Notice of Claims in Claims-Made Insurance Policies Identifying Claims; Evaluating Whether and When to Report Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. WEDNESDAY, FEBRUARY 22, 2012 Presenting a live 90-minute webinar with interactive Q&A Eric G. Barber, Atty, Perkins Coie, Madison, Wis. Mark D. Villanueva, Atty., McCarter & English, Philadelphia Nancy R. Kornegay, Partner, Brown & Kornegay, Houston

Transcript

Notice of Claims in Claims-Made Insurance Policies Identifying Claims; Evaluating Whether and When to Report

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, FEBRUARY 22, 2012

Presenting a live 90-minute webinar with interactive Q&A

Eric G. Barber, Atty, Perkins Coie, Madison, Wis.

Mark D. Villanueva, Atty., McCarter & English, Philadelphia

Nancy R. Kornegay, Partner, Brown & Kornegay, Houston

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the word balloon button to send

FOR LIVE EVENT ONLY

Tips for Optimal Quality

Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-370-2805 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

Usually quite broad; Often includes: Civil or criminal proceedings; Written demands; Administrative or regulatory proceedings;

May include investigations of insureds As distinguished from a “Circumstance”

Definition of "Claim"

6

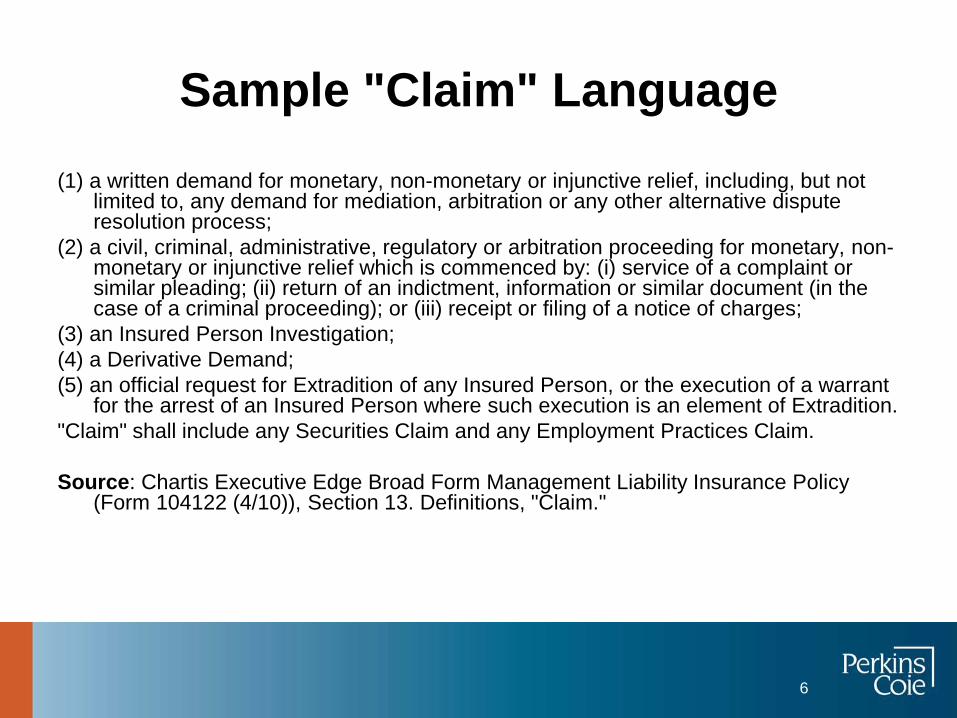

Sample "Claim" Language (1) a written demand for monetary, non-monetary or injunctive relief, including, but not

limited to, any demand for mediation, arbitration or any other alternative dispute resolution process;

(2) a civil, criminal, administrative, regulatory or arbitration proceeding for monetary, non-monetary or injunctive relief which is commenced by: (i) service of a complaint or similar pleading; (ii) return of an indictment, information or similar document (in the case of a criminal proceeding); or (iii) receipt or filing of a notice of charges;

(3) an Insured Person Investigation; (4) a Derivative Demand; (5) an official request for Extradition of any Insured Person, or the execution of a warrant

for the arrest of an Insured Person where such execution is an element of Extradition. "Claim" shall include any Securities Claim and any Employment Practices Claim. Source: Chartis Executive Edge Broad Form Management Liability Insurance Policy

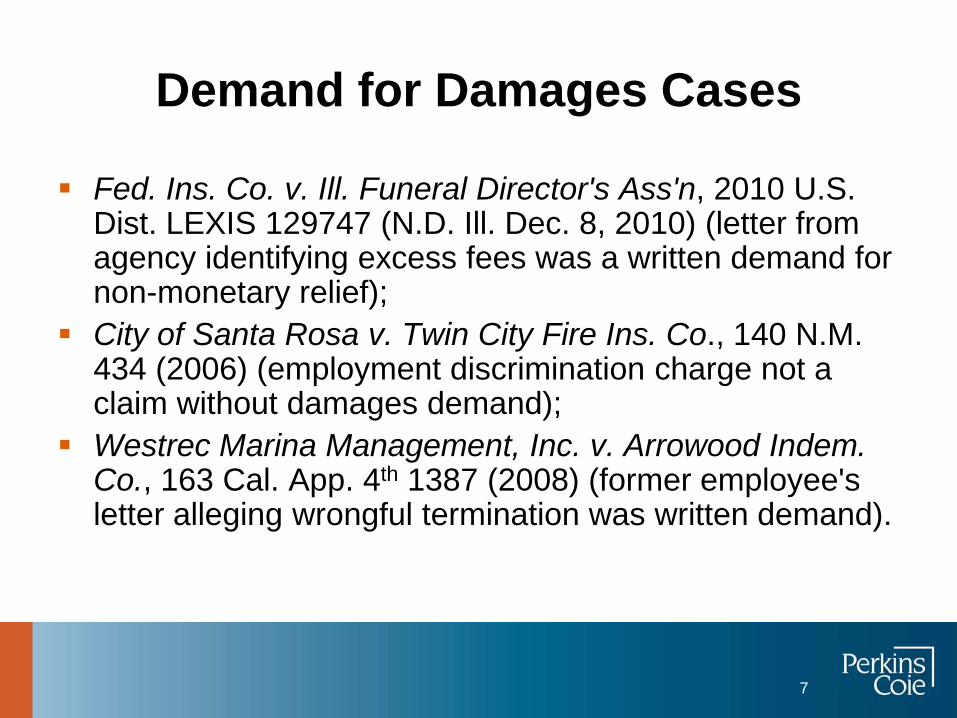

Fed. Ins. Co. v. Ill. Funeral Director's Ass'n, 2010 U.S. Dist. LEXIS 129747 (N.D. Ill. Dec. 8, 2010) (letter from agency identifying excess fees was a written demand for non-monetary relief);

City of Santa Rosa v. Twin City Fire Ins. Co., 140 N.M. 434 (2006) (employment discrimination charge not a claim without damages demand);

Westrec Marina Management, Inc. v. Arrowood Indem. Co., 163 Cal. App. 4th 1387 (2008) (former employee's letter alleging wrongful termination was written demand).

8

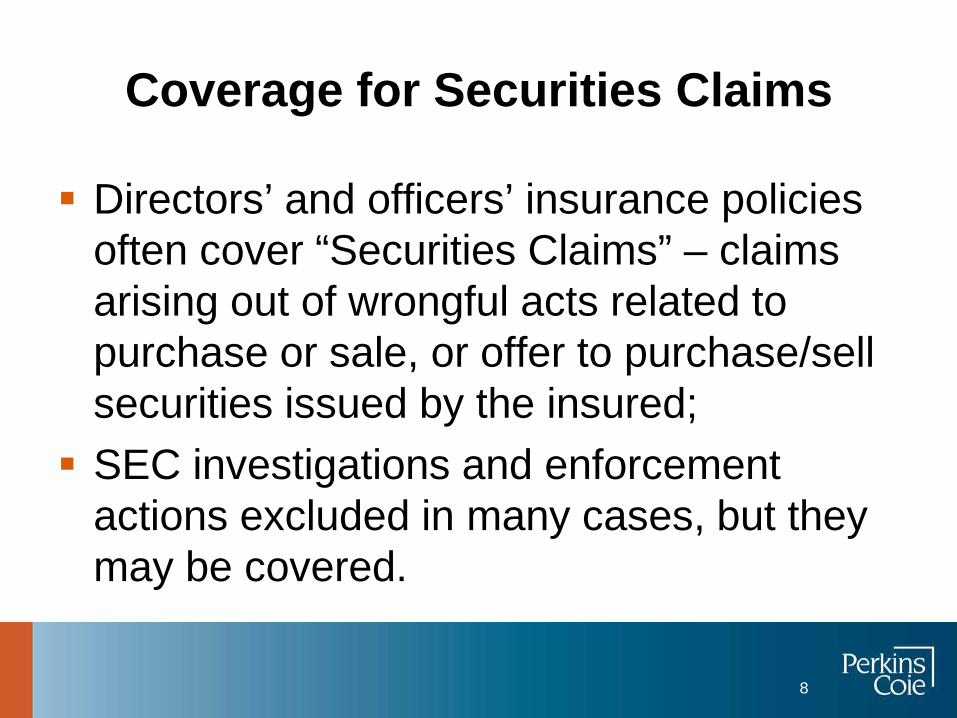

Coverage for Securities Claims

Directors’ and officers’ insurance policies often cover “Securities Claims” – claims arising out of wrongful acts related to purchase or sale, or offer to purchase/sell securities issued by the insured; SEC investigations and enforcement

actions excluded in many cases, but they may be covered.

9

Securities Claims Cases

Nat'l Stock Exch. V. Fed. Ins. Co., 2007 U.S. Dist. LEXIS 23876 (N.D. Ill. Mar. 30, 2007) (SEC investigation not a claim before formal order issued);

Minuteman Int'l, Inc. v. Great Am. Ins. Co., 2004 U.S. Dist. LEXIS 4660 (N.D. Ill. Mar. 18, 2004) (SEC investigation was a claim where policy required demand for non-monetary relief);

Highwoods Props. v. Exec. Risk. Indem., Inc., 407 F.3d 917 (8th Cir. 2005) (breach of fiduciary duty involving stock was a claim).

10

Are Subpoenas Claims?

No definite answer – recent cases go both ways and often turn on the policy’s specific language; Courts look at link between subpoenas

and related government investigations;

11

Recent Cases Involving Subpoenas as Claims

Ace Am. Ins. Co. v. Ascend One Corp., 570 F. Supp. 2d

789 (D. Md. 2008) (subpoena and investigative demands were claims);

Jemmco Partners v. Exec. Risk. Indem., Inc., No. L-486-07 (N.J. Super. Ct., filed Mar. 22, 2007) (subpoena seeking documents was a claim).

But see, Diamond Glass Cos. v. Twin City Fire Ins. Co., 2008 WL 4613170 (S.D.N.Y. Aug. 18, 2008) (grand jury subpoena for documents/testimony was not a claim);

12

Related/Interrelated Claims

Losses stemming from same/related acts generally considered a single claim; Policy language consolidates multiple

claims that have a "common nexus," or are "causally or logically connected"; Very contentious issue without a clear

resolution across courts.

13

Related/Interrelated Claims Cases

Quanta Lines Ins. Co. v. Investors Capital Corp., 2009 U.S. Dist. LEXIS 117689 (S.D.N.Y. Dec. 17, 2009) (claims must have sufficient factual nexus to be interrelated);

Axis Surplus Ins. Co. v. Johnson, 2008 U.S. Dist. LEXIS 77614 (N.D. Okla. Oct. 3, 2008) (factual analysis, not just legal theory, is essential to determine relatedness);

G-I Holdings v. Hartford Fire Ins. Co., 2007 U.S. Dist. LEXIS 19069 (D.N.J. Mar. 16, 2007) (construing "interrelated wrongful acts" as unambiguous).

Late Notice of Claims in Claims-Made Insurance Policies

What are Claims-Made Policies?

Professional liability policies such as Directors and Officers, Errors and Omissions, and Employment Practices Liability policies are typically written on a claims-made basis

Provide coverage for claims asserted against the insured during the policy period

15

Benefits to the Insurer of Claims-Made Policies

Limited tail exposure

Predictability of potential obligations at close of policy period

Smaller gap of time between when insurer prices policy and the time when the insurer may incur an obligation to pay

Notice Provision in Pure Claims Made Policies

Typically requires notice “as soon as practicable”

17

Notice Provision in Claims-Made and Reported Policies

Insurers place the reportingrequirement in the Insuring Agreement, Conditions, or both

Failure to trigger the Insuring Agreement bars all coverage, while breach of a reporting Condition may not bar all coverage for late notice

18

)

Notice Provision in Claims-Made and Reported Policies (cont.)

Insuring Agreement: “…affords coverage for claims first made against you and reported to us in writing during the period this Policy is in effect or within ninety (90) days following its termination.”

19

Notice Provision in Claims-Made and Reported Policies (cont.)

Conditions: “It is a condition precedent to this insurance that you … [provide notice] of any claim as soon as practicable during the Policy Period . . . but in no event later than ninety (90) days after the expiration of the Policy Period.”

20

Notice Provision in Claims-Made and Reported Policies (cont.)

Some policies may also include the following language in the definition of “Claim”: “A claim shall be considered ‘made’: (1) when it is

first reported to the Company”

21

The Notice Prejudice Rule

Many jurisdictions have considered the “notice prejudice rule” in the context of occurrence based policies.

Notice provision in occurrence based CGL policy may provide: “In the event of an occurrence, written notice containing

particulars sufficient to identify the insured and all reasonably obtainable information with respect to the time, place and circumstances thereof, and the names and addresses of the injured and of available witnesses, shall be given by or for the insured to the company or any of its authorized agents as soon as practicable.”

22

The Notice Prejudice Rule (cont.)

“As soon as practicable” has been construed to mean “within a reasonable time” and is a fact specific inquiry.

See, e.g., Bass v. Allstate Ins. Co., 77 N.J. Super. 491, 495

(App. Div. 1962); Country Mutual Insurance Company v. Livorsi Marine, Inc., 856 N.E.2d 338, 343 (Ill. 2006); Mount Vernon Fire Ins. Co. v. King Gen. Constr., 1998 U.S. App. LEXIS 20574 (2d Cir. 1998).

23

The Notice Prejudice Rule (cont.)

Some jurisdictions place burden on policyholder to prove that late notice did not prejudice the carrier

See, e.g., Grinnell Mut. Reinsurance Co. v. Jungling, 654

N.W.2d 530, 541-42 (Iowa 2002); Ferrando v. Auto-Owners Mut. Ins. Co., 781 N.E.2d 927 (Ohio 2002)

24

The Notice Prejudice Rule (cont.)

Other jurisdictions impose the burden of proving appreciable prejudice on the carrier

See, e.g., Cooper v. Government Employees Ins. Co., 51 N.J.

86, 94-95 (1968); Resolution Trust Corp. v. Moskowitz, 868 F. Supp. 634, 638 (D.N.J. 1994)

25

The Notice Prejudice Rule (cont.)

At least 8 states have passed legislation concerning the notice prejudice rule

Michigan Ins. Code § 500.3008, Missouri Reg. § 100-1.020, New York Ins. Code § 3420, Texas Board of Ins. Order No. 23080, Utah Ins. Code § 31A-21-312, Wisconsin Ins. Code § 631.81

26

The Notice Prejudice Rule (cont.)

Most courts have declined to apply the notice prejudice rule to claims-made and claims-made and reported policies.

See, e.g., Zuckerman v. National Union Fire Insurance

Company, 100 N.J. 304 (1985); Central Illinois Light Co. v. Home Insurance Co., 821 N.E.2d. 206 (Ill. 2004); Gulf v. Dolan, Fertig & Curtis, 433 So. 2d 512, 515-15 (Fla. 1983)

For example, a lawsuit filed against an insured during

the policy period, but served after the policy period was not covered in Slater v. Lawyers’ Mutual Ins. Co., 278 Cal. Rptr. 479 (Cal. Ct. App. 1991).

27

The Notice Prejudice Rule (cont.)

Some courts have applied the notice prejudice rule to claims-made and claims-made and reported policies.

See, e.g., Sherwood Brands, Inc. v. Great American Ins. Co.,

418 Md. 300 (2011); Financial Industries Corp. v. XL Specialty Ins. Co., 285 S.W.3d877 (Tex. Sup. Ct. 2009); Prodigy Communications Corp. v. Agricultural Excess & Surplus Ins. Co., 288 S.W.3d 374 (Tex. Sup. Ct. 2009); Sherlock v. Perry, 605 F. Supp. 1001 (E.D. Mich. 1985)

28

29

Notice: to Give or Not to Give. That is the Question!

Nancy R. Kornegay Brown & Kornegay, LLP Houston, Texas 713.528.3705 [email protected]

Brown & Kornegay LLP

30 30 Brown & Kornegay LLP

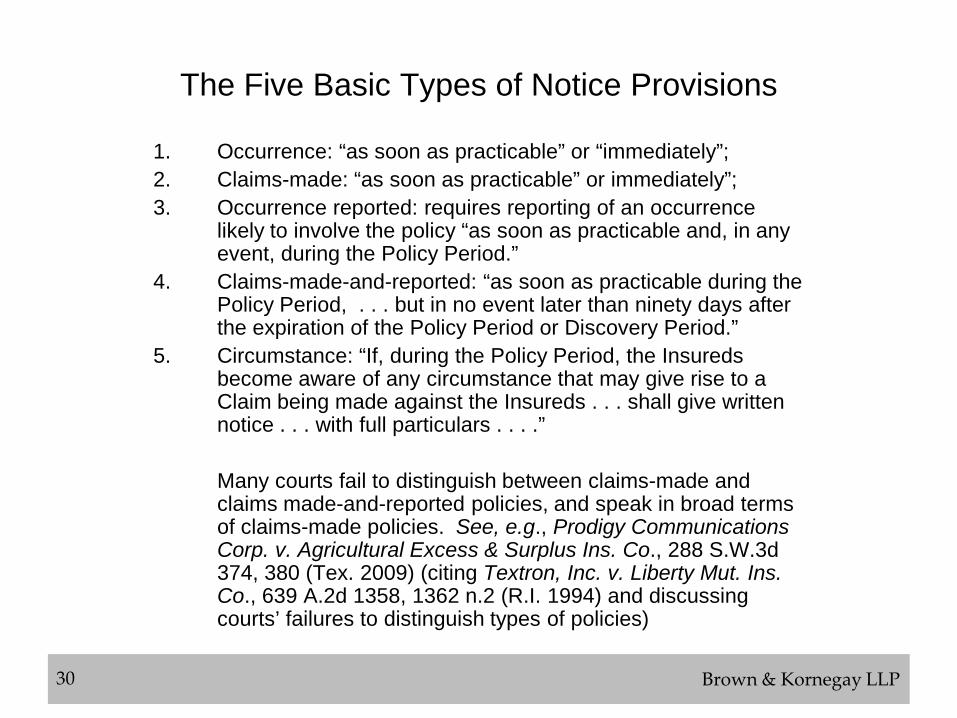

The Five Basic Types of Notice Provisions

1. Occurrence: “as soon as practicable” or “immediately”; 2. Claims-made: “as soon as practicable” or immediately”; 3. Occurrence reported: requires reporting of an occurrence

likely to involve the policy “as soon as practicable and, in any event, during the Policy Period.”

4. Claims-made-and-reported: “as soon as practicable during the Policy Period, . . . but in no event later than ninety days after the expiration of the Policy Period or Discovery Period.”

5. Circumstance: “If, during the Policy Period, the Insureds become aware of any circumstance that may give rise to a Claim being made against the Insureds . . . shall give written notice . . . with full particulars . . . .”

Many courts fail to distinguish between claims-made and

claims made-and-reported policies, and speak in broad terms of claims-made policies. See, e.g., Prodigy Communications Corp. v. Agricultural Excess & Surplus Ins. Co., 288 S.W.3d 374, 380 (Tex. 2009) (citing Textron, Inc. v. Liberty Mut. Ins. Co., 639 A.2d 1358, 1362 n.2 (R.I. 1994) and discussing courts’ failures to distinguish types of policies)

30

31 31 Brown & Kornegay LLP

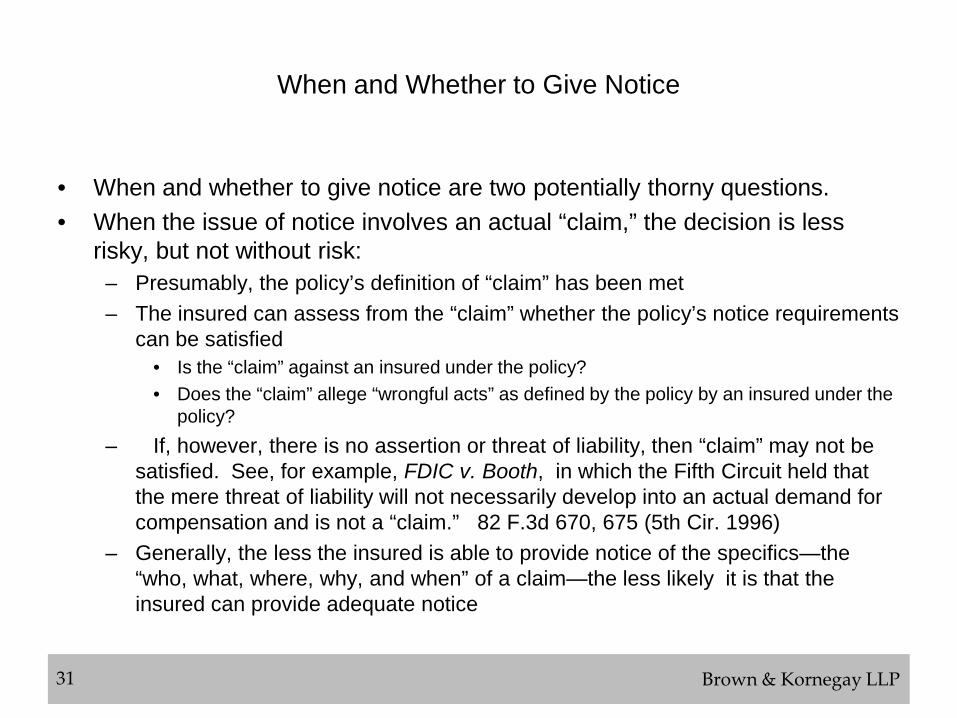

When and Whether to Give Notice

• When and whether to give notice are two potentially thorny questions. • When the issue of notice involves an actual “claim,” the decision is less

risky, but not without risk: – Presumably, the policy’s definition of “claim” has been met – The insured can assess from the “claim” whether the policy’s notice requirements

can be satisfied • Is the “claim” against an insured under the policy? • Does the “claim” allege “wrongful acts” as defined by the policy by an insured under the

policy? – If, however, there is no assertion or threat of liability, then “claim” may not be

satisfied. See, for example, FDIC v. Booth, in which the Fifth Circuit held that the mere threat of liability will not necessarily develop into an actual demand for compensation and is not a “claim.” 82 F.3d 670, 675 (5th Cir. 1996)

– Generally, the less the insured is able to provide notice of the specifics—the “who, what, where, why, and when” of a claim—the less likely it is that the insured can provide adequate notice

31

32 32

Examples of Non-Claims: No Wrongful Act

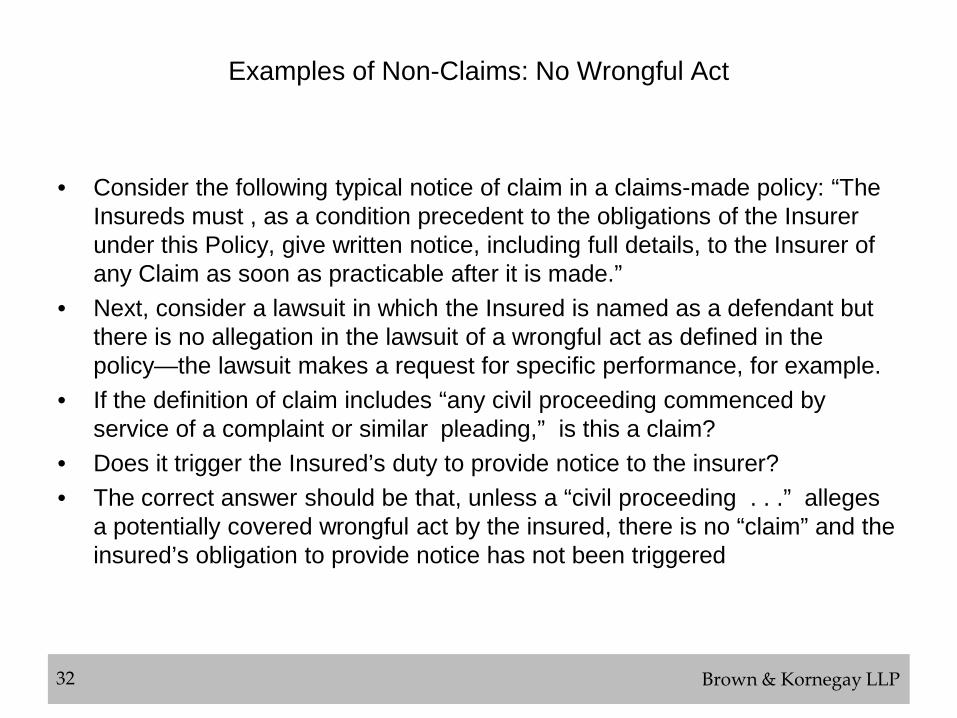

• Consider the following typical notice of claim in a claims-made policy: “The Insureds must , as a condition precedent to the obligations of the Insurer under this Policy, give written notice, including full details, to the Insurer of any Claim as soon as practicable after it is made.”

• Next, consider a lawsuit in which the Insured is named as a defendant but there is no allegation in the lawsuit of a wrongful act as defined in the policy—the lawsuit makes a request for specific performance, for example.

• If the definition of claim includes “any civil proceeding commenced by service of a complaint or similar pleading,” is this a claim?

• Does it trigger the Insured’s duty to provide notice to the insurer? • The correct answer should be that, unless a “civil proceeding . . .” alleges

a potentially covered wrongful act by the insured, there is no “claim” and the insured’s obligation to provide notice has not been triggered

Brown & Kornegay LLP 32

33 33

Only Excluded Acts are Alleged: National Union Fire Ins. v. Willis

• In 1998, Willis, an insured director and officer, was sued for intentional torts • He did not give notice of the lawsuit to his D&O carrier • In 2000, the plaintiffs amended their petition to include a claim of negligent

misrepresentation against Willis • He gave notice of claim under his 2000 D&O policy • The insurer denied invoking its “related claims” provision and arguing the

negligent misrepresentation claim related back to the 1998 suit • The Fifth Circuit upheld the trial court’s ruling in favor of National Union • The court relied upon the 1998 policy’s notice of circumstance provision,

which stated, “If during the policy period, . . . the Insureds shall become aware of any circumstances which may reasonably be expected to give rise to a Claim . . . and shall give written notice . . . with full particulars as to dates, persons, and entities invoked . . . .”

Brown & Kornegay LLP 33

34 34

Notice of Circumstance: a method for attaching coverage to a claim before an actual claim is made

• Different types of circumstance-notice provisions – Some are mandatory: the Insured “shall give notice” – Others are not: the Insured “may give notice” – Obviously, an insured risks losing coverage for a potential claim if a mandatory

“circ notice” provision is ignored. See Willis discussed above. – Some invoke an objective standard for assessing whether known circumstances

may give rise to a claim: “aware of any circumstances which may reasonably give rise to a Claim

– Others invoke a subjective standard: “aware of any circumstances the insured believes may give rise to a Claim

– Still others invoke a hybrid two-part standard: “aware of any circumstances the insured reasonably believes may give rise to a Claim”

• The wording of the “circ notice” provision determines the level of specificity required

• There is no bright-line rule for determining the sufficiency of the notice

Brown & Kornegay LLP 34

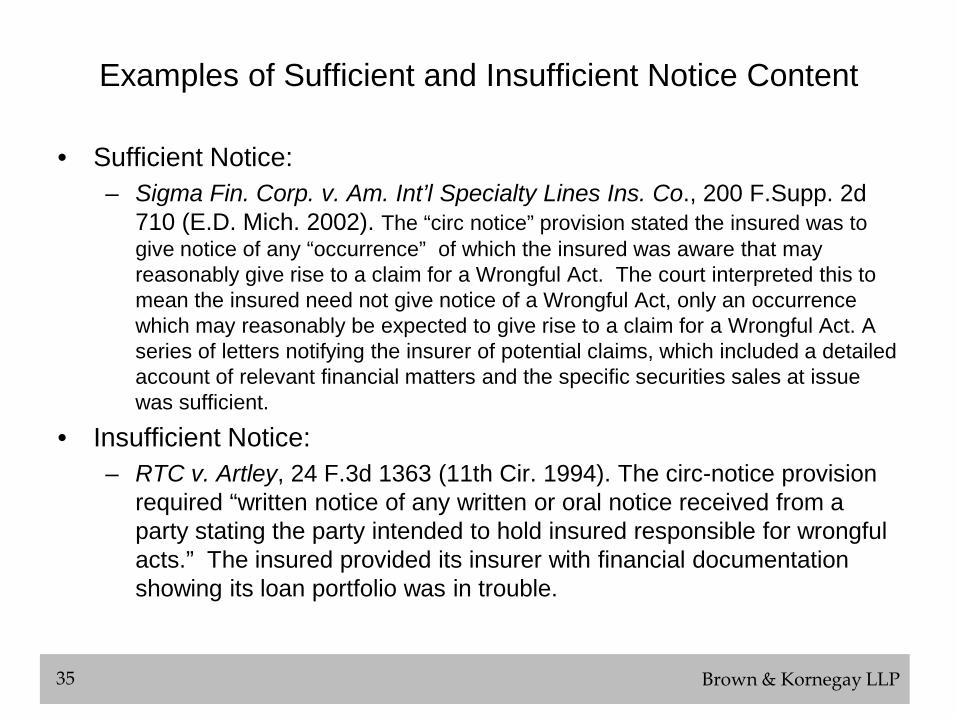

35 35

Examples of Sufficient and Insufficient Notice Content

710 (E.D. Mich. 2002). The “circ notice” provision stated the insured was to give notice of any “occurrence” of which the insured was aware that may reasonably give rise to a claim for a Wrongful Act. The court interpreted this to mean the insured need not give notice of a Wrongful Act, only an occurrence which may reasonably be expected to give rise to a claim for a Wrongful Act. A series of letters notifying the insurer of potential claims, which included a detailed account of relevant financial matters and the specific securities sales at issue was sufficient.

• Insufficient Notice: – RTC v. Artley, 24 F.3d 1363 (11th Cir. 1994). The circ-notice provision

required “written notice of any written or oral notice received from a party stating the party intended to hold insured responsible for wrongful acts.” The insured provided its insurer with financial documentation showing its loan portfolio was in trouble.

Brown & Kornegay LLP 35

36 36

“Best” Practices • Review the policy. Policies that allow the insured to provide a circ-

notice are not uniform in their wording. Do you have enough information to provide an adequate notice?

• Make sure there is sufficient internal discussion about the

circumstances—gather adequate detail for the notice. • Get outside advice from experienced coverage counsel and/or the

broker who placed the policy on the content of the notice letter. Does it satisfy the elements of the notice requirement?

• Follow up with the insurer. Make sure they received the notice. Get

their acknowledgement in writing that the notice was sufficient and accepted. If they decline, supplement with additional notice before the policy expires.