17

Note on FSD and SSD Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY March, 2015 1 / 17

Note on FSD and SSD

Shuoxun Hellen Zhang

WISE & SOE

XIAMEN UNIVERSITY

March, 2015

1 / 17

First-order stochastic dominance

Definition

First-order stochastic dominance(FSD)Let Fx(W ) and Gy (W ) be two cumulative probabilitydistributions for random payoffs in [a, b]. We say thatx FSD y if and only if for all W :

Fx(W ) ≤ Gy (W )

and for some Wi

Fx(W ) < Gy (W )

In other words, the pdf defined on wealth for asset y alwayslies to the left of the pdf of x , then x FSD y .

2 / 17

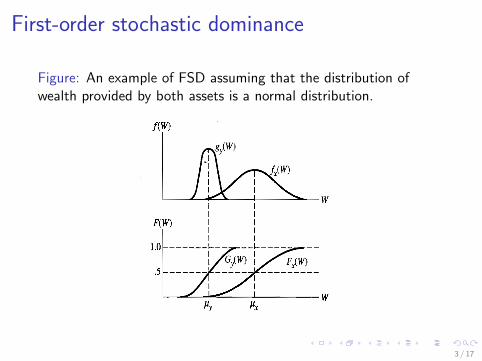

First-order stochastic dominance

Figure: An example of FSD assuming that the distribution ofwealth provided by both assets is a normal distribution.

3 / 17

Risk-AversionFirst-order stochastic dominance applies to all nondecreasingutility functions.

Figure: Three utility functions with positive marginal utility: (a)risk lover; (b) risk neutral; (c) risk averter

4 / 17

Risk-Aversion

I If U[E (W )] < E [U(W )] or the utility function is strictlyconvex, then the individual is a risk lover;

I If U[E (W )] = E [U(W )] or the utility function is linear,then the individual is risk neutral;

I If U[E (W )] > E [U(W )] or the utility function is strictlyconcave, then the individual is risk averse;

5 / 17

First-order stochastic dominance

Theorem

Let Fx(W ) and Gy (W ) be two cumulative probabilitydistributions for random payoffs in [a, b]. x FSD y if and onlyif

E [u(x)] ≥ E [u(y)]

for any nondecreasing Bernoulli utility function u.

6 / 17

First-order stochastic dominance

Figure: First-order stochastic dominance and expected utility.

7 / 17

First-order stochastic dominance

For a given frequency of wealth, fi(W ), the increasing utilityfunction assigns higher utility to the level of wealth offered byasset x than by asset y . This is true for every frequency.The expected utility is defined by,

E [u(W )] =

∫ ∞−∞

u(W )f (W )dW

8 / 17

Second-order stochastic dominance

Definition

second-order stochastic dominance(SSD)Let Fx(W ) and Gy (W ) be two cumulative probabilitydistributions for random payoffs in [a, b]. We say thatx SSD y if and only if for any W :∫W

−∞[Gy (W )− Fx(W )]dW ≥ 0

Gy (Wi) 6= Fx(Wi) for some Wi

9 / 17

Second-order stochastic dominance

second-order stochastic dominance not only assumes utilityfunctions where marginal utility of wealth is positive, but alsoassumes that total utility must increase at a decreasing rate.Inother words, utility functions are nondecreasing and strictlyconcave. Thus individuals are assumed to be risk averse.

10 / 17

Second-order stochastic dominance

Figure: An example of SSD

11 / 17

Second-order stochastic dominance

Asset x will dominate asset y if an investor is riskaversebecause they both offer the same expected level of wealthµx = µy because y is riskier.

This means that in order for asset x to dominate asset y forall risk-averse investors, the accumulated area under cdf of ymust be greater than the accumulated area for x , below anygiven level of wealth.

This implies that, unlike FSD, the cdf can cross.

12 / 17

Second-order stochastic dominance

SSD requires that the difference in areas under the cdf bepositive below any level of wealth Wi .

Figure: Graphic representation of the sum of the differences incumulative probabilities

13 / 17

Second-order stochastic dominance

Theorem

Let Fx(W ) and Gy (W ) be two cumulative probabilitydistributions for random payoffs in [a, b]. x SSD y if and onlyif,

E [u(x)] ≥ E [u(y)]

for any nondecreasing and concave Bernoulli utilityfunction u

14 / 17

Second-order stochastic dominance

15 / 17

Second-order stochastic dominance

The concave utility function of a risk averter has the propertyof decreasing marginal utility.

If we select a given frequency of wealth it maps out equalchanges in wealth 4W1 and 4W2. The difference in utilitybetween x and y below the mean is much greater than thedifference in utility for the same change in wealth above themean. Thus, if we take the expected utility by pairing all suchdifferences with equal probabilities, the expected utility of x isseen as greater than the expected utility of y .

If the individual were risk neutral, with a linear utility function,the differences in utility above and below the mean wouldalways be equal. Hence a risk-neutral investor would beindifferent between x and y .

16 / 17

Stochastic dominance

Stochastic dominance is founded on the basis of expectedutility maximization and it applies to any probabilitydistribution. This is because it takes into account every pointin the probability distribution.

We can be sure that if an asset demonstrates SSD, it will bepreferred by all risk-averse investors, regardless of the specificshape of their utility functions.

We can use stochastic dominance as the basis of the completetheory of how risk-averse investors choose among various riskyassets. All we need to do is to find the set of portfolios that isstochastically dominance.

17 / 17