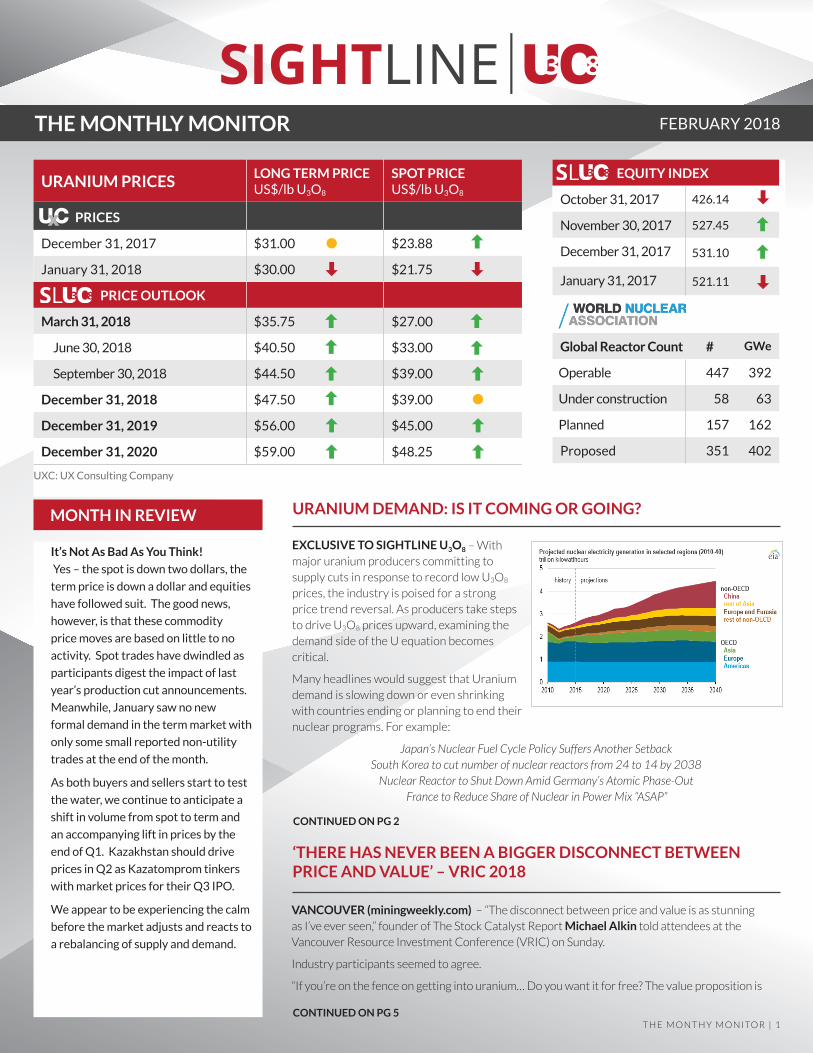

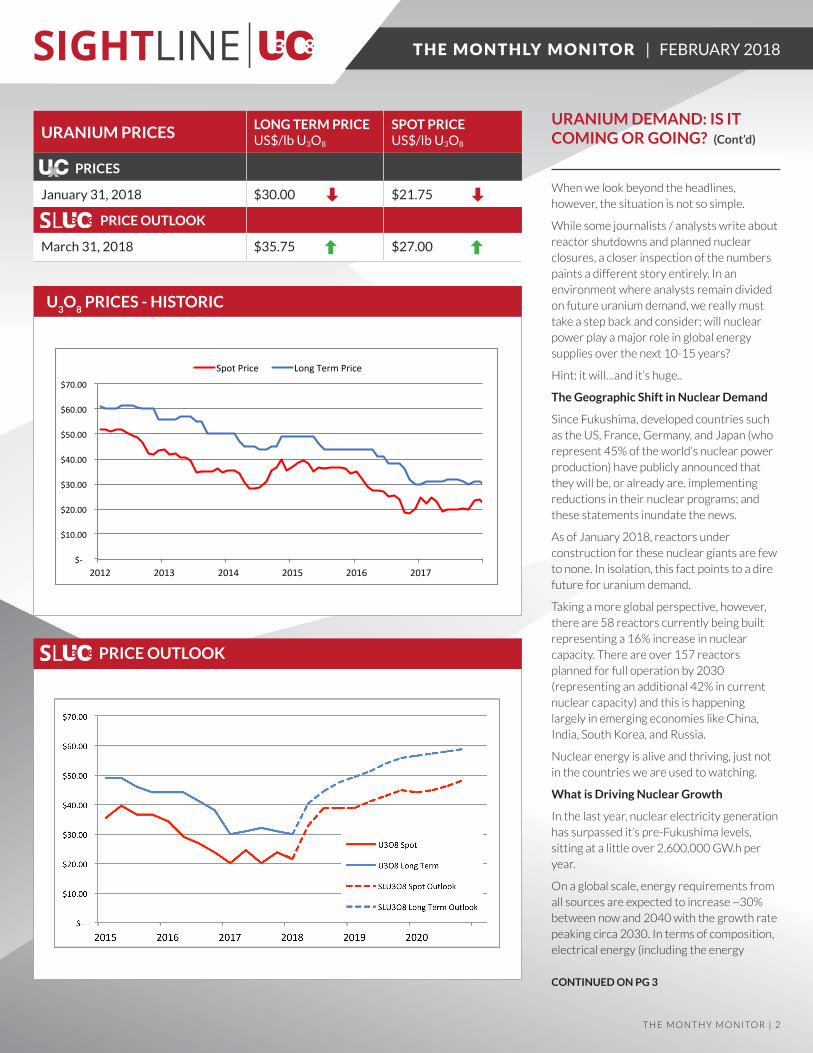

THE MONTHLY MONITOR MONTH IN REVIEW URANIUM DEMAND: IS IT COMING OR GOING? ‘THERE HAS NEVER BEEN A BIGGER DISCONNECT BETWEEN PRICE AND VALUE’ – VRIC 2018 It’s Not As Bad As You Think! Yes – the spot is down two dollars, the term price is down a dollar and equities have followed suit. The good news, however, is that these commodity price moves are based on little to no activity. Spot trades have dwindled as participants digest the impact of last year’s production cut announcements. Meanwhile, January saw no new formal demand in the term market with only some small reported non-utility trades at the end of the month. As both buyers and sellers start to test the water, we continue to anticipate a shift in volume from spot to term and an accompanying lift in prices by the end of Q1. Kazakhstan should drive prices in Q2 as Kazatomprom tinkers with market prices for their Q3 IPO. We appear to be experiencing the calm before the market adjusts and reacts to a rebalancing of supply and demand. EXCLUSIVE TO SIGHTLINE U 3 O 8 – With major uranium producers committing to supply cuts in response to record low U 3O8 prices, the industry is poised for a strong price trend reversal. As producers take steps to drive U 3O8 prices upward, examining the demand side of the U equation becomes critical. Many headlines would suggest that Uranium demand is slowing down or even shrinking with countries ending or planning to end their nuclear programs. For example: Japan’s Nuclear Fuel Cycle Policy Suffers Another Setback South Korea to cut number of nuclear reactors from 24 to 14 by 2038 Nuclear Reactor to Shut Down Amid Germany’s Atomic Phase-Out France to Reduce Share of Nuclear in Power Mix “ASAP” VANCOUVER (miningweekly.com) – “The disconnect between price and value is as stunning as I’ve ever seen,” founder of The Stock Catalyst Report Michael Alkin told attendees at the Vancouver Resource Investment Conference (VRIC) on Sunday. Industry participants seemed to agree. “If you’re on the fence on getting into uranium… Do you want it for free? The value proposition is THE MONTHY MONITOR | 1 URANIUM PRICES LONG TERM PRICE US$/lb U 3 O 8 SPOT PRICE US$/lb U 3 O 8 PRICES December 31, 2017 $31.00 $23.88 January 31, 2018 $30.00 $21.75 PRICE OUTLOOK March 31, 2018 $35.75 $27.00 June 30, 2018 $40.50 $33.00 September 30, 2018 $44.50 $39.00 December 31, 2018 $47.50 $39.00 December 31, 2019 $56.00 $45.00 December 31, 2020 $59.00 $48.25 EQUITY INDEX October 31, 2017 426.14 November 30, 2017 527.45 December 31, 2017 531.10 January 31, 2017 521.11 Global Reactor Count # GWe Operable 447 392 Under construction 58 63 Planned 157 162 Proposed 351 402 FEBRUARY 2018 CONTINUED ON PG 2 CONTINUED ON PG 5 UC x UXC: UX Consulting Company

Transcript

THE MONTHLY MONITOR

MONTH IN REVIEW URANIUM DEMAND: IS IT COMING OR GOING?

‘THERE HAS NEVER BEEN A BIGGER DISCONNECT BETWEEN PRICE AND VALUE’ – VRIC 2018

It’s Not As Bad As You Think!

Yes – the spot is down two dollars, the

term price is down a dollar and equities

have followed suit. The good news,

however, is that these commodity

price moves are based on little to no

activity. Spot trades have dwindled as

participants digest the impact of last

year’s production cut announcements.

Meanwhile, January saw no new

formal demand in the term market with

only some small reported non-utility

trades at the end of the month.

As both buyers and sellers start to test

the water, we continue to anticipate a

shift in volume from spot to term and

an accompanying lift in prices by the

end of Q1. Kazakhstan should drive

prices in Q2 as Kazatomprom tinkers

with market prices for their Q3 IPO.

We appear to be experiencing the calm

before the market adjusts and reacts to

a rebalancing of supply and demand.

EXCLUSIVE TO SIGHTLINE U3O8 – With

major uranium producers committing to supply cuts in response to record low U3O8 prices, the industry is poised for a strong price trend reversal. As producers take steps to drive U3O8 prices upward, examining the demand side of the U equation becomes critical.

Many headlines would suggest that Uranium demand is slowing down or even shrinking with countries ending or planning to end their nuclear programs. For example:

Japan’s Nuclear Fuel Cycle Policy Suffers Another SetbackSouth Korea to cut number of nuclear reactors from 24 to 14 by 2038

Nuclear Reactor to Shut Down Amid Germany’s Atomic Phase-OutFrance to Reduce Share of Nuclear in Power Mix “ASAP”

VANCOUVER (miningweekly.com) – “The disconnect between price and value is as stunning as I’ve ever seen,” founder of The Stock Catalyst Report Michael Alkin told attendees at the Vancouver Resource Investment Conference (VRIC) on Sunday.

Industry participants seemed to agree.

“If you’re on the fence on getting into uranium… Do you want it for free? The value proposition is

When we look beyond the headlines, however, the situation is not so simple.

While some journalists / analysts write about reactor shutdowns and planned nuclear closures, a closer inspection of the numbers paints a different story entirely. In an environment where analysts remain divided on future uranium demand, we really must take a step back and consider; will nuclear power play a major role in global energy supplies over the next 10-15 years?

Hint: it will…and it’s huge..

The Geographic Shift in Nuclear Demand

Since Fukushima, developed countries such as the US, France, Germany, and Japan (who represent 45% of the world’s nuclear power production) have publicly announced that they will be, or already are, implementing reductions in their nuclear programs; and these statements inundate the news.

As of January 2018, reactors under construction for these nuclear giants are few to none. In isolation, this fact points to a dire future for uranium demand.

Taking a more global perspective, however, there are 58 reactors currently being built representing a 16% increase in nuclear capacity. There are over 157 reactors planned for full operation by 2030 (representing an additional 42% in current nuclear capacity) and this is happening largely in emerging economies like China, India, South Korea, and Russia.

Nuclear energy is alive and thriving, just not in the countries we are used to watching.

What is Driving Nuclear Growth

In the last year, nuclear electricity generation has surpassed it’s pre-Fukushima levels, sitting at a little over 2,600,000 GW.h per year.

On a global scale, energy requirements from all sources are expected to increase ~30% between now and 2040 with the growth rate peaking circa 2030. In terms of composition, electrical energy (including the energy

generated from nuclear sources) is projected to grow at twice that rate (60%), meeting an increasing portion of future energy demand.

Coincidentally, this projected energy growth is primarily concentrated in emerging economies with large population growth and an emerging middle class driving the increase. Countries like China and India are already building and planning to build nuclear reactors to meet these future requirements.

With emission levels a hot topic, countries with high projected growth are already taking steps to make emission friendly, nuclear energy a bigger portion of their future energy delivery mix. The data shows growth in nuclear energy is positively correlated with the growth in electricity demand.

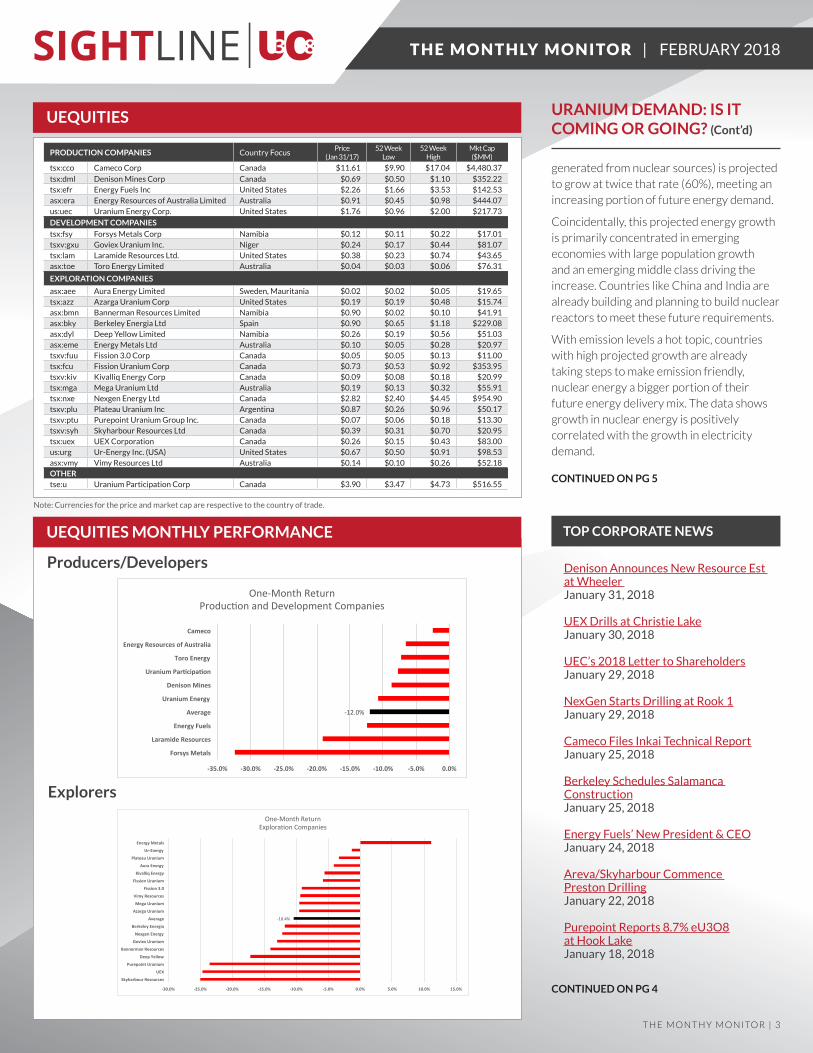

tsx:dml Denison Mines Corp Canada $0.69 $0.50 $1.10 $352.22 tsx:efr Energy Fuels Inc United States $2.26 $1.66 $3.53 $142.53 asx:era Energy Resources of Australia Limited Australia $0.91 $0.45 $0.98 $444.07 us:uec Uranium Energy Corp. United States $1.76 $0.96 $2.00 $217.73

DEVELOPMENT COMPANIES

tsx:fsy Forsys Metals Corp Namibia $0.12 $0.11 $0.22 $17.01 tsxv:gxu Goviex Uranium Inc. Niger $0.24 $0.17 $0.44 $81.07 tsx:lam Laramide Resources Ltd. United States $0.38 $0.23 $0.74 $43.65 asx:toe Toro Energy Limited Australia $0.04 $0.03 $0.06 $76.31

EXPLORATION COMPANIES

asx:aee Aura Energy Limited Sweden, Mauritania $0.02 $0.02 $0.05 $19.65 tsx:azz Azarga Uranium Corp United States $0.19 $0.19 $0.48 $15.74 asx:bmn Bannerman Resources Limited Namibia $0.90 $0.02 $0.10 $41.91 asx:bky Berkeley Energia Ltd Spain $0.90 $0.65 $1.18 $229.08 asx:dyl Deep Yellow Limited Namibia $0.26 $0.19 $0.56 $51.03 asx:eme Energy Metals Ltd Australia $0.10 $0.05 $0.28 $20.97 tsxv:fuu Fission 3.0 Corp Canada $0.05 $0.05 $0.13 $11.00 tsx:fcu Fission Uranium Corp Canada $0.73 $0.53 $0.92 $353.95 tsxv:kiv Kivalliq Energy Corp Canada $0.09 $0.08 $0.18 $20.99 tsx:mga Mega Uranium Ltd Australia $0.19 $0.13 $0.32 $55.91 tsx:nxe Nexgen Energy Ltd Canada $2.82 $2.40 $4.45 $954.90 tsxv:plu Plateau Uranium Inc Argentina $0.87 $0.26 $0.96 $50.17 tsxv:ptu Purepoint Uranium Group Inc. Canada $0.07 $0.06 $0.18 $13.30 tsxv:syh Skyharbour Resources Ltd Canada $0.39 $0.31 $0.70 $20.95 tsx:uex UEX Corporation Canada $0.26 $0.15 $0.43 $83.00 us:urg Ur-Energy Inc. (USA) United States $0.67 $0.50 $0.91 $98.53 asx:vmy Vimy Resources Ltd Australia $0.14 $0.10 $0.26 $52.18 OTHERtse:u Uranium Participation Corp Canada $3.90 $3.47 $4.73 $516.55

CONTINUED ON PG 5

CONTINUED ON PG 4

Note: Currencies for the price and market cap are respective to the country of trade.

Denison Announces New Resource Est at Wheeler January 31, 2018

and projected to grow for at least another 20 years. This growth is concentrated in emerging markets and it is these countries that are taking steps to meet energy requirements with nuclear sources.

As population growth slows in developed economies, more funding is allocated towards alternate energies. However, this certainly does not mean the mass decommissioning of existing reactors in developed states.

Globally, both reactors planned and reactors under construction are at an all time high. Nuclear energy creation is projected to continue its strong growth, with more reactors being built now than ever before.

To offset the nuclear growth in emerging economies the world would have to shut down and replace 70 reactors by 2021 and 253 reactors by 2030. That’s more operable reactors than France, Germany, US, UK, South Korea, and Japan have combined.

It’s just not going to happen.

URANIUM DEMAND: IS IT COMING OR GOING? (Cont’d)

T H E M O N T H Y M O N I TO R | 5

T H E M O N T H LY M O N I TO R | FEBRUARY 2018

Countries with high population growth and high electricity demands are driving record high reactor constructions which will very likely continue to drive nuclear demand for at least the next 10-15 years.

How Easy is Switching Out of Nuclear, Really?

For countries that want to reduce nuclear reliance, there is a need to replace any reactors phased out with an alternative source. Simply not meeting energy demands is not an option.

Think of alternative energy as coming from two sources: fossil fuels (coal, gas, etc.) or renewable energy (wind, solar, arguably hydro). The viability of these alternatives is a critical determinant for the rate at which nuclear power can be phased out.

History has proven that quickly replacing nuclear energy with another low emission fuel is impossible.

A perfect example is Japan, where nuclear energy reliance dropped from 29.2% to ~2% in the span of 2 years (2010-2012). When Japan began shutting down nuclear reactors seven years ago, it replaced that energy with fossil fuels not renewable energy. Even with emissions rising rapidly, Japan has continued to burn fossil fuel while their reactors sit on standby.

Switching out of one fuel type into another, especially in the face of rising energy and emission requirements, is like changing the tires on a moving car. Renewable energy is simply not at a stage where it can replace more consistent energy sources (nuclear/ fossil fuels) in the short term and excessive fossil fuel use derails emissions objectives.

You Won’t Be Seeing Mass Nuclear Shut Downs

Given the difficulty of a quick shift from uranium energy for countries already heavily invested in nuclear power, it is worthwhile to revisit the nuclear positions of countries promising nuclear phase-out.

When you read that countries are planning to lessen their dependence on nuclear energy by a certain date, it is important to remember that electricity requirements are usually rising during the same time.

Nuclear growth at a lower rate than overall

energy growth would certainly accomplish the goal of lessened reliance on uranium, especially on a global scale.

Nuclear share of electricity for countries touting phase-outs such as France, South Korea and the US has barely moved in the last 10 years. Couple this with low investments in new reactors and one can certainly make the argument for the investment in alternate energy to meet any rising demand rather than mass decommissioning and replacement of existing nuclear reactors.

The US for example has only had a 5% reduction in the total number of operable reactors since 2008. France has only taken one reactor offline in that time. Contrary to what media headlines and politicians might suggest, there will be no mass closing of existing nuclear reactors.

Global Nuclear Demand Won’t Fall, It Will Rise

The world’s demand for energy is growing

‘THERE HAS NEVER BEEN A BIGGER DISCONNECT BETWEEN PRICE AND VALUE’ – VRIC 2018 (Cont’d)

CONTINUED ON PG 6

so compelling for uranium, it is bound to return in the future. It requires some homework on the investor’s part, but once you do your homework, you’ll realise that you are buying future value for a song,” US uranium miner Uranium Energy Corp president and CEO Amir Adnani told a panel.

“We can sit here and beat up about utilities not contracting. The fact remains, they have always acted counter intuitively, thinking uranium prices will remain so low for long. As Rick Rule says it best: ‘It’s not a matter of if, but when’,” noted Fission Uranium president and CEO Dev Randhawa.

The industry is dealing with a sideways-crawling uranium price around the $20/lb-mark, amid low demand and an acute oversupply of yellowcake for several quarters now, despite a slew of production cuts and mine closures by the world’s largest producers – Kazakhstan’s Kazatomprom and Canada’s Cameco.

According to Randhawa, Fission’s 20% Chinese-based partner CGN – which he describes as the

‘THERE HAS NEVER BEEN A BIGGER DISCONNECT BETWEEN PRICE AND VALUE’ – VRIC 2018 (Cont’d)

T H E M O N T H Y M O N I TO R | 6

T H E M O N T H LY M O N I TO R | FEBRUARY 2018

ABOUT THE SLU3O8 OUTLOOK

The SLU3O8 Outlook; is an in-depth forecast model, optimized to anticipate the timing and extent of pending changes in uranium prices. Projections are maintained quarterly and based on the analysis of uranium price movement relative to detailed supply and demand changes over the past 15 years.

ABOUT THE SLU3O8 EQUITY INDEX

The SLU3O8 Equity Index tracks the relative share price of a select basket of uranium-based equities, checking the market’s reaction to industry activities. The Index is based on share price movement since January 1, 2012 (1,000.00) of the following companies*:

* As the significant stock price movement of Fission Uranium Corp and NexGen Energy Ltd. is a function of major uranium discoveries, we have not included their stock performance in the Index to better reflect the uranium equities market in general.

ABOUT SIGHTLINE SLU3O8

Sightline U3O8 is a monthly newsletter and supporting website created and maintained to provide uranium investors and industry stakeholders with a single source of insight into the ongoing factors that directly affect uranium prices.

We welcome your comments, questions and ideas. Please contact us at [email protected]

www. sightlineu3o8.com

‘mothership’ of the nuclear power industry – expects the market to be in balance this year, or to tip into deficit territory.

He does not see any suspended production coming back online below a uranium price of $40/lb, by which time the equities of most uranium companies present at the VRIC 2018 would probably have tripled, he quipped.

Skyharbour Resources president and CEO Jordan Trimble noted that the lowest-cost producers are taking production offline. This means that, when the lowest-quartile of production gets taken out, it is very telling that prices will soon rise.

“We’re talking a doubling in prices from $23/lb now,” he says.

Trimble pointed out that about 70% of the higher-priced long-term contracts roll off in the next five years, which means that, with uranium prices at their current historic lows, the higher-priced contracts will be executed at much lower, unsustainable prices. For that reason the majors are taking out supply with meaning to force prices back up to sustainable levels; otherwise, they risk shutting down.

GoviEx Uranium CEO Daniel Major added that the uranium enrichment side is in the same hot water as the uranium producers, staring down the spectre of lower-priced long-term contract prices.

“We are never going to see another buying window like this ever again. If you are willing to bet on global population growth, you cannot bet against nuclear growth,” UEC’s Adnani advised. “We need electricity in increasing intensity for everything going forward.”

He added that there was a significant opportunity for uranium production opening up in the US. “The US has the best supply/demand fundamentals of any commodity. With 99 commercial nuclear power reactors, the US has more nuclear reactors than China and India currently have combined.

“A market that demands about 50-million pounds of uranium a year, and produces less than 5% of its own supply, spells opportunity,” he said.