Payments system issues in financial markets that never sleep Herbert L. Baer and Douglas D. Evanoff Financial market participants rely heavily on the payments system to control risk arising out of the trading or exchange process. Because of this reli- ance, changes in the nature of financial trans- actions may necessitate changes in the pay- ment systems that support them. The last decade has witnessed a dramatic change in the nature of financial transactions. In particular, today's financial markets are globally intertwined and function on a 24-hour basis. For example, foreign currency trading has been growing at nearly 40 percent annu- ally. The resulting risks associated with the settlement of foreign currency contracts are perceived by many market participants to be significant. Major changes are also occurring in the futures and options markets, which may lead to increased payments activity during nontraditional hours. The Philadelphia Stock Exchange and the Chicago Board of Trade have introduced nighttime trading hours, and the Chicago Mercantile Exchange is promot- ing the introduction of its GLOBEX system, which will allow electronic trading at night. Moreover, the customer base for these instru- ments is significantly more international today than it was five years ago. During this same period, foreign countries have developed com- peting exchanges on which many U.S. custom- ers desire to participate. Finally, the growth of cross-border holdings of securities, and the associated increase in the demand for cross- border security lending, will also create a demand for changes in the payments system. Given the changing financial markets, many market participants and central bankers are concerned that existing payment systems do not provide adequate means for market participants to control the risks emerging from these transactions. In particular, while an increasing number of financial markets operate on a 24-hour basis, national payment systems generally continue to operate for eight hours a day. This makes the control of certain types of risks difficult and costly. This paper describes the types of risks that are encountered in finan- cial transactions, discusses how changes in payment systems can be used to control or eliminate these risks, and provides estimates for the demand for nighttime operation of a dollar-based payment system. The final sec- tion summarizes and offers policy options. Risks and payments systems: An overview Trading financial contracts creates two types of risk. Market risk arises because a party to the contract may incur costs when seeking to replace a defaulted agreement because the market value of the contract has changed. Delivery risk (or principal risk) The authors are assistant vice president and senior economist, respectively, at the Federal Reserve Bank of Chicago. Helpful comments on earlier drafts by John Davidson, George Juncker, John McElravey, John McPartland, Jeffrey Marquardt, Larry Mote, Janet Napoli, Patrick Parkinson, and Don Wilson are acknowledged. The authors also thank the numerous individuals who participated in background interviews. However, the views ex- pressed are those of the authors and may not be shared by others. 2 ECONOMIC PERSPECTIVES

Transcript

Payments system issuesin financial marketsthat never sleep

Herbert L. Baer and

Douglas D. Evanoff

Financial market participantsrely heavily on the paymentssystem to control risk arisingout of the trading or exchangeprocess. Because of this reli-

ance, changes in the nature of financial trans-actions may necessitate changes in the pay-ment systems that support them.

The last decade has witnessed a dramaticchange in the nature of financial transactions.In particular, today's financial markets areglobally intertwined and function on a 24-hourbasis. For example, foreign currency tradinghas been growing at nearly 40 percent annu-ally. The resulting risks associated with thesettlement of foreign currency contracts areperceived by many market participants to besignificant. Major changes are also occurringin the futures and options markets, which maylead to increased payments activity duringnontraditional hours. The Philadelphia StockExchange and the Chicago Board of Tradehave introduced nighttime trading hours, andthe Chicago Mercantile Exchange is promot-ing the introduction of its GLOBEX system,which will allow electronic trading at night.Moreover, the customer base for these instru-ments is significantly more international todaythan it was five years ago. During this sameperiod, foreign countries have developed com-peting exchanges on which many U.S. custom-ers desire to participate. Finally, the growth ofcross-border holdings of securities, and theassociated increase in the demand for cross-border security lending, will also create ademand for changes in the payments system.

Given the changing financial markets,many market participants and central bankersare concerned that existing payment systemsdo not provide adequate means for marketparticipants to control the risks emerging fromthese transactions. In particular, while anincreasing number of financial markets operateon a 24-hour basis, national payment systemsgenerally continue to operate for eight hours aday. This makes the control of certain types ofrisks difficult and costly. This paper describesthe types of risks that are encountered in finan-cial transactions, discusses how changes inpayment systems can be used to control oreliminate these risks, and provides estimatesfor the demand for nighttime operation of adollar-based payment system. The final sec-tion summarizes and offers policy options.

Risks and payments systems:An overview

Trading financial contracts creates twotypes of risk. Market risk arises because aparty to the contract may incur costs whenseeking to replace a defaulted agreementbecause the market value of the contract haschanged. Delivery risk (or principal risk)

The authors are assistant vice president and senioreconomist, respectively, at the Federal ReserveBank of Chicago. Helpful comments on earlierdrafts by John Davidson, George Juncker, JohnMcElravey, John McPartland, Jeffrey Marquardt,Larry Mote, Janet Napoli, Patrick Parkinson, andDon Wilson are acknowledged. The authors alsothank the numerous individuals who participated inbackground interviews. However, the views ex-pressed are those of the authors and may not beshared by others.

2

ECONOMIC PERSPECTIVES

arises because one party may default on acontract after the other has already performedits obligations. By moving cash and collateral,netting payment obligations, and facilitatingsettlement in a delivery vs. payment network,the payments system allows market partici-pants to manage these risks.

While financial instruments are increas-ingly being traded on a continuous basisaround the world, payment systems have re-mained more parochial. The problems causedby this parochialism can best be appreciatedby considering how clearance and settlementof obligations would occur, and risk would bemanaged, in a world in which transaction costswere unimportant. In this world, trades couldbe instantly transmitted to the clearing system.Any credit exposure due to market risk couldbe instantaneously eliminated through postingcash or collateral on a real-time basis. Anydelivery risk could be eliminated through theuse of delivery vs. payment mechanisms. (Pay-ment system risk definitions and means tomanage risk are presented as background ma-terial in the Box).'

It is unlikely that this system will ever beachieved. Participants would incur consider-able transaction costs in the form of wire fees,accounting costs, and forgone interest on cashbalances. However, today's global paymentssystem is further removed from this situationthan many market participants find desirable.For much of the 24-hour day, elimination ofemerging market risk through the transfer ofdollar-denominated currency or collateral iseither awkward or impossible. Proceduresto counteract the resulting risk on transfer net-works have frequently not been adopted.Delivery risk is also substantial in many mar-kets, and the development of formal nettingagreements and effective delivery vs. paymentmechanisms to counteract this has notoccurred.

Below we detail potential payments prob-lems that are emerging as a result of the rapidgrowth of cross-border trading of securities,interbank trading of foreign exchange obliga-tions, cross-border and nighttime trading ofderivative products such as futures and op-tions, and offshore clearing of dollar pay-ments. As these problems are analyzed, wealso attempt to reflect the likely impact ofanticipated market changes such as adjust-ments to procedures on CHIPS (Clearing

House Interbank Payments System), the intro-duction of delivery vs. payment arrangements,and the introduction of multilateral netting offoreign currency contracts?

International securities trading

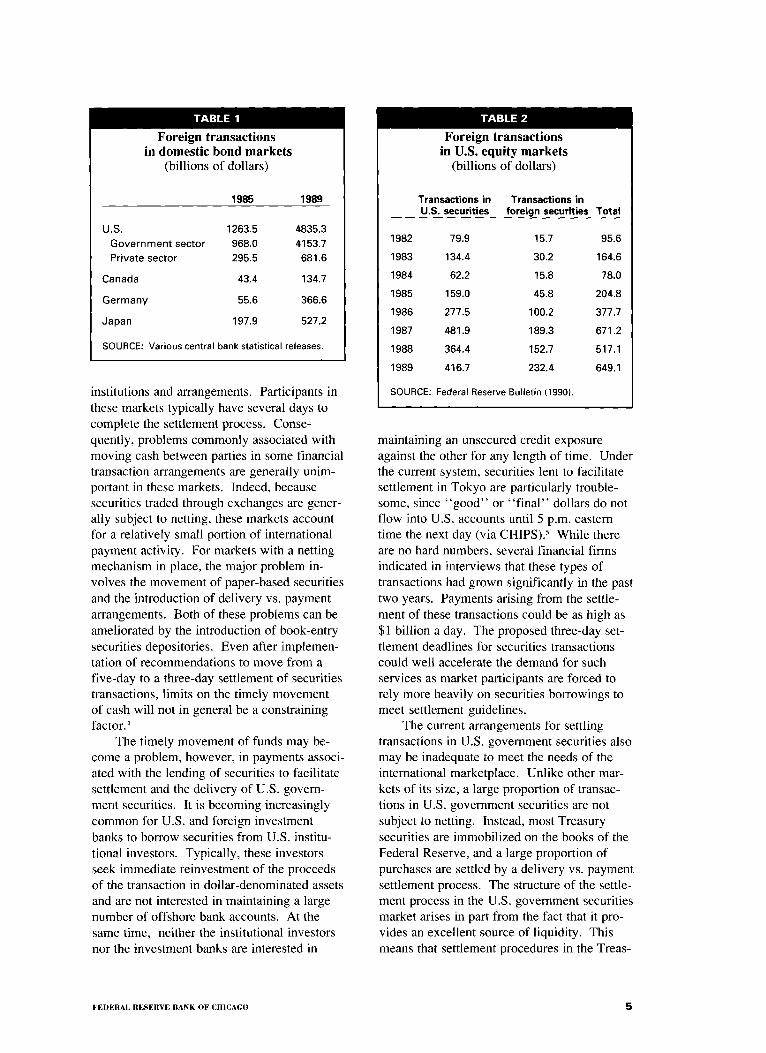

Cross-border secondary market trading ofU.S. government securities has grownrapidly—in recent years the average annualgrowth rate has been 22 percent (Pavel andMcElravey 1990)—and is now conducted on a24-hour basis.' In 1988, trading by nonresi-dents in these securities reached $3 trillion, orroughly $12 billion per day. Nighttime tradingof Treasury securities is also becoming moreimportant. While there are no good estimatesof the volume of off-hours trading of Treasurysecurities, an analysis of futures trading datasuggests that 15 percent of trades take placeduring these hours. This would suggest a dailynighttime volume of U.S. government securi-ties trading of approximately $53 billion. Thisgrowth has led to the development of off-hourstrading of Treasury bond futures contracts atthe Chicago Board of Trade (CBOT), theTokyo Stock Exchange, and the London Inter-national Financial Futures Exchange (LIFFE).In response to this growth in 24-hour tradingof U.S. government securities, the Public Se-curities Association has recently announced aplan to disseminate pricing data on a 24-hourbasis. Although the current volume of tradingin private securities is much smaller, that mar-ket has registered more dramatic growth rates.Foreign transactions in private sector U.S.bonds currently approach $640 billion peryear, and trading volumes have increased atan average annual rate of approximately 80percent.

Similar trends have been observed in othercountries (see Table 1). In Germany, for ex-ample, bond transactions have increased at a43 percent annual rate over the 1985-89 periodand accounted for over one-third of the valueof all transactions in German bond markets.Foreign investment in equity markets has alsoincreased dramatically. For instance, foreigntransactions in U.S. markets grew at nearly 30percent annually to $650 billion in 1989 (seeTable 2).

To a significant extent, the growth incross-border trading is likely to create rela-tively few demands on the global paymentssystem that cannot be handled by existing

FEDERAL RESERVE BANK OF CHICAGO

Payments system risk and means to manage it

The increase in the number and dollar vol-ume of international financial transactions isgiving financial market and payment systemparticipants the incentive to reduce both the costsand risks involved in these transactions. Tounderstand the deficiencies in existing paymentsystems, as well as the implications of proposedchanges, it is necessary to have an understandingof the nature of the risks involved and means toaddress them. We briefly discuss these aspectsof payment and clearing arrangements, and in theprocess introduce the terminology used through-out the article.

The major risks involved with financialtransactions are liquidity, credit, and systemicrisk. Liquidity risk results from the possibilitythat payments will not be made when due, butwill be forthcoming at a later date. Credit riskresults from the possibility that full payment maynot be possible at any date. Credit risk can beseparated into two components. If a counterpartydefaults on the obligation before it is due, thecontract may only be replaceable at a higher cost.This is market risk. It is a function not of thegross value of the contract, but of the differencebetween the original cost of the defaulted contractand the current cost of obtaining the same con-tract. Parties to transactions are also subject todelivery risk, the risk that one party will fulfill hissettlement obligations while the counterpartydoes not. Unlike market risk, delivery risk ap-plies to the gross value of the obligation. It is amajor problem in cross-border or multicurrencytransactions.

Systemic risk occurs when a large number ofparties find it so difficult to value the direct andindirect credit risks associated with the clearingand settlement of transactions that they simplyabandon the market. In the market for bankdeposits this is manifested in a run from depositsinto currency. In a securities or derivative prod-ucts market it is manifested in a cessation oftrading through conventional channels. Althoughregulators are concerned with risk in general, it issystemic risk that concerns them most and thatdrives most policy decisions.

Market participants have developed certainpractices to control payment system risks and

costs. For example, in certain markets, such asforeign exchange, participants have a large num-ber of contracts with one another that may beoffsetting over the course of the trading day. Toreduce transaction and accounting costs on thedelivery day, the parties may use a position net-ting procedure in which the net position of partiesis summarized. One payment covering the netposition therefore replaces all the individualtransactions. Position netting can be either bilat-eral (between any two parties) or multilateral (asingle net position between all market partici-pants). However, position netting does not re-duce risk. Risk can be reduced when netting pro-cedures are employed by introducing novation.With this legal device, each trade creates a newcontract or obligation for the resulting net posi-tion and previous contracts are discharged. Thus,participants are contractually obligated to a run-ning position. To further reduce risk and poten-tial counterparty squabbles, market participantscan have the entity that serves as the centralaccountant in the multilateral netting arrangement(frequently a clearinghouse) substitute as acounterparty for all trades. Thus, with multilat-eral netting with novation and substitution, mar-ket participants trade with indistinguishablecounterparties, are legally obligated to the substi-tute for the net position owed as a result of tradeswith all participants, and delegate risk manage-ment to the substitute.

The lag between initiation and final settle-ment of the transaction, especially troublesome incross-border transactions, can increase liquidity,market, and delivery risk. This can be eliminatedby introducing delivery vs. payment structures inwhich both sides of the transactions occur simul-taneously. This would be particularly useful inthe cross-border trading of securities where de-positories can be created that house the securitiesand act in conjunction with the payments systemto transfer payment and ownership simultane-ously. Other commonly used payments systemrisk-management tools include frequent scrutinyof the financial viability of clearinghouse partici-pants, limits or caps on intraday exposure toindividual counterparties or groups of counterpar-ties, and collateralization of debit positions.

4 ECONOMIC PERSPECTIVES

TABLE 1

Foreign transactionsin domestic bond markets

(billions of dollars)

1985 1989

U.S. 1263.5 4835.3

Government sector 968.0 4153.7

Private sector 295.5 681.6

Canada 43.4 134.7

Germany 55.6 366.6

Japan 197.9 527.2

SOURCE: Various central bank statistical releases.

TABLE 2

Foreign transactionsin U.S. equity markets

(billions of dollars)

Transactions inU.S. securities

Transactions inforeign securities Total

1982 79.9 15.7 95.6

1983 134.4 30.2 164.6

1984 62.2 15.8 78.0

1985 159.0 45.8 204.8

1986 277.5 100.2 377.7

1987 481.9 189.3 671.2

1988 364.4 152.7 517.1

1989 416.7 232.4 649.1

SOURCE: Federal Reserve Bulletin (19901.institutions and arrangements. Participants inthese markets typically have several days tocomplete the settlement process. Conse-quently, problems commonly associated withmoving cash between parties in some financialtransaction arrangements are generally unim-portant in these markets. Indeed, becausesecurities traded through exchanges are gener-ally subject to netting, these markets accountfor a relatively small portion of internationalpayment activity. For markets with a nettingmechanism in place, the major problem in-volves the movement of paper-based securitiesand the introduction of delivery vs. paymentarrangements. Both of these problems can beameliorated by the introduction of book-entrysecurities depositories. Even after implemen-tation of recommendations to move from afive-day to a three-day settlement of securitiestransactions, limits on the timely movementof cash will not in general be a constrainingfactor. 4

The timely movement of funds may be-come a problem, however, in payments associ-ated with the lending of securities to facilitatesettlement and the delivery of U.S. govern-ment securities. It is becoming increasinglycommon for U.S. and foreign investmentbanks to borrow securities from U.S. institu-tional investors. Typically, these investorsseek immediate reinvestment of the proceedsof the transaction in dollar-denominated assetsand are not interested in maintaining a largenumber of offshore bank accounts. At thesame time, neither the institutional investorsnor the investment banks are interested in

maintaining an unsecured credit exposureagainst the other for any length of time. Underthe current system, securities lent to facilitatesettlement in Tokyo are particularly trouble-some, since "good" or "final" dollars do notflow into U.S. accounts until 5 p.m. easterntime the next day (via CHIPS).' While thereare no hard numbers, several financial firmsindicated in interviews that these types oftransactions had grown significantly in the pasttwo years. Payments arising from the settle-ment of these transactions could be as high as$1 billion a day. The proposed three-day set-tlement deadlines for securities transactionscould well accelerate the demand for suchservices as market participants are forced torely more heavily on securities borrowings tomeet settlement guidelines.

The current arrangements for settlingtransactions in U.S. government securities alsomay be inadequate to meet the needs of theinternational marketplace. Unlike other mar-kets of its size, a large proportion of transac-tions in U.S. government securities are notsubject to netting. Instead, most Treasurysecurities are immobilized on the books of theFederal Reserve, and a large proportion ofpurchases are settled by a delivery vs. paymentsettlement process. The structure of the settle-ment process in the U.S. government securitiesmarket arises in part from the fact that it pro-vides an excellent source of liquidity. Thismeans that settlement procedures in the Treas-

FEDERAL RESERVE BANK OF CHICAGO 5

ury market are more focused on providingrapid availability than on minimizing transac-tion costs through netting. Because Treasurysecurities are used as short-term investmentvehicles, the growing importance of trading inTreasuries at night may also be an indicationof a growing demand for liquidity outside oftraditional trading hours. Without the opera-tion of a nighttime book-entry system, themarketplace's ability to provide this liquiditymay be limited.

Interbank foreign exchange markets

Based on the volume of transactions,foreign exchange trading is the largest singleinternational financial activity. The Bank forInternational Settlements estimated that the1989 daily turnover in the foreign exchangemarket was about $650 billion. It has beengrowing at approximately 40 percent annuallyduring the 1980s (Pavel and McElravey 1990).

Foreign exchange products—such as spot,forward, option, and swap instruments—specify a settlement or "value date" in thefuture on which the exchange of currencieswill be completed. Spot contracts are usuallyvalue-dated two days from the initiation date.Forward, option, and swap transactions arevalue-dated for longer periods, as specified bythe transacting parties. These foreignexchange transactions are initiated through in-formal, over-the-counter interbank markets.In most cases the market risk inherent in theseproducts is not collateralized. Instead, risk iscontrolled by setting exposure limits to indi-vidual counterparties. The risks inherent inthe foreign exchange markets have recentlybeen exacerbated by the somewhat deteriorat-ing creditworthiness of some of its partici-pants.

Today, most foreign exchange obligationsare subject only to position netting (not nova-tion). This occurs when final delivery instruc-tions are entered into the relevant paymentssystem (for example, CHIPS for the dollar legof a transaction). The reliance on positionnetting and the lack of delivery vs. paymentleaves market participants with temporaryexposures which are large relative to theircapital. This risk is particularly important insettling dollar-yen transactions because of the14-hour gap between the final payment of yenin Tokyo and the final payment of dollars inNew York. One way to reduce this delivery

risk is to close the settlement gap by making itpossible to transfer dollars and yen simultane-ously.

Another way to reduce delivery risk is tointroduce netting by novation. The foreignexchange market has several characteristicsthat make it a candidate for the introduction ofnetting by novation. The largest participantsenter into numerous transactions that ulti-mately offset one another. As a result, grossexposures are often large relative to the par-ticipating banks' capital, exposing banks todelivery risk. Since the net exposures aresmall, much of this risk could be avoided ifnetting by novation were implemented. Giventhe large number of value dates, currencies,and participants, multilateral netting wouldlead to greater reductions in transactions vol-ume and risk than would bilateral approaches.In addition, since most participants deal with awide array of parties, indirect credit risk issignificant and a participant can find itextremely difficult to assess accurately its ex-posure to other parties.

The private marketplace took the first steptoward netting foreign exchange transactionswith the formation of FXNET, a bilateral net-ting by novation system that began operationin London in 1987. However, because thesystem does not provide delivery vs. payment,it only reduces delivery risk and does noteliminate it. The major benefit of FXNET isthat it should significantly reduce transactionvolume—by an estimated 50 percent (Bartko1990)—which could lead in turn, to significantreductions in transaction costs and both liquid-ity and credit risks.

A multilateral netting procedure wouldreduce the costs of foreign exchange transac-tions even more. With this arrangement lossesare allocated according to a pre-arranged for-mula. Risk levels are controlled by settingstrict entry requirements and demandingfrequent demonstrations of financial strengthby group participants. This allows traders toview all counterparties as homogeneous. Thisapproach has worked particularly well in thefutures market where the clearinghouses haveenforced strict entry requirements and marginrequirements, and stand as the counterparty toall trades. Simulations conducted in 1990 byInternational Clearing Systems and 13 bankssuggested that multilateral netting by novationwould reduce the credit risk associated with

6 ECONOMIC PERSPECTIVES

foreign exchange trading by 70-75 percent. Itwas projected that payment transactions wouldbe reduced by more than 95 percent.

What has worked so well for the futuresmarket, however, may not apply to othermarkets. Conversations with investment bank-ers and large international bankers concerningthe various netting proposals for foreign ex-change activity suggest that they see thesenetting schemes as a leveling influence thatwould reduce the advantage of firms doing thebest job of evaluating and bearing risk. More-over, some firms are concerned that theseproposals place them in the undesirable posi-tion of being unable to control or monitorcounterparty risk. As a result, some of themajor firms may be unwilling to sacrifice theirability to evaluate and select counterpartiesindividually.

Recent proposals for multilateral nettingattempt to address this problem by tying aparty's exposure to the value of transactionsit originated with the failing counterparty. Inthe event of the failure of a member of theclearinghouse, only those losses in excess ofeach originating party's capital would be mu-tualized. It is hoped that this procedure willmaintain incentives for individual members tomonitor and control risk, and will protect thecompetitive advantage of those members withgreater expertise in risk analysis.

On the surface, the delivery risk associ-ated with the settlement of foreign exchangetrades would appear to make this market animportant factor in any decision to extendexisting payments system hours. However, theadoption of multilateral netting would signifi-cantly reduce this delivery risk, in turn reduc-ing the need for extended hours. Nevertheless,should multilateral netting systems fail todevelop, demand for improvements to theexisting payment services would increase.

Derivative products

Derivative products are financial instru-ments whose value is tied to an underlyinginstrument. Examples of exchange-tradedderivative products include futures and optionstied to Treasury bonds, Eurodollar interestrates, the S&P 500 stock index, or the Japa-nese yen. A futures contract is an agreementto buy or sell a commodity at a later date un-der terms specified by the exchange at a pricedetermined today. Options contracts provide

the owner with the right to buy or sell a finan-cial instrument under the terms of the contract.The contracts are standardized with respect tothe underlying commodity, the posting ofinitial and variation margin, the method ofdelivery, and the value date.

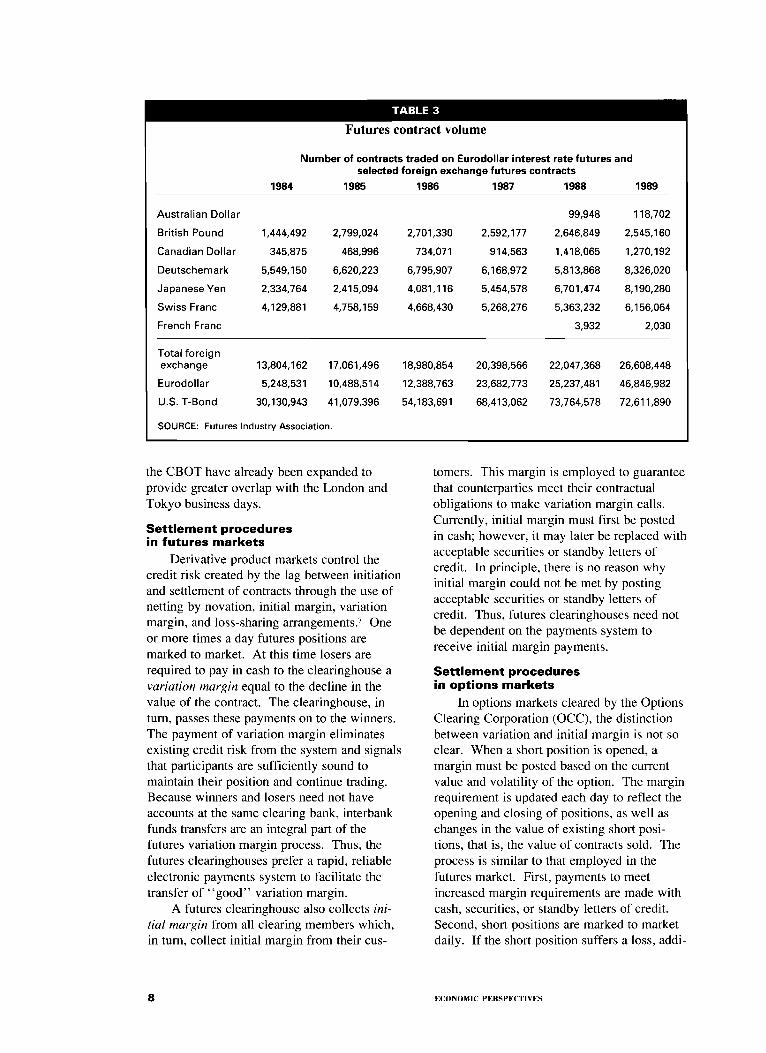

Globalization has spurred the creationand rapid growth of futures and options oninternational financial products (see Table 3).For example, futures contract trading on Euro-dollar interest rates increased almost 55 per-cent annually since 1984, reaching almost 47million in 1989. Moreover, combining futuresand options, nearly 40 million contracts onvarious foreign currencies were traded world-wide in 1988, up from 14 million in 1983. 6

Open interest, which is more closely associ-ated with clearinghouse risk and payments, hasalso grown (see Table 4).

Globalization has also led to the establish-ment of futures and options exchanges world-wide. Once the exclusive domain of U.S.markets, particularly in Chicago, derivativeproducts are now traded in significant volumesthroughout Europe and Asia. Between 1985and 1989, 20 new formal exchanges wereestablished, bringing the worldwide total to 72(Euromoney 1989). Obviously, competition inthis business line has increased as exchangesin London, Tokyo, and Singapore trade con-tracts that compete directly with those offeredon U.S. exchanges. In addition, foreign mem-bership on many exchanges is considerable.For example, over two-thirds of LIFFE'smembers are based outside of the United King-dom (Thagard 1989). As a result of growthoverseas, the share of exchange-traded futuresand options volume commanded by the U.S.exchanges dropped from 98 percent in 1983 toabout 80 percent in 1988 (Pavel and McE1-ravey 1990).

U.S. derivative product exchanges areresponding to the increased interest in round-the-clock trading as well as to the increasedcompetition from foreign exchanges. TheChicago Mercantile Exchange and the ChicagoBoard of Trade have made plans to extendtheir normal trading hours through computer-ized systems. The Chicago Board OptionsExchange (CBOE) is planning a 24-hour elec-tronic trading system. The trading hours forforeign currency options on the PhiladelphiaStock Exchange and Treasury bond futures on

FEDERAL RESERVE BANK OF CHICAGO 7

TABLE 3

Futures contract volume

Number of contracts traded on Eurodollar interest rate futures andselected foreign exchange futures contracts

1984 1985 1986 1987 1988 1989

Australian Dollar 99,948 118,702

British Pound 1,444,492 2,799,024 2,701,330 2,592,177 2,646,849 2,545,160

Canadian Dollar 345,875 468,996 734,071 914,563 1,418,065 1,270,192

U.S. T-Bond 30,130,943 41,079,396 54,183,691 68,413,062 73,764,578 72,611,890

SOURCE: Futures Industry Association.

the CBOT have already been expanded toprovide greater overlap with the London andTokyo business days.

Settlement proceduresin futures markets

Derivative product markets control thecredit risk created by the lag between initiationand settlement of contracts through the use ofnetting by novation, initial margin, variationmargin, and loss-sharing arrangements.' Oneor more times a day futures positions aremarked to market. At this time losers arerequired to pay in cash to the clearinghouse avariation margin equal to the decline in thevalue of the contract. The clearinghouse, inturn, passes these payments on to the winners.The payment of variation margin eliminatesexisting credit risk from the system and signalsthat participants are sufficiently sound tomaintain their position and continue trading.Because winners and losers need not haveaccounts at the same clearing bank, interbankfunds transfers are an integral part of thefutures variation margin process. Thus, thefutures clearinghouses prefer a rapid, reliableelectronic payments system to facilitate thetransfer of "good" variation margin.

A futures clearinghouse also collects ini-tial margin from all clearing members which,in turn, collect initial margin from their cus-

tomers. This margin is employed to guaranteethat counterparties meet their contractualobligations to make variation margin calls.Currently, initial margin must first be postedin cash; however, it may later be replaced withacceptable securities or standby letters ofcredit. In principle, there is no reason whyinitial margin could not be met by postingacceptable securities or standby letters ofcredit. Thus, futures clearinghouses need notbe dependent on the payments system toreceive initial margin payments.

Settlement proceduresin options markets

In options markets cleared by the OptionsClearing Corporation (OCC), the distinctionbetween variation and initial margin is not soclear. When a short position is opened, amargin must be posted based on the currentvalue and volatility of the option. The marginrequirement is updated each day to reflect theopening and closing of positions, as well aschanges in the value of existing short posi-tions, that is, the value of contracts sold. Theprocess is similar to that employed in thefutures market. First, payments to meetincreased margin requirements are made withcash, securities, or standby letters of credit.Second, short positions are marked to marketdaily. If the short position suffers a loss, addi-

8 ECONOMIC PERSPECTIVES

TABLE 4

Futures contract open interest

Open interest on Eurodollar interest rate futures andselected foreign exchange futures contracts

1984 1985 1986 1987 1988 1989

Australian Dollar 1,519 2,557

British Pound 18,385 25,082 23,145 28,589 16,442 20.208

Canadian Dollar 7,058 13,929 14,937 14,908 22,062 23,573

U.S. T-Bond 203,866 303,048 233,297 268,361 373,972 295,446

SOURCE: Futures Industry Association.

tional payments must be made to the clearing-house. If the short position gains, the clearingmember's margin requirement is reduced, per-mitting it to withdraw funds from the OCC.

Since the options settlement process doesnot move funds from winners to losers, it is, intheory, less dependent on the payments systemthan are the futures clearinghouses. The valueof payments to the OCC clearing membersnever exceeds the member's margin deposits,and payments to the clearinghouse couldbe-and in many cases are-made with securi-ties and standby letters of credit rather thancash. However, OCC clearing members fre-quently find it convenient to post securitiesand standby letters of credit after cash hasbeen supplied. In contrast, the only way that afutures clearinghouse could execute a variationmargin call without the payments system beingopen would be to have a single clearing bank.

Variation margin in derivative productsin a global market

Derivative product exchanges located inthe United States are seeking to expand theircustomer base in East Asia and Europe and arerapidly moving towards 24-hour trading.Meanwhile, U.S. firms are making increaseduse of products offered on foreign markets.These business development strategies will

have a significant impact on the settlementprocess in the futures and options industry.

Most of the problems faced by the OCCcould be dealt with by setting up overseasdepositories, using standby letters of credit,and having U.S. depositories execute securitiestransfers 24 hours a day. The problem ofeffecting settlements during nontraditionalbanking hours is more complex for the futuresclearinghouses and their clearing members.As business in Asia expands, the clearingmembers of these exchanges must confront thedifficulties of levying cash variation margincalls on Asian customers during the U.S. busi-ness day. If the margin call is issued duringChicago business hours, the Japanese bankingsystem is not open. Therefore, the only re-sources available to a Japanese customer aredeposits and lines of credit with bankingoffices in the United States. Clearing mem-bers currently make up any customer shortfallsout of working capital until the end of the nextU.S. business day. As the volume of businessfrom the Far East increases, this intraday expo-sure due to the time zone differences maygrow large relative to clearing members' capi-tal, making them less willing to continue thispractice.

By increasing the expense of dealing withEast Asian customers, the existing paymentsystems may be making it difficult for U.S.

FEDERAL RESERVE BANK OF CHICAGO 9

exchanges to penetrate further into the Asianmarkets. However, interviews with a numberof clearing members suggest that most foreigncustomers had U.S. balances arising fromother activities that were large relative to theirfutures activities in the United States. Wherethis was not the case, payments problems weretypically resolved using foreign exchangeservices provided by the clearing member.Because of the smaller size of the typical U.S.customer and the deficiencies of many foreignpayment systems and money markets, mostclearing members seemed more concernedabout the funds movements of U.S. customersdealing overseas than with the U.S. activitiesof foreign firms.

Round-the-clock trading creates additionalproblems for futures clearinghouses and theirmembers. For example, the substantial over-night price movement in a number of contractscreates the potential need for intraday margincalls between 5:00 p.m. and 7:00 a.m. easterntime. Indeed, the yen-dollar contract experi-ences more price movement overnight thanduring the U.S. business day (Lane 1989).Therefore, the ability to levy a nighttime mar-gin call would be particularly useful for thesecontracts. However, the margin call could becompleted only if the relevant institutions(U.S. banks) and their payment system wereopen during nighttime hours and had a meansof transferring value. When the paymentssystem is not operating, a clearing memberwould be exposed to increased risk commen-surate with the additional time necessary tocomplete the margin call (that is, the addi-tional time to confirm the customers' ability tocover their positions).

Derivative product markets can and dofunction at night even though the clearing-houses lack the ability to levy margin calls andreceive payments during these hours. How-ever, a large nighttime price move would cre-ate significant credit exposures between clear-ing members or between clearing membersand their customers. If the resulting exposureswere large relative to the resources of theclearinghouse, trading would slow and perhapscease as clearing members became unwillingto bear additional clearinghouse risk. Tradingwould resume only after the existing creditrisk had been eliminated by the transfer ofcash or securities from losing clearing mem-bers. Such a trading halt would be the market-

based analog to a regulatory circuit breaker.This market-induced trading halt, like its regu-latory counterpart, would be a nuisance ratherthan a disaster once the payment systemopened, since payments and settlement wouldstill take place." However, to the extent thatsuch halts are the result of deficiencies inpayment systems, market participants can bemade better off by altering payment practices.

In summary, as the trading hours andcustomer bases expand in derivative productmarkets, the desire to move margin moniesaround the world and around the clock willincrease. This in turn will lead market partici-pants to seek ways to execute cross-bordervariation margin calls outside of traditionalbusiness hours. While the critical pressure islikely to come from clearinghouses associatedwith exchanges, the growing collateralizedover-the-counter market could also be a sourceof demand.

Offshore dollar clearings

Offshore dollar clearing arrangementshave been introduced in foreign countries tomeet the demand of local institutions for dollartransactions with (local) same-day value.U.S. banks commonly serve as the clearingentity—they determine positions of the partici-pating parties and serve as the settling bankonce the U.S. markets open. Given the trendtoward globalization and the imposition ofdaylight overdraft limits on U.S. domestictransfer networks, the role of offshore dollarclearing arrangements may increase in thefuture. It was this potential which lead theFederal Reserve to issue its policy statementemphasizing the need for risk control measureson these arrangements (Board of Governors1989). 9

These clearing arrangements involve addi-tional risk when the operating hours of the hostcountry's banking system do not overlap withthe U.S. banking day. The resulting localsame-day value is essentially a credit exten-sion by the settlement bank. For example,these arrangements commonly have transac-tions netted and "provisionally" settled duringthe local business day, with final settlement in"good" funds at the end of the U.S. businessday through the account of the U.S.-basedclearing bank via CHIPS. Although a loss-sharing arrangement may be in place, theremay be no collateral backing the agreement,

10 ECONOMIC PERSPECTIVES

and nothing dictates that the positions arelegally binding, although customers may act asif they were. This may be particularly trouble-some during times of crisis. If settlement wereto occur over CHIPS, the clearing bank couldface significant problems if a participant in adebit position failed to make payment beforethe end of the U.S. banking day. The bankprobably would have already initiated irrevers-ible credits on CHIPS (to the remaining clear-ing arrangement members) and may havedifficulty meeting its settlement requirements.Thus, CHIPS' settlement could be impaired.Alternatively, the clearing bank could providethe necessary credit and, during the next busi-ness day, could request that participants un-wind credits received the previous day. Whilesmall reversals may be made to maintain thedollar clearing system, reversals of large posi-tions during a time of crisis would be unlikely.Institutions would probably simply defer untilmore information were available on the de-faulting participant. Therefore, the lack ofoverlapping business hours creates accountoverdrafts and temporal risk for the U.S. bankorganizing the dollar clearing arrangement.

Improvements could be made in the cur-rent clearing arrangements. First, legally bind-ing agreements that make the allocation ofcredit and liquidity risk explicit and whichguarantee finality could be initiated. Theguarantee could be backed by collateral or thecapital of the participants. Movement towardthis goal appears in prospect on some of thearrangements. Second, adjustments to thepayments system could be introduced so that adollar-based funds transfer network with final-ity operates during the U.S. nighttime hours.This would directly address problems evolvingfrom the lack of overlapping business days.

Nighttime transactions and thepotential demand for payments activity

Emerging stresses on the global paymentssystem arise from several sources: the increas-ing importance of cross-border securities lend-ing, growth in the nighttime trading of U.S.government securities, significant risk in theforeign exchange markets resulting from thelack of netting or delivery vs. payment mecha-nisms, rapid growth of offshore dollar clear-ings, and the attempt by futures and optionsexchanges to expand their trading hours andcustomer base.

The objectives in evaluating alternativeways to improve current means of transferringvalue during nontraditional U.S. banking hoursare twofold: to increase efficiency and to im-prove risk management. Since the level of riskresulting from payments activity during thesehours is closely correlated with payment vol-ume, the demand for nighttime transactions isthought to depend critically on the level ofactivity in the nighttime market.

What is the current level of demand fornighttime transactions? We attempt to gener-ate a rough estimate based on the assumptionthat the bulk of the activity will be generatedfrom the sources discussed above.

As noted earlier, there are no publiclyavailable estimates of the volume of off-hourstrading in Treasury securities. However, rea-sonable approximations can be generated. Ifwe assume that the hourly ratio of nighttime tototal trading is the same for the cash securitiesas for the futures contracts, then we can proj-ect that approximately 15 percent of totaltrading in Treasury securities occurs at night.However, only a portion of these transactionswould be for same-day settlement. The gen-eral rule-of-thumb is that about 50 percent oftransfer instructions received by the FederalReserve are for the settlement of trades madeearlier in the day. Given this assumption,about 7.5 percent of the Treasury transactionscrossing the books of the Federal Reserve on agiven day would arise from trades entered intothe previous night for same-day delivery. Thissuggests a daily volume of approximately $26billion.

In contrast, transactions from margin callsfor futures and options contracts are likely tobe relatively modest. On a typical day thederivative product markets create perhaps $12billion in payments traffic.'" Typically about70 percent of this represents variation marginwith the remaining portion meeting initialmargin requirements. During times of extremevolatilility like October 19, 1987, total pay-ments volume associated with the derivativemarkets might well exceed $30 billion. How-ever, only part of this total would shift tonighttime trading.

Based on Chicago Board of Trade experi-ence, nighttime trading constitutes about 15percent of daytime volume. Thus, we couldexpect that payment of initial margin associ-

FEDERAL RESERVE BANK OF CHICAGO

11

ated with the opening and closing of positionswould approximate 15 percent of the currentdaily total of approximately $3.6 billion—or$500 million. Since average nighttime pricemovements for derivative products is about 40percent of the total daily movement (Lane1989), nighttime variation margin paymentswould approach 40 percent of the daily total of$8.4 billion—or $3.3 billion. Summing thesetwo components, the total nighttime paymentsarising from margin calls would be approxi-mately $3.8 billion. A more conservativescenario, and perhaps more realistic, wouldhave payments restricted to transactions be-tween the clearinghouses and their clearingmembers and would exclude payments be-tween clearing members and their customers.These payments, which would only encompassvariation margin calls, currently account forapproximately 20 percent of the total $3.8billion variation margin. This would producea conservative nighttime estimate of approxi-mately $800 million. Rapid growth of the dol-lar-denominated contracts in London and Sin-gapore could cause this to grow, as could ashift in variation margin practices of Japanesefutures exchanges which currently give partici-pants three days to meet a margin call ondollar-denominated contracts.

Payment flows related to the settlement offoreign exchange contracts are the most diffi-cult to predict. Demand will depend criticallyon whether, and how, multilateral netting isintroduced into this market. In the absence ofa system of multilateral netting, contractsinvolving European currencies would probablysettle at the close of the European business day(12 noon to 2 p.m. eastern time) and, thus,would not contribute to the U.S. nighttimevolume. Similarly, movement toward a singlemonetary unit for Europe after 1992 could leadto reductions in foreign exchange activityinvolving these countries.

In the absence of multilateral netting,therefore, the primary source of nighttimeforeign exchange transactions would be con-tracts involving the Japanese yen. The Bankfor International Settlements (1989) estimatedthat dollar-yen trading averaged $162 billion aday in 1989. Of this, perhaps $25 billion isnetted away through existing offshore clearingarrangements. Thus, in the absence of anycontract netting, dollar volume could average$137 billion a day. However, netting is ex-

pected to occur. The introduction of bilateralnetting on a currency pair basis could reducethe $162 billion to $81 billion (Bartko 1990).Since bilateral netting should continue to pro-liferate, this approximation should provide anupward bound on the demand for transactions.

The introduction of a multilateral foreignexchange clearinghouse could dramaticallyreduce the volume of payments associatedwith the settlement of dollar-yen transactions.International Clearing Systems, Inc. estimatesthat multilateral netting reduces dollar volumeby approximately 95 percent, leaving us with aconservative revised total nighttime volume ofabout $8 billion. However, existing multilat-eral netting proposals would net dollar pay-ments associated with dollar-yen transactionsagainst dollar payments associated with otherforeign currency transactions. To eliminatedelivery risk completely, all currencies wouldneed to move at the same time. A logical timefor this to occur would be early in the U.S.morning when the other two payments systemsare open. However, even this would requirechanges in payments system practices in Eu-rope and Japan. With global foreign exchangetrading currently running at $650 billion a day,multilateral netting would reduce the dailydollar settlement by 95 percent to roughly$32.5 billion.

Summing these sources of demand, esti-mated nighttime transactions would run some-where between $27 and $110 billion a day,depending on the assumptions employed (seeTable 5)." The lower figure is comparable tothe Federal Reserve's 1968 electronic fundstransfer volume; in today's terms, it equalsapproximately 2 percent of current volume onCHIPS and FedWire combined. However, ifpast growth trends are any indication, we canexpect transaction volume to increase substan-tially in the future.

Summary and policy implications

During much of the 24-hour day, financialmarket participants find it difficult or impos-sible to eliminate market risk by transferringcash or collateral. In many cases participantsdo not have the option of settling transactionson a delivery vs. payment basis. Additionally,in contrast with domestic transactions, it isdifficult for participants to limit the deliveryrisks inherent in international transactions byhaving settlement occur relatively soon after

12 ECONOMIC PERSPECTIVES

TABLE 5

Potential nighttime transaction demand(billions of dollars)

Treasury securities 26

Derivative products' .8 to 3.8

Foreign exchange' 0 to 81

Total 26.8 to 110.8

The low end of the range assumes that the onlypayments made are between the clearinghouse andits members; the high end assumes that clearingmembers attempt to collect from and pay tocustomers at night.

bThe low end of the range represents the case ofmultilateral netting with delivery vs. paymentimplemented during daytime hours; the high endrepresents an environment with bilateral netting andnighttime settlement of dollar-yen transactions only.

NOTE: See text for citations.

the initiation of payment. Ten years ago theseproblems were less important. However, thefinancial markets have changed significantlysince then. The hours during which marketsare active have been extended for some finan-cial products and will be extended for others inthe immediate future. Financial transactionactivity has grown exponentially. Thesechanges have occurred without many corre-sponding changes in the payments system.

This study has reviewed trends in the flowof international payments, the characteristicsof existing payment system arrangements, andthe problems inherent in these arrangements.Such recent changes in payment system prac-tices as the movement toward netting arrange-ments and implementation of loss-sharingagreements allowing for settlement finalitywill lead to significant cost savings and reduc-tions in payments system risk. However,given the changing financial markets and thegrowing demand for transfers of value duringnontraditional business hours, the changes todate may be inadequate. Discussions withfinancial market participants as well as esti-mates based on what we believe to be realisticassumptions suggest a potentially significantdemand for nighttime payments arising fromthe market for U.S. government securities,cross-border securities lending, offshore dollarclearing systems, settlement of foreignexchange activity, and margin calls forexchange-traded derivative products. Exclud-

ing offshore dollar clearing arrangements, weestimate the potential demand for nighttimetransactions currently to be between $27 and$110 billion a day, or 1.5 percent of currentdaytime volume. Even at the low end of thisrange, the resulting risk from using currentpayments arrangements is thought by manymarket participants to be significant. Addi-tionally, the evidence suggests that in thefuture, transactions during this period will con-tinue to increase.

How can the demand for these transac-tions best be met? In our opinion, the bulk ofthe solution should come from the privatesector. Similarly, the bulk of the risks result-ing from payment system activity should beborne by financial institutions and their cus-tomers. However, for these solutions to beimplemented efficiently and effectively, theprivate sector needs the tools to managenighttime risk. The central bank has the abil-ity to provide those tools without distorting themarketplace. Thus, a combination of publicand private sector initiatives would appear tobe appropriate. This approach is based on twopropositions. First, the private sector has dem-onstrated that it has both the ability and incen-tives to evaluate and to manage risk, and anincentive structure that balances the benefits ofrisk reduction against its costs. Second, as aresult of investments made to service daytimedemand, the Federal Reserve may well have acost advantage in providing the tools to man-age nighttime risks. Likely private sectorinitiatives include the extension of netting bynovation and substitution to new markets, thecreation of new clearinghouses, improved fi-nality on private sector payments arrange-ments, and extended operating hours for pri-vate payments systems and securities deposito-ries. Likely central bank initiatives includeadditional net settlement services and extendedhours of operation for funds and securitiestransfer systems.

By opening the book-entry and fundstransfer services earlier and offering an addi-tional early net settlement service, the FederalReserve would make it possible for privatesector transfer networks to decrease temporalrisk.' 2 While proposed plans to enhance thedegree of finality on private transfer networksshould reduce the need for FedWire finality,offering the additional settlement coulddecrease the monitoring cost incurred by banks

FEDERAL RESERVE BANK OF CHICAGO 13

in controlling temporal risk. These riskswould otherwise exist until settlement at theend of the day on FedWire.

Market participants may advocate theextension of existing daytime Federal Reserveservices to cover the full 24-hour day. How-ever, we believe this approach has at least twoproblems. First, should the central bank sim-ply expand existing operations to the nighttimemarket, there would be significantly less in-centive for the private sector to make neededchanges in its operations. Second, we knowthat the central bank's presence in the provi-sion of payments, if not properly structured,can distort market behavior and can lead to thecreation of excessive risk exposures. How-ever, having a modified version of FedWireand book-entry services operating in conjunc-

tion with private firms during the nighttimehours may still be desirable, given that it al-ready operates during the daytime."

Any extension of Federal Reserve hours,however, should be preceded by the imple-mentation of modifications to eliminate thedistortions induced by current operating prac-tices. These would include the full collaterali-zation of overdrafts and the elimination of thebelow market interest rates currently chargedfor emergency loans at the discount window.Of course, strong consideration should begiven to making these changes even if theFederal Reserve continues to operate only inthe daytime market. At issue, obviously, anda topic beyond the scope of this paper, iswhether or not the central bank should havean operational presence in the daytime market.

FOOTNOTES

1 For a more complete description of payments system riskand costs and alternative means to manage them, see Bankfor International Settlements (1989), Parkinson (1990), orBaer and Evanoff (1990).

2CHIPS is a private clearing system located in New Yorkand operated by the New York Clearinghouse Association.It is a dollar-denominated network specializing in interna-tional payments. Payments undergo multilateral positionnetting (without novation) and settlement occurs at the endof the U.S. day over the books of the Federal Reserve Bankof New York. CHIPS is currently taking steps to improveits risk management procedures.

3The reader is referred to Pavel and McElravey (1990) for amore complete discussion of recent trends in internationalfinancial activity.

4A report by the Group of 30 (1989) recommended theproposed change. The report also seeks the creation ofdelivery vs. payment settlement systems where feasible andencourages securities lending as a means of expeditingsettlement.

5By "good" or "final" funds we mean the security ofreceivers that funds transferred to them via electronictransfer networks will actually be delivered. The degree ofsecurity depends on the characteristics of the sender and thenetwork on which the funds were transferred. For example,funds transferred over FedWire are considered "final"because the Federal Reserve guarantees them. Thus, to theextent the Federal Reserve can and will deliver on theguarantee, the transfer is considered final. Other networksmay declare all transfers final, but the claim is only as goodas the credibility of the network.

6See Pavel and McElravey (1990).

7For a discussion of the various settlement systems in thederivative product markets, see Rutz (1988).

"See Moser (1990) for a discussion of circuit breakers forthe U.S. stock market and financial derivatives market.

9When daylight overdraft caps were originally placed onCHIPS and FedWire there was concern that certain busi-ness and payments activities would shift offshore. Partly inresponse to this concern, the Federal Reserve issued itspolicy statement

10 The $12 billion figure and the other percentages used inthis analysis are approximations based on discussions withseveral bank and clearinghouse representatives; alternativesources suggest similar figures.

11 No publicly available information exists on the dollarflows through offshore dollar clearing arrangements. Sinceour estimates cover a relatively broad range it is doubtedthat the exclusion of this sector appreciably affects ourprojections.

12These alternatives are currently being evaluated by theFederal Reserve System.

13For a more thorough discussion of policy options to man-age payments system risk, see Baer and Evanoff (1990).

14 ECONOMIC PERSPECTIVES

REFERENCES

Baer, Herbert L., and Douglas D. Evanoff(1990). "Payments system risk issues in aglobal economy." Federal Reserve Bank ofChicago Working Paper Series WP:90-12(August).

Bank for International Settlements (1989).Report on netting schemes. Basle: BIS.

Bartko, Peter (1990). "Foreign exchangeand netting by novation." Paper presented atthe Federal Reserve System symposium oninternational banking and payment services,Washington, D.C., June 7-9, 1989. Summa-rized in Payment Systems Worldwide, pp. 48-51 (Spring).

Board of Governors of the Federal ReserveSystem (1989). Proposals to Modify thePayments System Risk Reduction Program.Press Release—Request for Comment andPolicy Statement. Docket Numbers R0665-R0670, Washington, D.C. (June 16)

Chicago Mercantile Exchange (1989)."Clearing House Banking Interfaces." Whitepaper (February).

Euromoney (1989). "U.S. exchanges fightfor market share." Special issue, pp. 9-12(July).

Group of Thirty (1989). "Clearance andsettlement systems in the world's securitiesmarkets." New York/London (March).

Lane, Morton (1989). "Blue print for theglobal broker." Research Paper, DiscountCorporation of New York Futures.

Moser, James (1990). "Circuit breakers."Federal Reserve Bank of Chicago, EconomicPerspectives, pp. 2-13 (September/October).

Parkinson, Patrick (1990). "Innovations inclearing arrangements: A framework for analy-sis." Proceedings of a Conference on BankStructure and Competition. Federal ReserveBank of Chicago (forthcoming).

Pavel, Christine, and John McElravey(1990). "Globalization in the financial serv-ices industry." Federal Reserve Bank ofChicago, Economic Perspectives, pp. 3-19(May/June).

Rutz, Roger D. (1988). "Clearing and settle-ment systems in the futures, options and stockmarkets." Paper presented at the RegulatoryIssues in Financial Markets Conference spon-sored by the Chicago Board of Trade, Wash-ington D.C. Summarized as "Backgroundpaper: Clearance, payment, and settlementsystems in the futures, options, and stockmarkets." The Review of Futures Markets,pp. 346-370 (November).

Thagard, Elizabeth R. (1989). "London'sjump." Intermarket, pp. 22-24 (May).