14

NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB FEBRUARY 2016

NORTH-WEST HYDERABADEMERGING MANUFACTURING HUBFEBRUARY 2016

Page 02 NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB

Structure

MANUFACTURINGHUB

UPCOMINGINFRASTRUCTURE

REAL ESTATELANDSCAPE

INSIGHTS NORTH-WESTHYDERABADOVERVIEW

While Hyderabad had come to a standstill during the Telangana dispute, the issue is now resolved and the city’s real estate landscape is set for a revival.

With an existing ecosystem of Pharmaceutical companies and announcement of Hyderabad-Nagpur Industrial Corridor (HNIC) and Information Technology Investment Region (ITIR), the region promises economic growth on the backbone of manufacturing which, in turn, has already attracted developers in proximity of this influence zone.

End-users and investors are looking at North-West Hyderabad as an attractive opportunity as planned infrastructural initiatives such as the proposed Outer Ring Road (ORR) and Metro Rail among others are likely to improve region’s connectivity.

With ongoing metro construction, North-West Hyderabad realty is getting a fresh lease of life. Once operational, the connectivity to the Southern and Western parts would improve significantly.

Residential real estate prices in Hyderabad are the lowest across most other metro cities like Bengaluru and Chennai which makes the city one of the most affordable metropolitan centers as well.

With the North-West region closely following the industrial/manufacturing footsteps of Tumkur Road in Bengaluru, the region holds high price potential in medium to long term.

Kukatpally, Miyapur and Medchal are the key localities in North-West region that are likely to witness an upsurge in residential demand, owing to their connectivity with National Highway-7, proximity to IT/ITeS hubs and manufacturing corridors.

Key Insights

Page 03 NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB

North-West HyderabadOverview

Page 04 EMERGING MANUFACTURING HUB

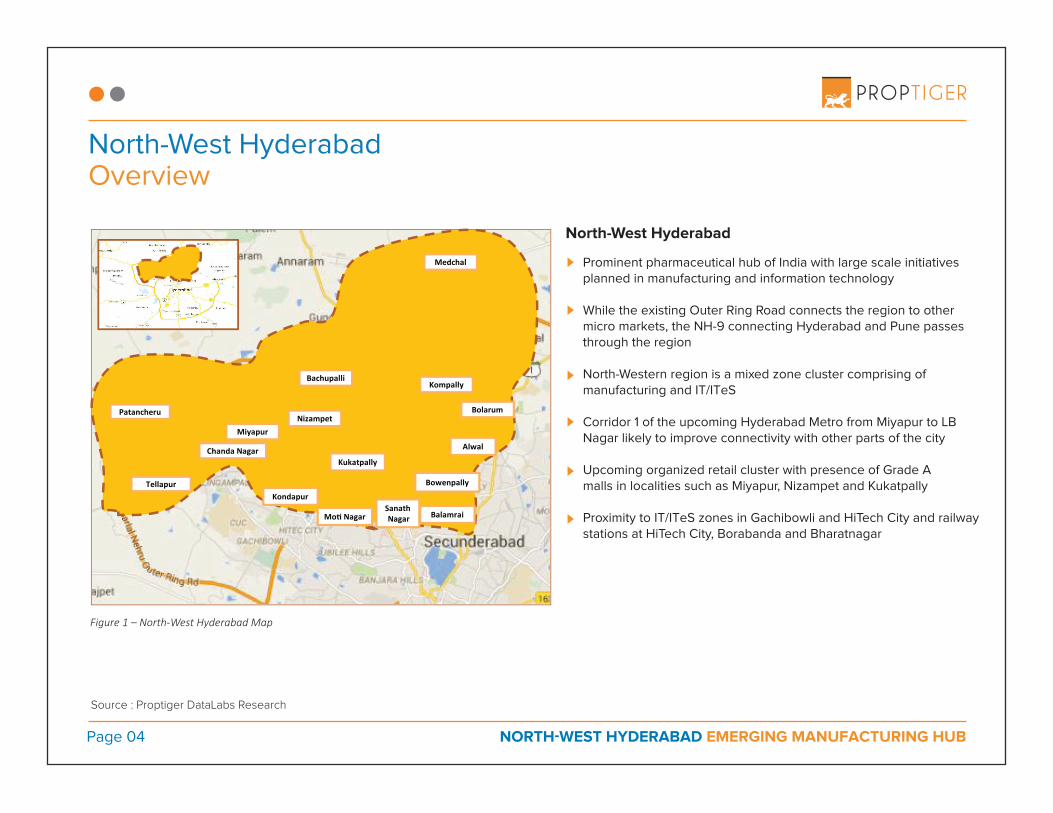

Figure 1 – North-West Hyderabad Map

North-West Hyderabad

Patancheru

Tellapur

Chanda Nagar

Miyapur

Nizampet

Bachupalli

Medchal

Kompally

Bolarum

Alwal

Bowenpally

Balamrai

Kukatpally

Mo NagarSanath Nagar

Kondapur

Prominent pharmaceutical hub of India with large scale initiatives planned in manufacturing and information technology

While the existing Outer Ring Road connects the region to other micro markets, the NH-9 connecting Hyderabad and Pune passes through the region

North-Western region is a mixed zone cluster comprising of manufacturing and IT/ITeS

Corridor 1 of the upcoming Hyderabad Metro from Miyapur to LB Nagar likely to improve connectivity with other parts of the city

Upcoming organized retail cluster with presence of Grade A malls in localities such as Miyapur, Nizampet and Kukatpally

Proximity to IT/ITeS zones in Gachibowli and HiTech City and railway stations at HiTech City, Borabanda and Bharatnagar

Source : Proptiger DataLabs Research

Manufacturing HubEpicenter for Pharma

Page 05 NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB

S.No. Industrial Area Major Companies

Patancheru Industrial Area Fenner India, Praxair India

Janachaitanya Industrial Area, Miyapur

Coca Cola Factory, TFL Quinn India, L&T

ALEAP Industrial Area, Gajularamaram

Neuheit Pharma, Lyophilization Systems, TherDose

Kukatpally Industrial EstateIDL Factory, Usha International, MTAR

Technologies, Hindustan Aeronautics, BHEL

Kattedan Industrial Area Dukes, Hindustan Adhesives, Balaji Packagings

IDA JeedimatlaShree Vinayaka Life Sciences, Therdose Pharma,

Alphine Pharmaceutical, HMT

Balanagar Industrial Development Area

Indian Drugs and Pharmaceuticals Limited (IDPL), SEC Industries, Usha International, Khaitan, BHEL

R&D

3

5

4

1

2

6

3

6

1

4

2

5

7

7

Table 1 - List of Industrial Areas in North-West Hyderabad

Figure 2 - Industrial Areas of North-West Hyderabad

Source : Proptiger DataLabs Research

Manufacturing HubHyderabad-Nagpur Industrial Corridor (HNIC)

Page 06 EMERGING MANUFACTURING HUB

Source : Socio Economic Outlook 2015, Government of Telangana Planning Department

Table 2 - District-wise focus on Industries

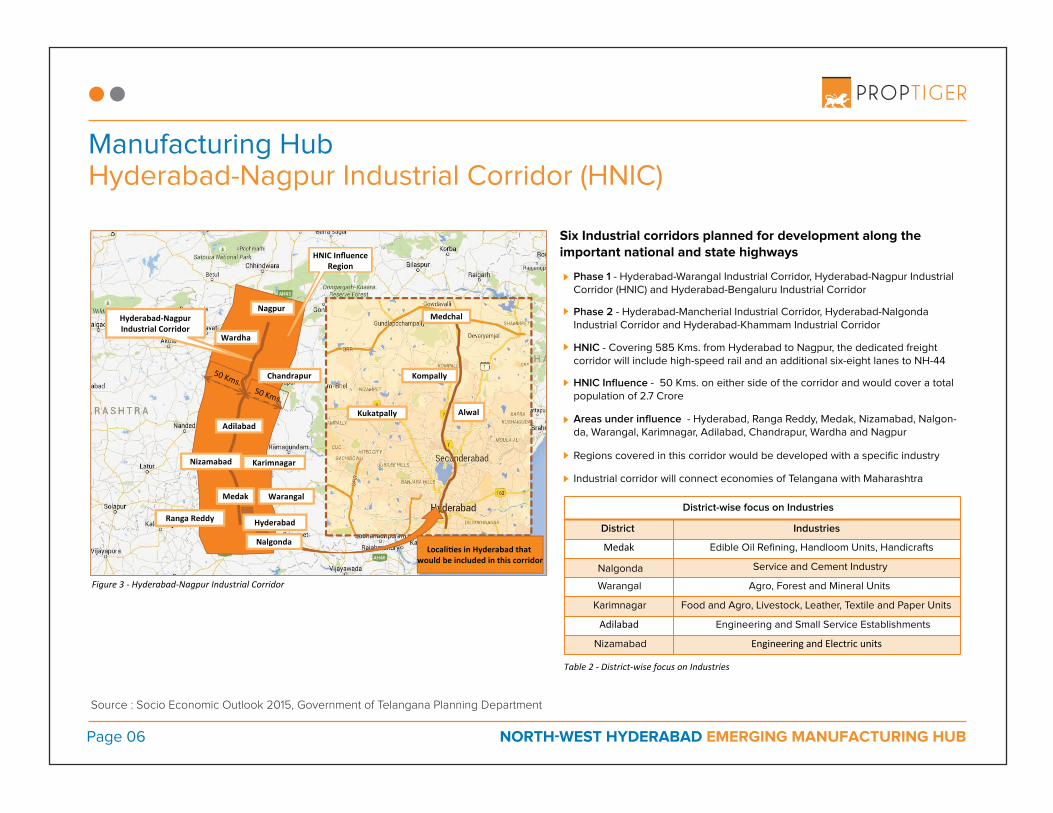

District-wise focus on Industries

IndustriesDistrict

Medak Edible Oil Refining, Handloom Units, Handicrafts

Nalgonda Service and Cement Industry

Warangal Agro, Forest and Mineral Units

Karimnagar Food and Agro, Livestock, Leather, Textile and Paper Units

Adilabad Engineering and Small Service Establishments

Nizamabad Engineering and Electric units

Six Industrial corridors planned for development along the important national and state highways

Phase 1 - Hyderabad-Warangal Industrial Corridor, Hyderabad-Nagpur Industrial Corridor (HNIC) and Hyderabad-Bengaluru Industrial Corridor

Phase 2 - Hyderabad-Mancherial Industrial Corridor, Hyderabad-Nalgonda Industrial Corridor and Hyderabad-Khammam Industrial Corridor

HNIC - Covering 585 Kms. from Hyderabad to Nagpur, the dedicated freight corridor will include high-speed rail and an additional six-eight lanes to NH-44

HNIC Influence - 50 Kms. on either side of the corridor and would cover a total population of 2.7 Crore

Areas under influence - Hyderabad, Ranga Reddy, Medak, Nizamabad, Nalgon-da, Warangal, Karimnagar, Adilabad, Chandrapur, Wardha and Nagpur

Regions covered in this corridor would be developed with a specific industry

Industrial corridor will connect economies of Telangana with Maharashtra

50 Kms.50 Kms.

Kompally

AlwalKukatpally

HNIC InfluenceRegion

Hyderabad-Nagpur Industrial CorridorFigure 3 -

MedchalNagpur

Hyderabad-NagpurIndustrial Corridor

Wardha

Chandrapur

Adilabad

Nizamabad Karimnagar

Medak Warangal

HyderabadRanga Reddy

NalgondaLocali es in Hyderabad that

would be included in this corridor

Manufacturing HubITIR (Information Technology Investment Region)

Page 07 EMERGING MANUFACTURING HUB

Source : Proptiger DataLabs Research

ITIR

Approved jointly by Govt. of India and Govt. of Telangana in September 2013 to promote investment in IT/ITeS and electronic hardware sector, expected to be completed over a period of 25 years in 2 phases

As per the new proposal of Telangana Govt., ITIR will now be developed all along the ORR, where the government is already in the process of crea ng Transit Oriental Growth Corridors (TOGC).

The government lands would be iden fied in one kilometre range on both sides of the ORR and they would be marked for industrial purpose, so as to reduce the hassle of land conversion

Planned to include IT SEZs, IT parks, industrial parks, warehouses and export oriented zones and is expected to create direct employment of ~15 lakhs and indirect employment of ~50 lakhs

Promoted by the Central government’s financial assistance, where Centre will release Rs. 50 Crore for every 100 acre land in the ITIR and is expected to generate IT exports of Rs. 2.35 Lakh Crore.

Figure 4 – Upcoming ITIR

Tellapur

Chanda Nagar

Miyapur

Nizampet

Bachupalli

Medchal

Kompally

Bolarum

Alwal

Bowenpally

Balamrai

Kukatpally

Mo NagarSanath Nagar

Patancheru

1 KM

1 KM

Outer Ring Road

ITIR

Approved jointly by Govt. of India and Govt. of Telangana in Septem-ber 2013 to promote investment in IT/ITeS and electronic hardware sector, expected to be completed over a period of 25 years in 2 phases

To be developed along the ORR, where the government is already in the process of creating Transit Oriental Growth Corridors (TOGC)

Govt. land, within 1 Km. range of both sides of ORR, will be identified and marked for industrial purpose, so as to reduce the hassle of land conversion

Planned to include IT/ITeS SEZs, IT parks, industrial parks, warehouses and export oriented zones and is expected to create direct employment of ~15 lakhs and indirect employment of ~50 lakhs

Promoted by the Central government’s financial assistance, where Centre will release Rs. 50 Crore for every 100 acre land in the ITIR and is expected to generate IT/ITeS exports of Rs. 2.35 Lakh Crore.

Upcoming InfrastructureOuter Ring Road, Suburban Railways and Hyderabad Metro

Page 08 NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB

Outer Ring Road

Suburban Railways

Hyderabad Metro

Figure 5 - Upcoming Infrastructure

Shamirpet

Ghatkesar

Patancheru

Tellapur

Miyapur

Sanathnagar

Begumpet

Falaknuma

Medchal

Shamshabad

Bolarum

Sitaphal Mandi

Secunderabad

Shilpamaram

LB Nagar

Nagole

Source : Proptiger DataLabs Research

Upcoming InfrastructureOuter Ring Road

Page 09 EMERGING MANUFACTURING HUB

Shamirpet

Keesara

Ghatkesar

Patancheru

Exis ng

Upcoming

21.3 Kms

Figure 6 - ORR

158 kms. In length with a width of 150m, ORR is an 8-lane fenced expressway which has 33 radial roads that connect it with the Inner Ring Road and the upcoming Regional Ring Road

21.3 Kms. stretch of ORR, to be completed by Dec’16, will improve connectivity of North-West Hyderabad with upcoming IT/ITeS hubs of East Hyderabad

State-run Telangana State Road Transport Corporation (TSRTC) is planning to build 22 terminals-cum-depots (TCD) along the Outer Ring Road

Source : Proptiger DataLabs Research

Upcoming InfrastructureMMTS – Suburban Rail Network

Page 10 EMERGING MANUFACTURING HUB

Source : Proptiger DataLabs Research

Stage StretchCost

(Rs.Crore)Length (Kms.)

1

Tellapur-Patancheru 32 5.5

Secunderabad-Bolarum 30 14.0

Sanathnagar-Moula Ali 170

2 Bolarum-Medchal 74 14.0

Exis ng Suburban Rail

Proposed Suburban Rail

Patancheru

TellapurLingampally

Sanathnagar

Begumpet

Hyderabad Ctrl. Jn.

Secunderabad

MalkajgiriMoula Ali

Medchal

Bolarum

Table 3 - List of suburban rail networks

Figure 7 - Upcoming Suburban Railway Sta ons

22.4

Upcoming InfrastructureHyderabad Metro

Page 11 EMERGING MANUFACTURING HUB

Source : Proptiger DataLabs Research

1

MiyapurKPHB

SR Nagar

LB Nagar

Figure 8 – Proposed Metro Route

To be built on PPP-basis by Central Govt. and L&T, the 72 Kms. long project is estimated to cost Rs.14,132 Crore, to be operational by 2016

With a frequency of 3 to 5 minutes during peak hours, Metro is expected to carry about 17 lakh passengers per day by 2017 and 22 lakh by 2024

L&T has planned to develop 18.5 million sq.ft. of realty space in a phased manner in sync with market requirements over the next 8-10 years, across ~20 locations in different micro markets of Hyderabad

About 1.1 million sq.ft. of high quality retail and office space is underway in the first phase across three locations- Punjagutta, Erramanzil and Hi-Tec City, to be commissioned in 2016

Hyderabad Metro Rail is expected to reduce the tra�c from the high density corridors of North-Western region

Real Estate LandscapeSupply & Pricing

Page 12 NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB

Source : Proptiger DataLabs Research

Note: 1. Analysis includes Apartments and Villas across the region 2. Price weighed on number of BHK units in respective projects

18%

42%

4+ BHK

Apr-Dec’ 13 CY 2014 CY 2015

39%

1%

9%

53%

36%

2%

7%

61%

32%

3 BHK 2 BHK 1 BHK

100%

80%

60%

40%

20%

0%

% of total launches

Figure 9 - Residential units launched since 2013 in North-West Hyderabad1

2,000

Q2

CY

’ 13

3,0003,097

3,928

3,085

4,000

5,000

Q3

CY

’ 13

Q4

CY

’ 13

Q1

CY

’ 14

Q2

CY

’ 14

Q3

CY

’ 14

Q4

CY

’ 14

Q1

CY

’ 15

Q2

CY

’ 15

Q3

CY

’ 15

Q4

CY

’ 15

3,135 3,168 3,182 3,196 3,215 3,236 3,257 3,278 3,317

3,8514,024 4,029 4,069

4,101 4,070 4,086 4,009 4,041 4,093

Apartments VillasBSP (Rs./sq.ft.)

Figure 10 - Wt. avg. BSP (Rs./sq.ft.) of residential units since 2013 in North-West Hyderabad

Analysis of Launches in North-West Hyderabad

Emerging real estate hub as ~40% of launches in Hyderabad have been concentrated in this region

Apartments accounted for nearly 65% of the total launches since 2013

Over 50% of launches have been in the 3-BHK category while 2 and 4-BHK have contributed ~36% and ~12% since 2013

Kondapur, Miyapur and Kompally are the prime localities in the region contributing 45% to the overall launches in the region since 2013

~80% of under-construction units will be complete by 2017. Out of these, 47% will be 2-BHK and 35% will be 3-BHK

Analysis of Pricing in North-West Hyderabad

Apartments are priced in the range of Rs.3,000 - 3,320 psf while villas are priced at Rs.3,900 -4,100 psf.

While 90% of the projects in the region are in the affordable segment, a few luxury projects have been launched in Kukatpally and Kondapur in the Rs.8,700-9,000 psf. price range

Kondapur, Chandanagar and Tellapur have witnessed a price appreciation of 10-18% over the last 12 months

1 2

Real Estate LandscapeAbsorption & Inventory

Page 13 NORTH-WEST HYDERABAD EMERGING MANUFACTURING HUB

Source : Proptiger DataLabs Research

45%

14%

4+ BHK

Apr-Dec’ 13 CY 2014 CY 2015

40%

1%

45%

15%

39%

1%

47%

38%

1%

3 BHK 2 BHK 1 BHK

100%

80%

60%

40%

20%

0%

% of units in inventory

Figure 12 - Unsold Inventory of residential units since April 2013 in North-West Hyderabad

14%

1

10%

49%

4+ BHK

Apr-Dec’ 13 CY 2014 CY 2015

39%

2%

9%

50%

39%

2%

10%

51%

38%

1%

3 BHK 2 BHK 1 BHK

100%

80%

60%

40%

20%

0%

% of absorbed units

Figure 11 - Residential units sold since April 2013 in North-West Hyderabad1

Analysis of Sales in North-West Hyderabad

Region accounts for ~44% of absorption in Hyderabad across apartments and villas from April’13 till Dec’15

69% of units sold over the last 12 months have been apartments

Consistent in-line with the launches, 3-BHK units have dominated the absorption of last 12 months contributing ~50% to the total sales in the region, followed by 2-BHK (39%)

Kukatpally, Miyapur, Kompally and Bachupally are the top grossers in terms of absorption across localities with over 50% contribution of total sales over the last 12 months

Analysis of Inventory in North-West Hyderabad

44% of Hyderabad’s inventory is stacked up in the North-Western region wherein 34% of units were launched in last 12 months

Apartments constitute 75% of inventory in the region, wherein ~40% are 2-BHK units and ~45% are 3-BHK units

Kukatpally, Kondapur, Kompally and Bachupally together contribute 60% of North-West Hyderabad’s inventory

Note: 1. Analysis includes Apartments and Villas across the region

DISCLAIMERAll data, figures, information provided hereto are provided and/or collated by Proptiger.com and that any of its representatives, o�cers, employees or a�liates makes no representations or warranties as to the accuracy or completeness of any information furnished hereto. This report has been prepared by Proptiger Data Labs solely for information purposes. It does not purport to be a complete description of the markets or developments contained in this material. The information on which this report is based has been obtained from sources that Proptiger believes in its reasonable bona fide faith to be reliable, but Proptiger has not independently verified such information and do not guarantee/ warranty the accuracy, genuineness or completeness of the information therein. This report contains information available to the public and has been relied upon by Proptiger on the basis that it is accurate and complete. Information contained herein should not, in whole or part, be published, reproduced or referred to without prior approval. Proptiger accepts no responsibility if this should prove not to be the case. Any such reproduction should be credited to Proptiger Data labs. ©2015 Proptiger.com . All rights reserved LIMITATION OF WARRANTY

The Information is provided “as is”, without warranty of any kind, it has not been independently verified by Proptiger or Its A�liates, O�cers, Employees or Agents and use of the Information is at your sole risk. Proptiger or Its A�liates, O�cers, Employees or Agents shall not be liable and expressly disclaim liability for any error or omission in the content of the Information, or for any actions taken by you or any third party, in reliance thereon. The Information is not guaranteed to be error-free, or to be relied upon for investment purposes, and Proptiger or Its A�liates, O�cers, Employees or Agents make no representation or warranty as to the accuracy, truth, adequacy, timeliness or completeness, fitness for purpose, title, non-infringement of third party rights or continued availability of the Information, withdrawal without notice and to any special conditions imposed by our principals.

ANURAG JHANWARHead – Consulting and Data Insights [email protected]+91 - 99678 49666

SUNIL MISHRAChief Business O�cer - Primary Business & Developer [email protected]+91 - 90044 40011

CONTACT PROPTIGER FOR REAL ESTATE INSIGHTS:

Detailed analysis of micro markets | Market Intelligence Report | Micro market surveys | Price Sensitivity analysis| City Dashboards and trends | Demand assessment