67

DOING BUSINESS IN INDIA A Guide for Foreign Companies Transacting in India 19 th January 2017

| Date post: | 07-Feb-2017 |

| Category: |

Business |

| Upload: | shruti-agarwal |

| View: | 57 times |

| Download: | 3 times |

DOING BUSINESS IN

INDIA

A Guide for Foreign Companies Transacting in India

19th January 2017

AgendaTo discuss the ongoing changes in the Indian Economy, Laws and Policies which are catalyzing the process of India becoming an attractive investment destination and to walk through the process of "Doing Business in India”.

2

3

▹ Introduction: India as an Investment Destination

▹ How to setup Business in India and Routes for Investment into India

▹ How to do Business in India: Compliance and Regulatory Obligations

▹ Know the taxes you’re paying in India and whether you should be paying them

▹ Demonetization and Impact of Other Changes on the Indian Economy

Detailed Agenda

8th November 2016The Decisive day for American, Indian and World Economy as a whole

4

Introduction: India as an Investment Destination▸ The government has

taken a series of measures such as easier governing and fund raising norms, clarification of tax related matters and higher FDI limits, thereafter numerous initiatives have been launched to help in ease of doing business in India.

▸ Campaigns like Make in India have had a major impact in bring India into the manufacturing globe.

5

Source: Haver Analytics, World Bank

FDI 30%Total FDI investments India received during April - September 2016 rose 30 per cent year-on-year to US$ 21.6 billion

6

“

”

Data for April - September 2016 indicates that the services sector attracted the highest FDI equity inflow of US$ 5.29 billion, followed by telecommunications – US$ 2.79 billion, and trading – US$ 1.48 billion. Most recently, the total FDI equity inflows for the month of September 2016 touched US$ 5.15 billion.

SOURCE OF FDI Equity Inflows : April – September 20168

$ 1.44 billion

$ 5.85 billion

$ 4.68 billion

$ 2.79 billion

FDI- Expected Growth Rate▸ Investments in India are expected to grow at a compound annual growth rate (CAGR) of 20-24 percent touching US $6-8 billion by 2025, from US $1 billion in 2015

9

1.How to setup Business In India

10

As a holder of American

Global Depository Receipts

(“ADR”) and Global

Depository Receipts (“GDR”s)

Types of Investment for a Non Resident Entity

As a registered

Foreign Institutional Investor

(“FII”)

Foreign Direct

Investment (“FDI”)

As a registered

Foreign Venture Capital Investor (“FVCI”)

under the Venture

Capital route

11

Foreign Investors Establishing Business in India (FDI)

▸ Foreign investors planning to set up their business in India are required to seek consent from the Government before investing in India.

12

Automatic Route

Under automatic route the Foreign Direct Investment, to the extent permitted, does not require any prior approval either by the Government or RBI. There are sectoral caps defined under the Automatic Route. The investors are only required to notify the Regional offices of RBI within 30 days of receipt of inward remittances and file the required documents with the respective office within 30 days of issue of shares to foreign investors.

Foreign Investors Establishing Business in India

13

Foreign Investors Establishing Business in India

14

Sectoral Caps

under the

Automatic

Route

Government Approvals for Foreign Companies Doing Business in India

Banking and NBFC's Activities

in Financial Services Sector

Housing & Real Estate

Development Sector.

Atomic Energy & Related Projects Print Media

Petroleum Including

Exploration/Refinery/Marketing

Venture Capital Fund and Venture Capital Company

Defense and Strategic Industries

Broadcasting

Civil AviationInvesting

Companies in Infrastructure & Service Sector

Agriculture (Including Plantation)

Postal Services

15

Automatic route unavailable for the following sectors

Approval Route

▸ FDI in sectors not covered under the automatic route, requires prior Government approval and are considered by the Foreign Investment Promotion Board (FIPB).

▸ Approvals of composite proposals involving foreign investment/foreign technical collaboration are also granted on the recommendations of the FIPB.

Foreign Investors Establishing Business in India

16

Foreign Company (Liason/ Project/ Branch Office)

Forms of Business Organisation

Partnership(Including

LLPs)

Proprietorship

Indian Company

(Joint Ventures &

Wholly Owned

Subsidiaries)

17

Foreign Investors Establishing Business in India

18

* RBI = Reserve Bank of India | ROC = Registrar of Companies

Simplified: Incorporation of a Private Limited Company

SPICe – Simplified

proforma for Incorporating

Company Electronically

19

e-Memorandum of Association

e-Articles of Association.

The Integrated Form INC-29 has been replaced with SPICe Form INC-32 and as such the Form INC-29 has been completely removed from the MCA portal. .

It has other added benefits wherein the DINs get allotted to those Directors who do not hold a valid DIN and also the Company’s PAN, TAN and ESIC registration can also be obtained easily in a single step.

*DIN = Director Identification Number | PAN = Permanent Account Number | TAN = Tax deduction Account Number

2.How to do Business in IndiaCompliance and Regulatory Obligations

20

Federal Tax Structure in India

India is a Federal Republic and the power to make laws is divided between the Central & State Governments.

21

This list is not exhaustive and is only for representational purposes

Compliance and Regulatory Obligations

Whether the company is a Private company or a Public company, a number of compliances are required to be carried out post incorporation.

22

Compliance and Regulatory Obligations

Compliances

ONE TIME:Application for

PAN/TAN, Opening of Bank

Account (s)Issuance and

Stamping of Share

Certificates

Periodic:

Accounts and Audit , Holding of

Share Holders/Board

Meetings,Annual Corporate

FilingsFiling of Income Tax Returns and Other Returns

under applicable laws

23

Compliance and Regulatory Obligations

Labour and

Employment

Regulations

Labour Welfare Fund &

Professional Tax

Maternity Payment & Prevention of Sexual

Harrasment

24

Minimum Wages

Act

Employe

es Provident Fund &

Insurance

Gratuity and Bonus

Compliance and Regulatory Obligations

FOREIGN EXCHANGE

LAWS

(FEMA + CUSTOMS + COFEPOSA)

FEMA, along with it’s rules

and regulations governs foreign

exchange transactions in and from India.

For transactions

on both Current & Capital Account reporting/prior

permissions are needed from RBI. Annual Filings of Investment into India to be made

25

Compliance and Regulatory Obligations

Competition Law

Anti- Competit

ive Agreeme

nts

Combination

26

Abuse of Dominant Position

Compliance and Regulatory Obligations

Environmental and

Consumer Legislation

Environment Act

Consumer

Protection Act

27

Public Liability Insurance Act

3.Know the taxes you’re paying in IndiaAnd are they applicable to you ?

28

Tax Structure29

Corporation Tax : Rate▸ The rate is 30% for domestic

companies and 40% for foreign companies and their branches.

▸ This rate is besides applicable surcharge & cess (if any).

▸ Special Exemptions given from Taxation – SEZs, StartUps, Industries setup in Notified Areas

▸ The Union Government has committed to reduce the rate to 25% in a staged manner by

30

Corporation Tax : DDT & MATA company is liable to pay Dividend Distribution Tax (hereinafter “DDT”) on the amounts declared or distributed as dividend at the rate of 15% (plus applicable surcharge and education cess)

In case tax liability of a company is less than 18.5% of its book profits, such book profits are deemed to be ‘taxable income’, and such company is liable to pay a Minimum Alternate Tax at 18.5% (plus applicable surcharge and education cess).

31

32

Source: FPI Survey PWC

Tax Withheld at Source

▸ Any person responsible for making a payment to a non-resident, which is chargeable to tax under the ITA, must withhold tax at the applicable rates.

▸ Tax Residency Certificates are a must to claim DTAA benefits for Foreign Companies.

33

Foreign Tax Credit

Foreign Tax Credit

Foreign tax paid may

be credited against

Indian tax on the same

profits

Credit is limited to

the amount of Income

Tax payable on foreign

income

34

Foreign Tax Credit35

Foreign Tax Credit - Types of Tax Relief

Unilateral Tax Relief - Relief as per domestic income tax provisions e.g. Section 91 of the Income-tax Act 1961

Bilateral Tax Relief - Relief as per mutual covenants / DTAAs (Article 23 read with domestic income-tax provisions) Relief via DTAAs generally more beneficial than the domestic tax laws DTAA restrict a country’s ability to unilaterally override provisions in

DTAA to the detriment of taxpayers Contracting state to decide which method to use

Exemption Method ; or Credit Method (Direct Credit | Indirect Credit (Underlying Tax Credit) |

Special Credit (Tax Sparing}

GAAR (Background)▸ In 2007, Vodafone entered the

Indian market by buying Hutchison Essar, the deal took place in Cayman Islands. The Indian government claimed over US $2 billion were lost in taxes. In September 2007, a notice was sent to Vodafone. Vodafone claimed that the transaction was not taxable as it was between two foreign firms. The government claimed that the deal was taxable as the underlying assets involved were located in India.

36

“

”

The regulation allows tax officials to deny tax benefits, if a deal is found without any commercial purpose other than tax avoidance. It allows tax officials to target participatory notes.

Under GAAR, the investor has to prove that the participatory note was not set to avoid taxes. It also allows officials to deny double taxation avoidance benefits, if deals made in tax havens were found to be avoiding taxes.

“

”

The Central Board for Direct Taxes (CBDT) has announced that the General Anti-Avoidance Rule (GAAR) will start from April 1, 2017 to check tax evasion and avoidance.

Indirect Tax Structure 39

Recent Amendments: Service Tax on OIDAR Services

▸ On 9 November 2016, India’s Ministry of Finance amended Service Tax rules related to Online Information and Database Access or Retrieval services (OIDAR) will require Non-Resident Service Providers to pay Service Tax when they provide Services to clients for Non-Business purposes.

40

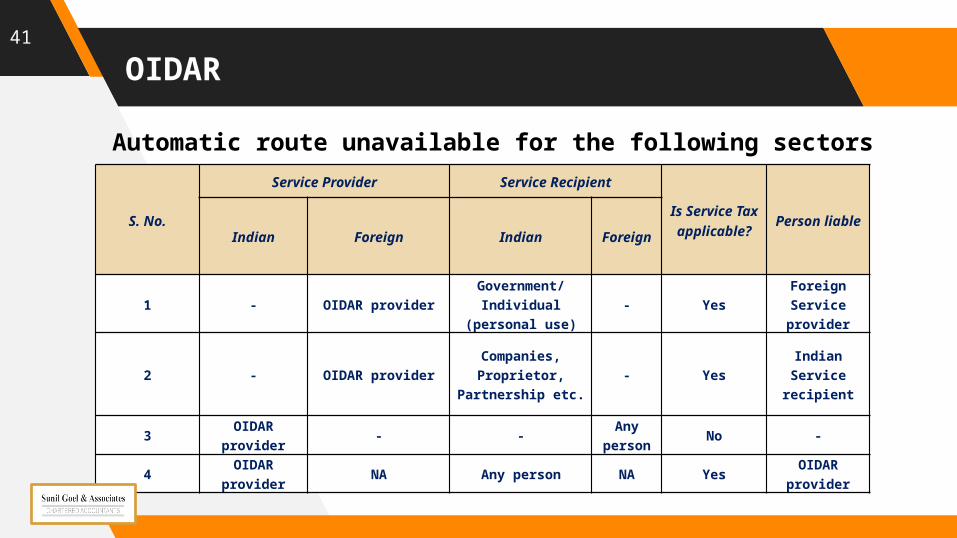

OIDAR41

S. No.

Service Provider Service RecipientIs Service

Tax applicable?

Person liableIndian Foreign Indian Foreig

n

1 - OIDAR providerGovernment/

Individual (personal use)

- YesForeign Service provider

2 - OIDAR providerCompanies, Proprietor,

Partnership etc.- Yes

Indian Service

recipient

3 OIDAR provider - - Any

person No -

4 OIDAR provider NA Any person NA Yes OIDAR

provider

Automatic route unavailable for the following sectors

“

”

Central Government had recently announced the procedure for online payment of service tax through foreign banks providing big relief to the foreign tax payers.

Recent Amendments: Equalization Levy

▸ Equalization levy was made effective from 1st June 2016 @ 6% to be deducted from amount paid to a non-resident (not having any permanent establishment in India) for specified services received by i. Resident who is running business in India OR ii. Non-resident having a permanent establishment in India.

43

Specified services include

Online Advertise

ment

Any provision for digital advertising space

Any other services as

may be notified

44

Key Points

▸ As it happens in case of remittances in India, it would be routine work for an Indian service recipient to ask the nonresident service provider for a ‘No PE’ declaration so as to decide on the applicability of the Equalization Levy.

▸ Online advertising services are separately subject to Service Tax @ 15% on a reverse charge basis which is to be collected and discharged by the Indian service recipient.

45

Advance rulings

▸ AAR rulings are equivalent to US private letter rulings. Like private rulings, they can be obtained for prospective transactions, and are only binding on the parties involved.

46

Advance rulings

The applicant already has a case pending

47

The issue involves determination of fair market value of any property

The issue relates to a transaction which is designed prima facie for avoidance of tax.

“

”

Similar to the AAR for income tax determination, an Authority for Advance Rulings (Central Excise, Customs and Service Tax) [AAR(CECST)] has also been set up to give binding rulings, in advance, on indirect tax matters concerning a foreign investment venture in India.

Goods & Services Tax (GST)▸ GST is a game changing reform for the Indian Economy which will reduce the cascading effect of tax on the cost of goods & services leading to a complete overhaul of the current indirect tax system.

49

“

”

Foreign Investors are reluctant to invest in India due to country’s regulatory and bureaucratic complexities which is going to change after the implementation of GST.

Goods & Services Tax (GST)51

Goods & Services Tax (GST)Advantages of GST are:▸ Unified Market which

would facilitate seamless movement of goods and reducing transaction cost of business.

▸ Logistics cost would fall as collection of taxes at state-borders will reduce.

▸ Reduction in Logistics cost will lower the inventories and working capital needs, hence improving asset utilization and increase efficiency.

52

“

”

It will be simpler for Foreign Companies to comprehend the tax norms and not have to file tax with multiple departments but one web-based form.

GST would integrate the economy and provide a larger base for foreign companies to operate in.

With reduced taxation, exports from India would increase and be more cost competitive in the global markets

4.DemonetizationImpact on Indian Economy

54

Demonetization

▸ Demonetization is a foremost step in assuring the Foreign Investors that India is moving away from corruption and towards a cashless economy where it is easy to carry out business and no bureaucracy is required to set up a new business.

55

▸ Moving towards Digital Economy: Technology has reached Tier 2 and Tier 3 cities giving companies a larger consumer base to target

▸ Removal of Petty Corruption: Bureaucracy & Corruption at lower levels would be eliminated

▸ Decrease in Real-Estate prices: Demonetization has reduced property prices by up to 30% which will reduce cost for Foreign Investors setting up their base in India.

Impact of Demonetization - Advantages56

Impact of Demonetization - Advantages

▸ Increase in online transactions: As reported by PayTM, the cash crunch has led a huge upward spike in online transactions.

▸ Shift Towards Organized Players: Curbing cash transactions will impact smaller players, leading to a move towards the organized segment

57

5.Case Studies

58

WHAT THE BIG PLAYERS ARE UPTO

Investments/ developments

Pepsi plans to invest Rs 500 crore (US$ 72.8 million) to set up another unit in Maharashtra to make mango, pomegranate and orange-based citrus juices, while biotechnology giant Monsanto plans to set up a seed plant in Buldhana district of Maharashtra.

Ford Motor Co. plans to invest Rs 1,300 crore (US$ 189.2 million) to build a global technology and business centre in Chennai, which will be designed as a hub for product development, mobility solutions and business services for India and other markets.JW Marriott plans to have 175-200 hotels in India over the next four years.

60

Vistra Group Ltd has acquired IL&FS Trust Company Ltd, India’s largest independent corporate trust services provider, which will enable Vistra to expand the platform to provide a broader suite of corporate and fiduciary services and thereby gain a foothold in the Indian corporate services market. .

Apple Inc has started its first development centre outside the US in Hyderabad, which will employ over 4,000 people and focus on Apple Maps, the company’s digital maps and navigation service.

The first Incredible India Tourism Investment Summit 2016, which was organized from September 21-23, 2016, witnessed signing of 86 Memoranda of Understanding (MoUs) worth around Rs 15,000 crore (US$ 2.18 billion), for the development of tourism and hospitality projects.

6. Government Initiatives

The Union Cabinet has approved a scheme allowing the grant of Permanent Residency Status (PRS) to foreign investors based on a minimum investment of Rs 10 crore (US$ 1.5 million) within 18 months or Rs 25 crore (US$ 3.6 million) within 36 months, which is expected to encourage foreign investment and facilitate Make in India program.

The Department of Industrial Policy and Promotion (DIPP) has allowed 100 per cent foreign direct investment (FDI) in asset reconstruction companies (ARC) under automatic route, which will help to tackle the issue of declining asset quality of banks.

CASE STUDIESSUCCESS AND DOWNFALLS

62

“

”

▸ Volvo India Pvt. Ltd. came to Bengaluru, India in 1998 and started shop with an investment of about USD 70 million.

▸ By 2013 it had expanded to around 100% and now has 76% of the luxury bus market in India.

Case Study: Success Story

▸ What Volvo did successfully was it sold the concept of luxury bus travel and not just its buses. Volvo was willing to depart from the norms and challenge the way the industry worked at that time. In India, bus length was capped at 11m but Volvo got that changed.

To persuade the operators, the sales team at Volvo demonstrated how Volvo would be more reliable and profitable. To make the deal more lucrative Volvo offered service support for the entire bus and not just the individual parts.

Volvo did not reach the top by cutting prices or toning down its products, it developed and nurtured the market and then waited for it to mature and then reap the profits

Volvo is now a synonym for luxury bus travel in India.

64

Case Study: DownfallsWALMART

▸ For Walmart the biggest issue was their proposed business model which did not fit in with the regulations.

▸ Lobbying is illegal in India and there was significant outcry when Walmart disclosed that it had been indulging in India specific lobbying.

IKEA▸ The Swedish retail giant entered India

in 2007 but could not open its stores because of infrastructural & economic laws pertaining in India at that time.

▸ IKEA wanted to open cafes in its store making it a multi-brand retail which was not permitted by the Indian Government and further stalled the proposal.

65

Question and Answers

67

Thanks !