The presentation is a property of Vinod Kothari Consultants Private Limited. No part of it can be copied, reproduced or distributed in any manner, without explicit prior permission.

In case of linking, please do give credit and full link

We are a team of consultants, advisors & qualified professionals having recently completed 25 years of practice.

Our Organization’s Credo:

Focus on capabilities; opportunities follow

Basic regulatory framework on NBFCs

Classification of NBFCs in terms of applicability of various regulations

Deposit taking NBFC

Prudential norms for NBFC-D

Corporate Governance norms

Other instructions applicable to all

NBFCs

Systemically Important Non Deposit taking

NBFC

Prudential norms for NBFC-ND-SI

Corporate Governance norms

Misc instructions for ND-SI

Other instructions applicable to all

NBFCs

Non Systemically Important Non Deposit

taking NBFC

Prudential norms for NBFC-ND-Non-

SI

Other instructions applicable to all

NBFCs

Applicability of prudential norms

Is it an NBFC?

Is it holding public deposits?

Is it having public funds?

Asset size < Rs. 500 crores?

Yes

Yes

No

Yes

No

Is it a company?

Asset size => Rs. 500 crores?

Non Banking Financial (Deposit Accepting or Holding) Prudential Norms (Reserve Bank) Directions, 2007 to

apply.

Non Systemically Important Non Banking Financial (Non Deposit Accepting or Holding) Prudential Norms

(Reserve Bank) Directions, 2015 to apply

Systemically Important Non Banking Financial (Non Deposit Accepting or Holding) Prudential Norms

(Reserve Bank) Directions, 2015 to apply

Only Clause 15 of Non Systemically Important Non Banking Financial (Non Deposit Accepting or Holding) Prudential Norms (Reserve Bank) Directions, 2015 to

apply

Yes

No

Yes

Yes

Both Income and Asset criteria to be satisfied

Matters to be checked for all NBFCs

Maintenance of minimum NOF

All NBFCs, irrespective of their date of existence are required to attain a minimum NOF of Rs. 2 crores. Presently the same was applicable for NBFCs registered with the RBI

from 21st April, 1999. For NBFCs in existence on before 21st April, 1999, the NOF had been

retained at Rs. 25 lakhs.

Existing NBFCs with NOF of less than 2 crores are required to submit a statutory auditor's certificate certifying compliance to the revised levels at the end of each of the two financial years as given in the adjacent table.

Minimum NOF of Rs. 200 lakh to be attained by the end of March 2017, as per the milestones given below: Rs. 100 lakh by the end of March 2016 Rs. 200 lakh by the end of March 2017

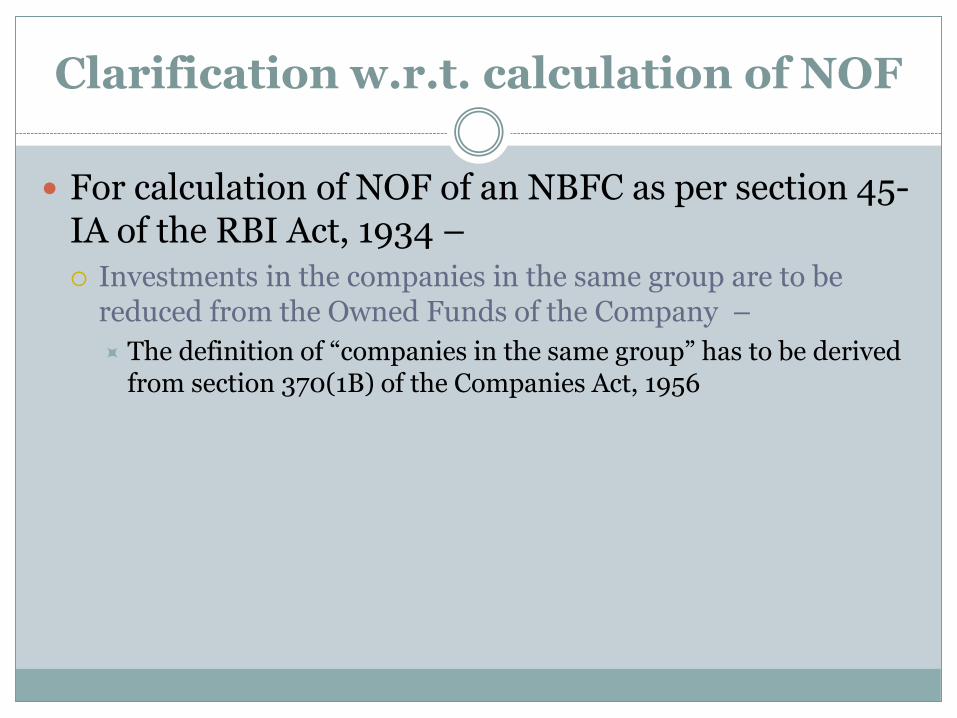

Clarification w.r.t. calculation of NOF

For calculation of NOF of an NBFC as per section 45-IA of the RBI Act, 1934 –

Investments in the companies in the same group are to be reduced from the Owned Funds of the Company –

The definition of “companies in the same group” has to be derived from section 370(1B) of the Companies Act, 1956

Aggregation of the total assets of NBFCs in a group in order to determine the

systemic importance of an NBFC

Aggregation of assets of Multiple NBFCs in the same group

Was a part of the 10th November, 2014 circular

Was dropped from the final notifications of 27th

March, 2015

Again re-instated in the Master Circular –Miscellaneous Instructions to all NBFCs

Multiple NBFCs in the same Group

For ascertaining asset size of NBFCs-ND-SI, the total assets ofNBFCs in a group (i.e. part of a corporate group or are floated bya common set of promoters), including NBFCs-D, if any, will beaggregated. That is, asset size will be clubbed as “group” level

Accordingly consolidation will fall within the asset sizes of the twocategories viz. NBFC-ND (with asset size of less than Rs, 500 crores); and NBFC-ND-SI (with asset size of Rs. 500 crore or more).

Regulations as applicable to the two categories will be applicable toeach of the NBFC-ND within the group, irrespective of itsindividual asset size.

For NBFC-D, all applicable regulations would apply.

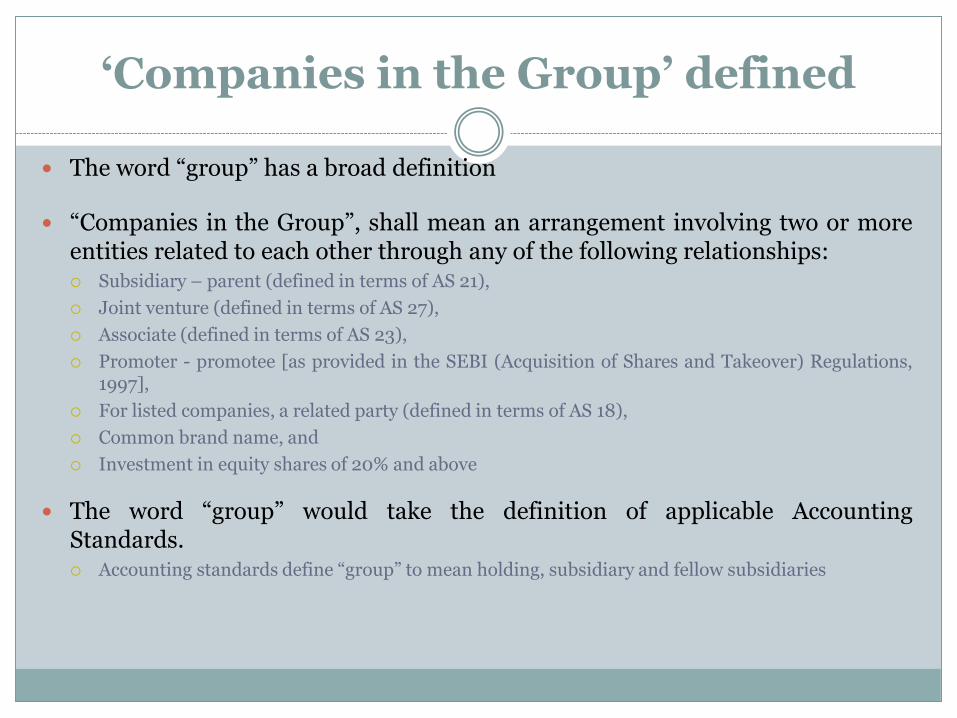

‘Companies in the Group’ defined

The word “group” has a broad definition

“Companies in the Group”, shall mean an arrangement involving two or moreentities related to each other through any of the following relationships: Subsidiary – parent (defined in terms of AS 21),

Joint venture (defined in terms of AS 27),

Associate (defined in terms of AS 23),

Promoter - promotee [as provided in the SEBI (Acquisition of Shares and Takeover) Regulations,1997],

For listed companies, a related party (defined in terms of AS 18),

Common brand name, and

Investment in equity shares of 20% and above

The word “group” would take the definition of applicable AccountingStandards. Accounting standards define “group” to mean holding, subsidiary and fellow subsidiaries

Compliance checks for the NBFC-ND-Non SIs

Important provisions applicable to NBFC-ND-Non SI

Regulations with respect to Income Recognition, Asset Classification and Provisioning Requirements

Submission of a certificate from Statutory Auditors

Requirements with respect to maintenance of CRAR [only a few classes of companies]

Applicability of leverage ratio – 7 times

Provisions pertaining to lending against gold

Provisions pertaining to lending against shares

Credit concentration limits (only which are held by NOFHC)

Restrictions with respect to opening of branches

Norms for restructuring of advances

Provisions pertaining to flexible structuring of long term project loans to Infrastructure and Core Industries

Cannot be a partner of a firm/ LLP

Submission of Branch Info Return

For the purpose of “Framework for Revitalizing Distressed Assets in the Economy” –Notified NBFCs would mean those NBFCs having net assets of Rs. 100 crores or above

This would however include all NBFC Factors

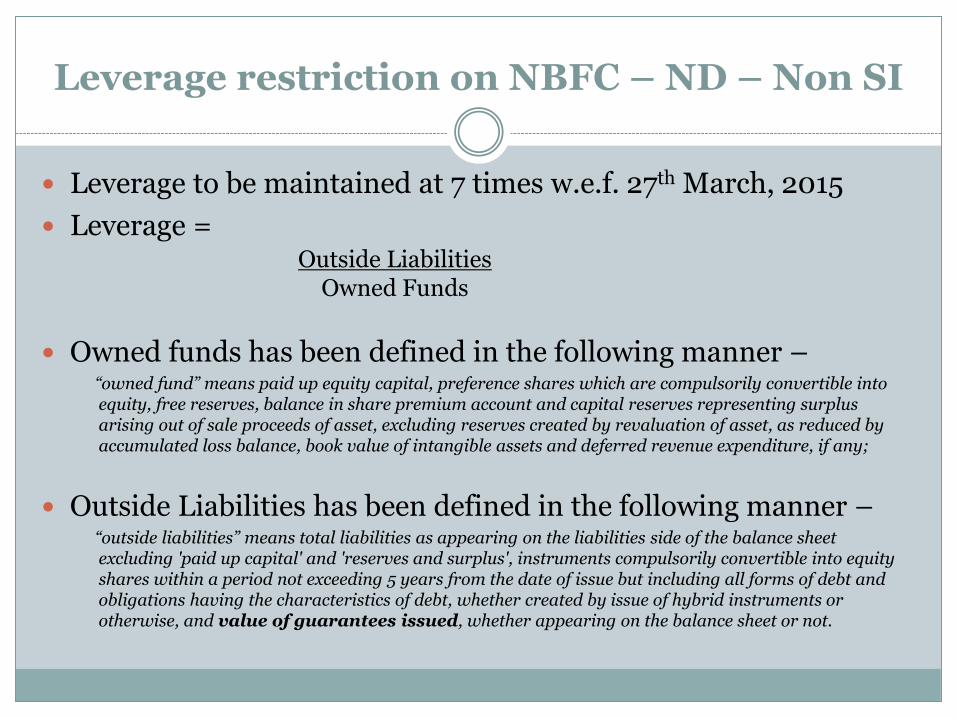

Leverage restriction on NBFC – ND – Non SI

Leverage to be maintained at 7 times w.e.f. 27th March, 2015

Leverage =

Owned funds has been defined in the following manner –“owned fund” means paid up equity capital, preference shares which are compulsorily convertible into equity, free reserves, balance in share premium account and capital reserves representing surplus arising out of sale proceeds of asset, excluding reserves created by revaluation of asset, as reduced by accumulated loss balance, book value of intangible assets and deferred revenue expenditure, if any;

Outside Liabilities has been defined in the following manner –“outside liabilities” means total liabilities as appearing on the liabilities side of the balance sheet excluding 'paid up capital' and 'reserves and surplus', instruments compulsorily convertible into equity shares within a period not exceeding 5 years from the date of issue but including all forms of debt and obligations having the characteristics of debt, whether created by issue of hybrid instruments or otherwise, and value of guarantees issued, whether appearing on the balance sheet or not.

Outside LiabilitiesOwned Funds

Exemptions from the provisions of the Non SI regulations

These regulations, save and except Para 15 [Annual certification by Statutory Auditors] ,will not applicable to a Non SI not accepting/ holding public funds

These regulations, save and except para 26 [Information with respect to change of address, directors, auditors, etc. to be submitted to the RBI ]shall not be applicable to Government Companies not accepting/ holding public funds

These regulations shall not apply to a CIC, not being a CIC-SI

Para 15, 16 and 17 shall not apply to CIC SI

Para 8,9 and 17 shall not apply to MFIs

Definition of public funds

funds raised directly or indirectly through public deposits, commercial papers, debentures, inter-corporate deposits and bank finance but excludes funds raised by issue of instruments compulsorily convertible into equity shares within a period not exceeding 5 years from the date of issue

RBI’s FAQs on NBFCs clarifies “indirect receipts of public funds” to be –

indirect receipt of public funds means funds received not directly but through associates and group entities which have access to public funds.

Compliance checks for the NBFC-ND-SIs

Meaning of NBFC-ND-SI changed

Earlier non-deposit accepting NBFCs with asset size of Rs. 100 crores or more were classified as NBFC-ND-SI.

Henceforth, NBFCs-ND which have asset size of Rs. 500 crore and above as per the last audited balance sheet would be classified as NBFC-ND-SI for the purpose of administering prudential norms.

Rs 500 crores is a reasonably big size

Expectedly, a whole lot of companies will go out of complying with all or some of the prudential norms requirement

NBFC- ND SIDetails of requirements applicable 1/6

Income recognition requirements – Income to be recognised based on recognised accounting standards

Income on NPAs should be recognised on cash basis, any income recognised before the asset became NPA remaining unrealised shall be reversed

Income from dividend on shares and mutual funds shall be recognised on cash basis

Income from bonds and debentures of corporate bodies and from Government securities/ bonds may be recognised on accrual basis

Income from securities of corporate bodies or PSUs, the payment of interest of repayment of principal of which has been guaranteed by the Central Government or State Government, may be recognised on accrual basis

Details of requirements applicable 2/6

Accounting Standards – AS and Guidance Notes issued by the ICAI to be followed

Where the provisions of AS are inconsistent with the directions – Directions to prevail

Accounting of investments – The Board of Directors of every company to frame investment policy

It should contain the criteria to classify current and long term investments Classification of current and long term investments should be done at the time of making the

investment

The quoted investments should be group into certain classes, as specified in the Directions, for the purpose of valuation Quoted instruments to be valued at cost or market value, whichever is lower

Unquoted investments to be valued at cost or break up value, whichever is lower Unquoted preference shares, in the nature of current investments, shall be valued at

cost or face value, whichever is lower Investments in unquoted Govt. Securities or Govt. Guaranteed bonds shall be the carrying

cost. Unquoted units of mutual funds in the nature of current investments to be done based

on the NAV Commercial papers to be valued at the carrying cost Long term investments shall be valued in accordance with AS – 13, issued by the ICAI

Details of requirements applicable 3/6

Policy on Demand/ Call Loans Board of Directors to frame a policy on Demand/ Call Loans

Cut off date within which the repayment of demand or call loan shall be demanded or called up should be mentioned in the policy

Rate of interest to be charged should be laid down in the policy

Asset Classification – Standard Assets Sub-standard Assets Doubtful Assets Loss Assets

Provisioning requirements – Discussed earlier in this presentation

Disclosure in balance sheet – Provisions for bad and doubtful debts Provisions for depreciation in investments

Schedule to the balance sheet – Company to append to its balance sheet a schedule to be drawn in the format prescribed in

Annex 1 of the Directions

Details of requirements applicable 4/6

Submission of certificate from Statutory Auditor to the RBI –

Stating that it is engaged in the business non banking financial activity and holds the CoR under section 45-IA and is eligible to hold it

Indicating the asset/ income pattern of the Company for making it eligible for classification as Asset Finance Company, Investment Company or Loan Company

Within 1 month from the date of finalization of the Balance Sheet and in any case not later than 30th December of that year.

Details of requirements applicable 5/6

Capital Adequacy Requirements – CRAR of 15% (Applicable only to Non-SI, MFI & IFC)

Tier I should not be less than 10%, in case of an IFC

Tier II in case of NBFC – MFI should not exceed Tier I

Lending against gold – Separate set of directions governing gold lending

Information with respect to change of address, directors, auditors etc – The company to inform the RBI the following within 1 month from the date of

occurrence – the complete postal address, telephone number/s and fax number/s of the

registered/corporate office

the names and residential addresses of the directors of the company;

the names and the official designations of its principal officers;

the names and office address of the auditors of the company; and

the specimen signatures of the officers authorised to sign on behalf of the company

Details of requirements applicable 6/6

Norms for restructuring of advances –

As per the guidelines dated 23rd January, 2014

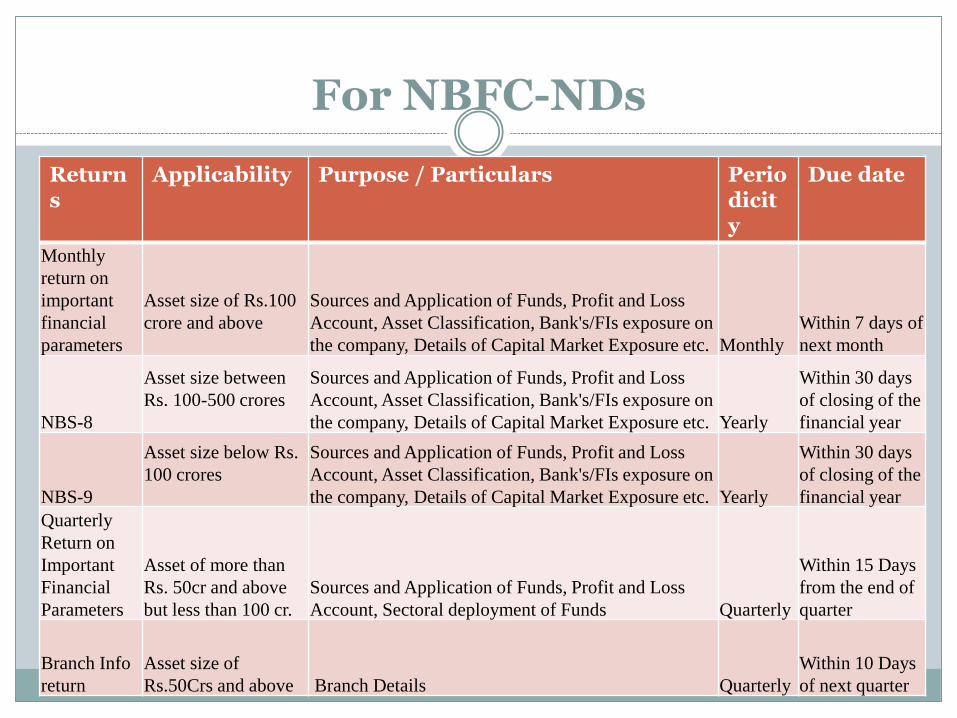

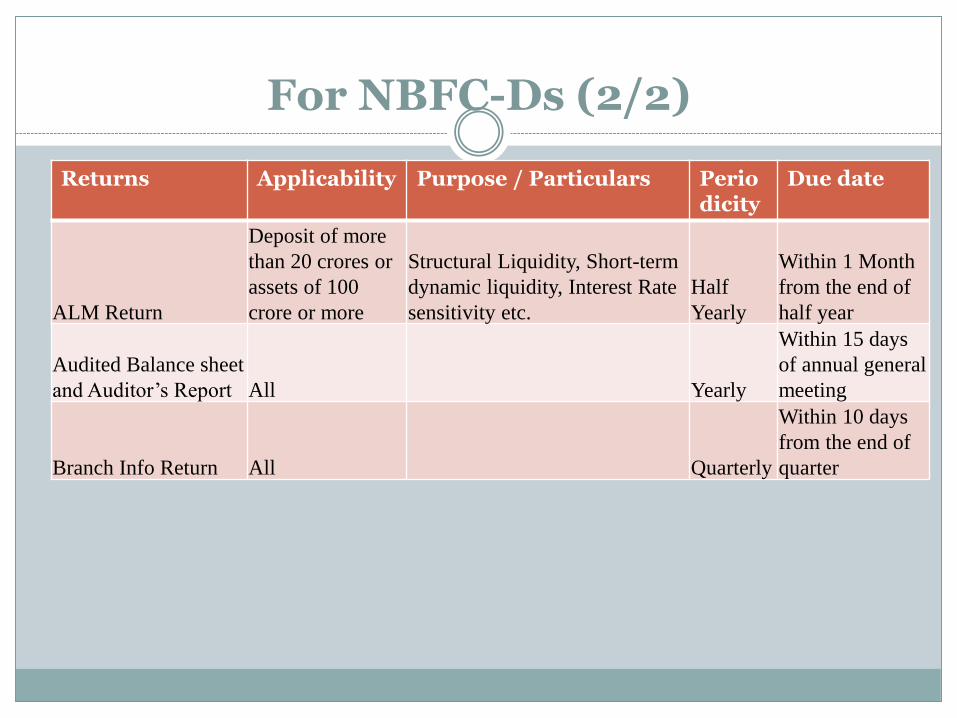

Submission of “Branch Info” Return –

All NBFCs having total assets of more than Rs. 50 crores to submit Branch Information on quarterly basis within 10 days from the expiry of relative quarter

Prudential Regulations for NBFCs-D and NBFCs-ND-SI

The following categories of asset classification has been provided: Determination of NPA for Lease Rental and Hire-Purchase Assets

Determination of NPA for other than Lease Rental and Hire-Purchase Assets

Determination of sub-standard asset for all loan and hire-purchase and lease assets

Determination of doubtful asset for all loan and hire-purchase and lease assets

For the existing loans, a one-time adjustment of the repayment schedule, which shall not amount to restructuring will, however, be permitted.

Change in provisioning norms – for standard assets

Revised to 0.40% for NBFCs-ND-SI and for all NBFCs-D;

Presently it is at 0.25% of the outstanding.

This change is in line with that of banks

The compliance to the revised norm will be phased in as given below:

0.30% by the end of March 2016

0.35% by the end of March 2017

0.40% by the end of March 2018

Change in asset classification norms

Time period for treating an as asset to be NPA has been reduced to 3 months

The accounting cycle has to be adjusted in the following manner – For NPA -

5 months for FY 2015-16

4 months for FY 2016-17

3 months for FY 2018-19

For doubtful assets –

16 months for FY 2015-16

14 months for FY 2016-17

12 months from FY 2017-18

Changes in credit/ investment concentration norms

Credit/ investment concentration restriction:

Lending –

Single borrower – 15%

Single group of borrowers – 25%

Investing in shares –

Single party – 15%

Single group of parties – 25%

Lending to/ Investing in –

Single party – 25%

Single group of parties – 40%

Exposures in group companies, to the extent that the same has been reduced from owned funds to arrive at net owned funds, shall not be considered for the purpose of concentration norms

Changes in the capital adequacy requirement

Tier 1 capital requirement increases to 8.5% on 31st

March 2016, and 10% in 31st March 2017

Basel II or Basel III definitions are seemingly not being applied to NBFCs

Core Investment Companies

Core Investment Company

CIC defined as:

not less than 90% of their assets were in investments in shares, debt, loans in group companies for the purpose of holding stake in the investee companies

Atleast 60% in equity of group companies

not trading in these shares except for block sale (to dilute or divest holding)

not carrying on any other financial activities,

not holding / accepting public deposits

Overview of CIC

Regulatory framework for CICs-SI

Systemically important CIC

Company having asset not less than Rs. 100 crore

Either individually or with other group CICs

Which raises or holds public deposits Capital requirements Minimum Capital Ratio to be maintained at all times Adjusted Net Worth shall not be less than 30% of its

aggregate risk weighted assets on balance sheet and riskadjusted value of off balance sheet items as on the date ofthe last audited balance sheet.

Regulatory framework for CICs-SI

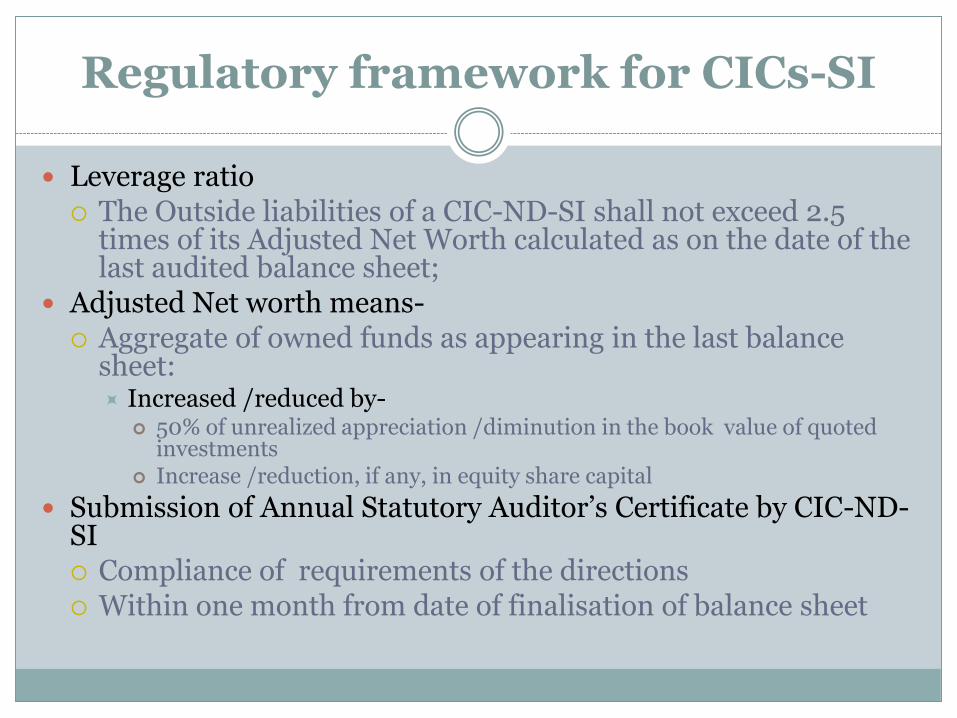

Leverage ratio The Outside liabilities of a CIC-ND-SI shall not exceed 2.5

times of its Adjusted Net Worth calculated as on the date of the last audited balance sheet;

Adjusted Net worth means- Aggregate of owned funds as appearing in the last balance

sheet: Increased /reduced by-

50% of unrealized appreciation /diminution in the book value of quoted investments

Increase /reduction, if any, in equity share capital

Submission of Annual Statutory Auditor’s Certificate by CIC-ND-SI Compliance of requirements of the directions Within one month from date of finalisation of balance sheet

Exemptions

CICs exempted from:

maintenance of statutory minimum NOF

requirements of Prudential norms for non-deposit accepting NBFC.

CICs-ND-SI required to submit an annual certificatefrom their statutory auditors regarding compliancewith the Directions

Regulations applicable to CICsWhether NBFC?

Principal business investments?

Qualifies to be a CIC?

Net assets >Rs. 100 crores?

Co has public funds?

Net assets >= 500 crores?

Non-Systemically Important Non Banking Financial (Non-Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2015, except Clauses 15, 16, 17, will be applicable

Systemically Important Non Banking Financial (Non-Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2015, except Clauses 15, 16, 24, will be applicable

The company is not required to obtain registration with the RBI and prudential norms will not be applicable

The company is not required to obtain registration with the RBI and prudential norms will not be applicable

It is an Investment Company and regulations applicable to such companies will become applicable

Yes

Yes

Yes

Yes

Yes

No

No

No

No

Acquisition/ Transfer of control over NBFCs

Definition of “control”

Meaning of control to be derived from SEBI (SAST) Regulations, 2011

As defined in SEBI (SAST) Regulations, 2011 –

“control” includes the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner

Change in control

Prior RBI approval required – Any takeover or acquisition of an NBFC, may or may not result in change

of management Any change in the shareholding of an NBFC, including progressive

increases over time, which would result in acquisition / transfer of shareholding of 26 per cent or more of the paid up equity capital of the NBFC prior approval not required in case shareholding goes beyond 26% due to

buyback of shares / reduction in capital where it has approval of a competent Court. The same is to be reported to the Bank not later than one month from its

occurrence;

Any change in the management of the NBFC which would result in change in more than 30 per cent of the directors, excluding independent directors.

Prior approval not required in case a directors gets re-elected on retirement by rotation

Change in control cont.

Whether transfer within the promoter group will also require prior approval?

Yes. Prior approval would be required in all cases of acquisition/ transfer of shareholding of 26 per cent or more of the paid up equity capital of an NBFC.

In case of intra-group transfers, NBFCs shall submit an application, on the company letter head, for obtaining prior approval of the Bank.

Based on the application of the NBFC, it would be decided, on a case to case basis, whether the NBFC requires to submit the prescribed documents.

This was clarified by way of FAQs.

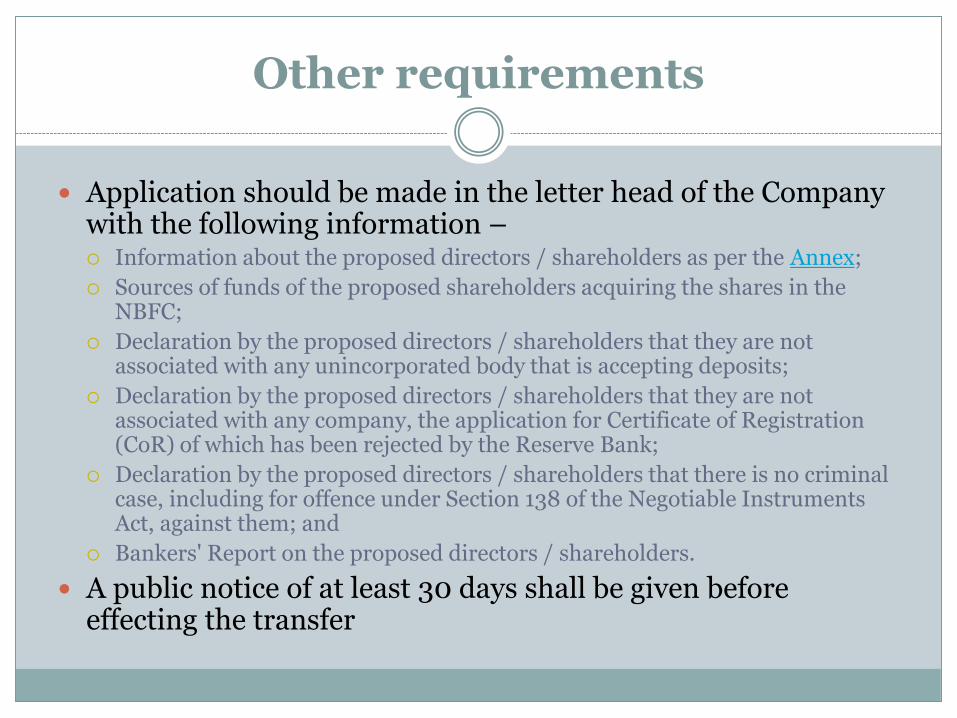

Other requirements

Application should be made in the letter head of the Company with the following information – Information about the proposed directors / shareholders as per the Annex;

Sources of funds of the proposed shareholders acquiring the shares in the NBFC;

Declaration by the proposed directors / shareholders that they are not associated with any unincorporated body that is accepting deposits;

Declaration by the proposed directors / shareholders that they are not associated with any company, the application for Certificate of Registration (CoR) of which has been rejected by the Reserve Bank;

Declaration by the proposed directors / shareholders that there is no criminal case, including for offence under Section 138 of the Negotiable Instruments Act, against them; and

Bankers' Report on the proposed directors / shareholders.

A public notice of at least 30 days shall be given before effecting the transfer

Returns Purpose / Particulars Periodicity Due date

CTR - Cash

Transaction

Reporting

Individual transactions below rupees fifty

thousand may not be included. Cash

transaction reporting by branches/offices of

NBFCs to their Principal Officer should

invariably be submitted on monthly basis

(not on fortnightly basis) and the Principal

Officer, in turn, should ensure to submit CTR

for every month to FIU-IND within the

prescribed time schedule Monthly

15th of the

succeeding

month

STR -

Suspicious

Transaction

Reporting

The Principal Officer should record his reasons for treating any transaction or a series of transactions as suspicious.

within 7 days

of arriving at

a conclusion

that any

transaction are

of suspicious

nature

Fraud Reporting

Returns Purpose / Particulars Periodicity

Due date

FMR-1

Report on Actual or Suspected

Frauds in NBFCs

Within 3 weeks (i.e.

21 days ) from date of

detection

FMR-2 Report on fraud outstanding Quarterly

within 15 days of the

end of the quarter

FMR-3

Case-wise quarterly progress reports

on frauds involving Rs. 1 lakh and

above Quarterly

within 15 days of the

end of the quarter

Snapshot of applicability of various requirements to the different classes of NBFCs

NBFC-

ND with

no PF

NBFC-

ND with

PF

CIC CIC-SI

with

Asset

100 -

500 crs

CIC-SI

with

Assets >

500 crs

NBFC-

ND-SI

with PF

NBFC-

ND-SI

without

PF

Concentration

Norms

Not

Applicable

Not

Applicable

Not

Applicable

Not

Applicable

Not

Applicable

Applicable Applicable

Capital

Adequacy

Not

Applicable

Not

Applicable

Not

Applicable

Respective

Directions

Respective

Directions

Applicable Applicable

Provisioning

norms

Not

Applicable

Applicable Not

Applicable

Not

Applicable

Applicable Applicable Applicable

Asset

Classification

Not

Applicable

Applicable Not

Applicable

Not

Applicable

Applicable Applicable Applicable

Statutory

Auditor

Certificate

Applicable Applicable Not

Applicable

Applicable Applicable Applicable Applicable

Leverage Ratio Not

Applicable

7 times Not

Applicable

2.5 times 2.5 times Not

Applicable

Not

Applicable

Corporate

Governance

Norms

Not

Applicable

Not

Applicable

Not

Applicable

Not

Applicable

Not

Applicable

Applicable Applicable

NBFCs Auditors Report Directions

Matters to be reported for all NBFCs

Whether the company is engaged in the business of non-banking financial institution and whether it has obtained a Certificate of Registration (CoR) from the Bank

In the case of a company holding CoR issued by the Bank, whether that company is entitled to continue to hold such CoR in terms of its asset/income pattern as on March 31 of the applicable year.

Whether the NBFC has complied with the following – the provisions of Chapter III B of Reserve Bank of India Act, 1934 (Act 2 of 1934);

or the Non-Banking Financial Companies Acceptance of Public Deposits (Reserve

Bank) Directions, 1998; or Non-Banking Financial (Deposit Accepting or Holding) Companies Prudential

Norms (Reserve Bank) Directions, 2007; or Systemically Important Non-Banking Financial (Non-Deposit Accepting or

Holding) Companies Prudential Norms (Reserve Bank) Directions, 2015 and Non-Systemically Important Non-Banking Financial (Non-Deposit Accepting or

Whether BOD has passed a resolution for not accepting public deposits

Whether the NBFC has accepted any public deposit during the year

Whether the NBFC has complied with prudential norms

For NBFC-ND-SI- Whether the CRAR reported in NBS 7 has been calculated properly

and whether such ratio is in compliance with minimum CRAR

Whether the company has furnished to the Bank the annual statement of capital funds, risk assets/exposures and risk asset ratio (NBS-7) within the stipulated period

Draft Companies (Auditor’s Report) Order, 2016

Yet to come into force

Whether the same will be applicable to NBFCs once implemented?

The Order shall be applicable to all except the following classes of companies – Banking companies Insurance companies Section 8 company OPCs and Small Companies A private limited company, not being a subsidiary or holding of a public

company, having a paid up capital and reserves and surplus not more than rupees one crore as

at the balance sheet date and which does not have total borrowings exceeding rupees one crore from any

bank or financial institution at any point of time during the financial year and which does not have a total revenue as defined in Scheduled III to the

Companies Act, 2013 exceeding rupees ten crore during the financial year as per the financial statements.

Therefore, unless the NBFC satisfies any of the above conditions, it will be covered under the same

Matters that might be of relevance for NBFCs

Loans granted by NBFCs to companies, firms or other parties covered by clause (76) of Section 2 of the Companies Act, 2013. Whether the terms of the same are prejudicial to the interest of the company; Whether receipt of the principal and interest amount is paid on the such loans regularly; Where the overdue amount is more than Rs. 5 lakhs, whether the company has taken

necessary steps to recover the same.

In respect of loans, investments and guarantees by the NBFC, whether provisions of Section 185 and 186 of the Companies Act, 2013 have been complied with.

Whether the company has defaulted in repayment of dues to a financial institution or bank or debenture holders? If yes, the period and amount of default to be reported.

Whether the proceeds of the term loans/ public issue/ follow on offer have been utilised for the specified end use.

Whether the requirements under section 42 of the CA, 2013 have been complied with for issue shares and partly or fully convertible debentures under private placement or preferential allotment basis? Whether the proceeds have been utilised for the specified end use?