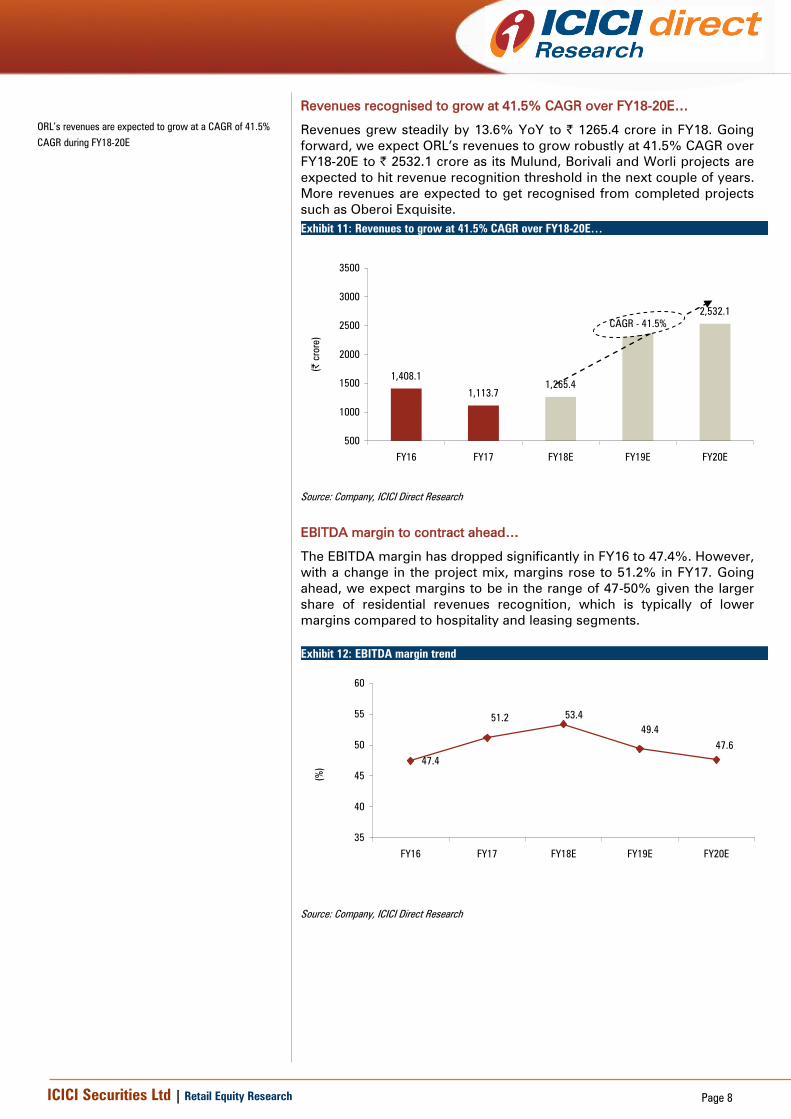

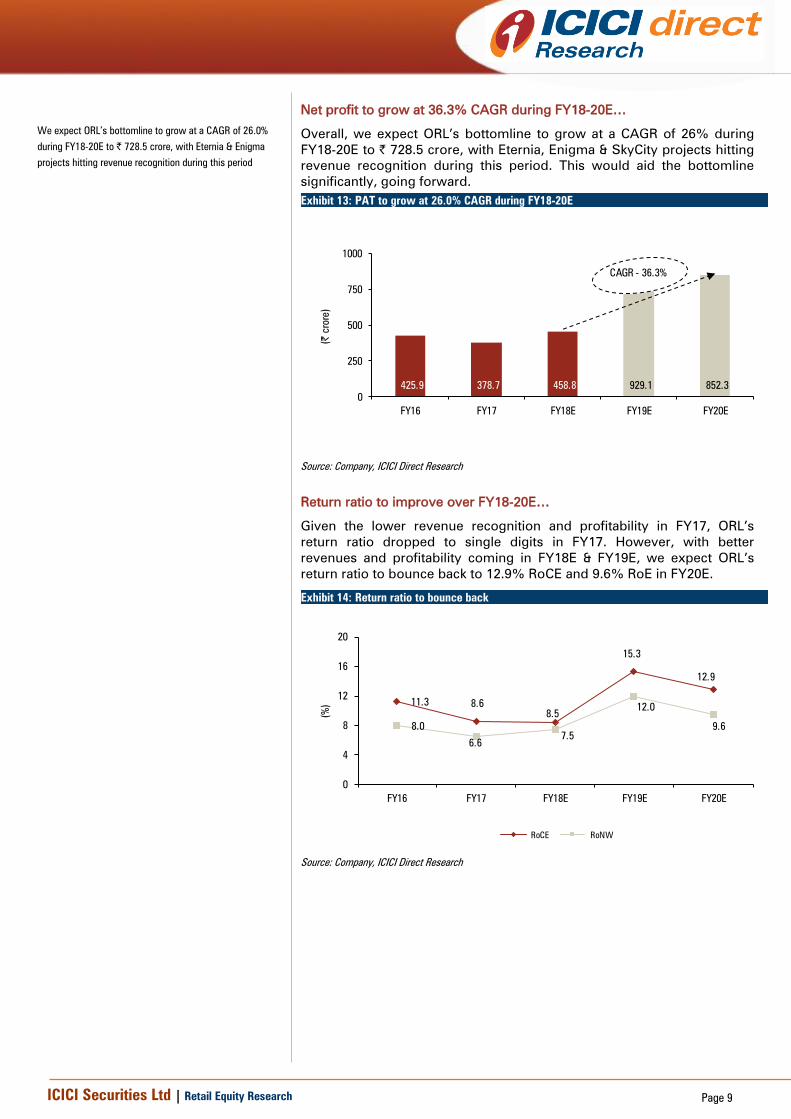

April 26, 2018 ICICI Securities Ltd | Retail Equity Research Result Update Healthy launch pipeline ahead… Oberoi Realty's Q4FY18 sales performance was below our estimate mainly due to subdued sales in Worli project. On the financials front, the results were above our estimates on the topline, bottomline front Oberoi Realty's (ORL) Q4FY18 sales volumes fell 13.6% sequentially to 1.31 lakh sq ft with sales value of | 263.3 crore. Sales volume was below our estimates of 1.66 lakh sq ft due to lower-than-expected sales of 9562 sq ft in Worli project (our expectation: 50000 sq ft) Revenues grew robustly by 19.1% YoY to | 345.0 crore and were slightly above our estimate of | 338.3 crore EBITDA margins expanded 80 bps YoY to 53.1% mainly on account of a change in the project mix. It was below our expectation of 54.3% PAT grew 40.4% YoY to | 142.9 crore (our estimate: | 114.4 crore) primarily due to topline growth and EBITDA margin expansion The board recommended a dividend of | 2 Sales volumes decline 13.6% QoQ to 1.31 lakh sq ft… ORL’s sales volumes de-grew 13.6% QoQ to 1.31 lakh sq ft in Q4FY18 due to the poor performance of the Worli project with sales volumes of 9562 sq ft (our expectation: 50000 sq ft). Overall, in FY18, sales volumes grew 3.9% YoY to 5.9 lakh sq ft. Going forward, the company a has strong launch pipeline in FY19E, with launches planned at Thane, Exquisite III in Goregaon and subsequent phases of Borivali, Mulund projects. Consequently, we expect sales volumes could grow at a healthy pace of 53.8% CAGR from 0.6 msf in FY18 to 1.3 msf in FY20E. Board passes enabling resolution… The board has passed an enabling resolution to issue non-convertible debentures up to | 1500 crore by way of private placement and also issue equity shares and/or any other securities convertible into equity worth ~| 2000 crore including premium, by way of one or more qualified institutions placement to qualified institutional buyers. The company could raise and use these funds, going ahead, in case it sees some good land acquisition opportunity in the market. Revenue recognition from new projects to boost bottomline… The management indicated the timelines for revenue recognition threshold timelines for different projects. It expects SkyCity to reach threshold in H1FY19, Eternia in H1FY19E, Enigma in Q2/Q3FY19E. Consequently, we expect the company to post healthy topline, PAT growth of 41.5%, 26.0% CAGR to | 2532.1 crore, | 728.5 crore, respectively, over FY18-20E. Occupancy to improve in Commerz II in FY19E… Recently, for Commerz II, the company has leased four more floors worth 0.7 lakh sq ft taking occupancy to ~63-64% (47.4% in Q4FY18). For the Worli mall (on Glaxo land), work has started. ORL plans to complete it by 2020. The Borivali mall is at the design stage while some excavation work has started. Await better entry point; maintain HOLD… We like the company given the quality of land bank, its healthy balance sheet and management bandwidth to execute large projects. However, the sales momentum for ORL has been sluggish. Also, the stock has run up ~41% in the last one year. Hence, we await a better entry point. Consequently, we continue to maintain our HOLD recommendation on the stock with a revised target price of | 550. Rating matrix Rating : Hold Target : | 550 Target Period : 12 months Potential Upside : -4% What’s Changed? Target Changed from | 490 to | 550 EPS FY19E Changed from | 27.7 to | 24.3 EPS FY20E Changed from | 24.0 to | 21.5 Rating Unchanged Quarterly Performance | crore Q4FY18 Q4FY17 YoY (%) Q3FY18 QoQ (%) Revenue 344.9 289.5 19.1 356.2 -3.2 EBITDA 183.3 151.5 21.0 192.6 -4.8 EBITDA (%) 53.1 52.3 83 bps 54.1 -93 bps PAT 142.9 101.8 40.3 120.2 18.9 Key Financials | Crore FY17 FY18E FY19E FY20E Net Sales 1,113.7 1,265.4 2,674.1 2,532.1 EBITDA 569.9 675.3 1,320.6 1,204.8 Net Profit 378.7 458.8 929.1 852.3 EPS (|) 11.2 13.5 27.4 25.1 Valuation summary (x) FY17 FY18E FY19E FY20E P/E 51.2 42.3 20.9 22.7 Target P/E 49.3 40.7 20.1 21.9 EV / EBITDA 31.7 27.3 13.0 14.2 P/BV 3.4 3.2 2.8 2.5 RoNW (%) 6.6 7.5 12.0 9.6 RoCE (%) 8.6 8.5 15.3 12.9 Stock data Particular Amount (| crore) Market Capitalization 19,387.5 Total Debt 901.6 Cash 1,763.0 EV 18,526.1 52 week H/L (|) 609 / 339 Equity capital 328.2 Face value (|) 10.0 Price performance (%) Return % 1M 3M 6M 12M Sunteck Realty 12.2 10.1 23.5 105.8 Oberoi Realty 21.0 4.2 21.7 40.9 Sobha Ltd 16.3 (4.6) 1.3 39.3 Mahindra Lifespace 7.9 (13.3) (3.6) 12.2 BSE Realty 8.1 (10.8) 9.2 21.8 Research Analyst Deepak Purswani, CFA [email protected]Vaibhav Shah [email protected]Oberoi Realty (OBEREA) | 571

Transcript

April 26, 2018

ICICI Securities Ltd | Retail Equity Research

Result Update

Healthy launch pipeline ahead…

Oberoi Realty's Q4FY18 sales performance was below our estimate

mainly due to subdued sales in Worli project. On the financials front,

the results were above our estimates on the topline, bottomline front

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Bloomberg, Company, ICICI Direct Research

Key events

Date Event

Jun-15 Oberoi Realty approves raising of | 324 crore through preferential issue of shares to Aranda Investments, an indirect subsidiary of Temasek Holdings

Aug-15 As per media sources, Oberoi Realty to buy Crompton Greaves’ Worli building spread over ~1 acre for over | 200 crore.

Oct-15 Oberoi Realty launches its multi-tower project “Sky City” at Borivali spread across 25 acres consisting of multiple towers of up to 60 storeys each. The project has a

saleable area of ~4.5 million square feet (msf) and the company expects to earn revenues of ~| 6000-7000 crore from the project

Mar-16

The Bombay High Court stays new constructions of either residential/commercial buildings or hotels in Mumbai from March 1, 2016 because the state government

and Brihanmumbai Municipal Corporation (BMC) have failed to comply with the municipal solid waste (MSW) rules at Deonar and Mulund dumping grounds,due to

which Oberoi will be unable to launch projects until the ban is lifted

Mar-16 Rajya Sabha passes the real estate regulation bill paving the way for regulation in the real estate sector. The bill would promote timely execution of projects, ensure

speedy adjudication of disputes and help promote private participation, positive for Oberoi

Apr-16 Swedish furniture retailing giant Ikea in talks with Oberoi Realty to buy a built-to-suit retail space for over | 900 crore in Borivali. As per media reports, if the deal

happens, this will monetise Oberoi's landbank at better prices of ~| 112.5 crore per acre vs. Oberoi's acquisition price of ~| 46.2 crore per acre

May-16 Oberoi allots 59,104 equity Shares of | 10 each to certain option grantee(s) pursuant to exercise by them of options granted to them under Company’s Employee

Stock Option Scheme 2009. The exercise price for options is | 260/ share. Post allotment, share capital has increased to | 339.4 crore.

Aug-16

According to media sources, Oberoi Realty is in talks with US-based investor Morgan Stanley and Singapore’s sovereign fund, GIC, to set up a joint venture (JV) for

developing malls. The venture would have a corpus of | 1,000 crore. Oberoi is expected to hold about 75%. Further, it could also initiate talks with Canada Pension

Plan Investment Board, which has shown an interest in buying in malls

Sep-16 Teva Pharmaceuticals buys ~1.0 lakh sq ft space in Oberoi Commerz II in Goregaon

Mar-17 Samsung India Electronics leases ~1.1 lakh sq ft space in Oberoi Commerz II in Goregaon for ~| 145/ sq ft per month. The lease is for nine years with 15% rental

escalation every three years

Sep-17 Oberoi Realty has acquired GlaxoSmithKline (GSK) Pharmaceuticals’ 60 acre land parcel at Thane for | 555 crore.

Source: Company, ICICI Direct Research

Top 10 Shareholders Shareholding Pattern

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Oberoi (Vikas Ranvir) 31-Mar-18 62.7% 212.9 0.0

2 R S Estate Developers Pvt. Ltd. 31-Mar-18 9.8% 33.3 0.0

3 Franklin Templeton Investment Management Ltd. 31-Mar-18 3.1% 10.4 0.0

ICICI Securities Ltd | Retail Equity Research Page 15

ANALYST CERTIFICATION

We /I, Deepak Purswani, CFA MBA (Finance), Vaibhav Shah, MBA (Finance); Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views

about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered Research Analyst

with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management,

life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a

significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or

derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may

not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information

herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate

that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to

this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for

informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report

constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable

for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any

recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before

investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public

offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the

companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of

this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Vaibhav Shah, MBA (Finance); Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research

report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report.

It is confirmed that Deepak Purswani, CFA MBA (Finance), Vaibhav Shah, MBA (Finance); Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be

contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.