48

Nonprofits are Not Exempt From Fraud Marie Schmitz, CPA October 2, 2015

Nonprofits are Not Exempt From Fraud

Marie Schmitz, CPA

October 2, 2015

1

bergankdv.com

Nonprofits are Not Exempt from Fraud

Is it fraud?

2

bergankdv.com

Nonprofits are Not Exempt from Fraud

Agenda

• Fraud fundamentals

• Fraud statistics

• Role of external auditor

• Preventing and detecting fraud

• Risk assessment

• Questions

3

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

Definition of fraud• Dishonesty calculated for advantage• Deception intended to result in financial or

personal gain• Deliberate misuse or misapplication of the

employing organizations resources or assets.

4

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

Types of fraud• Misappropriation of assets

• Skimming• Financial statement fraud

5

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

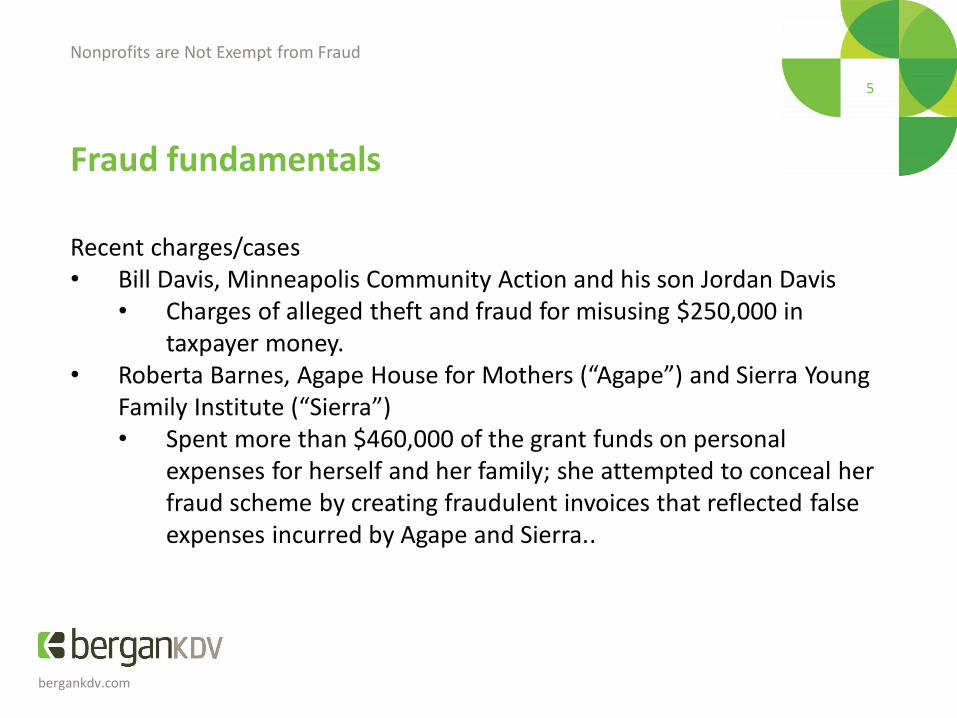

Recent charges/cases • Bill Davis, Minneapolis Community Action and his son Jordan Davis

• Charges of alleged theft and fraud for misusing $250,000 in taxpayer money.

• Roberta Barnes, Agape House for Mothers (“Agape”) and Sierra Young Family Institute (“Sierra”)• Spent more than $460,000 of the grant funds on personal

expenses for herself and her family; she attempted to conceal her fraud scheme by creating fraudulent invoices that reflected false expenses incurred by Agape and Sierra..

5

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

How fraud happens• Starts small• Inconsistency

• Application of controls• Accountability

• Trust

Reference:http://www.asaecenter.org/Resources/ANowDetail.cfm?ItemNumber=644445

6

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

7

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

5 areas employee fraud commonly occurs:• Purchase-to-pay• Corporate credit cards• Payroll• Sales and receivables• Information systems and critical data

Reference:http://ww2.cfo.com/accounting-tax/2013/11/top-five-areas-monitor-employee-fraud/

8

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

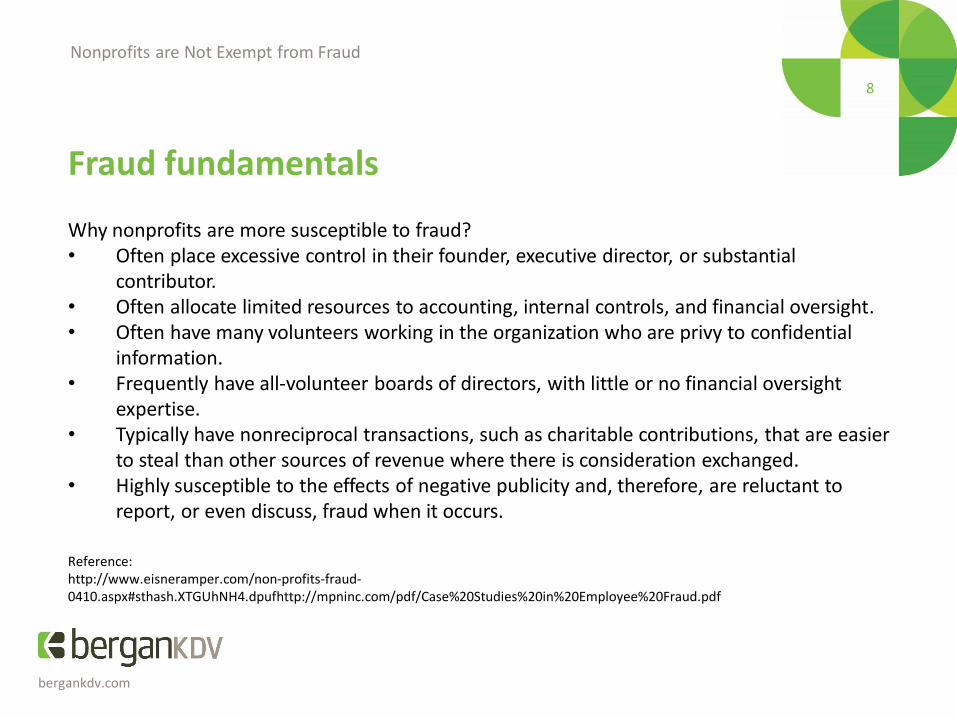

Why nonprofits are more susceptible to fraud?• Often place excessive control in their founder, executive director, or substantial

contributor.• Often allocate limited resources to accounting, internal controls, and financial oversight.• Often have many volunteers working in the organization who are privy to confidential

information.• Frequently have all-volunteer boards of directors, with little or no financial oversight

expertise.• Typically have nonreciprocal transactions, such as charitable contributions, that are easier

to steal than other sources of revenue where there is consideration exchanged.• Highly susceptible to the effects of negative publicity and, therefore, are reluctant to

report, or even discuss, fraud when it occurs.

Reference:http://www.eisneramper.com/non-profits-fraud-0410.aspx#sthash.XTGUhNH4.dpufhttp://mpninc.com/pdf/Case%20Studies%20in%20Employee%20Fraud.pdf

9

bergankdv.com

Nonprofits are Not Exempt from Fraud

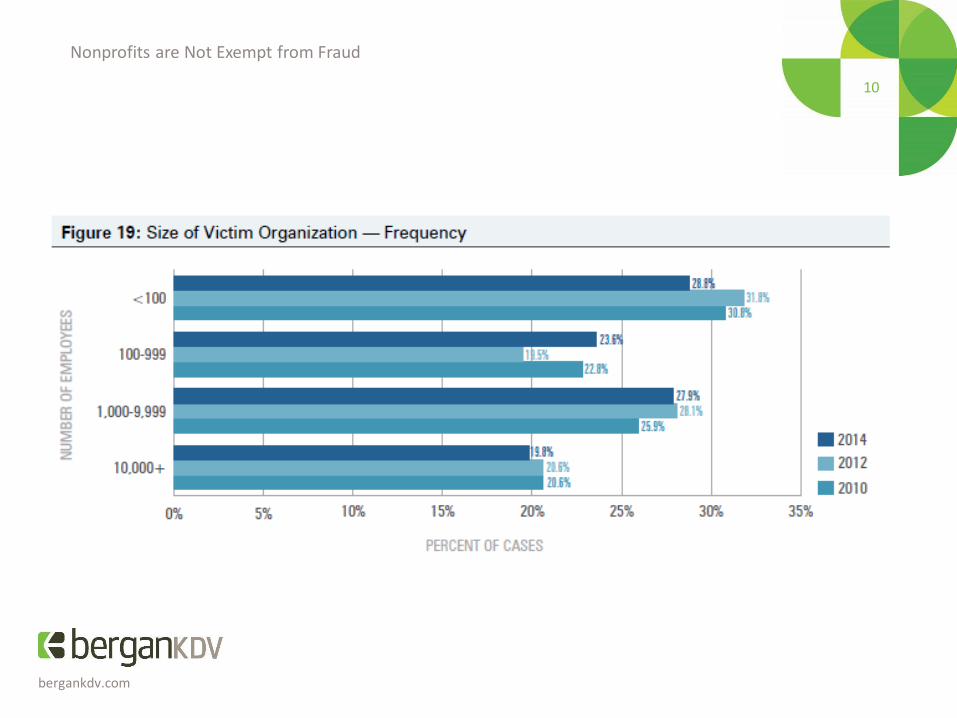

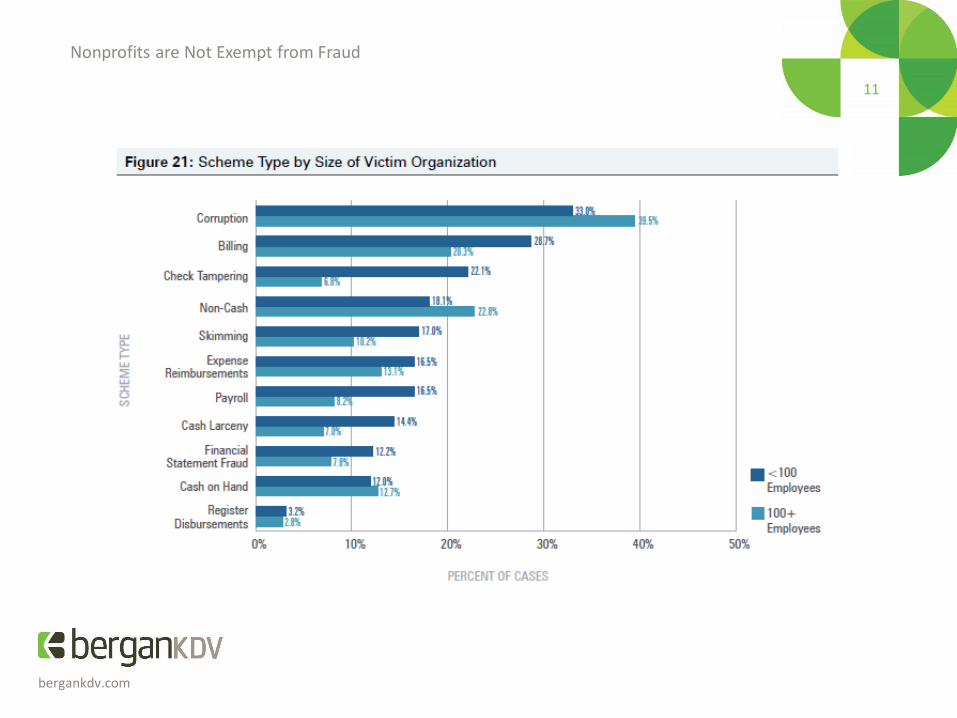

Fraud statistics

2014 Global Fraud Study – ACFE (Association of Certified Fraud Examiners)

Summary of findings:• Typical organization loses 5% of revenues each

year to fraud• Median loss caused by frauds was $145,000

Reference:Report to the Nations on Occupational Fraud and Abuse: 2014 Global Fraud Study, ACFE

10

bergankdv.com

Nonprofits are Not Exempt from Fraud

11

bergankdv.com

Nonprofits are Not Exempt from Fraud

12

bergankdv.com

Nonprofits are Not Exempt from Fraud

Fraud statistics

Summary of findings - continued:• Median duration was 18 months• 85% - Misappropriation of assets• 9% - Financial statement fraud• Over 40% of cases detected by tips

Reference:Report to the Nations on Occupational Fraud and Abuse: 2014 Global Fraud Study, ACFE

13

bergankdv.com

Nonprofits are Not Exempt from Fraud

14

bergankdv.com

Nonprofits are Not Exempt from Fraud

15

bergankdv.com

Nonprofits are Not Exempt from Fraud

8

bergankdv.com

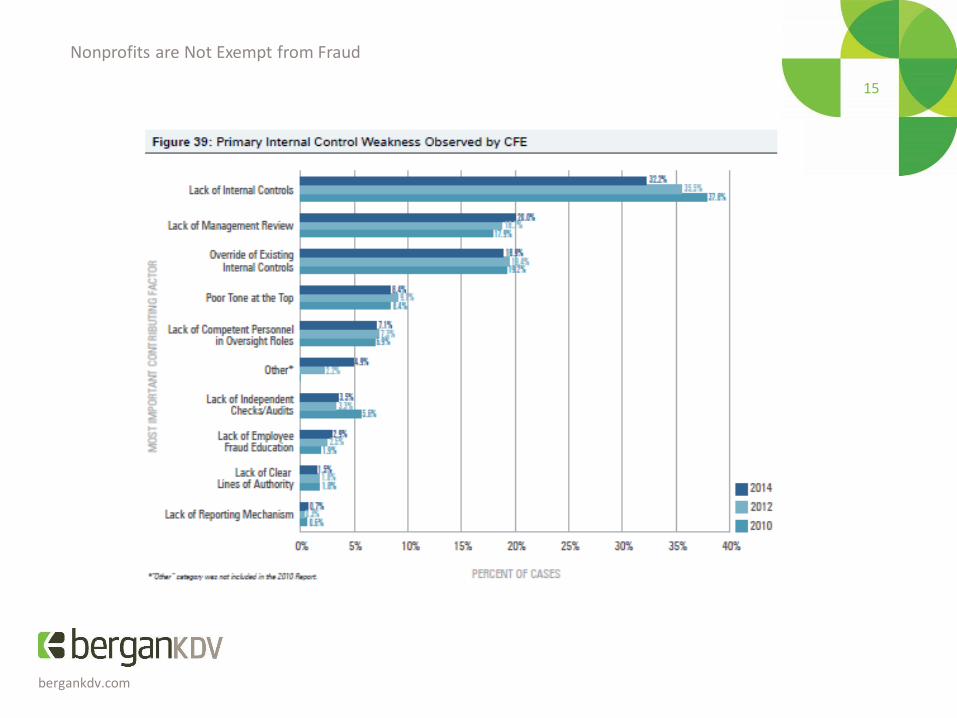

Nonprofits are Not Exempt from Fraud

Fraud fundamentals

Impacts of fraud• Costs are not just monetary• Negative publicity• Employee moral• Disrupted operations

Reference:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspxhttp://mpninc.com/pdf/Case%20Studies%20in%20Employee%20Fraud.pdf

16

bergankdv.com

Nonprofits are Not Exempt from Fraud

Role of external auditor

Responsibility:• Provide reasonable assurance that the financial

statements are free of material misrepresentations• Do not guarantee that the organization is free from

fraud

17

bergankdv.com

Nonprofits are Not Exempt from Fraud

Role of external auditor

Risk based audit planning process:• Detection of fraud not primary purpose• Top down approach• Internal planning meeting• Specific tests to cover risks

• Inquiry• Focused testing

18

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

Internal control categories• Preventive• Detective• Monitoring

Reference:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspx

19

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

Preventive control examples:• Segregation of asset handling and recordkeeping

duties• Physical security over cash and other assets• Pre-reimbursement expense report review and

approval• Dual signatures on checks

Reference:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspx

20

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

Detective control examples:• Bank reconciliations• Automated user access and edit logs for computer

systems • Master vendor list audits• Periodic inventories• Whistleblower hotlines or other reporting

mechanismsReference:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspx

21

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

Monitoring control examples:• Comparing monthly and quarterly financial activity

to budgeted activity• Review of monthly and quarterly expenses• Review of account reconciliations • Review compliance with policies set in place

Reference:http://www.blueandco.com/nfp_12062012.html

22

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

Other means to prevent fraud• Diligent background checks• Recurring fraud-risk assessments

Reference:http://www.asaecenter.org/Resources/ANowDetail.cfm?ItemNumber=644445

23

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

What if fraud is discovered?• Follow organization plan• Never assume controls are sufficient• Seek professionals

• Attorney• Forensic accountant

Reference:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspx

24

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

What can you do now?• Foster culture• Educate yourself about fraud• Evaluate fraud risk and design controls to match• Have a good fraud prevention policy and program

(including hotline)

References:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspxhttp://www.councilofnonprofits.org/files/YH%20-%20Fraud%20+%20EO%20Final.pdf

25

bergankdv.com

Nonprofits are Not Exempt from Fraud

Preventing and detecting fraud

What can you do now - continued?• Have a well-developed fraud management plan • Identify the role of board members• Perform internal audits or spot checks

References:http://www.raffa.com/Fraud/Resources/Pages/Fraud-Fundamentals-How-Your-Association-Can-Prevent-and-Detect-It.aspxhttp://www.councilofnonprofits.org/files/YH%20-%20Fraud%20+%20EO%20Final.pdf

26

bergankdv.com

Nonprofits are Not Exempt from Fraud

Is it fraud?

27

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

• Are you hearing about Enterprise Risk Management (ERM) initiatives?• Prevalent since early 1990s in corporate America and more recently in the

nonprofit sector.

• What is ERM in simple terms?• Identifying risks,• Prioritizing risks, • Developing plans to mitigate risks

• Drivers for ERM• Accelerating pace of social and technological change,• Complexity of a digitized and globalized business environment,• Evolving regulatory demands have intensified

27

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

• Trends• Success

• Identifying and prioritizing risks• Generating high level reports

• Falters• Lack of common approach or framework• Don’t understand the benefits and goals

• Tips• Involve the entire team• Identify risks early• Communicate, communicate, communicate• Analyze and prioritize then reprioritize• Plan and implement risk responses • Developing plans to mitigate risks

27

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

• Risk = the chance of something happening that will have an impact on objectives.

• Important to understand what the objectives are prior to attempting to analyze the risks.

• Risk Management = the systematic application of management policies, procedures and practices to the tasks of establishing the context, identifying, analyzing, assessing, treating, monitoring and communicating.

• Risk management can be applied to all levels of an organization, in both the strategic and operational contexts, to specific projects, decisions and recognized risk areas.

References:http://scu.edu.au/risk_management/index.php/2

28

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

1. Identify the risks:

Most nonprofit organizations will share the same type of broad risks that can be generally described as follows:• Internal or external fraud• Misuse of assets• Inadequate monitoring or understanding of investments• Incomplete, unreliable or improperly reported information• Damage to reputation caused by a variety of potential factors• Violation of legal requirements• Government investigations or audits

References:http://scu.edu.au/risk_management/index.php/2http://nonprofitquarterly.org/2012/05/08/risky-business-why-all-nonprofits-should-periodically-assess-their-risk/

29

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

2. Identify the causes: • Try to identify what might cause these things to occur

• Example: the key team member might be disillusioned with his/her position, might be head hunted to go elsewhere; the person upon whom you are relying for information might be very busy, going on leave or notoriously slow in supplying such data; the supervisor required to approve the undertaking might be risk averse and need extra convincing before taking the risk etc.

References:http://scu.edu.au/risk_management/index.php/2

30

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

3. Identify the controls: • Identify all the things (controls) that you have in place that are aimed at

reducing the likelihood of your risks from happening in the first place and, if they do happen, what you have in place to reduce their impact (consequence) • Example: providing a friendly work environment for your team; multi-

skill across the team to reduce the reliance on one person; stress the need for the required information to be supplied in a timely manner; send a reminder before the deadline; provide additional information to the supervisor before he/she asks for it etc.

References:http://scu.edu.au/risk_management/index.php/2

31

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

4. Establish your likelihood and consequence descriptors, remembering that these depend upon the context of your analysis

• i.e.. if your analysis relates to your work unit, any financial loss or loss of a key staff member, for example, will have a greater impact on that work unit than it will have on the Organization as a whole so those descriptors used for the whole-of-Organization (strategic) context will generally not be appropriate for the work unit or the individual

• Example: a loss of $300,000 might be considered insignificant to the Organization, but it could very well be catastrophic to your work unit.

References:http://scu.edu.au/risk_management/index.php/2

32

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessmentRisk Likelihood Descriptors

33

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessmentRisk Consequence Descriptors

34

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

5. Establish your risk rating descriptors: • What is meant by a Low, Moderate, High or Extreme Risk

needs to be decided upon ahead of time.

References:http://scu.edu.au/risk_management/index.php/2

35

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessmentRisk Rating Descriptors

36

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

6. Add other controls: • Generally speaking, any risk that is rated as High or Extreme should

have additional controls applied to it in order to reduce it to an acceptable level.

• What the appropriate additional controls might be, whether they can be afforded, what priority might be placed on them etc. is something for the group to determine.

References:http://scu.edu.au/risk_management/index.php/2

37

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

7. Make a Decision: • Once the above process is complete, if there are still some risks that are

rated as High or Extreme, a decision has to be made as to whether the activity will go ahead.

• There will be occasions when the risks are higher than preferred but there may be nothing more that can be done to mitigate that risk• Example: they are out of the control of the work unit but the

activity must still be carried out. In such situations, monitoring the circumstances and regular review is essential.

References:http://scu.edu.au/risk_management/index.php/2

38

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

Risk treatment• Identifying the range of options for treating risk, • Assessing those options, • Preparing risk treatment plans, and• Implementing them

The options available for the treatment of risks include:• Retain/accept the risk • Reduce the likelihood of the risk occurring• Reduce the consequences of the risk occurring• Transfer the risk • Avoid the risk

References:http://scu.edu.au/risk_management/index.php/2

39

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

8. Monitor and Review: • The monitoring of all risks and regular review of the

unit's risk profile is an essential element for a successful risk management program.

References:http://scu.edu.au/risk_management/index.php/2

39

bergankdv.com

Nonprofits are Not Exempt from Fraud

Risk assessment

A simple process

8. Monitor and Review: • Regardless of size and sophistication you should consider:

• Segregation of duties• Set payment controls• Conduct due diligence and legal review• Conduct audits (external and internal)• Implement and follow strong internal policies• Set the right tone at the top

40

bergankdv.com

Nonprofits are Not Exempt from Fraud

41

bergankdv.com

Nonprofits are Not Exempt from Fraud

Questions?

42

bergankdv.com

Nonprofits are Not Exempt from Fraud

Contact

Marie Schmitz, CPA, CGMAAudit DirectorNonprofit Industry Group [email protected]