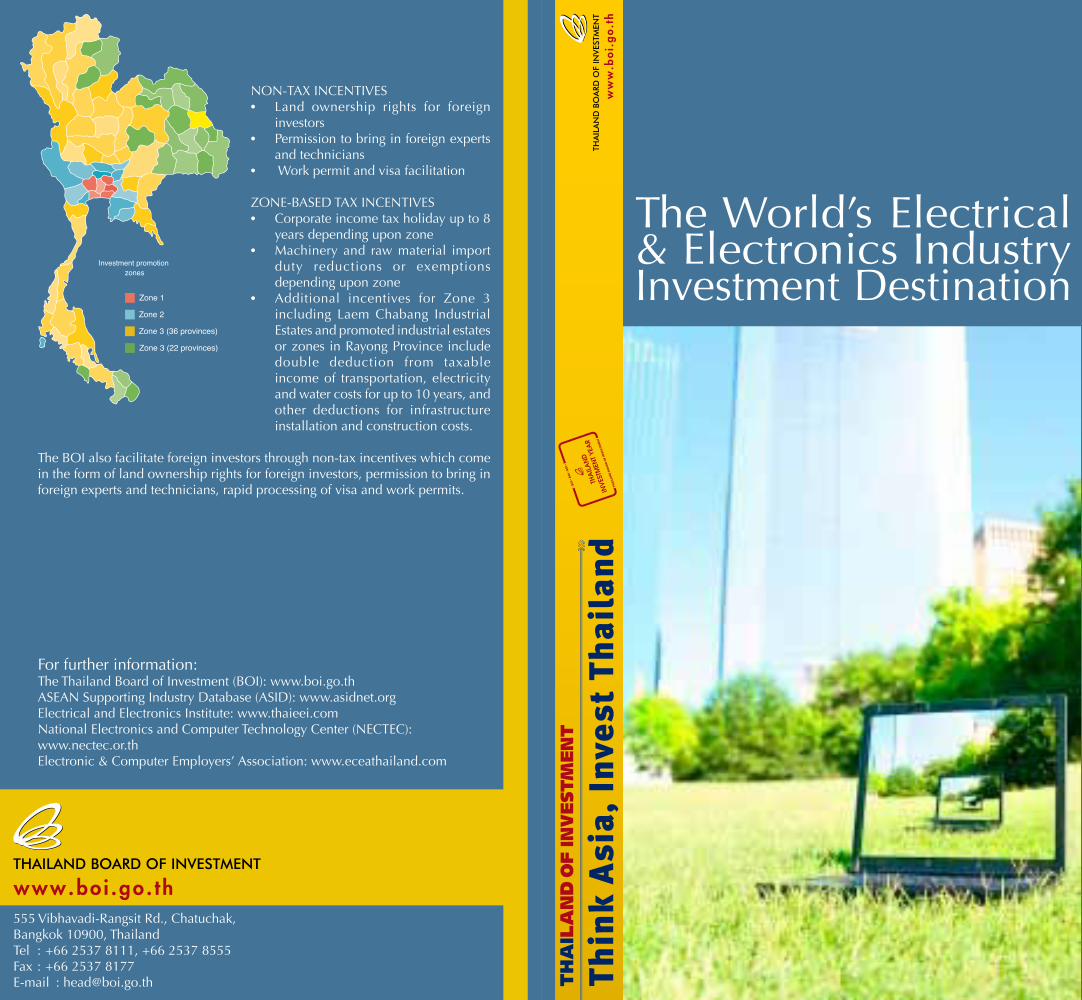

The World’s Electrical & Electronics Industry Investment Destination THAILAND 555 Vibhavadi-Rangsit Rd., Chatuchak, Bangkok 10900, Thailand Tel : +66 2537 8111, +66 2537 8555 Fax : +66 2537 8177 E-mail : [email protected]Zone 1 Zone 3 (22 provinces) Zone 3 (36 provinces) Zone 2 Investment promotion zones NON-TAX INCENTIVES • Land ownership rights for foreign investors • Permission to bring in foreign experts and technicians • Work permit and visa facilitation ZONE-BASED TAX INCENTIVES • Corporate income tax holiday up to 8 years depending upon zone • Machinery and raw material import duty reductions or exemptions depending upon zone • Additional incentives for Zone 3 including Laem Chabang Industrial Estates and promoted industrial estates or zones in Rayong Province include double deduction from taxable income of transportation, electricity and water costs for up to 10 years, and other deductions for infrastructure installation and construction costs. For further information: The Thailand Board of Investment (BOI): www.boi.go.th ASEAN Supporting Industry Database (ASID): www.asidnet.org Electrical and Electronics Institute: www.thaieei.com National Electronics and Computer Technology Center (NECTEC): www.nectec.or.th Electronic & Computer Employers’ Association: www.eceathailand.com The BOI also facilitate foreign investors through non-tax incentives which come in the form of land ownership rights for foreign investors, permission to bring in foreign experts and technicians, rapid processing of visa and work permits.

Transcript

The World’s Electrical & Electronics Industry Investment Destination

NON-TAX INCENTIVES• Land ownership rights for foreign

investors• Permission to bring in foreign experts

and technicians• Work permit and visa facilitation

ZONE-BASED TAX INCENTIVES• Corporate income tax holiday up to 8

years depending upon zone• Machinery and raw material import

duty reductions or exemptions depending upon zone

• Additional incentives for Zone 3 including Laem Chabang Industrial Estates and promoted industrial estates or zones in Rayong Province include double deduction from taxable income of transportation, electricity and water costs for up to 10 years, and other deductions for infrastructure installation and construction costs.

For further information:The Thailand Board of Investment (BOI): www.boi.go.thASEAN Supporting Industry Database (ASID): www.asidnet.org Electrical and Electronics Institute: www.thaieei.com National Electronics and Computer Technology Center (NECTEC): www.nectec.or.thElectronic & Computer Employers’ Association: www.eceathailand.com

The BOI also facilitate foreign investors through non-tax incentives which come in the form of land ownership rights for foreign investors, permission to bring in foreign experts and technicians, rapid processing of visa and work permits.

Thailand’s electrical and electronics industry has been experiencing strong and steady growth for more than 25 years, and has played a significant role in the nation’s economy as an export earner. The government’s proactive investment policies and designation of the electrical and electronics industry as a priority have encouraged the successful development of the industry and created an attractive investment environment for multinational companies.

In 2008, the electrical and electronics industry contributed almost 30% of Thailand’s annual export revenues, generating US$ 47 billion. Major export destinations were the Association of South East Asian Nations (ASEAN) (16%), the EU (16%), the US (15%), China (15%), Japan (12%), and the Middle East (4%). The Federation of Thailand Industry has set a goal for the electrical and electronics industry’s exports to grow to US$ 50 billion by the year 2010.

0

10,000

20,000

30,000

40,000

50,000Million U

S$

20032004

20052006

20072008

Year

Electronics Electrical Appliance

Thailand is ASEAN’s largest electrical appliance production base as well as the world’s 2nd largest producer of air conditioning units and 4th largest producer of refrigerators. Thailand’s 2008 electrical appliance exports were valued at US$ 17.8 billion, 9% higher than the previous year. From 2007 to 2008, imports increased 15% to a total of US$ 14.5 billion.

The Thai electrical appliance industry is expected to continue to grow steadily. Virtually all of the major manufacturers of electrical appliances have located in Thailand, attracted by its robust manufacturing base and excellent hard infrastructure. Thailand is truly a leader in this industry – not only in the region, but also in the world. The country has become ASEAN’s hub for white goods production for Japanese, Korean, European and American multinational companies.

ELECTRICAL APPLIANCE INDUSTRY

Thailand’s Electrical and Electronics Industry Exports

Source: Thai Electrical and Electronics Institute

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Million U

S$

20032004

20052006

20072008

Year

Export Import

The Thai electrical appliance industry is currently comprised of approximately 800 factories. Most of the major players in this industry are foreign or joint-venture companies. 43% of the total companies are Japanese, including Sony, Hitachi, Mitsubishi, and Panasonic. In addit ion, many world-class European, American and Korean electrical appliance manufacturers, including Electrolux, Schneider

0

500

1,000

1,500

2,000

2,500

3,000

Million U

S$

Digital Cams & Video Cam Recorders

Refrigerators

Air Conditioners

2004 2004 2006 2007 2008

Electric, Honeywell Electronic Materials, Emerson Electric, Carrier, LG and Samsung, also use Thailand as production base for their exports. Recently, Fisher&Paykel, a New Zealand’s big electrical appliance producer, has moved its production base from New Zealand to Thailand since end of 2007.

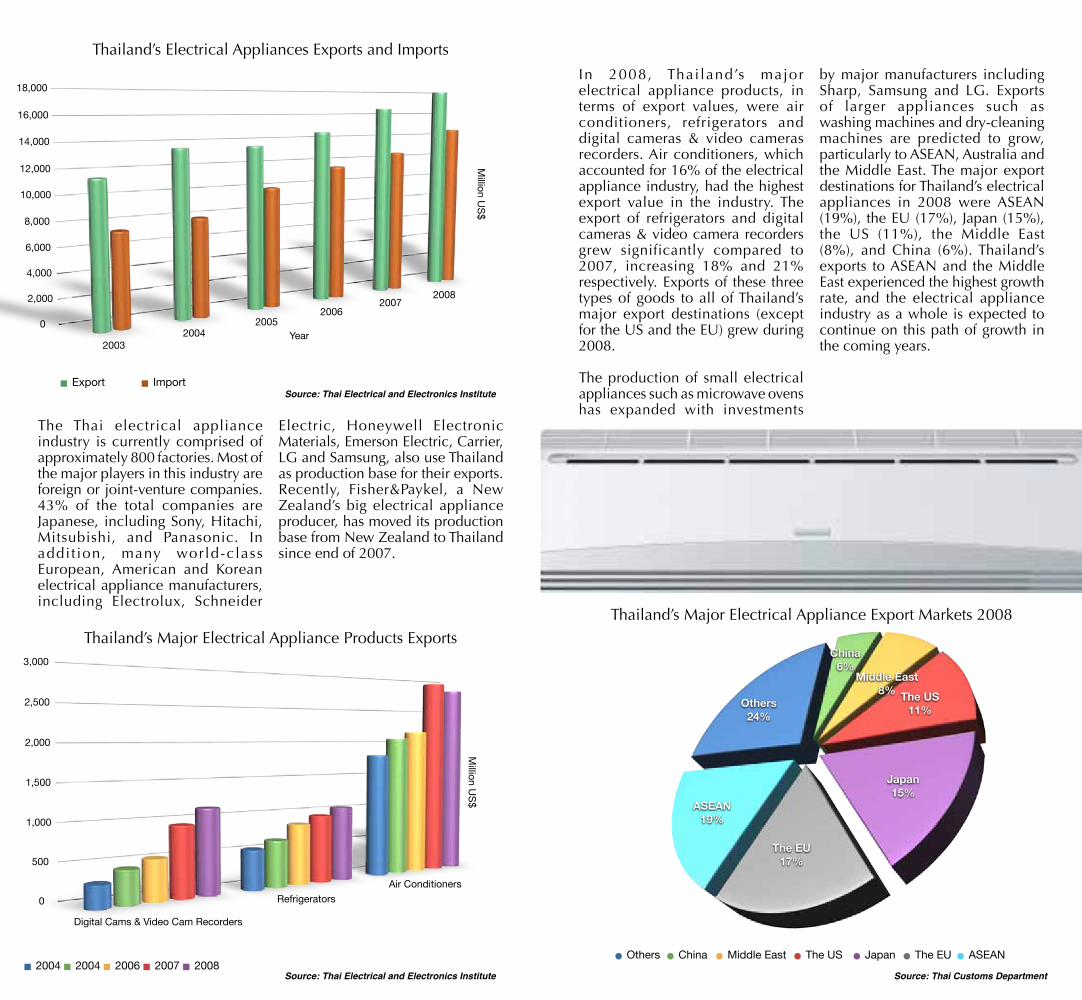

In 2008, Thai land’s major electrical appliance products, in terms of export values, were air conditioners, refrigerators and digital cameras & video cameras recorders. Air conditioners, which accounted for 16% of the electrical appliance industry, had the highest export value in the industry. The export of refrigerators and digital cameras & video camera recorders grew significantly compared to 2007, increasing 18% and 21% respectively. Exports of these three types of goods to all of Thailand’s major export destinations (except for the US and the EU) grew during 2008.

The production of small electrical appliances such as microwave ovens has expanded with investments

by major manufacturers including Sharp, Samsung and LG. Exports of larger appliances such as washing machines and dry-cleaning machines are predicted to grow, particularly to ASEAN, Australia and the Middle East. The major export destinations for Thailand’s electrical appliances in 2008 were ASEAN (19%), the EU (17%), Japan (15%), the US (11%), the Middle East (8%), and China (6%). Thailand’s exports to ASEAN and the Middle East experienced the highest growth rate, and the electrical appliance industry as a whole is expected to continue on this path of growth in the coming years.

Others24%

China6%

Middle East8% The US

11%

Japan15%

The EU17%

ASEAN19%

Others China Middle East The US Japan The EU ASEAN

Thailand’s Major Electrical Appliance Export Markets 2008Thailand’s Major Electrical Appliance Products Exports

Thailand’s Electrical Appliances Exports and Imports

Source: Thai Electrical and Electronics Institute Source: Thai Customs Department

Source: Thai Electrical and Electronics Institute

As global demand for high-technology consumer electronics such as wireless devices, flat panel displays, MP3 players, gaming consoles and computers continues to grow, Thailand is an ideal location for electronics industry investment. Such growing demand, coupled with strong government support for the sector, promises a bright future for electronics – and electronics investors.

Wor ld -c l a s s manu fac tu re r s dominate this fast-growing sector. Multinational companies, such as Fujitsu from Japan, Seagate from the US, Philips Electronics from the Netherlands, and LG Electronics

from Korea, have established production, testing, assembly or research and development facilities in Thailand.

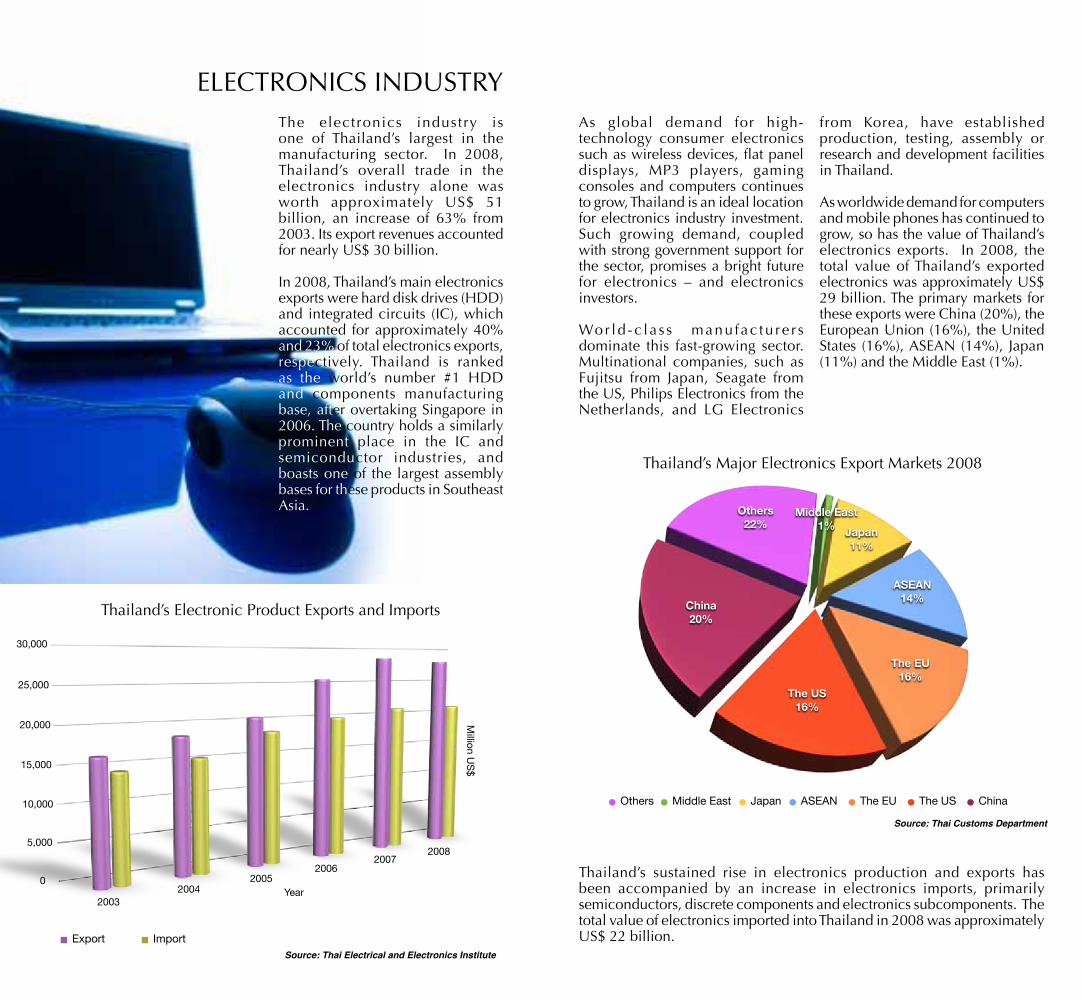

As worldwide demand for computers and mobile phones has continued to grow, so has the value of Thailand’s electronics exports. In 2008, the total value of Thailand’s exported electronics was approximately US$ 29 billion. The primary markets for these exports were China (20%), the European Union (16%), the United States (16%), ASEAN (14%), Japan (11%) and the Middle East (1%).

0

5,000

10,000

15,000

20,000

25,000

30,000

Million U

S$

20032004

20052006

20072008

Year

Export Import

The electronics industry is one of Thailand’s largest in the manufacturing sector. In 2008, Thailand’s overall trade in the electronics industry alone was worth approximately US$ 51 billion, an increase of 63% from 2003. Its export revenues accounted for nearly US$ 30 billion.

In 2008, Thailand’s main electronics exports were hard disk drives (HDD) and integrated circuits (IC), which accounted for approximately 40% and 23% of total electronics exports, respectively. Thailand is ranked as the world’s number #1 HDD and components manufacturing base, after overtaking Singapore in 2006. The country holds a similarly prominent place in the IC and semiconductor industries, and boasts one of the largest assembly bases for these products in Southeast Asia.

ELECTRONICS INDUSTRY

Thailand’s sustained rise in electronics production and exports has been accompanied by an increase in electronics imports, primarily semiconductors, discrete components and electronics subcomponents. The total value of electronics imported into Thailand in 2008 was approximately US$ 22 billion.

Others22%

Middle East1% Japan

11%

ASEAN14%

The EU16%

The US16%

China20%

Others Middle East Japan ASEAN The EU The US China

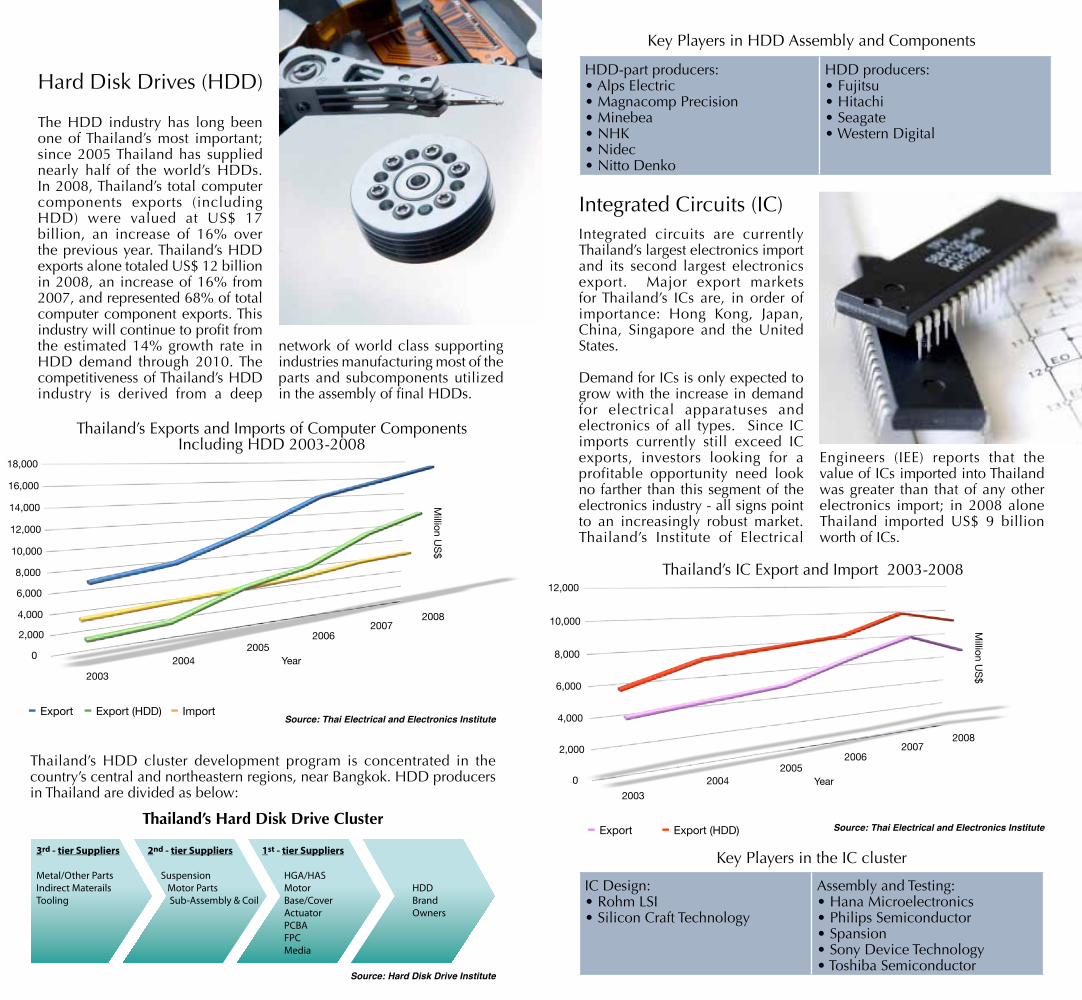

HDD producers:• Fujitsu• Hitachi• Seagate• Western Digital

Key Players in HDD Assembly and Components

Thailand’s Exports and Imports of Computer Components Including HDD 2003-2008

Thailand’s Hard Disk Drive Cluster

Source: Hard Disk Drive Institute

The HDD industry has long been one of Thailand’s most important; since 2005 Thailand has supplied nearly half of the world’s HDDs. In 2008, Thailand’s total computer components exports (including HDD) were valued at US$ 17 billion, an increase of 16% over the previous year. Thailand’s HDD exports alone totaled US$ 12 billion in 2008, an increase of 16% from 2007, and represented 68% of total computer component exports. This industry will continue to profit from the estimated 14% growth rate in HDD demand through 2010. The competitiveness of Thailand’s HDD industry is derived from a deep

Hard Disk Drives (HDD)

network of world class supporting industries manufacturing most of the parts and subcomponents utilized in the assembly of final HDDs.

Thailand’s HDD cluster development program is concentrated in the country’s central and northeastern regions, near Bangkok. HDD producers in Thailand are divided as below:

Integrated circuits are currently Thailand’s largest electronics import and its second largest electronics export. Major export markets for Thailand’s ICs are, in order of importance: Hong Kong, Japan, China, Singapore and the United States.

Demand for ICs is only expected to grow with the increase in demand for electrical apparatuses and electronics of all types. Since IC imports currently still exceed IC exports, investors looking for a profitable opportunity need look no farther than this segment of the electronics industry - all signs point to an increasingly robust market. Thailand’s Institute of Electrical

Integrated Circuits (IC)

Engineers (IEE) reports that the value of ICs imported into Thailand was greater than that of any other electronics import; in 2008 alone Thailand imported US$ 9 billion worth of ICs.

0

2,000

4,000

6,000

8,000

10,000

12,000

Million U

S$

2003

20042005

20062007

2008

Year

Export Export (HDD)

Thailand’s IC Export and Import 2003-2008

IC Design:• Rohm LSI• Silicon Craft Technology

Assembly and Testing:• Hana Microelectronics• Philips Semiconductor• Spansion• Sony Device Technology• Toshiba Semiconductor

Key Players in the IC cluster

Source: Thai Electrical and Electronics Institute

Source: Thai Electrical and Electronics Institute

OPPORTUNITIES

HDD and IC

Thailand’s preeminent position as the world’s largest production base for HDDs and components offers suppliers within the HDD value chain the opportunity to develop world-scale manufacturing capacity within a dynamic and highly concentrated industrial cluster. Almost all of the world’s key HDD manufacturing players are located within a 250-kilometer radius of Bangkok, offering unparalleled opportunities for manufacturers within the HDD industry.

Thailand has established itself as a competitive location for the assembly and testing of HDDs, ICs and electronic subcomponents such as printed circuit boards (PCBs). However, many key components of the upstream electronics value chain such as semiconductor devices, discrete components such as diodes and transistors as well as ICs, are still imported from abroad, primarily from Korea, Japan, Taiwan and Singapore. Manufacturers looking to expand their market in Thailand can find excellent opportunities in manufacturing these components locally.

IC design and related activities possess strong growth potential. The government provides outstanding support to relevant organizations and institutes by holding human resource development-training programs and conducting research on their behalf.

RFID Thailand is positioning itself at the vanguard of cutting-edge technologies including radio-frequency identification (RFID), which offers great potential for applications including supply chain, manufacturing and logistics. In 2008, the total RFID market in Thailand was approximately US$ 30 million and is expected to reach US$ 32 million by 2010. Investment opportunities in this sector are attractive, especially considering that Thailand is one of Asia’s major production centers for inlay and coil parts used in RFID.

In 2008, the value of the entire worldwide RFID market was estimated at US$ 5.3 billion, and it is expected to skyrocket to US$ 12.3 billion in 2010 and US$ 26.2 billion in 2016. As the worldwide demand for RFID expands, Thailand is aiming to encourage the growth of the technology locally, and to be at the forefront of global RFID markets by 2010.

Automotive Electronics With consumers demanding ever more sophisticated gadgets and consumer electronic applications in their vehicles, automotive electronics offers a burgeoning field of opportunity in a global industry

valued at over US$ 110 billion. The automotive electronics industry is forecast to show continued volume growth, especially for side impact airbags. The market for navigation will continue to converge with audio, and entertainment will be one of the fastest growing segments of the automotive electronics market. Driver assistance systems such as collision avoidance, night vision and lane departure warning will also show strong growth. With automakers looking to reduce expenditures by moving production to lower cost locations like Thailand, the country will also be an attractive destination for system and component suppliers, which tend to locate near their automaker customers.

Thailand is currently one of the world’s top fifteen automobile manufacturing countries, and is moving towards a place in the top ten. This has encouraged the growth of supporting industries, including automotive electronics and parts. Demand for OEM automotive electronics in Thailand is predicted to reach US$ 2.6 billion by 2011.

In sum, Thailand offers a number of unique advantages for electrical appliance and electronics producers. These include:

Additionally, Thailand offers several resources for technical training, including:• The Thai Microelectronics

Center (TMEC), established by the Ministry of Science and Technology in 1998;

• The Western Digital HDD Technology Training Institute (HTTI), an institution established through the cooperative efforts of Thailand’s National Electronics and Computer Technology Center (NECTEC) and Western Digital; and

• NECTEC’s Industry/University Cooperative Research Centers in 3 areas:» HDD Advanced Manufacturing – The Institute of Field Robotics (F IBO) , K ing Mongkut ’s University of Technology Thonburi» HDD Components – The Engineering Faculty, Khon Kaen University» Data Storage Technology and Application – King Mongkut Ins t i tu te o f Technology Ladkrabang»

Access to markets:

Thailand’s many Free Trade Agreements (FTAs) with countries such as Australia, New Zealand, India, Japan and members of ASEAN enhance the already highly competitive electronics industry. Parts and finished products exported throughout ASEAN face minimal or zero tariffs. For example, the majority of electronic components exported to ASEAN member nations are currently subject to tariffs of less than 5%, and by 2010, they will be tariff-free.

Excellent logistics systems:

With its unbeatable location in the heart of Southeast Asia and state-of-the-art ports, airports and communications facilities, Thailand is an excellent hub of electrical and electronics manufacturing.

Why Thailand?

“Thailand has good experience in HDD manufacturing compared to other countries, and is also a strategic location for the production of HDD components” Dr Chitiporn Pupaichitkul, Seagate Technology (Thailand) senior director for engineering.

“The strength of Thailand is that there are many supporting industries” Naoki Iwaki, Fujitsu Systems (Thailand) president.

Efficient customs services:

Thai Customs has implemented Electronic Data Interchange (EDI) at Suvarnabhumi Airport and Laem Chabang Deep Seaport to enable paperless, quick and accurate import and export procedures. Customs has also adopted a fixed x-ray inspection system to allow business operators and international traders to move cargo more rapidly and conveniently through the Laem Chabang facility. Such increased efficiency and transparency confirms Thailand’s status as a regional hub.

Development of electronics clusters:

In order to foster greater productivity and efficiency in the industry, the government has encouraged the development of the electronics clusters. Proximity between firms and their input suppliers in these clusters allows for not only enhanced communication, but also improved flow of goods. In addition, clusters help to reduce logistics costs by fostering improved supply chain management, and allowing manufacturers to benefit from shared core technologies and human resource development programs.

Strong Government Support:

The Thai government supports the development of the electronics industry through several bodies as follows:

Competitive workforce:

Over 400,000 people are employed in the electrical and electronics sector. Thailand not only boasts relatively low labor costs, but also has an exceptionally well-educated workforce. Literacy rates are uncommonly high at 96%. Currently, 61 public and private engineering institutes in Thailand are accredited by the Council of Engineers. The country’s annual number of engineering graduates is approximately 18,400.

The Thai government is aware of the need to support the continued development of the technological capabilities of its workforce. To this end, the BOI and the Ministry of Education have adopted a Human Resources Development Plan, which is designed to insure an adequate supply of qualified personnel for the electrical and electronics industry.

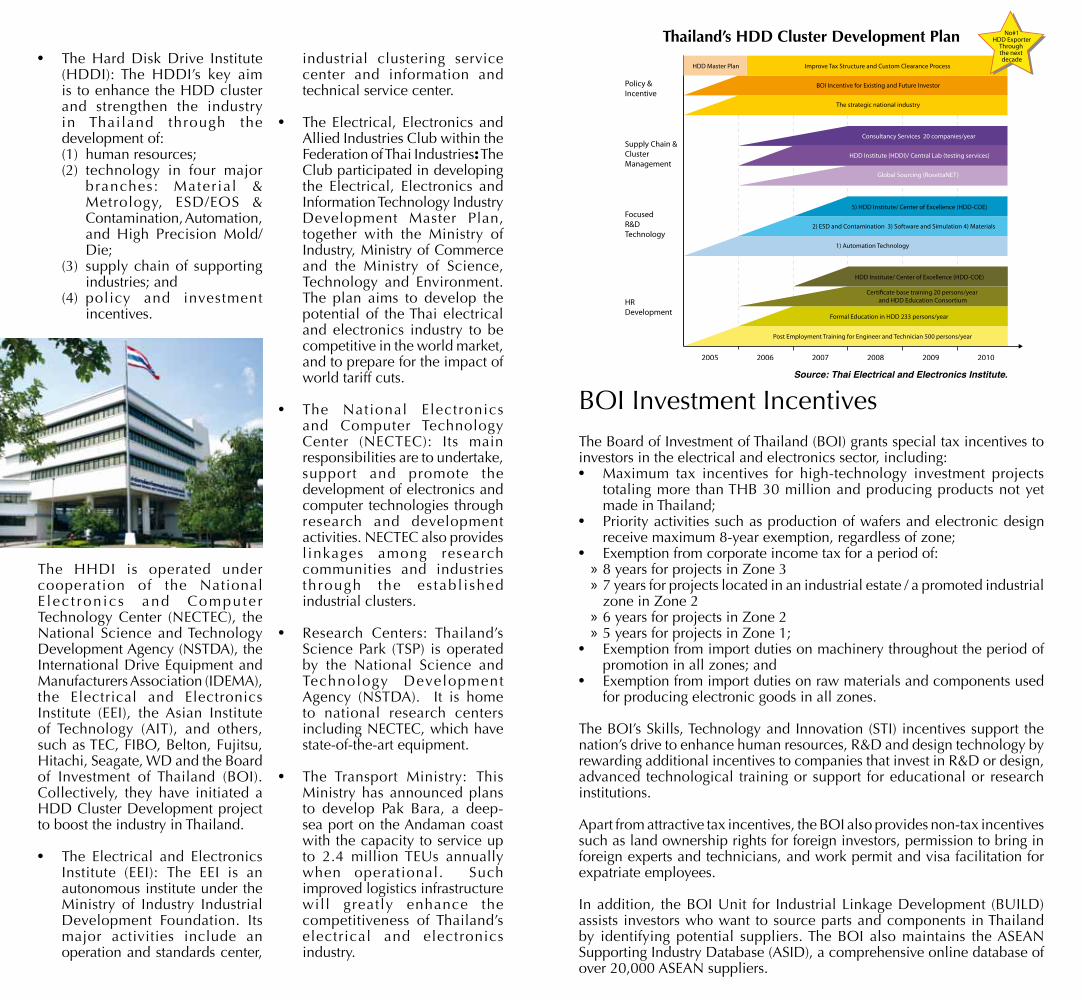

Thailand’s HDD Cluster Development Plan

Source: Thai Electrical and Electronics Institute.

• The Hard Disk Drive Institute (HDDI): The HDDI’s key aim is to enhance the HDD cluster and strengthen the industry in Thailand through the development of: (1) human resources; (2) technology in four major

branches: Material & Metrology, ESD/EOS & Contamination, Automation, and High Precision Mold/Die;

(3) supply chain of supporting industries; and

(4) policy and investment incentives.

The HHDI is operated under cooperation of the National E lec t ron ics and Compute r Technology Center (NECTEC), the National Science and Technology Development Agency (NSTDA), the International Drive Equipment and Manufacturers Association (IDEMA), the Electrical and Electronics Institute (EEI), the Asian Institute of Technology (AIT), and others, such as TEC, FIBO, Belton, Fujitsu, Hitachi, Seagate, WD and the Board of Investment of Thailand (BOI). Collectively, they have initiated a HDD Cluster Development project to boost the industry in Thailand.

• The Electrical and Electronics Institute (EEI): The EEI is an autonomous institute under the Ministry of Industry Industrial Development Foundation. Its major activities include an operation and standards center,

industrial clustering service center and information and technical service center.

• The Electrical, Electronics and Allied Industries Club within the Federation of Thai Industries: The Club participated in developing the Electrical, Electronics and Information Technology Industry Development Master Plan, together with the Ministry of Industry, Ministry of Commerce and the Ministry of Science, Technology and Environment. The plan aims to develop the potential of the Thai electrical and electronics industry to be competitive in the world market, and to prepare for the impact of world tariff cuts.

• The National Electronics and Computer Technology Center (NECTEC): Its main responsibilities are to undertake, support and promote the development of electronics and computer technologies through research and development activities. NECTEC also provides l inkages among research communities and industries through the es tabl i shed industrial clusters.

• Research Centers: Thailand’s Science Park (TSP) is operated by the National Science and Technology Development Agency (NSTDA). It is home to national research centers including NECTEC, which have state-of-the-art equipment.

• The Transport Ministry: This Ministry has announced plans to develop Pak Bara, a deep-sea port on the Andaman coast with the capacity to service up to 2.4 million TEUs annually when operational. Such improved logistics infrastructure will greatly enhance the competitiveness of Thailand’s electrical and electronics industry.

The Board of Investment of Thailand (BOI) grants special tax incentives to investors in the electrical and electronics sector, including:• Maximum tax incentives for high-technology investment projects

totaling more than THB 30 million and producing products not yet made in Thailand;

• Priority activities such as production of wafers and electronic design receive maximum 8-year exemption, regardless of zone;

• Exemption from corporate income tax for a period of: » 8 years for projects in Zone 3» 7 years for projects located in an industrial estate / a promoted industrial zone in Zone 2» 6 years for projects in Zone 2» 5 years for projects in Zone 1;

• Exemption from import duties on machinery throughout the period of promotion in all zones; and

• Exemption from import duties on raw materials and components used for producing electronic goods in all zones.

The BOI’s Skills, Technology and Innovation (STI) incentives support the nation’s drive to enhance human resources, R&D and design technology by rewarding additional incentives to companies that invest in R&D or design, advanced technological training or support for educational or research institutions.

Apart from attractive tax incentives, the BOI also provides non-tax incentives such as land ownership rights for foreign investors, permission to bring in foreign experts and technicians, and work permit and visa facilitation for expatriate employees.

In addition, the BOI Unit for Industrial Linkage Development (BUILD) assists investors who want to source parts and components in Thailand by identifying potential suppliers. The BOI also maintains the ASEAN Supporting Industry Database (ASID), a comprehensive online database of over 20,000 ASEAN suppliers.