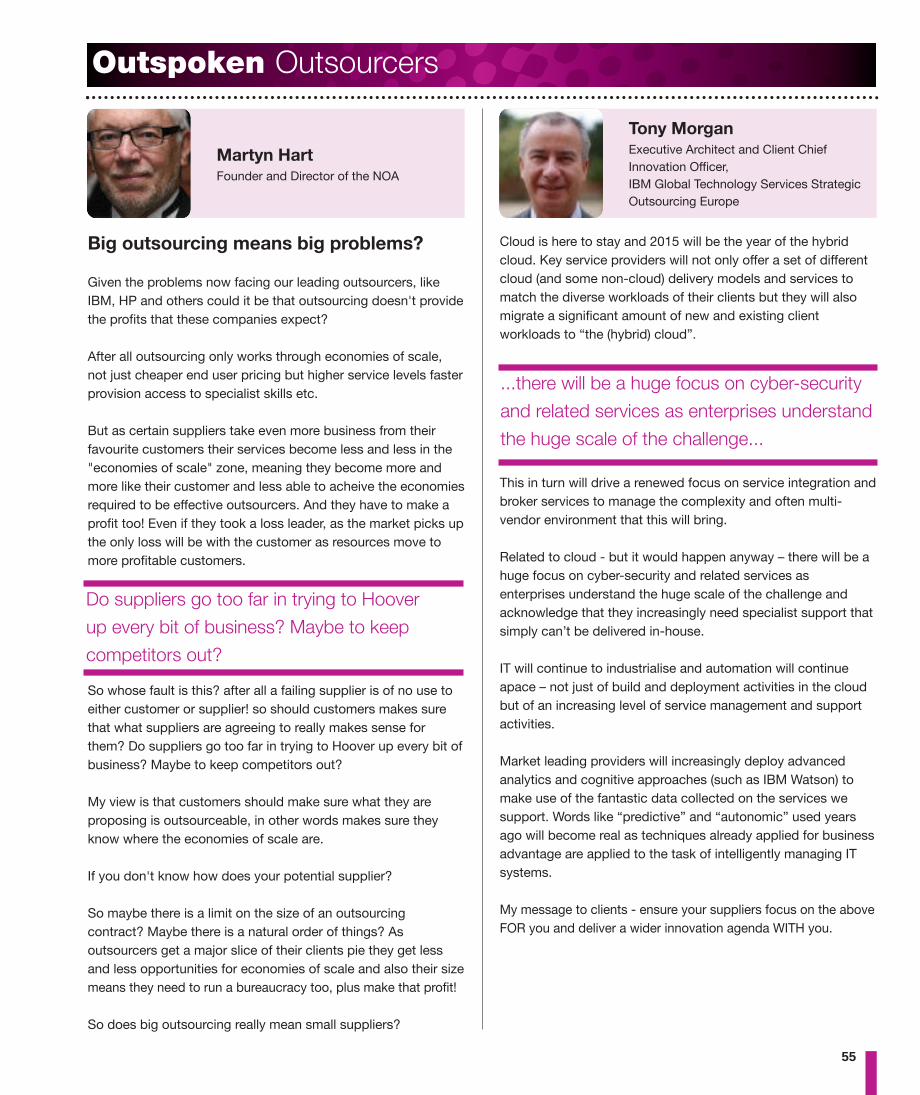

84

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:02 Page 1

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:02 Page 2

Contents

4 Events calendar6 Review of 201416 Industry insight28 Predicitions42 Case studies50 Outspoken outsourcers58 Outsourcing Directory

Welcomefrom the CEOWelcome to the 2015 edition of the NOA’s annual Outsourcing Yearbook. This issue features

a variety of opinions, predictions, studies and showcases, along with essential best practice

advice, statistical analysis and expert thought leadership.

Professionalising the outsourcing industry has always been a high priority for the NOA and

it is one of the more prominent themes in this Yearbook. The industry is finally beginning to

shed its negative reputation of yesteryear – this can only continue if the personnel involved

are trained correctly, and we see it as the NOA’s mission to grow the reach and positive

reputation of outsourcing through promoting best practice globally.

Professionalisation on a Corporate LevelBuyers of outsourcing come in all shapes and sizes, yet they all need similar proficiencies in

order to achieve outsourcing excellence. Last year, the NOA introduced its Corporate

Accreditation Programme to help companies recognise this. We also did it because those

that are excellent deserve to be recognised! The Accreditation Programme has been

heralded as a cost effective way to locate those hard-to-find problems and solve them,

allowing stakeholders and investors to sleep easier at night. Head to page 12 for more

information.

Continuous Professional DevelopmentHowever, the buck doesn’t stop with the executives. Every individual should be doing his or

her bit to ensure that organisations manage their outsourcing as well as possible. Capita is a

prime example, having demonstrated its commitment to individual development by rolling

out an NOA ‘Excellence in Outsourcing’ qualification across its service delivery teams.

CPD is the next logical step - the practice facilitates personal growth and optimises the

benefits attained from every learning opportunity. Now that the NOA has launched its own

CPD scheme, these benefits are available to outsourcing professionals everywhere. We

firmly believe that if every individual involved in outsourcing practised CPD, the industry

would reach unprecedented levels of professionalism.

Ethics and Codes of ConductThe hype surrounding this year’s general election has brought public sector outsourcing to

the forefront of the public eye. UK citizens want more ethics and transparency in

outsourcing, and who can disagree with them? The NOA has long campaigned for the

promotion of ethical outsourcing management and delivery; our research into ‘value beyond

cost’ demonstrates that buyers appreciate supplier transparency just as much as the public,

if not more so.

Value beyond CostThe same research goes on to offer brand new insight into what companies are looking for

when they outsource and how the perceptions of the buy and supply-side differ, making it a

must-read piece in this year’s edition. You’ll find it on page 18.

In short, this issue offers a comprehensive guide on how to succeed in outsourcing. You

can get involved by joining our existing professional development programmes, or

suggesting new ones that the NOA could provide.

Otherwise, just watch this space! I sincerely hope that you enjoy this year’s Yearbook – we

look forward to working with you in the future.

Kind Regards

Kerry Hallard, CEO, NOA

3

Published by EOA Ltd in association

with the National Outsourcing

Association and

www.sourcingfocus.com.

44 Wardour Street, London W1D 6QZ

Editorial:Glenn Hickling, Jeremy Coward

Business Development:Natalie Milsom

Outsourcing Directory:Aine McEvoy

Creative and Design:The Ark Design Consultancy Limited

Images:www.123rf.com

Print:Tyson Press

Many thanks to all our sponsors and

contributors.

©EOA Ltd. All rights reserved.

Kerry Hallard CEO, NOA

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:02 Page 3

4

2015 NOA Events CalendarNOA Events

Outsourcing is collaborative by nature, so it makesperfect sense to come together to learn from each other.NOA events & training workshops cater for buyers,suppliers and advisors alike, building a community thatprides itself on the sharing of knowledge anddevelopment of best practice.

Being committed to professional development for thosein the outsourcing industry the NOA offers a wide variety

of event topics and formats.

Take a look at our events calendar below for the first halfof the year to find out which is perfect for you.

To register for any of the below or for further detailsplease email [email protected] or visit the noa website,www.noa.co.uk.

Date Type Title Location Fees excluding VAT

APRIL

22nd April Breakfast Club Digitalisation in Outsourcing London Corporate members – FREE

Individual members - £150

Non Members – N/A

28th April Special Interest Customer Experience London Corporate members – FREE

Group Individual members - £150

Non Members – N/A

28th & 29th April Two Day Intensive London Members - £990

Workshop Non Members - £1089

MAY

13th May Afternoon Club Outsourcing Contract Perfection Manchester Corporate members – FREE

Individual members - £150

Non Members – N/A

21st May Awards Ceremony Professional Awards London 10% discount for all members

JUNE

24th June NOA Symposium NOA Symposium London 10% discount for all members

SEPTEMBER

16th - 17th Sept Awards Ceremony EOA Summit and Awards Lisbon, Portugal 10% discount for all members

NOVEMBER

19th November Awards Ceremony NOA Awards London 10% discount for all members

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:02 Page 4

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:02 Page 5

6

It’s been a busy year for the NOA andthis section pays reference to our mainactivities and applauds those thatcontributed in 2014

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:02 Page 6

7

Review of

2014NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 7

8

Review 2014

EOA Awards 2014• European BPO Contract of the Year

Conectys

• European IT Outsourcing Project of the Year

HCL & AstraZeneca

• European Outsourcing Service Provider of the Year

Teleperformance

• European Outsourcing Advisory of the Year

Eversheds LLP

• Offshoring Destination of the Year

Fiji

• Award for Corporate Social Responsibility

SPi Global - SPi for Visayas

• Award for Innovation in Pan-European Outsourcing

Teleperformance - CX Lab

• Outsourcing Works – Award for Delivering Business Value in

European Outsourcing

ITC Infotech & Danske Bank

• European Outsourcing Professional of the Year

William Pattison, Chief Executive Officer, Mindpearl BPO

• European Outsourcing Buyer of the Year

Ziggo & TechMahindra

Our award winning entrants!The NOA organises three types of major award ceremonies each year;

• EOA AwardsCelebrates excellence in pan-European outsourcing. Rewards buyers, suppliers, advisors and destinations from

all over Europe

• NOA's Professional AwardsDedicated awards ceremony that celebrates the individuals and teams that add most value to their companies,

their partners and the global outsourcing industry

• NOA AwardsOur largest award ceremony that rewards innovation and pioneering best practice by suppliers, buyers and

advisors. Now entering its twelfth year, it is firmly established as the awards all outsourcers want to win

These ceremonies provide the perfect opportunity to recognise you, your colleagues, your team and your

organisation amongst the elite of the outsourcing industry.

Here are our winners from 2014…

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 8

9

Review 2014

NOA’s Professional Awards 2014• Outsourcing Rising Star of the Year

Anthony Day, Partner, DLA Piper

• Outsourcing Professional of the Year

John McKinlay, Partner, DLA Piper

• Award for Academic Achievement

Philip Allery, Founder, Prescience Outsourcing Limited

• Award for Personal Development in Outsourcing

Tina Rizzo, Head of Service Integration, EE

• Best Relationship Management Team

Aviva

• Best IT Outsourcing Team

Miratech

• Best Finance & Accounts Outsourcing Team

Parseq

• Best Outsourced Customer Service Team

Firstsource & giffgaff

• Best Business Process Outsourcing Team

Firstsource & giffgaff

• Best Offshored Team

NashTech

• Award for Skills Development Programme of the Year

BPeSATata Consultancy Services BPS

NOA Awards 2014• International Contract of the Year

CSC and Zurich Insurance Group

• Offshoring Project of the Year

Telefonica and Capita

• Offshoring Destination of the Year

Sri Lanka

• Telecommunications, Utilities and High-Tech Outsourcing

Project of the Year

Firstsource Solutions Ltd and giffgaff

• Public Sector Outsourcing Project of the Year

Capgemini UK and the Environment Agency

• Financial Services Outsourcing Project of the Year

Herbert Smith Freehills LLP and TSB Bank plc separationproject

• Best Contribution to the Reputation of Outsourcing

KPMG LLP (UK)

• Award for Corporate Social Responsibility

Teleperformance and Citizen of the World (COTW)

• BPO Contract of the Year

Serco and De Vere• ITO Project of the Year

Deloitte

• Award for Innovation in Outsourcing

Parseq and Metalcashcard Ltd

• Shared Service Centre of the Year

Steria - NHS Shared Business Services

• Outsourcing Advisory of the Year

Slaughter and May

• Outsourcing Contact Centre Provider of the Year

Conectys

• Outsourcing Service Provider of the Year

HCL Great Britain LtdMidlandHR

• Outsourcing Buyer of the Year

BBC

• Outsourcing Works - Award for Delivering Business Value

TechMahindra and GlaxoSmithKline

Details on how to enter the 2015 award ceremonies can befound on our website www.noa.co.uk

NOA’sPROFESSIONAL

AWARDS

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 9

1�

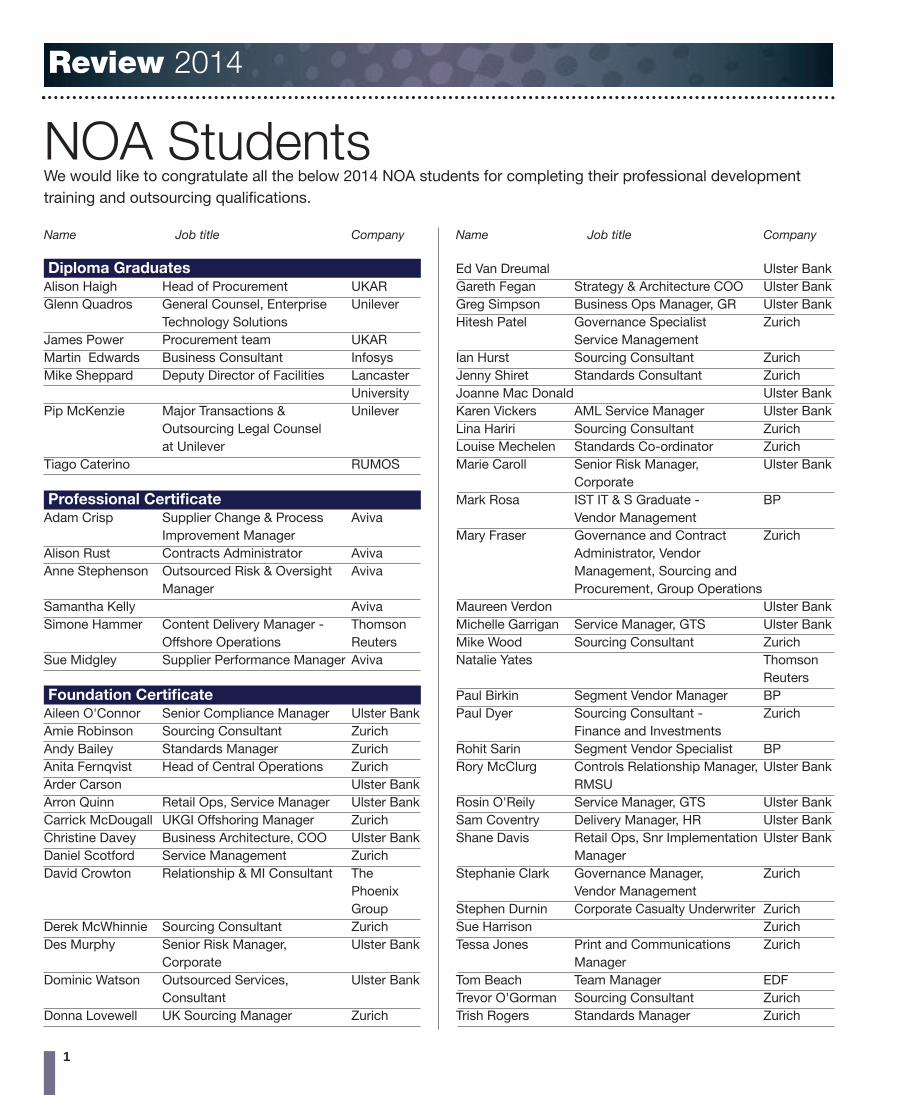

Review 2014

NOA StudentsWe would like to congratulate all the below 2014 NOA students for completing their professional development

training and outsourcing qualifications.

Name Job title Company

Diploma GraduatesAlison Haigh Head of Procurement UKAR

Glenn Quadros General Counsel, Enterprise Unilever

Technology Solutions

James Power Procurement team UKAR

Martin Edwards Business Consultant Infosys

Mike Sheppard Deputy Director of Facilities Lancaster

University

Pip McKenzie Major Transactions & Unilever

Outsourcing Legal Counsel

at Unilever

Tiago Caterino RUMOS

Professional CertificateAdam Crisp Supplier Change & Process Aviva

Improvement Manager

Alison Rust Contracts Administrator Aviva

Anne Stephenson Outsourced Risk & Oversight Aviva

Manager

Samantha Kelly Aviva

Simone Hammer Content Delivery Manager - Thomson

Offshore Operations Reuters

Sue Midgley Supplier Performance Manager Aviva

Foundation CertificateAileen O'Connor Senior Compliance Manager Ulster Bank

Amie Robinson Sourcing Consultant Zurich

Andy Bailey Standards Manager Zurich

Anita Fernqvist Head of Central Operations Zurich

Arder Carson Ulster Bank

Arron Quinn Retail Ops, Service Manager Ulster Bank

Carrick McDougall UKGI Offshoring Manager Zurich

Christine Davey Business Architecture, COO Ulster Bank

Daniel Scotford Service Management Zurich

David Crowton Relationship & MI Consultant The

Phoenix

Group

Derek McWhinnie Sourcing Consultant Zurich

Des Murphy Senior Risk Manager, Ulster Bank

Corporate

Dominic Watson Outsourced Services, Ulster Bank

Consultant

Donna Lovewell UK Sourcing Manager Zurich

Name Job title Company

Ed Van Dreumal Ulster Bank

Gareth Fegan Strategy & Architecture COO Ulster Bank

Greg Simpson Business Ops Manager, GR Ulster Bank

Hitesh Patel Governance Specialist Zurich

Service Management

Ian Hurst Sourcing Consultant Zurich

Jenny Shiret Standards Consultant Zurich

Joanne Mac Donald Ulster Bank

Karen Vickers AML Service Manager Ulster Bank

Lina Hariri Sourcing Consultant Zurich

Louise Mechelen Standards Co-ordinator Zurich

Marie Caroll Senior Risk Manager, Ulster Bank

Corporate

Mark Rosa IST IT & S Graduate - BP

Vendor Management

Mary Fraser Governance and Contract Zurich

Administrator, Vendor

Management, Sourcing and

Procurement, Group Operations

Maureen Verdon Ulster Bank

Michelle Garrigan Service Manager, GTS Ulster Bank

Mike Wood Sourcing Consultant Zurich

Natalie Yates Thomson

Reuters

Paul Birkin Segment Vendor Manager BP

Paul Dyer Sourcing Consultant - Zurich

Finance and Investments

Rohit Sarin Segment Vendor Specialist BP

Rory McClurg Controls Relationship Manager, Ulster Bank

RMSU

Rosin O'Reily Service Manager, GTS Ulster Bank

Sam Coventry Delivery Manager, HR Ulster Bank

Shane Davis Retail Ops, Snr Implementation Ulster Bank

Manager

Stephanie Clark Governance Manager, Zurich

Vendor Management

Stephen Durnin Corporate Casualty Underwriter Zurich

Sue Harrison Zurich

Tessa Jones Print and Communications Zurich

Manager

Tom Beach Team Manager EDF

Trevor O'Gorman Sourcing Consultant Zurich

Trish Rogers Standards Manager Zurich

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 10

Talent is the outsourcing

industry’s number one

concern.“

”We offer a range of training programmes andindustry qualifications, for professionals operatingat all levels.

Whether you need a skilled outsourcingprofessional or wish to become one, the NOA is the leadingbody for developing the outsourcing profession and industry.

To find out more, contact [email protected] or call 0207292 8686. www.noa.co.uk/professional-development/

Join the industryelite and sign upfor the 2015Spring Diploma in Outsourcingtoday

NATIONAL OUTSOURCING ASSOCIATION

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 11

OSYB: Why has the NOA developed a corporateaccreditation programme?

KH: We have spent the best part of two years developing our

corporate accreditation programme as a part of our ongoing

campaign to professionalise the outsourcing industry. Our

accreditation programme complements our existing portfolio of

qualifications for outsourcing professionals.

Users of outsourcing services frequently ask us: are they

working to outsourcing best practice? How do they know if their

service providers are guiding them to best effect? Are there any

shortfalls in the management of their outsourcings that could be

improved to deliver better results?

Although there are some emerging standards in outsourcing, all

of which the NOA has been involved with, these have needed to

be broad reaching and are generally non–prescriptive, as such

the NOA has developed its accreditation programme to sit

above these emerging standards and which is focused on the

maturity of an organisation‘s processes across all stages of the

outsourcing lifecycle model.

OSYB: Why would a company want to undertake the NOA’saccreditation programme?

KH: Benefits are manifold, but predominantly, users of

outsourcing services will: gain understanding as to how well

they compare to industry best practice; go on a journey of

improvement towards outsourcing best practice, which will yield

increased value in terms of cost savings and/or service

improvements, etc.; gain recognition for their outsourcing

competency and maturity; assure stakeholders of their

commitment to the delivery of best practice, to include the

Board, shareholders and customers.

OSYB: What is accredited?

KH: The NOA’s accreditation programme has been developed

to be flexible to cater to the huge variety of company

requirements. As such, the accreditation can be the company-

wide approach to outsourcing, that of a division, for a particular

business function or for a standalone outsourcing project. As

our accreditation programme is based on our Lifecycle Model,

companies can also choose to be partially accredited for their

practices in just one stage of the Lifecycle Model, for a couple

of stages, or achieve full accreditation for all four stages!

OSYB: What’s involved in undertaking an NOAAccreditation?

KH: The first stage of the accreditation process is to complete

our Outsourcing Lifecycle Assessment Level 1, which is hosted

online and is free of charge for members. A fifteen minute

questionnaire will quickly assess your outsourcing maturity

level, measured against the NOA’s own best practice standards

(there’s a secret algorithm embedded within). The resulting

report will give the user an overall maturity report, as well as

highlight specific areas for development.

After completing this stage, companies can choose to reflect

12

Review 2014

Spotlight on the NOA’s CorporateAccreditation ProgrammeThe Outsourcing Yearbook caught up with Kerry Hallard, CEO of the NOA to learnmore on the Association’s latest programme for improving performance in outsourcing

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 12

on their performance and develop their own journey of

improvement or alternatively embark upon a programme

towards NOA accreditation.

OSYB: So what’s involved in the journey to NOAAccreditation?

KH: There are 3 main stages to NOA corporate accreditation.

Put simply these are:

1. Accreditation Readiness Assessment2. Performance Improvement Programme3. NOA Accreditation Audit

Accreditation Readiness AssessmentCompanies or divisions keen to embark upon NOA

Accreditation need to sign up to NOA’s accreditation

programme. Upon enrolment, each company will be given three

things:

1. The first stage is to assign a project manager to lead this

accreditation programme for the company, who will be

responsible for involving all necessary participants at the

different stages of the programme. The project manager will be

given an information pack and access to a webinar detailing the

accreditation programme, how the NOA will assess and training

on how to use the software.

2. Working with your project manager, the NOA will help set the

company up on the Outsourcing Maturity Assessment software

platform and assign appropriate controls across the designated

users. The software collates and contrasts views of different

individuals/teams, and even the views of suppliers if so desired,

across level 2 of the Outsourcing Maturity Assessment to

deliver a solid and objective picture of company-wide

performance. By highlighting areas of weakness, the platform

facilitates deep dives to help the company understand where it

needs to improve performance. The software can be configured

to the specific needs of the client company, by refining and

tailoring the questionnaires accordingly.

3. The NOA, or a NOA accreditation partner, will host a one-day

workshop with the company to assess performance and what

needs to be done to work towards achieving NOA accreditation.

Performance Improvement ProgrammeThe Accreditation Readiness Assessment process will provide a

detailed report on performance against NOA’s standards. Armed

with this information, the client company may choose any of a

number of routes forward, to include but not limited to:

• Embarking upon a journey of improvement themselves

• Working with an NOA accreditation partner, or partner of their

own choice, on a journey of best practice improvements to be

accreditation ready

• Immediately undertake the accreditation Audit

Client companies will need to continue to use the software to

assess performance, though after the initial period of three

months, there is a quarterly license fee to continue to use the

software.

NOA Accreditation AuditWhen the company is ready, the NOA will go in and undertake

the Audit process. In preparation of the Audit the NOA will

review performance recorded in the software programme and

will request specific evidence in advance. The audit itself will

ordinarily take one day on site, interviewing different team

members and requesting different evidence from each, but this

varies depending on the scope for the accreditation audit.

Within one week of the audit taking place the NOA will

announce the level of accreditation achieved: Competent or

Excellent (there is another level: Foundation, which is not an

accredited level).

Companies will be given detailed feedback as to why they

achieved the level they did and recommendations of what

needs to be done to achieve the next level. Companies can

continue to move up the accreditation level over time if they

so wish.

OSYB: How long does accreditation take?

KH: The time the process takes really depends on the

company’s alignment to best practice. Some companies will be

ready to go straight to accreditation audit and achieve it within 3

months, others may need to go on a significant journey of

improvement.

The Accreditation is valid for three years when companies are

invited to undertake an

accreditation refreshment

programme.

OSYB: What’s coming up nextfor the Accreditationprogramme?

KH: We have been pleasantly

13

Review 2014

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 13

surprised by interest in accreditation from suppliers, as such we

are reworking the embedded templates and the processes to

work for the accreditation of suppliers. Watch this space.

During the preparation for accreditation, the data input by all

users will be aggregated and analysed anonymously to form an

industry wide picture of performance against best practice.

Sectoral analysis will be published periodically by the NOA to

drive industry performance.

If you are interested in corporate or project accreditation please

contact the NOA to receive a free link to the initial Outsourcing

Lifecycle Assessment, or to arrange a call about the full

process.

If you are a consultant or advisory and are interested in

becoming a NOA Accreditation Partner, please contact

Chris Halward at [email protected].

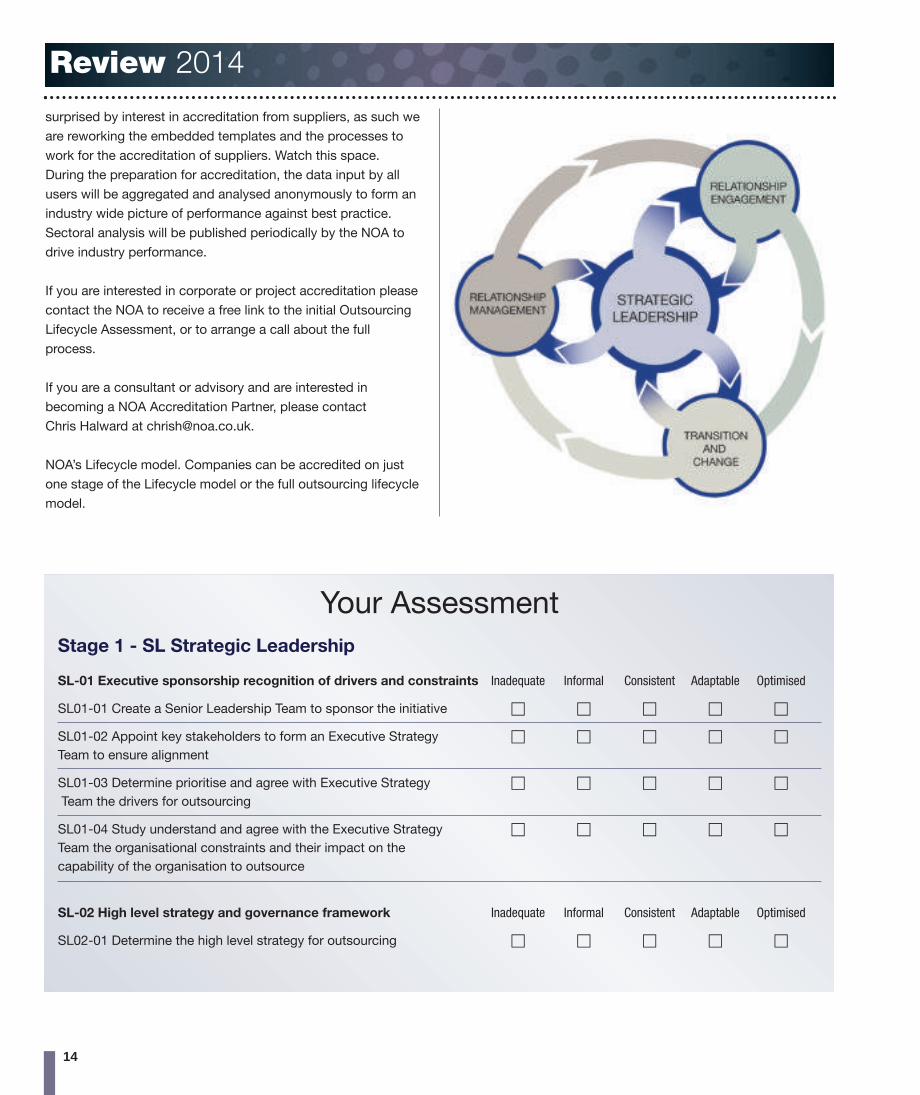

NOA’s Lifecycle model. Companies can be accredited on just

one stage of the Lifecycle model or the full outsourcing lifecycle

model.

Review 2014

Your Assessment

Stage 1 - SL Strategic Leadership

SL-01 Executive sponsorship recognition of drivers and constraints Inadequate Informal Consistent Adaptable Optimised

SL01-01 Create a Senior Leadership Team to sponsor the initiative c c c c c

SL01-02 Appoint key stakeholders to form an Executive Strategy c c c c c

Team to ensure alignment

SL01-03 Determine prioritise and agree with Executive Strategy c c c c c

Team the drivers for outsourcing

SL01-04 Study understand and agree with the Executive Strategy c c c c c

Team the organisational constraints and their impact on the

capability of the organisation to outsource

SL-02 High level strategy and governance framework Inadequate Informal Consistent Adaptable Optimised

SL02-01 Determine the high level strategy for outsourcing c c c c c

14

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 14

15

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 15

How can buyers and suppliers bringadded value?

16

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 16

17

Industryinsight

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 17

Executive SummaryCreation of added value is moving to central importance in

terms of delighting outsourcing clients. As contemporary buyers

leave behind the old school ‘your mess for less’ attitude and

demand much more from their partners, the National

Outsourcing Association and Polaris conducted a poll to delve

into the key influencers, indicators and drivers of added value in

outsourcing.

The results were highly encouraging. It is clear that the vast

majority of those who participate in outsourcing are convinced

of its value, with a significant percentage of buyers certain that

there is more value to outsourcing than simply cost-cutting.

Despite this, many buyers are not confident in their ability to

assess how well their partners are performing, which is highly

surprising in this age of data analytics and performance

tracking. Buyers are also suspicious when their suppliers offer

‘innovation’; the ability to innovate is always desirable, but there

appears to be ongoing confusion between buyers and suppliers

over what innovation actually is.

Buyers and suppliers unsurprisingly agreed that a strong

relationship founded on trust is a vital component in good

outsourcing. However, a strong outsourcing relationship

requires aligned beliefs and objectives. While buyers and

suppliers were aligned on value-adding activities, commercial

constructs and reasons for outsourcing, there’s discord

between the two parties regarding performance assessment,

delivering value, sharing risk, cost-reduction and more.

Suppliers are often guilty of adopting a more ‘rose-tinted’

perspective than their buyers.

Nevertheless, the future looks positive for both sides, with the

majority of buyers expecting to expand their outsourcing over

the next five years. This may be connected to the rise of

outcome-based contracts, which should allow both buyers and

suppliers to attain more certainty regarding the success of their

outsourcing activities.

18

Glenn HicklingIndependent Writer

Industry insight

NOA Research - value beyond costHow can buyers and suppliers bring added value to their outsourcing relationships? The questionnaire thatNOA members were provided with was designed to reveal how successful their outsourcing is, where thesuccesses and flaws lie, and what their aspirations for the future are. The aim was to ascertain not just howimportant added value is, but what those involved in the outsourcing marketplace are doing to make it work.

It is well known that the best outsourcing relationships are founded on aligned goals and expectations.Hence why another key objective of the research was to find sympathies and disconnects among buyer andsupplier attitudes: buyers were asked their view, and suppliers were asked what they thought theircustomers are thinking, both in terms of their current picture and their plans for the future.

This report documents the results. It provides a comprehensive picture of the outsourcing industry’s state,where it’s likely to go and what changes are necessary. The analysis should serve to provoke further thoughtand discussion regarding the report’s findings.

Enjoy!

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 18

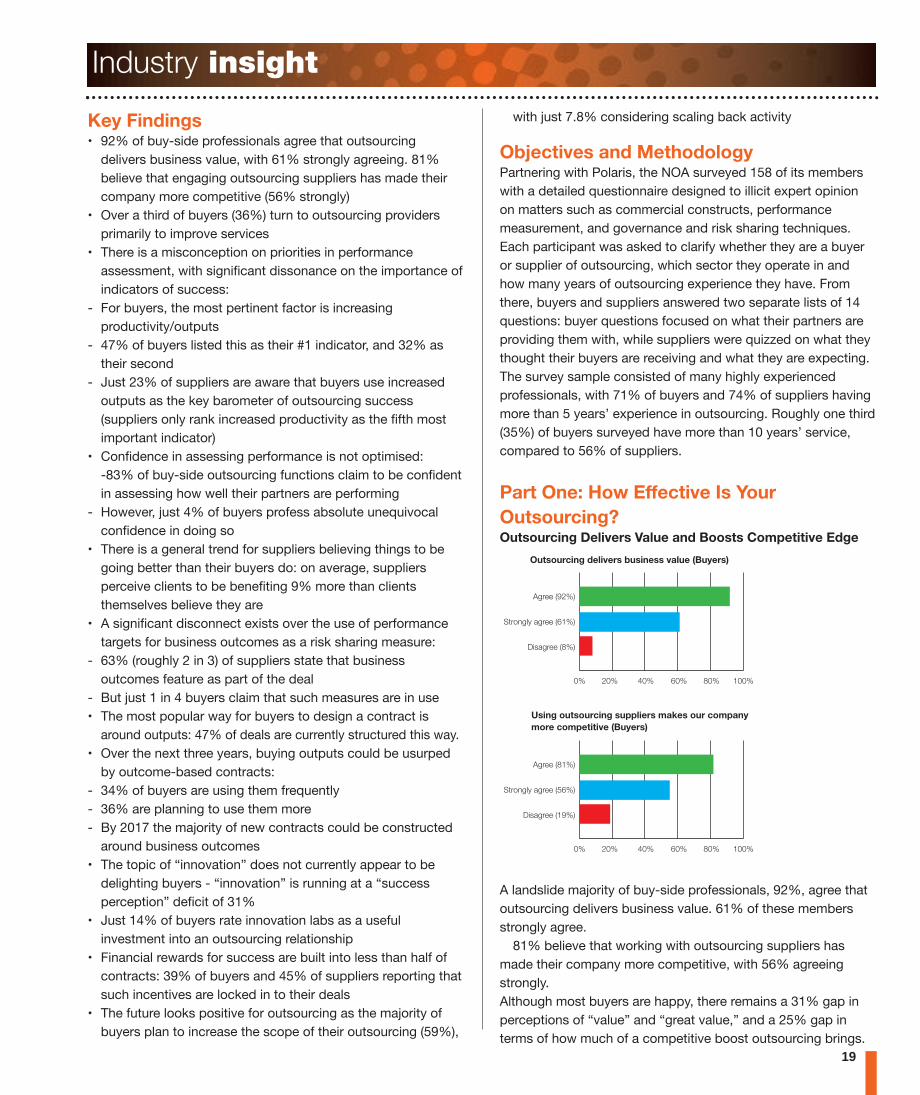

Key Findings• 92% of buy-side professionals agree that outsourcing

delivers business value, with 61% strongly agreeing. 81%

believe that engaging outsourcing suppliers has made their

company more competitive (56% strongly)

• Over a third of buyers (36%) turn to outsourcing providers

primarily to improve services

• There is a misconception on priorities in performance

assessment, with significant dissonance on the importance of

indicators of success:

- For buyers, the most pertinent factor is increasing

productivity/outputs

- 47% of buyers listed this as their #1 indicator, and 32% as

their second

- Just 23% of suppliers are aware that buyers use increased

outputs as the key barometer of outsourcing success

(suppliers only rank increased productivity as the fifth most

important indicator)

• Confidence in assessing performance is not optimised:

-83% of buy-side outsourcing functions claim to be confident

in assessing how well their partners are performing

- However, just 4% of buyers profess absolute unequivocal

confidence in doing so

• There is a general trend for suppliers believing things to be

going better than their buyers do: on average, suppliers

perceive clients to be benefiting 9% more than clients

themselves believe they are

• A significant disconnect exists over the use of performance

targets for business outcomes as a risk sharing measure:

- 63% (roughly 2 in 3) of suppliers state that business

outcomes feature as part of the deal

- But just 1 in 4 buyers claim that such measures are in use

• The most popular way for buyers to design a contract is

around outputs: 47% of deals are currently structured this way.

• Over the next three years, buying outputs could be usurped

by outcome-based contracts:

- 34% of buyers are using them frequently

- 36% are planning to use them more

- By 2017 the majority of new contracts could be constructed

around business outcomes

• The topic of “innovation” does not currently appear to be

delighting buyers - “innovation” is running at a “success

perception” deficit of 31%

• Just 14% of buyers rate innovation labs as a useful

investment into an outsourcing relationship

• Financial rewards for success are built into less than half of

contracts: 39% of buyers and 45% of suppliers reporting that

such incentives are locked in to their deals

• The future looks positive for outsourcing as the majority of

buyers plan to increase the scope of their outsourcing (59%),

with just 7.8% considering scaling back activity

Objectives and Methodology Partnering with Polaris, the NOA surveyed 158 of its members

with a detailed questionnaire designed to illicit expert opinion

on matters such as commercial constructs, performance

measurement, and governance and risk sharing techniques.

Each participant was asked to clarify whether they are a buyer

or supplier of outsourcing, which sector they operate in and

how many years of outsourcing experience they have. From

there, buyers and suppliers answered two separate lists of 14

questions: buyer questions focused on what their partners are

providing them with, while suppliers were quizzed on what they

thought their buyers are receiving and what they are expecting.

The survey sample consisted of many highly experienced

professionals, with 71% of buyers and 74% of suppliers having

more than 5 years’ experience in outsourcing. Roughly one third

(35%) of buyers surveyed have more than 10 years’ service,

compared to 56% of suppliers.

Part One: How Effective Is YourOutsourcing?Outsourcing Delivers Value and Boosts Competitive Edge

A landslide majority of buy-side professionals, 92%, agree that

outsourcing delivers business value. 61% of these members

strongly agree.

81% believe that working with outsourcing suppliers has

made their company more competitive, with 56% agreeing

strongly.

Although most buyers are happy, there remains a 31% gap in

perceptions of “value” and “great value,” and a 25% gap in

terms of how much of a competitive boost outsourcing brings.

19

Industry insight

Agree (92%)

Strongly agree (61%)

Disagree (8%)

0% 20% 40% 60% 80% 100%

Outsourcing delivers business value (Buyers)

Agree (81%)

Strongly agree (56%)

Disagree (19%)

0% 20% 40% 60% 80% 100%

Using outsourcing suppliers makes our companymore competitive (Buyers)

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 19

Concurrent Cost Cutting and Service Improvement isBecoming the New Normal

Only 54% of buyers state that reducing costs is their number

one driver. 36% of buyers now choose outsourcing primarily to

improve their services.

The supplier view is similar: 56% of suppliers reason that their

buyers are mainly looking to cut costs on their bottom line, but

27% consider their clients to be mainly choosing outsourcing

for the purpose of improving services.

So it would seem that, while buyers certainly want it better,

they still want it cheaper too…and who can blame them?

17% of suppliers believe they are being selected for benefits

such as cutting edge technology, better talent and processes

etc., compared to 11% of buyers citing this reason.

It could be argued that clients are more interested in end

results than the alchemy that goes into achieving them, which is

a sign of a progressive industry where trust in suppliers is

growing.

How is Performance and Value Assessed?Buyers and suppliers were asked to rank their top 3 measures

for evaluating outsourcing performance, where 1 indicated their

most used measure.

The first significant dissonance in the survey comes in the form

of incorrect assumptions of how buyers like to evaluate an

outsourcing deal’s performance.

For buyers, the most pertinent factor is an increase in

productivity/outputs - 47% of buyers listed this as their #1

indicator, and 32% as their second.

Suppliers only ranked “increased outputs” as the fifth most

important indicator, with just 23% of suppliers aware that

buyers use it as the key barometer of outsourcing success.

Cost reduction remains an important metric. 56% of suppliers

suppose it is the #1 KPI, compared to just 24% of buyers.

Buyer and supplier returns were almost identical on the topic

of customer surveys, highlighting a 360° awareness of the role

outsourcing plays in delighting consumers/ultimate end users.

These statistics all point towards a buy-side culture of quality

over cost, but the difference of opinion in the vitality of

increased outputs needs to be addressed.

Reductions in inputs, improved outputs and positive staff

user surveys are all important to buyers, but none more so than

the boost to productivity once the outsourcing deal beds in.

Confidence Levels in Assessing Performance83% of buy-side outsourcing functions claim to be confident in

assessing how well their partners are performing, but a mere

4% profess absolute unequivocal confidence in doing so.

1% of buyers are really unconfident, with a further 16%

admitting that their confidence levels in performance

assessment are less than desired.

From a supplier perspective, 88.5% are confident their efforts

are being accurately appraised, with just 3.8% suggesting that

their clients are not confident in their own ability to measure

suppliers’ performance.

2�

Industry insight

Reduce costs

Improve services

Access othervalue-add benefits

0% 20% 40% 60% 80% 100%

Prime drivers for outsourcing

BuyersSuppliers

""

## + + ### # # # #

# # # # # ## # # # #

# # # # # ## # # #

# # # # # #

""

## + + ### # # # #

# # # # # ## # # # #

# # # # # ## # # #

# # # # # #

""

## + + ### # # # #

# # # # # ## # # # #

# # # # # ## # # #

# # # # # #

desUtsMo

$-&0"4 $&-(.887"+:9;:9#87/+,/.645 =%(< &&(<+A/@9.+./8?:>9+ ''(< 3=(<

85*:796/.:>8+ 3!(< !3$<+/[email protected]+/.+9DC,CB: !'$< !3$<+/?86:9#87/@8.;4? $$$< $($<

+:9;5*7/+,/.6)/ E!$< $'$<

""

## + + ### # # # #

# # # # # ## # # # #

# # # # # ## # # #

# # # # # #

85*:796/.:>8++A/@9.+./8?:>9++/?86:9#87/@8.;4?

7/+,/.6)/ +:9;*5+:9;:9#87/+,/.645+/[email protected]+/.+9DC,CB:

""

## + + ### # # # #

# # # # # ## # # # #

# # # # # ## # # #

# # # # # #

A smaller survey, conducted during a plenary session at the

NOA Symposium 2014, posed this question to the audience:

Service improvement is a top priority for both buyers andsuppliers. What do you think is the main inhibitor to this?

43% of attendees answered that contracts are structured

around headcount rather than service

30% blamed the lack of simple methodology to measure

service improvement

15% called for higher levels of expertise

12% said that it is not in suppliers’ interest as it may reduce

business volumes

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 20

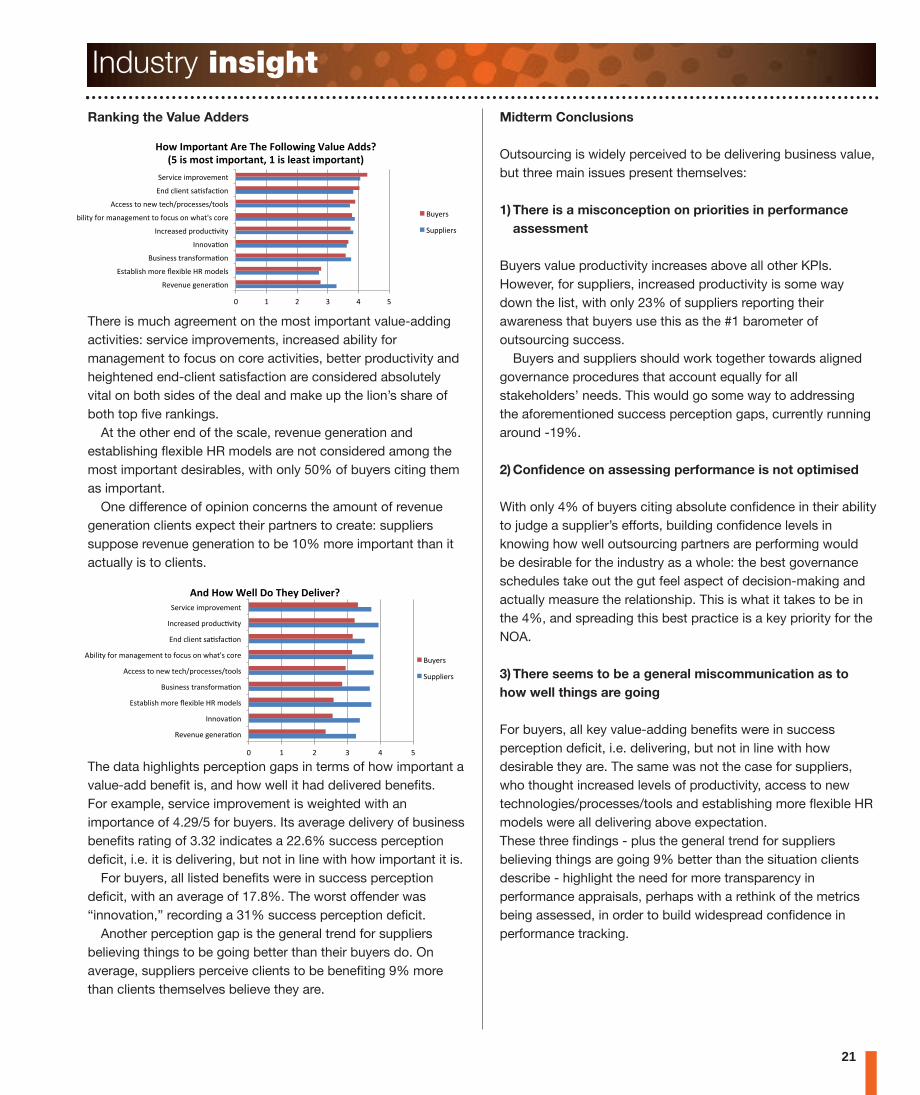

Ranking the Value Adders

There is much agreement on the most important value-adding

activities: service improvements, increased ability for

management to focus on core activities, better productivity and

heightened end-client satisfaction are considered absolutely

vital on both sides of the deal and make up the lion’s share of

both top five rankings.

At the other end of the scale, revenue generation and

establishing flexible HR models are not considered among the

most important desirables, with only 50% of buyers citing them

as important.

One difference of opinion concerns the amount of revenue

generation clients expect their partners to create: suppliers

suppose revenue generation to be 10% more important than it

actually is to clients.

The data highlights perception gaps in terms of how important a

value-add benefit is, and how well it had delivered benefits.

For example, service improvement is weighted with an

importance of 4.29/5 for buyers. Its average delivery of business

benefits rating of 3.32 indicates a 22.6% success perception

deficit, i.e. it is delivering, but not in line with how important it is.

For buyers, all listed benefits were in success perception

deficit, with an average of 17.8%. The worst offender was

“innovation,” recording a 31% success perception deficit.

Another perception gap is the general trend for suppliers

believing things to be going better than their buyers do. On

average, suppliers perceive clients to be benefiting 9% more

than clients themselves believe they are.

Midterm Conclusions

Outsourcing is widely perceived to be delivering business value,

but three main issues present themselves:

1)There is a misconception on priorities in performance assessment

Buyers value productivity increases above all other KPIs.

However, for suppliers, increased productivity is some way

down the list, with only 23% of suppliers reporting their

awareness that buyers use this as the #1 barometer of

outsourcing success.

Buyers and suppliers should work together towards aligned

governance procedures that account equally for all

stakeholders’ needs. This would go some way to addressing

the aforementioned success perception gaps, currently running

around -19%.

2)Confidence on assessing performance is not optimised

With only 4% of buyers citing absolute confidence in their ability

to judge a supplier’s efforts, building confidence levels in

knowing how well outsourcing partners are performing would

be desirable for the industry as a whole: the best governance

schedules take out the gut feel aspect of decision-making and

actually measure the relationship. This is what it takes to be in

the 4%, and spreading this best practice is a key priority for the

NOA.

3)There seems to be a general miscommunication as tohow well things are going

For buyers, all key value-adding benefits were in success

perception deficit, i.e. delivering, but not in line with how

desirable they are. The same was not the case for suppliers,

who thought increased levels of productivity, access to new

technologies/processes/tools and establishing more flexible HR

models were all delivering above expectation.

These three findings - plus the general trend for suppliers

believing things are going 9% better than the situation clients

describe - highlight the need for more transparency in

performance appraisals, perhaps with a rethink of the metrics

being assessed, in order to build widespread confidence in

performance tracking.

21

Industry insight

""

A

O

!# (# $# E# %# M#

K/@/59/#-/5/.,N85#

O+:,IG*+F#?8./#P/Q*IG/#RK#?87/G+#

L9+*5/++#:.,5+C8.?,N85#

4558@,N85#

456./,+/7#;.8796N@*:A#

I*G*:A#C8.#?,5,-/?/5:#:8#C869+#85#SF,:T+#68./#

266/++#:8#5/S#:/6FD;.86/++/+D:88G+#

O57#6G*/5:#+,N+C,6N85#

B/.@*6/#*?;.8@/?/5:#

@%A+B<8%)#+C&-+DE-+?%..%A()*+12."-+CFF$G++3H+($+<%$#+(<8%)#I+J+($+.-2$#+(<8%)#5+

L9A/.+#

B9;;G*/.+#

""

A

O

!# (# $# E# %# M#

K/@/59/#-/5/.,N85#

4558@,N85#

O+:,IG*+F#?8./#P/Q*IG/#RK#?87/G+#

L9+*5/++#:.,5+C8.?,N85#

266/++#:8#5/S#:/6FD;.86/++/+D:88G+#

2I*G*:A#C8.#?,5,-/?/5:#:8#C869+#85#SF,:T+#68./#

O57#6G*/5:#+,N+C,6N85#

456./,+/7#;.8796N@*:A#

B/.@*6/#*?;.8@/?/5:#

C)F+@%A+K-..+,%+DE-4+,-.(/-&G++

L9A/.+#

B9;;G*/.+#

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 21

Part Two: Making Outsourcing WorkCommitting to Better Productivity

Over one in five buyers (22%) have been promised between 11-

20% productivity improvements. Around 1 in 3 is expecting a

boost of up to 10%; an ambitious 1.5% are expecting a 31-

40% hike in productivity.

1 in 3 suppliers believe their clients have been promised

between 21-30% better productivity, while only around 1 in 10

buyers think that this is the case.

When considering cases of no expected improvements at all,

1 in 3 buyers have not been promised improvements, while only

10% of suppliers report there being no expected commitment

to enhanced productivity.

Customers’ views are usually based on what is actually

contracted for, whereas suppliers’ views represent their

capability deliver. When drawing these intentions into a

contract, proposed improvements tend to be toned down due

to the customers’ appetite for internal change, adaptions to new

processes and tools, and also their willingness to switch from

staff augmentation to outcome-based models.

It should also be mentioned that many contracts focus purely

on cost reduction and prioritise reduced staffing levels over

productivity. These deals can only ever commit to agreed price

rates, because they lack the maturity to measure and improve

productivity.

Committing to Lower Costs

Suppliers appear to be offering more cost reductions than

buyers believe are on offer.

38% of buyers are expecting up to 10% cost reduction,

which was the most popular answer.

The second most common return was no commitment at all,

which around 34% of buyers are expecting. No buyers are

expecting cost cutting of 30+%, but 17% of suppliers declare

they are offering such reductions.

42% of suppliers claim to be offering 21-30% cost

reductions. Less than 1 in 10 confess that they have no

immediate plans to reduce their clients’ costs.

Suppliers are committing to cost reductions and productivity

improvements simultaneously. Both elements are linked to an

extent, e.g. where process efficiency or automation leads to

lower headcounts.

At the same time, as service providers bear much of the

investment and risk of internal process improvements that

generate productivity benefits, situations where not all of

advantages can be passed on to the client are not uncommon.

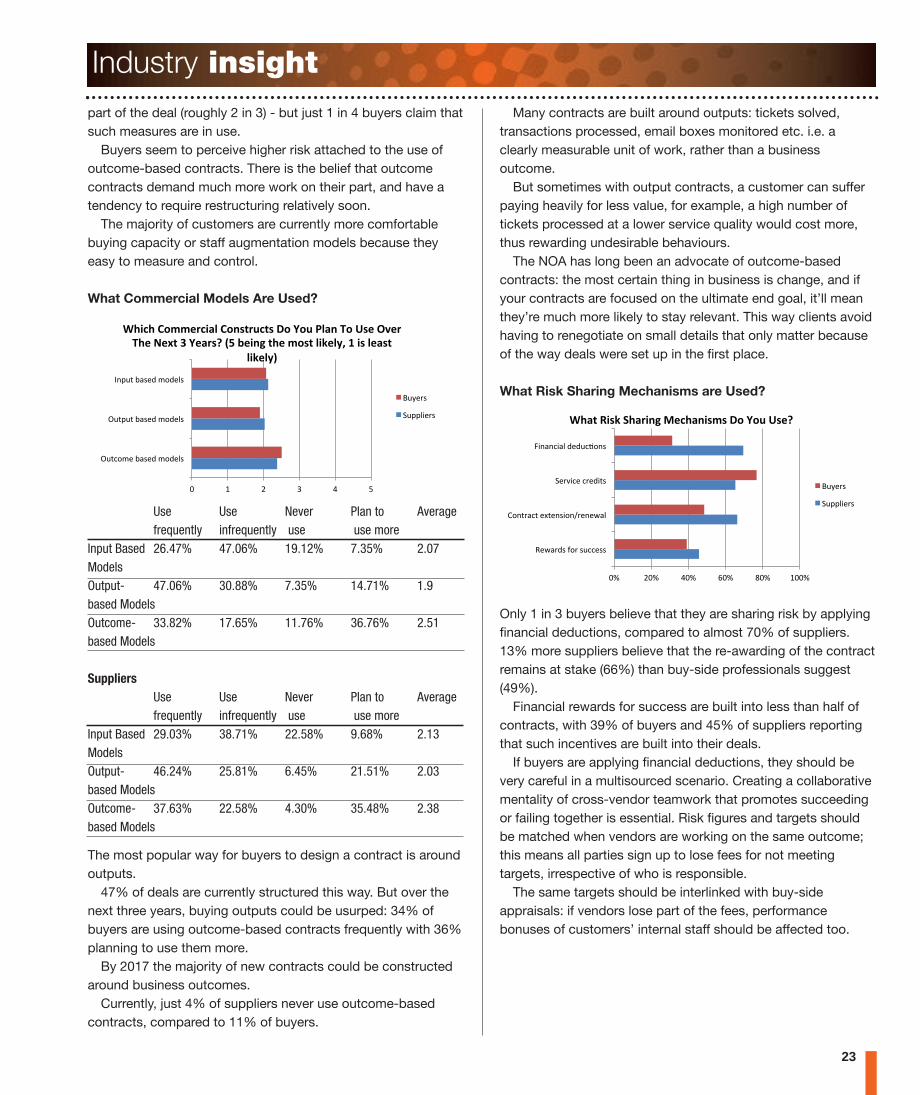

How Is Risk Shared?

Almost exactly an equal number of suppliers and buyers

reported heavy usage of risk sharing via delivery metrics such

as SLAs and cost commitments.

Timeline commitments are used in less than half of deals (46%).

14% of deals appear not use SLAs - or at least not with

particular rewards or penalties attached.

One major disconnect is over the use of targets on certain

business outcomes as a risk sharing measure.

63% of suppliers state that business outcomes feature as

22

Industry insight

""

1 in 3 suppliers believe their clients have been promised between 21-30% better p

W

I

N

B

# # # # # # # # # # #

U8#68??*:?/5:#

%("V#

E(H%!"#

$(HE!"#

((H$!"#

!H(!"#

KE2#+>&%F"'=/(#4+B<8&%/-<-)#$+C&-+0-()*+;%<<(L-F+D%G++

L9A/.+#

B9;;G*/.+#

""

-

"

3

T

S

A

!<!!"# $!<!!"# %!<!!"# &!<!!"# '!<!!"# (!!<!!"#

U85/#

%("V#

E(H%!"#

$(HE!"#

((H$!"#

!H(!"#

KE2#+;%$#+M-F"'=%)$+C&-+0-()*+;%<<(L-F+D%G++

L9A/.+#

B9;;G*/.+#

""

T

1

O

6

B

T

!"# $M"# M!"# =M"# (!!"#

L9+*5/++#89:68?/#68??*:?/5:#0/<-<#./796/#68+:#;/.#:.,5+,6N85#IA#Q"1#

W*?/G*5/#68??*:?/5:+#

>8+:#68??*:?/5:+#0*</<#JQ/7#;.*6/#685:.,6:+1#

)/G*@/.A#0*</<#BX2+1#

@%A+,%+N%"+7E2&-+M($:G+

L9A/.+#

B9;;G*/.+#

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Another small survey conducted during a plenary session at

the NOA Symposium 2014 posed this question to the seated

audience:

Buyers believe that suppliers are not committing toproductivity improvements. Why?11% of attendees thought buyers are not really insisting upon

them.

34% said buyer expectations are too high, without even

knowing current levels.

25% claimed suppliers need real expertise to deliver, hence

they hesitate to commit.

21% believed suppliers are showing willingness to commit

but make it too difficult to implement.

8% thought none of the above.

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 22

part of the deal (roughly 2 in 3) - but just 1 in 4 buyers claim that

such measures are in use.

Buyers seem to perceive higher risk attached to the use of

outcome-based contracts. There is the belief that outcome

contracts demand much more work on their part, and have a

tendency to require restructuring relatively soon.

The majority of customers are currently more comfortable

buying capacity or staff augmentation models because they

easy to measure and control.

What Commercial Models Are Used?

The most popular way for buyers to design a contract is around

outputs.

47% of deals are currently structured this way. But over the

next three years, buying outputs could be usurped: 34% of

buyers are using outcome-based contracts frequently with 36%

planning to use them more.

By 2017 the majority of new contracts could be constructed

around business outcomes.

Currently, just 4% of suppliers never use outcome-based

contracts, compared to 11% of buyers.

Many contracts are built around outputs: tickets solved,

transactions processed, email boxes monitored etc. i.e. a

clearly measurable unit of work, rather than a business

outcome.

But sometimes with output contracts, a customer can suffer

paying heavily for less value, for example, a high number of

tickets processed at a lower service quality would cost more,

thus rewarding undesirable behaviours.

The NOA has long been an advocate of outcome-based

contracts: the most certain thing in business is change, and if

your contracts are focused on the ultimate end goal, it’ll mean

they’re much more likely to stay relevant. This way clients avoid

having to renegotiate on small details that only matter because

of the way deals were set up in the first place.

What Risk Sharing Mechanisms are Used?

Only 1 in 3 buyers believe that they are sharing risk by applying

financial deductions, compared to almost 70% of suppliers.

13% more suppliers believe that the re-awarding of the contract

remains at stake (66%) than buy-side professionals suggest

(49%).

Financial rewards for success are built into less than half of

contracts, with 39% of buyers and 45% of suppliers reporting

that such incentives are built into their deals.

If buyers are applying financial deductions, they should be

very careful in a multisourced scenario. Creating a collaborative

mentality of cross-vendor teamwork that promotes succeeding

or failing together is essential. Risk figures and targets should

be matched when vendors are working on the same outcome;

this means all parties sign up to lose fees for not meeting

targets, irrespective of who is responsible.

The same targets should be interlinked with buy-side

appraisals: if vendors lose part of the fees, performance

bonuses of customers’ internal staff should be affected too.

23

Industry insight

""

T

1

O

6

B

T

!# (# $# E# %# M#

Y9:68?/#I,+/7#?87/G+#

Y9:;9:#I,+/7#?87/G+#

45;9:#I,+/7#?87/G+#

KE('E+;%<<-&'(2.+;%)$#&"'#$+,%+N%"+>.2)+D%+6$-+!/-&+DE-+O-P#+Q+N-2&$G+3H+R-()*+#E-+<%$#+.(:-.4I+J+($+.-2$#+

.(:-.45++

L9A/.+#

B9;;G*/.+#

Use Use Never Plan to Average frequently infrequently use use more Input Based 26.47% 47.06% 19.12% 7.35% 2.07ModelsOutput- 47.06% 30.88% 7.35% 14.71% 1.9based Models Outcome- 33.82% 17.65% 11.76% 36.76% 2.51based Models

Suppliers Use Use Never Plan to Average frequently infrequently use use moreInput Based 29.03% 38.71% 22.58% 9.68% 2.13ModelsOutput- 46.24% 25.81% 6.45% 21.51% 2.03based Models Outcome- 37.63% 22.58% 4.30% 35.48% 2.38based Models

""

1

I

T

!"# $!"# %!"# &!"# '!"# (!!"#

K/S,.7+#C8.#+966/++#

>85:.,6:#/Q:/5+*85D./5/S,G#

B/.@*6/#6./7*:+#

Z*5,56*,G#7/796N85+#

KE2#+M($:+7E2&()*+9-'E2)($<$+,%+N%"+6$-G+

L9A/.+#

B9;;G*/.+#

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 23

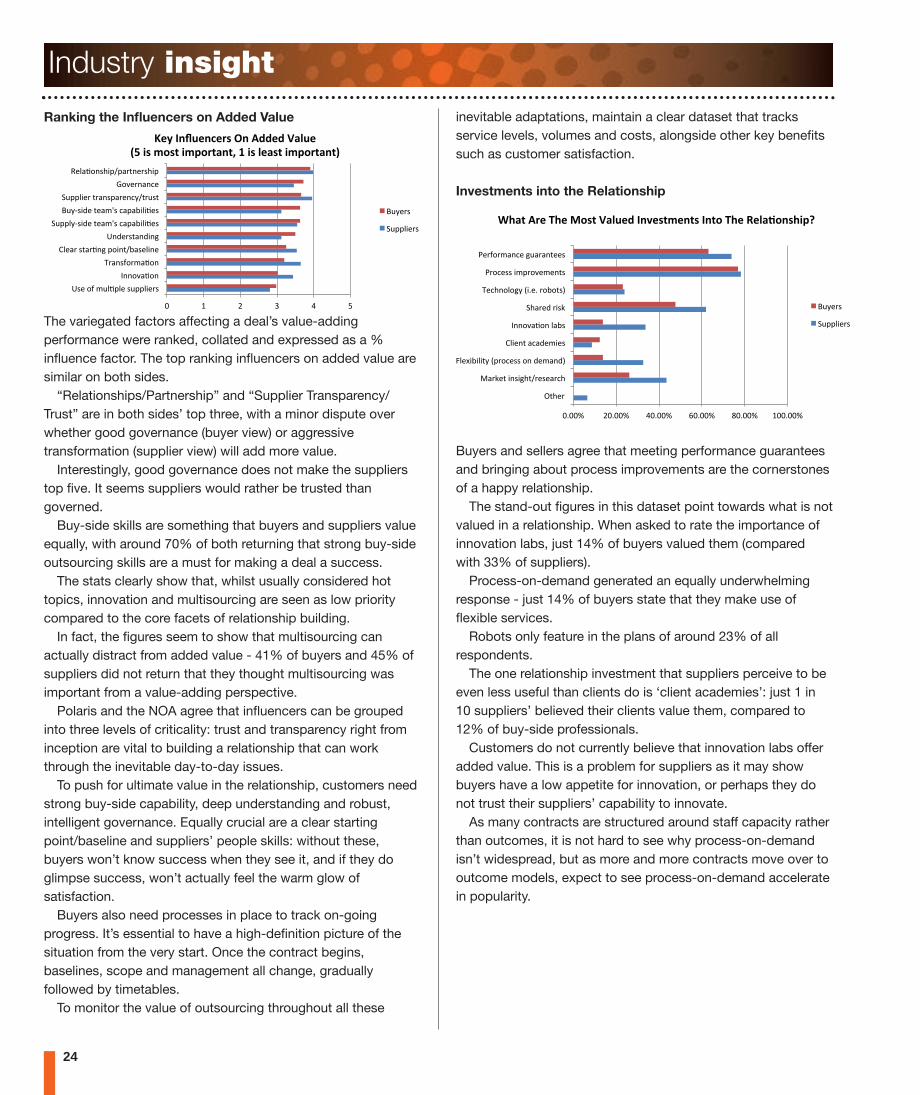

Ranking the Influencers on Added Value

The variegated factors affecting a deal’s value-adding

performance were ranked, collated and expressed as a %

influence factor. The top ranking influencers on added value are

similar on both sides.

“Relationships/Partnership” and “Supplier Transparency/

Trust” are in both sides’ top three, with a minor dispute over

whether good governance (buyer view) or aggressive

transformation (supplier view) will add more value.

Interestingly, good governance does not make the suppliers

top five. It seems suppliers would rather be trusted than

governed.

Buy-side skills are something that buyers and suppliers value

equally, with around 70% of both returning that strong buy-side

outsourcing skills are a must for making a deal a success.

The stats clearly show that, whilst usually considered hot

topics, innovation and multisourcing are seen as low priority

compared to the core facets of relationship building.

In fact, the figures seem to show that multisourcing can

actually distract from added value - 41% of buyers and 45% of

suppliers did not return that they thought multisourcing was

important from a value-adding perspective.

Polaris and the NOA agree that influencers can be grouped

into three levels of criticality: trust and transparency right from

inception are vital to building a relationship that can work

through the inevitable day-to-day issues.

To push for ultimate value in the relationship, customers need

strong buy-side capability, deep understanding and robust,

intelligent governance. Equally crucial are a clear starting

point/baseline and suppliers’ people skills: without these,

buyers won’t know success when they see it, and if they do

glimpse success, won’t actually feel the warm glow of

satisfaction.

Buyers also need processes in place to track on-going

progress. It’s essential to have a high-definition picture of the

situation from the very start. Once the contract begins,

baselines, scope and management all change, gradually

followed by timetables.

To monitor the value of outsourcing throughout all these

inevitable adaptations, maintain a clear dataset that tracks

service levels, volumes and costs, alongside other key benefits

such as customer satisfaction.

Investments into the Relationship

Buyers and sellers agree that meeting performance guarantees

and bringing about process improvements are the cornerstones

of a happy relationship.

The stand-out figures in this dataset point towards what is not

valued in a relationship. When asked to rate the importance of

innovation labs, just 14% of buyers valued them (compared

with 33% of suppliers).

Process-on-demand generated an equally underwhelming

response - just 14% of buyers state that they make use of

flexible services.

Robots only feature in the plans of around 23% of all

respondents.

The one relationship investment that suppliers perceive to be

even less useful than clients do is ‘client academies’: just 1 in

10 suppliers’ believed their clients value them, compared to

12% of buy-side professionals.

Customers do not currently believe that innovation labs offer

added value. This is a problem for suppliers as it may show

buyers have a low appetite for innovation, or perhaps they do

not trust their suppliers’ capability to innovate.

As many contracts are structured around staff capacity rather

than outcomes, it is not hard to see why process-on-demand

isn’t widespread, but as more and more contracts move over to

outcome models, expect to see process-on-demand accelerate

in popularity.

24

Industry insight

""

“

I

B

T

I

P

T

B

!# (# $# E# %# M#

[+/#8C#?9GN;G/#+9;;G*/.+#4558@,N85#

W.,5+C8.?,N85#>G/,.#+:,.N5-#;8*5:DI,+/G*5/#

[57/.+:,57*5-#B9;;GAH+*7/#:/,?T+#6,;,I*G*N/+#

L9AH+*7/#:/,?T+#6,;,I*G*N/+#B9;;G*/.#:.,5+;,./56AD:.9+:#

\8@/.5,56/#K/G,N85+F*;D;,.:5/.+F*;#

S-4+B)T"-)'-&$+!)+CFF-F+12."-++3H+($+<%$#+(<8%)#I+J+($+.-2$#+(<8%)#5+

+

L9A/.+#

B9;;G*/.+#

""

T

P

R

C

A

!<!!"# $!<!!"# %!<!!"# &!<!!"# '!<!!"# (!!<!!"#

Y:F/.#

],.^/:#*5+*-F:D./+/,.6F#

ZG/Q*I*G*:A#0;.86/++#85#7/?,571#

>G*/5:#,6,7/?*/+#

4558@,N85#G,I+#

BF,./7#.*+^#

W/6F58G8-A#0*</<#.8I8:+1#

_.86/++#*?;.8@/?/5:+#

_/.C8.?,56/#-9,.,5://+#

KE2#+C&-+DE-+9%$#+12."-F+B)/-$#<-)#$+B)#%+DE-+M-.2=%)$E(8G++

L9A/.+#

B9;;G*/.+#

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 24

Part Three: Outsourcing Aspirations forthe FutureThe Future Intentions of Outsourcers

The majority of buyers plan to increase the scope of their

outsourcing (59%), while just 7.8% are considering scaling back

activity.

Half of buyers are seeking greater business transformation

but suppliers are expecting even more transformation, with 72%

of them suggesting clients will ramp up efforts to transform.

Attitudes to offshoring may come as a slight surprise: 1 in 4

buyers are planning to offshore more, and only 6% are seriously

considering re-shoring.

Suppliers, however, think that three-quarters of their clients

are keen to re-shore.

Only 29% buyers are currently planning to move to cloud, but

suppliers think that over half (55%) are considering such a

move.

The feeling that multi-sourcing isn’t an essential driver of

added value could be represented by the number of buyers, just

28%, who are planning to work with more suppliers.

But as just 34% are planning to work with less suppliers, the

figures could indicate that most buy-side outsourcing functions

feel that their current blend of suppliers is working well.

There are many more suppliers under the impression that

clients will push for shorter term contracts (36%) than there are

buyers with a mind to do so. Just 14% of clients are planning to

initiate shorter term contracts over the next three years.

ConclusionsThe Future Appears Bright60% of outsourcing buyers plan to use outsourcing more in the

next five years: the outsourcing industry will continue to grow,

as existing buyers increase the scope of the work they send

out. It is expected that suppliers would appear more

enthusiastic about the results being delivered than clients;

despite this, the survey clearly elucidates how the vast majority

of outsourcing arrangements deliver solid business value, with

most outsourcing buyers satisfied that outsourcing improved

the competiveness of their business. But expectation is running

high, as the majority of suppliers are committing to concurrent

productivity improvements and lower bills for clients.

Outcome-based Contracts Will Catch On, EventuallyOutcome-based contracts will increase in popularity, although

traditional output-based contracts with SLAs and cost

commitments are still commonplace. There does appear to be

some confusion around outcome-based contracts and risk

sharing: nearly triple the amount of suppliers purport that risk is

shared via outcome-based contracts than the amount of buyers

who state that they operate with such models.

Performance Tracking Needs ImprovingThere are also some issues around performance tracking, with

major dissonance around the importance of key indicators such

as productivity. As improvements are being widely promised,

there needs to be redoubled effort at every turn when it comes

to tracking these productivity improvements and their residual

benefits.

Relationships and Skills before Innovation While there is slight buyer/supplier dissonance around how to

make relationships work optimally, it appears that a greater

emphasis on people and relationship skills would go some way

to aligning perceptions of collaborative success.

Relationships are the most valued contributor to positive

performance: their importance is lauded by buyers and

suppliers equally. Investing in the relationship is vital, but so is

making the right investments. Popular initiatives like client

academies and innovation labs are not as well received as their

organisers would hope; maybe there is a need to reinvent these

activities, as well as to track them and celebrating any value

they create.

Innovation does not currently appear to be delighting buyers -

the success perception deficit of 31% and the distain for

innovation labs point towards this. Buyers and suppliers need to

work together to foster innovation at appropriate levels, to avoid

a slowdown in terms of generating competitive advantage in the

client’s business.

Above all else, getting the basics right, such as building

relationships and developing quality intelligent governance are

lauded as the cornerstones of creating added value in an

outsourcing relationship.

25

Industry insight

""

H

S

O

T

B

T

!<!!"# $!<!!"# %!<!!"# &!<!!"# '!<!!"#

K/+F8.*5-#[+/#G/++#8@/.,GG#

[+/#.8I8N6#,9:8?,N85#BF8.:/.#:/.?#685:.,6:+#

U/,.+F8./#?8./#Y`+F8./#?8./#

a8.^#S*:F#?8./#+9;;G*/.+#]8@/#:8#6G897#

a8.^#S*:F#G/++#+9;;G*/.+#B//^#-./,:/.#I9+*5/++#:.,5+C8.?,N85#

a8.^#85#,#.*+^#./S,.7#?87/G#[+/#?8./#8@/.,GG#

!"#$%"&'()*+B)#-)=%)$+B)+DE-+O-P#+?(/-+N-2&$+

L9A/.+#

B9;;G*/.+#

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 25

Carl Adkins of Infinity CCS looks at how outsourced contactcentre operators using on-demand technology platformscan help their clients satisfy omni-channel customers withintoday’s budget constraints.

In June 2007 Apple launched the first iPhone, since whenconsumers have fully embraced digital, any time, any placeconsumption and service. If they want to tweet you from theirphone at 2am, chat with a live agent from their browser beforefinalising a purchase, or use their tablet to video-link withtechnical support from the middle of nowhere, you’d better beable to respond. Unfortunately this new business reality, and the investment itrequires of companies, arrived at the worst possible time. Justsix months after the iPhone launch, in December 2007, theglobal economy was sucker-punched by the start of the GreatRecession. Despite recent signs of recovery most companiesare still under pressure to reduce costs, headcounts and capitalspending.

A Way Out of the Trash CompactorFor occupiers of the C-Suite it must feel like being trapped inthe trash compactor from the first Star Wars movie. On one sidethere is the pressure to be more efficient, and on the other theneed to do more to meet customers’ new demands. Han, Lukeand Leia escaped by passing the job on to R2D2, a droid. Thesame mix of outsourcing and technology can help companiesmeet their challenges today. In this article we will look at how outsourced service providers(OSPs) able to leverage the right technology can have atransformative impact on their clients’ businesses by facilitatingomni-channel communication.

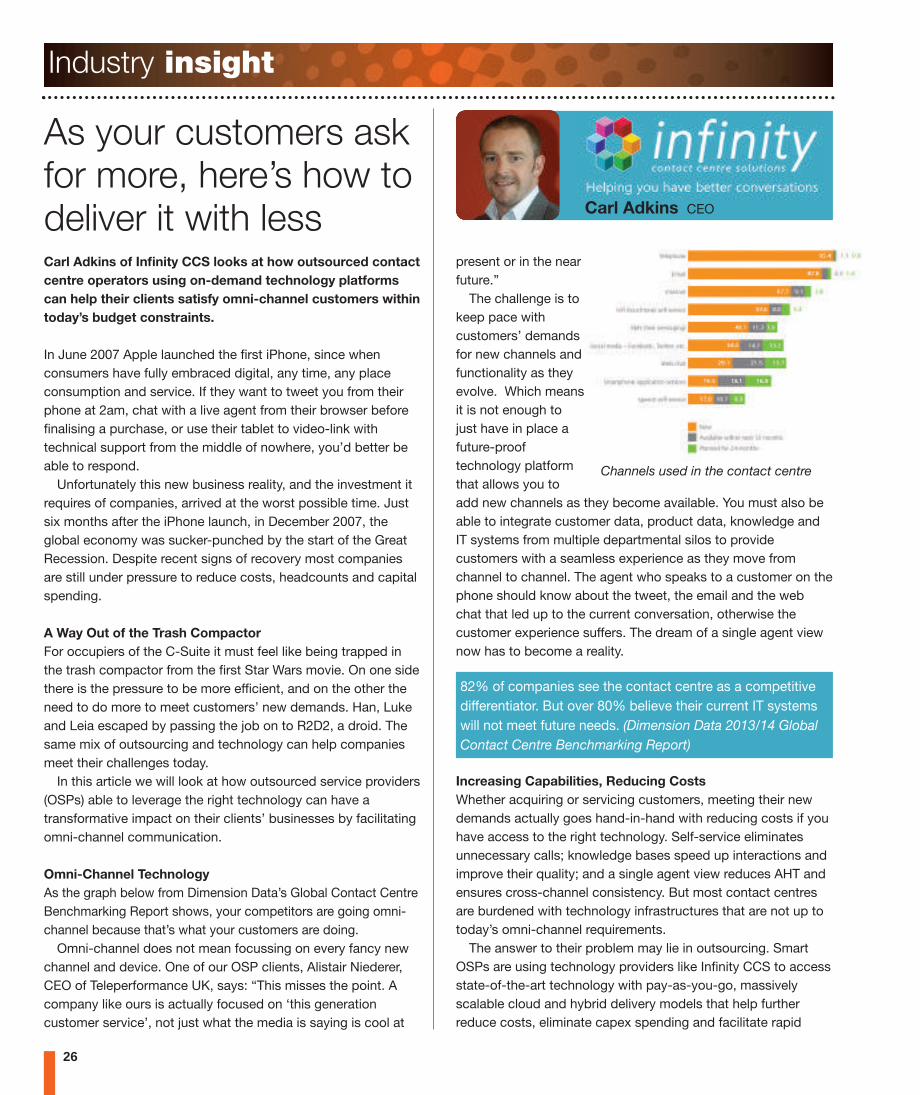

Omni-Channel TechnologyAs the graph below from Dimension Data’s Global Contact CentreBenchmarking Report shows, your competitors are going omni-channel because that’s what your customers are doing. Omni-channel does not mean focussing on every fancy new

channel and device. One of our OSP clients, Alistair Niederer,CEO of Teleperformance UK, says: “This misses the point. Acompany like ours is actually focused on ‘this generationcustomer service’, not just what the media is saying is cool at

present or in the nearfuture.” The challenge is tokeep pace withcustomers’ demandsfor new channels andfunctionality as theyevolve. Which meansit is not enough tojust have in place afuture-prooftechnology platformthat allows you toadd new channels as they become available. You must also beable to integrate customer data, product data, knowledge andIT systems from multiple departmental silos to providecustomers with a seamless experience as they move fromchannel to channel. The agent who speaks to a customer on thephone should know about the tweet, the email and the webchat that led up to the current conversation, otherwise thecustomer experience suffers. The dream of a single agent viewnow has to become a reality.

Increasing Capabilities, Reducing CostsWhether acquiring or servicing customers, meeting their newdemands actually goes hand-in-hand with reducing costs if youhave access to the right technology. Self-service eliminatesunnecessary calls; knowledge bases speed up interactions andimprove their quality; and a single agent view reduces AHT andensures cross-channel consistency. But most contact centresare burdened with technology infrastructures that are not up totoday’s omni-channel requirements. The answer to their problem may lie in outsourcing. SmartOSPs are using technology providers like Infinity CCS to accessstate-of-the-art technology with pay-as-you-go, massivelyscalable cloud and hybrid delivery models that help furtherreduce costs, eliminate capex spending and facilitate rapid

26

Carl Adkins CEO

As your customers askfor more, here’s how todeliver it with less

Channels used in the contact centre

82% of companies see the contact centre as a competitivedifferentiator. But over 80% believe their current IT systemswill not meet future needs. (Dimension Data 2013/14 GlobalContact Centre Benchmarking Report)

Industry insight

14�

testing and roll-out. Those OSPs can then pass on these

benefits to their clients.

The Transformation of OutsourcingWith access to the necessary technology, OSPs can now not

only manage but transform the functions they manage. Instead

of being given systems and a job and relying on economies of

scale to deliver savings, OSPs are now able to address

competitive business goals – service or acquire customers,

increase NPS or advocacy scores.

Our client David Turner, CEO of Webhelp UK, a leading OSP

in the customer experience management sector, says: “While

OSPs have typically been reluctant to invest in technology

ahead of client demand, many are now realising that their future

prosperity depends on their ability to manage multiple channels

and are investing in technology to support it.” They are doing

so, he says, to enable their clients to achieve “a step change in

customer management capability, as well as a real and

sustainable reduction in cost.”

In recent years OSPs have built robust technology

infrastructures capable of coping with the ever-more stringent

compliance and data security requirements placed upon them.

While no doubt a good thing, this can conflict with the need to

be responsive and nimble.

Partnering with a technology company like Infinity CCS – as

OSPs such as Teleperformance, Webhelp, HGS and Interact do

– brings them this flexibility. With our single agent view and on-

demand contact centre solutions, OSPs are able to satisfy their

clients’ demands for transformative services quickly, efficiently

and without overloading their internal IT teams.

Ask for More, for LessThe new business reality ushered in by customers’ adoption of

multiple digital channels and the Great Recession’s lingering

impact on budgets is not going away. The good news is

enlightened OSPs that have adopted on-demand technology

infrastructures can help any company meet these two

seemingly contradictory challenges head-on.

For more information contact Infinity CCS on

+44 (0)121 450 7830, email [email protected] or visit

www.infinityccs.com

With thanks to Dimension Data, Teleperformance UK,

Webhelp UK

Industry insight

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:03 Page 27

28

The outsourcing industry grewthroughout 2014 and all indicators arethere will be more growth in 2015, butwhat will this future growth look like andwhat lies ahead for the outsourcingindustry? Outsourcing Yearbook soughtthe views of the outsourcing analystcommunity…

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:04 Page 28

29

predictionsNOA Year book 2015 aw.qxp_ark 10/04/2015 10:04 Page 29

3�

Can you predict the future? No, neither can I! But what I can do

is analyse the thousands of conversations I have in a year about

outsourcing and make informed guesses, based on people’s

questions and concerns, on which of those conversations will

morph into trends over the next 12 months. If you look into the

present hard enough, it turns into the future…

The As-a-Service EconomyThe "As-a-Service Economy" is set to disrupt the traditional

outsourcing industry we know and love in a major way,

impacting on how service buyers receive services and how

service providers sell and deliver them.

Organisations are reviewing how they can maximise value in this

new era, be that through infrastructure-as-a-service, platform-

as-a-service or software-as-a-service. The NOA is supporting

HfS Research in a study in this area. We'll tell you how ready UK

companies are to embrace this new dawn, compared to their

European and American counterparts, at our Symposium on

24 June in London.

Outsourcing politicised 2015 being an election year, expect outsourcing to pop up on

the campaign trail, as well as in live TV debates - and get

roundly criticised by MPs who know very little about how it

works. Expect them to snipe about the supposed ‘creeping

privatisation’ of the NHS and condemnation of PFI initiatives,

while simultaneously offering no concrete plans on how to

improve infrastructure and services without private sector help.

And don’t expect any party to speak up in favour of outsourcing

- even though privately they might be in favour, when running in

the quinquennial national popularity contest, showing a

modicum of support for outsourcing might cost them a few vital

votes from the red-top reading White Van man.

Skills crunch to turn a cornerIf you believe all you read, every industry is in a skills crisis.

The outsourcing industry does need more skilled people on the

technology side and also the interpersonal, relationship

governance side. The BBC’s Make It Digital initiative, to boost

coding and digital creativity skills among young people, is a

very welcome move and most of the political parties are calling

for businesses to create more apprenticeships… I predict a rush

of new apprenticeships in late 2015, once the government is

decided and tax breaks for making apprentice jobs are

announced.

On the interpersonal skills side, there needs to be training for

young people on how to be client-facing, collaborative and have

a good customer service ethic - they could do a lot worse than

take on the NOA’s GCSE-level qualification. I also believe it’s

high time negotiation was taught in schools - negotiation is a

big part of life and kids should leave school with a good

understanding of the process. I’d like to see that form part of

any upcoming reviews of the national curriculum.

Cloud gets more expensive as it grows up2015 is touted as the year businesses stop fighting the cloud,

but the cloud will have its own battles to overcome if this is to

be its watershed year: towards the end of 2015, the world will

be right on the brink of producing more data than it can store.

In 2013, we generated around 600bn DVDs’ worth - by 2020,

it’s expected to be 7500bn, a whopping 44 zettabytes (source:

BBC news). This means the cloud has got to grow, therefore

we’ll need massive investments in data centres and new, cutting

edge technology that means a greater density of data can be

stored in a smaller space. Of course, there will be a fresh round

of security concerns, with firewalls beefed up accordingly. Will

all this make cloud solutions more expensive? Probably! Get a

price-fix built in before 2015 ends, folks.

Customer experience management will becomeincreasingly importantWe’re living in an age of peer reviews and social media, where

consumers call the shots. As more and more consumers get

confident with this power, we are going to see a situation where

heightening the customer experience across all touch-points is

at the forefront of every outsourcing buyers’ mind. If suppliers

don’t make the effort to noticeably improve the customers’

experience, questions will be asked around the value of their

work. I’m expecting many more companies to increase their

customer-centricity across various platforms, and I’m predicting

that many more companies will engage specialist social media

customer service agencies to up-skill in this area.

Robots might not mean bargainsSome say that robotics is to 2015 what offshore BPO was 10

years ago: that it will change the game forever… signifying a

Kerry Hallard CEO, NOA

Predictions

NOA Year book 2015 aw.qxp_ark 10/04/2015 10:04 Page 30

31

death knell to long-distance, low-cost offshoring. Yet offshoring

to India et al could become the PR-friendly moralist’s choice:

we might see a perception shift to ‘at least jobs are being

created somewhere’. Robotics certainly has an allure for anyone

wishing to save money on their BPO. But who will save the

money, really? I think there will be some interesting

conversations going on where BPO contracts are already live.

Will suppliers proactively switch from FTE models and pass the

savings on to their clients? Or will they simply reap the benefits

of their innovation themselves? I expect that will depend on the

length and quality of the individual relationship… and the calibre

and expertise of the buy-side team.

Impact sourcing to make a big impactWe know all about outsourcing to do well - now you can

outsource to do good. I predict a rise of impact sourcing in

2015 with partnerships set up in underdeveloped geo-locations,

with one eye on the bottom line and one on the bigger picture.

It’s not strictly CSR, which can be any type of philanthropic

activity - this is giving back by redirecting jobs where they are

needed most which, synergistically, happens to be cheap labour

pools. An emphatic win/win and the counterbalance to the rise

of the robots. I’m not sure this will take off at quite the same

pace as robotics, but it is an option that is well and truly on the

map in 2015 and that can only be a good thing.

The internet of everythingConnectivity ubiquity is coming on strong in 2015. Using a

smartphone to turn your central heating on during your

commute homewards will be just the start of it. Soon enough,

there will be fully smart homes, smart offices, smart cars: how

about a coffee percolator that orders its own refills, delivered by

a Google Car within the hour?

With a whole new range of connected devices being built, by

2017, the internet of things is predicted to be bigger than the

PC, tablet and smartphone markets combined, hence why

venture capital is flooding in for developers of IoT devices. I’ll

bet both cyber criminals and anti-malware companies are

rubbing their hands with glee; imagine your central heating

catching a virus and holding you to ransom before you can get

your radiators going. Taking the right steps to secure the new

digital ‘wild west’ will be absolutely paramount to it taking off.

Open book accounting will be all the rageWhat started a few years ago as an exercise in public sector

freedom of information is moving headlong into the private

sector: if the public sector can insist on knowing profit margins

etc., why can’t the private? More and more deals are being

negotiated with such clauses, even when contracts are already

underway. In 2015, anyone not making use of such contractual

obligations, in my opinion, isn’t governing their outsourcing

contracts in an optimised fashion. Many, many books will be

falling open all through this year.

Contracting for outcomes will become keyCould 2015 be the year the world gets wise to KPIs? Buyers still

love them, but intelligent governance reporting only has them as

a small snippet of information. They’re not much use - they

often create dysfunctional behaviour because, once you make a

measure a target, it’s no longer fit for purpose as a measure.

Contracting for outcomes is the way to avoid suppliers striving

to meet a target that doesn’t really mean anything - and that

way you only pay for what you really wanted in the first place.

Innovation will remain mysterious Innovation has always been tricky to pin down. All the

frameworks in the world won’t make a company automatically

innovative; you can’t just turn it on like a light switch. Leaders

will continue to covet it, suppliers will promise it, buyers will be

suspicious of paying upfront for it. Will we be any closer to a

magic formula to guarantee innovation in 2015? Possibly not,

but big innovations will happen, in companies with a culture

sufficiently open-minded to allow it. A lot of the time, they’re the

smaller players, and when they have an eye-catching innovative

success, they get acquired by the behemoths and bring a bit of

that culture with them. So I predict lots of innovation, lots of

acquisition and maybe a few new models such as innovation-

as-a-service or, more aptly, the results of innovation-as-service.

That’s what buyers want, so suppliers will have to work out a

way to sell it to them.

Standards to raise the bar 2015 will be a year for suppliers and buyers to assess their

outsourcing maturity levels against global benchmarks, with the

best getting accredited for their excellence.

Thanks to the hard work of our very own Adrian Quayle

(amongst others), late 2014 saw the rubberstamping of ISO

37500, a global standard in outsourcing. With the outsourcing

market predicted to keep on growing, the more people who