24

www. eidebailly.com Financial Statements June 30, 2017 and 2016 Northwest Iowa Mental Health Center d/b/a Seasons Center For Behavioral Health

www.eidebai l ly.com

Financial Statements June 30, 2017 and 2016

Northwest Iowa Mental Health Center d/b/a Seasons Center For Behavioral Health

Northwest Iowa Mental Health Center Table of Contents

June 30, 2017 and 2016

Board of Directors ...................................................................................................................................................... 1

Independent Auditor’s Report .................................................................................................................................... 2

Financial Statements

Statements of Financial Position ............................................................................................................................ 4 Statements of Activities ......................................................................................................................................... 5 Statement of Functional Expenses ......................................................................................................................... 6 Statements of Cash Flows ...................................................................................................................................... 8 Notes to Financial Statements ................................................................................................................................ 9

1

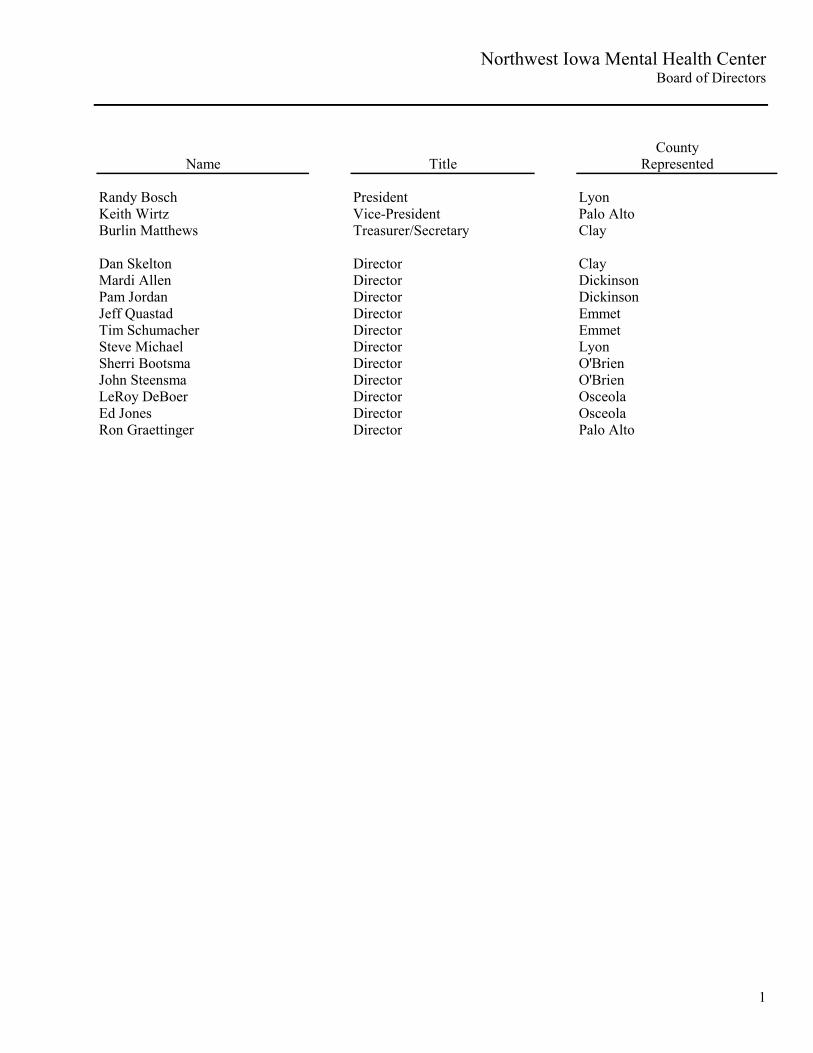

Northwest Iowa Mental Health Center Board of Directors

Randy Bosch President LyonKeith Wirtz Vice-President Palo AltoBurlin Matthews Treasurer/Secretary Clay

Dan Skelton Director ClayMardi Allen Director DickinsonPam Jordan Director DickinsonJeff Quastad Director EmmetTim Schumacher Director EmmetSteve Michael Director LyonSherri Bootsma Director O'BrienJohn Steensma Director O'BrienLeRoy DeBoer Director OsceolaEd Jones Director OsceolaRon Graettinger Director Palo Alto

CountyRepresentedTitleName

What inspires you, inspires us. Let’s talk. | eidebailly.com200 E. 10th St., Ste. 500 | P.O. Box 5125 | Sioux Falls, SD 57117-5125 | T 605.339.1999 | F 605.339.1306 | EOE

2

Independent Auditor’s Report

To the Board of Directors Northwest Iowa Mental Health Center d/b/a Seasons Center For Behavioral Health Spencer, Iowa

Report on the Financial Statements We have audited the accompanying financial statements of Northwest Iowa Mental Health Center d/b/a Seasons Center For Behavioral Health, (Center) which comprise the statements of financial position as of June 30, 2017 and 2016, and the related statements of activities, functional expenses, and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Northwest Iowa Mental Health Center d/b/a Seasons Center For Behavioral Health as of June 30, 2017 and 2016, and the changes in its net assets and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

3

Emphasis of Matter Regarding Restatement of the June 30, 2016 Financial Statements As discussed in Note 11 to the financial statements, the June 30, 2016 financial statements have been restated to properly record a receivable and restricted revenue for grant funds earned in 2016 but not recorded until 2017. In addition the June 30, 2016 financial statements were also restated to reduce a receivable and grant revenue for unearned grants. Our opinion is not modified with respect to this matter. Emphasis of Matter Regarding Going Concern The accompanying financial statements have been prepared assuming that Northwest Iowa Mental Health Center d/b/a Seasons Center for Behavioral Health will continue as a going concern. As discussed in Note 12 to the financial statements, the Center has suffered a material operating loss in its unrestricted net assets as reported in the statement of activities. The Center also has a low amount of cash and cash equivalents on hand as of June 30, 2017 and material lines of credit which mature on March 27, 2018. These conditions raise substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 12. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to this matter. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated February 15, 2018 on our consideration of Northwest Iowa Mental Health Center, d/b/a Seasons Center For Behavioral Health’s internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Northwest Iowa Mental Health Center d/b/a Seasons Center For Behavioral Health’s internal control over financial reporting and compliance.

Sioux Falls, South Dakota February 15, 2018

See Notes to Financial Statements 4

Northwest Iowa Mental Health Center Statements of Financial Position

June 30, 2017 and 2016

2017 2016Assets (As Restated)

Current AssetsCash and cash equivalents 94,435$ 311,932$ Receivables

Patient, net of estimated uncollectiblesof $175,000 in 2017 and $120,000 in 2016 954,989 1,138,392

Counties and other governmental agencies 989,621 513,485 Promises to give, current portion 118,516 96,791

Prepaid expenses 141,016 116,311

Total current assets 2,298,577 2,176,911

Property and Equipment, net 5,541,134 2,922,306

Other AssetsPromises to give, net 117,836 110,201

Total assets 7,957,547$ 5,209,418$

Liabilities and Net Assets

Current LiabilitiesCurrent maturities of long-term debt 178,918$ 206,658$ Lines of credit 2,399,756 150,000Accounts payable

Trade 129,825 69,721 Construction - 381,836

Accrued expensesSalaries and wages 111,361 72,513 Vacation 290,644 186,737 Payroll taxes and other 130,268 108,842 Deferred revenue 150,500 -

Total current liabilities 3,391,272 1,176,307

Long-Term LiabilitiesLong-Term Debt, Less Current Maturities 875,519 657,048

Total liabilities 4,266,791 1,833,355

Net Assets Unrestricted 2,517,722 3,056,413

Temporarily restricted 1,173,034 319,650

Total net assets 3,690,756 3,376,063

Total liabilities and net assets 7,957,547$ 5,209,418$

See Notes to Financial Statements

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Public Support and RevenuesPublic support

State and local government 886,924$ -$ -$ 886,924$ Grants 1,118,105 853,384 - 1,971,489 Contributions 154,046 314,135 - 468,181

Total public support 2,159,075 1,167,519 - 3,326,594

RevenuesPatient services 6,080,256 - - 6,080,256 Other program and fee income 185,371 - - 185,371

Total revenues 6,265,627 - - 6,265,627

Total public support and revenues 8,424,702 1,167,519 - 9,592,221

ExpensesOutpatient care 2,011,791 - - 2,011,791 Psychiatric 1,829,792 - - 1,829,792 Community support 282,615 - - 282,615 Case management - - - - Psychological testing 259,749 - - 259,749 Substance abuse 522,258 - - 522,258 Integrated health home 1,351,296 - - 1,351,296 Juvenile court 348,937 - - 348,937 Fundraising 27,481 - - 27,481 Regional partnership grant 476,349 - - 476,349 Other 530,845 - - 530,845 Administration 1,640,599 - - 1,640,599

Total expenses 9,281,712 - - 9,281,712

Operating Income (Loss) (857,010) 1,167,519 - 310,509

Other Income Investment income 4,184 - - 4,184

Revenue in Excess of (less than) Expenses (852,826) 1,167,519 - 314,693

Net Assets Released from Restrictionsfor Capital 314,135 (314,135) - -

Change in Net Assets (538,691) 853,384 - 314,693

Net Assets, Beginning of Year 3,056,413 319,650 - 3,376,063

Net Assets, End of Year 2,517,722$ 1,173,034$ -$ 3,690,756$

2017

5

Northwest Iowa Mental Health Center Statements of Activities

Years ended June 30, 2017 and 2016

Temporarily PermanentlyUnrestricted Restricted Restricted Total

693,296$ -$ -$ 693,296$ 955,351 319,650 - 1,275,001

45,099 158,117 - 203,216

1,693,746 477,767 - 2,171,513

5,473,285 - - 5,473,285 222,007 - - 222,007

5,695,292 - - 5,695,292

7,389,038 477,767 - 7,866,805

1,320,498 - - 1,320,498 1,176,453 - - 1,176,453

240,971 - - 240,971 183,427 - - 183,427 197,225 - - 197,225 341,985 - - 341,985

1,112,335 - - 1,112,335 334,524 - - 334,524

73,701 - - 73,701 607,294 - - 607,294 436,443 - - 436,443

1,228,510 - - 1,228,510

7,253,364 - - 7,253,364

135,674 477,767 - 613,441

1,042 - - 1,042

136,716 477,767 - 614,483

880,601 (880,601) - -

1,017,317 (402,834) - 614,483

2,039,096 722,484 - 2,761,580

3,056,413$ 319,650$ -$ 3,376,063$

2016 (As Restated)

See Notes to Financial Statements

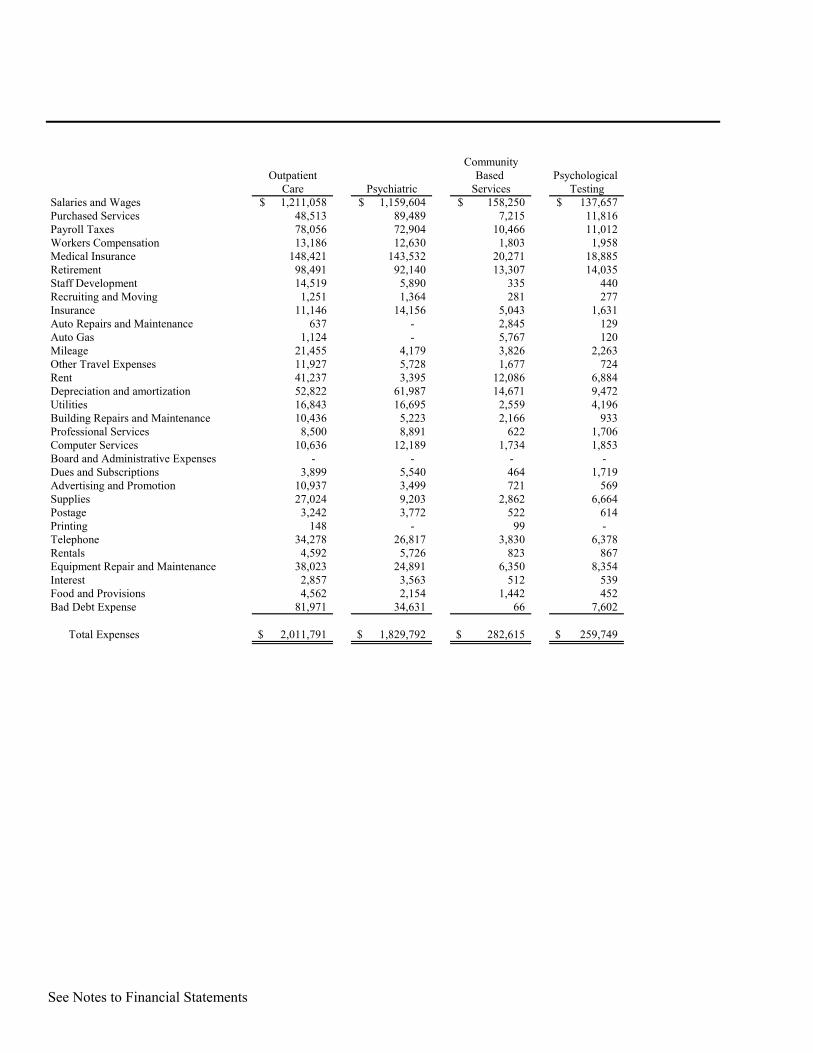

CommunityOutpatient Based Psychological

Care Psychiatric Services TestingSalaries and Wages 1,211,058$ 1,159,604$ 158,250$ 137,657$ Purchased Services 48,513 89,489 7,215 11,816 Payroll Taxes 78,056 72,904 10,466 11,012 Workers Compensation 13,186 12,630 1,803 1,958 Medical Insurance 148,421 143,532 20,271 18,885 Retirement 98,491 92,140 13,307 14,035 Staff Development 14,519 5,890 335 440 Recruiting and Moving 1,251 1,364 281 277 Insurance 11,146 14,156 5,043 1,631 Auto Repairs and Maintenance 637 - 2,845 129 Auto Gas 1,124 - 5,767 120 Mileage 21,455 4,179 3,826 2,263 Other Travel Expenses 11,927 5,728 1,677 724 Rent 41,237 3,395 12,086 6,884 Depreciation and amortization 52,822 61,987 14,671 9,472 Utilities 16,843 16,695 2,559 4,196 Building Repairs and Maintenance 10,436 5,223 2,166 933 Professional Services 8,500 8,891 622 1,706 Computer Services 10,636 12,189 1,734 1,853 Board and Administrative Expenses - - - - Dues and Subscriptions 3,899 5,540 464 1,719 Advertising and Promotion 10,937 3,499 721 569 Supplies 27,024 9,203 2,862 6,664 Postage 3,242 3,772 522 614 Printing 148 - 99 - Telephone 34,278 26,817 3,830 6,378 Rentals 4,592 5,726 823 867 Equipment Repair and Maintenance 38,023 24,891 6,350 8,354 Interest 2,857 3,563 512 539 Food and Provisions 4,562 2,154 1,442 452 Bad Debt Expense 81,971 34,631 66 7,602

Total Expenses 2,011,791$ 1,829,792$ 282,615$ 259,749$

6

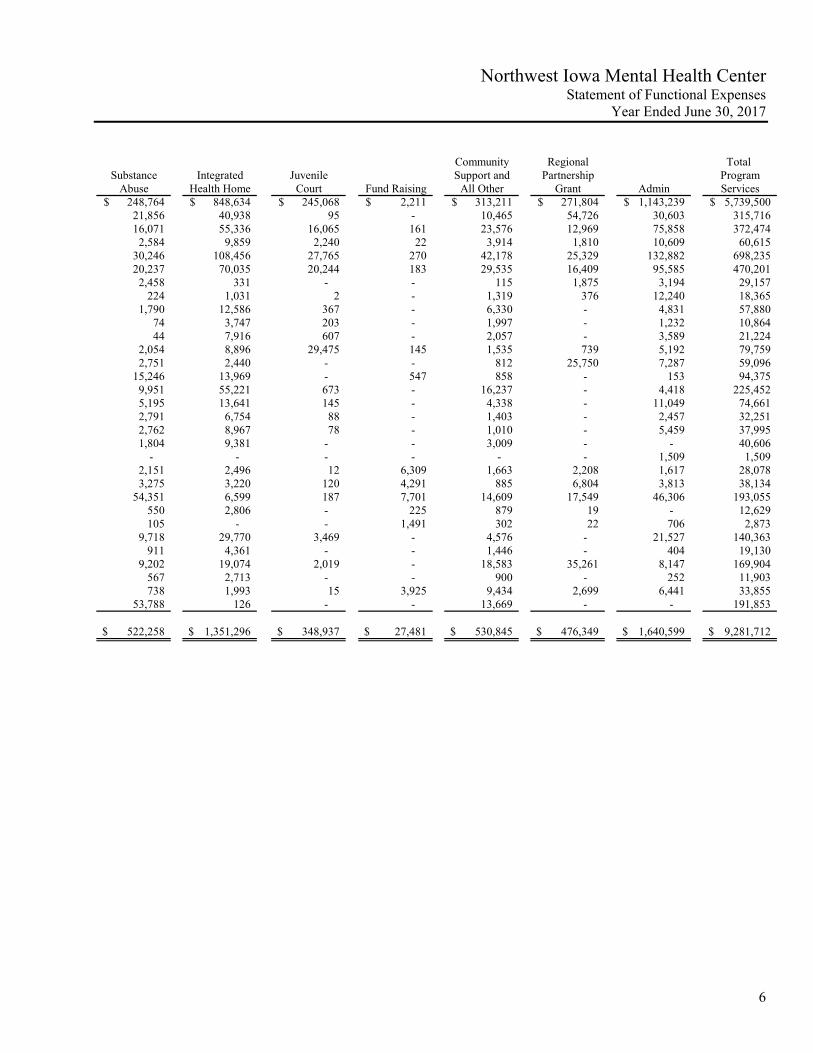

Northwest Iowa Mental Health Center Statement of Functional Expenses

Year Ended June 30, 2017

Community Regional Total Substance Integrated Juvenile Support and Partnership Program

Abuse Health Home Court Fund Raising All Other Grant Admin Services248,764$ 848,634$ 245,068$ 2,211$ 313,211$ 271,804$ 1,143,239$ 5,739,500$

21,856 40,938 95 - 10,465 54,726 30,603 315,716 16,071 55,336 16,065 161 23,576 12,969 75,858 372,474

2,584 9,859 2,240 22 3,914 1,810 10,609 60,615 30,246 108,456 27,765 270 42,178 25,329 132,882 698,235 20,237 70,035 20,244 183 29,535 16,409 95,585 470,201

2,458 331 - - 115 1,875 3,194 29,157 224 1,031 2 - 1,319 376 12,240 18,365

1,790 12,586 367 - 6,330 - 4,831 57,880 74 3,747 203 - 1,997 - 1,232 10,864 44 7,916 607 - 2,057 - 3,589 21,224

2,054 8,896 29,475 145 1,535 739 5,192 79,759 2,751 2,440 - - 812 25,750 7,287 59,096

15,246 13,969 - 547 858 - 153 94,375 9,951 55,221 673 - 16,237 - 4,418 225,452 5,195 13,641 145 - 4,338 - 11,049 74,661 2,791 6,754 88 - 1,403 - 2,457 32,251 2,762 8,967 78 - 1,010 - 5,459 37,995 1,804 9,381 - - 3,009 - - 40,606

- - - - - - 1,509 1,509 2,151 2,496 12 6,309 1,663 2,208 1,617 28,078 3,275 3,220 120 4,291 885 6,804 3,813 38,134

54,351 6,599 187 7,701 14,609 17,549 46,306 193,055 550 2,806 - 225 879 19 - 12,629 105 - - 1,491 302 22 706 2,873

9,718 29,770 3,469 - 4,576 - 21,527 140,363 911 4,361 - - 1,446 - 404 19,130

9,202 19,074 2,019 - 18,583 35,261 8,147 169,904 567 2,713 - - 900 - 252 11,903 738 1,993 15 3,925 9,434 2,699 6,441 33,855

53,788 126 - - 13,669 - - 191,853

522,258$ 1,351,296$ 348,937$ 27,481$ 530,845$ 476,349$ 1,640,599$ 9,281,712$

See Notes to Financial Statements

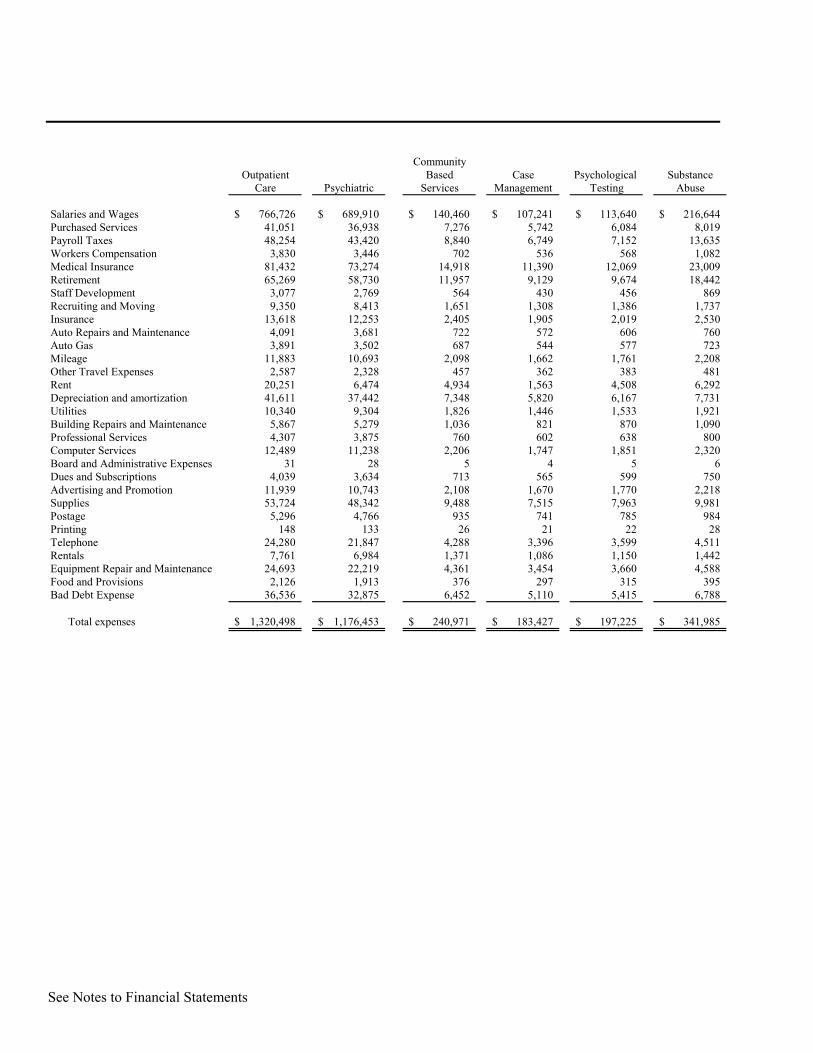

CommunityOutpatient Based Case Psychological Substance

Care Psychiatric Services Management Testing Abuse

Salaries and Wages 766,726$ 689,910$ 140,460$ 107,241$ 113,640$ 216,644$ Purchased Services 41,051 36,938 7,276 5,742 6,084 8,019 Payroll Taxes 48,254 43,420 8,840 6,749 7,152 13,635 Workers Compensation 3,830 3,446 702 536 568 1,082 Medical Insurance 81,432 73,274 14,918 11,390 12,069 23,009 Retirement 65,269 58,730 11,957 9,129 9,674 18,442 Staff Development 3,077 2,769 564 430 456 869 Recruiting and Moving 9,350 8,413 1,651 1,308 1,386 1,737 Insurance 13,618 12,253 2,405 1,905 2,019 2,530 Auto Repairs and Maintenance 4,091 3,681 722 572 606 760 Auto Gas 3,891 3,502 687 544 577 723 Mileage 11,883 10,693 2,098 1,662 1,761 2,208 Other Travel Expenses 2,587 2,328 457 362 383 481 Rent 20,251 6,474 4,934 1,563 4,508 6,292 Depreciation and amortization 41,611 37,442 7,348 5,820 6,167 7,731 Utilities 10,340 9,304 1,826 1,446 1,533 1,921 Building Repairs and Maintenance 5,867 5,279 1,036 821 870 1,090 Professional Services 4,307 3,875 760 602 638 800 Computer Services 12,489 11,238 2,206 1,747 1,851 2,320 Board and Administrative Expenses 31 28 5 4 5 6 Dues and Subscriptions 4,039 3,634 713 565 599 750 Advertising and Promotion 11,939 10,743 2,108 1,670 1,770 2,218 Supplies 53,724 48,342 9,488 7,515 7,963 9,981 Postage 5,296 4,766 935 741 785 984 Printing 148 133 26 21 22 28 Telephone 24,280 21,847 4,288 3,396 3,599 4,511 Rentals 7,761 6,984 1,371 1,086 1,150 1,442 Equipment Repair and Maintenance 24,693 22,219 4,361 3,454 3,660 4,588 Food and Provisions 2,126 1,913 376 297 315 395 Bad Debt Expense 36,536 32,875 6,452 5,110 5,415 6,788

Total expenses 1,320,498$ 1,176,453$ 240,971$ 183,427$ 197,225$ 341,985$

7

Northwest Iowa Mental Health Center Statement of Functional Expenses

Year Ended June 30, 2016

Regional Community Total Partnership Support and Program

Grant All Other Admin Services

248,709$ 270,093$ 855,388$ 4,318,148$ 142,956 9,921 17,505 322,675

17,561 17,162 91,880 314,119 2,424 1,610 8,378 28,379

24,495 38,832 84,516 458,620 20,309 25,115 71,988 367,592 18,234 6,537 4,012 39,651 18,393 1,809 9,026 61,181

- 2,608 4,567 53,715 19 783 1,833 16,739 98 745 3,120 17,435

1,979 10,623 8,107 94,322 27,091 759 679 37,334

4,548 1,468 (170) 53,439 - 7,969 1,487 151,493 - 1,980 11,716 48,901 - 1,124 2,767 23,909

37 843 4,794 20,401 1,000 2,392 - 45,907

- 6 1,159 1,269 4,118 773 1,012 24,279

12,437 2,286 4,590 64,118 45,710 10,309 8,577 266,265

83 1,026 49 19,413 723 28 - 2,219

- 5,822 22,706 116,121 - 1,486 - 27,907

892 4,782 5,453 96,804 15,478 552 3,370 29,647

- 6,997 - 131,366

607,294$ 436,443$ 1,228,510$ 7,253,364$

See Notes to Financial Statements 8

Northwest Iowa Mental Health Center Statements of Cash Flows

Years Ended June 30, 2017 and 2016

2017 2016(As Restated)

Operating ActivitiesChange in net assets 314,693$ 614,483$ Adjustments to reconcile change in net assets to net cash

from operating activitiesDepreciation and amortization 225,452 151,493 Bad debt expense 191,853 131,366 Forgiveness of debt (100,000) - Contributions restricted by donors (1,167,519) (477,767)

Changes in assets and liabilitiesAccounts receivable - patients (8,450) (517,047) Accounts receivable - counties and other

governmental agencies (132,084) (458) Prepaid expenses (24,705) (16,490) Accounts payable 60,104 (33,211) Accrued expenses 164,181 (55,798) Deferred revenue 150,500 -

Net Cash used for Operating Activities (325,975) (203,429)

Investing ActivitiesPurchase of property and equipment (2,861,011) (1,792,116)

Financing ActivitiesChange in promises to give (29,360) 160,379 Contributions restricted by donors 823,467 228,785 Change in lines of credit 2,249,756 150,000 Proceeds from issuance of debt - 775,000 Principal payments on long-term debt (74,374) (21,294)

Net Cash from Financing Activities 2,969,489 1,292,870

Net Change in Cash and Cash Equivalents (217,497) (702,675)

Cash and Cash Equivalents, Beginning of Year 311,932 1,014,607

Cash and Cash Equivalents, End of Year 94,435$ 311,932$

Supplemental Disclosure of Non-cash Investing and Financing ActivityAccounts payable - construction -$ 381,836$

Equipment financed through capital lease arrangements 95,002$ -$

Property acquired through the issuance of notes payable 270,103$ -$

Supplemental Disclosure of Cash Flow InformationCash paid during the year for interest, net of amountscapitalized of $47,634 and $20,744 -$ -$

9

Northwest Iowa Mental Health Center Notes to Financial Statements

June 30, 2017 and 2016 Note 1 - Organization and Significant Accounting Policies Organization Northwest Iowa Mental Health Center, d/b/a Seasons Center For Behavioral Health (Center) is a non-profit corporation established to provide a comprehensive community mental health program for the diagnosis and treatment of psychiatric and psychological disorders and to promote the prevention of mental illness. The Center provides these services to individuals in a ten-county area which includes Buena Vista, Clay, Dickinson, Emmet, Lyon, O’Brien, Osceola, Palo Alto, Sioux, and Woodbury counties. Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Cash and Cash Equivalents Cash and cash equivalents include highly liquid investments with an original maturity of three months or less. Patient Receivables and Credit Policies Accounts receivable consist primarily of uncollateralized individual and third-party payor obligations. Unpaid accounts receivable are not charged interest on amounts owed. Payments of patient receivables are allocated to the specific claims identified on the remittance advice or, if unspecified, are applied to the earliest unpaid claim. The carrying amount of patient receivables is reduced by a valuation allowance that reflects management’s estimate of amounts that will not be collected from patients and third-party payors. Management reviews patient receivables by payor class and applies percentages to determine estimated amounts that will not be collected from third parties under contractual agreements and amounts that will not be collected from clients due to bad debts. Accounts receivable are written off when deemed uncollectible. Revenue and Revenue Recognition Revenue is recognized when earned. Program service fees and payments under contracts or grants received in advance are deferred to the applicable period in which the related services are performed or expenditures are incurred, respectively. Contributions are recognized when cash, securities or other assets, an unconditional promise to give, or notification of a beneficial interest is received. Conditional promises to give are not recognized until the conditions on which they depend have been substantially met. Promises to Give Unconditional promises to give are initially recorded and subsequently carried at fair value using present value techniques incorporating risk-adjusted discount rates designed to reflect the assumptions market participants would use in pricing the asset.

10

Northwest Iowa Mental Health Center Notes to Financial Statements

June 30, 2017 and 2016 Property and Equipment Property and equipment additions over $5,000 are recorded at cost, or if donated, at fair value on the date of donation. Depreciation and amortization are computed using the straight-line method over the estimated useful lives of the assets ranging from four to fifty years, or in the case of capitalized leased assets or leasehold improvements, the lesser of the useful life of the asset or the lease term. When assets are sold or otherwise disposed of, the cost and related depreciation or amortization are removed from the accounts, and any resulting gain or loss is included in the statements of activities. Costs of maintenance and repairs that do not improve or extend the useful lives of the respective assets are expensed currently. The carrying values of property and equipment are reviewed for impairment whenever events or circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. When considered impaired, an impairment loss is recognized to the extent carrying value exceeds the fair value of the asset. The Center has determined that certain long-lived assets were impaired during the year ended June 30, 2017, and has recorded an impairment loss of $26,791 at June 30, 2017. The impairment loss was included in depreciation and amortization in the statement of activities. There were no indicators of asset impairment during the year ended June 30, 2016. Net Assets Net assets, revenues, gains, and losses are classified based on the existence or absence of donor-imposed restrictions. Accordingly, net assets and changes therein are classified and reported as follows:

Unrestricted Net Assets – Net assets available for use in general operations. Temporarily Restricted Net Assets – Net assets subject to donor restrictions that may or will be met by expenditures or actions of the Center and/or the passage of time. The Center reports contributions as temporarily restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions.

Permanently Restricted Net Assets – Net assets whose use is limited by donor-imposed restrictions that neither expire by the passage of time nor can be fulfilled or otherwise removed by action of the Center. As of June 30, 2017 and 2016, the Center did not have any permanently restricted net assets.

11

Northwest Iowa Mental Health Center Notes to Financial Statements

June 30, 2017 and 2016 Accounting for Income Taxes The Center is organized as an Iowa non-profit corporation and has been recognized by the Internal Revenue Service (IRS) as exempt from federal income taxes under Internal Revenue Code Section 501(c)(3). The Center is annually required to file a Return of Organization Exempt from Income Tax (Form 990) with the IRS. In addition, the Center is subject to income tax on net income that is derived from business activities that are unrelated to its exempt purpose. The Center has determined that it is not subject to unrelated business income tax and has not filed an Exempt Organization Business Income Tax Return (Form 990T) with the IRS. The Center believes that it has appropriate support for any tax positions taken affecting its annual filing requirements, and as such, does not have any uncertain tax positions that are material to the financial statements. The Center would recognize future accrued interest and penalties related to unrecognized tax benefits and liabilities in income tax expense if such interest and penalties are incurred. Advertising Costs Costs incurred for producing and distributing advertising is expensed as incurred. The Center incurred $15,790 and $36,288 for advertising costs for the years ended June 30, 2017 and 2016. Functional Allocation of Expenses The costs of providing the various programs and activities have been summarized on a functional basis in the statements of activities. Accordingly, certain costs have been allocated among the programs and supporting services benefited. Subsequent Events Subsequent events have been evaluated through February 15, 2018, the date the financial statements were available to be issued. Note 2 - Property and Equipment A summary of property and equipment at June 30, 2017 and 2016, is as follows:

Accumulated Accumulated Cost Depreciation Cost Depreciation

Land 622,140$ -$ 83,300$ -$ Buildings and improvement 5,453,830 883,119 1,954,721 738,371 Furniture and equipment 823,520 504,187 502,348 442,692 Vehicles 146,346 117,396 146,346 98,188 Construction in progress - - 1,514,842 -

7,045,836$ 1,504,702$ 4,201,557$ 1,279,251$

Net property andequipment 5,541,134$ 2,922,306$

20162017

12

Northwest Iowa Mental Health Center Notes to Financial Statements

June 30, 2017 and 2016

Note 3 - Promises to Give Unconditional promises to give are estimated to be collected as follows as of June 30, 2017 and 2016:

2017 2016

Within one year 118,516$ 96,791$ Within one to five years 194,250 169,100

312,766 265,891 Adjustment to fair value (76,414) (58,899)

Promises to give, net 236,352$ 206,992$

Note 4 - Fair Value Measurements The Center reports certain assets at fair value in the financial statements. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal, or most advantageous, market at the measurement date under current market conditions regardless of whether that price is directly observable or estimated using another valuation technique. Inputs used to determine fair value refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability based on the best information available. A three-tier hierarchy categorizes the inputs as follows: Level 1 – Quoted prices (unadjusted) in active markets for identical assets or liabilities that can be accessed at the measurement date. Level 2 – Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly. These include quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability, and market-corroborated inputs. Level 3 – Unobservable inputs for the asset or liability. In these situations, inputs are developed using the best information available in the circumstances. In some cases, the inputs used to measure the fair value of an asset or a liability might be categorized within different levels of the fair value hierarchy. In those cases, the fair value measurement is categorized in its entirety in the same level of the fair value hierarchy as the lowest level input that is significant to the entire measurement. Assessing the significance of a particular input to entire measurement requires judgment, taking into account factors specific to the asset or liability. The categorization of an asset within the hierarchy is based upon the pricing transparency of the asset and does not necessarily correspond to an assessment of the quality, risk or liquidity profile of the asset or liability.

13

Northwest Iowa Mental Health Center Notes to Financial Statements

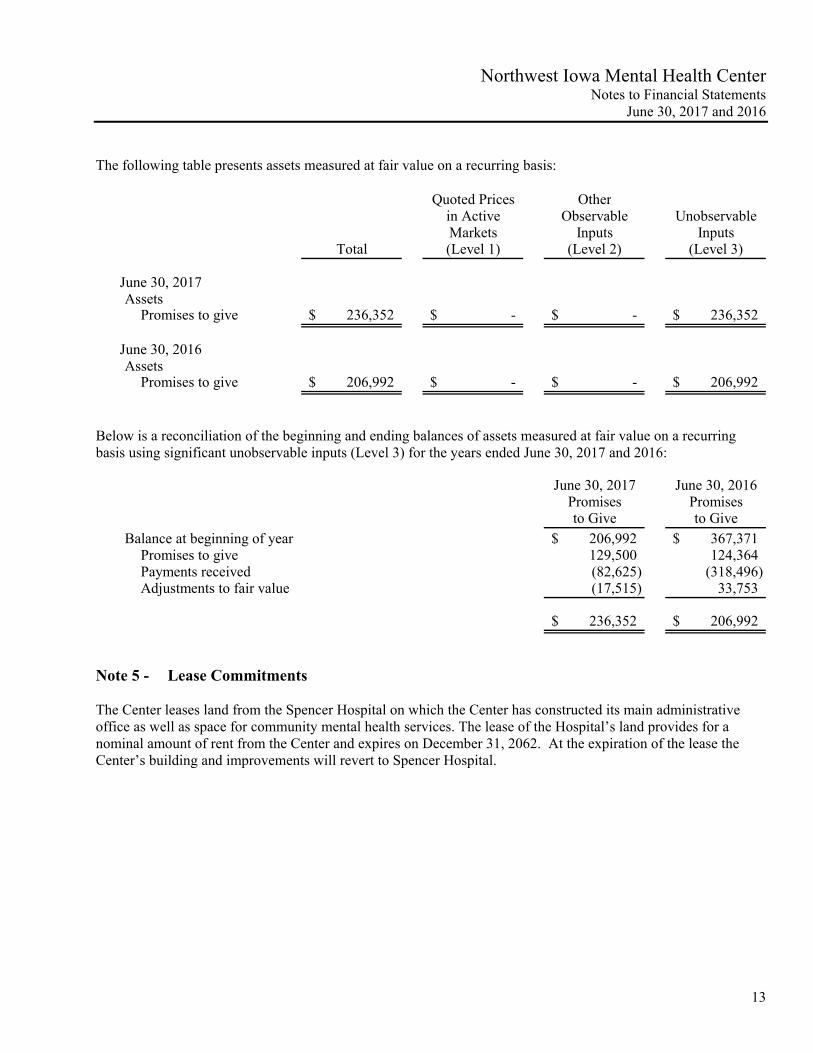

June 30, 2017 and 2016 The following table presents assets measured at fair value on a recurring basis:

Quoted Prices Otherin Active Observable UnobservableMarkets Inputs Inputs

Total (Level 1) (Level 2) (Level 3)

June 30, 2017Assets

Promises to give 236,352$ -$ -$ 236,352$

June 30, 2016Assets

Promises to give 206,992$ -$ -$ 206,992$

Below is a reconciliation of the beginning and ending balances of assets measured at fair value on a recurring basis using significant unobservable inputs (Level 3) for the years ended June 30, 2017 and 2016:

June 30, 2017 June 30, 2016Promises Promisesto Give to Give

Balance at beginning of year 206,992$ 367,371$ Promises to give 129,500 124,364 Payments received (82,625) (318,496) Adjustments to fair value (17,515) 33,753

236,352$ 206,992$

Note 5 - Lease Commitments The Center leases land from the Spencer Hospital on which the Center has constructed its main administrative office as well as space for community mental health services. The lease of the Hospital’s land provides for a nominal amount of rent from the Center and expires on December 31, 2062. At the expiration of the lease the Center’s building and improvements will revert to Spencer Hospital.

14

Northwest Iowa Mental Health Center Notes to Financial Statements

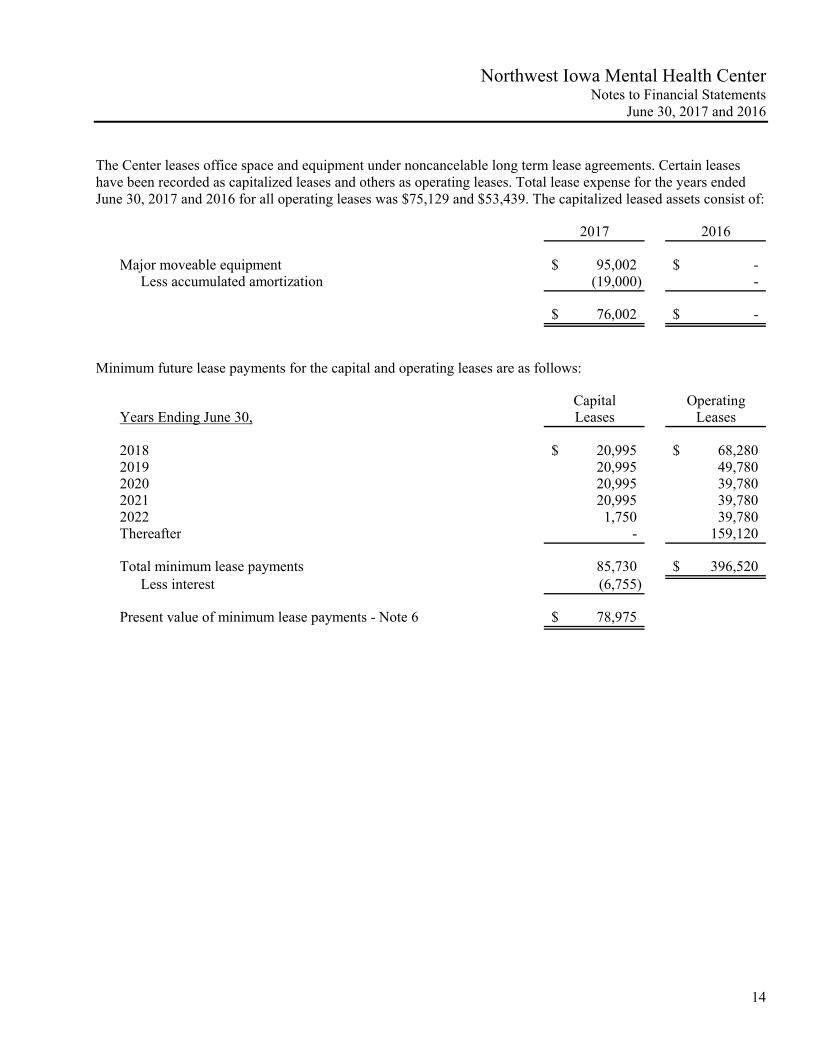

June 30, 2017 and 2016 The Center leases office space and equipment under noncancelable long term lease agreements. Certain leases have been recorded as capitalized leases and others as operating leases. Total lease expense for the years ended June 30, 2017 and 2016 for all operating leases was $75,129 and $53,439. The capitalized leased assets consist of:

2017 2016

Major moveable equipment 95,002$ -$ Less accumulated amortization (19,000) -

76,002$ -$

Minimum future lease payments for the capital and operating leases are as follows:

Capital OperatingYears Ending June 30, Leases Leases

20,995$ 68,280$ 20,995 49,780 20,995 39,780 20,995 39,780

1,750 39,780 Thereafter - 159,120

Total minimum lease payments 85,730 396,520$ Less interest (6,755)

Present value of minimum lease payments - Note 6 78,975$

20182019202020212022

15

Northwest Iowa Mental Health Center Notes to Financial Statements

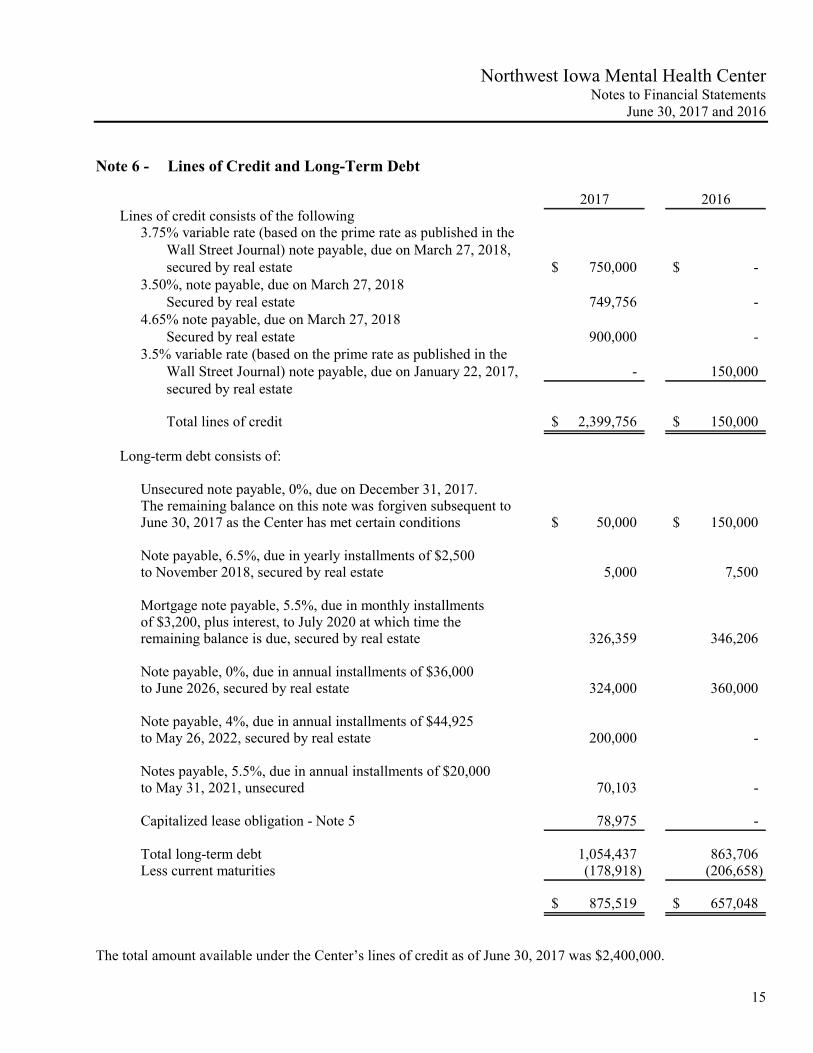

June 30, 2017 and 2016 Note 6 - Lines of Credit and Long-Term Debt

2017 2016Lines of credit consists of the following

3.75% variable rate (based on the prime rate as published in theWall Street Journal) note payable, due on March 27, 2018, secured by real estate 750,000$ -$

3.50%, note payable, due on March 27, 2018Secured by real estate 749,756 -

4.65% note payable, due on March 27, 2018Secured by real estate 900,000 -

3.5% variable rate (based on the prime rate as published in theWall Street Journal) note payable, due on January 22, 2017, - 150,000 secured by real estate

Total lines of credit 2,399,756$ 150,000$

Long-term debt consists of:

Unsecured note payable, 0%, due on December 31, 2017. The remaining balance on this note was forgiven subsequent to June 30, 2017 as the Center has met certain conditions 50,000$ 150,000$

Note payable, 6.5%, due in yearly installments of $2,500to November 2018, secured by real estate 5,000 7,500

Mortgage note payable, 5.5%, due in monthly installmentsof $3,200, plus interest, to July 2020 at which time theremaining balance is due, secured by real estate 326,359 346,206

Note payable, 0%, due in annual installments of $36,000to June 2026, secured by real estate 324,000 360,000

Note payable, 4%, due in annual installments of $44,925 to May 26, 2022, secured by real estate 200,000 -

Notes payable, 5.5%, due in annual installments of $20,000 to May 31, 2021, unsecured 70,103 -

Capitalized lease obligation - Note 5 78,975 -

Total long-term debt 1,054,437 863,706 Less current maturities (178,918) (206,658)

875,519$ 657,048$

The total amount available under the Center’s lines of credit as of June 30, 2017 was $2,400,000.

16

Northwest Iowa Mental Health Center Notes to Financial Statements

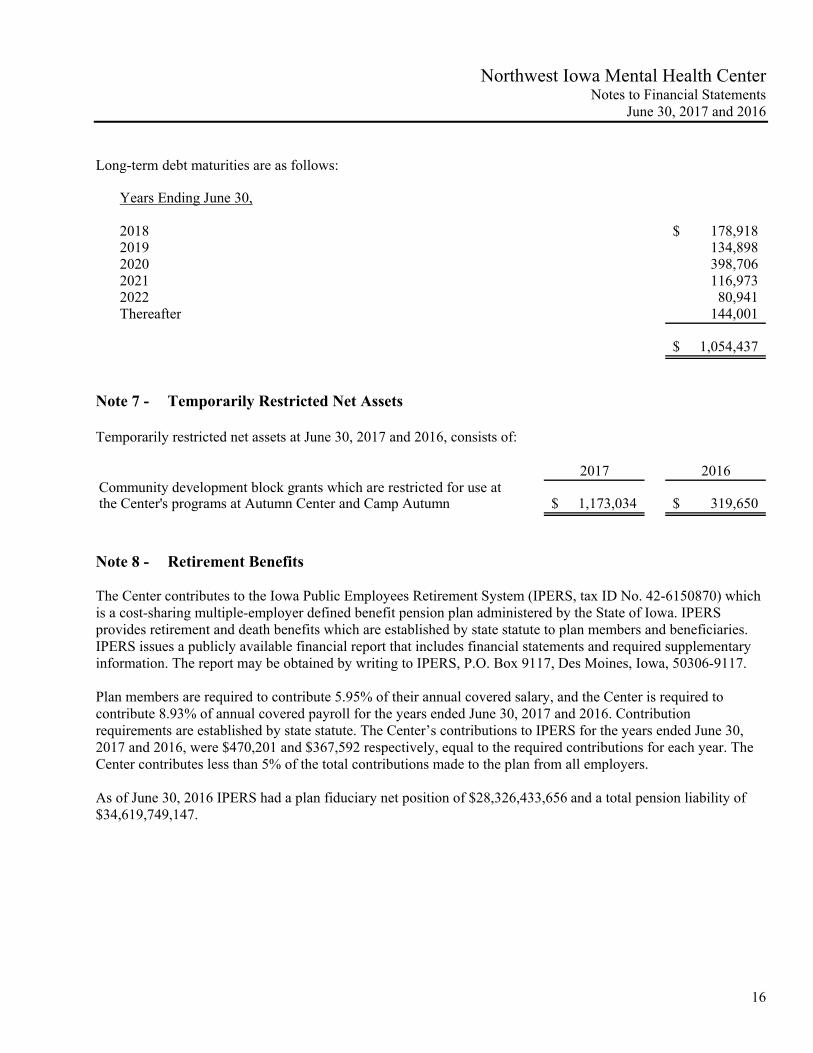

June 30, 2017 and 2016 Long-term debt maturities are as follows:

Years Ending June 30,

178,918$ 134,898 398,706 116,973

80,941 Thereafter 144,001

1,054,437$

20182019202020212022

Note 7 - Temporarily Restricted Net Assets Temporarily restricted net assets at June 30, 2017 and 2016, consists of:

2017 2016Community development block grants which are restricted for use atthe Center's programs at Autumn Center and Camp Autumn 1,173,034$ 319,650$

Note 8 - Retirement Benefits The Center contributes to the Iowa Public Employees Retirement System (IPERS, tax ID No. 42-6150870) which is a cost-sharing multiple-employer defined benefit pension plan administered by the State of Iowa. IPERS provides retirement and death benefits which are established by state statute to plan members and beneficiaries. IPERS issues a publicly available financial report that includes financial statements and required supplementary information. The report may be obtained by writing to IPERS, P.O. Box 9117, Des Moines, Iowa, 50306-9117. Plan members are required to contribute 5.95% of their annual covered salary, and the Center is required to contribute 8.93% of annual covered payroll for the years ended June 30, 2017 and 2016. Contribution requirements are established by state statute. The Center’s contributions to IPERS for the years ended June 30, 2017 and 2016, were $470,201 and $367,592 respectively, equal to the required contributions for each year. The Center contributes less than 5% of the total contributions made to the plan from all employers. As of June 30, 2016 IPERS had a plan fiduciary net position of $28,326,433,656 and a total pension liability of $34,619,749,147.

17

Northwest Iowa Mental Health Center Notes to Financial Statements

June 30, 2017 and 2016 Note 9 - Concentration of Credit Risk The Center provides counseling to individuals in a nine-county area. The Center grants credit without collateral to its patients, most of whom are insured under third-party payor agreements. The mix of receivables from third-party payors and patients at June 30, 2017 and 2016, was as follows:

2017 2016

Medicaid 46% 58%Commercial insurance 18% 12%Private pay 18% 12%Blue Cross 13% 10%Medicare 5% 8%

100% 100%

The Center's cash balances are maintained in various bank accounts. At various times during the year the balances in these bank accounts were over the FDIC insurance limits. Note 10 - Economic Dependency The Center received $886,924 and $693,296 or 11% and 9% of the Center’s total revenues, from state and local governments during the years ended June 30, 2017 and 2016, respectively, for mental health services. In addition another $140,207 and $201,340 or 2% and 3% of total revenues was received from local governments for management fees, related to those residents. The Center also received a substantial amount of its revenue from third-party payors, such as Medicare, Medicaid and Blue Cross. A significant reduction in reimbursement from any of these parties could have a material impact on the Center’s programs and services. Note 11 - Restatement The financial statements for the year ended June 30, 2016 have been restated to properly reflect a receivable and restricted revenue of $248,982 for grant funds which were received during the fiscal year ended June 30, 2017 but earned during the year ended June 30, 2016 and to reduce a receivable and grant revenue for an over accrual of $39,585.

18

Northwest Iowa Mental Health Center Notes to Financial Statements

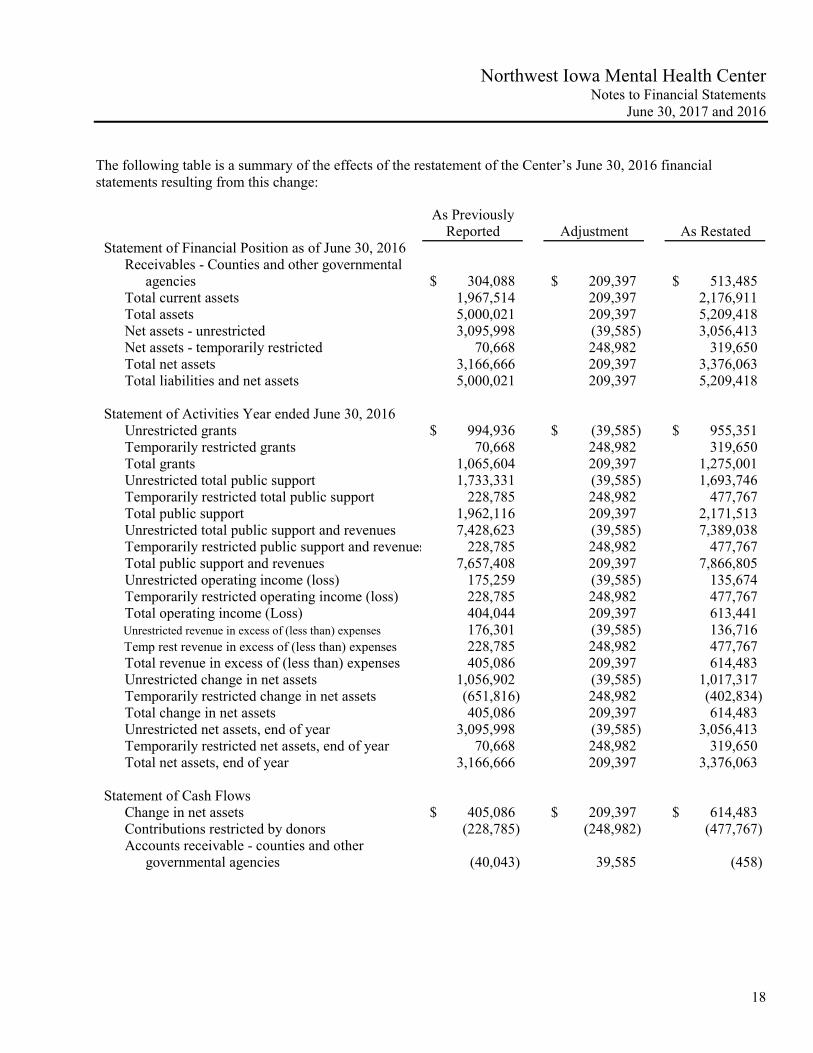

June 30, 2017 and 2016 The following table is a summary of the effects of the restatement of the Center’s June 30, 2016 financial statements resulting from this change:

As PreviouslyReported Adjustment As Restated

Statement of Financial Position as of June 30, 2016Receivables - Counties and other governmental

agencies 304,088$ 209,397$ 513,485$ Total current assets 1,967,514 209,397 2,176,911 Total assets 5,000,021 209,397 5,209,418 Net assets - unrestricted 3,095,998 (39,585) 3,056,413 Net assets - temporarily restricted 70,668 248,982 319,650 Total net assets 3,166,666 209,397 3,376,063 Total liabilities and net assets 5,000,021 209,397 5,209,418

Statement of Activities Year ended June 30, 2016Unrestricted grants 994,936$ (39,585)$ 955,351$ Temporarily restricted grants 70,668 248,982 319,650 Total grants 1,065,604 209,397 1,275,001 Unrestricted total public support 1,733,331 (39,585) 1,693,746 Temporarily restricted total public support 228,785 248,982 477,767 Total public support 1,962,116 209,397 2,171,513 Unrestricted total public support and revenues 7,428,623 (39,585) 7,389,038 Temporarily restricted public support and revenues 228,785 248,982 477,767 Total public support and revenues 7,657,408 209,397 7,866,805 Unrestricted operating income (loss) 175,259 (39,585) 135,674 Temporarily restricted operating income (loss) 228,785 248,982 477,767 Total operating income (Loss) 404,044 209,397 613,441 Unrestricted revenue in excess of (less than) expenses 176,301 (39,585) 136,716 Temp rest revenue in excess of (less than) expenses 228,785 248,982 477,767 Total revenue in excess of (less than) expenses 405,086 209,397 614,483 Unrestricted change in net assets 1,056,902 (39,585) 1,017,317 Temporarily restricted change in net assets (651,816) 248,982 (402,834) Total change in net assets 405,086 209,397 614,483 Unrestricted net assets, end of year 3,095,998 (39,585) 3,056,413 Temporarily restricted net assets, end of year 70,668 248,982 319,650 Total net assets, end of year 3,166,666 209,397 3,376,063

Statement of Cash FlowsChange in net assets 405,086$ 209,397$ 614,483$ Contributions restricted by donors (228,785) (248,982) (477,767) Accounts receivable - counties and other

governmental agencies (40,043) 39,585 (458)

19

Northwest Iowa Mental Health Center Notes to Financial Statements

June 30, 2017 and 2016 Note 12 - Management plans The Center has experienced an increase in expenses during the year ended June 30, 2017 that exceed the increase in unrestricted revenue, and its cash position decreased during the year then ended. The Center’s other assets increased during the year ended June 30, 2017 primarily due to grant funds earned in the year ended June 30, 2017 that were not received until July 2017. In addition the Center’s current assets were less than its current liabilities due to short term borrowings which were used to fund property and equipment acquisitions. These conditions indicated that there is substantial doubt about the Center’s ability to continue as a going concern within one year after the date the financial statements are issued. Management has reviewed its operations with the goal of increasing revenues and decreasing expenses in order to generate positive cash flows and revenues which would be greater than its expenses. Some of the items management has implemented to improve its financial condition include establishing a new compensation plan for outpatient therapists and substance use disorder counselors which provide incentives for meeting expectations; developing more flexible scheduling opportunities for individuals so that it is easier to access services offered by the Center; and eliminating staff positions and changing benefit programs. Management is also in the process of decreasing programs and services which have historically generated negative cash flows. Management believes the steps it is taking will improve its ability to meet its obligations and produce positive cash flows.