T he Green Sheet Web site, www.greensheet.com, has recently undergone some significant upgrades. As a result of the new functions with faster processing time, the site and its services are enjoying an average of more than 15,000 hits a day 1 . Contributing to the success of the family of online services is the revamped ISO Forum. More interactive and stream- lined than its predecessor, the forum sports a new look and feel. In this grow- ing community of friends, associates and newbies, there is an unparalleled wealth of information and insight. The strength of the site is not in reckless self-promotion but in the amount of rel- evant industry news and data that ISOs can put into action. With a click, visitors can get the most up- to-date trends in smart cards, equipment, H ave you been piecing together all the news about debit cards over the last year? We are all aware of the battle in which the nation’s major retailers are challenging Visa’s requirement that merchants accepting credit cards with the Visa brand also must accept Visa-branded debit cards. Major retailers like Wal-Mart believe that the interchange rate for debit cards is much higher than the actual risk that Visa members are exposed to, and Wal-Mart, the Publix grocery chain and other retailers have filed a class-action suit seeking damages. While the judge has not yet ruled on the merits of the suit, Visa recently offered a settlement with Wal-Mart and others, which they declined. Industry insiders speculate that the offer was made because Visa wants to be free to re-price debit card transactions. On another front, Wal-Mart, Publix and others have announced that they no longer will accept Interlink PIN- based debit cards. Interlink is a Visa USA-owned brand. This announce- ment came on the heels of Interlink’s announcement of an interchange price increase. Then another story came from the world of debit: the fact that Bank of America would be leaving the STAR ATM network, recently acquired by The Financial Services Industry Source for Education, Inspiration and Actionable Advice October 22, 2001 Issue 01:10:02 Inside This Issue: Notable Quote: Features Paper Trail of Check Presentment vs. Re-presentment by Brandes Elitch.............................9 Company Profiles Secure Payment Systems ....................29 GoEmerchant.com ............................34 Identico Systems................................41 News TeleCheck Names Drucker President and CEO .........................4 VeriFone is Back! ..............................17 NACHA Rule Finalized......................23 Alogent’s New International Headquarters ...............................27 Army Drafts Schlumberger.................28 New Products An A-Team for ISOs .........................47 360Commerce Steps Up Its Solutions ..................................49 Inspiration You’ve Got Mail ...............................57 Spinning the Perfect Web .................57 Departments Forum ................................................6 FYISOs .............................................51 Datebook .........................................58 Resource Guide ................................59 Web sites are there to add to customer satisfaction, not overwhelm and distract users from the ultimate goal – a sale. Remember, keep it simple. Story on Page 57 STAR Could Become the Visa of Debit Transactions GS Online Flexes Muscle to Empower Industry See STAR on Page 4

Transcript

The Green Sheet Web site,www.greensheet.com, hasrecently undergone somesignificant upgrades. As

a result of the new functions withfaster processing time, the site andits services are enjoying an averageof more than 15,000 hits a day1.

Contributing to the success of the familyof online services is the revamped ISOForum. More interactive and stream-lined than its predecessor, the forumsports a new look and feel. In this grow-ing community of friends, associates andnewbies, there is an unparalleled wealthof information and insight.

The strength of the site is not in recklessself-promotion but in the amount of rel-

evant industry news and data that ISOscan put into action.

With a click, visitors can get the most up-to-date trends in smart cards, equipment,

Have you been piecingtogether all the newsabout debit cards overthe last year?

We are all aware of the battle inwhich the nation’s major retailersare challenging Visa’s requirementthat merchants accepting creditcards with the Visa brand also mustaccept Visa-branded debit cards.Major retailers like Wal-Martbelieve that the interchange rate fordebit cards is much higher than theactual risk that Visa members areexposed to, and Wal-Mart, thePublix grocery chain and otherretailers have filed a class-action suitseeking damages.

While the judge has not yet ruled onthe merits of the suit, Visa recently

offered a settlement with Wal-Martand others, which they declined.Industry insiders speculate that theoffer was made because Visa wantsto be free to re-price debit cardtransactions.

On another front, Wal-Mart, Publixand others have announced that theyno longer will accept Interlink PIN-based debit cards. Interlink is a VisaUSA-owned brand. This announce-ment came on the heels of Interlink’sannouncement of an interchangeprice increase.

Then another story came from theworld of debit: the fact that Bank ofAmerica would be leaving the STARATM network, recently acquired by

The Financial Services Industry Source for Education, Inspiration and Actionable Advice

October 22, 2001Issue 01:10:02

I n s i d e T h i s I s s u e :

N o t a b l e Q u o t e :

FeaturesPaper Trail of Check Presentment

vs. Re-presentment by Brandes Elitch.............................9

Company ProfilesSecure Payment Systems....................29GoEmerchant.com ............................34Identico Systems................................41

NewsTeleCheck Names Drucker

President and CEO .........................4VeriFone is Back! ..............................17NACHA Rule Finalized......................23Alogent’s New International

Web sites are there to addto customer satisfaction, notoverwhelm and distractusers from the ultimate goal– a sale. Remember, keep itsimple.

Story on Page 57

STAR Could Become the Visaof Debit Transactions

GS Online Flexes Muscleto Empower Industry

See STAR on Page 4

check processing and mergersin the industry. All of the wis-dom and objective reportingreaders have come to trust, andthen some, is right at their fin-gertips.

One of the most excitingaspects of the Web site is theturbocharged search engine.The new search engine waswritten with speed and use-fulness in mind. The fiveyears of prior issues archivedonline are a great resourcefor anyone doing researchfor this industry.

Such a resource, however, is useful only if inquisitiveviewers are able to comb through it and find what they arelooking for. The search is built to make easy work of find-ing relevant results with a superb keyword search. Thesearch has been engineered so that even complex searchestake mere seconds.

Another useful new feature of the search engine is view-ing a document as a highlighted version. Each searchresult has a link at the end offering the user to “view thehighlighted version.” This function takes the user to amodified version of a desired article, where up to six indi-vidual keywords are highlighted throughout the text witha different color. This makes it very easy to wade througha document and quickly find the text one is looking for.There are also many advanced sorting options for theresults.

The Green Sheet has always been as much a mission as acompany, and for all of us who work at The Green Sheet,this is not going to change. What we believe can change,however, is our ability to serve the industry in even moreways, and you have seen many changes from us alreadythis year.

All our efforts have been directed toward helping the aver-age professional salesperson succeed in the ISO market-place. Because we believe knowledge is power, we haveworked hard to bring you breaking announcements, prod-uct information and detailed evaluations of the changes inthe payments industry, while making you aware of the suc-cess stories and opportunities for income. In addition, ourgoal is always to make some element of each Green Sheetturn into an action item for our readers, and this is why wecontinue to say that The Green Sheet is about education,inspiration and actionable advice.

As you well know, we have been making a lot of changes

to increase our ability to servethe ISO community andenhance our ability to provideeven more support, and wewould like to know if you thinkwe are succeeding.

While our Web presence wasborn in 1995, the changes wehave been making in the lastfew months will help The GreenSheet Online be the robust 21st-century tool that we believe theindustry expects from us. I hopethat you will give our new Webpresence a try. Use the forum,search for information or dropme a line.

Paul H. Green

1 Statistics compiled using Webalizer v 1.3

Page 3

Concord EFS Inc. B of A, the founder of the Visa brand, made itsannouncement after Concord EFS announced the acquisition.Concord EFS already owned the MAC network (the second-largestATM network in the U.S.) and Cash Station.

Concord’s online debit networks, which arebeing consolidated under the STAR brand,

reach from coast to coast and processmore than half of the U.S. online debittransactions, more than four times thenext-largest network, Interlink.

We believe that with Concord’s recentlyannounced interchange rate increases and

broad reach, debit card issuers will beincreasingly attracted to the STAR network. While the interchangeincrease is a negative from the retailers’ perspective, all of the otherdebit networks’ prices also are going up, and online debit is stillsubstantially more attractive than offline debit or credit.

Furthermore, STAR has the largest network of cardholders, maxi-mizing the reach for retailers. We believe STAR will continue tosecure more business with retailers at the expense of other net-works. Wal-Mart is coming online in the next few months for mer-chant debit processing with Concord, and we expect other retailersto drop Interlink as well.

Page 4

STAR from Page 1

NOVA

INFORMATION SYSTEMS, INC.

At NOVA, we focus on what’s important toyour business – bringing together the bestexperience, tools and communications to helpyou implement innovative strategies that leadto profitable, lasting customer relationships.

That’s why you need a strong business partnerto help you cut through the clutter and maxi-mize your sales potential.

We offer a long list of customized services andprograms that you won’t find anywhere else.And we don’t make it complicated. Throughour MSP Bankcard Program, you make thechoices based on your specific business needs,and we service them. It’s that simple.

We’re growing...and we want you to join our team as a NOVAMSP Bankcard Partner.

Income• Statement Fee Income• Annual Fee Income• Residuals Paid Monthly• No Liability/Risk• Unlimited Income Potential• Leasing with NOVALease.com• Residual Stream Purchases• NOVA’s Proprietary Downline

Compensation (DLC) Software

For more information about becoming a part of this remarkable program, please contact our

Relationship Management Team at: 1-800-964-7716, ext. 5158 and refer to code 0600GS.

NOVA is publicly traded on the New York Stock Exchange (“NIS”).

NOVA Information Systems, Inc. is an EEO/AA employer. 001

TeleCheck NamesDrucker Presidentand CEO

After significant defections in its seniormanagement team, TeleCheckannounced a major change: CharlesD. Drucker is its new President and

CEO.

TeleCheck, subsidiary of Greenwood Village,Colo.-based processor First Data Corp., has losta number of senior managers this year, includingJames Lerdal, now the new CEO ofInternational Check Services (ICS), and is onthe move to fill the management void. ICS is aGTCR-backed roll-up company.

Drucker had been a senior vice president withWells Fargo Bank, where he managed the mer-chant portfolio. Drucker is a member of theacquirer’s committees at both MasterCardInternational and Visa USA.

Schlumberger

Customers will give you a lot of credit

for accepting charge cards out here.

Remote downloading of newapplications allows you tocreate new opportunities forvalue-added services.

Companies on the move are making it easy for their customers to pay anywhere. And they’re using the MagIC 9000 Mobitex fromSchlumbergerSema. The Mobitex wireless link supports fast online payments wherever customers are–at home, in taxis, at sportingevents, even on the highway. The MagIC 9000 Mobitex checksand processes all card transactions, from traditional credit and debit cards to sophisticated smart cards. Its open platform supports multiple applications with built-in firewall protection. SchlumbergerSema offers acomplete range of POS terminals, including RF, IR, portable, stationary and PC-connected units–and the MagIC Management System Solution. To learn more about where a MagIC POS terminal can take your business, call SchlumbergerSema at 800.732.6868, ext. 202 or visit us at www.slb.com.

Good Job!

Great job on the new look and feel ofThe Green Sheet and Green SheetOnline. I especially like the new sub-stance and all of the changes. As always,you are staying a few steps ahead of thecurve.

Regards,John H. Beebe

Chairman & CEOGlobal eTelecom

Thanks!

The staff at Electronic Cash Systemswould like to thank you for the wonderfulprofile you wrote about our company inThe Green Sheet. The response has beenfantastic. We have received calls fromold friends and from new ISOs wantingto join our team. I received a call fromsomeone who said they read the articlethree times. Our program was just whathe was looking for, and he could notbelieve that he had finally found it.

Sincerely,Electronic Cash Systems

Interchange Rates

I am an ISO and would like subscriptioninformation. I also was advised that Imight be able to find a list of interchangerates for all of the different categories ofcards. Is there a chart available?

Thanks,Bob Malin

Dear Bob:

First, to subscribe to The Green Sheet, goto www.greensheet.com. Find the PUBLI-CATIONS page. Click on that page andthen scroll down the page to the bottomright corner and locate the SUBSCRIBE

TO GREEN SHEET AND GSQ link andfollow that link. You will then find a sub-scription form. Fill out the requestedinformation and then click on the linkthat says “SUBMIT TRANSACTION.” Youalso may call The Green Sheet office at800-757-4441.

The February 1999, No. 1 issue of TheGreen Sheet (99:02:01) contains an arti-cle, “Visa Price Increase April 1999,”that lists the MasterCard and Visa inter-change rates as well as rates for othercards as well. To access these, go to TheGreen Sheet Web site, as above. Thistime, locate the ISSUE ARCHIVE page.Click there and click on 1999, then clickon the number 990201, or February1999 second issue, and there you willfind the listings.

Good Selling,The Green Sheet Staff

What About FMBS?

I am trying to acquire informationregarding First Merchants BancardServices. Can you give me info on FMBS,good or bad?

Thank you,MJ

Page 6

Publisher: The Green Sheet, Inc. 1-800-757-4441 Fax: 1-707-586-4747Email: [email protected] 6145 State Farm Drive,Rohnert Park, CA 94928

Subscription Price: $425 per year (24 issues) U.S. &Canada, $575 Foreign, $125 per year forIndependent Sales Organizations (ISOs), agents, andbankcard service providers in the financial servicesindustry. Visit www.greensheet.com to subscribeonline.

Any questions regarding information contained in TheGreen Sheet should be directed to the Editor in Chief at(800) 757-4441. The Green Sheet is a semi-monthly publi-cation. Editorial opinions and recommendations are solelythose of the Editor in Chief.

In publishing The Green Sheet, neither the authors nor thepublisher are engaged in rendering legal, accounting, orother professional services. If legal advice or other expertassistance is required, the services of a competent profes-sional should be sought. The Resource Guide is paid classi-fied advertising. The Green Sheet is not responsible for, anddoes not recommend or endorse any product or service.Advertisers and advertising agencies agree to indemnifyand hold the publisher harmless from any claims, damage,or expense resulting from printing or publishing of anyadvertisement.

ACCPC ...........................................56Advanced Payment Services .............15Bridgeview Payment Solutions...........10Business Center USA........................18Business Payment Systems ................53CDE Services ...................................25Certified Merchant Services ..............62Concord EFS ...................................16Cornerstone Payment Systems...........40CrossCheck .......................................8Cynergy Data..................................28Datacap..........................................13Electronic Cash Systems .....................9Electronic Payment Systems ..............22First American Payment Systems .......50First Data Merchant Services ............20Global eTelecom ..............................44GO Software...................................37Horizon Group................................64Humboldt Bank................................55Imperial Bank ..................................23Integrated Leasing............................39International CyberTrans .................17IRN/Partner America.................32, 33LinkPoint International ......................24Lipman USA....................................14Merchant First .................................49Merchant Services Inc. .....................42Merchants’ Choice Card Services......38Merchants Leasing Systems ..............19Network 1 Financial ........................31North American Bancard .................12NOVA ..............................................4NPC ...............................................52One Stop Check ..............................45PayNet Merchant Services................27POS Payment Systems ......................30POS Portal ......................................54Resource Leasing .............................57Retriever..........................................26RichSolutions ...................................21Schlumberger ....................................5Signature Card Services...................43TASQ Technology ............................63Tasq.com.........................................48Tech Leasing ....................................46Teertronics.......................................11Thales e-Transactions .........................2United Merchant Services ...................3U.S. Wireless Data ..........................36Worldwide Merchant Services ..........35

Send your Questions, Comments and Feedback to us today!6145 State Farm Drive • Rohnert Park, CA 94928 or [email protected]

Dear MJ:

The Green Sheet published an extensivearticle in the January 1999, No. 2 issue(99:01:02), “Special Report: ISOsLooking For Agents.” To access our Websit, enter www.greensheet.com on yourbrowser and then click on the“Publications” button. Click on “IssueArchives” and in the search box type inthe code, 990102.

First Merchants Bancard Services, anagent of Chittenden Bank, recently cele-brated its 12th year. Service segments ofthe merchant market include home-based, MO/TO, start-up, wholesale,retail and Internet businesses. It offerscheck guarantee, ACH, credit, debit,phone card activation and EBT. Thetransaction fee is $.15 and up, and thestatement fee is $5 and up. It offers soft-ware and equipment solutions, includingterminal and PC-based integratedpatient “easy pay” programs for thehealth-care industry, and full support ofthe Lipman line. There is no monthly min-imum. Contact FMBS at www.fmbs.com,or e-mail [email protected].

Good Selling,The Green Sheet Staff

Just a Front?

I recently sent an e-mail to TransactionWorld magazine and asked for deliverynotification. I was surprised by theresponse. I mailed to [email protected] as well as [email protected], and inboth cases, it was delivered toexchsrv.dallas.checktronics.net. What’sup with this? Is Transaction World maga-zine just an advertising front forChecktronics?

Glenn Fry

Dear Glenn:

We have previously commented on thisquestion, but based on the e-mail resultsthat you have received, it appears thatChecktronics is no longer trying to hidethe fact that Transaction World (TW) is itsmagazine. We will further note for yourfiles that Checktronics is refusing adsfrom businesses that it deems competitiveto its own agenda, something we believeis bad for the industry. When questionedabout an offer of trading ads, HaroldMontgomery, noted that besides himselfthere were other owners/investors inTW. Who these owners are might be thebest-kept secret in the industry.

If you would like to read the entire com-ment from the first issue of April 2000,please go to The Green Sheet’s Webpage and do a word search in the topright-hand corner. In part, this is what wesaid: “... if the ownership of TransactionWorld was intended to be a secret, theanswer is not hard to uncover. ArtHoldings, Inc., according to the Office ofthe Comptroller of Texas, is a Texas cor-poration chartered on Oct. 8, 1993.Chief Executive Officer and registeragent is Harold Montgomery, also CEOof Checktronics Check Services. (Thiswould explain) why, among a full publi-cation of advertorials, HaroldMontgomery has a story/ad in eachissue.”

Good Selling,The Green Sheet Staff

CORRECTION

The Web site of U.S. MerchantServices in Stuart, Fla., featured in aCompany Profile in the Sept. 24, 2001issue (01:09:02) of The Green Sheet,is www.us-merchantservices.com (witha hyphen).

Page 9

ISOs from around the country have been asking foran update on point-of-sale check conversion, partic-ularly regarding imaging and RCK (collecting a badcheck with an ACH debit). Here is a status report

and overview of the situation:

First, there is some confusion about what a merchant cando and cannot do to convert a check to an ACH debit entryagainst a consumer’s checking account. There has been lit-tle noncompliance at point-of-sale with the rule requiringa signed consumer authorization. (There has been massivenoncompliance with the rule for a signed authorization inthe Mail Order/Telephone Order/Internet world, but that isa subject for another article.)

There are other issues, such as the possibility of merchantor merchant employee fraud and the whole question ofwho keeps the check (the rules are changing in January).Most operational issues revolve around the fact that, untilnow, there was no effective way to image the front andback of the check, so all the merchant had was a swipe ofthe Magnetic Ink Character Recognition (MICR) line.Without the image, the merchant lacked the informationon the face of the check, such as name and address, tele-phone number and driver’s license number – ways thatguarantee companies have of finding the consumer.

(Just having an MICR line does not help in tracking downa deadbeat consumer; the guarantee company would haveto build an in-house cross-reference file to the driver’slicense.)

Now, imaging of the check is starting to emerge as a viableproduct. It requires that the merchant attach an imagereader to the terminal, add a high-speed modem and pro-vide a way to store and retrieve the images. Up to now, thiswas a big issue. Large retailers who have thousands ofmultilane stores needed to find a financially stable vendorcapable of large-scale implementation that would bearound for the long haul. This proved to be problematic.

As a result, early attempts at POS conversion have gonenowhere. The large retailers decided to wait it out until atruly reliable imaging solution came down the pike. Thefirst vendor in the conversion business (without imaging)went through, by my estimate, at least $10 million tryingto implement a solution and has, for all intents and pur-poses, withdrawn from the business. Conversion is stalled,awaiting adoption by major retailers, who must have animaging solution.

What kind of pitfalls can a conversion product bring to amerchant? Here is a note that I received from a companyin the cash-management business that sells payment pro-cessing. What is interesting about this case study is that itpoints out concisely why check conversion doesn’t alwayswork for the merchant. In this case, it created more prob-lems than it solved. The merchant incurred more fees, hadcustomer-service problems, processing wasn’t alwaystimely, and customers were aggravated. What happenedhere was that the service provider didn’t understand themerchant’s business and tried to plug in its product any-way (sound familiar?).

————————“We had called on this customer six months ago, andthey were very interested. They sell product only viacatalogue and Internet. They told us that six monthsago they were receiving $20,000 per month in checksvia the mail, and the average sale was $119. They werenot sure they were interested in check guaranteebecause they were experiencing only one return per

Paper Trail of Check Presentment vs. Re-presentment

By Brandes Elitch

Are you interested in working with acompany that provides great sales

support?

You handle the sales,

We’ll handle the details,

You enjoy a big commission

Support includes:

$ Lease Application Processing

$ Lease Financing

$ Equipment Ordering

$ Shipping and Installation

$ Signs

$ Customer Service

$ Nationwide Processing

For more information and toreceive a package on how tobecome an ISO contact us at(888) 327-2864

Master Distributor of Cross International,Inc.

POS & ATM Equipment

®

We handle most makes and models of ATM’s and Credit CardEquipment and are also a Master distributor for many manufacturers

710 Quail Ridge DriveWestmont, IL 60559630.321.0117www.bridgeviewbank.com

Your Bridge to Better Merchant Processing

A league of our own.

Team up with BridgeviewPayment Solutions and score big profits with a proven winner in merchant processing. Our Net Income Split Programcan’t be beat.

Welcome to the big leagues.

item per quarter, which cleared on the next present-ment.

“They received a call from TeleCheck and decided tosubscribe to its ACH online check product. They wereanxious to automate check processing to the same levelas their credit card processing. They did not want tohandle and deposit paper checks.

“TeleCheck set an initial discount rate of 4.2 percent,then raised it to 4.7 percent after several months and 6percent after six months. During this six-month period,the merchant received $4,000 per month in checks viamail, and $15,000 per month was processed via theTeleCheck ACH online check option. The merchantcontinued to see about one check per quarter returnedand collected on these returns via deposit. However,TeleCheck informed the merchant that it was seeingnine return items per month, and that was the reasonfor the corresponding increases in the discount rate.

“With the merchant experience of processing 100 per-cent of their checks before using the TeleCheck ACHproduct as well as the experience of depositing theirown checks alongside the TeleCheck ACH product, Iwould wager that the reason for the high percentage ofreturns at TeleCheck is a direct result of the use ofpaper check MICR lines as origination documents forACH transactions.

“It is my guess that TeleCheck is experiencing admin-istrative returns that it is resubmitting via RCK andthat are being returned for the same reasons on the sec-ond and third presentment. I assume that this is a fullyautomated process that it is not prepared for, and it isnot capable of turning these items back into paperchecks, which would solve the problem.

“Needless to say, the merchant told TeleCheck to takea hike when it suggested a 6 percent discount rate. Themerchant also is aggravated that TeleCheck was charg-ing the same discount rate for denials, which were fre-quent, and that the Internet service was down on a reg-ular basis, once for an entire week. This down timerequired phone calls and delays in response-timeorders.”

————————————

We should not draw the wrong conclusions, however.Conversion can work in certain circumstances:

• There are high-volume, low-dollar payments (and I meanhigh volume as in “grocery store”).• Check handling is onerous.• There are multiple locations that require multiple bankaccounts and the attendant money movement, idle bal-

ances, bank fees, etc.• The consumers are repeat buyers, so the data can bescrubbed at the front end (using Notifications of Changeand prenotes).

Often, particularly when there is a higher average ticket ormore risk in the transaction, merchants ask that the con-verted item be guaranteed. There may or may not be aneed for guarantee in these circumstances. Remember,speaking for CrossCheck, our primary role is not to doverification or collection – it is to make the sale happen bystanding in when the consumer does not have enoughfunds in his or her account to cover the purchase, regard-less of how it is originated.

If we can increase sales by 5 to 10 percent, why wouldn’tthe merchant pay 1 or 2 percent for that? The need for this– for someone to stand in and approve the sale in advancewhen no money is there – is not going to go away becausethe payment is settled as an ACH or an ATM transaction;in fact, it might even increase.

Is there any other way to meet the merchant’s needs forreduced check handling without using the ACH? Ofcourse, I wouldn’t ask the question if I didn’t have a solu-tion. The answer is: Use a paper draft. How does this

Page 11

Page 13

work? Let’s use a couple of examples.

First, in the non-face-to-face world, when you take a pay-ment over the phone or over the Internet, you aren’t get-ting a check from the consumer. But rather than create anACH item, the merchant (or the processor) can create apaper item. Yes, you can print a check on the consumer’saccount and deposit it, even though it doesn’t have a sig-nature (it’s legal!). There are a number of providers whosell the ability to print checks in this manner. Here’s whatyou need to look for:

• Is the payment being guaranteed? From one to 10 percentof the time the money is not going to be there, for one rea-son or another. Do you really want to try to collect it your-self?

• Is the bank going to reject the item? Many check-print-ing systems do not comply with the rigorous standardsimposed by the Bank Administration Institute for check

printing. If you print your checks with a bubble jet printer,I can guarantee that when the bank puts them in its high-speed reader/sorter, they are going to stick together like abrick.

Even if they don’t, if you are not using an MICR toner car-tridge, the bank will have to outsort them and process themas an exception item. Banks HATE exception items. Ifyou have any kind of volume, it is only a matter of timebefore the bank asks you to close your account and findanother home.

• How are you going to deal with the issue of administra-tive returns? You can count on at least 3 percent of theitems you convert to come back and visit you again. Thisis because the bank where the account lies is not alwaysthe bank that is doing the data and item processing. Thisproblem is actually getting worse with POS conversionbecause you don’t have the traditional checks (NOC andprenotes) that you have for recurring payments.

• Who is going to print the checks for you if you have highvolume? Do you really want to print a few thousandchecks a day? Some vendors, such as CrossCheck, willprovide a seamless, all-electronic back end with automat-ic funding of the merchant’s account.

Well, that covers some of the issues with “presentment.”

Datacap

Banks HATE exception items. If you haveany kind of volume, it is only a matter oftime before the bank asks you to closeyour account and find another home.

Lipman USA gives

you freedom of choice –

and freedom of movement – to

do business your way. Now, our new

Nurit® 8000 wireless POS terminal sets

you free to go anywhere there's a sale.

It's the world's smallest

and most powerful hand

held POS terminal from

the world leader in wireless

transaction solutions. The Nurit 8000 is the size

of a postcard. Tuck it into a pocket, and open all

kinds of new opportunities for your business.

The Nurit 8000 is yet another innovation from

Lipman USA, where ever y th ing we do is

designed to give you freedom of choice...

freedom of movement... freedom to be the best.

Visit us on the web at

www.lipmanusa.com.

Or call 1.800.454.7626.

TM

Freedom of ChoiceFreedom of ChoiceThe amazing new wireless Lipman Nurit® 8000

lets you do business any way... anywhere.

Now, what is “representment?” This occurs when the orig-inal item is returned and you are faced with the decision,“What do I do with it now?”

If it has been converted to an ACH debit, you can return itvia the ACH network. This is called an “RCK,” which isshort for “returned check” (all ACH categories have athree-letter abbreviation). The NACHA rules say that youcan represent this twice and that’s it. However, you canrepresent a paper check drawn on a consumer’s account asoften as you want. The same goes for the service fee,which can be particularly important in certain sectorswhere there is low dollar, high volume and a high percent-age of return items.

You can only go after the service fee twice with an ACH;not so with a paper draft. Plus, with a paper draft you can

avoid the NACHA rules and regulations, which almostrequire a full-time interpreter. ACH aficionados will saythat it’s cheaper and faster to submit an ACH item, but thatisn’t true; if you submit an encoded-items cashletter, yourbank is going to charge you less than 10 cents per item andgive you around a 1.5-day availability.

If you submit it via the ACH, you will pay 20 cents peritem (we have heard reports of as much as 75 cents!) andwait three days for settlement (plus have rolling reservesand other credit enhancements). You can use software,such as the “ChecksNow” product from CrossCheck, toprint a draft from any source (you just fill in the appropri-ate fields) and if you use an MICR toner cartridge and therecommended paper, you will be compliant with the BankAdministration Institute (BAI) specs, so your bank won’tget mad at you. Now you can make a paper RCK, and isn’tthat a lot easier than trying to create an ACH file?

So, now that you know all about presentment, you can seewhy “representment” can make more sense with a paperdraft than with an ACH. Bet you didn’t think you’d believethat when you started reading this.

I would be interested in similar case studies. If you haveone that you believe our readers would be interested in,please e-mail it to me at [email protected].

Page 15

You can only go after the service fee twicewith an ACH; not so with a paper draft.

Plus, with a paper draft you can avoid theNACHA rules and regulations, whichalmost require a full-time interpreter.

If you are like most of us, you probably did-n’t even know VeriFone was away. For thelast four years, VeriFone Inc. has been theexclusive property of computer giant

Hewlett-Packard Co. On July 20, 2001, theGores Technology Group1 acquired VeriFonefrom H-P for an undisclosed amount of cash.

Douglas G. Bergeron, the new Group Presidentof Verifone, isn’t one to mince words. His obser-vation of H-P’s stint as the point-of-sale termi-nal maker’s owner: “They gummed it up withH-P bureaucracy and sucked the entrepreneurialoxygen out of it.”

On the surface, Gores’ goal for 20-year-oldVeriFone seems simple: return the Santa Clara,Calif.-based company to its POS roots. But,clearly, the Gores VeriFone is a much moreaggressive company.

No matter who owns it, VeriFone will face amarket growing tougher by the day. Terminal

Page 17

VeriFone is Back!

If you are looking for a long term partner with a proven background

CALL US TODAY! 1-877-804-3300 ext. 236

International

CyberTransDefining the future of transaction automation

We have been providing Automated Payment Solutionsto merchants nationwide since 1980. ICT is a FinanciallySound, Well Capitalized, Rapidly Growing Company withan impeccable reputation, founded on integrity and run bya sales oriented management staff. ICT continues to create

relationships with Agents, Sales Offices, and ISO’s offering:

• Aggressive equipment pricing and leasing programs

•Revenue sharing at interchange plus

•Internet/e-commerce and all other traditional markets

•Loyalty/gift card, check conversion

•We provide the best sales support in the industry

makers are locked in price competition, and many mer-chants are content with their existing machines.

In addition, foreign terminal makers are moving intoVeriFone’s North American “backyard” as never before.On Aug. 8, France’s Ingenico S.A. bought IVI CheckmateCorp., the No. 3 terminal seller in the U.S. and Canada,and is poised to challenge leaders VeriFone andHypercom.

Even in that light, Bergeron, who also is a group presidentat Gores, is undaunted.

“This is a business with a great franchise and great cus-tomer value,” he says. “This is not a business that is at theend of its life cycle.” Bergeron adds, “Despite the allegedH-P mediocrity, VeriFone’s organs are not damaged. Thereare great VeriFone managers waiting to be set free. We are

confident that, working with VeriFone management, wecan capitalize on its strengths and maximize its potentialfor growth.”

“VeriFone is a great addition to the GTG portfolio of com-panies,” said Alec Gores, Founder and Chairman of GoresTechnology Group. “We look at this acquisition as a long-term strategic investment. The company has tremendouspotential. It is the global leader in an industry that webelieve is going to continue experiencing significantgrowth.”

Pierre-Francois Catte, General Manager of VeriFone, says,“The parties are working to ensure that the acquisition byGTG would not result in any disruptions of service, prod-uct shipments or changes in the business relationships withVeriFone’s partners and customers. ... VeriFone plans tokeep all of its existing employees in its current ongoingoperations.”

VeriFone could not have asked for a better partner. GoresTechnology Group has an outstanding reputation for

Page 19

“They gummed it up with H-P bureaucracyand sucked the entrepreneurial oxygenout of it.”

— Douglas G. Bergeron, group president, VeriFone.

achieving positive results by empowering managementand employees to effectively and efficiently improve per-formance and supporting growth through investment andacquisition.

“We consider this return to VeriFone’s roots as a nimble,entrepreneurial, stand-alone technology company with thefreedom to innovate and grow,” Catte says.

VeriFone’s newest payment hardware and software meetsthe highest security and performance standards for cus-tomers using the Europay, Mastercard and Visa (EMV)standard for smart card transactions.

“VeriFone has established the groundwork for the long-awaited growth of smart cards in the United States,”Bergeron says. “The company has staked its claim tofuture payment markets by taking a lead in emerging smartcard and mobile commerce technologies. We believe itsbest years are yet to come.”

In a message released Sept. 25, 2001, Bergerson toldemployees, “I am tremendously impressed and encour-aged by our performance as a business, and as a reinvigo-rated culture. We are already exhibiting the fighting spiritthat first made VeriFone great. Since the acquisition of

VeriFone on July 20, we have achieved many goals. Wehave greatly improved the speed in which our businessmakes decisions. We have renewed our decades-long com-mitment to the core payment business that we invented 20years ago. We are now profitable, very well capitalizedand backed by an investment group that believes in ourfuture and in our leadership.

“We have restructured our work force, introduced our newcompany to key customers and launched what will becomeanother best-selling terminal, the Omni 37002. We areproud of our 20 years of industry leadership achievedthrough technical innovation and supreme customer serv-ice. We are convinced that this is the recipe for continuedsuccess in the future for all of our employees, investorsand customers.”

1 Gores Technology Group, which specializes in acquiring high-techorganizations and managing them for growth and profitability, has todate acquired approximately 35 companies providing high-tech servic-es and products to millions of customers worldwide with annual rev-enues of more than $2 billion combined.2 The Omni 3700 family of terminals delivers customer value, per-formance and innovative EMV and multiapplication capabilities.

Page 21

Turning payments into profits• that's what it's all about. And RichSolutions is your key to profit.

• New secure ePayment Web service supports credit cards,debit cards and check services that you can sell as a lease.

• Sold exclusively through partners lets you set the priceso you can maximize your profit potential.

• Supports retail as well as MOTO & eCommerce industriesallowing integration of on-line and store front operations.

• Free PC application and browser solution that you can resell.

• New technology that works on any device, any time and any place lets you expand your markets.

Learn how you can become a RichSolutions partner. www.richsolutions.com/partners • 425.836.4251

Your Key To

RichSolutions, Inc.ePayment Solutions That Work!

Imperial Bank

NACHA Rule Finalized

Under the new rules of NACHA1, consumers willbe able to make e-check payments over the tele-phone. The rule, which became effective onSept. 14, 2001, permits merchants, billers and

government agencies to offer e-checks by telephone as apayment option.

An e-check is an electronic debit to a checking accountthat is initiated on the Internet, at the point-of-sale, overthe telephone or even by a bill payment sent through themail.

E-checks by telephone are governed by the FederalReserve’s Regulation E2. NACHA’s rules for the use of e-checks by telephone mirror the Federal TradeCommission’s telemarketing sales rule and provide anadditional consumer protection by specifically prohibitingcompanies that cold-call consumers from using e-checksfor any resulting sales.

Since July 1999, NACHA has been conducting a pilot pro-gram3 to evaluate the use of e-checks by telephone. In theprogram, a participating financial institution signs up cor-porate customers, permitting them to offer this authoriza-

tion method for debit payments. The debit is made usingthe Automated Clearing House (ACH) Network4.

The ACH Network is commonly used for direct deposit ofpayroll and government benefits such as Social Security,direct payment of consumer bills, business-to-businesspayments, federal tax payments and, increasingly, e-checks and e-commerce payments. In 2000, there were 6.9billion ACH payments made, worth more than $20 trillion.

Previously, operating rules for the ACH Network requireddebit authorizations to be in writing and signed or similar-ly authenticated. While this works in recurring bill pay-ments for mortgages, insurance premiums, utilities andother such recurring payments, a written authorization canbe cumbersome for one-time, non-recurring payments.

Under the pilot program, oral authorizations take the placeof written authorizations for these non-recurring pay-ments. Consumers can authorize, by telephone, electronicdebits to their checking or savings accounts to pay forgoods and services. The authorization is either tape-recorded or a written confirmation notice is sent to theconsumer.

The same consumer rights and protections that apply torecurring debits are maintained during the pilot program.

Page 23

If you think ISA means

I’M SOAWESOME

call us.

Think you’re pretty special? Contact Ken Stewart at 1-800-790-2670 [email protected].

Imperial Bank is looking for independent sales agents with, well let’s just say,very high self-esteem. Put your confidence and experience to work in a directrelationship with an aggressive, acquiring bank.

• Interchange as your buy rate on all transactions

• 10-cent transaction cost• No monthly minimums

• Excellent sales support• Superior customer service• Integrity backed by $7 billion

in assets

Member FDIC

Agent Direct features:

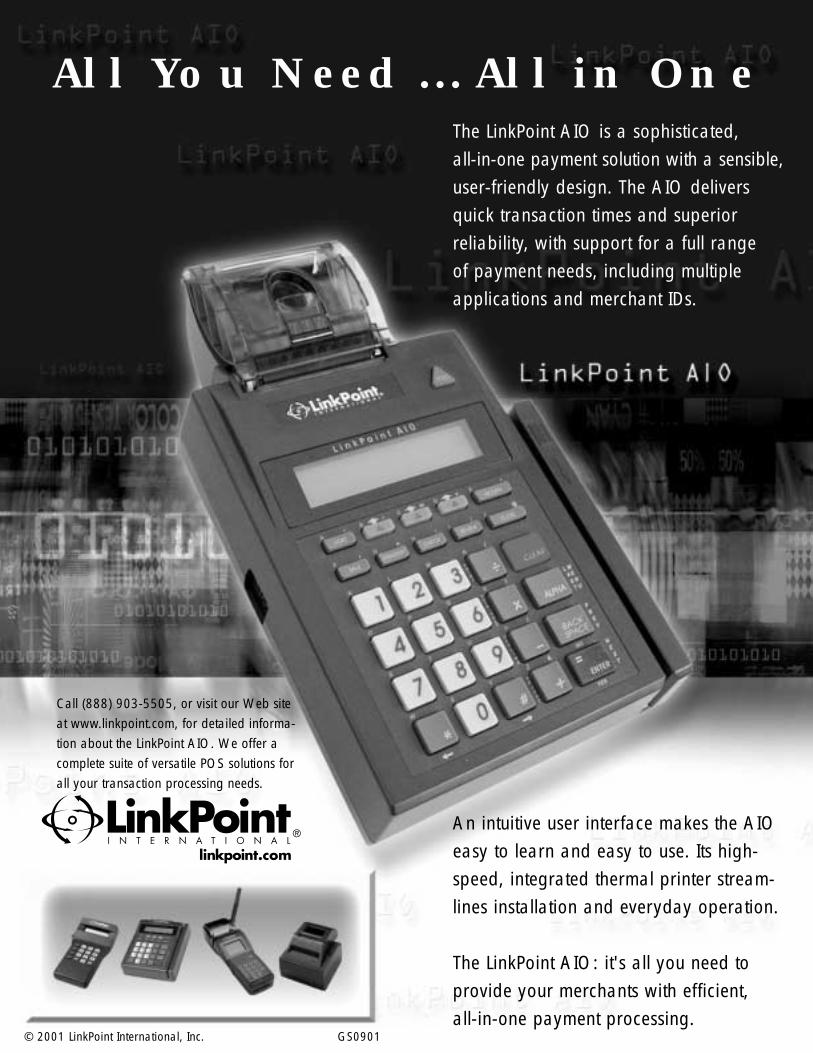

LinkPoint

The LinkPoint AIO is a sophisticated, all-in-one payment solution with a sensible,user-friendly design. The AIO deliversquick transaction times and superior reliability, with support for a full range of payment needs, including multipleapplications and merchant IDs.

An intuitive user interface makes the AIOeasy to learn and easy to use. Its high-speed, integrated thermal printer stream-lines installation and everyday operation.

The LinkPoint AIO: it's all you need toprovide your merchants with efficient, all-in-one payment processing.

Call (888) 903-5505, or visit our Web siteat www.linkpoint.com, for detailed informa-tion about the LinkPoint AIO. We offer acomplete suite of versatile POS solutions forall your transaction processing needs.

A separate authorization is required for each debit transac-tion. The originating company is required to keep a recordof the authorization for two years, and consumers have 60days to challenge debits they believe to be unauthorized.

The pilot program specifically prohibits companies fromcalling consumers with whom they have no previous rela-tionship. From its inception through July 2001, the latestmonth for which statistics are available, the pilot programhas originated more than 10.5 million e-checks.

“Telephone authorizations will provide consumers with aneasy and convenient method to make one-time payments,”said Elliott C. McEntee, President and CEO of NACHA.“An e-check authorized over the telephone is an easy andconvenient option for consumers to make payments. Aconsumer paying a bill or making a purchase would havean alternative to mailing a check.”

To find out more about NACHA and its rulings, visitNACHA on the Internet at www.nacha.org.

1 The National Automated Clearing House Association (NACHA) rep-resents more than 13,000 financial institutions through its 34 regionalACH associations, six councils and corporate Affiliate Membershipprogram. NACHA develops operating rules for the Automated ClearingHouse Network and for emerging electronic payment solutions in the

areas of Internet commerce, bill payment and invoice presentment andpayment (EBPP, EIPP), e-checks, financial electronic data interchange(EDI), cross-border transactions, electronic checks and electronic ben-efits transfer (EBT).

2 Regulation E prescribes rules for the solicitation and issuance of EFTcards; governs consumers’ liability for unauthorized electronic fundtransfers (resulting, for example, from lost or stolen cards); requiresinstitutions to disclose certain terms and conditions of EFT services;provides for documentation of electronic transfers (on periodic state-ments, for example); sets up a resolution procedure for errors; and cov-ers notice of crediting and stoppage of preauthorized payments from acustomer’s account.

3 The financial institutions that enrolled in the pilot are AFBA IndustrialBank, AmSouth Bank, Bank of America, Bank of Denver, Bank One,Capital City Bank, Chase Manhattan Bank, Citibank, First NationalBank in Brookings, FNB of Central Texas, First Premier Bank, FirstRegional Bank, First State Bank, First Union, Florida Bank, Ft. KnoxNational Bank, Legacy Bank of Texas, Mellon Bank, Northern TrustCompany, Oakland State Bank, Pacific Mercantile Bank, PNC Bank,Riverway Bank, Sears National Bank and Wells Fargo/Norwest.

4 The ACH Network is a nationwide, inter-bank payments system thathas been in use for more than 25 years. The ACH Network serves20,000 financial institutions, 3.5 million businesses and 100 millionindividuals.

Page 25

Alogent Corp., a developer of payment transac-tion processing solutions for global financialinstitutions and remittance processors, hasexpanded its U.S. presence by opening a new

corporate headquarters in Alpharetta, Ga.

Founded in 1995 by CEO Brian R. Geisel as a paymentsystems project consulting and software developmentcompany, Alogent is based on its proven success in merg-ing paper check processing and image-captured data. Thecompany made the decision to leverage its legacy-systemexpertise into a strategic product that facilitates the transi-tion from paper to electronic payment processing.

Alogent has experienced rapid growth and expansion andthis year expects to double its total revenues from 2000and quadruple its license revenue. It has achieved prof-itability every year since its inception and continues togenerate profits and positive cash flows. Staffing hasgrown by 70 percent since last year, and company hiring isexpected to continue at a record pace through the end ofthis year.

The company’s origins are deep in both Great Britain andUnited States financial services industry through the indi-vidual and collective experience of its highly skilled staff.The know-how gained from providing consulting projectsto Chase Manhattan Bank and five Federal Reserve Bankdistricts positioned the company to provide its fast andefficient payment solution product to such global clienteleas Lloyds TSB Bank, HSBC Bank, Barclays Bank,Girobank and the outsource processing consortium iPSL.

In the U.S., remittance-processing giants such asSouthwestern Bell Communications, Texas Utilities,Florida Power and Light, and First Energy employ thecompany’s transaction-processing engine, and other bigbillers were scheduled to begin this year.

By 1999, Alogent was forced to move to new facilities tohouse its rapidly expanding software development andmanagement team. The organization is exemplified bypayment system and information technology professionalswho average almost a decade of software developmentexperience per person. This talent is backed by superbtraining and rigorous team project management practices.

On May 1, 2000, the corporation announced the openingof its new office in London, further expanding its tacticalsales and service to international customers.

Now, Alogent has moved its international corporate head-quarters yet again, this time to a 35,000-square-foot facil-

ity with an 8,000-square-foot Sierra Solutions Center, ded-icated to testing, qualifications education, and demonstra-tions of the company’s Sierra range of products. The cen-ter contains both countertop and high-speed image captureand document processing devices from key manufacturers,such as Epson, Seac Banche, Digital Check, NCR, Unisysand IBM.

It features the banking industry’s top payment processingplatforms, including CPCS running on an IBM 3890, fortesting the company’s back-office payment processingsoftware, Sierra Clearing. It also provides an array ofhardware and software for developing and testing inter-faces between its front-office product, Sierra xClearing,and its third-party front-office software applications.

This highly sophisticated, multiplatform processing envi-ronment supports the company’s focus on developingenterprise-wide Windows NT/2000 software products thatsupplement and enhance critical operations of large finan-cial institutions.

Alogent develops and delivers the Sierra open-architecturepayment processing software solutions to banks, financial

Page 27

Alogent’s New International Headquarters

institutions and remittance processors who want tomake payment processing more efficient and moreprofitable. Alogent’s front- and back-office imageand MICR payment solutions are scalable, Web-deployed and based on the Microsoft DNA architec-ture and XML.

Alogent was named to the Atlanta BusinessChronicle’s Pacesetter lists in 2000 and 2001 as wellas to the Deloitte & Touche Technology Fast 500and the Inc. 500 lists of fastest-growing companies.

“Alogent’s reputation for high-quality technicalsolutions has moved us into new spheres of influ-ence and scale,” Geisel said. “Since we are devel-oping mission-critical software solutions for severalof the largest financial institutions in the world, itmakes sense for us to create a world-class office anddemonstration facility. We want our current clientsand future customers to see for themselves how ourtradition of excellence results in product innovationand quality in both legacy environments and distrib-uted operations.”

For more information, visit the company’s Web siteat www.alogent.com, phone 770-752-6362 or fax678-966-9124.

Page 28

Army Drafts Schlumberger

SchlumbergerSema recently announced that Logicon, asubsidiary of Northrop Grumman Corp. and a providerof advanced information-technology solutions, engi-neering and business services for government and com-

mercial clients, has acquired nearly 60,000 of its advanced Reflexsmart card readers for the U.S. Army’s implementation of theDepartment of Defense (DoD) Common Access Card (CAC) pro-gram.

This new order represents the largest single deployment of smartcard readers in the U.S. to date and complements the company’sprevious announcement that EDS purchased 600,000 of its Java-based Cyberflex Access smart cards for the overall DoD CACprogram.

The Army will utilize the Reflex 72 USB and Reflex 20 PCMCIAreaders, which connect with desktop and portable PCs, to authen-ticate smart cards used for secure network access, as part of itsimplementation of the DoD CAC program. The DoD CAC pro-gram is using highly secure, multiple-application smart cards,such as the SchlumbergerSema Cyberflex Access card, for physi-cal identification, building access and network access in a multi-tiered program that is being rolled out throughout the DoD overthe next few years.

Page 29

Secure Payment Systems isno start-up. It was born inthe mind of Linden “Lin”Fellerman five years ago,

shortly after leaving his 20-yeartenure and 10-year stint as thePresident of Equifax Check Services(formerly Telecredit Check Services)and moving back home to SouthernCalifornia.

Lin began in 1975, while still in col-lege, working part-time as a voice-authorization clerk, a role lower thanworking in the mailroom of then LosAngeles-based Telecredit Inc., thenation’s largest check guaranteecompany. Lin found that he had apassion for the check business andtook to it like a duck to water.

As the company progressed, Lin did,too, and he eventually was promotedto President shortly before his 30thbirthday in 1986. In 1991, Equifax,the nationwide credit-reportingagency, purchased the company. Linhad accomplished what few onlydream.

Even before he left in 1996, Lin hada vision. He saw that working for alarge corporation had its advantagesbut also some major shortfalls. Plus,he found that the fun was gone. SoLin set out to build a company thatcould be different in many ways butstill deliver a superior product andre-instill the passion that got himinto this business in the first place.

Lin believed that his background inthe business gave him the insight todevelop a privately held company

that could offer some major differ-ences to his customer base and createa successful enterprise:

• He could create a more sophisticat-ed, efficient and cost-effective risk-management engine given his oper-ating expertise at Telecredit/Equifax,where he was instrumental in creat-ing many risk-management innova-tions.• He could target the small- to medi-um-size merchant sector with a low-cost, high-personal-service operatingstructure and thus keep customerattrition at a fraction of the competi-tion’s rate.• Given personal care and low attri-tion, he could create a check servicescompany that ISOs could trust withtheir credit card customers.• He could rapidly develop a suite oftransaction-processing services tostay competitive in the ever expand-ing payments business.• He could create a company thatwas lean, flexible, swift and devoidof paralysis by committee.

Lin proposed that no matter whatsize SPS grew to over time, he wouldat all times behave as a small compa-ny to avoid the bureaucratic trap-pings that hinder a company’s flexi-bility and interaction with its cus-tomers. If SPS was going to be suc-cessful, it was going to be hands-onand customer-focused.

As a matter of fact, before he evenopened his doors, Lin performed amarketing study to determine whatthe average small to midsize mer-chant loathed in the check compa-

support (RDM)• Multiple terminal support (VeriFone,

Hypercom, Thales, Nurit)• Low cost/high service provider with

standard 14-day claim payment• $36,000 individual check limit

(paper and electronic conversion)• 24/7 technical, consumer affairs

and operator call center support• No claim rejections for not writing

miscellaneous data on the check• Integrated gift card transaction pro-

cessing and card issuance

nies operating at the time. With that data and a couple ofbucks from his retirement account, SPS was born in SanDiego with a skeleton crew and a song in his heart.

Given technological advances, his understanding of riskalgorithms and the programming connections he madeduring his career, Lin believes he has satisfied his primarygoal – and the core of SPS – by building a superior riskmanagement and analytics engine.

Lin went with what he knows and first hired direct-salespeople. While that was moderately successful, the compa-ny’s real success story has been through its growing baseof independent sales organizations. And that was puttogether mostly through the efforts of Lin, his reputationand word of mouth.

In April, SPS will celebrate its fifth year in business. SPShas experienced a great deal of success and continues togrow at a pace of 40 percent per year. It has accomplisheda remarkable feat in the check world in that it has keptattrition below 6 percent when the industry average prob-ably hovers around 20 percent. And … ISOs trust SPS.Just ask Lynda Neuman, CFO of United MerchantServices, based in Glendale, Calif., who says:

“Secure Payment Systems is a dream come true. In the

three short years we have been associated with Lin’s team,we can think of no other guarantee company that evencomes close by comparison. And we have used all the big-name companies over the last 10 years.

“In fact, prior to using Lin’s company, we were terminat-ing the relationship with our prior service provider andnever going to offer check services again because of theincessant complaints from our merchants. Claims werenot being paid timely, if at all; customer service was poor;fees were being raised; and authorization controls werebeing changed at will.

“Because of Lin’s prior background and commitment topersonal service, we decided to give Secure PaymentSystems the opportunity. We could not be happier becausethe silence is deafening! We have not had one merchantcomplaint in three years! I invite all other ISOs to try tomake the same claim with their service provider!”

All of this has not sidetracked Lin from continuing tofocus on his vision. He still believes in being hands-on.Ask the people at SPS headquarters in San Diego, andthey will tell you that Lin trained them in each one of theirjobs. Not only that, they will tell you that Lin outpaceseveryone there and still provides as-needed assistancewith their respective roles. It is not unusual for Lin to takea customer-service call, download a terminal, visit an ISOacross the country, or go cold-calling with one of his sales-people!

Last year, Lin discovered that he has only two hands andfinally conceded that his hands-on approach was limitedby the number of hours in a day. Lin has been deliberatein hiring a team of key people who believe in the samephilosophy, the same customer-driven desire to be fast,flexible and reliable – but also to have a little bit of funalong the way.

He is now announcing a major selling program for the ISOmarket because he believes he has found the right personto whom he can hand the ISO ball. Lin never advertised,believing it was far wiser to fly under the radar, stealthilycapturing share while making sure that all the operatingpieces were in place for an all-out assault.

SPS has stayed ahead of the competition by continuing tooffer more enhancements to its check services. Early thisyear, SPS rolled out its check conversion program. Eventhough Lin believes that check conversion has manyissues associated with it, “it is a program that ISOs believein and want to sell.” Therefore, Lin set out to have the bestprogram available and offers conversion with guaranteethat deposits funds within 24 to 48 hours in the merchant’saccount and keeps merchants whole throughout theprocess, even if the ACH fails to post.

Page 30

“It’s all about how you manage the risk,” Lin says whenyou ask him about all the different companies out therethat offer conversion. “If you think that you are going tomake any money in the conversion guarantee business,you had better understand the inherent risks associatedwith each class of merchant. … For example, simpleauthorization logic found in most vanilla verification sys-tems will not win the day in a conversion guarantee pro-gram for high-risk sectors such as jewelry, audio/video,computers or leather goods.”

Lin has stayed focused on offering a broad array of pay-ments products and has just rolled out its own proprietaryterminal and PC-based Gift Card Program. Integrated withor apart from electronic check conversion, this programoffers merchants of even the smallest-size store the oppor-tunity to take part in a low-cost electronic gift cardprocess.

Whether the merchant is interested in the generic cardtypes already offered by SPS or custom artwork, SPS takesthe merchant full circle in issuing the cards, installing theterminal software and processing the transactions. SPSeven has entered into a strategic partnership with anotherCalifornia-based company for a patent-pending mini CD-based gift card with magnetic strip! This CD gift cardoffers incredible potential for associations, franchiseorganizations or large retailers interested in using the mul-

timedia opportunity.

With a base of thousands of locations and adding hundredsof merchants each month, SPS serves customers and ISOsnationwide from its California headquarters. With 24-hourtechnical support, voice authorizations and customer serv-ice, SPS also supports the spectrum of nationally recog-nized POS devices (Hypercom, Nurit, Verifone, Thales)and check scanners (IVI/Checkmate, Magtek, Verifoneand RDM imager). What many check authorization firmscharge merchants extra for, SPS does as part of its stan-dard program, which is already priced competitively.

“I would rather take a lower margin and have our mer-chants believe that we are priced fairly to begin with,”says Lin. “I believe that fair pricing and attention tounusual ‘personal’ customer service is what it takes toensure that ISOs and merchants alike trust in the commit-ments we make. Every guaranteed check, every voiceauthorization, every technical-support call is an individualcommitment.”

All in all, Lin has accomplished most of what he set out todo. The company continues to grow at a dramatic pace,attrition remains remarkably low, new services and prod-ucts continue to be developed, but, most of all, he will tellyou that he is having fun.

Page 31

Page 34

Attention, ISOs! Do yourmerchants just want to beable to drag and drop? Doyour merchants want to be

free from lengthy leases and compli-cated contracts? Do your merchantswant to pay an all-inclusive, inex-pensive monthly fee for all of theire-commerce needs?

If the answer to these questions is“yes,” then let GoEmerchant.compresent to you the “Amazing, SuperFantastic, No Experience NecessaryBuy_Me Button.”

All hype aside, this is a story abouttwo individuals who looked at themerchant payment-processing indus-try, sized it up and put out a productthat was developed by listening tomerchants. From small beginningsin the basement of a family-ownedPhiladelphia five-and-dime store,Gary Dvorkin and James Battista,veterans of the computer hardwarebusiness, created GoEmerchant.comusing what they knew best to pro-vide easy-to-use products at reason-able prices.

The result: the first horizontal andvertical integrated service providerof its kind.

“Our technology was so revolution-ary at the time, we were convincedsomeone would steal it from us, butno one found us,” says Dvorkin, thecompany’s CEO.

What exactly is this revolutionarytechnology? According to Dvorkin,it’s all about automation with secure

gateways for transaction processing.

“We own it all,” says Dvorkin,whose company has both U.S. andinternational patents on the entiredrag-and-drop Buy_Me Button tech-nology process. “We work throughseveral processors, giving merchantsmore than an Internet store that isbrain-dead-easy to set up. We givethem an Internet store product, aBuy_Me Button and a Buy_MeButton Creator.”

GoEmerchant.com heard merchantslament, “Don’t you have anything Ican just drop on my Web page?”Dvorkin says, “What we had weremerchants telling us what they need-ed, and we figured out how to filltheir need. We’re not brilliant. Wejust developed an information chan-nel and control system.

“Every time we heard somethingrepeated two or three times a day, itwas sent to development. If you lis-ten to people in business, what theysay is pretty sensible. We are mer-chant-centric. I don’t know of anyother companies who can even getthe development community on thephone.”

Sitting in his office one night, settingup stores and monitoring systems,Dvorkin started playing with thebrowser with the HTML editor onone side. Pulling objects off thebrowser and throwing them into theHTML editor, Dvorkin thought,“Why not create an object on thebrowser, drag it from the browserinto the HTML editor and save it on

E-commerce Made E-easy

GoEmerchant.com

ISO contact:James Battista, PresidentPhone: 888-638-7867E-mail: [email protected]

Company address:31 South Eagle Road, Suite 206 Havertown, PA 19083Phone: 888-638-7867Fax: 610-446-1855Web site: www.goemerchant.com

ISO benefits:• Keeps e-commerce transaction

processing simple with “NoExperience Necessary Buy_MeButton.”

the HTML page, and then post it on the Internet, keepingthe button on the page?”

Two and a half weeks later, enter the “Amazing, SuperFantastic, No Experience Necessary Buy_Me Button.”Within two weeks, GoEmerchant.com was selling 5 to 1with the Buy_Me Button. Merchants were able to keeptheir Web site with its current design and just drop in a but-ton to provide for e-commerce transactions.

But Dvorkin didn’t stop there. His next vision was toaggregate GoEmerchant.com’s e-commerce solutions andbundle them all, leaping from selling a single product to abundled e-commerce product set. Sales soared again.

Dvorkin’s inspiration continued. Watching transactionreports, seeing the Buy_Me Button stores moving morequickly because of their vertical e-commerce enabledprocess, Dvorkin asked himself, “What if these peoplecould make an e-mail to all their customers containing agraphic, product description and a Buy_Me Button?”

It would be an efficient way to reach out to customerswithout having them go to the merchant Web site.CyberCircular was born. An interface through which anymerchant could type in their name, upload graphics, buildan e-mail and send it to a customer list,GoEmerchant.com’s patented CyberCircular sent transac-tions soaring even higher, giving merchants the advantageof impulse purchasing.

“Our hot product is our E-commerce Total package,”Dvorkin says. “With one merchant account, you get anInternet store, the Buy_Me Button Builder and Creator,CyberCircular, a stats package and a financial-manage-ment console.”

An added plus to the package is that batch transactions arenot written in bank language. “We want merchants tounderstand what they’re doing,” Dvorkin says. “We makeit as simple and easy as possible.”

Page 35

“No one is doing it the way we’re doingit. First, they must have the technologyand a sales force who know how to sellit. We close better than 36 percent of ourinbound sales leads, and we have lessthan 3 percent attrition.”

—Gary Dvorkin, CEO, GoEmerchant

What sets GoEmerchant.com apart from other e-com-merce solution providers?

“No one is doing it the way we’re doing it,” Dvorkin says.“First, they must have the technology and a sales forcewho know how to sell it. We close better than 36 percentof our inbound sales leads, and we have less than 3 percentattrition. We have taken a lot of time to set up a system thatallows our sales people to sell our products. There areother companies that have stores, gateways, etc., but wehave it all. We even own our own multiprocessor, certi-fied-transaction gateway.”

There is clear-cut appeal to ISOs. Consider the two optionsGoEmerchant.com offers.

“First, if you are a NOVA guy, you can brand our product,own the merchant account, discount-rate the product andbrand it as your own,” Dvorkin says. “If you’re an NDCreseller, you can do the same thing. We work directly withNOVA and NDC. We also are working with Concord EFSas well.”

The second ISO scenario involves simply passing a leadon to GoEmerchant.com and receiving a finder’s fee, so tospeak. “Send us a lead and we will send you back $265 foreach lead closed,” says Dvorkin.

For the lead option, the agent clicks over toGoEmerchant.com’s Web site and fills out a form. Once itis submitted, the seller automatically creates his or herown reseller site. The agent agrees to a reseller agreementand enters in his or her own information as related to theWeb site, creating a Web address to which the ISO cansend all business.

“The ISO notifies all their customers that they now havean e-commerce package that has their brand on,” Dvorkinsays. “Those leads are automatically generated to

Page 37

“We want it to be the way that small tomidsize businesses can stick their toesin the water and see if it works forthem.”

— Gary Dvorkin, CEO, GoEmerchant

GoEmerchant.com’s sales office. Forthese transactions, there is no ISOownership on these merchantaccounts, no residuals. But they doget $265 up front.”

If ISOs prefer to own the merchantaccount and receive residuals, that’sthe GoEmerchant.com “BrandedISO Program.”

“We give them a discounted buy ratefor the product, and they determinethe set-up frees and discount rates,”Dvorkin says. “They are basicallyjust buying the product from uswholesale.”

ISOs enter their merchant data intoGoEmerchant.com’s merchant-enrollment process, andGoEmerchant.com handles all tech-nicalities.

“The ISOs own these accounts,”Dvorkin says. “GoEmerchant.comACH’s merchants for their piece of

the pie.”

The catch is that this program is onlyavailable to NOVA resellers, NDCresellers and Concord EFS resellers.GoEmerchant.com has 2,700resellers.

The appeal to merchants, on theother hand, is the “no lease, no con-tract” aspect of GoEmerchant.com.

“We didn’t want merchants signingup without education,” saysDvorkin. “No set-up fee meant wewouldn’t charge anything. Ours is avirtual-tenancy, at-will program –pay as you go, every month.”

The monthly cost is $49.95 with noadvance notice in writing needed tocancel the service. It’s an easy-in,easy-out process thatGoEmechant.com hopes will facili-tate e-commerce to everyone whowants it.

“We want it to be the way that smallto midsize businesses can stick theirtoes in the water and see if it worksfor them,” Dvorkin says.

GoEmerchant.com knows that if itworks for them, their merchants willstay ... and they are staying, even inthese times of “dotcomaphobia.”

“If they get up on the Web, it is acompendium to their sales efforts,”Dvorkin says. “They don’t have towait for traffic using theCyberCircular, using the Buy_MeButton. We give them a gateway, anInternet store and all the trimmings.They’re not going to get this any-where else.”

Where else can merchants puttogether a list of their customers, gettheir e-mail addresses, load them inand send out e-mails with their bestmerchandise and see how many buyfrom them? ISOs, wouldn’t you allbecome golden to your merchants!

Page 38

No lion . . . you’ll love this program!Merchants’ Choice Card Services-the industry king of Customer Service &Tech Support- Competitive discount rates

- Transaction fee income including Debit and EBT

- Income from statement fees

- Rollover Bonuses

- American Express bonus and residual income

- Discover and Diners Club bonuses

- No liability for merchant losses

- Same-day approvals

- Liberal underwriting

- Guaranteed equipment leasing

Call 800-478-9367 to go with a proven

team. . . ‘cause it’s a jungle out there!

GoEmerchant.com also has the big boys using its e-com-merce packaging. About 6,000 merchants are enjoyingGoEmerchant.com, with 400 to 700 accounts being addedper month.

What does GoEmerchant.com attribute to this ramp-up?Dvorkin believes that merchants need to find the ease ofthe facilitation of e-commerce, the real-world profitabilityof it rather than the dreamscape scenario.

“The bottom line – e-commerce was confusing,” hesays. “Suppose you had invented the wheel and ithad eight corners on it. That was the problem withe-commerce – a lot of the stuff out there made nosense. The first thing we understood was that every-thing had to be simple.”

GoEmerchant.com strives to share that simple phi-losophy with sales training.

“Depending on the size of the ISO, we will sendsomeone down to train them,” Dvorkin says. “Wealso have in-house training. We will also give ad

slicks, the whole nine yards.”

GoEmerchant.com also offers free customer support witha real live person from 7 a.m. to 10 p.m. EST.Headquartered in Havertown, Pa., and Cherry Hill, N.J.,GoEmerchant.com has an in-house staff of 72.

“Ours is a David vs. Goliath story where David just had aclearer vision of the future and, therefore, prevailed,”Dvorkin says.

Page 39

Call Integrated Leasing for details

800-398-9701

How Does .02699 Sound?(Unbelievable? It’s the real deal.)

Fastest Turn-around

Great Personal Service

Most Flexible Lease Programs

you have no idea.

Crazy...Crazy...

“The bottom line – e-commerce was confusing.Suppose you had invented the wheel and ithad eight corners on it. That was the problemwith e-commerce – a lot of the stuff out theremade no sense. The first thing we understoodwas that everything had to be simple.”

— Gary Dvorkin, CEO, GoEmerchant

The figures are staggering:1.7 million bad checkswritten per day and $15billion in check fraud in

2000, with a 12 to 17 percent riseexpected this year. Add in fraudulentcredit cards, mortgages and loans,and the total grows to $60 billion.

How many bad checks did your mer-chants unwittingly take today? Andwhat impact does it have, not just ontheir business but also on yours?

Check fraud has become a hugeissue, and Identico Systems hascome up with a powerful new solu-tion – a tactical service called TrueID.

It all started in 1996 when someonestole a credit card belonging to BobHouvener, co-founder of Image DataLLC, which recently changed itsname to Identico Systems. He could-n’t figure out why the crook hadn’tgotten caught when he used it.

Being an engineer, Bob sought tofind a solution. He tried differentmethods to verify identity but quick-ly realized there was no real way toverify who the person was at thepoint-of-sale. Believing there had tobe a reliable and inexpensive wayfor merchants to use a product thatalso was inoffensive to consumers,Houvener searched biometrics anddata-based solutions.

Identico Systems’ original conceptwas to acquire databases of people’simages from each state’s Departmentof Motor Vehicles through a swipe

device at the point-of-sale. ButIdentico Systems soon discoveredthat the DMV data itself was rifewith fraud – multiple individualsusing one driver’s license, deceasedpeople’s driver’s licenses beingused, several people on one SocialSecurity number. DMV’s screeningwasn’t as reliable as IdenticoSystems had hoped.

Then there were political issues.When the media raised the privacyissue of DMV selling its data in cer-tain states, politicians jumped on thatbandwagon and made it difficult foroutside organizations to secureDMV data for identification purpos-es.

Identico Systems met those chal-lenges with a complete redesign ofits service. Rather than acquiringdata from the DMV, IdenticoSystems acquired it directly from theconsumer at the point-of-sale. Theresult: True ID, an enrollment trans-action that scans the consumer’s dri-ver’s license at the point-of-sale,captures the person’s data and storesit in a secure, encrypted database forpresent and future use.

True ID’s loss-prevention servicesare based on Identico Systems’ prin-ciple that the most secure and cost-effective method of preventing iden-tity-based fraudulent transactions isthrough real-time digital image veri-fication at the point-of-service. TheTrue ID services use real-time cus-tomer image verification to proac-tively prevent check, credit card,application and other losses related

Page 41

Facing Off with FraudIdentico Systems

ISO contact:Neil Fallon, VP of SalesPhone: 603-598-7500, ext. 139E-mail: [email protected]

Company address:15 Charron AvenueNashua, NH 03063Phone: 603-598-7500Fax: 603-886-9699Web site:

www.identicosystems.com

ISO benefits:• True ID loss-prevention services,

with built-in security and extraor-dinary attention to detail

• Turns merchants’ fraud-related loss-es into profits

• Keeps process simple• “Service-intensive approach” to

ISOs• Up-front fee and recurring revenue

for ISOs

to identity fraud.