows Natural gas as playing major role in country’s economic development by accounting for nearly 50% of its total primary energy supply mix. Pakistan’s Natural gas production has remained stagnant at nearly 4,000 mmcfd during the last decade. Over last few decades, Pakistan has developed a

formidable gas sector. Its economy has so far survived due to abundant initial gas discoveries. The Natural gas market of Pakistan is among the biggest in Asia and is some what comparable with the size to France and Netherlands. Pakistan was gas sufficient till 2005 however after that gas production didn’t keep up with the gas demand. The constrained demand of Natural gas is 6,000 mmcfd whereas the unconstrained demand is 8,000 mmcfd (8 BCFD) or even potentially higher than this during winters when the domestic gas demand surges exponentially.

Pakistan’s total Natural gas Transmission and Distribution (T&D) network is approx 150,000 Kms with the consumer base of nearly 7.5 Million. During last 5 years, on average, approximately 0.38 million consumers were added on the pipeline network of the country despite a decline in natural gas volumes. This also shows that demand of natural gas is high in the country. Piped gas is available to only 25% of population.

The T&D network of the country is administered by two Government owned companies i.e. SNGPL and SSGCL. Sui Northern Gas Pipelines Limited (SNGPL) supplies natural gas in the northern part of the country i.e. the provinces of Punjab, Khyber Pakhtunkhwa

1,500 40 Exhibitors

EXHIBIT IN YOUR SECTOR OF EXPERTISECreating business opportunities across industry sectors

If you supply products or services within any of the sectors highlighted below then you need to reserve your stand at the GAS exhibition.

Other industry sectors expected to exhibit include:

Integrated Energy Company, Industry Associations, Extraction, Production & Processing, Health, Safety, Security & Environment, Human Resources, Information Technology, Media, Natural Gas Vehicles, Government, Explorations, Alternative Energy, Education, Embassies

Engineering Procurement

Construction & Management

Marine Shipping and Storage

Contracting, Commercial, Investment &

Trading

Petrochemicals RegasificationTransmission and

Distribution & PowerGeneration

Exhibit at Gas Asia Summit

PROJECTED DEMOGRAPHICS FOR GAS 2016

TargetedAudience

TechnicalAudience

CommercialAudience

Senior & C-levelManagement

35%30%

35%

Attendeesby job

function*

55%Asia & Oceania

10%Middle East

20%Europe

5%Africa

10%The Americas

AttendeesBY REGION

For more details about exhibiting or participating, please call +65 6422 1475, email [email protected] or visit www.gasasiasummit.com/ngvtransportation1

4th EDITION

Powered by

INCORPORATING:ORGANISED BY: SUPPORTED BY: PART OF: HELD IN:

Commercial Audience: Business Development Manager, Sales & Marketing Manager, Purchasing Manager, Country Manager, Purchasing Director, Trader, Operations Manager, Financier & Lawyer, Analyst/Business Advisor/Consultant

Senior & C-level Management: General Manager, Head of Dept & Directors, Chairmen, Presidents, CEO, COO, Vice Presidents, Commercial/Business Development Director & Sales/Marketing Director

GAS A4 Advert v2.indd 1 04/04/2016 15:10

20NGV Transportation Vol. 26 Apr - Jun 2016

SPECIAL REPORT

and State of the Azad Jammu and Kashmir while Sui Southern Gas Company Limited (SSGCL) caters to gas needs of consumers in southern Pakistan i.e. the provinces of Sind and Balochistan. The consumer price of gas is regulated and determined on the basis of a fixed rate of return on the assets of gas utility companies by the Government of Pakistan. The Oil and Gas Regulatory Authority (OGRA) is publishing and overseeing Natural gas consumer prices in the country.

The peculiar energy mix of the country created space for oil as a major fuel source for power generation which resulted in piling up of circular debt. The gas dependant sectors are suffering with the number of power plants shut down on account of uneconomical fuel use (HSD), rationing of gas. This resulted in enhanced imports of urea. The largest use of natural gas is in power sector followed by domestic, fertilizer, industrial and transport sectors. Pakistan is being ranked as the World’s top CNG consuming country with approximately 3 million vehicles running on CNG, having been invested $0.5 billion comprising mainly of machinery and CNG kits. During winters (December to February)

gas supply to CNG Stations is completely cut off in Punjab under the load management as its share in gas supply is about 5% while consumption is approximately 46% of national gas consumption. The choice of conversion from petrol to CNG is basically due to the fact that prices of CNG are significantly less than that of petrol. The low pressure issues are faced by the consumers especially by those situated at the tail-end of our distribution network, mainly during winter. Pakistan is the sixth largest urea producer in the World with total installed capacity of 6.9 million tons whereas the domestic demand stands at around 5.9 million tons despite which the country has to opt for import option as production falls short of demand due to intermittent gas supplies.

The gas shortages in the country resulted, among

affecting other sectors, in curtailment of supply to power producers, contributing to the electricity load shedding which in turn badly impacts the economy. The economic cost of the Natural gas shortages is incurring one billion dollars per years, as the country has to import expensive furnace oil, kerosene, LPG and diesel to make up for its energy requirements. The country is facing severe Natural gas shortages to the tune of nearly 2 bcfd.

Government of Pakistan (GoP) is taking following steps to overcome the shortage of Natural gas in the country:

i. Restrain Natural gas demand at current level,

ii. Enhance indigenous gas production,

iii. Import of Gas from Iran (IP Pipeline),

iv. Import of Gas from Turkmenistan (TAPI Pipeline),

v. Import of LNG.

It may not be a logical approach to restrain the demand of energy products at a certain levels unless a cost effective alternative is provided to consumers. There emerges a need for multiple sources of energy so that if one source dries up or is not available for what so ever reasons, the other option is there to fill the gap. For geopolitical reasons, pipeline imports have failed to materialize and have been

Year Gas Demand Gas Supplies ShortfallFY 15 6 4 2.0FY 20 6.9 3.1 3.8FY 25 7.6 1.6 6.0FY 30 8.7 0.7 8.0

Table: Natural Gas Demand - Supply Projections of Pakistan (BCFD)Source: Annual Report of Oil and Gas Regulatory Authority (OGRA)

21 Vol.26 Apr - Jun 2016 NGV Transportation

SPECIAL REPORT

Pakistan-India (TAPI) pipeline which is 56 inch – 1,325 mmcfd capacity is not available before end 2019.

Liquefied Natural Gas (LNG), therefore, remains the only immediate cost-effective solution for Pakistan’s energy problems. LNG is a game changer which could help the resource constrained Pakistan save more than a billion dollars per year in cost-to-energy terms.

After ten years, five failed attempts at various times by the four consecutive governments for setting up LNG infrastructure in Pakistan, the country’s first LNG terminal got completed and country’s pipeline network saw its first LNG molecule on 28th March 2015, just less than 11 months from date of contract award i.e. 30th April 2014. A 100% Government owned company Inter State Gas Systems (ISGS) with expertise in handling large international infrastructure projects like IPI and TAPI; was mandated the task to coordinate the Fast Track Project by facilitating the acquisition of LNG services through an open competitive

termed as pipedream by the international energy experts because of security concerns involving Afghanistan’s terrain and financial difficulties associated with the projects.

Indigenous exploration and production of oil and gas in the country can help in huge monetary savings and would go a long way in enhancing Pakistan’s national security and buttressing energy self reliance of the country with more anticipated infrastructure developments in the areas of the country which are somewhat less developed. Geographically speaking, Pakistan is best positioned to act as the energy corridor as it is in a good location for pipelines to come through it. The 42 inch - 750 mmcfd Iran-Pakistan (IP) pipeline, first conceived in 1995, got delayed due to international sanctions on Iran and the first gas shipment from it will not be available till the end 2017. Iranian gas is an energy lifeline for Pakistan with longer future availability from a country having the World’s second largest gas reserves. Turkmenistan-Afghanistan-

bidding process. GoP’s entity i.e. SSGCL was assigned to enter a 15 years contract with Engro Elengy Terminal Limited (EETL). As per GoP’s above scheme, the terminal will be for tolling services having a contracted capacity of 200 MMCFD of RLNG in year-1 and 400 MMCFD from year-2 till the end of contract term of 15 years whereas EETL’s FSRU shall be capable of pumping 690 mmcfd (peak) of RLNG into the grid with an average output of 600 mmcfd.

Pakistan’s LNG receiving infrastructure for offshore regasification terminal is being served by a Floating Storage and Regasification Unit (FSRU). An FSRU is a flexible, cost effective way to receive and process shipments of LNG. FSRU is increasingly being used to meet natural gas demand in smaller markets or as temporary solution until onshore facilities are built. It is likely to remain a preferred technology option for emerging markets because of its flexible deployment capabilities, smaller capacities, quick start-ups and relatively low costs

22NGV Transportation Vol. 26 Apr - Jun 2016

SPECIAL REPORT

compared to those of onshore terminal.

The LNG supply chain is a captious process and stability of supply is the most important factor in LNG procurement. In order to secure long-term LNG the countries have to pay certain premium. There is no LNG benchmark in the world and LNG prices are affected by a variety of financial, geographical, and political variables. LNG trading portfolios are built on a mix of long-term, medium-term, and spot procurement at significantly different price levels. Pakistan will need several long-term and medium-term LNG contracts in addition to spot LNG procurement to satisfy its demand.

LNG import is a major milestone for Pakistan’s gas sector. LNG development will serve as an impetus for growth not only in gas sector but also in gas consuming sectors including fertilizer and power sector. Pakistan State Oil (PSO), state owned oil marketing company, has been assigned the task of LNG imports from Qatar. Pakistan State Oil (PSO) and Qatargas Operating Company Limited (QOCL) were nominated by the two respective governments to negotiate the LNG Sales Purchase Agreement (LNG SPA).

At present, SNGPL and SSGC have the capacity to transport only 400 mmcfd of LNG through their pipeline networks. Pakistan’s North side is with intense appetite for Natural gas. For laying an LNG pipeline from Lahore to Karachi, called North-South pipeline, Pakistani and Russian governments signed an agreement last year. Russia would spend 85% of the $2 billion cost of the project. Pakistan and China signed a government-to-government deal to develop the Gwadar LNG pipeline and terminal. China

would provide 85% of financing at a concessionary rate for the pipeline, which is expected to cost less than $2 billion.

Pakistan and Qatar during last month have signed a worth $16 billion deal of LNG for a period of 15 years. Pakistan has been suffering through a severe energy crisis and the import of LNG from Qatar would be a positive step to address the issue. The deal has large prospects for the energy sector as Pakistan would be able to meet its energy requirements. 3.75 million tons of LNG would be imported annually on a government-to-government basis. The price of 13.37pc of Brent value has been agreed which is claimed to be a cheaper one than the gas to be imported through pipelines projects including Iran-Pakistan (IP) and Turkmenistan-Afghanistan-Pakistan-India (TAPI) projects.

In the first phase, from 2016 to first quarter of 2017, the annual contract LNG quantity would be prorate of 2.25m tons which would be increased to 3.75m tons per annum beginning second quarter of

2017. The long-term agreement would also provide for annual upward and downward flexibilities of up to three LNG cargoes against per contract year. The LNG deal would also provide the LNG to Pakistan on a 15-day defer payment scheme against the earlier settlement of defer payment for 10 days.

Regasified LNG (RLNG) is the most cost effective fuel for power generation due to greater efficiency, low maintenance costs, ease of transportation, no pilferage or adulteration and minimal environmental impact. Pakistan is expected to be a 20 mtpa (2.5 bcfd) market within 3 years with anticipated ranking of being among top 5 importers of the world. LNG imports will help diversifying energy portfolio of the country being a short-medium term solution however in order to achieve sustainable energy development and foster investment and economic growth of the country it will have to keenly focus on such multiple energy fronts.

NTM By Rahil Ihsan Pitafi

Mr. Rahil Ihsan Pitafi is a graduate Chemical Engineer (2006) with additional qualifications of Executive MBA - Project Management (2009), Master in Energy Management (2010) and MS in Supply Chain Management (currently in final semester).Beside studies, Mr. Pitafi has acquired approximately nine (09) years of work experience with the energy regulator i.e. Oil and Gas Regulatory Authority (OGRA) of Pakistan which was established in 2002.Mr. Pitafi has an extensive experience as regards

regulation of natural gas sector of Pakistan. He remained involved in development of Natural Gas Transmission and Distribution Standards, Natural Gas Regulated (Third Party Access) Rules 2012 and grant of 7 licenses to various local and international LNG Project Developers.Since year 2011, Mr. Pitafi has been working as Assistant Executive Director (LNG) and dealing with regulation of LNG Sector which is a developing sector. He has worked from start to consultant appointment and during commissioning, operation and issuance of license to Pakistan’s first ever LNG Re-gasification Terminal (Engro Elengy Terminal Limited).

RAHIL IHSAN PITAFI

NETWORK WITH AN INTERNATIONAL AUDIENCE OF POWER PROFESSIONALS8,000+ industry experts working together to exchange ideas on ways to expand and strengthen the Asian power industry.

REGISTER TO ATTEND AT: WWW.ASIAPOWERWEEK.COM

50+ conference sessions as part of a multi-track conference programme

150+ eminent international speakers from around the world

Hot topic presentations and panel discussions

about best practices and new technology developments, with the aim of providing

solutions for the Asian power sector

8,000+ attendees from around the world looking to do business

and discover new solutions

Stay ahead of the competition, meet your customers face to face

85% of exhibitors stated the event met/exceeded their objectives

of establishing contacts for future sales and improving business

230+ leading exhibitors from the region and world-wide showcasing

their latest technologies

8,000+ attendees from around the world looking to do business

and discover new solutions

Attending as a visitor is FREEwhen you pre-register online

Owned & Managed by:

ASIA POWER WEEK

20-22 SEPTEMBERKINTEX, SEOUL, SOUTH KOREA

2016

3 DAYS u 3 SHOWS u 1 VENUE

Official Publications

LEARNabout the latest challenges

and solutions for the Asian power

generation industry

SHOWCASEyour company’s products

and services to the Asian power generation

industry

EXPERIENCEfirst-hand the latest technology for the

Asian power generation industry

JOIN US AT ASIA’S PREMIER POWER GENERATION EVENT

0672_APW16_UK_A4_Ad.indd 1 3/14/16 1:44 PM

24NGV Transportation Vol. 26 Apr - Jun 2016

FEATURE ARTICLE

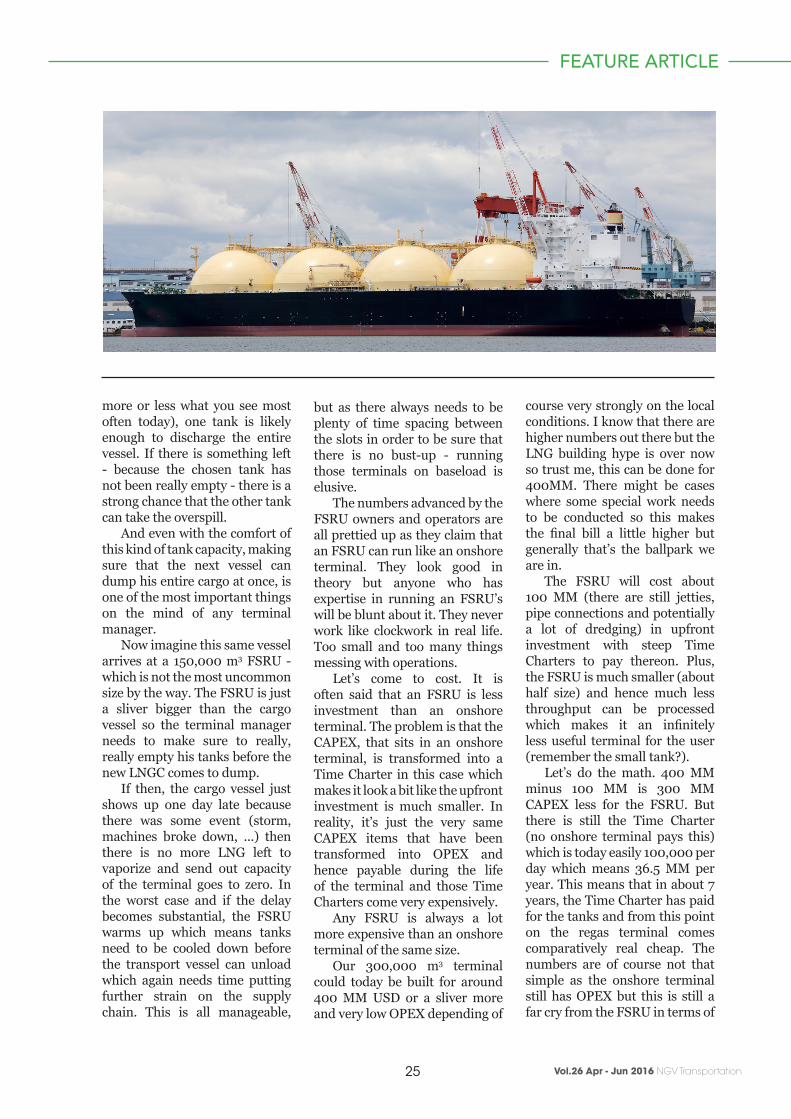

FLOATING REGASIFICATION

Many years ago, an old sea bear and a good friend told me that whatever

you do on land gets inevitably harder when you are on the water. Space is confined and processes that have been designed for still land are exposed to all kinds of movements.

This simple deduction stuck with me and shaped my thinking

when it came to industrial processes off the shore - especially when it comes to LNG.

At the last GasTech, FSRU’s were all the rage. No wonder as those vessels are being noted as technologically mature by now. They also appear to be a quick way to get LNG into a yet to be developed market for LNG. And to be totally open with you - this reasoning strikes more than just a cord with any sane person.

Tuck the processing part of the receiving terminal inside the vessel and henceforth you deliver Natural Gas, not a super-cold liquid that needs processing before it can be used. Besides, all the design, engineering and building part can be done in the dock of a shipyard instead of some point in the total wilderness (potentially) providing lots of savings as the plants comes all built up, pre-tried, pre-stress tested to the theater of operations. Wherever this may be.

Cool ...However, no matter how cool

those vessels are (hey, they are truly neat and I have nothing but admiration for the folks putting those swimming processing plants together), but they are no key to eternal bliss for each and everyone wanting to have a quick regasification terminal up and running in little time.

FSRU’s are still basically a ship with its constrained deck space where industrial processes must be performed in perpetual movement. That’s not a technological problem as the processes involved do not do much more than exchanging heat. It rather is a problem of putting things - that were designed for operations from the solid ground - onto a wallowing deck. Those are really big boats, so they cannot enter any little bitsy harbor just as LNG Carriers can’t go everywhere. Even some deepwater harbors need dredging in order to put those FSRU’s there.

But for all their enormous size, compared to the storage capacity of even a smaller terminal, they are very restricted. Let’s imagine a 300,000 m3 LNG terminal with two 150,000 m3 tanks. That’s not really super large - but a decent size. If a vessel with 145,000 m3 of LNG comes in (and that’s

- A REALITY CHECK

25 Vol.26 Apr - Jun 2016 NGV Transportation

FEATURE ARTICLE

more or less what you see most often today), one tank is likely enough to discharge the entire vessel. If there is something left - because the chosen tank has not been really empty - there is a strong chance that the other tank can take the overspill.

And even with the comfort of this kind of tank capacity, making sure that the next vessel can dump his entire cargo at once, is one of the most important things on the mind of any terminal manager.

Now imagine this same vessel arrives at a 150,000 m3 FSRU - which is not the most uncommon size by the way. The FSRU is just a sliver bigger than the cargo vessel so the terminal manager needs to make sure to really, really empty his tanks before the new LNGC comes to dump.

If then, the cargo vessel just shows up one day late because there was some event (storm, machines broke down, ...) then there is no more LNG left to vaporize and send out capacity of the terminal goes to zero. In the worst case and if the delay becomes substantial, the FSRU warms up which means tanks need to be cooled down before the transport vessel can unload which again needs time putting further strain on the supply chain. This is all manageable,

but as there always needs to be plenty of time spacing between the slots in order to be sure that there is no bust-up - running those terminals on baseload is elusive.

The numbers advanced by the FSRU owners and operators are all prettied up as they claim that an FSRU can run like an onshore terminal. They look good in theory but anyone who has expertise in running an FSRU’s will be blunt about it. They never work like clockwork in real life. Too small and too many things messing with operations.

Let’s come to cost. It is often said that an FSRU is less investment than an onshore terminal. The problem is that the CAPEX, that sits in an onshore terminal, is transformed into a Time Charter in this case which makes it look a bit like the upfront investment is much smaller. In reality, it’s just the very same CAPEX items that have been transformed into OPEX and hence payable during the life of the terminal and those Time Charters come very expensively.

Any FSRU is always a lot more expensive than an onshore terminal of the same size.

Our 300,000 m3 terminal could today be built for around 400 MM USD or a sliver more and very low OPEX depending of

course very strongly on the local conditions. I know that there are higher numbers out there but the LNG building hype is over now so trust me, this can be done for 400MM. There might be cases where some special work needs to be conducted so this makes the final bill a little higher but generally that’s the ballpark we are in.

The FSRU will cost about 100 MM (there are still jetties, pipe connections and potentially a lot of dredging) in upfront investment with steep Time Charters to pay thereon. Plus, the FSRU is much smaller (about half size) and hence much less throughput can be processed which makes it an infinitely less useful terminal for the user (remember the small tank?).

Let’s do the math. 400 MM minus 100 MM is 300 MM CAPEX less for the FSRU. But there is still the Time Charter (no onshore terminal pays this) which is today easily 100,000 per day which means 36.5 MM per year. This means that in about 7 years, the Time Charter has paid for the tanks and from this point on the regas terminal comes comparatively real cheap. The numbers are of course not that simple as the onshore terminal still has OPEX but this is still a far cry from the FSRU in terms of

26NGV Transportation Vol. 26 Apr - Jun 2016

FEATURE ARTICLE

total cash.Let’s attack the time factor

now. FSRU’s are essentially ready to go instantly.

Really?First, there needs to be

preparations at the harbor of operation for the FSRU which usually takes around a year to complete. But then, you really need to have an FSRU ready for action. But since LNG has become real cheap now and as those prices are expected to stay low for a little while, there suddenly is enormous demand for FSRU’s. Now they are hard to get and if you ever get one, you will pay a really steep price. The times of cheap FSRU’s are over - at least for a little while. So waiting for an FSRU to be available for your project might make you wait for years. Or you pay high. Pick your torture.

Are FSRU’s all bad then? Absolutely not.

If they are used the right way, they are technical marvels that will serve you well if you understand your own situation and know what you are doing. You must use them the right way for the right set of circumstances to give you pleasure.

So, what’s the right use then?Let’s come back to the size

of the vessel for a moment. Most of the newly built FSRU’s in shipyards today are in the 170,000 m3 range. This means, that one can safely unload vessels up to 150,000 m3 there at once which will cover most of the LNGC fleet of this planet. Still, this means that every time they want to take in a new load, they must go very close to their heel in order to make enough space which means that the dance of the vessels must be really well choreographed. There is no demand variation that can be accommodated with this arrangement. Or variation is built artificially at astronomic costs as the real throughput of

your installation goes down a lot or the transport chain involves a lot of LNGC vessel parking.

If there is an LNG hub nearby that is willing and able to dispatch a vessel at short notice in order to keep the terminal running, this might just work out for you. Better still if the nearby hub dispatches much smaller vessels (let’s say a 125,000 m3) as this would enable the FSRU to keep significant spare for the next vessel and the dance of the vessels does not have to be so precarious. In those instances, FSRU’s are great tools to open a new market or hook a city that has no access to gas otherwise into the network.

But if there are strong demand variations, if the terminal is far away from any potential hub (and I will define the notion of LNG hub a bit further in another post) or if the throughput needs are colossal, skip the FSRU and go for the steel and mortar kind. It’s going to take you a little longer to get it up and running but it will save you a big wad of bucks and it’s not going to make you mad as you will be able to tailor its operations to your needs.

Plus, if ever you think of expanding for whatever reason, you just put another tank or some more vaporizers there.

However, if you really need a quick solution, put an FSU (Floating Storage Unit) which is essentially a regular transport vessel fixed on a berth and acting as a floating tank, put some vaporizers on the ground (that’s, not the dealbreaker, believe me) and you will need the jetty anyhow and build the onshore tanks while your FSU makes up for them fully knowing that the current mess is not going to last.

FSRU’s are great for peak markets where for some months demand just goes through the roof for a little while and they need a way to cover that. That’s Brazil, that’s Kuwait, that’s Dubai. In those peak markets, the peaks are so incredibly expensive that even a super expensive FSRU makes sense. Anything makes sense there if it just works. However, in a baseload market, you need something more solid.

You need a big, classic, solid, reliable, concrete gray, onshore terminal on your coast, not a flimsy FSRU.

Rudolf is an entrepreneur and consultant active in the “methane based fuels and energy” industry. He is the founder of countless initiatives all with the aim to promote a methane based economy and affordable environmental protection.He is a professional business developer and negotiator who is involved in all aspects of the LNG business. He is also very actively promoting green technologies that work well with methane based technologies.

Rudolf has helped secure first Regasification capacity for his former employer EconGas at the GATE terminal in 2007 and holds a Masters degree in Commercial and Taxation law from the Jean Monnet faculty in Paris. He also runs a number of blogs, among them www.lng.guru and www.lng.jetzt.

RUDOLF HUBER

NTM By Rudolf Huber

19th

October 2016, Resorts World Sentosa, Singapore

SINGAPORE INTERNATIONAL BUNKERINGConference and Exhibition

www.sibconsingapore.com

1600+TOTAL

PARTICIPANTS

70COUNTRIES

THE WORLD’S

LARGESTBUNKERING

EVENT

Organised by:Maritime and Port

Authority of Singapore

Managed by:IBC Asia (S) Pte Ltd

The 18th Singapore International Bunkering Conference and Exhibition brought in over 1600 participants from all over the world, and lived up to its reputation of the “place to be” for the marine fuel industry. The programme comprising of cross sector industry roundtables, high level keynote speeches and market analysis sessions proved extremely popular. The SIBCON Cocktail was a spectacular success and the highlight of the various networking opportunities available.

The Maritime and Port Authority of Singapore is pleased to announce that the next edition of SIBCON will be back in October 2016 – watch the website for more details on dates and location.

PROGRAMME AND SPEAKING OPPORTUNITIES:Sukumar Verma

Jonathan KiangSenior Business Development ManagerEmail: [email protected]

GUEST OF HONOURLui Tuck Yew

Minister for Transport

KEYNOTE ADDRESSTerence Yuen

Country PresidentBP Singapore

KEYNOTE ADDRESSJeremy Nixon

Chief Executive Offi cer - Global Liner Division

NYK Line

INDUSTRY ADDRESSChris MidgleyVice President

Oil Markets AnalysisShell International Petroleum

Company

2014 SPEAKERS INCLUDED

PLEASE CONTACT THE PROJECT TEAM FOR ANY INQUIRIES:

NG

VTM

2016

C

M

Y

CM

MY

CY

CMY

K

LNG FUELS A4 2016 ADVERT.pdf 1 01/03/2016 16:32

29 Vol.26 Apr - Jun 2016 NGV Transportation

SPECIAL REPORT

SAFETY AND RISKS OFA DUAL FUEL SYSTEM WITH LNG AND DIESEL