97

ANNUAL REPORT 2009/10

Assisting parliament to improve the accountability and performance of the state

Level 15, 1 Margaret Street Sydney NSW 2000 Australia GPO Box 12 Sydney NSW 2001 Tel +61 2 9275 7100Fax +61 2 9275 [email protected] am–5.00 pm

www.audit.nsw.gov.au

The A

ud

iT Office O

f NeW

SOu

Th W

ALeS A

NN

uA

L RePORT / yeA

R eNd

ed 30 Ju

Ne 2010

ANNuAL RePORT

2009/10

highlights inside front cover

Ourorganisation 1

Parliament Regularly seek and use our advice 7

agencies Act on our recommendations and regularly seek advice 15

People Our people are highly skilled and dedicated to improving the public sector 29

Profession We are known for influencing auditing in Australia 39

Finances We break even financially over the medium term 43

Financialreport 47

appendices 71

index inside back cover

contents

GPO BOX 12 Sydney NSW 2001

Members of Legislative Assembly Parliament house Sydney NSW 2000

under section 12A of the Annual Reports (Statutory Bodies) Act 1984, i have pleasure in submitting for the information of members, the Reports of the activities of the Audit Office of New South Wales for the year ended 30 June 2010.

Peter Achterstraatauditor-General29October2010

cover: L–R chariee Bultitude, Angelina Pillay, Jonathan Lam, daniel AlizadehThisreport

This annual report summarises the activities and performance of the Audit Office of New South Wales for 2009–10 against the main objectives, strategies and targets in its strategic plan. As well as looking at the year gone past, the report looks to the year ahead and reports on financial results for the year. This and earlier annual reports are available on the Audit Office website: www.audit.nsw.gov.au. Printed copies are available on request from the Office.

The Audit Office of New South Wales AnnuAl RepoRt 2009/10a

allegations of waste 13annual report costs inside back cover contact details back coverAudit and Risk Committee 36Auditor-General message 2 history 1Australasian Council of Auditors-General 41

b

benchmarking inside front cover, 9, 11, 36budget 44business risks 35

c

central government reporting 36client satisfaction 16code of conduct 35committees 36–37consultants 66corporate governance 35credit card certification 92creditor payments 45

d

disability action plan 90

e

employee satisfaction 30energy management 38environmental action 38equal employment opportunity 89equity 33executive positions 4, 72–73

f

financial audits clients 74 qualifications 10, 20 recommendations, acceptance of 18 reports 87 satisfaction with 16 timeliness 19financial commentary 44 accounts payable performance 92 break-even target 44 financial statistics 46financial statements 47freedom of information 37

h

highlights inside front cover

i

industrial relations 32information management 31internal audit and risk management statement 35, 37, 91ISO 9001 37ISO 27001 31

l

legislation 35letter of transmission inside front cover

m

mission 1multicultural policies and services program 89–90

o

objectives 1occupational health and safety 38office executive 4 performance statements 72office hours back coveroverseas secondments 32, 34 travel 80

p

parliamentarian satisfaction 8parliamentary committees, appearances before 81people 29people development 34

performance audits 22 follow-up 14, 22, 28 recommendations, acceptance of 18 reports 87 satisfaction 16performance management 31presentations private sector 40, 85 public sector 40, 82privacy 37professional activities 40–41professional development 34Public Accounts Committee 14 hearings 14publications 87

q

quality assurance 36–37

r

reviews, internal and external 37risk management 35, 37

s

social club 33stakeholders/clients 1staff counselling 33 productivity 31 recruitment 32strategic plan 6, 35structure 4

t

training 34, 41turnover 32

v

values 1vision 1

w

Waste Reduction and Purchasing Plan 38

y

year ahead, the 6

Index

Annualreportproduction

Total external costs to produce 400 copies were $32,000 for design, photography and printing.

Design

CampbellBarnett www.campbellbarnett.com

photography

Martin Mischkulnig www.martinmischkulnig.com

Parliament

Parliamentarians generally satisfied with our reports and refer to them frequently.

90 per cent satisfied with our reports and services.

95 per cent agree that our financial audits provide valuable assurance.

90 per cent believe our financial audit reports have effective layout and design.

93 per cent believe our performance audit reports identify significant issues.

86 per cent of financial audits reported to parliament on time.

8 performance audits reviewed by the Parliament of New South Wales’ Public Accounts Committee.

Refer to page 7

Agencies

Good ratings for agencies’ overall perceptions of our financial audits.

Significant increase in agencies’ overall perceptions of our performance audits.

97 per cent of financial audit recommendations accepted.

92 per cent of performance audit recommendations accepted.

95 per cent of audit opinions were unqualified.

495 financial audits completed.

14 performance audits completed, 7 more than last year.

Refer to page 15

People

79 per cent employee satisfaction.

91 per cent of staff ‘satisfied’ or ‘extremely satisfied’.

83 per cent of employees highly engaged.

86 per cent employee morale—a 7-year high.

65 per cent productivity—an increase on last year.

44 per cent of middle management are women— a significant increase on last year.

7 per cent staff turnover.

4-star greenhouse building rating maintained.

Refer to page 29

Profession

38 presentations delivered to the public and the profession.

23 submissions made on proposed changes to accounting and auditing standards.

Refer to page 39

Finances

$0.8 million loss (excluding superannuation adjustments), the 5-year cumulative result outside our medium-term break-even point.

Current ratio (solvency) is healthy.

99 per cent of our creditors paid on time.

Refer to page 43

Benchmarks

We benchmark ourselves against the national average for audit offices.

We expect our costs, as a proportion of total state assets and transactions, to be lower than most other states. As NSW agencies are typically larger than their interstate counterparts and the Audit Office of New South Wales is also larger, the economies of scale allow us to achieve lower costs on these measures.

Audit Office of NSW Average of Australian audit offices

Total audit costs (excluding payroll tax) per $’000 of public sector assets $2010 results not available.

.14

.23

.13

.20

.12

.21

.13.21

.14.20

2005

2006

2007

2008

2009

38 presentations made, 3 more than last year

$0.8 million loss (excluding superannuation adjustments), the 5-year cumulative result outside our medium-term break-even target

Our costs are significantly less than other Australian state audit offices

90% satisfied with our reports and services

97% of financial audit and 92% of performance audit recommendations accepted

91% of staff ‘satisfied’ or ‘extremely satisfied’

Highlights

86

93

91

94

90

2005

2006

2008

2009

2010

Overall satisfaction % satisfied or very satisfied.Surveys not conducted in 2007.

2011 target 90

Overall satisfaction %Aggregate performance indices.

Financial audit clients

702006

Performance audit clients

67

712007

68

712008

77

702009

67

702010

73

752011 target

75

76

79

76

78

79

80

2006

2007

2008

2009

2010

2011 target

Employee satisfaction %

35

31

21

36

38

35

2006

2007

2008

2009

2010

2011 target

Presentations given

2006

2007

2008

2009

2010

2011

tar

get

2006

2007

2008

2009

2010

2011 target-1.0

-0.8

2.2

2.6

3.7

Operating results $mExcluding superannuation.

2.1

Total audit costs (excluding payroll tax) per $’000 of public sector transactions $ 2010 results not available.

Audit Office of NSW Average of Australian audit offices

.38

.35

.37

.39

.37

.282005

.252006

.242007

.262008

.272009

The Audit Office of New South Wales annualrePOrT2009/10a

allegations of waste 13annual report costs inside back cover contact details back coverAudit and Risk committee 36Auditor-General message 2 history 1Australasian council of Auditors-General 41

b

benchmarking inside front cover, 9, 11, 36budget 44business risks 35

c

central government reporting 36client satisfaction 16code of conduct 35committees 36–37consultants 66corporate governance 35credit card certification 92creditor payments 45

d

disability action plan 90

e

employee satisfaction 30energy management 38environmental action 38equal employment opportunity 89equity 33executive positions 4, 72–73

f

financial audits clients 74 qualifications 10, 20 recommendations, acceptance of 18 reports 87 satisfaction with 16 timeliness 19financial commentary 44 accounts payable performance 92 break-even target 44 financial statistics 46financial statements 47freedom of information 37

h

highlights inside front cover

i

industrial relations 32information management 31internal audit and risk management statement 35, 37, 91iSO 9001 37iSO 27001 31

l

legislation 35letter of transmission inside front cover

m

mission 1multicultural policies and services program 89–90

o

objectives 1occupational health and safety 38office executive 4 performance statements 72office hours back coveroverseas secondments 32, 34 travel 80

p

parliamentarian satisfaction 8parliamentary committees, appearances before 81people 29people development 34

performance audits 22 follow-up 14, 22, 28 recommendations, acceptance of 18 reports 87 satisfaction 16performance management 31presentations private sector 40, 85 public sector 40, 82privacy 37professional activities 40–41professional development 34Public Accounts committee 14 hearings 14publications 87

q

quality assurance 36–37

r

reviews, internal and external 37risk management 35, 37

s

social club 33stakeholders/clients 1staff counselling 33 productivity 31 recruitment 32strategic plan 6, 35structure 4

t

training 34, 41turnover 32

v

values 1vision 1

w

Waste Reduction and Purchasing Plan 38

y

year ahead, the 6

index

Annualreportproduction

Total external costs to produce 400 copies were $32,000 for design, photography and printing.

Design

campbellBarnett www.campbellbarnett.com

Photography

Martin Mischkulnig www.martinmischkulnig.com

Parliament

Parliamentarians generally satisfied with our reports and refer to them frequently.

90 per cent satisfied with our reports and services.

95 per cent agree that our financial audits provide valuable assurance.

90 per cent believe our financial audit reports have effective layout and design.

93 per cent believe our performance audit reports identify significant issues.

86 per cent of financial audits reported to parliament on time.

8 performance audits reviewed by the Parliament of New South Wales’ Public Accounts committee.

Refer to page 7

Agencies

Good ratings for agencies’ overall perceptions of our financial audits.

Significant increase in agencies’ overall perceptions of our performance audits.

97 per cent of financial audit recommendations accepted.

92 per cent of performance audit recommendations accepted.

95 per cent of audit opinions were unqualified.

495 financial audits completed.

14 performance audits completed, 7 more than last year.

Refer to page 15

People

79 per cent employee satisfaction.

91 per cent of staff ‘satisfied’ or ‘extremely satisfied’.

83 per cent of employees highly engaged.

86 per cent employee morale—a 7-year high.

65 per cent productivity—an increase on last year.

44 per cent of middle management are women— a significant increase on last year.

7 per cent staff turnover.

4-star greenhouse building rating maintained.

Refer to page 29

Profession

38 presentations delivered to the public and the profession.

23 submissions made on proposed changes to accounting and auditing standards.

Refer to page 39

Finances

$0.8 million loss (excluding superannuation adjustments), the 5-year cumulative result outside our medium-term break-even point.

current ratio (solvency) is healthy.

99 per cent of our creditors paid on time.

Refer to page 43

Benchmarks

We benchmark ourselves against the national average for audit offices.

We expect our costs, as a proportion of total state assets and transactions, to be lower than most other states. As NSW agencies are typically larger than their interstate counterparts and the Audit Office of New South Wales is also larger, the economies of scale allow us to achieve lower costs on these measures.

Audit Office of NSW Average of Australian audit offices

Total audit costs (excluding payroll tax) per $’000 of public sector assets $2010 results not available.

.14

.23

.13

.20

.12

.21

.13.21

.14.20

2005

2006

2007

2008

2009

38 presentations made, 3 more than last year

$0.8 million loss (excluding superannuation adjustments), the 5-year cumulative result outside our medium-term break-even target

Our costs are significantly less than other Australian state audit offices

90% satisfied with our reports and services

97% of financial audit and 92% of performance audit recommendations accepted

91% of staff ‘satisfied’ or ‘extremely satisfied’

highlights

86

93

91

94

90

2005

2006

2008

2009

2010

Overall satisfaction % satisfied or very satisfied.Surveys not conducted in 2007.

2011 target 90

Overall satisfaction %Aggregate performance indices.

Financial audit clients

702006

Performance audit clients

67

712007

68

712008

77

702009

67

702010

73

752011 target

75

76

79

76

78

79

80

2006

2007

2008

2009

2010

2011 target

Employee satisfaction %

35

31

21

36

38

35

2006

2007

2008

2009

2010

2011 target

Presentations given

2006

2007

2008

2009

2010

2011

tar

get

2006

2007

2008

2009

2010

2011 target-1.0

-0.8

2.2

2.6

3.7

Operating results $mExcluding superannuation.

2.1

Total audit costs (excluding payroll tax) per $’000 of public sector transactions $ 2010 results not available.

Audit Office of NSW Average of Australian audit offices

.38

.35

.37

.39

.37

.282005

.252006

.242007

.262008

.272009

Assisting parliament to improve the accountability and performance of the state

Level 15, 1 Margaret Street Sydney NSW 2000 Australia GPO Box 12 Sydney NSW 2001 Tel +61 2 9275 7100Fax +61 2 9275 [email protected] am–5.00 pm

www.audit.nsw.gov.au

The A

ud

iT Office O

f NeW

SOu

Th W

ALeS A

NN

uA

L RePORT / yeA

R eNd

ed 30 Ju

Ne 2010

ANNuAL RePORT

2009/10

highlights inside front cover

Ourorganisation 1

Parliament Regularly seek and use our advice 7

agencies Act on our recommendations and regularly seek advice 15

People Our people are highly skilled and dedicated to improving the public sector 29

Profession We are known for influencing auditing in Australia 39

Finances We break even financially over the medium term 43

Financialreport 47

appendices 71

index inside back cover

contents

GPO BOX 12 Sydney NSW 2001

Members of Legislative Assembly Parliament house Sydney NSW 2000

under section 12A of the Annual Reports (Statutory Bodies) Act 1984, i have pleasure in submitting for the information of members, the Reports of the activities of the Audit Office of New South Wales for the year ended 30 June 2010.

Peter Achterstraatauditor-General29October2010

cover: L–R chariee Bultitude, Angelina Pillay, Jonathan Lam, daniel AlizadehThisreport

This annual report summarises the activities and performance of the Audit Office of New South Wales for 2009–10 against the main objectives, strategies and targets in its strategic plan. As well as looking at the year gone past, the report looks to the year ahead and reports on financial results for the year. This and earlier annual reports are available on the Audit Office website: www.audit.nsw.gov.au. Printed copies are available on request from the Office.

Who we are

The Audit Office of New South Wales (the ‘Office’) is a statutory authority, established under the Public Finance and Audit Act 1983, that conducts audits for the Auditor-General. The Auditor-General helps parliament hold government accountable for its use of public resources.

What we do

The Auditor-General is responsible for audits and related services.

The Office conducts financial and performance audits, principally under the Public Finance and Audit Act 1983 and the Corporations Act 2001, and examines allegations of serious and substantial waste of public money (under the Protected Disclosures Act 1994).

The Auditor-General also provides certain assurance services for Commonwealth grants and payments to the state under Commonwealth legislation.

Our main clients

Parliament of New South Wales.

NSW government agencies.

The people of New South Wales.

Our resources

254 staff at 30 June 2010.

$28.6 million from government agencies for audits of their financial reports.

$5.8 million from the government towards our performance audits and reports to parliament.

Nine external audit contractors assist with our financial report audits, representing about six per cent of our financial audit work.

Our history

For more than 180 years, the Audit Office of New South Wales has been assisting the Parliament of New South Wales hold government accountable for its use of public resources.

We do this by reporting directly to parliament on our audits of government financial reports and performance.

Our organisationBuilt on strategic foundations

The history of the Auditor-General

1824William Lithgow appointed Colonial Auditor-General, to compile and examine the colony’s accounts and report on government departments to the Governor.

1855The UK Constitution Act 1855 formalised government in New South Wales, and Auditor-General made a member of the government.

1870Powers and duties of Auditor-General first set in legislation, in the Audit Act 1870.

1902Audit Act 1902 prohibited the Auditor-General from being a member of the Executive Council or of parliament.

1929Audit (Amendment) Act 1929 changed the tenure of office of the Auditor-General from life to ceasing at 65. Position of Assistant Auditor-General created.

1984Public Finance and Audit Act 1983 established Auditor-General’s Office (6 January 1984).

1989Auditor-General’s Office declared a statutory body, allowing it to be both more independent and more commercial.

1991The Public Finance and Audit Act 1983 expanded the Auditor-General’s role to include performance audits, limited tenure to seven years and prevented acceptance of any other post in the NSW public service.

2001Auditor-General’s role expanded to reporting on issues of waste, probity and financial judgement.

2004Auditor-General given power to employ staff directly, and set wages and conditions.

Our vision

To make the people of New South Wales proud of the work we do.

Our mission

To perform high quality independent audits of government in New South Wales.

Our objectives

Our advice—parliament and agencies regularly seek our advice and act on our recommendations.

Our people—our people are highly skilled and dedicated to improving the public sector.

Our profession—we are known for influencing auditing in Australia.

Our finances—we break even over the medium term.

Our values

Purpose—we have an impact, are accountable, and work as a team.

People—we trust and respect others and have a balanced approach to work.

Professionalism—we are recognised for our independence and integrity and the value we deliver.

The Audit Office of New South Wales AnnuAl RePORt 2009/10

1

The Audit Office of New South Wales AnnuAl RePORt 2009/10

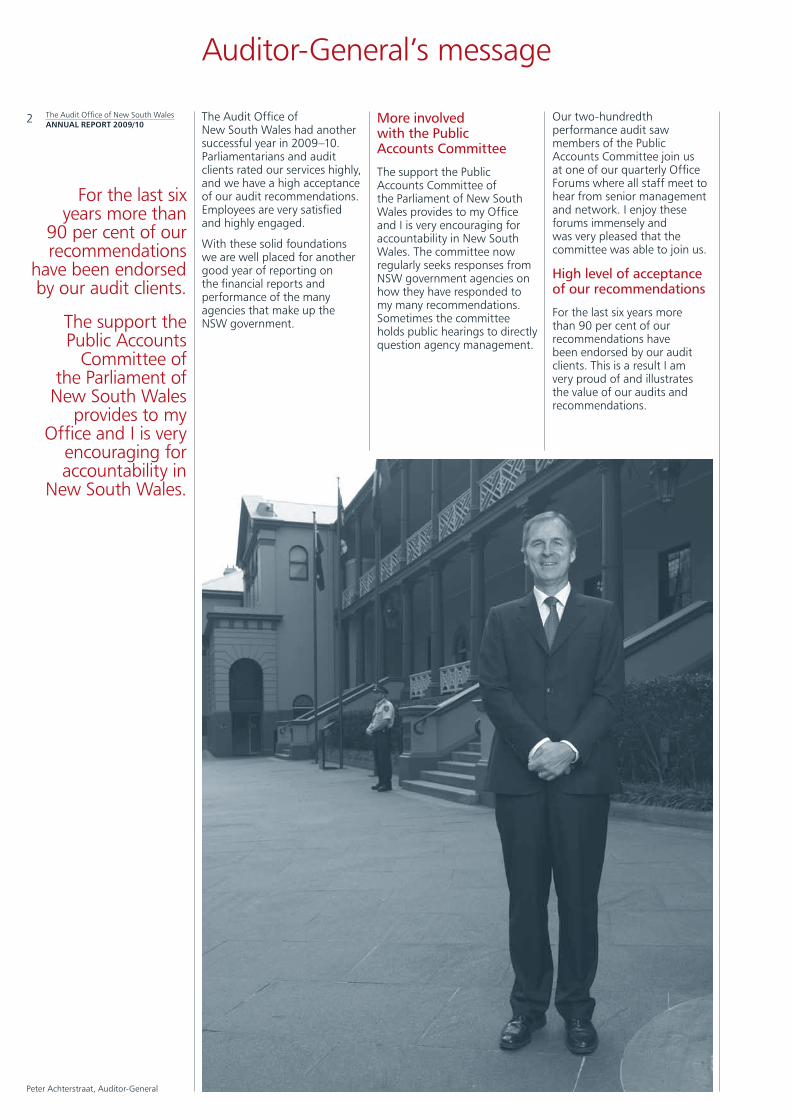

2 The Audit Office of New South Wales had another successful year in 2009–10. Parliamentarians and audit clients rated our services highly, and we have a high acceptance of our audit recommendations. Employees are very satisfied and highly engaged.

With these solid foundations we are well placed for another good year of reporting on the financial reports and performance of the many agencies that make up the NSW government.

More involved with the Public Accounts Committee

The support the Public Accounts Committee of the Parliament of New South Wales provides to my Office and I is very encouraging for accountability in New South Wales. The committee now regularly seeks responses from NSW government agencies on how they have responded to my many recommendations. Sometimes the committee holds public hearings to directly question agency management.

Our two-hundredth performance audit saw members of the Public Accounts Committee join us at one of our quarterly Office Forums where all staff meet to hear from senior management and network. I enjoy these forums immensely and was very pleased that the committee was able to join us.

High level of acceptance of our recommendations

For the last six years more than 90 per cent of our recommendations have been endorsed by our audit clients. This is a result I am very proud of and illustrates the value of our audits and recommendations.

For the last six years more than

90 per cent of our recommendations

have been endorsed by our audit clients.

The support the Public Accounts

Committee of the Parliament of New South Wales

provides to my Office and I is very

encouraging for accountability in

New South Wales.

Auditor-General’s message

Peter Achterstraat, Auditor-General

I am very pleased that senior management now have a collective understanding of what we need to focus on, what we are trying to achieve and how we will get there.

I feel fortunate to have the role I have and would like to sincerely thank all the people that make up the Office for the work they do.

New look financial audit reports

A pleasing achievement for the year was the publication of 12 volumes of my financial audit reports to the Parliament of New South Wales that are each based on the broad services of government. For the first time, we issued separate reports on the agencies that collectively provide public services such as education, health, transport and law and order.

These service-based reports on the outcomes of my financial audits provide a more complete picture of NSW government agencies’ financial reporting.

Clients rate us highly

The clients we audit continued to be satisfied with our work. A notable achievement for the year was the improved satisfaction from our performance audit clients.

Last year some of our performance audit clients had concerns about our value, audit process and reporting. This year a lot of effort went into improving these perceptions with our clients now giving us our best ever value rating of 71 per cent and returning to the previously high satisfaction levels for our audit processes and reporting.

Our people are very satisfied and highly engaged

Our people continue to be highly motivated with engagement levels of over 80 per cent. A very pleasing part of our culture is that more than 90 per cent of staff are willing to go that ‘extra mile’ to help co-workers and clients. This is a very encouraging sign for an organisation that depends so much on team work and client satisfaction.

An improved strategic planning process

This year saw the start of a new strategic planning process — one that involves more of our senior staff and has a strong focus on accountability and developing the leadership potential of our current and future leaders.

The leadership team now meets every month. At these meetings we assess our progress against our key focus areas and if necessary modify what we will do in the next three months, keeping in mind our long term vision of making the people of New South Wales proud of the work we do.

I am very pleased that senior management now have a collective understanding of what we need to focus on, what we are trying to achieve and how we will get there.

Thank you to all staff

I feel very fortunate to have the role I have and would like to sincerely thank all the people that make up the Office for the work they do. Without their commitment, dedication and professionalism our achievements would not be possible.

Peter Achterstraat Auditor-General

The Audit Office of New South Wales AnnuAl RePORt 2009/10

3

The Audit Office of New South Wales AnnuAl RePORt 2009/10

4

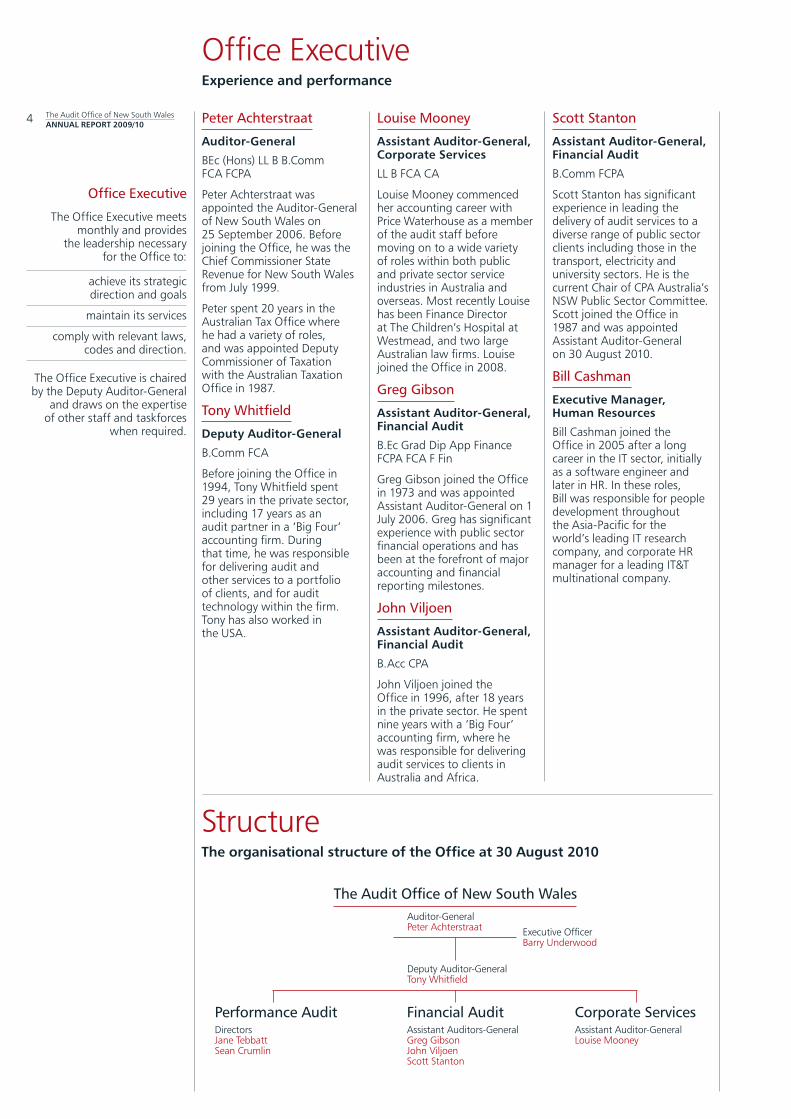

Office Executive

The Office Executive meets monthly and provides

the leadership necessary for the Office to:

achieve its strategic direction and goals

maintain its services

comply with relevant laws, codes and direction.

The Office Executive is chaired by the Deputy Auditor-General

and draws on the expertise of other staff and taskforces

when required.

Office Executiveexperience and performance

Peter Achterstraat

Auditor-General

BEc (Hons) LL B B.Comm FCA FCPA

Peter Achterstraat was appointed the Auditor-General of New South Wales on 25 September 2006. Before joining the Office, he was the Chief Commissioner State Revenue for New South Wales from July 1999.

Peter spent 20 years in the Australian Tax Office where he had a variety of roles, and was appointed Deputy Commissioner of Taxation with the Australian Taxation Office in 1987.

Tony Whitfield

Deputy Auditor-General

B.Comm FCA

Before joining the Office in 1994, Tony Whitfield spent 29 years in the private sector, including 17 years as an audit partner in a ‘Big Four’ accounting firm. During that time, he was responsible for delivering audit and other services to a portfolio of clients, and for audit technology within the firm. Tony has also worked in the USA.

Louise Mooney

Assistant Auditor-General, Corporate Services

LL B FCA CA

Louise Mooney commenced her accounting career with Price Waterhouse as a member of the audit staff before moving on to a wide variety of roles within both public and private sector service industries in Australia and overseas. Most recently Louise has been Finance Director at The Children’s Hospital at Westmead, and two large Australian law firms. Louise joined the Office in 2008.

Greg Gibson

Assistant Auditor-General, Financial Audit

B.Ec Grad Dip App Finance FCPA FCA F Fin

Greg Gibson joined the Office in 1973 and was appointed Assistant Auditor-General on 1 July 2006. Greg has significant experience with public sector financial operations and has been at the forefront of major accounting and financial reporting milestones.

John Viljoen

Assistant Auditor-General, Financial Audit

B.Acc CPA

John Viljoen joined the Office in 1996, after 18 years in the private sector. He spent nine years with a ‘Big Four’ accounting firm, where he was responsible for delivering audit services to clients in Australia and Africa.

Scott Stanton

Assistant Auditor-General, Financial Audit

B.Comm FCPA

Scott Stanton has significant experience in leading the delivery of audit services to a diverse range of public sector clients including those in the transport, electricity and university sectors. He is the current Chair of CPA Australia’s NSW Public Sector Committee. Scott joined the Office in 1987 and was appointed Assistant Auditor-General on 30 August 2010.

Bill Cashman

executive Manager, Human Resources

Bill Cashman joined the Office in 2005 after a long career in the IT sector, initially as a software engineer and later in HR. In these roles, Bill was responsible for people development throughout the Asia-Pacific for the world’s leading IT research company, and corporate HR manager for a leading IT&T multinational company.

Structurethe organisational structure of the Office at 30 August 2010

Performance AuditDirectorsJane TebbattSean Crumlin

Financial AuditAssistant Auditors-General Greg GibsonJohn ViljoenScott Stanton

Corporate ServicesAssistant Auditor-General Louise Mooney

Auditor-General Peter Achterstraat

Deputy Auditor-GeneralTony Whitfield

The Audit Office of New South Wales

Executive Officer Barry Underwood

L–R Tony Whitfield, Louise Mooney, Bill Cashman, Greg Gibson,

Peter Achterstraat, Scott Stanton, John Viljoen

The Audit Office of New South Wales AnnuAl RePORt 2009/10

6 Strategic planning process

Our strategic planning process was expanded in 2009–10 to include a much wider representation of Office staff. This expansion has resulted in the creation of a Leadership Team which includes financial audit and performance audit Business Team Leaders, as well as senior Corporate Services managers. The Leadership Team meets with the Office Executive every 30 days to set and report on tasks, develop and review strategic milestones, and monitor and review the outcomes we expect to achieve at the end of the annual strategic planning cycle.

Strategic focus areas

Outlined below are the outcomes we are expecting to achieve within each of our strategic focus areas by the end of 2010–11. Some of the activities we plan to undertake to achieve these outcomes are detailed throughout this report and referenced below.

Double-Glazing the Glasshouse

Outcomes:

We are recognised as a centre of excellence for governance

Our KPIs are recognised as relevant, understood and actioned

We action relevant recommendations we receive from the Public Accounts Committee, internal audit and other external reviews

Issues reported to clients do not exist in the Office.

Activity includes:

Forming a group of dedicated risk management champions

Performing a gap analysis on our current governance policies and practices

Developing a reporting system that ensures no issues reported to our clients exist in the Office.

See page 35 for further details

Putting the Business into Business teams

Outcomes:

Our teams operate as a business

We have the right systems in place to operate our business

Our people can access the information they need to do their job.

Activity includes:

Creating a robust business indicators measurement framework to give managers clear, real-time views of goals and productivity.

See page 31 for further details

People Power

Outcomes:

Our people are ready to step forward

We recognise our people for excellence

Our people are satisfied and rewarded for the contributions they make

Underperformance is actively addressed

We have the right number of people with the right skills in the right jobs at the right time.

Activity includes:

Delivering a comprehensive and continuous workforce plan to ensure the Office has the right people with the right skills at the right time

Consolidating the work that has been done to define leadership behaviours and modelling at all levels.

See page 31 for further details

Delivering Value

Outcomes:

Agencies and parliament value our services

Our reports and recommendations add value.

Activity includes:

A complete redesign of our Auditor-General’s Reports to Parliament

A complete redesign of our financial audit management letters

The expansion of performance audit’s ‘3x3’ methodology into financial audit, ensuring each report has at least three clear issues and three clear recommendations.

See pages 9 and 17 for further details

Influencing for Impact

Outcomes:

Our work informs and influences

We are a key player in the auditing profession

Our brand is recognised for professional excellence.

Activity includes:

The development of a new corporate website with better presented online reports

Increased representation on key professional accounting bodies

Using Hansard to track how much impact our reports have on parliament in terms of discussion or debate on the key issues and recommendations in our tabled reports.

See pages 9, 17 and 41 for further details

The year aheadAchieving our strategic objectives

Right hand page: Peter Achterstraat, Auditor-General and Tom Muller

ParliamentRegularly seek and

use our adviceThe Auditor-General and the

Audit Office of New South Wales assess the performance

and accountability of NSW government agencies by:

reporting to the Parliament of New South Wales on our audits

working closely with parliamentary committees

The Audit Office of New South Wales AnnuAl RePORt 2009/10

8 Satisfaction remains high

Parliament is our primary client, so it is vital that we understand parliamentarians’ views of our performance. We gather their views in an annual survey, except in election years such as 2007. The 2010 survey was conducted in June and July and 48 of the 135 parliamentarians responded.

The results provide feedback on how parliamentarians view the Audit Office of New South Wales. We are proud that our Office continues to perform strongly in its drive to meet the expectations of parliamentarians.

In 2010, we continued to meet our satisfaction target for our reports and services of 90 per cent, a target that we have met for the past four years. Parliamentarians were positive about:

— our responsiveness to their requests, with 91 per cent rating it as good or higher, similar to 93 per cent in 2009

— our integrity in conducting our audits, with 93 per cent in agreement, up from 89 per cent in 2009

— our assurance to parliament, with 95 per cent in agreement, up from 93 per cent in 2009.

The results also highlighted some areas for improvement. We had a slight decline in parliamentarians agreeing that our reports communicate issues clearly at 87 per cent, down from 90 per cent in 2009. We also noted a slight decrease in the perception that our reports and services are of a high quality at 84 per cent, down from 86 per cent in 2009. In response to this we have redesigned the structure and appearance of our reports to ensure they more clearly highlight our recommendations.

Financial audit reports rate well

Parliamentarians rated the Auditor-General’s financial audit reports very well. The majority of parliamentarians who had referred to our reports in the previous 12 months felt they:

— clearly identified significant issues and their implications, the 88 per cent agreement up from 83 per cent in 2009

— were easy to understand, 91 per cent agreeing, matching the 91 per cent in 2009 and above our target of 90 per cent

— had effective layout and design, the agreement remaining high at 90 per cent, but down from 97 per cent in 2009.

Parliamentarians referring to our financial audit reports for information trended up, with 45 per cent stating they often referred to the reports compared to 41 per cent in 2009. Parliamentarians felt our financial audit reports could be improved by making them more effective in helping parliament monitor the financial performance of the NSW public sector.

SatisfactionParliamentarians very satisfied with reports and services

Satisfaction with financial audit reportsSurveys not conducted in 2007.

2006

2008

2009

8792

83

2010

90

2011

tar

get

9193 93 91 90

2006

2008

2009

2010

2011

tar

get

Identify issues and implications Easy to understand

88

Identify issues and implications

8793 91

979089

9490

Satisfaction with performance audit reports Surveys not conducted in 2007.

2006

2008

2009

2010

2011

tar

get

2006

2008

2009

2010

2011

tar

get

Easy to understand

9397

95% agree that our financial audits

provide valuable assurance

90% believe our financial reports

have effective layout and design

93% believe our performance audit

reports identify significant issues

Performance audit reports rate highly

Parliamentarians rated the Auditor-General’s performance audit reports highly. Parliamentarians who had referred to a performance audit report in the previous 12 months thought the reports:

— were easy to understand, the 97 per cent agreement matching the 97 per cent in 2009

— clearly identified significant issues and their implications, the 93 per cent agreement marginally down from the 94 per cent in 2009, but still above our target of 90 per cent

— had effective layout and design, with 97 per cent agreeing, matching the 97 per cent in 2009.

Although our performance audit reports rate well, fewer than half the respondent parliamentarians accessed them regularly. Forty-one per cent had often accessed information from our performance audit reports during the previous 12 months, matching the 41 per cent in 2009. However, 20 per cent reported rarely or never using our reports, down slightly from 21 per cent in 2009.

Satisfaction with our reports down slightly compared with other state audit offices

The Auditor-General has regularly suggested that government agencies should assess their performance by comparing results with similar organisations in other states. In 2005, we began comparing how satisfied our parliamentarians were with our reports and services against results from other state audit offices. In 2010, the Victorian, Western Australian and Tasmanian audit offices conducted similar surveys.

On an overall measure of satisfaction with reports and services, 90 per cent of our parliamentarians were satisfied, slightly below the 92 per cent average for Victoria, Western Australia and Tasmania.

A lower satisfaction rating is further reflected in 91 per cent of parliamentarians agreeing our services provide valuable information on public sector performance. This is lower than the 96 per cent average of other states. Our parliamentarians also rated us comparably lower on the clarity of how we report our issues, 87 per cent compared with the Victorian, Western Australian and Tasmanian state averages of 90 per cent.

The Audit Office of New South Wales AnnuAl RePORt 2009/10

9

The year ahead

Our Strategic Plan has a number of initiatives aimed at improving the value and impact of our audits and reports within the ‘Delivering Value’ and ‘Influencing for Impact’ focus areas (see page six for more details on our strategic focus areas).

These initiatives include:

a complete redesign of our Auditor-General’s Reports to Parliament, both financial and performance audit, with a clearer presentation of our findings and greater focus on key issues

the expansion of performance audit’s ‘3x3’ methodology into financial audit, ensuring each report has at least three clear issues and three clear recommendations which will make it easier for parliamentarians to see ‘at a glance’ what the big issues in a particular portfolio may be

the development of a new corporate website with better presented online reports allowing parliamentarians to access electronic versions of reports quickly and in a more reader-friendly format

using Hansard to track how much impact our reports have on parliament in terms of discussion or debate on the key issues and recommendations in our tabled reports

reviewing the way we select the topics and issues we audit to ensure they appeal to parliamentarians and the ‘person in the street’.

Satisfaction compared with other participating state audit offices

Audit Office of NSW Other state audit offices

Satisfaction with reports and services

Provide information on public sector performance

Help improve public sector administration

Reports communicate clearly

91

83

87

90

92

96

90

90

The Audit Office of New South Wales AnnuAl RePORt 2009/10

10 Providing an independent opinion

The core task of the Audit Office of New South Wales is to issue opinions on whether NSW government agencies’ financial reports are fairly presented and accord with accounting standards and legislative requirements. These financial reports show the agencies’ financial position and financial performance for the year.

We issue a ‘qualified’ audit opinion if we believe a financial report contains material errors or does not comply with accounting standards, relevant laws and government directions. An ‘unqualified’ opinion provides reasonable assurance that an agency’s financial report is materially correct.

We report opportunities for improving financial management methods and processes. Our work includes consideration of waste, probity, financial judgment and agency performance.

We completed 495 financial audits of NSW government agencies this financial year— see Appendix Two for a full list of our financial report audit clients.

We report to parliamentarians on the outcomes of these audits so they are better informed when considering the state’s financial performance and position, and when deciding on how best to allocate public resources.

Qualified audit opinions

During the year, we issued qualified audit opinions on the financial reports of five per cent (23 of the 495) of NSW government agencies, an increase of one per cent on last year.

Qualified audit opinions mean these agencies’ financial reports did not fully comply with accounting standards, contained material errors or there were limitations on the scope of our audits. Many of these were for agencies that have collections from fundraising activities and due to their nature are unable to have sufficient controls over these activities prior to the receipt of funds.

Repeat qualifications

During 2009–10, there were 18 repeat qualifications, which is three more than in 2008–09. We will continue to notify parliament of these qualifications and encourage the agencies concerned to act on our recommendations.

New qualifications

We issued five new qualifications in 2009–10, compared with seven in 2008–09. For details of these qualifications see pages 20 and 21.

Costs compare well with other states

We compare our financial audit costs with other Australian audit offices.

At $60,500, our average cost of a financial audit compares very favourably with the $68,000 average for all Australian audit offices. As the Audit Office of New South Wales is larger than its interstate counterparts, the economies of scale allow us to achieve lower costs. However, because we audit larger organisations, we would expect our costs per audit opinion to be higher.

Our lower than average cost is most pleasing, and is the result of our ongoing drive to improve our processes.

495 financial audits completed

Average cost per financial audit lower than other

audit offices

AssuranceOur financial audits provide assurance to parliament

448

513495 496

Number of audited entities

2006

2007

2008

2009

2010

495

5

16

9

34

2006

2007

2008

2009

2010

Qualified audit opinions %

The Audit Office of New South Wales AnnuAl RepoRt 2009/10

11Timeliness of reporting to parliament

We report the results of our financial audits to parliament. To better assist parliament, in 2009–10 we aligned our reports with the new super department structure implemented by the government in July 2009. We now report to parliament in 12 volumes compared to six volumes in 2008–09. Most of the 12 volumes published in 2009–10 had a specific industry focus as follows:

Volume 1 No industry focus

Volume 2 Universities

Volume 3 Electricity

Volume 4 Total State Sector

Volume 5 Treasury

Volume 6 Human Services and Technology

Volume 7 Environment, Climate Change and Water

Volume 8 Emergency Services and Law and Order

Volume 9 Education and Communities

Volume 10 Transport, Planning and Industry

Volume 11 Health

Volume 12 No industry focus

Our reports included results for each agency audited. Of those agencies, 86 per cent were reported within 19 weeks of receiving their financial reports (our internal benchmark), slightly below our 90 per cent target and similar to the 87 per cent achieved in 2008–09.

We believe that timely reporting of our audit findings is important as it allows parliament to promptly scrutinise agencies’ financial reports.

For clients with a 30 June balance date (the majority of our clients) we aim to report to parliament before the end of the calendar year. Our other financial audits (mainly universities) have a December year-end and we aim to report on these by May each year.

Other assurance engagements

We assess how well agencies comply with legal requirements, government policies and central agency directives. In undertaking these assessments we comply with the requirements of the Standard on Assurance Engagements, ASAE 3100 Compliance Engagements issued in September 2008.

In 2009–10 we reported the results of our first compliance engagement under the standard, a review of compliance with the government’s ‘Total Asset Management’ policy. The results were reported to parliament in Volume 12 of the Auditor-General’s report for 2009. Of 12 major agencies reviewed, none fully complied with the government’s requirements.

We anticipate recommendations from our compliance assurance programs will provide solutions to issues that may be applied across the NSW public sector.

The year ahead

In 2010–11 we will:

continue improving the content of our reports to parliament by providing more analysis of issues at the agency and industry levels

focus on improving the timeliness of our reporting to agencies through our audit opinions on financial statements and management letters

continue to work with agencies when auditing their financial reports to clear up as many financial report qualifications as possible

collaborate with individual and central agencies to resolve financial reporting and governance issues arising from the implementation of the new super department structure

continue refinement of our Special Interest Groups to ensure they are focused on the important issues facing agencies, their industries and the government

evaluate available audit methodologies and compare them with our current methodology to ensure we have the most suitable approach for our public sector audits.

2005 2006 2007 2008 2009

Cost per financial audit opinion $’000Data for 2010 is not yet available.

5053 51

60

51

5761

67

Audit Office of NSW All Australian audit offices

61

6889

95

8487

90

2006

2007

2008

2009

2010

2011

tar

get

Reports to parliament within 19 weeks %

86

Audit_text_2010_ART+varnish_v2.indd 11 29/10/10 9:03 AM

The Audit Office of New South Wales AnnuAl RePORt 2009/10

12 Helping to improve public administration

Our performance audits review the effectiveness, efficiency and economy of government agencies. A performance audit may assess the whole of an agency’s operations, one agency’s activity, or an activity that involves more than one agency.

If an issue affects a number of agencies, we may issue a better practice guide to help them, and other agencies, improve.

We published 14 performance audit reports during the year, seven more than last year. Detailed information on our reports, findings, recommendations and agency responses is on pages 22 to 28.

We aim to release 10 performance audit reports in 2010–11.

The cost of performance audits

Each performance audit cost an average of $198,429 in 2009–10, which was lower than the $390,000 of last year, and lower than our target of $290,000.

We have initiated new practices in audit planning and design to produce more reports. This has allowed us to improve our productivity compared to last year. We are confident that the average cost of performance audits in 2010–11 will meet our target of $200,000.

Another indicator of our productivity is the number of performance audit reports per staff member. This year we produced 0.73 performance audits per staff member which was more than our target of 0.60 and a significant increase on the 0.35 reports per staff member achieved in 2008–09.

Some of the improvements in productivity can be attributed to a change in audit focus to ensure our audits better meet the needs of parliamentarians and the public. We have achieved this improvement and continued to assist the Public Accounts Committee in its follow-ups of previously tabled audits. Detailed information on our work with the Public Accounts Committee is on page 14.

This is an essential part of making sure that our audits make a difference.

Reporting agency performance information

During 2009–10, our financial audit reports to parliament included comments on agencies’ key performance indicators and focused on:

— Universities — Electricity — Total State Sector — Treasury and Public

Financing Enterprises — Human Services

and Technology — Environment, Climate

Change and Water — Law and Order and

Emergency Services — Transport, Planning

and Industry — Education — Communities and Health.

The reports included recommendations for financial and operational improvements focusing on large agencies across these sectors.

Most agencies exist to provide services efficiently to the people of New South Wales, and whilst much information relating to financial performance is reflected in the financial statements of the agencies we audit, we believe that publishing additional key performance information offers parliament a balanced ‘report card’ on agencies’ performance. We also believe this information helps citizens assess whether their tax dollars have been spent efficiently and effectively.

14 performance audits completed,

7 more than last year

Effectiveness, efficiency and economyOur performance and financial audits help improve agency performance

11

15 15

7

14

2006

2007

2008

2009

2010

2011

tar

get

Number of performance audits completed

10

265

200

264 262

390

198

2006

2007

2008

2009

2010

2011

tar

get

Average cost of performance audits $’000

0.73

0.35

0.73

0.58 0.60

2006

2007

2008

2009

2010

2011

tar

get

Performance audits per staff member

0.73

13The Audit Office of New South Wales AnnuAl RePORt 2009/10Auditing performance

information

Each year the Audit Office of New South Wales is asked to verify the accuracy of specific performance data published in the NSW Government’s State Plan Annual Report. The work we performed for the year ended 30 June 2009 did not identify any errors or exceptions and we reported our findings in March 2010.

We identified some opportunities for improved reporting of State Plan performance data and reported these to the Department of Premier and Cabinet and to parliament in June 2010.

Allegations of serious and substantial waste

The Audit Office of New South Wales examines allegations of serious and substantial waste of public money under the Protected Disclosures Act 1994. This Act protects public officers who become ‘whistle-blowers’ when they identify maladministration, corruption, or serious and substantial waste.

We assess any allegations of serious and substantial waste in NSW public agencies other than local government. The NSW Ombudsman examines maladministration, and the Independent Commission Against Corruption investigates corruption.

We received and examined 21 allegations in 2009–10. Most did not have sufficient evidence to conclude serious or substantial waste. One was significant enough to warrant a separate performance audit which commenced during the year.

When confidentiality of the complainant is not compromised, we advise management of the relevant agency so it can improve its processes and controls.

The year ahead

We will continue to work closely with parliament through the Public Accounts Committee in choosing the topics and issues we will audit. This should ensure that our audits look at areas of most interest to parliamentarians and the community. We expect that the general topic areas we audit will remain similar to previous years, namely:

transport services

law, order and public safety

health and welfare services

education

water management

governance and public sector management.

2119

15

19

2006

2007

2008

2009

Number of allegations of serious and substantial waste

21

2010

The Audit Office of New South Wales AnnuAl RePORt 2009/10

14

The year ahead

To improve on our already high parliamentarian satisfaction

we will continue to:

support the Public Accounts Committee in its inquiries into

the activities of government and its follow-up of our

report recommendations

meet with the committee on sitting days to brief

parliamentarians on the reports we are presenting

to parliament

provide advice and support to parliamentary committees

for their reviews.

Parliamentary response to our workParliament continues to use our reports

Parliament now regularly questions agencies on our report recommendations

As parliament is our most important client, we always look at how it responds to the reports we publish.

Our work for parliament extends well beyond its reading of our reports. We work actively and closely with parliamentary committees, and they regularly draw on our audits and advice, and follow up and reinforce our work.

Our primary relationship is with the Public Accounts Committee which follows up aspects of the Auditor-General’s reports to parliament. We regularly meet with the committee on sitting days to brief parliamentarians on the reports we are presenting to parliament. At times, we also make submissions to the committee and appear at its inquiries.

In 2007–08 the Public Accounts Committee started to regularly follow up with agencies on what they have done in response to our performance audit report recommendations. These reviews occur about 12 months after the release of a report. We comment on what the agency says it has been doing to address the issues we raised and give evidence at the committee’s follow-up hearings.

In 2009–10 the Public Accounts Committee released three reports on follow-up reviews of the following eight performance audits:

Ageing Workforce—Teachers

Efficiency of the Office of the Director of Public Prosecutions (29/10/09 and 24/6/10)

Working with Hotels and Clubs to Reduce Alcohol-related Crime

Signal Failures on the Metropolitan Rail Network

Recycling and Reuse of Waste by the NSW Public Sector

Improving Literacy and Numeracy in NSW Public Schools

Delivering Health Care out of Hospitals

Managing Injured Police.

Follow-up reviews by the Public Accounts Committee have provided an effective means for parliament to assess agency responses to our reports, to encourage agency performance improvement, and for us to obtain useful feedback on our impact.

The Public Accounts Committee reports to parliament on the outcome of its follow-up examinations of our performance audit reports. In its fifth report to parliament in this series, Mr Paul Gibson MP, Chair of the Public Accounts Committee, stated:

‘I am pleased to table the Public Account Committee’s fifth report under its comprehensive performance audit follow-up review program. Since implementing the program, the committee has seen tangible evidence of its effectiveness, with agencies providing comprehensive information on the action they have taken in the year since the performance audit was tabled, and agreeing to adopt recommendations they had previously rejected in the face of evidence of the recommendations’ efficacy.

In our fourth follow up report, we quoted the Director-General of the Department of Education who had stated, “Since our March correspondence, which informed the committee of our response to the recommendations of the audit, we as a departmental executive met and modified to some extent the bald rejection of a couple of those proposals.” The Director-General then went on to say that the committee’s review process “is a good mechanism for keeping the pressure on us and, frankly, it was part of the reason that we as an executive revisited the March response.”

While we found the Department of Environment, Climate Change and Water and the Department of Education and Training to be very responsive to our inquiries,

the same cannot be said of RailCorp. In the committee’s opinion, RailCorp’s repeated delays in responding to the committee’s requests for information and its inconsistent and confusing answers mean that it has failed to discharge its obligations to parliament in a timely and transparent manner. The Public Accounts Committee was set up to examine the efficiency and effectiveness of government activity on behalf of the people of New South Wales, and it is not for RailCorp to decide that it will undermine the committee’s capacity to fulfil its role.

I would like to thank the Auditor-General and the Audit Office staff, as well as the departmental staff who assisted us with our inquiries.’

Case studyWorking with the Public Accounts Committee

Right hand page: L–R Lauren Sharp, Steven Martin, Harminder Singh

The Audit Office of New South Wales AnnuAl RePORt 2009/10

15

AgenciesAct on our

recommendations and regularly seek advice

We work collaboratively with our financial and

performance audit clients

Together with our financial audit clients we identify opportunities

to improve financial reporting and management

Our performance audits examine agency programs critically and from an independent

perspective in order to identify potential improvements

The Audit Office of New South Wales AnnuAl RePORt 2009/10

16

Over 90% of clients believe we

conduct our audits professionally

Improvements made in providing a value

for money service

SatisfactionOur audits are well regarded

General satisfaction with our services

We survey our audit clients every year to determine how satisfied they are with our work and where we can improve. This year we surveyed 435 financial audit clients and received 327 responses. This response rate of 75 per cent is a significant improvement on the 55 per cent achieved in both 2008 and 2007. The response rate for performance audit clients was 70 per cent, lower than the 83 per cent of 2009, with 14 out of 20 invited agencies participating in the survey.

Financial audit process improved

Our financial audit clients generally assessed us favourably for our audit processes and reporting, and for adding value to their organisation, with overall results steady in comparison to 2009. Although there was a slight drop in overall perceptions of value, this was offset by a slight increase in satisfaction with our audit process.

Performance audits significantly improved overall

Performance audit clients generally assessed us favourably in relation to the quality of audit process, reporting and value in 2010, with overall results significantly higher than those achieved in 2009.

Our value for money increases

Financial audit value for money increases

The number of respondents who think our fees are reasonable remained steady, the 55 per cent result only marginally lower than last year’s 56 per cent. There was a five per cent increase in the number of respondents who thought our financial audit services provide value for money, from 53 per cent in 2009 to 58 per cent in 2010. This builds on a previous five per cent increase on the measure from 2008 to 2009. Although we are pleased with these improvements, work still needs to be done in improving clients’ perceptions of the reasonableness of our fees.

Other measures of value were down on last year, with financial audit clients believing we can improve the sense of assurance our audits provide, and the value of our advice.

Significant increase in performance audit value

Both key measures of performance audit value were up significantly on last year, with the 2010 result the most positive result achieved to date. Seventy-nine per cent of clients believed the audit would help improve their administration of the activity audited, up from 60 per cent in 2009. Clients also value the contribution our audits make in providing them with a sense of assurance, up from 70 per cent in 2009 to 79 per cent in 2010.

Audit process shows improvement

Financial audit process rated positively

Clients believe the continuity of audit staff has improved, up from 68 per cent in 2009 to 77 per cent in 2010. Our understanding of our clients’ organisation has also improved, the 75 per cent result in 2010 up from 69 per cent in 2009. Improvements were made on the timeliness of audits, with 70 per cent agreeing our audits were conducted in a timely manner, up from 66 per cent in 2009, and that we used clients’ staff time efficiently, up from 72 per cent in 2009 to 75 per cent in 2010.

As in 2009, more than 80 per cent agreed they had adequate opportunity to comment on the audit plan, senior audit staff were appropriately involved in the audit, and communication was effective.

Clients believe we can improve the professionalism of our staff in their interactions with clients, as although the 90 per cent result is good, it is down on the 95 per cent achieved in 2009. Further areas for improvement are our responsiveness to our clients’ needs, and keeping them better informed of significant issues and findings during the course of the audit.

Performance audit process improves significantly

Over 90 per cent of respondents agreed that our interaction with staff was professional, communication between auditors and their organisation was effective, and our auditors responded promptly to requests or concerns raised.

Significant improvements were made in auditors clearly explaining the audit approach, up from 89 per cent in 2009 to 100 per cent in 2010, and in clients being given adequate opportunity to comment on audit findings before reports are finalised, up from 80 per cent in 2009 to 93 per cent in 2010. The biggest improvement was an increase in our understanding of client organisations and their operating environments, up sharply from 40 per cent in 2009 to 79 per cent in 2010.

605962

69 7168 69 68 69 70

Satisfaction with audit value Aggregate performance indices.

Financial audit clients

2006

2007

2008

2009

2010

2011

tar

get

Performance audit clients

2007

2008

2009

2010

2006

2011

tar

get

6670

The Audit Office of New South Wales AnnuAl RePORt 2009/10

17

The year ahead

Our Strategic Plan has a number of initiatives aimed at improving the value and impact of our audits and reports within the ‘Delivering Value’ and ‘Influencing for Impact’ focus areas (see page six for more details on our strategic focus areas).

These initiatives include:

A complete redesign of our Auditor-General’s reports to parliament with a clearer presentation of our findings and greater focus on the issues of relevance to our clients

A complete redesign of our financial audit management letters to improve the way we communicate our findings and provide more value to our clients in terms of the information they receive in these letters

The expansion of performance audit’s ‘3x3’ methodology into financial audit, ensuring each report has at least three clear issues and three clear recommendations of real value and benefit to our clients

The development of a new corporate website with better presented online reports allowing our clients to access electronic versions of reports quickly and in a more reader-friendly format.

We are also continually analysing the reasons we don’t meet the expectations of our clients and in 2010–11 we will be focusing on:

improving the timeliness of reporting

improving our interactions with our clients

continuing to improve clients’ perceptions of the reasonableness of our fees.

Areas that require improvement are the quality of our research and analysis, and our understanding of the specific subject matter addressed in our audits.

Our reports are well received

Financial audit reports rate positively

Eighty-five per cent of clients felt our audit findings were reported in a balanced and fair way, a marked increase of eight per cent on 2009. The perceived accuracy of our findings has also improved, up from 83 per cent in 2009 to 88 per cent in 2010.

However, there was an overall decline in satisfaction with our management letters. Our clients were less likely to agree that our management letters were: balanced and fair, down slightly to 76 per cent from 78 per cent; were issued in a timely manner, down from 78 per cent to 71 per cent; and contained ‘no surprises’, down from 75 per cent to 69 per cent.

Practical recommendations for improving performance

Ninety-three per cent of performance audit respondents felt they were given adequate opportunity to comment on performance audit findings before the report was finalised, up significantly on the 80 per cent achieved last year. Respondents also rated positively how clearly our reports communicate audit findings, the 86 per cent result up 16 per cent on last year.

There was a sharp decline in the perceived practicality of our recommendations, down from 90 per cent in 2009 to 69 per cent in 2010, and the presentation of our findings in a balanced and fair manner, down from 80 per cent in 2009 to 57 per cent in 2010.

Other areas that require improvement are ensuring reports contain ‘no surprises’, and that the benefits of our audit recommendations are clear.

Comparing well with other states

We began comparing our client satisfaction with other state audit offices in 2005. Queensland, Victoria, Western Australia and Tasmania conducted surveys in 2010, using the same method.

When compared with these other states, our financial audit clients were more satisfied with the accuracy, and the balance and fairness, of our findings, and equally satisfied with our audit fees, professionalism and the capacity for our recommendations to improve their financial management.

However, we rated below other states for our communication, timeliness, continuity of audit staff, understanding of our clients’ organisations, and our skills and knowledge.

The survey placed our performance audit clients’ satisfaction as higher than the other states in terms of communication between our staff and the organisation, and our professionalism and assurance. We also rated higher than most states in informing our clients of significant issues and our understanding of their organisation and operating environment. However, we rated below other states for senior staff involvement, and presenting our findings in a balanced and fair manner.

71 69

79

68

7571 71 72 71

Satisfaction with audit processAggregate performance indices.

Financial audit clients Performance audit clients

2006

2007

2008

2009

2010

2011

tar

get

2006

2007

2008

2009

2010

2011

tar

get

7275 76

Satisfaction with audit reportingAggregate performance indices.

Financial audit clients

71 7172 72 73 75

2006

2007

2008

2009

2010

2011

tar

get

73 7571

74

82

Performance audit clients

2007

2008

2009

2010

2006

2011

tar

get

74

97% of financial audit and 92% of

performance audit recommendations

accepted

The Audit Office of New South Wales AnnuAl RePORt 2009/10

18

Acceptance of recommendationsHigh acceptance

Continued high acceptance of our financial audit recommendations

A good measure of the effectiveness of our financial audits is an agency’s acceptance of our recommendations. We include most of our recommendations in our reports to client management, and publish the more significant matters in our reports to parliament. Our recommendations are varied and come from our assessment of agencies’ financial reporting and management systems.

Of the 898 recommendations we made to our top 50 clients in 2009–10, 867 (97 per cent) were accepted, up from 94 per cent in 2008–09.

Continued high acceptance of our performance audit recommendations

Similarly, a performance audit client’s acceptance of our recommendations increases the likelihood that we will have a positive impact on agency performance— a good measure of our success.

Of the 14 performance audit reports completed in 2009–10, agencies accepted 98 of our 106 recommendations. At 92 per cent this is slightly down on the 99 per cent result last year. Most significantly, agencies accepted all recommendations in 10 of the 14 completed performance audits.

Recommendations accepted %

2006

2007

2008

2009

2010

2011

tar

get

9494 9297

9993 93

9095

Financial audits

Performance audits

2009

2006

2007

2008

2010

95

2011

tar

get

97

92

Case studyImproving the road safety of school zones

In 2010, we conducted a performance audit into the effectiveness of school zones and found that motorists continue to exceed the 40 km/h school zone speed limit, and that enforcement of school zone speed limits was almost entirely dependent on fixed speed cameras. The one per cent of school zones fitted with fixed speed cameras accounted for 93 per cent of all school zone speeding infringements.

We recommended that the RTA publish how many of the mobile speed cameras promised in 2006 have been acquired for school zone purposes and how often they have been deployed.

The Minister for Roads announced on 27 June that six mobile cameras will start operating from 19 July 2010. From July 2011, a larger program will start operating, ramping up to 12,200 hours per month of mobile speed enforcement.

The year ahead

Improving the timeliness of our reporting allows our clients to act promptly on our findings and recommendations.

We will continue to work on improving the timeliness of our financial audit opinions and management letters.

We will also continue to work on delivering performance audit reports in the most efficient and timely way.

We will closely analyse where we don’t meet the expectations of our financial and performance audit clients, and over the next three years implement initiatives to address these expectations.

The Audit Office of New South Wales AnnuAl RePORt 2009/10

19We are working to improve the timeliness of our reporting to agencies. The earlier we give agencies our audit opinions and management letters, the sooner they can develop any necessary solutions.

In 2008–09, we changed how we measure the timeliness of issuing our financial audit opinions. In prior years, if we had completed our audit by the due date but our opinion was issued late due to delays caused by the agency, we concluded we had achieved our target. Public accountability requires agencies to report in a timely manner and the Office has a role in influencing agencies to improve their timeliness. We therefore now measure the time taken to issue financial audit opinions irrespective of delays caused by agencies. If we improve our performance, the timeliness of agencies’ financial reporting to stakeholders will also improve.

The percentage of opinions issued within 10 weeks was 71 per cent in 2009–10 which was an improvement over last year’s 61 per cent. We have set a target for 2010–11 of 100 per cent due to the importance of this measure.

In 2008–09, we also changed how we measure the timeliness of issuing our management letters to agencies to improve on their timeframes. Our goal now is to have our management letters, including agency comments, issued to agencies within six weeks from the issue of the audit opinion. In 2009–10 we achieved 48 per cent which was less than the 52 per cent achieved in 2008–09 and significantly below our target of 85 per cent.

Management letters include suggestions for improving the systems and processes we review during our audits. We have increased our efforts to ensure the letters are issued earlier by ensuring reporting to large and higher risk agencies follows the completion of both interim and final audit work. Another change in our approach includes increased liaison with agencies to obtain their responses to matters raised in a timelier manner.

Timeframes for performance audits similar to other states

The average time for Australian audit offices to complete a performance audit decreased slightly from 10.4 months in 2007–08 to 10.1 months in 2008–09 (the most recent result available).

We take longer, 11 months in 2007–08 increasing to 12.1 months in 2008–09.

During 2009–10 we put in place a strategy to perform more shorter, sharper performance audits. This strategy includes the selection of suitable topics that lend themselves to that style of audit. It also involves reducing the size of the performance audit reports to no more than 20 pages and costing no more than $200,000 each. We have also looked at the structure of our performance audit reports and standardised them to allow readers to quickly understand the focus of the audit and its outcomes.

Timelinesstimeliness of reporting to agencies

71

61

100

2009

2010

2011

tar

get

Audit opinions within 10 weeks %Calculated for the first time in 2009.

4852

85

2009

2010

2011

tar

get

Management letters within 6 weeks %Calculated for the first time in 2009.

The Audit Office of New South Wales AnnuAl RePORt 2009/10

20

Our financial auditsProviding value to our financial audit clients

What are financial audits?

Financial audits provide independent opinions on NSW government agencies’ financial reports. They identify whether agencies comply with accounting standards and relevant laws, regulations and government directions. Additional financial report audits are undertaken each year on the Total State Sector Accounts and the Statement of the Budget Result. Financial report audits also highlight opportunities for agencies to improve their accounting and financial systems.

A report on each financial audit is provided to the minister responsible for the agency, the agency, the Treasurer, and parliament through the Auditor-General’s reports to parliament.

Our client base

We completed 495 financial audits of NSW government agencies in 2009–10 (see Appendix Two for the full list of our clients). These agencies collected income of approximately $92.2 billion, spent about $77.9 billion and managed more than $337.6 billion in assets. They provide a diverse range of services and vary in size from large government departments, universities, state super-annuation entities and utilities, to small boards and trusts.

Less new qualifications

In 2009–10 we issued five new qualifications, two less than 2008–09.

Agency Reason for qualification

Forestry Commission of New South Wales (Trading as Forests NSW)

We were unable to form an opinion as to whether costs incurred to establish a plantation forest are deductible for tax purposes.

NSW Department of Primary Industries

We were unable to form an opinion as to whether costs incurred to establish a plantation forest are deductible for tax purposes.