66

University of Limerick Niall Gilbride Dynamic Jet Fuel Hedging using an Error Correction Model with GARCH Error Terms MSc in Computational Finance 2014-2015

| Date post: | 23-Jan-2018 |

| Category: |

Documents |

| Upload: | niall-gilbride |

| View: | 612 times |

| Download: | 2 times |

University of Limerick

Niall Gilbride

Dynamic Jet Fuel Hedging

using an Error Correction

Model with GARCH Error

Terms

MSc in Computational Finance

2014-2015

This dissertation is solely the work of the author and submitted in partial fulfilment of the

requirements of the MSc in Computational Finance, University of Limerick, Ireland

Dynamic Jet Fuel Hedging using an Error

Correction Model with GARCH Error Terms

Niall Gilbride 09008201

MSc in Computational Finance

2014-2015

Dr. Bernard Murphy

Word Count: 16,500

i

Abstract

Jet fuel hedging has been shown to stabilise airline profits and increase airline value. This

research analyses the cross hedging performance of Brent crude oil, West Texas Intermediary

crude oil, low sulphur gasoil and NYMEX heating oil in reducing airlines spot price exposure

to Gulf54 grade jet fuel. Three econometric techniques popular in the cross hedging literature

are applied to the cross-hedge portfolios with the added constraint that the portfolios must be

able to qualify for hedge accounting status. The analysis shows that hedging on a weekly

horizon is not sufficient for any of the cross-hedge portfolios to meet hedge accounting

standards and that instead hedging must be accomplished on monthly and quarterly horizons.

The results indicate that cross-hedging Gulf54 grade jet fuel using futures on Brent crude oil

provides the best hedging option for airlines across all horizons when the constraint of

meeting hedge accounting standards is taken into account.

ii

Acknowledgements

I would sincerely like to thank Dr. Bernard Murphy for his feedback and support, not only

throughout the process of carrying out this study, but throughout the year in all aspects of the

MSc. in Computational Finance for which this research represents the conclusion.

As this study is not the product of any one area of my academic work this year and rather a

culmination of the academic progress made since last September, I must also thank Dr.

Finbarr Murphy, Orla McCullagh and Dr. Weiou Wu for the progress that was made under

their guidance. I would also like to thank Prof. Zeno Adams and Mathias Gerner on whose

research this study is based, in particular Prof. Adams and for his correspondence during the

summer months.

iii

Table of Contents Abstract ....................................................................................................................................... i

Acknowledgements .................................................................................................................... ii

Table of Tables .......................................................................................................................... v

Table of Figures ........................................................................................................................ vi

Table of Equations .................................................................................................................... vi

Research Question ..................................................................................................................... 1

Introduction ................................................................................................................................ 2

Jet Fuel Hedging ........................................................................................................................ 3

SFAS 133 ................................................................................................................................... 4

Preliminary Considerations ........................................................................................................ 7

Hedge Ratio & Hedging Performance ................................................................................... 7

Hypothesis Testing & Statistical Significance ....................................................................... 9

Regression Model .................................................................................................................... 11

Unit Root Testing ................................................................................................................. 11

Regression Analysis ............................................................................................................. 13

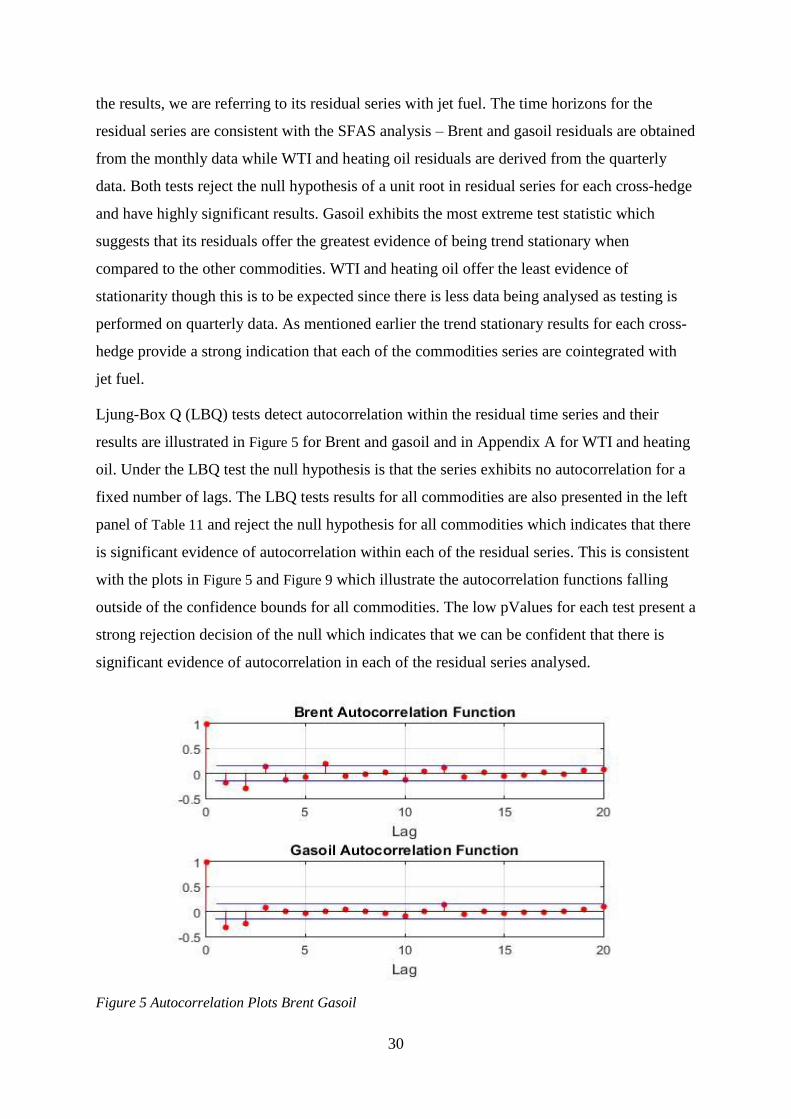

Residual Series ......................................................................................................................... 15

Autocorrelation .................................................................................................................... 15

Heteroscedasticity ................................................................................................................ 16

Error Correction Model............................................................................................................ 17

Co-Integration ...................................................................................................................... 17

Error Correction Analysis .................................................................................................... 19

Basis Risk............................................................................................................................. 22

GARCH Extension................................................................................................................... 21

GARCH Analysis................................................................................................................. 21

Results & Discussion ............................................................................................................... 23

SFAS 133 ............................................................................................................................. 23

iv

Unit Root Testing ................................................................................................................. 27

Residual Diagnostics ............................................................................................................ 29

Cointegration Analysis......................................................................................................... 32

Optimal Hedge Ratio ........................................................................................................... 34

Hedge Performance .................................................................................................................. 37

Brent Crude Oil .................................................................................................................... 38

Low Sulphur Gasoil ............................................................................................................. 40

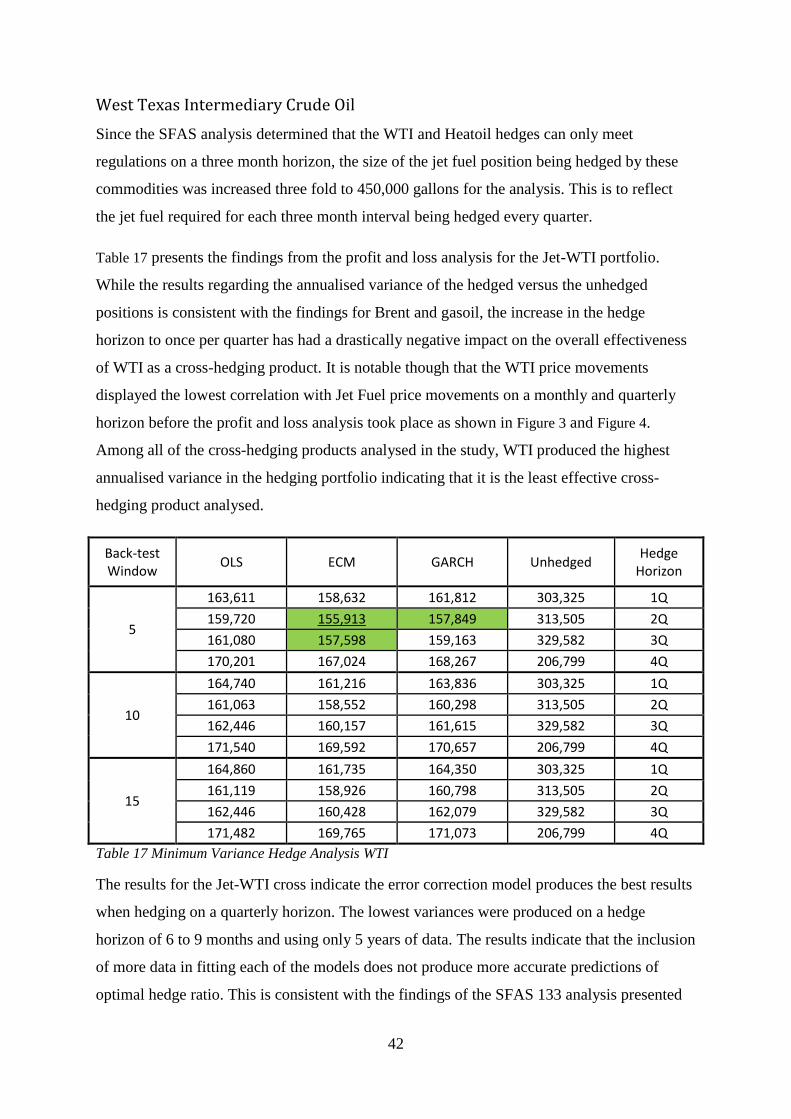

West Texas Intermediary Crude Oil .................................................................................... 42

Home Heating Oil ................................................................................................................ 44

Conclusions .............................................................................................................................. 45

Bibliography ............................................................................................................................ 46

Appendix A .............................................................................................................................. 50

Appendix B .............................................................................................................................. 51

MATLAB Import Data ........................................................................................................ 51

MATLAB Define Parameters .............................................................................................. 51

MATLAB Loop Arguments ................................................................................................ 51

MATLAB SFAS 133 ........................................................................................................... 51

MATLAB Unit Root Analysis ............................................................................................. 52

MATLAB OLS Regression Model ...................................................................................... 53

MATLAB Residual Diagnostics .......................................................................................... 53

MATLAB Error Correction Model ...................................................................................... 54

MATLAB ECM GARCH Extension ................................................................................... 54

MATLAB Dynamic Hedge Ratio ........................................................................................ 55

MATLAB Calculate P&L .................................................................................................... 57

v

Table of Tables

Table 1 Commodity Hedge Horizons ........................................................................................ 5

Table 2 Unit Root Hypotheses ................................................................................................. 12

Table 3 R-Square Value based on Weekly Hedging Horizon ................................................. 23

Table 4 R-Square Value based on Monthly Hedge Horizon ................................................... 23

Table 5 R-Square Value based on Quarterly Hedge Horizon .................................................. 23

Table 6 Augmented Dickey Fuller Test Levelled Series ......................................................... 27

Table 7 Kwiatkowski Phillips Schmidt Shin Test Levelled Series .......................................... 28

Table 8 Augmented Dickey Fuller Test Differenced Series .................................................... 28

Table 9 Kwiatkowski Phillips Schmidt Shin Test Differenced Series .................................... 29

Table 10 Residual Series Stationarity Tests............................................................................. 29

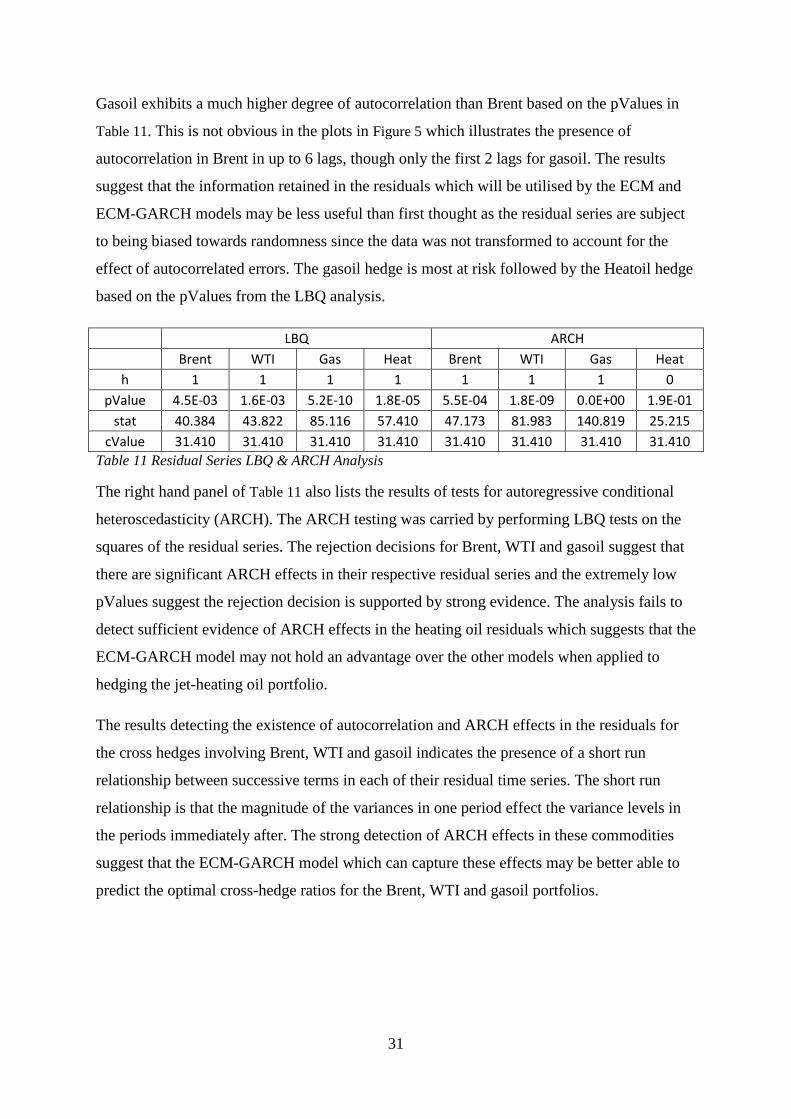

Table 11 Residual Series LBQ & ARCH Analysis ................................................................. 31

Table 12 Residual Series Heteroscedasticity Analysis ............................................................ 32

Table 13 Cointegration Analysis ............................................................................................. 32

Table 14 ECM Residual Speed of Adjustment ........................................................................ 34

Table 15 Minimum Variance Hedge Analysis Brent ............................................................... 38

Table 16 Minimum Variance Hedge Analysis Gasoil ............................................................. 40

Table 17 Minimum Variance Hedge Analysis WTI ................................................................ 42

Table 18 Minimum Variance Hedge Analysis Heatoil ............................................................ 44

vi

Table of Figures

Figure 1 Jet-Brent OLS Regression Plot .................................................................................. 14

Figure 2 SFAS Analysis Weekly Time Horizon...................................................................... 24

Figure 3 SFAS Analysis Monthly Time Horizon .................................................................... 25

Figure 4 SFAS Analysis Quarterly Time Horizon ................................................................... 26

Figure 5 Autocorrelation Plots Brent Gasoil ........................................................................... 30

Figure 6 Commodity Spot Prices 2009-2015 .......................................................................... 33

Figure 7 Dynamic Hedge Ratio Brent Crude Oil..................................................................... 34

Figure 8 Dynamic Hedge Ratio LS Gasoil .............................................................................. 35

Figure 9 Residual Autocorrelation Plots .................................................................................. 50

Figure 10 Residual QQ Plots ................................................................................................... 50

Figure 11 Residual Histograms ................................................................................................ 50

Table of Equations

Equation 1 Optimal Hedge Ratio ............................................................................................... 7

Equation 2 Optimal Number of Contracts ................................................................................. 8

Equation 3 P&L Series............................................................................................................... 8

Equation 4 Profit and Loss Spot ................................................................................................ 8

Equation 5 Profit and Loss Futures ............................................................................................ 9

Equation 6 Annualised Variance Gasoil .................................................................................... 9

Equation 7 Linear Model ......................................................................................................... 13

Equation 8 Error Correction Model ......................................................................................... 20

Equation 9 Conditional Variance ............................................................................................. 21

1

Research Question

The research question posed is which commodity out of Brent crude oil, WTI crude oil,

low sulphur gasoil and home heating oil is most effective when utilised in a cross-hedge

in order to reduce an airlines price exposure to Gulf54 grade jet fuel. The work intends to

build on similar research carried out by (Adams & Gerner, 2012) who evaluated the

performance of the four cross-hedge commodities listed above using (i) an OLS

regression model, (ii) an Error Correction model (ECM) and (iii) an ECM with GARCH

error terms. This study hopes to build on this and other previous work by conducting the

similar research to (Adams & Gerner, 2012) but will also incorporate analysis on whether

each potential cross-hedge can qualify for hedge accounting classification under

contemporary FAS 133 regulations. Each of the three models will be fitted to the data and

all three will be used in back-testing. The best performing commodity will be the one

which qualifies for hedge accounting under FAS 133 guidelines and produces the lowest

annualised variance for a portfolio containing 150,000 gallons of jet fuel when back-

tested over a varying number of years for each commodity leading up to 2015.

It is hoped that this study will contribute to the current literature in the field in two

existing ways and one new way. It is expected the results will support the evidence that

error correction models perform better than OLS regression models when hedging price

exposure in commodity portfolios using futures contracts. This research will also

contribute to the debate about which crude oil based commodity provides the best cross-

hedging instrument for jet fuel under current market conditions. Finally it is hoped that

the research will draw attention to the fact that hedging jet fuel on a weekly horizon, as is

the practice in a number of studies, does represent the best option for airlines as futures

hedging using the chosen products on this horizon may not be eligible for hedge

accounting status under the current regulations.

2

Introduction

The passenger airline industry is growing at a rate of 5% per annum and is by and large a

competitive industry. While jet fuel fluctuates in price regularly and accounts for the

second largest expenditure for passenger airlines, the competitive pressures associated

with the passenger airline business mean that increases in jet fuel prices cannot easily be

passed on to consumers for fear that increases in charges will result in a loss of market

share. The resulting exposure to this volatile commodity represents a significant source of

uncertainty for airline profits. Jet fuel hedging is the practice of entering into financial

contracts in order the fix the future price of jet fuel purchases. This reduces an airlines

exposure to fluctuating fuel prices, depending of the percentage of jet fuel hedged. This

would usually be done through buying jet fuel ahead of time but unfortunately due to the

lack of a liquid market for jet fuel futures, airlines are left unable to buy fuel at a fair price

ahead of time and so hedging must instead be done via futures on other commodities. The

rationale is that if the prices of jet fuel and another commodity with a liquid futures

market tend to move up and down together, then buying futures on the other commodity

will allow the hedger to profit if prices jointly increase and then use this profit to offset

the corresponding increase in jet fuel prices. The practice of hedging using futures on a

different underlying asset is known as a cross-hedge and in the aviation industry is

generally accomplished through buying futures on crude oil, gasoil and home heating oil

due to the similar price characteristics they share with jet fuel. This does not mean that

the prices of these commodities are the same or even similar, rather their prices are highly

correlated and tend to move upwards and downwards together.

The proposed dissertation is influenced by the earlier work of (Adams & Gerner, 2012)

who apply least squares regression and error correction techniques in order to evaluate the

cross hedging performance of Brent crude oil ,West Texas Intermediary crude, NYMEX

heating oil and low sulphur gasoil for hedging spot price exposure to Gulf54 grade jet

fuel. The research is concerned with which commodity of Brent, WTI, gasoil and heating

oil forms the most effective cross-hedge with jet fuel while being eligible to qualify for

hedge accounting status under current regulations. Three models are utilised for testing

hedge effectiveness are a least squares regression model, an error correction model and an

error correction model with GARCH error terms. The most effective cross-hedge is the

one that leads to the lowest annualised variance in a portfolio containing 150,000 gallons

of Gulf54 jet fuel and a model estimated quantity of the cross-hedging product.

3

Jet Fuel Hedging

Jet fuel hedging is undertaken by a large number of airlines annually including Ryanair in

Europe and Southwest Airlines in the United States. Jet fuel is a volatile commodity and

from the early 2000’s the spot price of Gulf54 grade jet fuel rose from $0.53 per gallon to

over $4 per gallon at its peak in 2008, an increase of 647%. The price has since fallen

64% to $1.42 per gallon. Jet fuel accounts for the second largest expenditure for airlines

and since its price can drift substantially over time it’s found by (Carter, et al., 2006) that

if airlines can better manage the cost of fuel then they can more accurately estimate

budgetary costs and forecast future income. Fuel hedging also has positive benefits for the

overall value of the airline. Analysing US airlines over an eleven year period (Carter, et

al., 2006) find that participation in fuel hedging strategies is associated with increases in

airline value of between 5% and 10% while (Cobbs & Wolf, 2004) also determine that

using derivatives to hedge fuel costs creates a competitive advantage for the hedged

airline.

There are a number of strategies available to airlines when proposing hedging solutions to

the cost of jet fuel and (Cobbs & Wolf, 2004) suggest a strategy which is dynamically

managed throughout the life of the hedge achieves the greatest results and note that many

airlines prefer the use of over-the-counter derivatives such as collar structures and swaps

due to their customisability. Using these types of instruments airlines attempt to lock in

prices when they feel jet fuel prices are at a low point and cap prices when they feel they

are at a high point. While the use of these instruments represent a complex hedging

strategy (Carter, et al., 2004) note that their use has been quite successful for Southwest

Airlines. Not every airline will have the expertise to manage a derivative portfolio in

order to hedge fuel costs and so for other businesses hedging through the purchase of

commodity futures may be more appropriate.

Futures contracts allow one to enter into an agreement to buy a standardised quantity of

some product (say 1,000 gallons of Brent Crude Oil) for a certain price at a certain time in

the future. Unlike a Call Option which gives the buyer the right but not the obligation to

take delivery of the product, a futures contract is legally binding. As a result if an airline

enters into a futures contract to buy jet fuel at this time next year and the subsequent price

is below that which was agreed in the contract then the airline still has to pay the higher

price. From this perspective (Morrell & Swan, 2006) note that airlines hedge in order to

4

stabilize fuel prices, rather than speculate on whether the price of jet fuel will increase or

decrease in the future. A hedge is simply taking a position which minimises the price

variance of the asset being hedged. For example a $100 asset which is perfectly hedged

would never change in value from $100 regardless of market events. It’s also worth

noting that most futures are not settled with physical delivery of the underlying assets and

rather are settled for cash at maturity.

SFAS 133

Statements of Financial Accounting Standards 133 or SFAS 133 are an accounting

standard relating to ‘Accounting for Derivative Instruments and Hedging Activities’.

SFAS 133 was originally implemented as (FASB, 1998) which was introduced in order to

deal with some of the shortcomings of its predecessor SFAS 80. During the lifespan of a

derivatives hedge the value each derivative may deviate largely from its’ initial cost and

as a result the traditional accounting methods that required instruments to be booked and

carried at historical cost were not sufficient to reflect the true value of these derivative

assets whose prices changed daily. From this the first major doctrine of SFAS 133 is that

all derivative instruments are marked-to-market, or represented at their fair value. SFAS

133 also requires businesses to match gains in a derivative instrument with losses in a

hedged asset which has the effect of preventing companies from booking gains in either

the hedged item or derivative while failing to report losses on the other side of the hedge

until quarter close.

In order to qualify for hedge accounting under SFAS 133 it’s necessary for businesses to

demonstrate that each hedge is liable to be highly effective in reducing the risk exposure

of the underlying portfolio. It is noteworthy that (FASB, 1998) does not specify any one

measure of hedge effectiveness to be used in order to qualify for hedge accounting rules

and that the appropriateness of any assessment of hedge effectiveness can depend on the

nature of the risk being hedged. Once the measure of hedge effectiveness has been chosen

by the hedging party, (FASB, 1998) states that if the hedge fails this effectiveness test at

any time then the hedge ceases to qualify for hedge accounting rules. The (FASC, 2008)

note that the advantages of hedge accounting outweigh the disadvantages of fair value

accounting for financial instruments and there are a number of reasons why companies

want their hedge portfolios to qualify for hedge accounting rules. The principal advantage

is that it recognises the earnings effects of the hedging instrument and the hedged item in

5

the same financial period and also recognises their earnings effects in proportion to each

other which results in lower earnings volatility for companies. The lower earnings

volatility is in part due to the fact that when operating under hedge accounting rules

earnings and losses on hedged assets are deferred and recorded as offsetting gains or

losses in the value of the hedging instruments whereas outside these standards gains and

losses must be recorded individually and immediately (FASC, 2008).

In the absence of a specific recommendation much of the accounting profession has

adopted the 80-125 dollar offset ratio standard as a measure of hedge effectiveness. Under

current guidelines if one demonstrates that the R-Squared value obtained from regressing

price changes in the hedged asset on price changes in the hedging instrument is greater

than 0.8 then the hedge is deemed highly effective and will qualify for hedge accounting.

Hedge effectiveness is generally measured by the beta coefficient of a least squares

regression and must demonstrate that its value is greater than 0.8 at all times during the

life of the hedge in order to qualify for hedge accounting rules.

This method is criticised by (Charnes, et al., 2003) as during periods of low volatility the

R-Square value may fall below 0.8 and disqualify companies from hedge accounting and

its associated benefits. Its suggested by (Juhl, et al., 2012) that the time frame for back-

testing price changes should match the hedge horizon and so for each potential cross

hedge the back-testing period will be subject to the availability of futures on each

commodity. As of July 2015 the (CMEGroup, 2015) lists futures contracts on Brent and

WTI until December 2022, gasoil until December 2021 and heating oil until January

2019. It’s empirically shown by (Juhl, et al., 2012) that regressing price changes

generates an R-Squared value that converges towards one as the time horizon is extended.

The findings suggest that using monthly as opposed to weekly price changes enhances the

ability of the underlying commodities to qualify for hedge accounting as does back-

testing over a longer time period. As a result commodities with the farthest extending

futures markets (Brent and WTI) should have an advantage over gasoil and heating oil in

qualifying for hedge accounting.

Brent WTI Gas Heat

Hedge Horizon Dec-22 Dec-22 Dec-21 Jan-19

Back-test Horizon (years)

6.5 6.5 5.5 3.5

Table 1 Commodity Hedge Horizons

6

(Juhl, et al., 2012) determine that if the commodity time series are co-integrated and that

price data is available for an adequate sample period then the hedger can be confident of

meeting hedge accounting standards and that with regards to hedge accounting it doesn’t

matter whether a least squares regression model or an error correction model are used to

determine hedge effectiveness as both will yield an R-Square that approaches one as the

hedge horizon is increased. In another study on optimal hedge ratio for cross-hedging jet

fuel (Adams & Gerner, 2012) perform hedge adjustments using a weekly horizon which

they note reduces commodity price risk without having to overspend on transaction fees

and is in line with other studies1. These studies do not account for the impact of hedge

accounting and while operating on a weekly horizon offers the opportunity to adjust the

hedge on a regular basis it may not display eligibility for hedge accounting under (FASB,

1998).

Starting with a weekly time horizon if the R-Square value lies below the 0.80 threshold

then the time horizon for the hedging product will be extended to monthly and re-

evaluated to see if the hedge meets SFAS accounting standards. The time horizon may

subsequently be extended up to a maximum of three months as each quarter is the

minimum time frame for which hedge effectiveness must be reported under FAS 133

guidelines. The time horizon for which each commodity qualifies for hedge accounting

(i.e. weekly, monthly or quarterly) will be the time frame carried forward for optimal

hedge ratio analysis. Due to the varying availability of futures contracts on Brent, WTI,

Gasoil and Home Heating oil and how this applies to (FASC, 2008), it will be assumed

that the hedge horizon for each commodity will be maximised in order to run the longest

possible back-test for each commodity. Thus the commodities Brent and WTI which have

the farthest extending futures will also have the longest back-test period.

1 (Clark, et al., 2003) (Coffey, et al., 2000)

7

Preliminary Considerations

Hedge Ratio & Hedging Performance

The hedge ratio is the proportion of the size of the position taken in futures contracts

compared to the size of the exposure. (Hull, 2015) notes that because jet fuel futures are

not actively traded airlines must hedge their exposure to jet fuel using futures on other

commodities in what is known as a cross-hedge. In a regular futures hedge when the asset

underlying the futures contract is the same as the asset being hedged the hedge ratio

would naturally be 1.0. Thus to hedge the cost of 10,000 barrels of crude oil the hedger

would have to buy 10 futures contracts, which corresponds to that exact amount. The goal

of hedging is to minimise the price variance of the hedged position. When the asset

underlying the futures contracts is not the same as the asset being hedged, their prices are

unlikely to be 100% correlated and so applying a hedge ratio of 1.0 may not be the best

solution.

Finding the hedge ratio which produces the minimum variance in the cross-hedge

portfolio is clearly dependent on the relationship between the price of the asset underlying

the futures contracts and the price of the asset being hedged. Studies such as (Ederington,

1979) were among the earliest to utilise the technique of regressing cash and futures

prices and use the resulting x-coefficient to determine the optimal cross-hedge ratio. This

has become the conventional approach in determining optimum hedge ratio though it has

been improved upon a number of times. In (Nelson & Plosser, 1982) it’s demonstrated

that non-stationary data (i.e. cash and futures price levels) can lead to inaccurate results in

regression testing. To account for these findings (Benninga, et al., 1984) introduce the

usage log returns in regression testing as they are trend stationary and this technique is

still widely used today. Through the regression method optimum hedge ratio is acquired

by finding the x-coefficient of an ordinary least squares (OLS) regression. (Hull, 2015)

describes the formula for optimal hedge ratio ℎ∗ as

ℎ∗ = 𝜌𝜎𝑆

𝜎𝐹

Equation 1 Optimal Hedge Ratio

In Equation 1 above 𝜎𝑆 corresponds to the standard deviation of the change in spot price,

𝜎𝐹 represents the standard deviation of the change in futures price and 𝜌 is the coefficient

of correlation between the spot and the futures prices. It’s maintained within the SFAS

133 regulations that the back-tested for a period for testing hedge effectiveness should be

8

equal to the life of the hedge, thus if the hedge will last for five years, then the five years’

leading up to June 2015 will be used for back-testing. The optimal number of contacts to

be bought for hedging may be determined by Equation 2 below. In Equation 2 the 𝑁∗

variable represents the optimal number of futures contracts required for hedging, while

𝑄𝐴 is the size of the position being hedged and 𝑄𝐹 corresponds to the size of one futures

contract (Hull, 2015).

𝑁∗ = ℎ∗𝑄𝐴

𝑄𝐹 Equation 2 Optimal Number of Contracts

In another jet fuel hedging study (Adams & Gerner, 2012) research the hedging

performance of a number of commodities by analysing the annualised variance of a

portfolio containing jet fuel and a model calculated amount of the cross-hedging product.

The best performing hedge was determined by the lowest annualised variance produced

by the total profit-and-loss (P&L) series for each portfolio and this methodology is

followed again in this study. The total P&L series is a product of the P&L on each leg of

the cross hedge and is shown as Equation 3.

𝑃&𝐿𝑇𝑜𝑡𝑎𝑙 = 𝑃&𝐿𝑆𝑝𝑜𝑡 + 𝑃&𝐿𝐹𝑢𝑡𝑢𝑟𝑒𝑠 Equation 3 P&L Series

There will be a some deviations from the methodology of (Adams & Gerner, 2012)

whereby instead of using a $1,000,000 investment in jet fuel, the portfolio will instead

contain 150,000 gallons of Gulf 54 grade jet fuel as this was roughly the amount of jet

fuel consumed by Southwest Airline per month in 2014 (Transtats, 2015). Also the total

P&L will be calculated as a monetary amount rather than as a percentage change in

prices. The profit and loss on each leg of the hedge is shown in Equation 4 and Equation 5.

The P&L is calculated on either a weekly, monthly or quarterly horizon depending on the

results from the SFAS 133 analysis as this will determine the hedge horizon that each

cross-hedge commodity must operate on in order to be in line with hedge accounting

regulations. In the Equation 4 and Equation 5 below ℎ∗ represents the optimal number of

futures contracts needed to hedge the jet fuel exposure. The variables 𝐽𝑡 and 𝐹𝑡

correspond to the spot prices of jet fuel and the cross-hedging product at the time the

hedge is placed. The variables 𝐽𝑡+𝑇 and 𝐹𝑡+𝑇 correspond to the time horizon used for

hedging and are varied between 1, 3, 6, 9and 12 months for each hedge.

𝑃&𝐿𝑆𝑝𝑜𝑡 = 150,000 ∗ (𝐽𝑡

− 𝐽𝑡+𝑇) Equation 4 Profit and Loss Spot

9

𝑃&𝐿𝐹𝑢𝑡𝑢𝑟𝑒𝑠 = (𝐹𝑡+𝑇

− 𝐹𝑡) ∗ℎ∗ ∗ 150,000

𝑄𝐹

Equation 5 Profit and Loss Futures

The total returns series is a sum of Equation 4 and Equation 5 for each time period during

the back-testing window. The best performing cross-hedge will be the one which

produces the lowest annualised variance as measured by the standard deviation of the

total profit and loss series multiplied by the square root of number of periods per year.

For example the annualised variance equation for gasoil being hedged on a monthly

horizon is given in Equation 6, and the annualised variance will be calculated for each of

the three models across all time horizons.

𝐴𝑛𝑛 𝑉𝑎𝑟 = 𝑠𝑡𝑑(𝑇𝑜𝑡𝑎𝑙 𝑃&𝐿𝐺𝑎𝑠𝑜𝑖𝑙) ∗ √12 Equation 6 Annualised Variance Gasoil

The methodology for determining the optimal hedge ratio also differs from that of

(Adams & Gerner, 2012) in that the price levels are transformed to first differences

instead of log returns before being input into the OLS, ECM and ECM-GARCH models.

The reason for this approach is due to the way the P&L is calculated. Determining

optimal hedge ratio using log returns would yield erroneous P&L results as using log

returns does not capture the magnitude of the changes in monetary value for each

commodity, i.e. a positive 1% return of Gasoil does not perfectly hedge a 1% loss on jet

fuel because their prices are vastly different and this must be captured in the P&L

calculation. The final P&L methodology change from (Adams & Gerner, 2012) in how

the dynamic cross hedge ratio is calculated. In the analysis instead of calculating a new

optimal cross hedge ratio for each year based on all the previously available data, the 𝛽

value is calculated for each hedge placed during back-testing based on the most recent 5,

10 and 15 years of data to contrast the differences (if any) resulting from including more

years of data in determining optimal hedge ratio.

Hypothesis Testing & Statistical Significance

The methodology utilises a number of hypotheses tests throughout. Hypotheses are

investigated by specifying a null hypothesis and investigating whether this condition can

be accepted or rejected based on the evidence presented. In hypothesis testing the null

hypothesis is presumed to be true, until the data presented provides sufficient evidence to

show that it is not. There are two outcomes to hypothesis testing, rejecting the null and

failing to reject the null. The terminology here is important, as the null can never truly be

10

accepted, only rejected or not rejected based on the sample provided. Think in terms of a

murder trial where the null hypothesis is that the accused is innocent. There are two

outcomes, the first is that the court may be provided with sufficient evidence to reject this

hypothesis, i.e. the accused is guilty. On the other hand the trial may be provided be

insufficient evidence to reject this hypothesis. This doesn’t mean that the null hypothesis

is true and that the accused is innocent, just that there is not sufficient evidence to

disprove the null and the trial has found them not guilty i.e. it has failed to reject the null.

When carrying out a hypothesis test one must specify a significance level which also

represents the ‘size’ of the test. The test ‘size’ is the probability of falsely rejecting the

null i.e. the probability of a type I error (Alexander, 2008). A type I error is the false

rejection of a true null hypothesis, i.e. detecting an affect that is not present. There is also

a type II error which is failing to reject a false null hypothesis, i.e. failing to detect and

affect that is present. Thought of another way a type I error is finding an innocent person

guilty while a type II error is finding a guilty person innocent, and when testing a type I

error is more serious. Increasing the significance level reduces the size of the test but also

increases the probability of a type II error, thus decreasing its’ power which is a tests

ability to correctly reject the null hypothesis (Alexander, 2008).

The critical values for each hypothesis test represent the upper and lower percentiles of

the sample. Thus if the significance level is 5%, the critical values represent the points

between which 95% of the data lies. As a result choosing a lower significance level (of

say 90%) increases the tests chance of rejecting the null hypothesis but suffers from

losing statistical power making the results less convincing (Banerjee, et al., 1993). For the

null hypothesis to be rejected the test statistic must fall within the critical region (be more

extreme than the critical values) and produce a pValue which is lower than the

significance level. For a one sided hypothesis test such as the (Dickey & Fuller, 1979) test

for a unit root the test statistic must fall below the critical value.

11

Regression Model

A theoretical framework for determining the optimal futures position in a cross hedge is

described in (Anderson & Danthine, 1981) who specify that the proportion of output that

should be hedged in each contract, i.e. the cross-hedge ratio, is determined by the slope

coefficient output from regressing cash prices on futures prices. For most practical

purposes (Conroy, 2003) notes that one can simply use the spot prices for the cross-hedge

commodities in determining optimal hedge ratio and so that is the method pursued in this

paper. For practical purposes however the cross-hedge product spot prices will still be

referred to as futures prices for distinction from the jet fuel spot prices. The price levels

for each commodity represent a non-stationary array of data. The research of (Nelson &

Plosser, 1982) demonstrated that non-stationary data can lead to inaccurate results in

regression testing, and so to account for these findings (Benninga, et al., 1983) introduce

the usage log returns in place of cash and futures prices and this method is found to lead

to more accurate results when using regression methods for commodity hedging (Myers

& Thompson, 1989).

The use of regression testing also provides a measure of explanatory power between the

dependent and independent variables. The R-Squared value indicates the percentage of

variation in jet fuel returns which can be explained by the variation in the returns of the

cross-hedging products. While regression analysis has the advantage of being straight

forward to implement (Cecchetti, et al., 1988) note that this process for estimating

optimal hedge ratio suffers from major drawbacks. This research cites that no adjustment

can be made for the fact that the joint distribution of the time series varies over time and

that this important characteristic cannot be captured via the OLS approach. Other issues

are noted by (Kroner & Sultan, 1993) who show that if the time series are co-integrated

that the regression is misspecified as it involves over differencing the data and losing

information regarding the long run relationship between the spot and futures prices. This

can lead to a downward bias in hedge ratio estimation and as a result under-hedging.

Unit Root Testing

In time series analysis a trend-stationary series is one whose error term follows a

stationary process while an integrated time series is one whose error term follows a

random walk (DeJong, et al., 1992). Tests for stationarity are carried out on each of the

12

series as (Granger & Newbold, 1974) show that two integrated time series which are

completely unrelated can demonstrate an apparently significant relationship when one is

regressed on the other. The findings of (Granger & Newbold, 1974) led econometric

analysis to become interested in transformations to induce stationarity. Stationary series

have a number of favourable characteristics such as a finite variance and finite time

between crossings of the series mean, as well as this stationary series have the important

property that certain functions of the sample values converge to constants as the number

of sample values increases (Banerjee, et al., 1993). This means that for stationary time

series the mean and variance of the sample being tested converge towards the true mean

and variance of the process as the sample size is increased.

Shown below in Table 2 are the hypotheses for a unit root test where the variables display

either a stationary I(0) or a non-stationary I(1) trend. Its’ noted by (Alexander, 2008) that

if the test statistic falls outside the critical region and the null hypothesis is not rejected

that another unit root test should be performed of the first differenced time series to

analyse its order of integration. Differencing involves calculating the differences between

consecutive observations in a time series. The first difference of a time series 𝑥 at period 𝑡

is 𝑥𝑡 − 𝑥𝑡−1. If the price levels for any of the commodities analysed are found to be non-

stationary and 𝑦𝑡, the first differenced time series of that commodity, is subsequently

found to be stationary then the time series being analysed is termed to be integrated of the

order I(1). If the sample does not achieve stationarity until its second differences (the first

difference of 𝑦𝑡) then the sample is said to be integrated of the order I(2). Thus unit root

testing is not only useful in identifying stationary trends in data but also helps to identify

the order of integration of each time series.

Levels 𝐻0: 𝑋𝑡 ~ 𝐼(1) 𝐻1: 𝑋𝑡 ~ 𝐼(0)

First Differences 𝐻0: ∆𝑋𝑡 ~ 𝐼(1) 𝐻1: ∆𝑋𝑡 ~ 𝐼(0)

Table 2 Unit Root Hypotheses

As part of the methodology the Augmented Dickey-Fuller (ADF) test of (Dickey &

Fuller, 1979) will be carried out on the data to test each time series for stationarity. An

ADF test is a unit root test which returns a rejection decision based on the detection of a

unit root in the time series. The null hypothesis is that a unit root exists and the time

series is integrated, thus a rejection of the null hypothesis indicates that the time series is

trend-stationary. It is noted by (Alexander, 2008) that the ADF test is also the least

13

powerful unit root test. This is likely because the impact of type I errors have on the

results, i.e. at a 5% significance level the ADF test will incorrectly return a decision of

stationarity (where none is present) approximately once every twenty times. To account

for this the KPSS test of (Kwiatkowski, et al., 1992) will also be carried out on each time

series. The KPSS test is a stationarity test in which the null hypothesis is that the time

series is trend-stationary and it is expected the KPSS results should be consistent with the

ADF tests.

Regression Analysis

Regression testing is a process which involves evaluating the linear relationship between

variables. Regression analysis typically indicates how the value of a dependent variable

changes as a result of changes in value of some independent variable. Using this

statistical method we wish to find out how a change in the value of 𝑋 affects the value

of 𝑌, or looked at in a slightly different way, can we use the observed change in the value

of 𝑋 to predict the resulting change in the value of 𝑌. The simplest example of a linear

relationship is given by the equation of a straight line in Equation 7.

𝑌𝑡 = 𝛼 + 𝛽𝑋𝑡 + 휀𝑡 Equation 7 Linear Model

In Equation 7 above 𝑌 represents the dependent variable (jet fuel spot) and 𝑋 represents

the independent variable (commodity futures) while the intercept and slope of the

regressions line of best fit between the two are denoted by 𝛼 and 𝛽 respectively. The x-

coefficient or 𝛽 value also corresponds to the optimal hedge ratio estimated by the linear

regression. Figure 1 illustrates a regression between the first differenced series for Brent

crude oil and Gulf54 grade jet fuel. From Figure 1 it’s clear that not all of the data points

will form a perfectly straight line and as a result an error term is included in Equation 7

Linear Model which defines the distance between each data point and the regression line of

best fit. If the correlation between 𝑋 and 𝑌 is low then one would observe a high variance

in the errors which are represented in Equation 7 by 휀𝑡 while a high correlation between

regression variables would yield a low variance in 휀𝑡 (Alexander, 2008).

14

Figure 1 Jet-Brent OLS Regression Plot

Ordinary least squares (OLS) is a technique for estimating the unknown parameters of a

linear regression by minimising the regression residuals. The residuals represent the

difference between the observed value and the estimated value of the quantity of interest.

In the context of cross hedging where one is attempting to understand how changes in the

price of futures contracts can predict changes in the spot price of jet fuel, the OLS

regression will attempt to fit a linear model to the data such that the errors between the

predicted change in jet fuel spot prices and actual observed changes are minimised. The

research of (Engle & Granger, 1987) among others notes that the residual series made up of the

error terms may retain important information about the relationship between the variables.

Characteristics such as its speed of adjustment towards the line of best fit and whether the error

terms are autocorrelated remain unaccounted for in the linear regression model (Kroner & Sultan,

1993).

While regression analysis is unable to capture several time series characteristics important

in determining optimum hedge ratio the technique has been shown in some scenarios to

outperform other models such as the error correction model that captures long a short run

hedge dynamics. Using futures on the Nordic power exchange (Byström, 2003)

determines that an OLS hedge outperforms more elaborate moving average and

generalized autoregressive conditional heteroscedasticity (GARCH) hedging models. In

further support of OLS hedging methods (Lien, et al., 2002) find the OLS technique

outperforms a (vector) VGARCH model when hedging a sample of currency, commodity

15

and stock index futures. This may be related to the findings of (Stock, 1987) that if time

series are co-integrated and the 𝛼′𝑦𝑡 combination of its co-integrating vector and

logarithm vector is I(0) then a simple regression is likely to yield very consistent results

of the co-integrating vector (Baille & Bollerslev, 1994). In contrast with these findings

(Ghosh, 1993) shows that an error correction model (ECM) presents a significant

improvement over the OLS regression approach when determining optimum hedge ratios

using stock index futures as this method incorporates non-stationarity, the long run

equilibrium relationship and short-run dynamics of each time series. Similarly (Chou, et

al., 1997) find an ECM outperforms the traditional regression approach when Japans

Nikkei Stock Average index futures.

Residual Series

There are some characteristics of the residual time series resulting from the OLS

regression approach which can provide important information surrounding the suitability

of each model to fit the data. Autocorrelation refers to the cross-correlation of a signal

with itself at different points in time while heteroscedasticity refers to the mean variance

in the residual series changing over time (Engle, 1982). The influence of

heteroscedasticity and autocorrelation in the error structure (residuals) of a regression

may lead to spurious results if not accounted for in the analysis (Granger & Newbold,

1974).

In large sample sizes (Alexander, 2008) notes that the presence of autocorrelation and

heteroscedasticity will not have a damaging impact on the outcome of an OLS regression

but that in a small sample size where autocorrelation and heteroscedasticity are detected a

generalised least squares approach should be used instead of the ordinary least squares

method. This has consequences surrounding the hedge horizon used for testing as if hedge

horizon is increased past a monthly basis in order to meet hedge accounting standards, it

will greatly reduce the amount of data available for testing which could potentially

increase the impact that autocorrelation and heteroscedasticity can have on the results.

Autocorrelation

Autocorrelation is the linear dependence of a variable with itself at two different points in

time, or looked at in another way an autocorrelated time series is one which exhibits

similarity with a lagged version of itself. A basic assumption underlying the OLS

16

regression is that the error terms are independent and once this assumption is satisfied the

OLS procedure is valid whether or not the time series themselves are serially correlated

(Durbin & Watson, 1950). From this we can deduce that it is not important to test the

individual commodity time series for autocorrelation but instead need to analyse the

residual series produced by each OLS regression. The presence of autocorrelation is a

problem in the least squares approach because it indicates that the error terms are not

independent and this may lead to the variance of the least square estimators in the

regressions to be too large (Anderson, 1954). The presence of autocorrelation may require

modification to the usual methods of estimation and prediction and (Cochrane & Orcutt,

1949) note that when estimates of autoregressive properties are based on autocorrelated

residuals there is a large bias towards randomness. This implies that the presence of

autocorrelation in the residual series may substantially impact the results derived from the

ECM and ECM-GARCH models which incorporate residual information, or rather it can

diminish the advantage the ECM and ECM GARCH models have over the OLS

regression because the presence of autocorrelation muddles the useful information

contained in the residuals.

Heteroscedasticity

Heteroscedasticity refers to sub-populations in a collection of random variables having

different variability’s from others, which translates to the time series demonstrating

different variances over time. In a residual series this translates to serially uncorrelated

residual errors displaying a constant unconditional variance but a non-constant

conditional variance (Engle, 1982). Before the autoregressive conditional

heteroscedasticity (ARCH) model proposed by (Engle, 1982) most econometric models

assumed constant variance. The defining feature of an autoregressive conditional

heteroscedastic (ARCH) process is the specification of a non-constant variance which is

conditional on past variance levels. Under ARCH the conditional variance of the current

error term is dependent on its’ realised past values and (Engle, 1982) notes this model has

the advantage of reflecting clustering between large and small error terms (i.e. volatility

clustering).Thus in an ARCH process periods of low volatility tend to be followed by

periods of low volatility while periods of high volatility tend to be followed by further

periods of high volatility.

17

Error Correction Model

The error correction model (ECM) represents an extension of the OLS regression and

operates on the premise that important information that predicts the future evolution of

the time series under analysis is retained in the residual time series. As a result the ECM

incorporates a lagged version of the residual errors in order to capture elements of the

short term relationship between the variables. The ECM also accounts for the long run

equilibrium relationship between the time series through considering the presence of a co-

integration relationship between the variables. The research of (Engle & Granger, 1987)

shows that if the linear combination of two non-stationary variables forms a stationary

time series, then the equilibrium condition and adjustment process to equilibrium can be

represented by an error correction model (Ghosh, 1993). The incorporation of elements

that capture some of the short and long run dynamics of the time series accounts for a

number of the disadvantages of the OLS regression noted by (Kroner & Sultan, 1993).

Co-Integration

Integrated time series are non-stationary and tend to drift randomly over time, yet some

pairs of integrated series may be defined by some long-run relationship to which the

system converges to over time (Banerjee, et al., 1993). The research of (Engle & Granger,

1987) makes note that economic time series can wander substantially and yet some series

are expected to move so that they do not drift too far apart. If two time series are co-

integrated it will be observed that over time they will tend not to drift too far apart and

that the distance between them (i.e. their residual series) will follow a stationary trend that

is normally distributed around some mean value. The presence of co-integration suggests

a long run memory between the co-integrated time series. While the series may diverge

substantially in the short run and the effects of shocks may only vanish over long time

horizons, pairs of co-integrated series will always display a tendency over time to drift

back towards their equilibrium relationship (Baille & Bollerslev, 1994). In this respect the

drift between co-integrated series must be stochastically bounded and, at some point,

diminishing over time (Banerjee, et al., 1993). In terms of the time series which represent

jet fuel and each of the cross-hedge commodity prices, carrying out tests for co-

integration will indicate whether or not their price series are linked in the long run and

forms the basis of fitting an error correction model to the data (Stock & Watson, 1988).

18

“The components of the vector 𝑥𝑡 are said to co-integrated of order 𝑑, 𝑏, denoted

𝑥𝑡 ~ 𝐶𝐼(𝑑, 𝑏), if (i) all components of 𝑥𝑡 are I(d); (ii) there exists a vector α (≠0) so that

𝑧𝑡 = 𝛼′𝑥𝑡 ~ 𝐼(𝑑 − 𝑏), b > 0. The vector α is called the co-integrating vector”

To make sense of the co-integration definition above offered by (Engle & Granger, 1987)

consider the components of the vector 𝑥𝑡 are two time series 𝑗𝑡 and 𝑓𝑡 which represent the

spot price of jet fuel and the futures price of the cross-hedging commodity. Assume the

unit root tests carried out determine that 𝑗𝑡 and 𝑓𝑡 are both I(1) integrated variables which

fulfils the first condition in the above definition. It is noted by (Engle & Granger, 1987)

that for most observations 𝛼′𝑥𝑡 will not be in equilibrium and that there exists a univariate

quantity outlined above as 𝑧𝑡 called the equilibrium error. If there exists some vector α

such that the residual error series 𝑧𝑡 formed by a linear combination of α with 𝑥𝑡 is I(0),

or trend-stationary, then the second condition is fulfilled and time series 𝑗𝑡 and 𝑓𝑡 are said

to be co-integrated.

In other words co-integration implies that deviations from equilibrium are stationary with

finite variance even though the series themselves may be non-stationary with infinite

variance. Thus if 𝑧𝑡 represents the error or distance from 𝛼′𝑥𝑡 to the long run equilibrium,

it can be used to independently verify the existence of co-integration between time series

𝑗𝑡 and 𝑓𝑡 by testing whether the residuals derived from a regressing 𝑗𝑡 on 𝑓𝑡 display

stationarity.

It’s shown by (Ghosh, 1993) that smaller than optimal futures positions are taken when

the effect of co-integration is omitted from hedging models. A number of fuel hedging

strategies are described by (Cobbs & Wolf, 2004) however they fail to acknowledge a co-

integration relationship between the jet fuel and any of the cross-hedging products as

being significant though its importance is recognised in the research by (Adams &

Gerner, 2012) on which this study is based. It’s inclusion in the analysis is deemed

essential as “co-integration is the only true indispensable component when comparing ex-

post performance of various hedge strategies” (Da-Hsiang, 1996). There are a number of

tests for co-integration which may be pursued in this study, however the simple two-step

estimation of (Engle & Granger, 1987) is followed for a number of reasons. The two-step

estimation has a very practical advantage of being the most straight-forward of co-

integration tests and is easily implemented in MATLAB. Alternative cointegration testing

methods are available such as the vector auto-regression (VAR) method of (Johansen,

19

1991) which allows for testing of co-integration rank and seasonal dummies among the

variables. However due to each potential co-integration relationship containing only a

pair of variables, the more complex approach associated with the VAR method of

(Johansen, 1991) is rejected in favour of the more straight forward two-step approach of

(Engle & Granger, 1987). The effect of co-integration when hedging jet fuel futures is

studied by (Adams & Gerner, 2012) who’s research found that an error correction model

(ECM) outperforms an OLS regression when cross-hedging jet fuel with a number of

crude oil based commodities.

Error Correction Analysis

Error correction terms may be used as a way of capturing adjustments in a dependent

variable which depended not on the corresponding level of some explanatory variable but

on the extent to which the explanatory variable deviated from its equilibrium relationship

with the dependent variable (Banerjee, et al., 1993). In other words, assuming that some

long run equilibrium relationship is present between the time series (which is why co-

integration is a prerequisite), an error correction model (ECM) may be used to estimate

adjustments in jet fuel prices based on how its time series has deviated from its’

equilibrium relationship with the cross-hedging product. It’s noted by (Engle & Granger,

1987) that for a two variable system a classic error correction model would relate the

changes in one variable to past equilibrium errors as well as past changes in both

variables. (Kroner & Sultan, 1993) note that regression models can obscure the long run

relationship between spot and futures prices while (Adams & Gerner, 2012) note that the

ECM framework accounts for the autoregressive structure of spot and forward price

changes and thus incorporates the long run relationship between both markets. It can be

viewed such that if an OLS regression estimates the linear relationship between the first

differences for jet fuel and the hedging commodity, then the error correction model estimates the

dynamic structure between the first differenced series by incorporating short and long run

information about their co-integrated relationship (Alexander, 2008). The model operates on the

idea that the short term deviations from the long run equilibrium relationship will be subsequently

corrected by the time series on its own.

The error correction model employed in the methodology is the same one employed by

(Adams & Gerner, 2012) with the substitution of first differences for log returns and takes

the form

20

∆𝑓𝑑𝑆𝑡 = 𝑐 + 𝛽∆𝑓𝑑𝐹𝑡,𝑇 + ∑ 𝛾𝑘∆𝑓𝑑𝐹𝑡−𝑘,𝐾

𝐾

𝑘=1

+ ∑ 𝛿𝑙∆𝑓𝑑𝑆𝑡−𝑙

𝐿

𝑙=1

+ 𝜆𝑒𝑡−1 + 휀𝑡

Equation 8 Error Correction

Model

Where ∆𝑓𝑑𝑆𝑡 and ∆𝑓𝑑𝐹𝑡,𝑇 represent the changes in the first differenced price series, 𝑐 represents

the intercept and 𝛾𝑘 and 𝛿𝑙 signify the short run dynamics coming from the lagged changes in the

spot price (hence 𝐹𝑡−𝑘,𝐾). The 𝜆 term represents the adjustment parameter which captures the

speed at which each time series reacts to deviations from the long run equilibrium relationship

and 𝑒𝑡 is the error term, which comes in lagged form, as each time series must first deviate from

the long run relationship before beginning its correction process. The 𝑒𝑡 term is formed by the

residual series from an OLS regression of the differenced series for jet fuel on the differenced

series for the chosen cross-hedge commodity. Finally 휀𝑡 represents the standard error while 𝛽

represents the optimal hedge ratio.

The ECM analysis will be carried out using the same rolling window as the OLS regression and

will convert the residual series produced by each loop of the OLS regression model to lagged

form for use in the ECM, as shown in the MATLAB Dynamic Hedge Ratio section of

Appendix B. Like the OLS model the ECM will be run on either a weekly, monthly or quarterly

hedging horizon based on the SFAS 133 analysis for each commodity. The model itself is based

on data provided by (Adams, 2015). Since it’s noted by (Kroner & Sultan, 1993) that an OLS can

result in downward bias which leads to under hedging we may observe a slightly higher optimal

hedge ratio output from the error correction model when compared to the ordinary least squares

regression model.

The representation theorem of (Granger, 1986) specifies that that when integrated

variables share a co-integration relationship that a vector autoregressive (VAR) model of

first differences will be misspecified as the disequilibrium term is missing from the vector

autoregressive representation. This term is also missing from the more simplified OLS

regression Equation 7 outlined above. It’s noted by (Alexander, 2008) that when lagged

disequilibrium terms are included as explanatory variables that the model becomes well

specified. As shown above in Equation 8 the error correction framework accounts for the

misspecification of OLS regression models and VAR models by including a lagged error

correction term in order to incorporate the previous periods’ equilibrium error (Ghosh,

1993). The model also includes additional information about the lagged series through a

linear combination of the lagged values of the first differenced time series for each

commodity with a term that estimates the short run dynamics.

21

GARCH Extension

The OLS regression has been described by (Engle, 2001) as the “great workhorse of

applied econometrics” however he notes that when attempting to estimate and examine

the size of the errors within a model that the questions are about volatility, for which the

standard tools are the ARCH and GARCH models. Generalised autoregressive

conditional heteroscedasticity (GARCH) is a generalisation of the ARCH process

discussed earlier whereby the variance of the error terms is assumed to follow an

autoregressive moving average (ARMA) process. GARCH models are thus an extension

of the non-constant conditional variance approach of ARCH models whereby the

conditional variance at any one time is based on a weighted sum of its passed values. The

GARCH model of (Bollerslev, 1986) is generally considered superior because it can

account for the time varying variance of the spot and futures prices during the life of the

hedge and can also account for price shocks. While the classic error correction model

incorporates the cointegrated relationship and lagged residuals in order to capture the

short and long run dynamics between the time series, the GARCH extension substitutes

the lagged residual series for GARCH residuals in order to capture the non-constant

conditional variance of the residual time series as well as the short run dynamics.

GARCH Analysis

The error correction model employed by (Adams & Gerner, 2012) also specifies a

GARCH extension to obtain greater accuracy and they state that a univariate GARCH

should be sufficient to model the optimal hedge ratio. In contrast studies such as (Kroner

& Sultan, 1993) and (Baillie & Myers, 1991) use a bivariate GARCH model as they state

that in the case of two I(1) variables being co-integrated so that their linear combination is

I(0) then they should be represented by a bivariate model that includes an error correction

term. For the purpose of simplicity a univariate GARCH approach is taken where the

non-constant conditional variance is estimated using Equation 9. In order to incorporate

GARCH residuals into the model the lagged residual series used in the regular ECM will

be transformed to its GARCH representation using Equation 9 and then analysed in the

same way as the regular ECM.

ℎ𝑡2 = 𝜇 + 𝜃1휀𝑡−1

2 + 𝜃2ℎ𝑡−12 Equation 9 Conditional Variance

22

In a study based on exchange rates (Hansen & Lunde, 2005) find that there is no evidence

to suggest that a GARCH(1,1) model is outperformed by over 330 other ARCH-type

models in its ability to model conditional variance. Dynamic hedging using an error

correction model with a GARCH error structure was carried out by (Kroner & Sultan,

1993) using a GARCH(1,1) model while (Adams & Gerner, 2012) also employ the this

type of model for capturing non-constant condition variance. For these reasons a

GARCH(1,1) will be fitted to the data in order to compute the GARCH residuals. In a

GARCH(1,1) model the conditional variance is based on the most recent observation of

the residuals and the most recent estimate of the variance rate as shown by the 𝑡 − 1

subscript for the variables in Equation 9. The GARCH model will be fitted using the

MATLAB ‘estimate’ function which estimates the GARCH(1,1) model via maximum

likelihood methods. As with the lagged residuals of the ECM the ECM-GARCH will be

based off a new set of OLS residuals generated with every loop of the model. Once the

GARCH model has been fitted using the MATLAB function the residuals will be

transformed using Equation 9. Each residual may be represented as √ℎ𝑡2 and will be

substituted for the lagged error terms in the ECM model.

Basis Risk

Basis risk is described by (Figlewski, 1984) as the varying nature of the difference

between the spot and futures prices and that hedging using futures exposes the position to

this type of risk since the evolution of the futures price over time may not match the

change in value of the cash position. Since this basis may be represented by the residual

series between the spot and futures prices, then the error correction models incorporation

of the lagged error term as well as the adjustment parameter should enable an ECM to

better account for the evolution of basis risk when compared to an OLS regression. It’s

observed by (Figlewski, 1984) that this type of risk increases as the length of the hedging

horizon decreases so it’s likely that if the hedge horizon must be increased in order to

meet hedge accounting standards as per (Juhl, et al., 2012) that this will have the effect of

reducing basis risk for all of the models analysed.

23

Results & Discussion

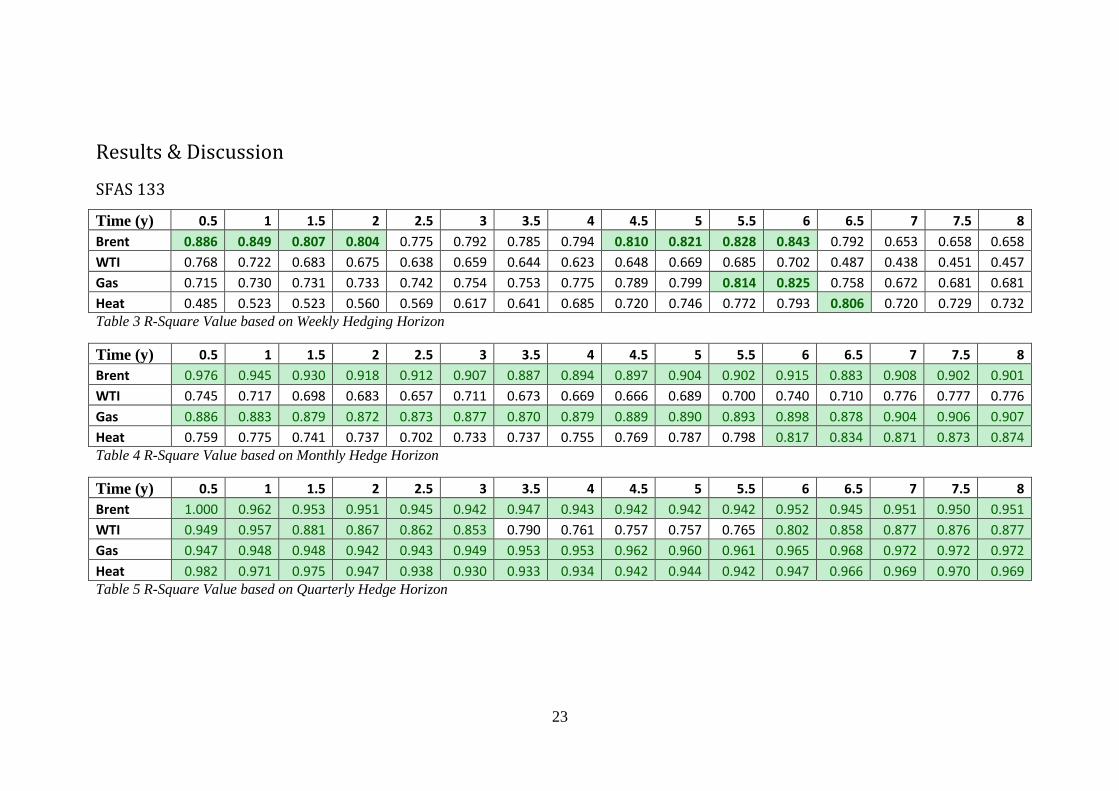

SFAS 133

Time (y) 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8

Brent 0.886 0.849 0.807 0.804 0.775 0.792 0.785 0.794 0.810 0.821 0.828 0.843 0.792 0.653 0.658 0.658

WTI 0.768 0.722 0.683 0.675 0.638 0.659 0.644 0.623 0.648 0.669 0.685 0.702 0.487 0.438 0.451 0.457

Gas 0.715 0.730 0.731 0.733 0.742 0.754 0.753 0.775 0.789 0.799 0.814 0.825 0.758 0.672 0.681 0.681

Heat 0.485 0.523 0.523 0.560 0.569 0.617 0.641 0.685 0.720 0.746 0.772 0.793 0.806 0.720 0.729 0.732 Table 3 R-Square Value based on Weekly Hedging Horizon

Time (y) 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8

Brent 0.976 0.945 0.930 0.918 0.912 0.907 0.887 0.894 0.897 0.904 0.902 0.915 0.883 0.908 0.902 0.901

WTI 0.745 0.717 0.698 0.683 0.657 0.711 0.673 0.669 0.666 0.689 0.700 0.740 0.710 0.776 0.777 0.776

Gas 0.886 0.883 0.879 0.872 0.873 0.877 0.870 0.879 0.889 0.890 0.893 0.898 0.878 0.904 0.906 0.907

Heat 0.759 0.775 0.741 0.737 0.702 0.733 0.737 0.755 0.769 0.787 0.798 0.817 0.834 0.871 0.873 0.874 Table 4 R-Square Value based on Monthly Hedge Horizon

Time (y) 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8

Brent 1.000 0.962 0.953 0.951 0.945 0.942 0.947 0.943 0.942 0.942 0.942 0.952 0.945 0.951 0.950 0.951

WTI 0.949 0.957 0.881 0.867 0.862 0.853 0.790 0.761 0.757 0.757 0.765 0.802 0.858 0.877 0.876 0.877

Gas 0.947 0.948 0.948 0.942 0.943 0.949 0.953 0.953 0.962 0.960 0.961 0.965 0.968 0.972 0.972 0.972

Heat 0.982 0.971 0.975 0.947 0.938 0.930 0.933 0.934 0.942 0.944 0.942 0.947 0.966 0.969 0.970 0.969 Table 5 R-Square Value based on Quarterly Hedge Horizon

24

Table 3, Table 4 and Table 5 on the previous page present the results of simple regression

analysis on the log returns series for jet fuel on the log returns series for each of cross-hedge

commodities. The R-Square values of each regression are presented as these values may be

presented as a means to qualify for hedge accounting status. It is recommended by (FASC,

2008) that the back-testing period for each commodity matches the hedge horizon and so the

times in years across the top of each of the tables correspond to horizons extending

backwards from June 1st 2015. Thus the results presented as 0.5 years correspond to an R-

Square derived from using data from January 1st 2015 to June 1

st 2015, 3 year results

correspond to testing from June 1st 2012 to June 1

st 2015 etc. The threshold for qualifying for

hedge accounting is an R-Square value of 0.8 and in Table 3, Table 4 and Table 5 the R-Square

results which meet this criteria are highlighted in green. Each commodity was analysed on a

hedge horizon ranging from 0.5 to 8 years and on a weekly, monthly and quarterly time

horizon. It’s important to bear in mind that the available hedge horizon for each commodity

varies under SFAS regulations varies due to differences in the availability of futures on each

cross hedge product. The time horizons are shown in Table 1 and as a reminder are 6.5 years

for Brent and WTI, 5.5 years for gasoil and 3.5 years for heating oil. Figure 2 illustrates the

results from the weekly analysis and it’s clear from the results that none of the commodities

can consistently meet (FASB, 1998) hedge accounting standards on a weekly time horizon.

Figure 2 SFAS Analysis Weekly Time Horizon

Figure 2 illustrates the data presented in Error! Reference source not found. and offers a

visual breakdown on the ability of each of the cross-hedge portfolios to achieve hedge

accounting status when used to hedge jet fuel. The R-Square values on the x-axis begin at 0.4

0.400

0.500

0.600

0.700

0.800

0.900

1.000

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8

R-S

qu

are

Hedge Horizon (years)

SFAS Weekly Horizon

Brent WTI Gas Heat SFAS

25

while the commodity data is analysed on a weekly time horizon and for a hedge horizon

stretching from 0.5 to 8 years. The weekly price correlation between the commodities jumps

significantly between year 7 and year 6 (2008 and 2009) and while Brent and West Texas

Intermediate see their weekly price correlations rise overall by 2015, gasoil and heating oil

see their price correlations drop off slightly in recent years. The increase in the returns

correlations across all commodities during the time of the financial crisis is consistent with

the findings of (Silvennoinen & Thorp, 2013) who found that returns correlations between

commodities increased significantly during the financial crisis and is consistent with the

theory that asset returns are more highly correlated in a market downturn. Of the four cross-

hedging products analysed on a weekly basis only Brent and gasoil meet hedge accounting

criteria at any stage during the test period and neither do it on a consistent basis. As a results

none of the cross hedging products will be brought forward for profit and loss testing on a

weekly basis as hedging jet fuel with either Brent, WTI, gasoil or heating oil on this time

horizon can qualify for hedge accounting status.

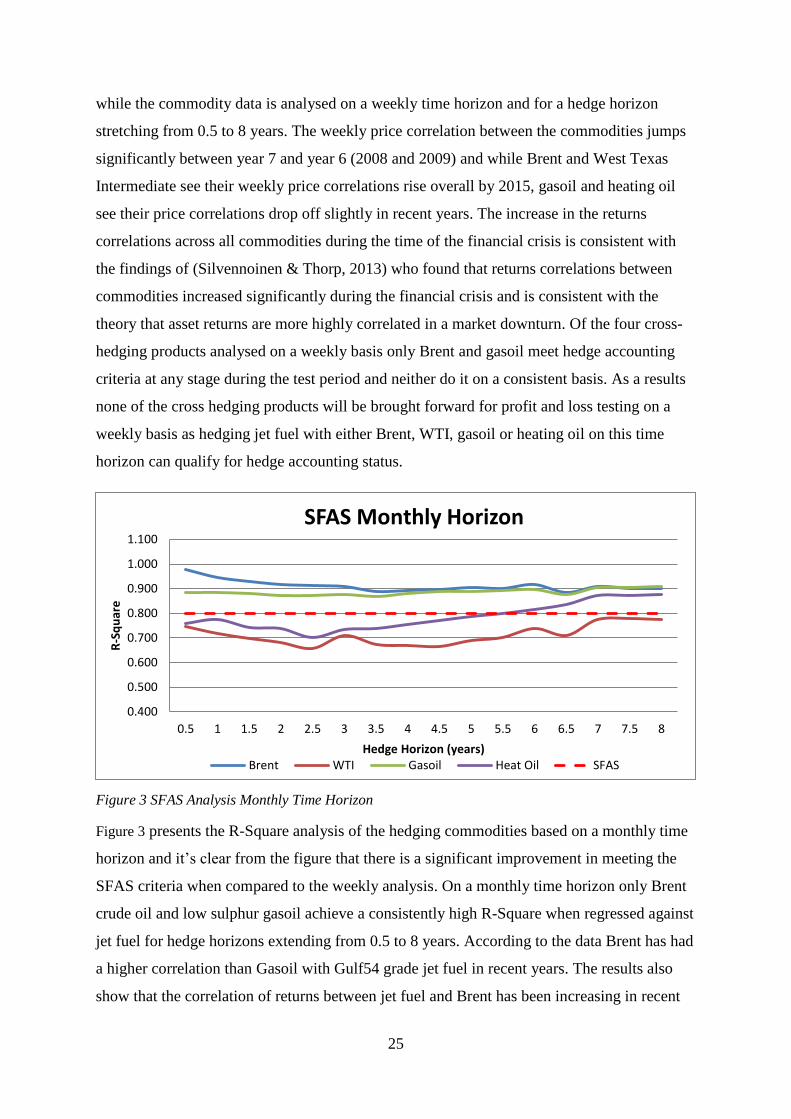

Figure 3 SFAS Analysis Monthly Time Horizon

Figure 3 presents the R-Square analysis of the hedging commodities based on a monthly time

horizon and it’s clear from the figure that there is a significant improvement in meeting the

SFAS criteria when compared to the weekly analysis. On a monthly time horizon only Brent

crude oil and low sulphur gasoil achieve a consistently high R-Square when regressed against

jet fuel for hedge horizons extending from 0.5 to 8 years. According to the data Brent has had

a higher correlation than Gasoil with Gulf54 grade jet fuel in recent years. The results also

show that the correlation of returns between jet fuel and Brent has been increasing in recent

0.400

0.500

0.600

0.700

0.800

0.900

1.000

1.100

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8

R-S

qu

are

Hedge Horizon (years)

SFAS Monthly Horizon

Brent WTI Gasoil Heat Oil SFAS

26

years while the R-Square for gasoil and jet fuel has remained relatively constant. In contrast

to the weekly findings three of the four commodities demonstrate a dip in correlation around

2008 which indicates that the drivers of monthly returns on jet fuel and the cross-hedging

products became inconsistent during the financial crisis due to the high levels of volatility in

the market. There is a significant fall in correlation between jet fuel and heating oil during the

past seven years and this trend is consistent with the weekly heating oil analysis in Figure 2,

while WTI does not meet the 0.8 R-Square criteria at any stage during testing when using a

monthly time period. The results from the monthly hedge analysis are significant enough to

carry Brent and gasoil forward for profit and loss analysis on a monthly time horizon while

WTI and Heatoil will be retained for quarterly analysis.

Figure 4 SFAS Analysis Quarterly Time Horizon

Although only WTI and heating oil were required to be analysed the other commodities are

included for comparison. Figure 4 shows the results for the quarterly horizon R-Square

analysis for each of the commodities and illustrates how three of the four cross hedging