Page 1

NIGERIAN CAPITAL MARKET:MODERNIZATION, REFORMS, TRENDS &

OUTLOOK FOR THE FUTURE

Presented by

Oscar N. Onyema

CEO, The Nigerian Stock Exchange

for

NIGERIA ECONOMIC & FINANCIAL MARKETS CONFERENCE

Bloomberg Auditorium, London, UK

23 March, 2012

23/03/2012 1The Nigerian Stock Exchange

Page 2

Established in 1960

Approx. 5 million investors:Foreign – 81% of market activityLocal – 19% of market activity

234 active Broker-Dealer firms28 member Issuing Houses

Equities – 199 listed cos. N6.35t ($40.56b) mkt cap

Bonds – 52 bonds N5.23t ($33.40b) mkt capETFs – 1 ETF N1.09b ($6.96m) AUM

14 electronic trading floors around Nigeria

About the NSE

23/03/2012 The Nigerian Stock Exchange 2

Figures as at 29-Feb-2012

Page 3

NSE Vision and Goal

23/03/2012 The Nigerian Stock Exchange 3

Page 4

• Consistent inflationary pressure

– 10.9% 12-mo average (12.6% in Jan 2012 – remains in double-digit territory)

• Tight monetary policy to manage inflation and high FX demand

– High MPR from 6.25% to 12%

• Increase in credit to private sector

– Up 30% month-on-month

• High lending rates

– 16.75% prime (23.21% max)

• High level of unemployment

– 23.9%; 15-24 year olds are highest bracket (approx 35m)

• Relative exchange rate stability

– N148.67 to N156.70 for USD1

23/03/2012 The Nigerian Stock Exchange 4

Nigerian Economic Trends2011

Page 5

23/03/2012 The Nigerian Stock Exchange 5

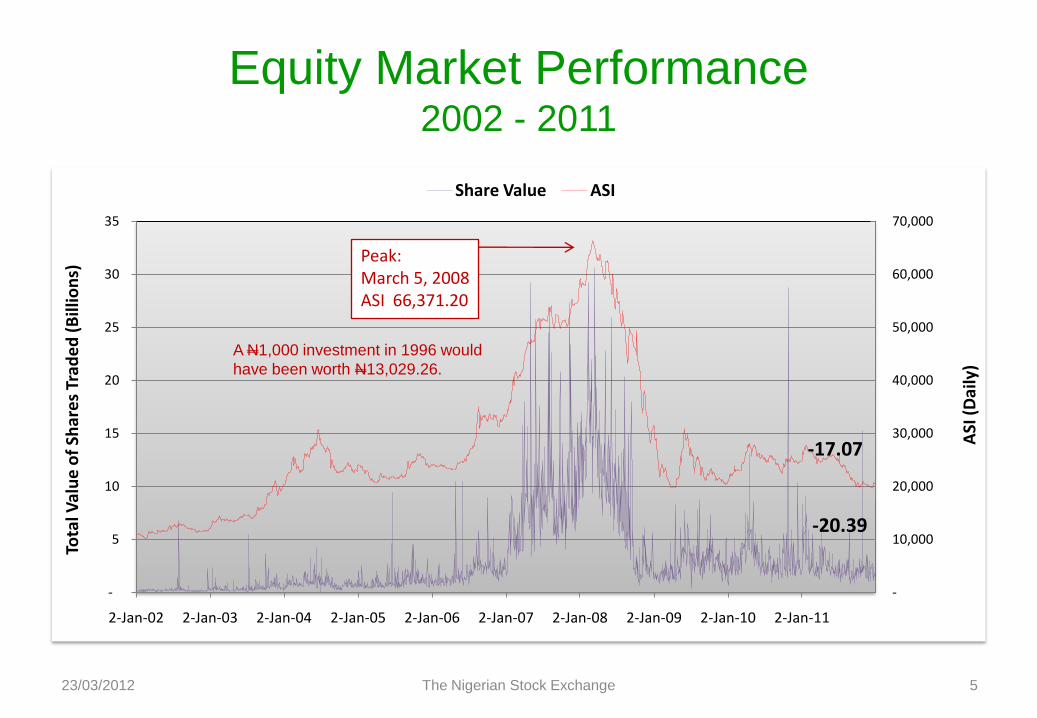

Equity Market Performance2002 - 2011

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

-

5

10

15

20

25

30

35

2-Jan-02 2-Jan-03 2-Jan-04 2-Jan-05 2-Jan-06 2-Jan-07 2-Jan-08 2-Jan-09 2-Jan-10 2-Jan-11

ASI

(D

aily

)

Tota

l Val

ue

of

Shar

es

Trad

ed

(B

illio

ns)

Share Value ASI

A N1,000 investment in 1996 would

have been worth N13,029.26.

Peak:March 5, 2008ASI 66,371.20

-17.07

-20.39

Page 6

• Soft global economy and cautious foreign investors

– Eurozone contraction (Aug-Dec) with 17-year unemployment high in UK and record high of

10.7% in 17-member zone; Credit ratings for 9 Euro nations cut by S&P (Jan 2012)

– US economy recovering – 3.0% growth in Q411; Inflation at 2.9%; Unemployment down to

8.30% (Jan 2012) from 8.50%

• Eroded investor confidence

– Preference for fixed income, especially for government paper

• Nigeria banking crisis

– N30b ($119.13m) market cap erased in one day; Banking Index down 34.69%

• Low broker-dealer participation rates

– Margin loan debt overhang and lack of access to financing (CBN prudential guidelines)

• Unfavorable interest rates

• Lack of liquidity and depth

– Low equity issuance, no IPO in 2011

– PFAs and Institutionals on the sidelines; Inordinate ratio of foreign-to-local participation

Equity Market Drivers

23/03/2012 The Nigerian Stock Exchange 6

Page 7

23/03/2012 The Nigerian Stock Exchange 7

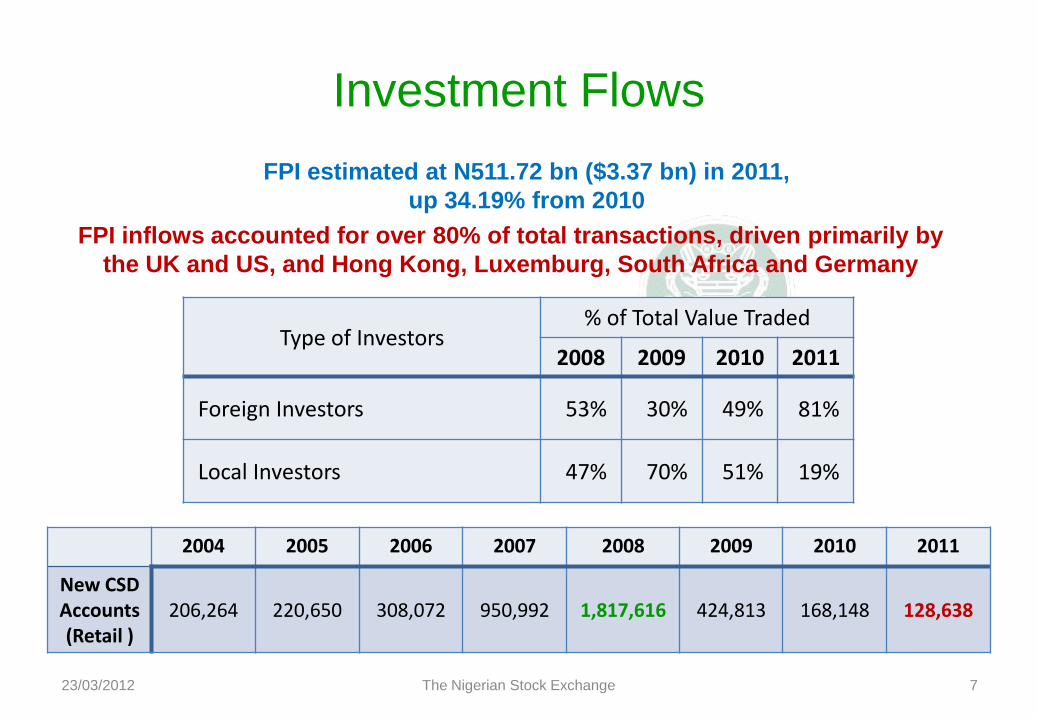

Investment Flows

Type of Investors% of Total Value Traded

2008 2009 2010 2011

Foreign Investors 53% 30% 49% 81%

Local Investors 47% 70% 51% 19%

2004 2005 2006 2007 2008 2009 2010 2011

New CSD Accounts(Retail )

206,264 220,650 308,072 950,992 1,817,616 424,813 168,148 128,638

FPI inflows accounted for over 80% of total transactions, driven primarily by

the UK and US, and Hong Kong, Luxemburg, South Africa and Germany

FPI estimated at N511.72 bn ($3.37 bn) in 2011,

up 34.19% from 2010

Page 8

• Stocks

– 1 fund: Closed-end fund – Sim Capital Alliance Value Fund

– Prospective issuers delaying raising new capital, i.e., no IPOs

– Investors rewarded with bonus and rights ($24.85b) issues, and dividends

• Exchange Traded Products

– 1 ETF: 1st ETF in Nigeria (and West Africa) – NewGold ETF; up 10.2% YTD (Feb 2012)

• Sovereign/State Bonds

– 2 state bonds: $329.33m Delta bond and $59.28m Niger bond

• Corporate Bonds

– 7 corporate bonds:

• $14.16m NAHCO bond

• $30.5m Tower Funding (x2) bonds

• $52.76m Dana Group bond

• $230.54m UBA bond

• $4.45b AMCON (3 tranches) bonds

23/03/2012 The Nigerian Stock Exchange 8

New Issues

2011

Page 9

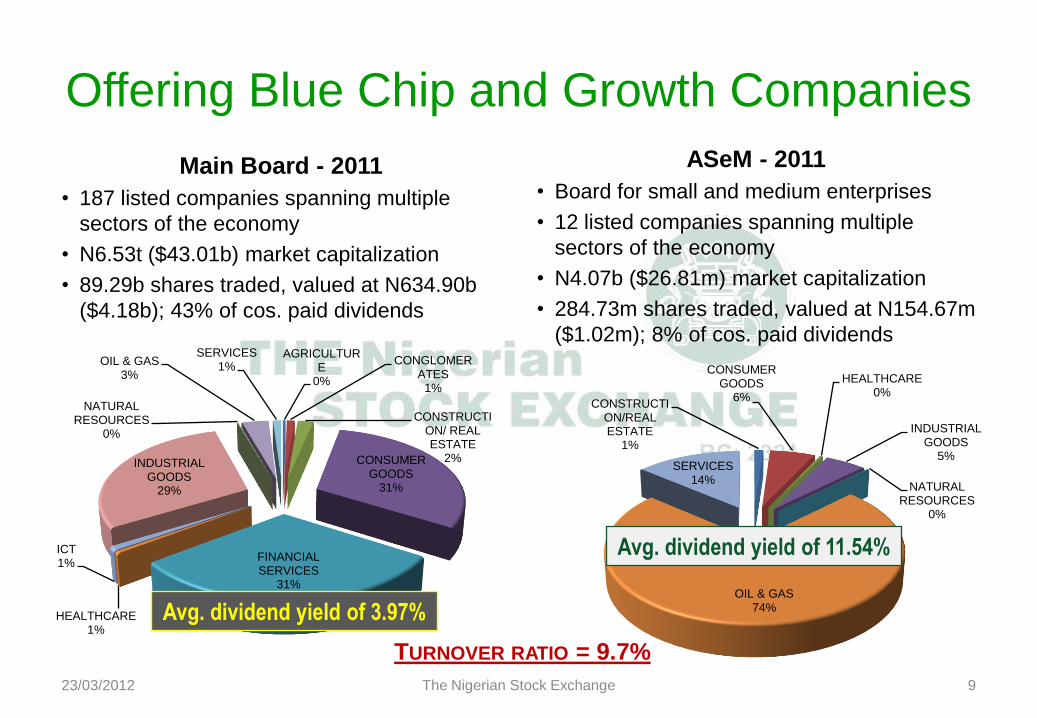

Offering Blue Chip and Growth Companies

Main Board - 2011

• 187 listed companies spanning multiple

sectors of the economy

• N6.53t ($43.01b) market capitalization

• 89.29b shares traded, valued at N634.90b

($4.18b); 43% of cos. paid dividends

ASeM - 2011

• Board for small and medium enterprises

• 12 listed companies spanning multiple

sectors of the economy

• N4.07b ($26.81m) market capitalization

• 284.73m shares traded, valued at N154.67m

($1.02m); 8% of cos. paid dividends

23/03/2012 The Nigerian Stock Exchange 9

AGRICULTURE

0%

CONGLOMERATES

1%

CONSTRUCTION/ REAL ESTATE

2%CONSUMER GOODS

31%

FINANCIAL SERVICES

31%

HEALTHCARE1%

ICT1%

INDUSTRIAL GOODS

29%

NATURAL RESOURCES

0%

OIL & GAS3%

SERVICES1%

CONSTRUCTION/REAL ESTATE

1%

CONSUMER GOODS

6%

HEALTHCARE0%

INDUSTRIAL GOODS

5%

NATURAL RESOURCES

0%

OIL & GAS74%

SERVICES14%

TURNOVER RATIO = 9.7%

Avg. dividend yield of 11.54%

Avg. dividend yield of 3.97%

Page 10

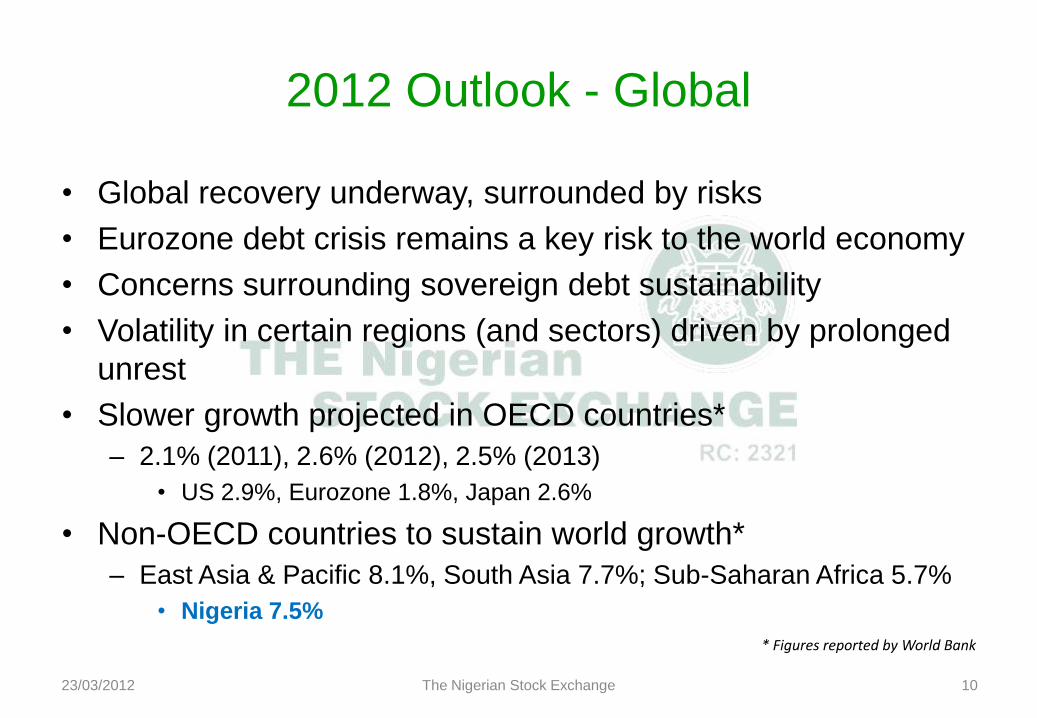

• Global recovery underway, surrounded by risks

• Eurozone debt crisis remains a key risk to the world economy

• Concerns surrounding sovereign debt sustainability

• Volatility in certain regions (and sectors) driven by prolonged

unrest

• Slower growth projected in OECD countries*

– 2.1% (2011), 2.6% (2012), 2.5% (2013)

• US 2.9%, Eurozone 1.8%, Japan 2.6%

• Non-OECD countries to sustain world growth*

– East Asia & Pacific 8.1%, South Asia 7.7%; Sub-Saharan Africa 5.7%

• Nigeria 7.5%

2012 Outlook - Global

23/03/2012 The Nigerian Stock Exchange 10

* Figures reported by World Bank

Page 11

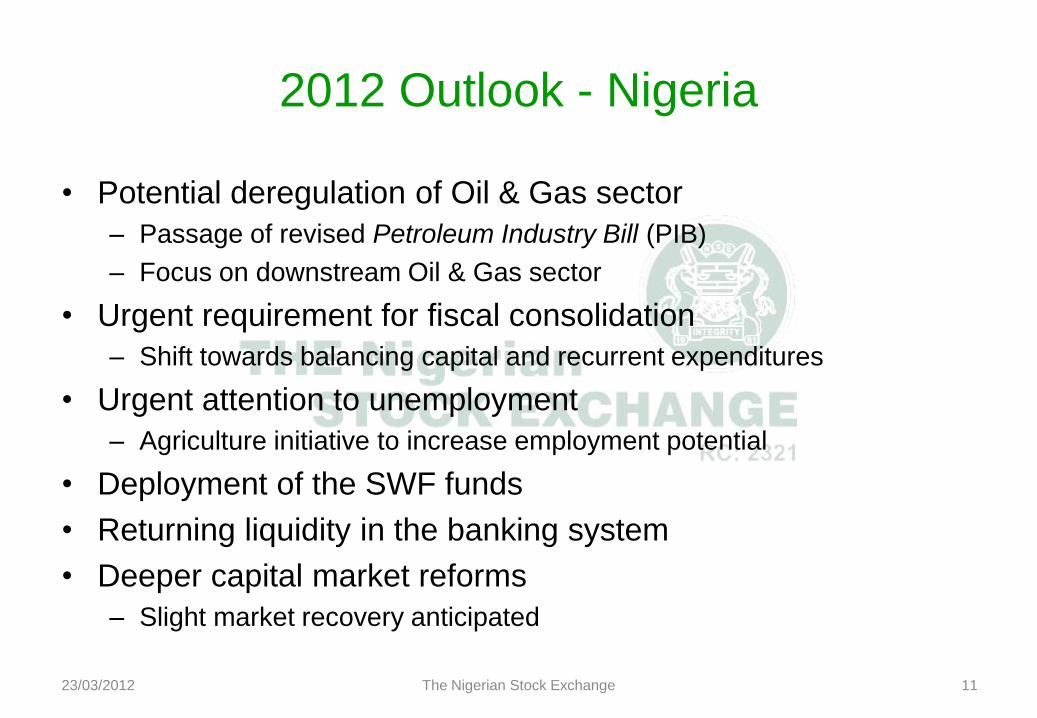

• Potential deregulation of Oil & Gas sector

– Passage of revised Petroleum Industry Bill (PIB)

– Focus on downstream Oil & Gas sector

• Urgent requirement for fiscal consolidation

– Shift towards balancing capital and recurrent expenditures

• Urgent attention to unemployment

– Agriculture initiative to increase employment potential

• Deployment of the SWF funds

• Returning liquidity in the banking system

• Deeper capital market reforms

– Slight market recovery anticipated

2012 Outlook - Nigeria

23/03/2012 The Nigerian Stock Exchange 11

Page 12

Reform-Driven 5-Year Outlook

23/03/2012 The Nigerian Stock Exchange 12

Targeted Business

Development Efforts

Strong Regulatory

Environment

“21st” Century

Technology Strategies

Growth-Enabling Market

Structure

First-Rate Investor

Protection Programs

$1t Market

Cap Target

Page 13

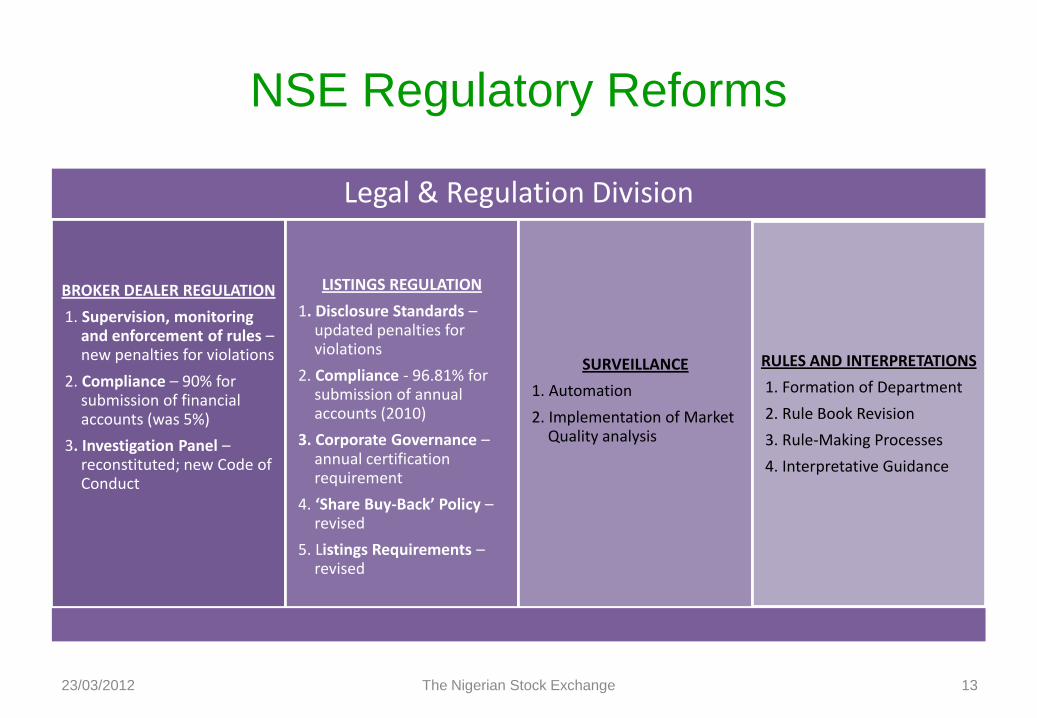

Legal & Regulation Division

BROKER DEALER REGULATION

1. Supervision, monitoring and enforcement of rules –new penalties for violations

2. Compliance – 90% for submission of financial accounts (was 5%)

3. Investigation Panel –reconstituted; new Code of Conduct

LISTINGS REGULATION

1. Disclosure Standards –updated penalties for violations

2. Compliance - 96.81% for submission of annual accounts (2010)

3. Corporate Governance –annual certification requirement

4. ‘Share Buy-Back’ Policy –revised

5. Listings Requirements –revised

SURVEILLANCE

1. Automation

2. Implementation of Market Quality analysis

RULES AND INTERPRETATIONS

1. Formation of Department

2. Rule Book Revision

3. Rule-Making Processes

4. Interpretative Guidance

23/03/2012 The Nigerian Stock Exchange 13

NSE Regulatory Reforms

Page 14

• Technology infrastructure

• X-Net (virtual private network) for brokers

• Development of NASDAQ OMX X-stream

trading platform

• New corporate database

• Market data services

• New data policy

• Feeds, subscriptions and reports for

market participants

• NSE Web site

• Access and market information for

investors and all stakeholders

• Value-added services

• Corporate Governance, Investor

Relations, Institutional Services, Equity

Research Coverage, and Corporate

Access for listed companies

23/03/2012 The Nigerian Stock Exchange 14

New Products and Services

Equities

Bonds

ETFs (Launched 2011)

Options (2013)

Futures (2015)

Page 15

Reform-Based Key Initiatives

23/03/2012 The Nigerian Stock Exchange 15

Term

Short (2011) Medium (2012)

Key

Init

iati

ves

Wit

hin

NSE

Co

ntr

ol

- Market Segmentation

- Company Share Buy-Back

- Introduction of ETFs

- Investor Clinics

- New Web Site

- Revised Listing Rules - Market Making (rules approved)

- Securities Lending (rules approved)

- Short Selling (rules approved)

- Develop Product Liquidity and Depth- Attract and Retain More Listings- E2E Trading Automation- Continued Enhancement of Regulatory Programs- Financial Literacy Program- IFRS Compliance- Demutualization- Market Data Services- Advocacy- Dematerialization

Ou

tsid

e N

SE C

on

tro

l - AMCON Debt Resolution- Advocacy

- Review PFA Investment Guidelines- Tax Breaks on Transaction Fees- Policy on Large Cap Firms to Deepen Market- Access to SWF Funds- Exit Strategy for Privatized Entities- Reduce Focus on Dividends- Capacity of Local Institutional Investors- Broker Margin Debt Resolution- Broker Access to Funding

Page 16

First-Rate Market, First-Rate Companies

23/03/2012 The Nigerian Stock Exchange 16

Page 17

“The Gateway to African Markets”

23/03/2012 The Nigerian Stock Exchange 17

We offer some of the highest yields

available at maturity, and the

potential for capital appreciation.

Growing per capita income as a result of an

economy that is growing over 7% annually.

Page 18

The Nigerian Stock ExchangeStock Exchange House

2-4 Customs Street

P.O. Box 2457, Marina

Lagos Island

Lagos, Nigeria

[email protected]

www.nse.com.ng

Thank You

23/03/2012 The Nigerian Stock Exchange 18