15

Oct 2008 The Brazilian Economy

| Date post: | 05-Jan-2016 |

| Category: |

Documents |

| Upload: | adelia-barber |

| View: | 222 times |

| Download: | 0 times |

Oct 2008

The Brazilian Economy

Global Slowdown …

World Growth

1%

2%

3%

4%

5%

6%

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

1%

2%

3%

4%

5%

6%

Base caseStressOptimistic

Global Slowdown …

World Growth (2009, %)

0.3 0.5

8.5

-0.5

7.5

0.7

0

1.3

9.2

-2

0

2

4

6

8

10

USA Euro Area China

base case

stress

optimistic

Commodity Prices to Fall…

Last Quarter 2008 2009Baseline 384 345

% baseline vs last price -2% -12%Stress 376 305 % stress vs last price -4% -22%

Last price (07/10): 392

…affecting Brazil

Stress: Direct effect (lower export growth)

Stress: Total effect (lower export growth,

consumption and investment)

GDP growth (4Q/4Q, %)

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

4T

-07

1T

-08

2T

-08

3T

-08

4T

-08

1T

-09

2T

-09

3T

-09

4T

-09

1T

-10

2T

-10

3T

-10

4T

-10

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Base case

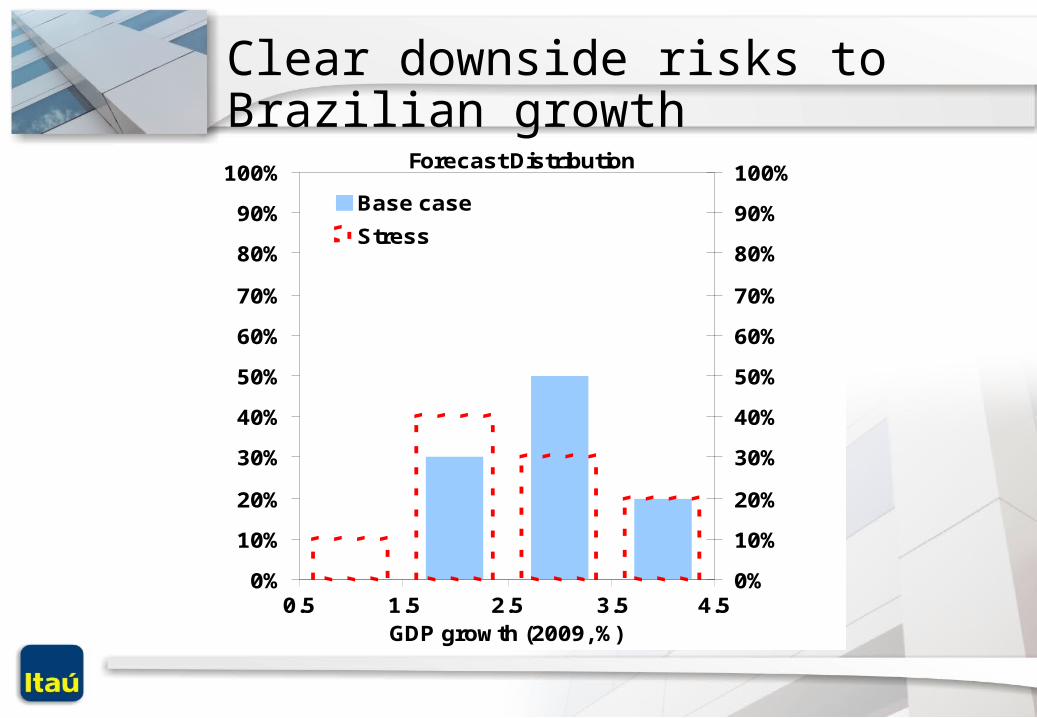

Clear downside risks to Brazilian growth

Forecast Distribution

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Base case

Stress

GDP growth (2009, %)1.5 2.5 3.5 4.50.5

Expanding potential output

Potential GDP growth (4Q/4Q)

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

4Q-9

6

2Q-9

7

4Q-9

7

2Q-9

8

4Q-9

8

2Q-9

9

4Q-9

9

2Q-0

0

4Q-0

0

2Q-0

1

4Q-0

1

2Q-0

2

4Q-0

2

2Q-0

3

4Q-0

3

2Q-0

4

4Q-0

4

2Q-0

5

4Q-0

5

2Q-0

6

4Q-0

6

2Q-0

7

4Q-0

7

2Q-0

8

productivity

capital

human capital

natural capital utilization

natural unemployment rate

potential output

Public Debt

Premises:

Social security expenses, transferences to state and local governments and wages are considered rigid, they represent 2/3 of total expenditures. Other expenditures growth with GDP.

GDP growth of 2.8% in 2009 and 2010.

Currency devaluation impact is considered with an exchange rate of R$/US$ 2.0

Public Debt

34%

36%

38%

40%

42%

44%

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

% GDP

Surplus=4.30 USD=1.64R$

Surplus=4.30 USD=2.00R$

Surplus=3.82 USD=2.00R$

GDP Growth (%)Primary Surplus

(%GDP)2.5 3.752.8 3.823,0 3.863.5 3.974,0 4.085,0 4.30

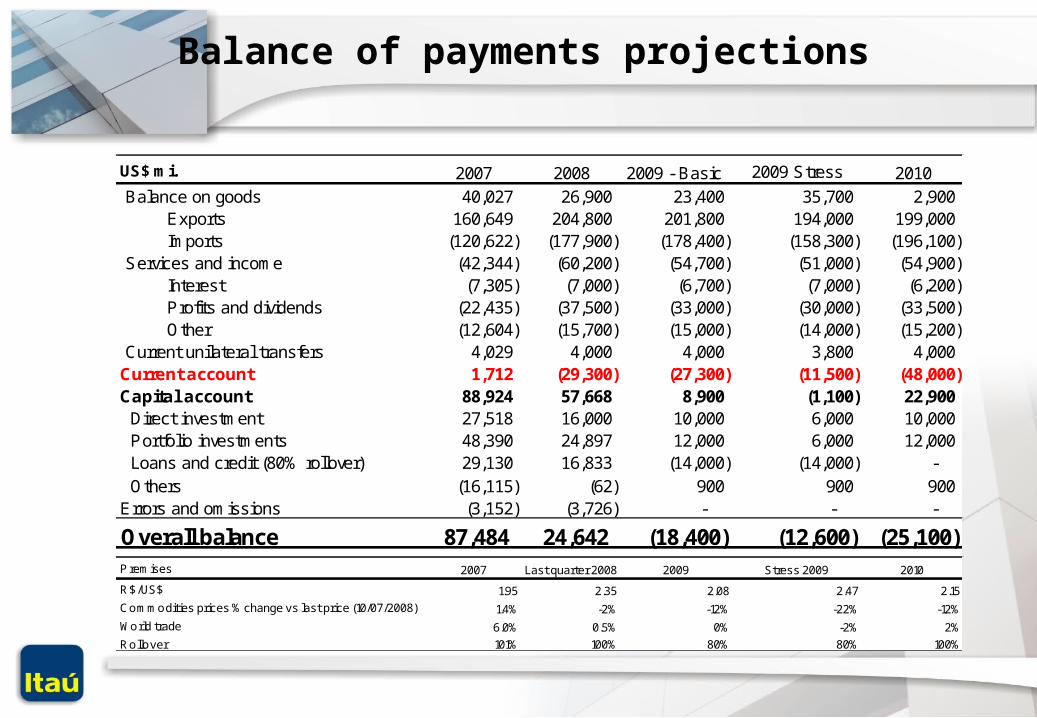

Balance of payments projections

US$ mi. 2007 2008 2009 - Basic 2009 Stress 2010 Balance on goods 40,027 26,900 23,400 35,700 2,900 Exports 160,649 204,800 201,800 194,000 199,000 Imports (120,622) (177,900) (178,400) (158,300) (196,100) Services and income (42,344) (60,200) (54,700) (51,000) (54,900) Interest (7,305) (7,000) (6,700) (7,000) (6,200) Profits and dividends (22,435) (37,500) (33,000) (30,000) (33,500) Other (12,604) (15,700) (15,000) (14,000) (15,200) Current unilateral transfers 4,029 4,000 4,000 3,800 4,000 Current account 1,712 (29,300) (27,300) (11,500) (48,000) Capital account 88,924 57,668 8,900 (1,100) 22,900 Direct investment 27,518 16,000 10,000 6,000 10,000 Portfolio investments 48,390 24,897 12,000 6,000 12,000 Loans and credit (80% rollover) 29,130 16,833 (14,000) (14,000) - Others (16,115) (62) 900 900 900 Errors and omissions (3,152) (3,726) - - -

Overall balance 87,484 24,642 (18,400) (12,600) (25,100) P remises 2007 Last quarter 2008 2009 Stress 2009 2010

R$/US$ 1.95 2.35 2.08 2.47 2.15Commodities prices % change vs last price (10/07/2008) 1.4% -2% -12% -22% -12%World trade 6.0% 0.5% 0% -2% 2%Rollover 101% 100% 80% 80% 100%

Brazilian liabilities(US$ bi.) 142

70 59

-

20

40

60

80

100

120

140

160

Equity in Brazil ¹ Debt maturing in 12months²

Domestic bonds ¹

1- Itaú estimated data of Sep/08 - R$/US$ 2.2 2- Central Bank estimated data of Aug/08

Brazilian Liabilities

Policy Options

• The central bank is addressing the scant international credit lines instead of wide intervention on the exchange rate

• Monetary policy faces the challenge of keeping inflation on target in an uncertain international environment.

• The prudent decision is to adopt a wait and see stance • Tighter fiscal policy may help to avoid crowding out of

private investment

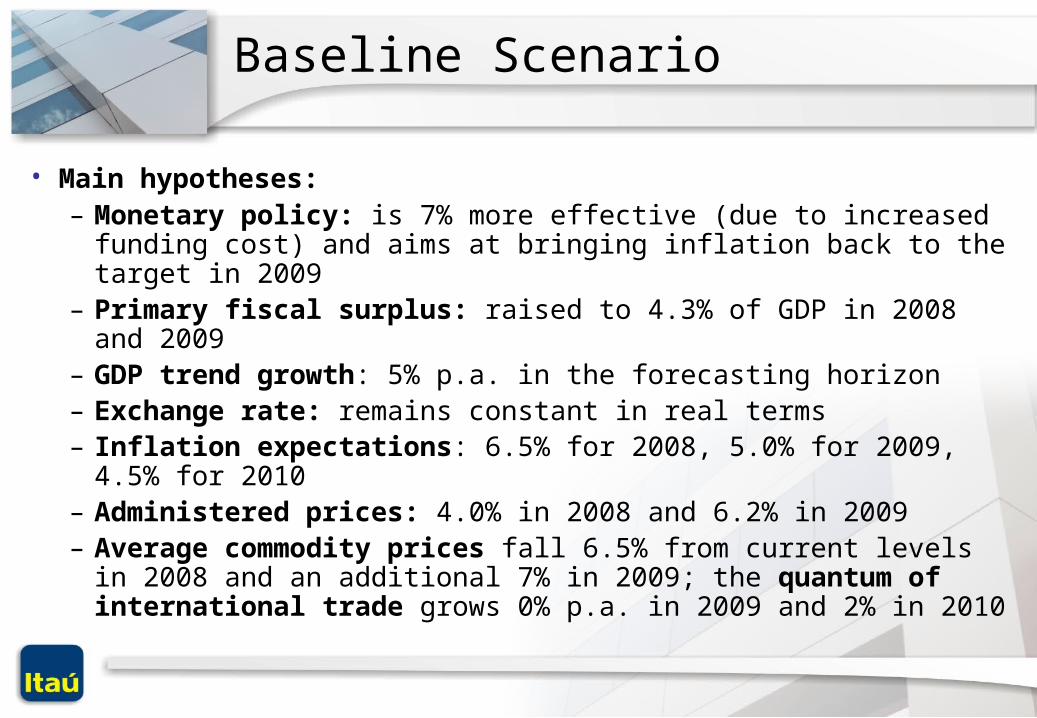

Baseline Scenario

• Main hypotheses: – Monetary policy: is 7% more effective (due to increased funding

cost) and aims at bringing inflation back to the target in 2009– Primary fiscal surplus: raised to 4.3% of GDP in 2008 and 2009– GDP trend growth: 5% p.a. in the forecasting horizon– Exchange rate: remains constant in real terms– Inflation expectations: 6.5% for 2008, 5.0% for 2009, 4.5% for 2010– Administered prices: 4.0% in 2008 and 6.2% in 2009– Average commodity prices fall 6.5% from current levels in 2008 and

an additional 7% in 2009; the quantum of international trade grows 0% p.a. in 2009 and 2% in 2010

Baseline Scenario

Period Nominal Interest CPI (IPCA) IGP-M Real Real CDS

exchange rate inflation inflation GDP growth interest Brazil

rate target y-o-y y-o-y y-o-y rate y-o-y 5 y

Year Q (BRL/USD) (% p.a.) (%) (%) (%) (%) (bp)

2007 4 1.79 11.25 4.46 7.75 5.4 7.3 96

2008 1 1.74 11.25 4.73 9.10 5.8 6.6 149

2008 2 1.66 11.80 6.06 13.44 6.0 5.1 110

2008 3 1.67 12.97 6.25 12.31 5.8 5.4 139

2008 4 2.00 13.97 6.49 12.32 5.3 5.8 210

2009 1 2.01 14.25 6.57 11.64 4.6 6.6 210

2009 2 2.02 14.25 5.58 8.41 3.7 8.2 202

2009 3 2.04 13.99 5.62 8.02 3.1 8.4 195

2009 4 2.05 13.24 4.45 5.09 2.9 9.5 188

2010 1 2.07 12.23 4.10 4.74 3.2 9.3 181

2010 2 2.09 11.51 3.85 4.46 3.9 8.9 174

2010 3 2.10 11.00 4.09 4.72 4.6 7.9 168

2010 4 2.12 10.48 4.60 5.28 4.8 6.7 162

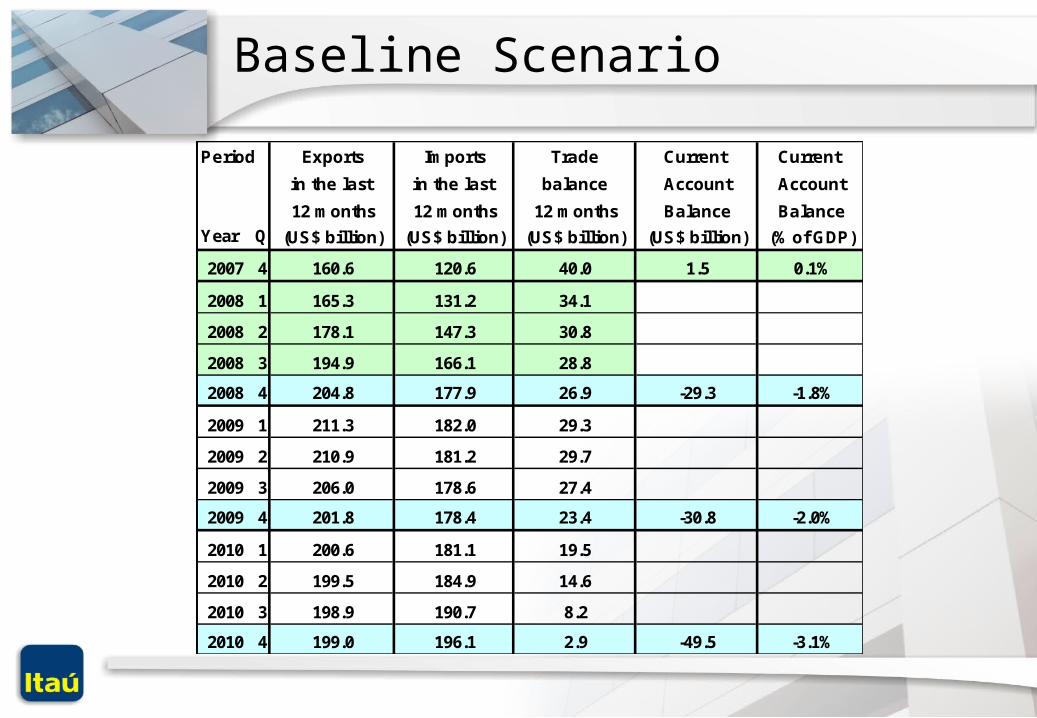

Baseline Scenario

Period Exports Imports Trade Current Current

in the last in the last balance Account Account

12 months 12 months 12 months Balance Balance

Year Q (US$ billion) (US$ billion) (US$ billion) (US$ billion) (% of GDP)

2007 4 160.6 120.6 40.0 1.5 0.1%

2008 1 165.3 131.2 34.1

2008 2 178.1 147.3 30.8

2008 3 194.9 166.1 28.8

2008 4 204.8 177.9 26.9 -29.3 -1.8%

2009 1 211.3 182.0 29.3

2009 2 210.9 181.2 29.7

2009 3 206.0 178.6 27.4

2009 4 201.8 178.4 23.4 -30.8 -2.0%

2010 1 200.6 181.1 19.5

2010 2 199.5 184.9 14.6

2010 3 198.9 190.7 8.2

2010 4 199.0 196.1 2.9 -49.5 -3.1%