28

Balance of Payments and Foreign Exchange International Business Lecture 2b

| Date post: | 28-Jul-2015 |

| Category: |

Business |

| Upload: | samiya-tabassum |

| View: | 51 times |

| Download: | 0 times |

Balance of Payments and Foreign Exchange

International BusinessLecture 2b

Factors of International Business

• Production of Goods and Services• Routes, Roads and Transportation System• Technological Development• Development of Monetary and Exchange

System• Advertising world wide

• Today we want to talk about national monetary system before we discuss international monetary system

• And influence and determination of Exchange Rate

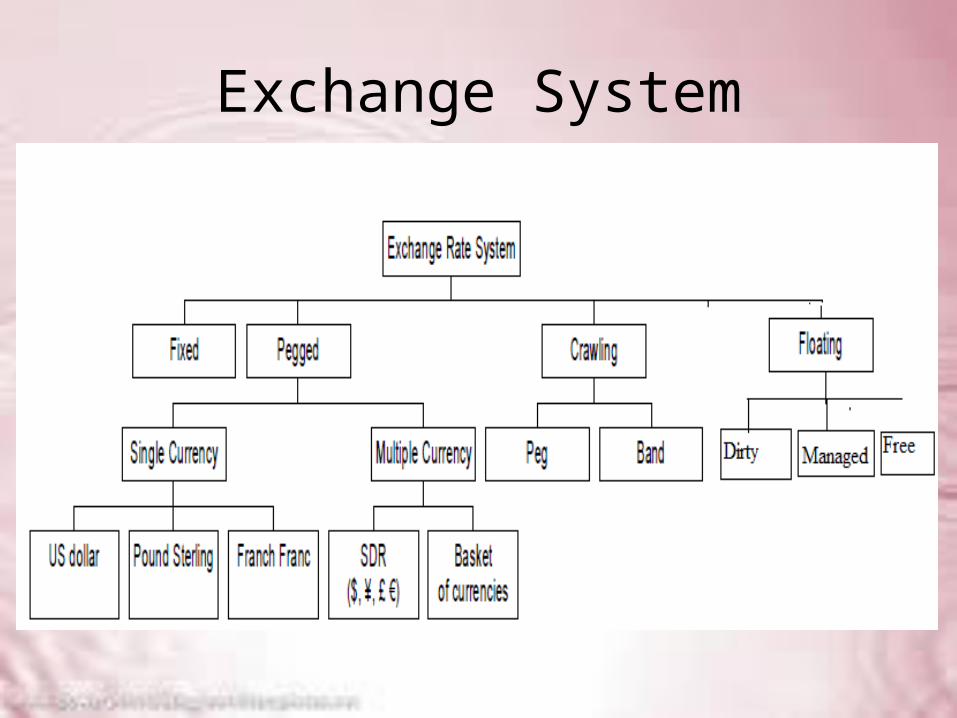

Exchange System

Foreign Exchange Rate

Foreign exchange rates (the price of one country’s currency in terms of another’s) are important because they affect the price of domestically produced goods sold abroad and the cost of foreign goods bought domestically.

Factors Affecting Exchange Rate –Long Run

• The theory of purchasing power parity suggests that long-run changes in the exchange rate between two countries’ currencies are determined by changes in the relative price levels in the two countries.

• Other factors that affect exchange rates in the long run are tariffs and quotas, import demand, export demand, and productivity.

Determinants of Exchange Rate – Short Run

3. In the short run, exchange rates are determined bychanges in the relative expected return on domesticassets, which cause the demand curve to shift. Any factor that changes the relative expected return on domestic assets will lead to changes in the exchangerate. Such factors include changes in the interest rateson domestic and foreign assets as well as changes inany of the factors that affect the long-run exchangerate and hence the expected future exchange rate.

Determinants of Exchange Rate

4. The asset market approach to exchange rate determination can explain both the volatility of exchange rates and the rise of the dollar in the 1980–1984 period and its subsequent fall.

5. Forecasts of foreign exchange rates are very valuableto managers of financial institutions becausethese rates influence decisions about which assetsdenominated in foreign currencies the institutionsshould hold and what kinds of trades should be madeby their traders in the foreign exchange market.

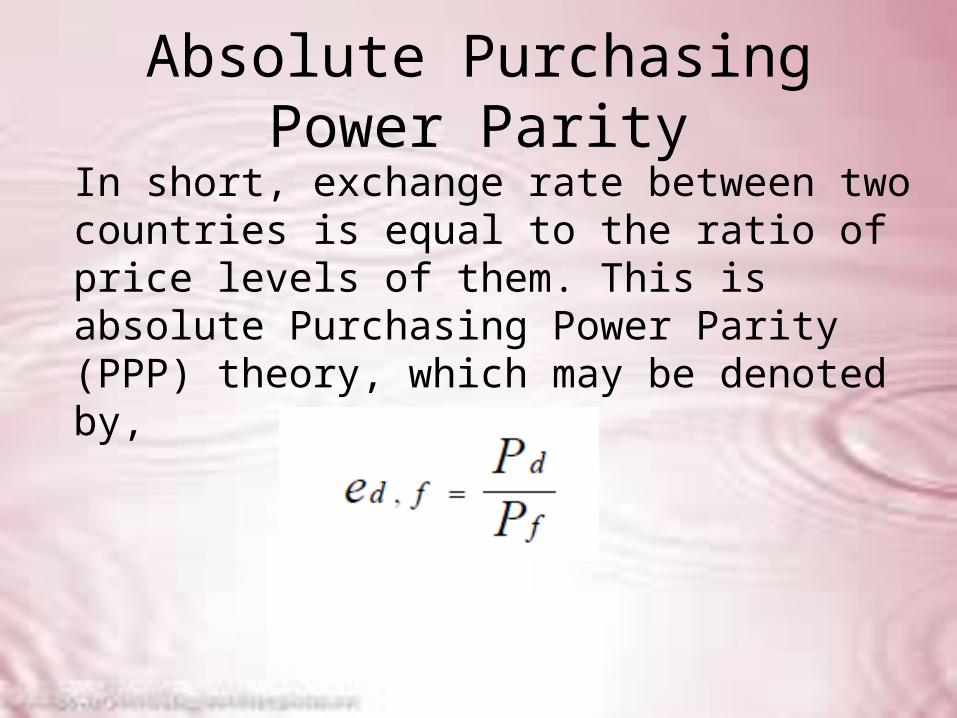

Absolute Purchasing Power ParityIn short, exchange rate between two countries is equal to the ratio of price levels of them. This is absolute Purchasing Power Parity (PPP) theory, which may be denoted by,

Relative Purchasing Power Parity

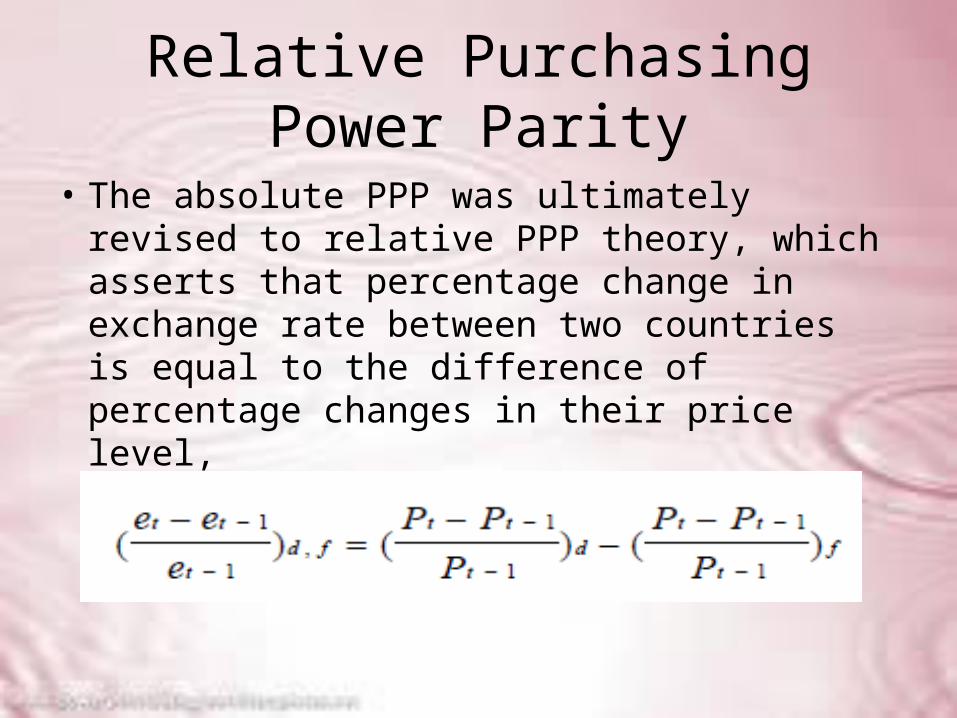

• The absolute PPP was ultimately revised to relative PPP theory, which asserts that percentage change in exchange rate between two countries is equal to the difference of percentage changes in their price level,

• %Δe = %ΔPd -%ΔPf

• Or, • When π is inflation rate • %Δe = π d - πf

• Note that inflation is the percentage changes in prices

Fisher Effect

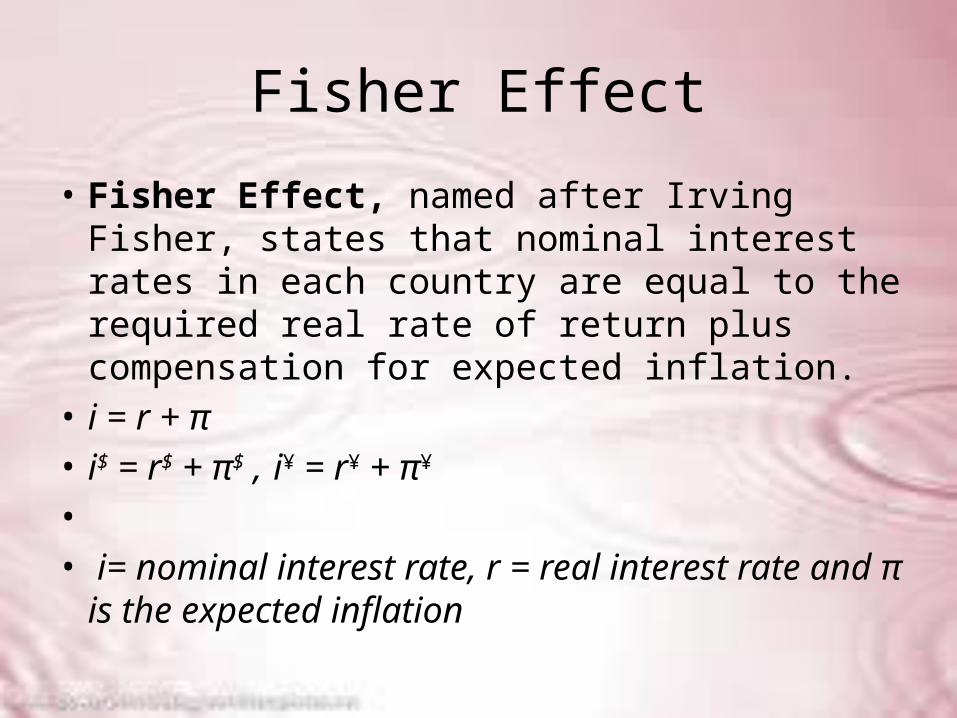

• Fisher Effect, named after Irving Fisher, states that nominal interest rates in each country are equal to the required real rate of return plus compensation for expected inflation.

• i = r + π • i$ = r$ + π$ , i¥ = r¥ + π¥ • • i= nominal interest rate, r = real interest rate

and π is the expected inflation

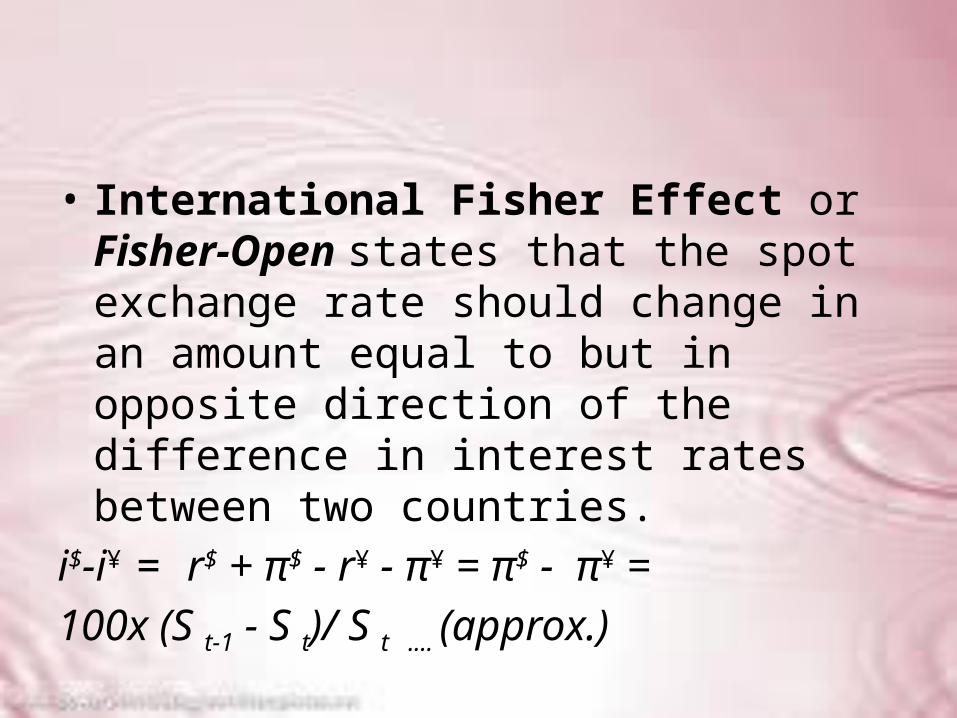

• International Fisher Effect or Fisher-Open states that the spot exchange rate should change in an amount equal to but in opposite direction of the difference in interest rates between two countries.

i$-i¥ = r$ + π$ - r¥ - π¥ = π$ - π¥ = 100x (S t-1 - S t)/ S t .... (approx.)

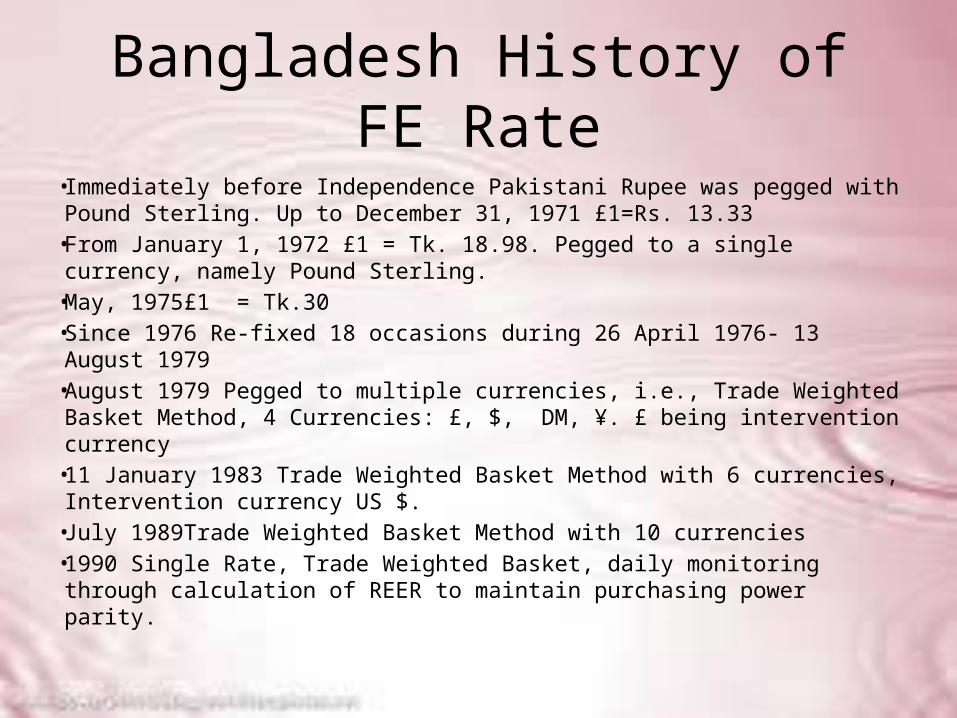

Bangladesh History of FE Rate• Immediately before Independence Pakistani Rupee was pegged with

Pound Sterling. Up to December 31, 1971 £1=Rs. 13.33• From January 1, 1972 £1 = Tk. 18.98. Pegged to a single currency, namely

Pound Sterling.• May, 1975£1 = Tk.30• Since 1976 Re-fixed 18 occasions during 26 April 1976- 13 August 1979• August 1979 Pegged to multiple currencies, i.e., Trade Weighted Basket

Method, 4 Currencies: £, $, DM, ¥. £ being intervention currency• 11 January 1983 Trade Weighted Basket Method with 6 currencies,

Intervention currency US $.• July 1989Trade Weighted Basket Method with 10 currencies• 1990 Single Rate, Trade Weighted Basket, daily monitoring through

calculation of REER to maintain purchasing power parity.

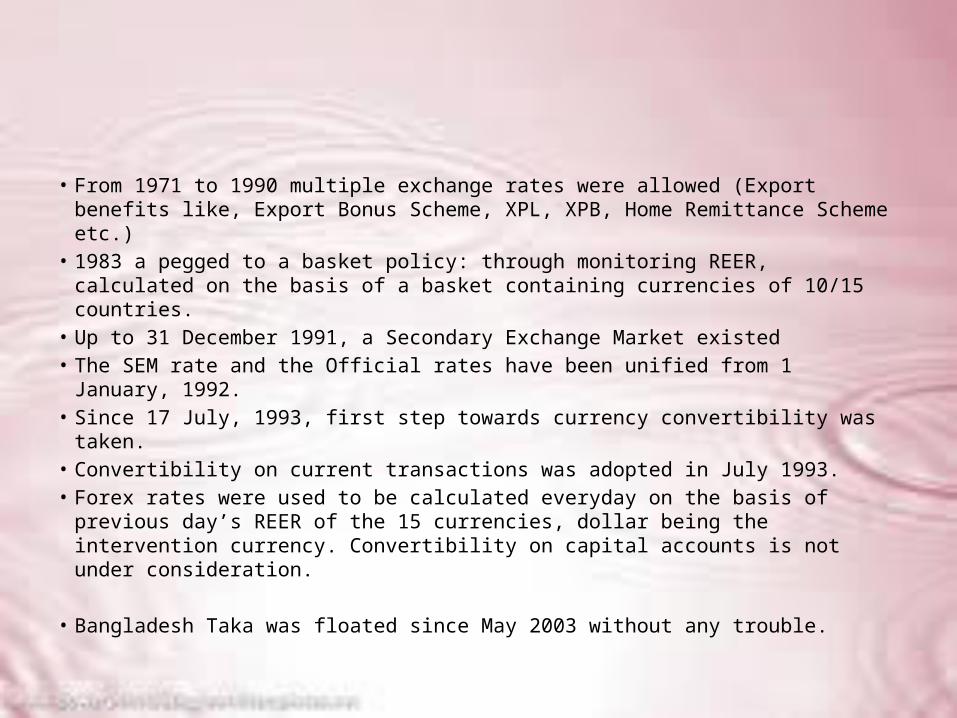

• From 1971 to 1990 multiple exchange rates were allowed (Export benefits like, Export Bonus Scheme, XPL, XPB, Home Remittance Scheme etc.)

• 1983 a pegged to a basket policy: through monitoring REER, calculated on the basis of a basket containing currencies of 10/15 countries.

• Up to 31 December 1991, a Secondary Exchange Market existed • The SEM rate and the Official rates have been unified from 1 January, 1992. • Since 17 July, 1993, first step towards currency convertibility was taken.• Convertibility on current transactions was adopted in July 1993. • Forex rates were used to be calculated everyday on the basis of previous

day’s REER of the 15 currencies, dollar being the intervention currency. Convertibility on capital accounts is not under consideration.

• Bangladesh Taka was floated since May 2003 without any trouble.

International Finance© Mojmir Mrak

Page 16

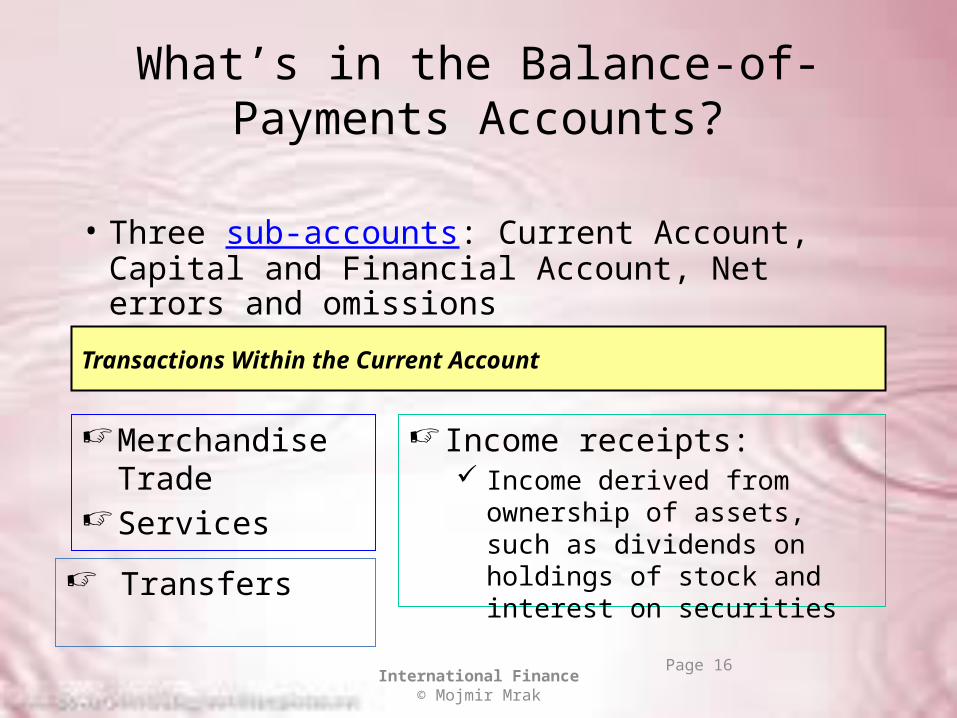

What’s in the Balance-of-Payments Accounts?

• Three sub-accounts: Current Account, Capital and Financial Account, Net errors and omissions

Merchandise TradeServices

Transactions Within the Current Account

Income receipts: Income derived from ownership of

assets, such as dividends on holdings of stock and interest on securities Transfers

International Finance© Mojmir Mrak Page 17

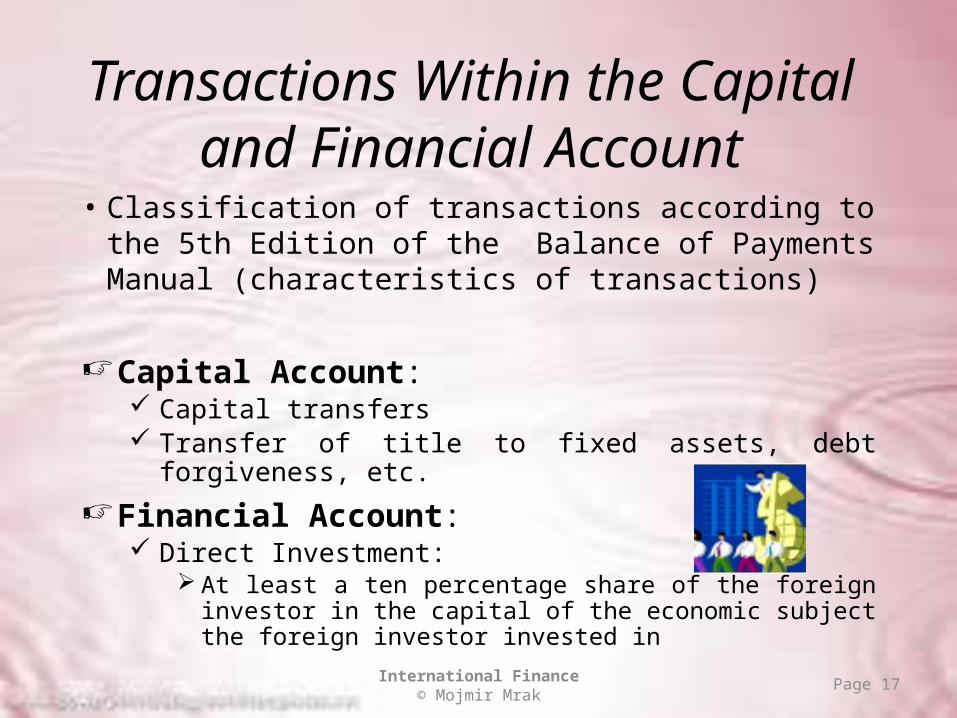

Transactions Within the Capital and Financial Account

• Classification of transactions according to the 5th Edition of the Balance of Payments Manual (characteristics of transactions)

Capital Account: Capital transfers Transfer of title to fixed assets, debt forgiveness, etc.

Financial Account: Direct Investment:

At least a ten percentage share of the foreign investor in the capital of the economic subject the foreign investor invested in

International Finance© Mojmir Mrak Page 18

Transactions Within the Capital and Financial Account

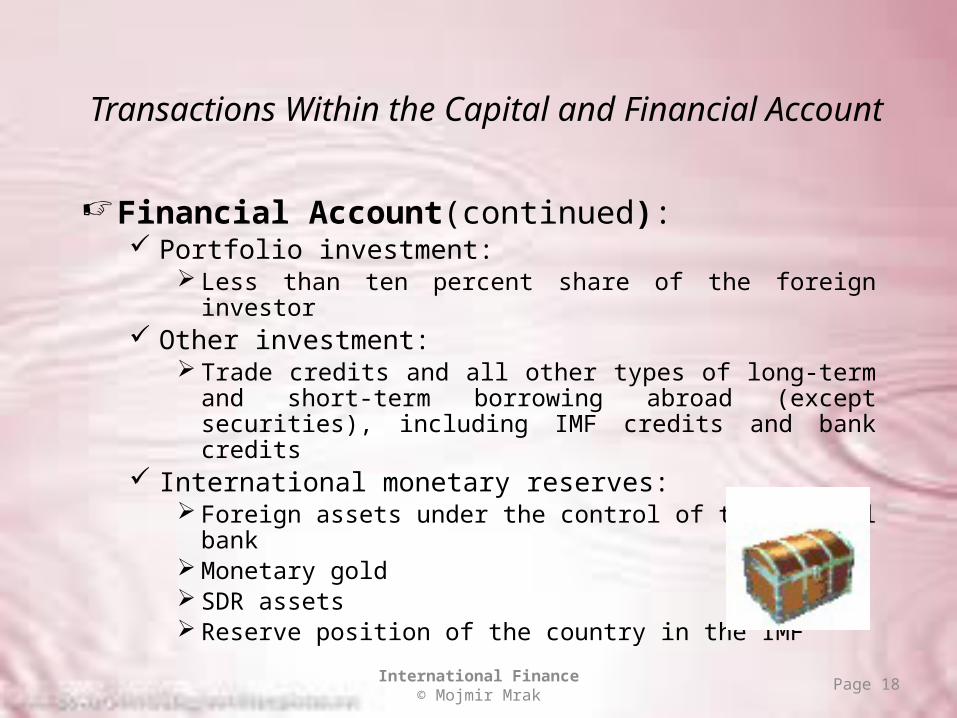

Financial Account(continued): Portfolio investment:

Less than ten percent share of the foreign investor Other investment:

Trade credits and all other types of long-term and short-term borrowing abroad (except securities), including IMF credits and bank credits

International monetary reserves: Foreign assets under the control of the central bank Monetary gold SDR assets Reserve position of the country in the IMF

International Finance© Mojmir Mrak Page 19

Errors and Omissions Complete recording of transactions is impossible Errors and omissions reflect the statistical discrepancy of recording

the BOP transactions: Difference between recorded credit statements and recorded debit

statements Reasons for errors and omissions:

Incomplete recording of transactions between residents and non-residents

Tax evasion Time discrepancy between the occurrence of the transaction and its

settlement Unregistered international merchandise trade Incomplete data about the “escape of capital” and about the financial

transactions in offshore centers

International Finance© Mojmir Mrak Page 20

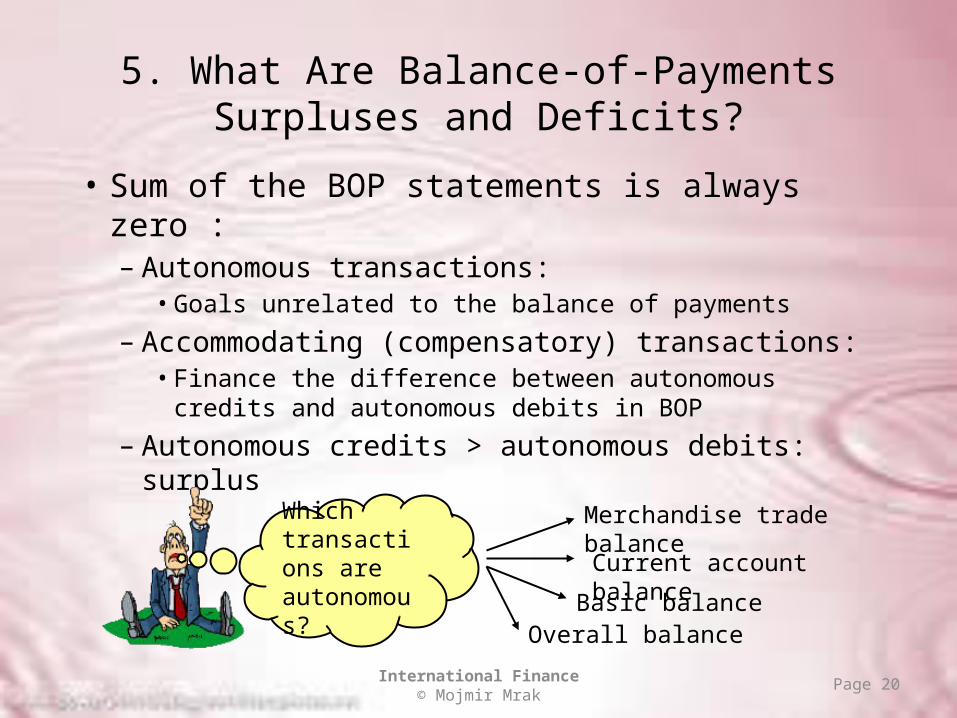

5. What Are Balance-of-Payments Surpluses and Deficits?

• Sum of the BOP statements is always zero :– Autonomous transactions:

• Goals unrelated to the balance of payments

– Accommodating (compensatory) transactions:• Finance the difference between autonomous credits

and autonomous debits in BOP

– Autonomous credits > autonomous debits: surplus

Which transactions are autonomous?

Merchandise trade balance

Current account balance

Basic balanceOverall balance

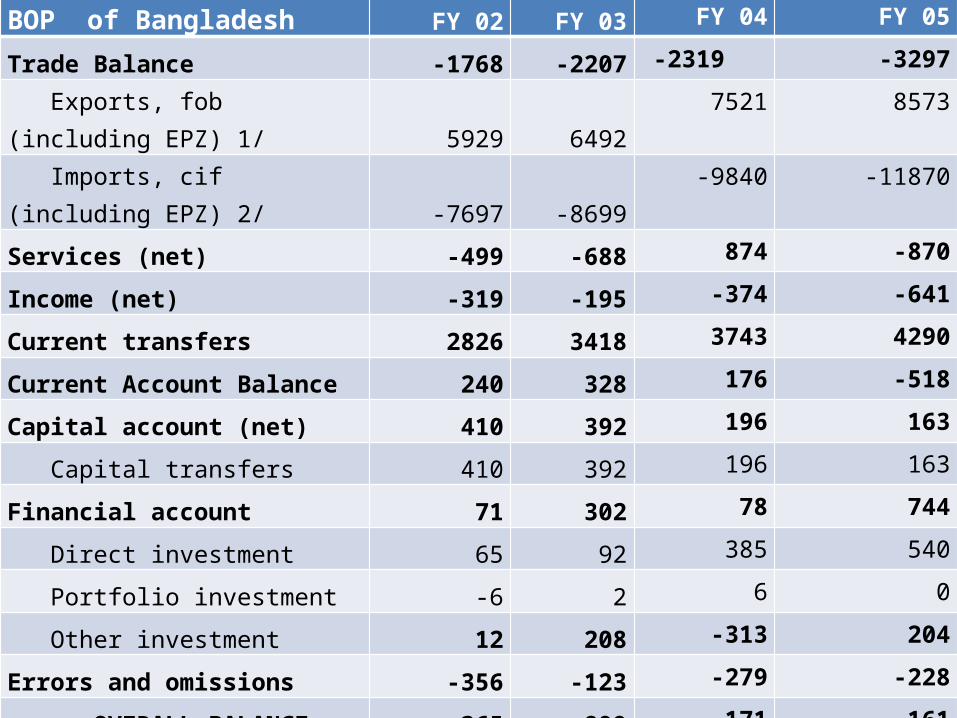

Bangladesh BOPBOP of Bangladesh FY 02 FY 03 FY 04 FY 05

Trade Balance -1768 -2207 -2319 -3297

Exports, fob (including EPZ) 1/ 5929 6492 7521 8573

Imports, cif (including EPZ) 2/ -7697 -8699 -9840 -11870

Services (net) -499 -688 874 -870

Income (net) -319 -195 -374 -641

Current transfers 2826 3418 3743 4290

Current Account Balance 240 328 176 -518

Capital account (net) 410 392 196 163

Capital transfers 410 392 196 163

Financial account 71 302 78 744

Direct investment 65 92 385 540

Portfolio investment -6 2 6 0

Other investment 12 208 -313 204

Errors and omissions -356 -123 -279 -228

OVERALL BALANCE 365 899 171 161

Reserve Assets -365 -899 -171 -161

CONVENTIONS IN

FOREIGN EXCHANGE

MARKET

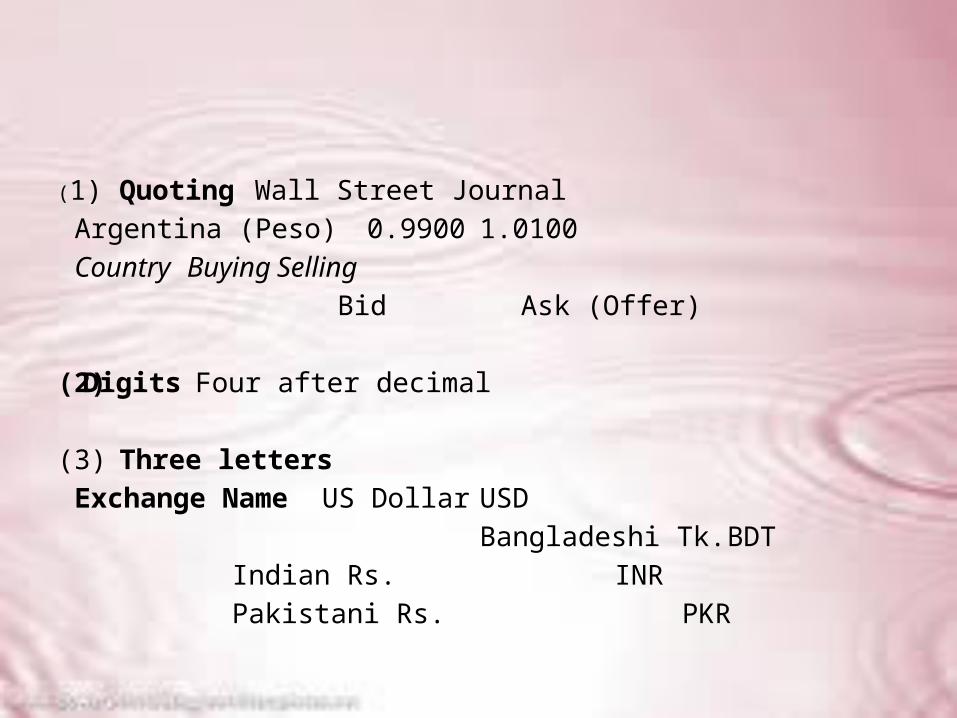

(1)Quoting Wall Street Journal Argentina (Peso) 0.9900 1.0100CountryBuying Selling

Bid Ask (Offer) (2) Digits Four after decimal (3) Three letters

Exchange Name US Dollar USD Bangladeshi Tk. BDT

Indian Rs. INR Pakistani Rs. PKR

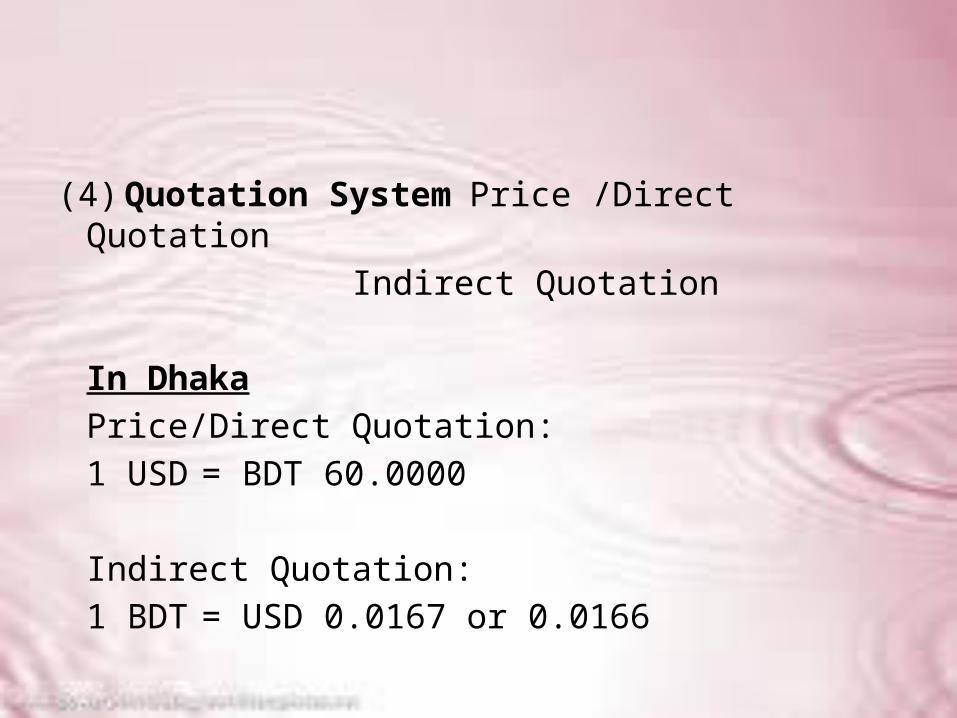

(4) Quotation System Price /Direct Quotation Indirect Quotation

In DhakaPrice/Direct Quotation:1 USD = BDT 60.0000

Indirect Quotation:1 BDT = USD 0.0167 or 0.0166

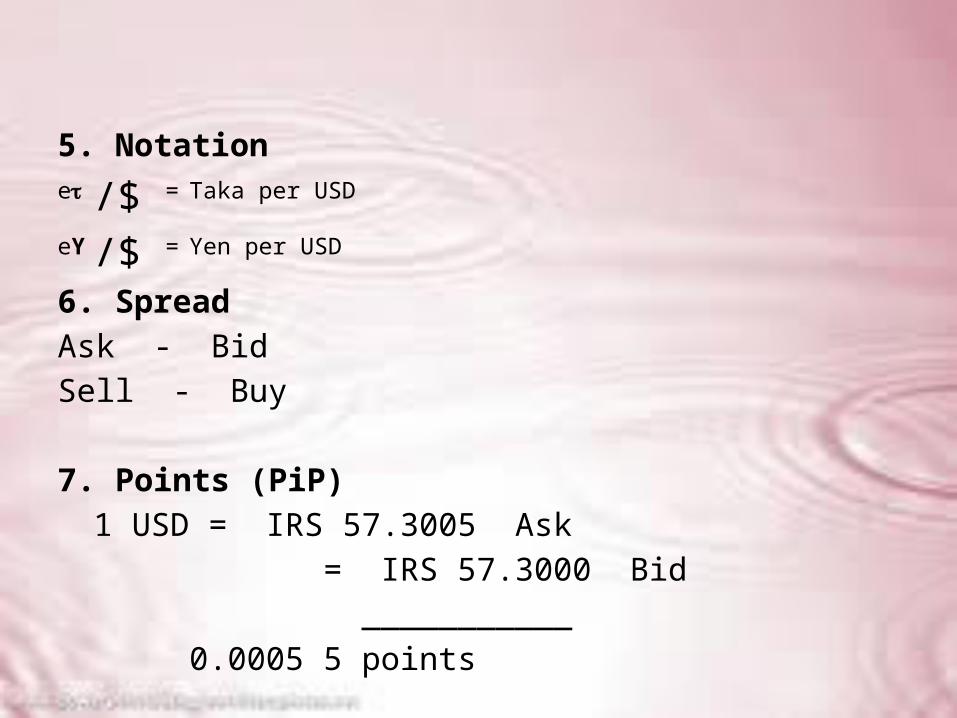

5. Notatione /$ = Taka per USD

eY /$ = Yen per USD

6. SpreadAsk - BidSell - Buy

7. Points (PiP)1 USD = IRS 57.3005 Ask = IRS 57.3000 Bid ___________

0.0005 5 points

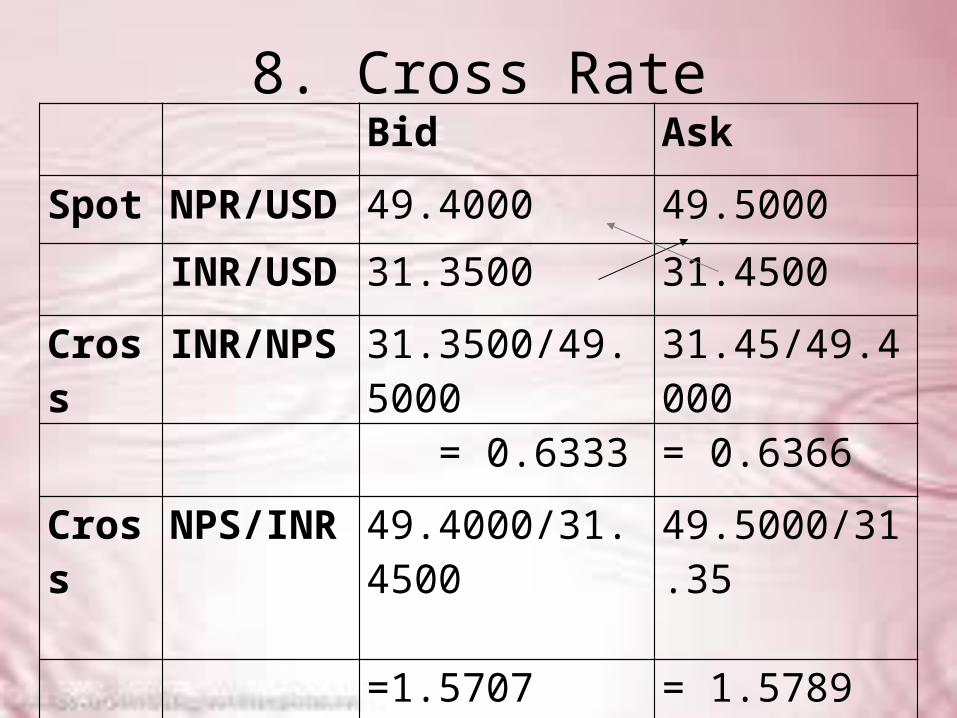

8. Cross RateBid Ask

Spot NPR/USD 49.4000 49.5000

INR/USD 31.3500 31.4500

Cross INR/NPS 31.3500/49.5000 31.45/49.4000

= 0.6333 = 0.6366

Cross NPS/INR 49.4000/31.4500 49.5000/31.35

=1.5707 = 1.5789

(Others Bid divided by own Ask; Others Ask divided by own Bid)

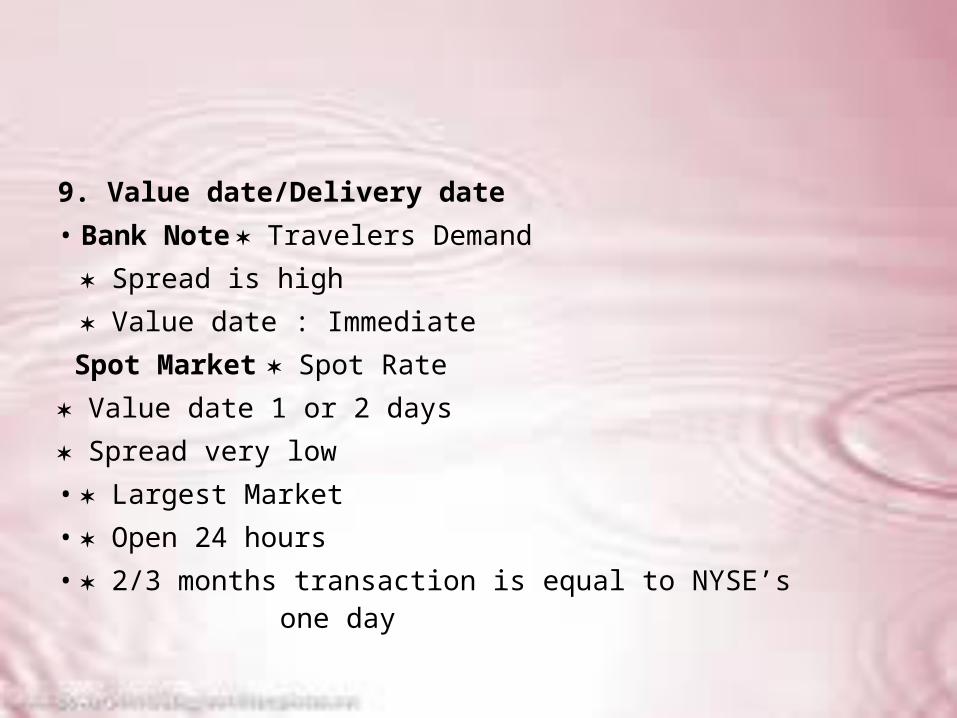

9. Value date/Delivery date• Bank Note Travelers Demand

Spread is high Value date : Immediate

Spot Market Spot Rate Value date 1 or 2 days Spread very low• Largest Market • Open 24 hours• 2/3 months transaction is equal to NYSE’s one day

Forward Market• (Contacted today for the exchange of currencies at a specified date in the

future) 1, 2, 3, 4, 6, 9, 12 months

Value date + 1/2 days No forecasting No Speculation Ensure supply of currency later • Forward Premium Forward Rate Spot Rate

• Forward Discount Forward Rate Spot Rate

• Forward Flat Forward Rate = Spot Rate