36

Nuclear market trends Mike Saunders, President, Power & Process Europe Sellafield site investor trip: 21 June 2010 Sellafield site investor trip: 21 June 2010

Nuclear market trendsMike Saunders, President, Power & Process EuropeSellafield site investor trip: 21 June 2010Sellafield site investor trip: 21 June 2010

Agendag

Global nuclear market

Size and drivers

Market structure and characteristics

Investment costs and timelines

Challenges

UK nuclear market

Key part of energy mixKey part of energy mix

Market-driven approach

New build processNew build process

Addressing the challenges

2

AMEC’s position and strategy Sellafield panorama

Global nuclear marketCountries with nuclear power - 30; considering it - 20Countries with nuclear power 30; considering it 20

Nuclear countriesDeclared as interestedAMEC nuclear offices - main centres: UK

Hydro: 16%N l 14%

Coal: 41%G 21%

2008 global electricity

Oth 8% (~1,100 employees); Canada (~850)Nuclear: 14%Gas: 21% Others: 8%

SOURCE: WNA, IAEA

3

Note 1: Definition of ‘seriously considering’ varies between IAEA and WNA, twenty is the low figure (11 countries are ‘planning’ reactors, 5 more have ‘proposals’, others are ‘considering’ nuclear.)

Market size and driversMarket size and drivers

The numbers of planned and

New installed generating capacity after 2006 by geography (2007-2030)

GWeNet

proposed reactors in countries with existing nuclear power are constantly increasing

No of reactors

The number of countries with intent to launch nuclear programmes has increased significantly in the last 4 years

6 countries dominated nuclear market historically - represent 90market historically represent 90 percent of installed capacity

Asian countries will generate most th i t th f t

Source: AREVA estimatesgrowth into the future

B i i d l t l

* Source: WNA May 2010

4

Beginning a new and long-term cycle

Market structure and characteristics

Nuclear energy cycle Market structure

Sectors

Nuclear energy cycle

Chemistry

Enrichment Fuel fabrication

Players: countries, global OEM, nuclear utilities

Technologies: <10 globallyMining Clean up

New build

g g y

Market characteristics Political

Reactor support

Regulated

Competitive

Transmission

Distribution

End users

AMEC’s nuclear market areas

Additional AMEC activities

55

Investment costs, timelines*, and unit production costsproduction costs

Typical spend profile for a nuclear power plant (£m) Comparison of cost of electricity 1yp p p p p ( )

1500 4000Ph 3Ph 2Ph 1

25

p yp/kWh

1250

Spen

d (£

m)

2000

2500

3000

3500

ulat

ive

£m

Phase 3

Design, Construct & Commission

Phase 2

Definition, licensing,

public enquiry

Phase 1

GDA and Approvals1000

750

15

20

250

Ann

ual S

500

1000

1500

2000

Cum

750

500

5

10

00 1 2 3 4 5 6 7 8 9 10

Years

0

Annual spend

0

re w

ind

ith C

CS

ith C

CS

Biom

ass

CCG

T

re w

ind

Nucl

ear

N l i titi f l t i it

Source: Compiled from NIA published data

Cumulative spend

Offs

hor

Coal

wit

CCG

T w

i B

Ons

hor N

6

Nuclear is a competitive source of electricity* Approximate – for guideline only, using UK European Pressurised Reactor (EPR) 1 Parsons Brinkerhoff report 2010

Challengesg

Public opinion Safety, waste management, proliferation

Attraction of talent

N d i d l h i bili New designs and supply chain capability

Liberalised and volatile markets

C titi f F E t Competition from Far East

Cost

Length of process Length of process

Must continue to address challenges to ensure nuclear renaissance

7

Must continue to address challenges to ensure nuclear renaissance

Agendag

Global nuclear market

Size and drivers

Market structure and characteristics

Investment costs and timelines

Challenges

UK nuclear market

Key part of energy mixKey part of energy mix

Market-driven approach

New build processNew build process

Addressing the challenges

8

AMEC’s position and strategy Sellafield panorama

UK – nuclear a key part of energy mixUK nuclear a key part of energy mix

UK energy demand forecast to be 370TWh in 2020

Projections of (%) share of electricity t d b diff t (DECC)*370TWh in 2020

Reducing emissions by 34 percent by 2020 requires shift in energy mix

2 1 19

2008 2020

generated by different sources (DECC)*

Nuclear will remain a key part of UK energy mix

613

45 31

929

energy mix 10 plants currently operational

Aging nuclear fleet: 8 will close by 202532

822

Life extension opportunities limited Estimated energy demand today and in 2020 is 370TWh

*Assumes existing nuclear power stations are closed in line with published retirement dates and 1.6GW of new capacity is

GasCoalNuclearRenewablesOther sourcesNew build: 6 planned, 2 operational by

2020

f ‘

Source: DECC

dates and 1.6GW of new capacity is constructed by 2020 Oil

9

9Nuclear new build required to help fill UK’s ‘energy gap’

UK - market-driven approach to nuclear*pp

Labour built an environment that attracts nuclear investment

Regulatory framework

Processes to enable licensing and construction of reactors

Carbon pricing structure

Support skills development

Coalition government has signalled its continuing supportVincent de Rivas EDF's chief executive said:

"We welcome that the new Government has made clear its policy on nuclear energy through its commitment to practical t th t l t ti b ibl ”steps so that new nuclear construction becomes possible.”

Coalition government has signalled its continuing support

10

10g g g pp

*Very different to other countries – where nuclear is state funded or supported by significant subsidies etc

UK - new build process

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Department for Energy & Climate Change (DECC)

Operators

Nuclear Installations Inspectorate (NII)

KeyWaste & Decom. plans

Develop funding plans

Nuclear W

hi

Justification Infrastructure Planning Commission (IPC)

AMEC involvement

Generic Design Technology approvalite Paper (Ja

Generic Design Assessment

Sitelicensing

Technology approval

an 2008)

Planning Permission

Consent to operate

Designated National Policy StatementStrategic Site Assessment

g

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

PermissionProgramme Implementation

11

Typical 5yr decision and consents Typical 5yr construct / commission

UK - addressing the challengesg g

Skills base

Each nuclear plant needs approx 4,000 people to build Typically 700 people to operate and maintain

UK has an aging engineering base average age 50 years* UK has an aging engineering base - average age 50 years*

Bridging the skills gap will require collaboration Government industry academiaGovernment, industry, academia

Waste (legacy and future)( g y ) NDA spending £73bn to decommission legacy UK sites

Future waste management addressed in new build planning process

Challenges must be addressed to maintain public support

12*Source: Gibson Review

Challenges must be addressed to maintain public support

Agendag

Global nuclear market

Size and drivers

Market structure and characteristics

Investment costs and timelines

Challenges

UK nuclear market

Key part of energy mixKey part of energy mix

Market-driven approach

New build processNew build process

Addressing the challenges

13

AMEC’s position and strategy Sellafield panorama

AMEC - nuclear a key sector today and in future

AMEC 2009 revenue by sectorNuclear* 10%

Natural Resources

Transmission &

Conventional Power 5%

Nuclear* 10% Power & Process

Earth & Environmental

Mining 9%

Distribution 6%

Oil Sands 16%

W t /M i i l 3%

Renewables and Bioprocesses 6%

Oil & Gas 26%

Mining 3%Energy 2%

Water/Municipal 3%

Transport/Infrastructure 3%

Federal/State/Provisional 5%

p %Industrial/Commercial 3%

N l t i f f th t 2015

14

Nuclear sector is a focus for growth to 2015*Does not include the ‘equity accounted’ Sellafield contract

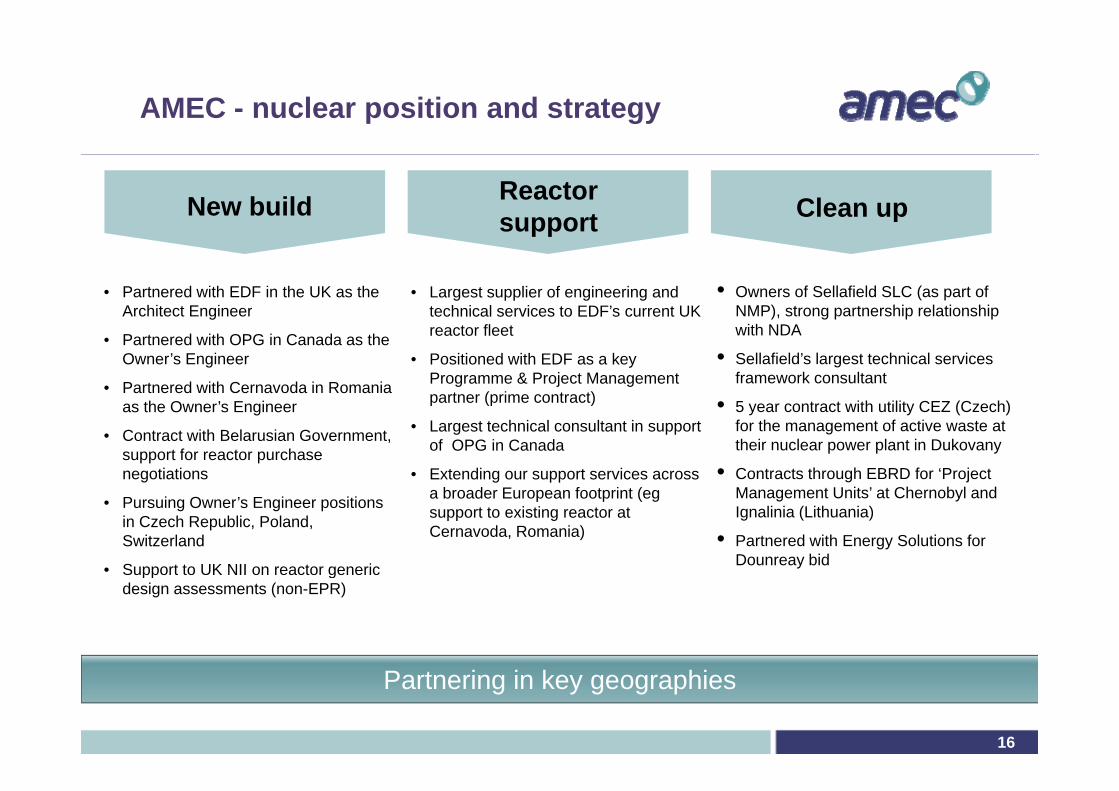

AMEC - nuclear position and strategy

ClReactor N b ild Clean upsupportNew build

Defend and grow leading position as the independent nuclear

Establish AMEC as a major UK nuclear clean up contractor (Tier 1) and long term partner to NDA

Establish AMEC as the utilities independent nuclear technology

t expert for existing reactors in current geographies

term partner to NDA

Pursue international growth priorities

partner

Assure the licensing, delivery and safe

UK, Canada, CEEoperation of the reactor and associated systems

Having a position in three segments is a competitive advantage

15

Having a position in three segments is a competitive advantage

AMEC - nuclear position and strategy

Clean upReactor tNew build Clean upsupport

• Owners of Sellafield SLC (as part of NMP) t t hi l ti hi

• Largest supplier of engineering and t h i l i t EDF’ t UK

• Partnered with EDF in the UK as the A hit t E i NMP), strong partnership relationship

with NDA

• Sellafield’s largest technical services framework consultant

technical services to EDF’s current UK reactor fleet

• Positioned with EDF as a key Programme & Project Management partner (prime contract)

Architect Engineer

• Partnered with OPG in Canada as the Owner’s Engineer

• Partnered with Cernavoda in Romania • 5 year contract with utility CEZ (Czech)

for the management of active waste at their nuclear power plant in Dukovany

• Contracts through EBRD for ‘Project

partner (prime contract)

• Largest technical consultant in support of OPG in Canada

• Extending our support services across

as the Owner’s Engineer

• Contract with Belarusian Government, support for reactor purchase negotiations

Management Units’ at Chernobyl and Ignalinia (Lithuania)

• Partnered with Energy Solutions for Dounreay bid

a broader European footprint (eg support to existing reactor at Cernavoda, Romania)

• Pursuing Owner’s Engineer positions in Czech Republic, Poland, Switzerland

• Support to UK NII on reactor generic pp gdesign assessments (non-EPR)

16

Partnering in key geographies

Summaryy

Nuclear renaissance is under way Long-term upward cycle – driven by climate change and security of supply

Opportunities in domestic markets and internationally

AMEC has a clear nuclear growth strategy Long-term partnering approach with customers and other major global supplierso g te pa t e g app oac t custo e s a d ot e ajo g oba supp e s

Selective geographic focus - where we can leverage existing strong relationships

Focus on synergies from three segments

AMEC positioned to engineer the change

17

AMEC positioned to engineer the change

QuestionsSellafield site investor trip: 21 June 2010Sellafield site investor trip: 21 June 2010

S l t i f tiSupplementary information• Opportunities across sectors• Europe ahead of North America

UK• UK• Canada• How a nuclear plant works• Reactor technology• Reactor technology

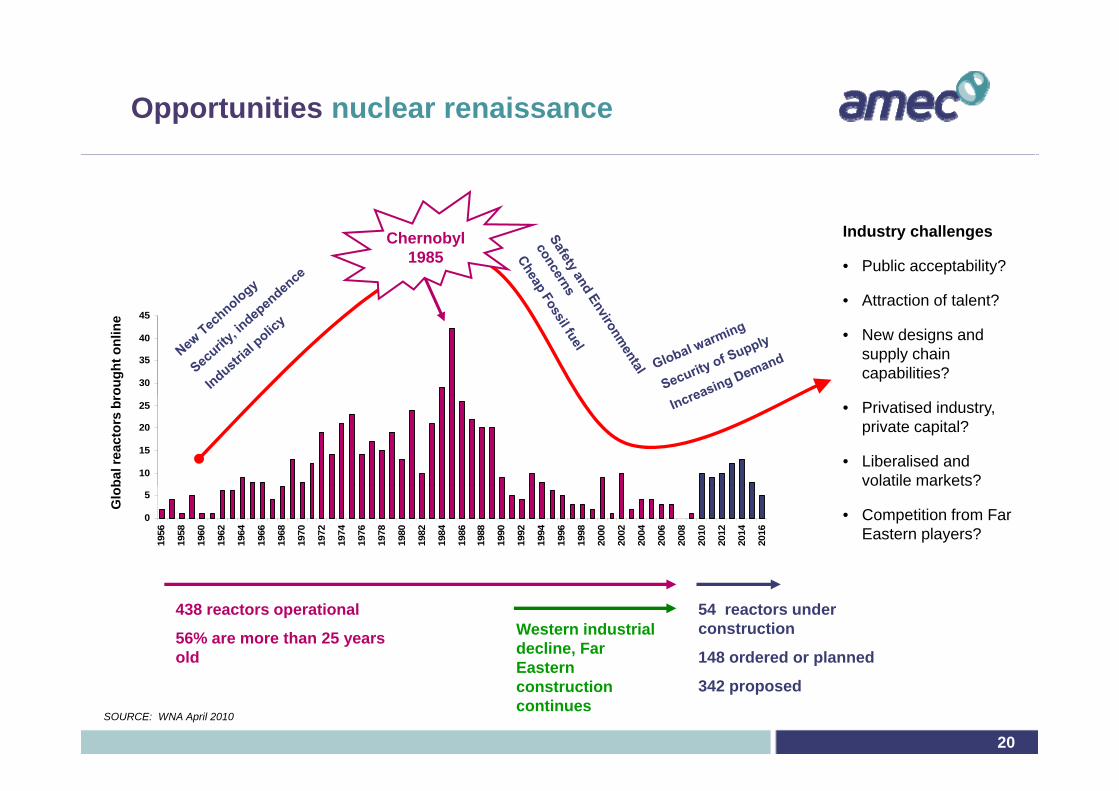

Opportunities nuclear renaissance

Chernobyl 1985

Industry challenges

• Public acceptability?

• Attraction of talent?

30

35

40

45

roug

ht o

nlin

e

• New designs and supply chain capabilities?

10

15

20

25

bal r

eact

ors

br • Privatised industry, private capital?

• Liberalised and volatile markets?

0

5

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Glo

b volatile markets?

• Competition from Far Eastern players?

54 reactors under construction

148 ordered or planned

438 reactors operational

56% are more than 25 years old

Western industrial decline, Far Eastern

20

p

342 proposed

SOURCE: WNA April 2010

Eastern construction continues

Opportunities reactor support

Maintaining and extending existing Number of operating reactor units by

Plant upgrades &

g g gfleet

Significant number of reactors to be supported and extended

p g yage (Jan 08)

No. of Reactors

Plant upgrades & life extension

pp

Services

Lifetime support

Operational Support

pp

Operational performance

Reactor servicing

21

More than 40 per cent of the fleet is more than 25 years old

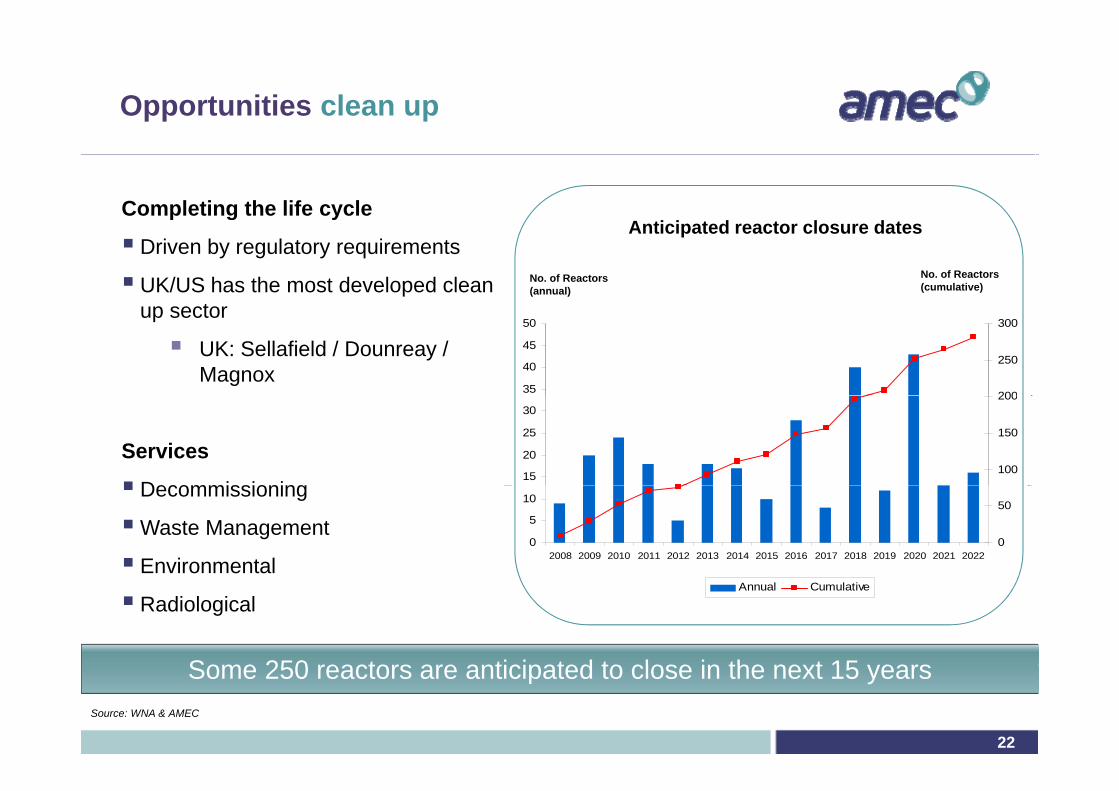

Opportunities clean up

Completing the life cyclep g y

Driven by regulatory requirements

UK/US has the most developed clean t

Anticipated reactor closure dates

No. of Reactors (annual)

No. of Reactors (cumulative)

up sector

UK: Sellafield / Dounreay / Magnox

Anticipated Reactor Closure Dates

35

40

45

50

Annu

al

200

250

300

umul

ativ

e

Services

Decommissioning15

20

25

30

ber o

f Rea

ctor

s -

100

150

200

er o

f Rea

ctor

s - C

u

Decommissioning

Waste Management

Environmental0

5

10

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Num

b

0

50

Num

be

Radiological

Some 250 reactors are anticipated to close in the ne t 15 ears

Annual Cumulative

22

Source: WNA & AMEC

Some 250 reactors are anticipated to close in the next 15 years

Opportunities – estimated size

New build

AREVA scenario for global installed capacity(GWe)

Reactor support

2020 global market estimate ~

2020 global market estimate ~

£18bn

600

700 Clean up

2020 global market estimate ~

£16bn

market estimate £55bn ~270 reactors ~630 reactors

358

72

400

500

438 reactors ~80 reactors

220 reactors 659

373 190

72

200

300~220 reactors

0

100

2008 Plant closures Life extensions New build 2030

23

2008 Plant closures Life extensions New build 2030

Sources: AREVA (WNA, USDoE, World Energy Outlook) Market estimates from AMEC analysis.

Nuclear increasingly competitive source of clean energyof clean energy

Comparison of greenhouse gas emissions

1400

gCO2 eq/kWh

Today

1000

1200 By 2050?

Today

600

800

200

400

600

0

200

Coal Gas Nuclear

24SOURCES: IAEA 2006, Paul Scherrer Institute 2003

Renaissance - Europe ahead of North America

New reactors under construction

New reactors plannedEurope

p• Primary drivers are real security of supply concerns and strong

environmental support across EU

• Olkiluoto 3 under construction in Finland, Flamanville 3 under construction in France

• Six reactors planned in UK, sites identified, consortia formed

• Feasibility studies by ENEL/EDF in Italy

• Tenders for two reactors issued in Czech Republic.

North America

• Primary drivers weaker, but growing security and environmental concerns

• Short lists for federal loan guarantees

• Duke Energy and others in negotiation with suppliers• Duke Energy and others in negotiation with suppliers

• Licence applications for 26 reactors since 2007

• Renaissance was signalled by the return to service of Bruce units 1 and 2 (Canada) and the restart of suspended construction

25

( ) pof Watts Bar (USA)

SOURCE: WNA, AREVA

Europe is investing - France

Fl ill 3Flamanville 3

26All photos copyright AREVA

Europe is investing - Finland

Olkiluoto 3

27All photos copyright AREVA

UK - committed to new build

UK government approved 10 ‘new build’ sites1. Bradwell, Essex, NDA sold to EDF Energy

2. Braystones, Cumbria, NDA sold to RWE npower

3. Hartlepool, Durham, EDF Energy

Proposed

Operating

Shut downp gy

4. Heysham, Lancashire, EDF Energy

5. Hinkley Point, Somerset, NDA sold to EDF Energy

6 Kirksanton Cumbria NDA sold to RWE npower6

4

328

6. Kirksanton, Cumbria, NDA sold to RWE npower

7. Oldbury, Gloucestershire, NDA sold to Horizon*

8. Sellafield, Cumbria, NDA sold to Iberdrola/SSE/GDF-Suez

4

10

9. Sizewell, Suffolk, EDF Energy

10.Wylfa, Anglesey, sold by NDA to Horizon*7

5

91

Nuclear energy required to fill UK’s ‘energy gap’

28

*RWE npower & EON UKSource: DECC

28

Nuclear energy required to fill UK s energy gap

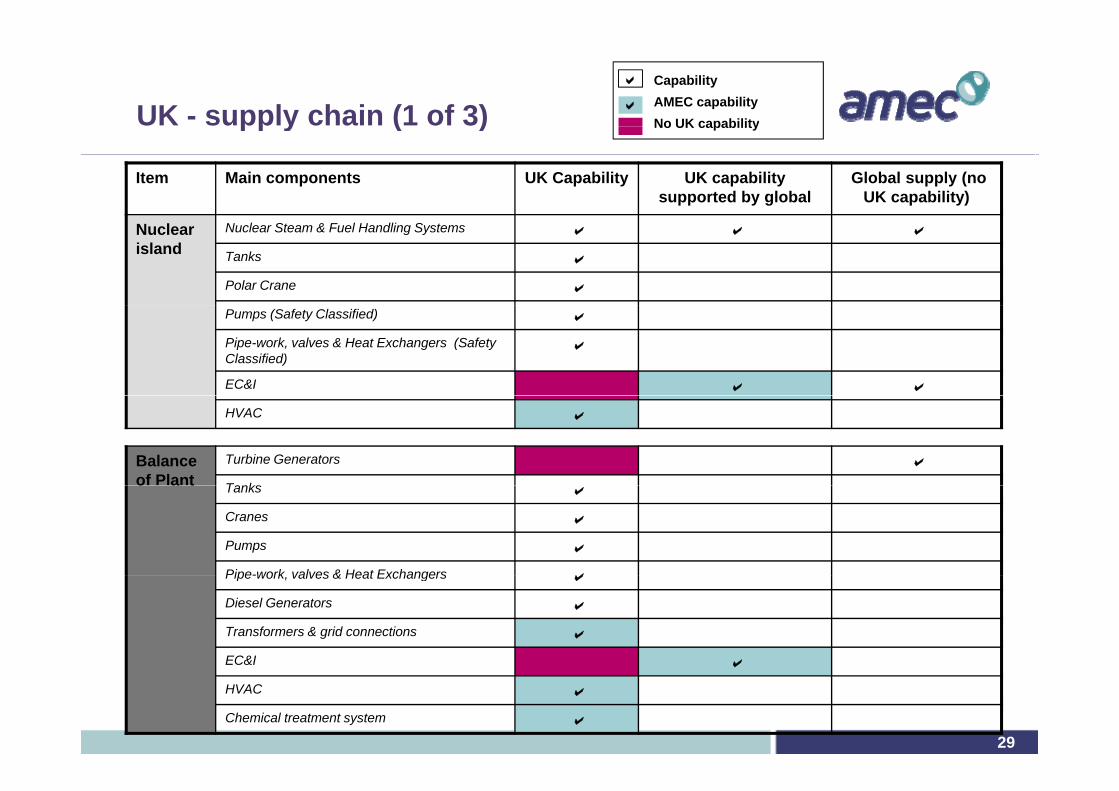

UK - supply chain (1 of 3) Capability

AMEC capabilityNo UK capability

pp y ( )

Item Main components UK Capability UK capability supported by global

Global supply (no UK capability)

No UK capability

Nuclear island

Nuclear Steam & Fuel Handling Systems Tanks Polar Crane Pumps (Safety Classified) Pipe-work, valves & Heat Exchangers (Safety Classified)

EC&I HVAC

Balance of Plant

Turbine Generators Tankso a t Tanks Cranes Pumps Pipe-work valves & Heat Exchangers Pipe-work, valves & Heat Exchangers Diesel Generators Transformers & grid connections EC&I

29

C& HVAC Chemical treatment system

UK - supply chain (cont 2 of 3)pp y ( )

CapabilityAMEC capability

Item Main components UK Capability UK capability supported by global

Global supply (no UK capability)

p yNo UK capability

Pre build Planning & licensing

Legal & financial services

Nuclear consultancy services Engineering & design services

Construction Project management Construction j g Building & construction Plant & Equipment On-site erection / fabrication Nuclear Island Nuclear fuel supply Commissioning – Nuclear island

30

g Commissioning BoP

UK supply chain (cont 3 of 3)pp y ( )

CapabilityAMEC capability

Item Main components UK Capability

UK capability supported by global

Global supply (no UK capability)

p yNo UK capability

Operation Operations

Nuclear fuel supply

Engineering / technical services Waste management & disposal

Decommissi Planning & licensing oning Decommissioning

31

Canada – nuclear is a pivotal part of energy mix

Nuclear will continue to be key to Canada’s economy and energy mix Approx 15 percent of Canada's electricity from nuclear powerApprox. 15 percent of Canada s electricity from nuclear power

– 18 reactors in three provinces provided over 12,600 MWe of power capacity

Committed to reducing emissions by 25 percent by 2020 – Ontario phasing out coal fuelled power generation by 2014– Ontario phasing out coal-fuelled power generation by 2014– Aging power facilities: 80 percent power plants in Ontario to be replaced or refurbished

in next 20 years

Canada produces over 50 percent of the world’s medical isotopes Approx. 33 percent of world’s uranium found in Saskatchewan

RefurbishmentRefurbishment Projects estimated at CDN$9+ billion CDN are currently underway or have been

announced– Ontario (~$6 billion)O a o ( $6 b o )– New Brunswick (~$1.4 billion)– Quebec (~$1.9 billion)

32

Canada is one of AMEC’s core nuclear markets

Canada – existing and planned

22 CANDU nuclear reactors, 17 operational as of 1 April 2008

New build: 9 planned by 2020 (potentially) Ontario, New Brunswick, Alberta and Saskatchewan

Hydro Quebec (1 operating unit)• Gentilly 2: operational

OPG* (10 operating units)• Pickering A 2&3: safe shut down

Pi k i A 1&4 ti l 1

3

New Brunswick Power (1 unit under refurbishment)

• Point Lepreau: undergoing

• Pickering A 1&4: operational• Pickering B 5-8: operational• Darlington 1-4: operational 2

5

• Point Lepreau: undergoing refurbishmentBruce Power (6 operating units)

Bruce A 1&2: under restart programBruce A 3&4: operational (next to refurbish)

4

Bruce A 3&4: operational (next to refurbish)Bruce B 5-8: operational

3

33

41

2

3

5

How a nuclear power plant works

CONVENTIONAL ISLAND

NUCLEAR ISLAND

34Source: BBC news website

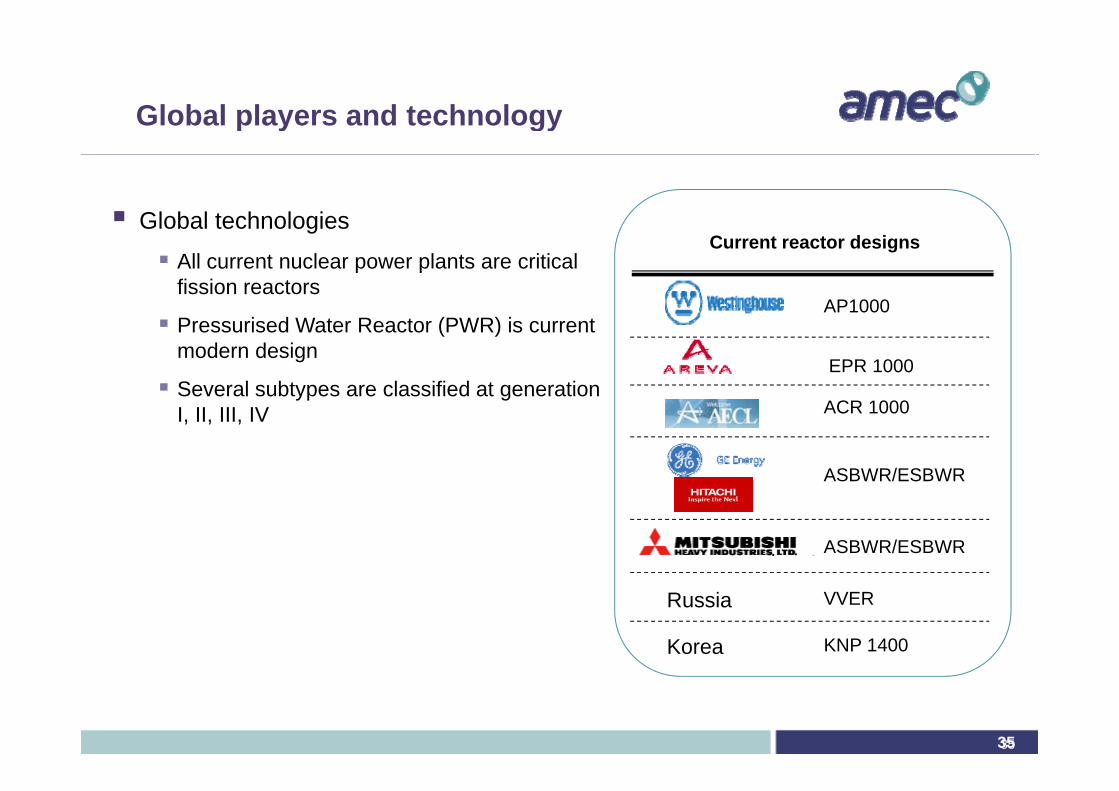

Global players and technologyp y gy

Global technologies

AP1000

Current reactor designs Global technologies

All current nuclear power plants are critical fission reactors

AP1000

EPR 1000

Pressurised Water Reactor (PWR) is current modern design

Several subtypes are classified at generationACR 1000

ASBWR/ESBWR

Several subtypes are classified at generation I, II, III, IV

ASBWR/ESBWR

Russia VVER

Korea KNP 1400

3535

Technologygy

N l fi i t d h t

Diablo Canyon (PWR)

Nuclear fission reactors produce heat through a controlled nuclear chain reaction in a critical mass of fissile materialmaterial

There are several subtypes of critical fission reactors, classified as Generation I, Generation II and

Superfenix (FBR)

Ignalina (RBMK) Ge e at o , Ge e at o a dGeneration III.

Igana Verde (BWR)

Q i h (CANDU)Torness (AGR) Sizewell A (Magnox) Quinshan (CANDU)

3636