23

OECD/ IOPS Global Forum On Private Pensions Reforming Private DB Plans Istanbul, Nov 2006 Brigitte Miksa, Head of AGI International Pensions

OECD/ IOPS Global Forum On Private Pensions

Reforming Private DB Plans

Istanbul, Nov 2006 Brigitte Miksa, Head of AGI International Pensions

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 2

Private pensions of key importance in pension reforms

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 3

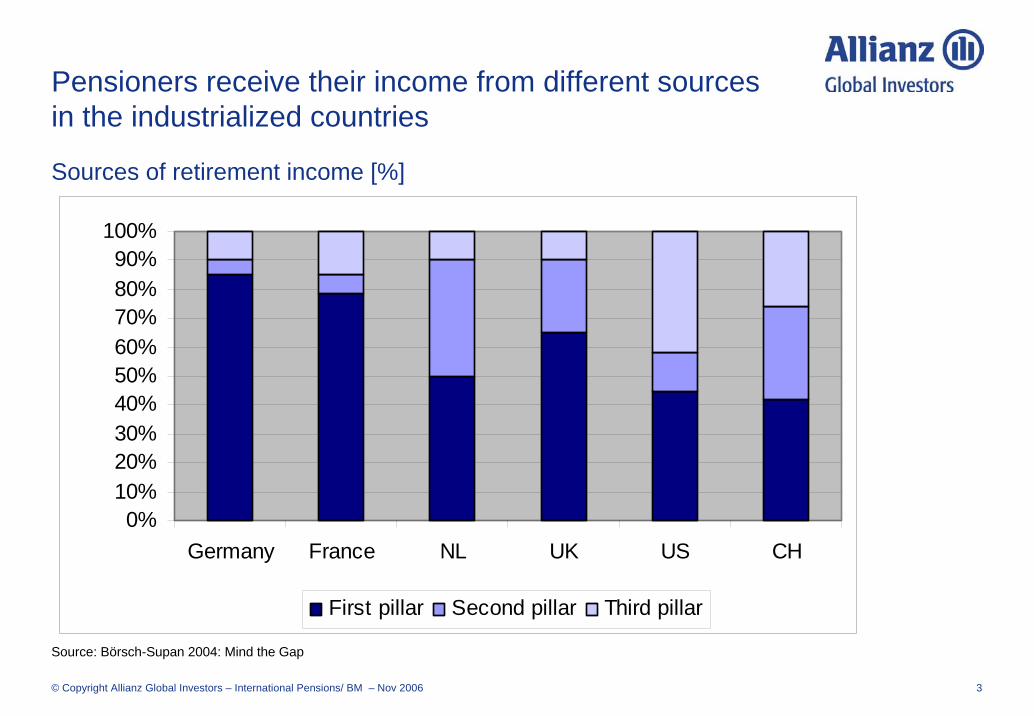

Pensioners receive their income from different sources in the industrialized countries

0%10%20%30%40%50%60%70%80%90%

100%

Germany France NL UK US CH

First pillar Second pillar Third pillar

Source: Börsch-Supan 2004: Mind the Gap

Sources of retirement income [%]

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 4

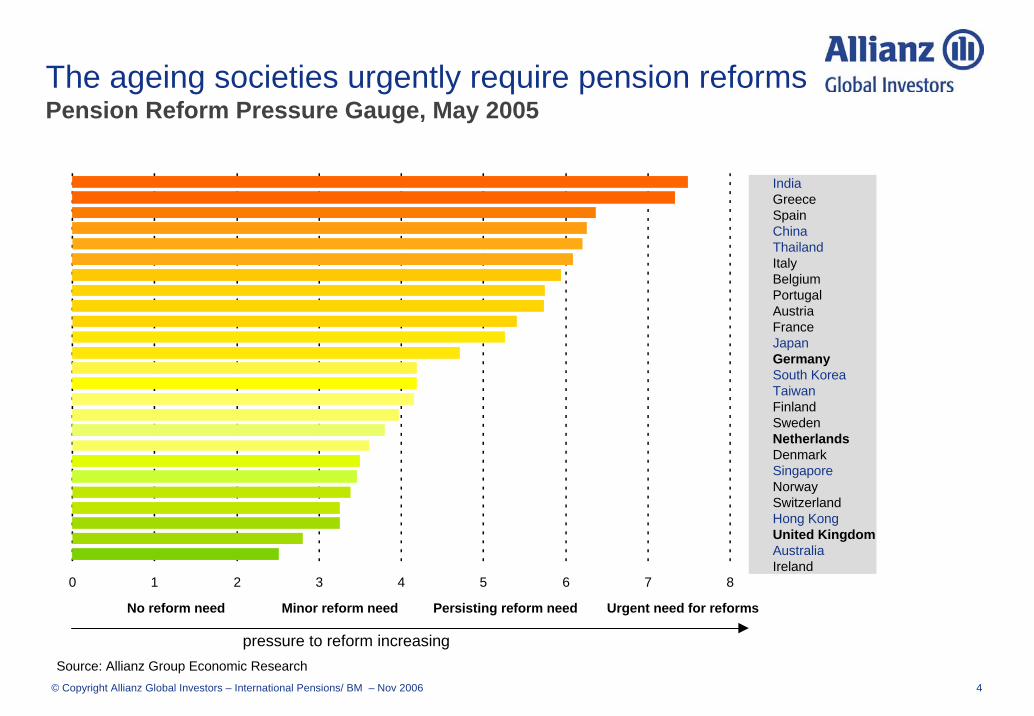

The ageing societies urgently require pension reformsPension Reform Pressure Gauge, May 2005

pressure to reform increasing

No reform need Minor reform need Persisting reform need Urgent need for reforms

Source: Allianz Group Economic Research

IndiaGreeceSpainChinaThailandItalyBelgiumPortugalAustriaFranceJapanGermanySouth KoreaTaiwanFinlandSwedenNetherlandsDenmarkSingaporeNorwaySwitzerlandHong KongUnited Kingdom

IrelandAustralia

0 1 2 3 4 5 6 7 8

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 5

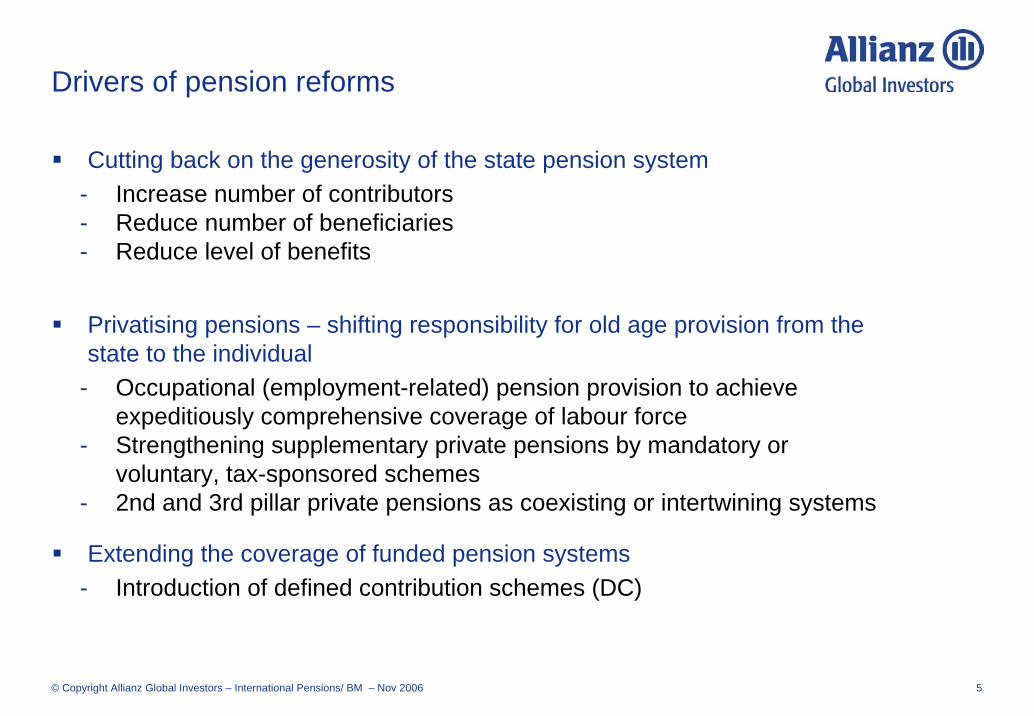

Drivers of pension reforms

Cutting back on the generosity of the state pension system- Increase number of contributors- Reduce number of beneficiaries- Reduce level of benefits

Privatising pensions – shifting responsibility for old age provision from the state to the individual

- Occupational (employment-related) pension provision to achieve expeditiously comprehensive coverage of labour force

- Strengthening supplementary private pensions by mandatory or voluntary, tax-sponsored schemes

- 2nd and 3rd pillar private pensions as coexisting or intertwining systems

Extending the coverage of funded pension systems- Introduction of defined contribution schemes (DC)

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 6

The coverage of occupational pensions varies considerably

Coverage rates of the second pillar [%] 2005

57,0

10,015,0

90

0

10

20

30

40

50

60

70

80

90

100

Germany France Italy NL Sweden UKSource: Center for Research on Pensions and Welfare Policies Turin (CeRP) / EU

90

43

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 7

Reforming DB plans – shift to DC

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 8

Occupational pensions - the distribution of DB and DC plans across countries is inconsistent

6535United States

7822United Kingdom

397Spain

919Netherlands

1000Germany

937Canada

1783Australia

DB plansDC plansCountry

Source: OECD Pension Markets in Focus October 2006

DC and DB plan assets distribution [%] 2004

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 9

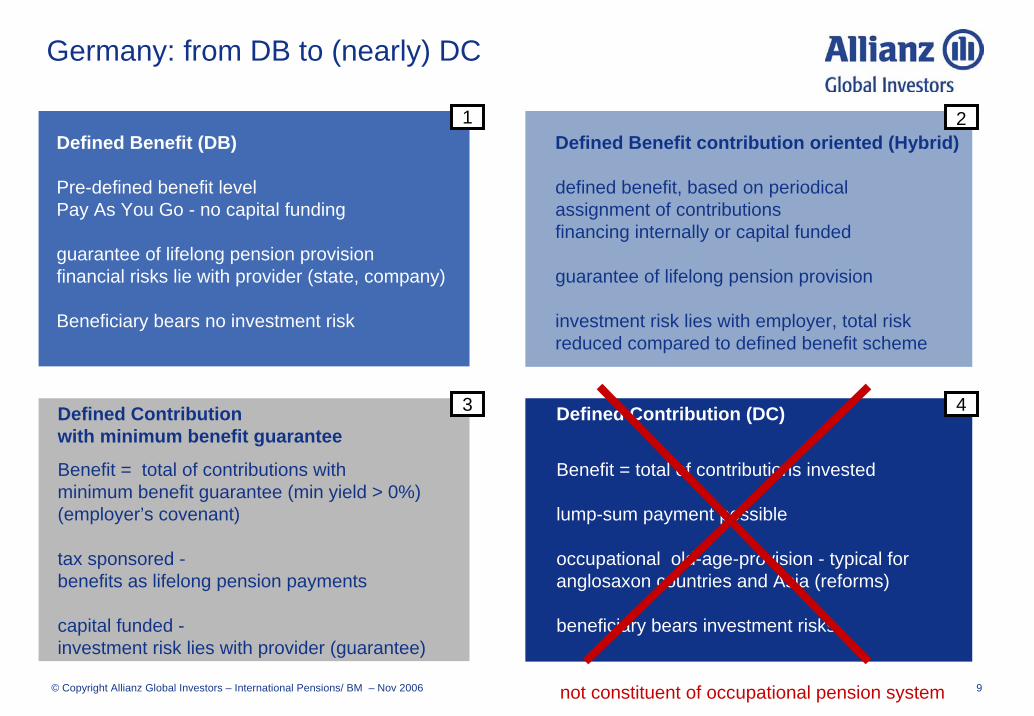

Germany: from DB to (nearly) DC

Defined Benefit (DB) Defined Benefit contribution oriented (Hybrid)

Pre-defined benefit level defined benefit, based on periodical Pay As You Go - no capital funding assignment of contributions

financing internally or capital fundedguarantee of lifelong pension provision financial risks lie with provider (state, company) guarantee of lifelong pension provision

Beneficiary bears no investment risk investment risk lies with employer, total riskreduced compared to defined benefit scheme

Defined Contribution Defined Contribution (DC) with minimum benefit guarantee

Benefit = total of contributions with Benefit = total of contributions investedminimum benefit guarantee (min yield > 0%)(employer’s covenant) lump-sum payment possible

tax sponsored - occupational old-age-provision - typical for benefits as lifelong pension payments anglosaxon countries and Asia (reforms)

capital funded - beneficiary bears investment risksinvestment risk lies with provider (guarantee)

not constituent of occupational pension system

1

43

2

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 10

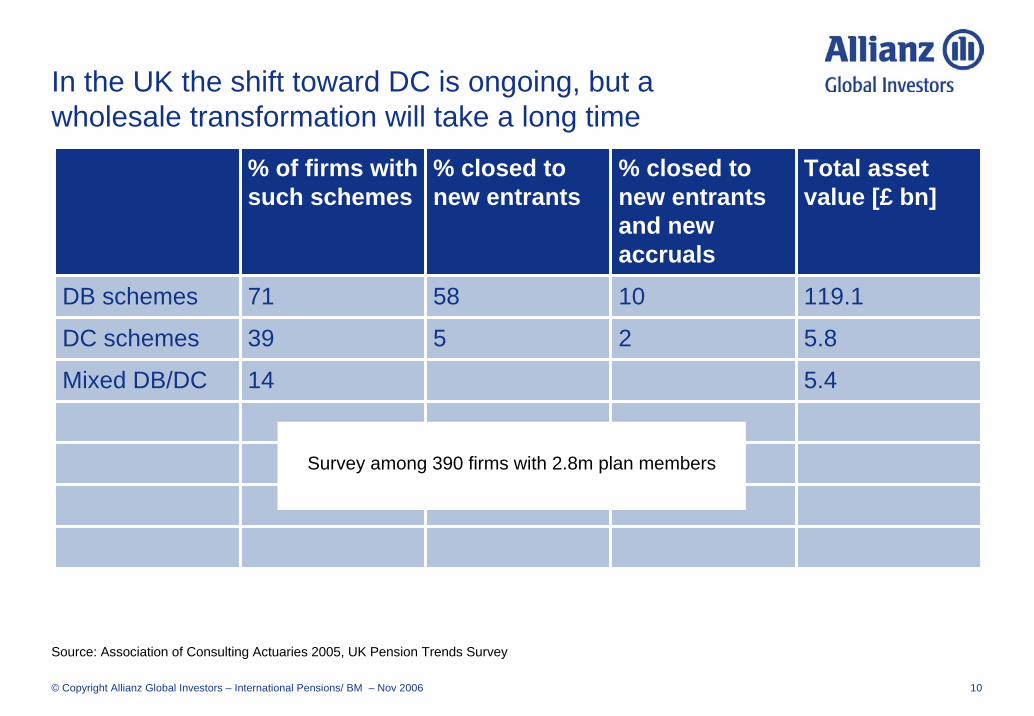

In the UK the shift toward DC is ongoing, but a wholesale transformation will take a long time

% of firms with such schemes

% closed to new entrants

% closed to new entrants and new accruals

Total asset value [£ bn]

DB schemes 71 58 10 119.1

DC schemes 39 5 2 5.8

Mixed DB/DC 14 5.4

Source: Association of Consulting Actuaries 2005, UK Pension Trends Survey

Survey among 390 firms with 2.8m plan members

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 11

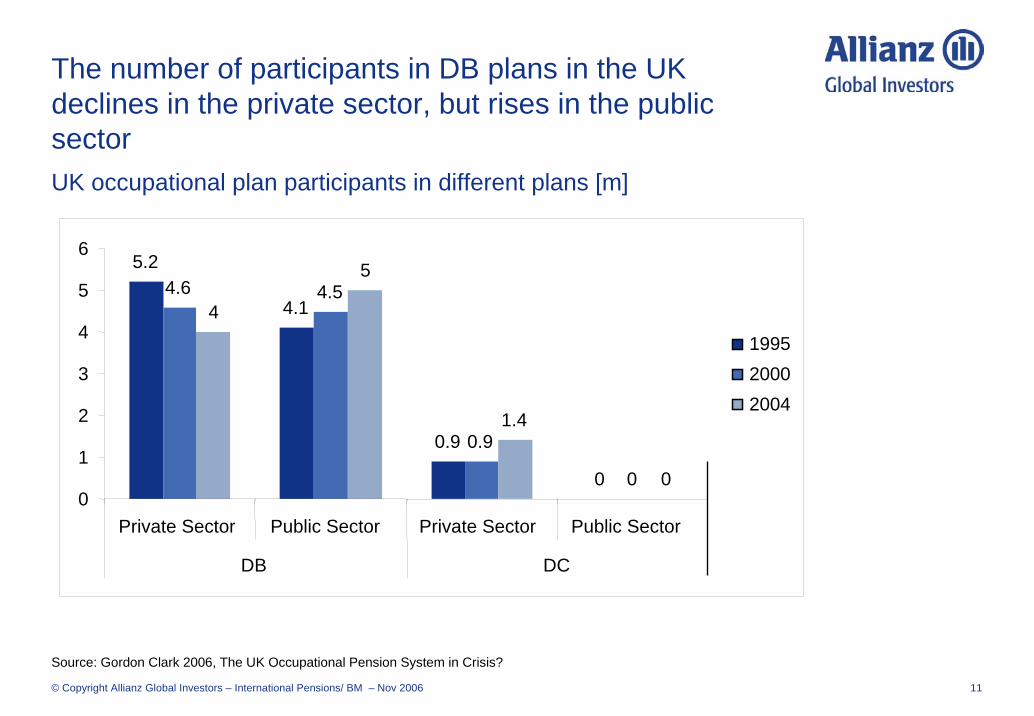

The number of participants in DB plans in the UK declines in the private sector, but rises in the public sector UK occupational plan participants in different plans [m]

Source: Gordon Clark 2006, The UK Occupational Pension System in Crisis?

5.2

4.1

0.9

0

4.6 4.5

0.9

0

4

5

1.4

00

1

2

3

4

5

6

Private Sector Public Sector Private Sector Public Sector

DB DC

199520002004

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 12

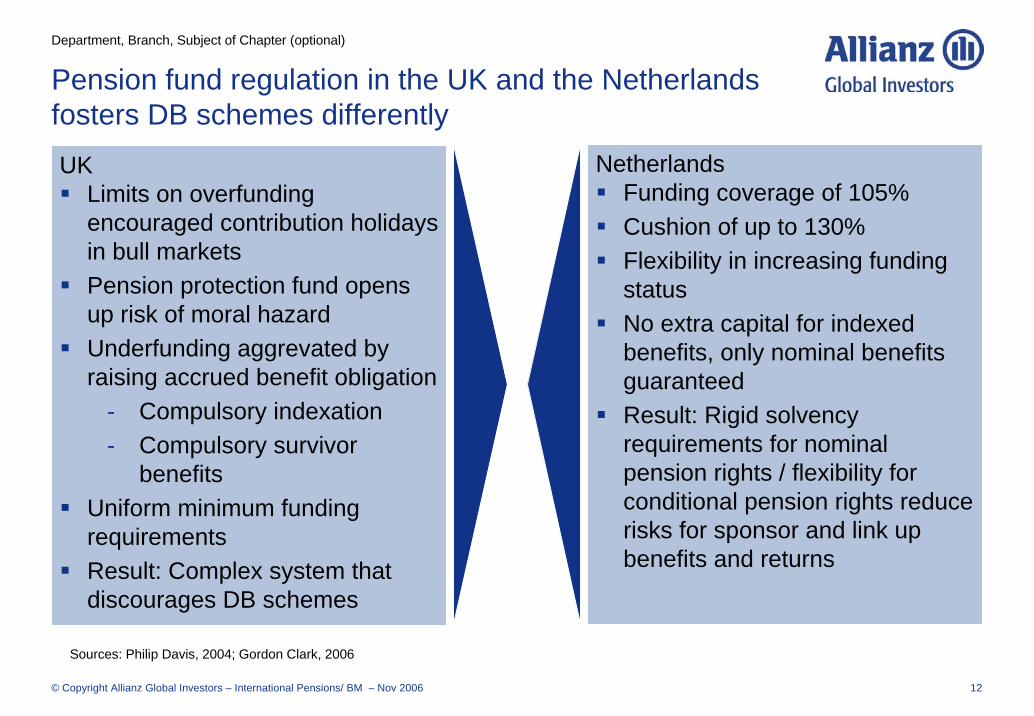

Pension fund regulation in the UK and the Netherlands fosters DB schemes differentlyUK

Limits on overfunding encouraged contribution holidays in bull marketsPension protection fund opens up risk of moral hazardUnderfunding aggrevated by raising accrued benefit obligation

- Compulsory indexation- Compulsory survivor

benefitsUniform minimum funding requirements Result: Complex system that discourages DB schemes

NetherlandsFunding coverage of 105%Cushion of up to 130%Flexibility in increasing funding statusNo extra capital for indexed benefits, only nominal benefits guaranteedResult: Rigid solvency requirements for nominal pension rights / flexibility for conditional pension rights reduce risks for sponsor and link up benefits and returns

Department, Branch, Subject of Chapter (optional)

Sources: Philip Davis, 2004; Gordon Clark, 2006

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 13

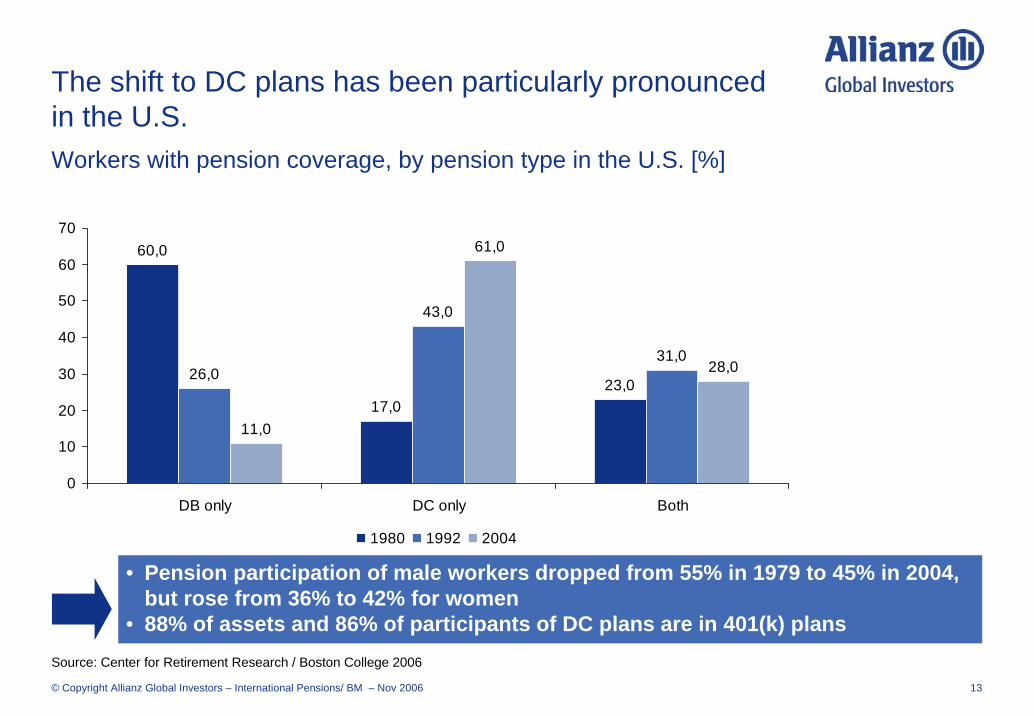

The shift to DC plans has been particularly pronounced in the U.S.Workers with pension coverage, by pension type in the U.S. [%]

60,0

17,023,0

26,0

43,0

31,0

11,0

61,0

28,0

0

10

20

30

40

50

60

70

DB only DC only Both

1980 1992 2004

Source: Center for Retirement Research / Boston College 2006

• Pension participation of male workers dropped from 55% in 1979 to 45% in 2004, but rose from 36% to 42% for women

• 88% of assets and 86% of participants of DC plans are in 401(k) plans

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 14

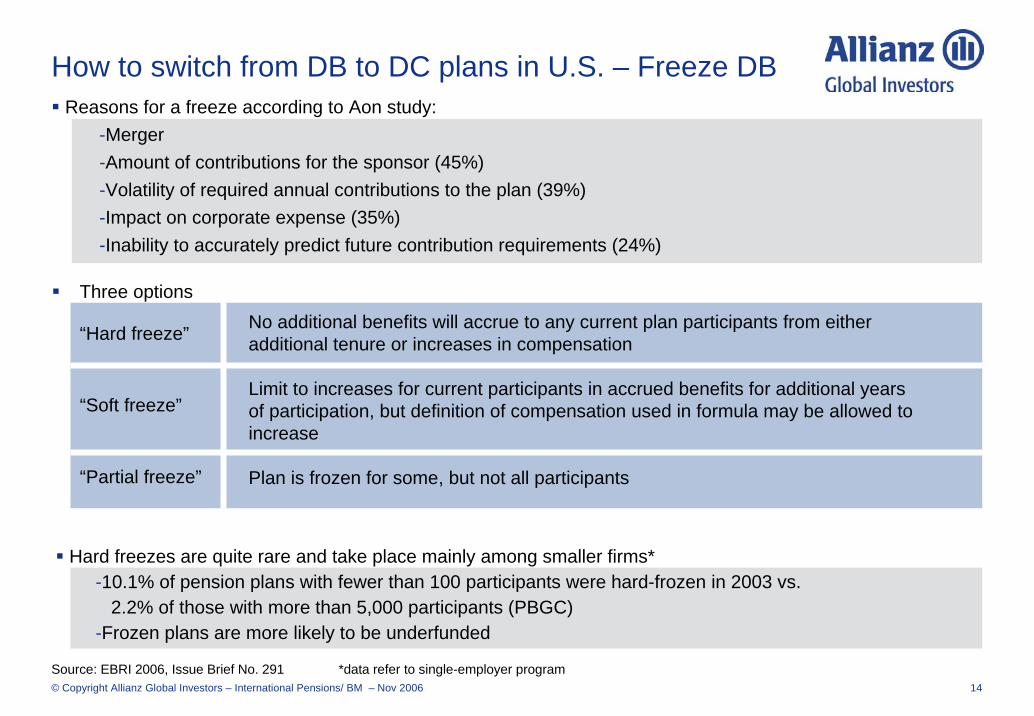

How to switch from DB to DC plans in U.S. – Freeze DB

Three options

“Hard freeze”

“Soft freeze”

“Partial freeze”

No additional benefits will accrue to any current plan participants from either additional tenure or increases in compensation

Limit to increases for current participants in accrued benefits for additional years of participation, but definition of compensation used in formula may be allowed to increase

Plan is frozen for some, but not all participants

Hard freezes are quite rare and take place mainly among smaller firms*-10.1% of pension plans with fewer than 100 participants were hard-frozen in 2003 vs.

2.2% of those with more than 5,000 participants (PBGC)-Frozen plans are more likely to be underfunded

Reasons for a freeze according to Aon study:-Merger-Amount of contributions for the sponsor (45%)-Volatility of required annual contributions to the plan (39%)-Impact on corporate expense (35%)-Inability to accurately predict future contribution requirements (24%)

Source: EBRI 2006, Issue Brief No. 291 *data refer to single-employer program

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 15

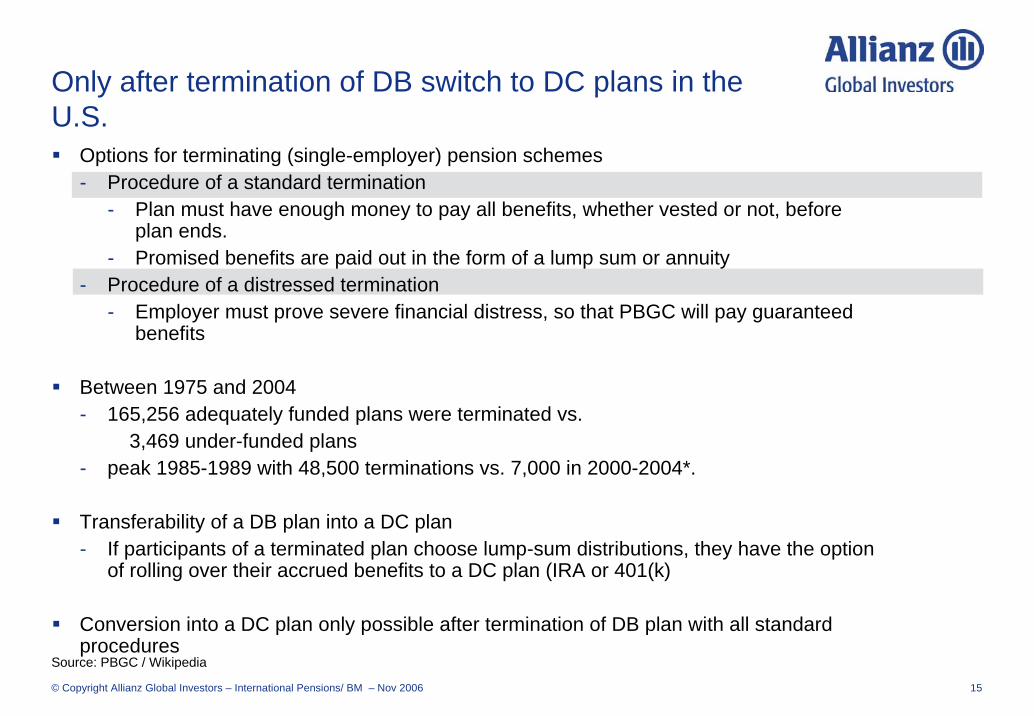

Only after termination of DB switch to DC plans in the U.S.

Options for terminating (single-employer) pension schemes- Procedure of a standard termination

- Plan must have enough money to pay all benefits, whether vested or not, before plan ends.

- Promised benefits are paid out in the form of a lump sum or annuity- Procedure of a distressed termination

- Employer must prove severe financial distress, so that PBGC will pay guaranteed benefits

Between 1975 and 2004 - 165,256 adequately funded plans were terminated vs.

3,469 under-funded plans - peak 1985-1989 with 48,500 terminations vs. 7,000 in 2000-2004*.

Transferability of a DB plan into a DC plan- If participants of a terminated plan choose lump-sum distributions, they have the option

of rolling over their accrued benefits to a DC plan (IRA or 401(k)

Conversion into a DC plan only possible after termination of DB plan with all standard procedures

Source: PBGC / Wikipedia

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 16

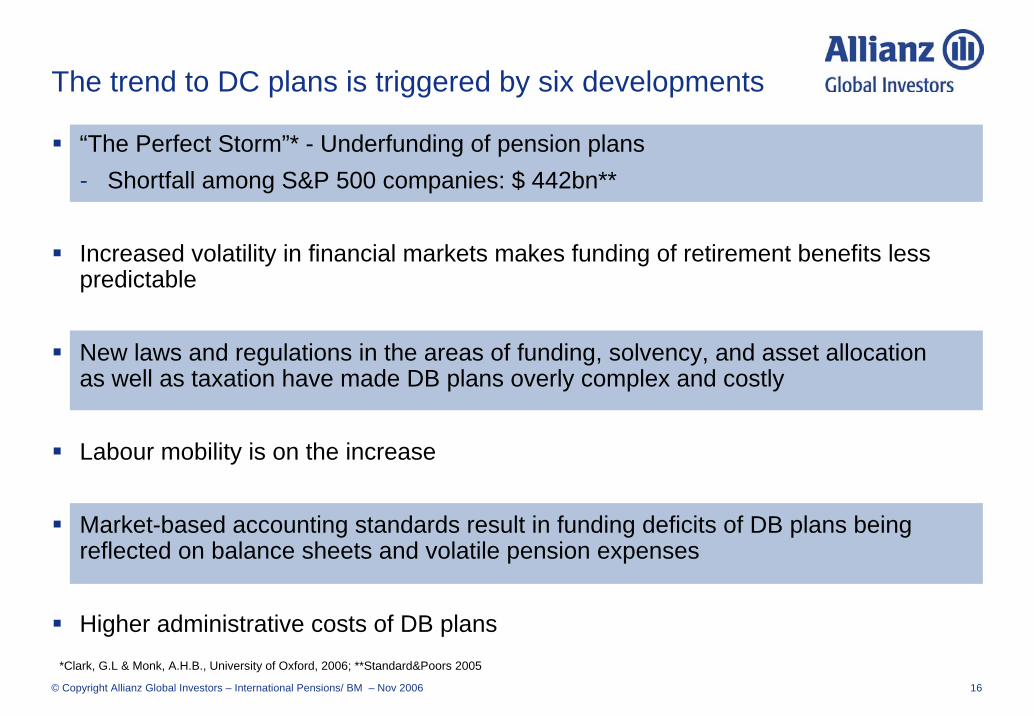

The trend to DC plans is triggered by six developments

“The Perfect Storm”* - Underfunding of pension plans- Shortfall among S&P 500 companies: $ 442bn**

Increased volatility in financial markets makes funding of retirement benefits less predictable

New laws and regulations in the areas of funding, solvency, and asset allocation as well as taxation have made DB plans overly complex and costly

Labour mobility is on the increase

Market-based accounting standards result in funding deficits of DB plans being reflected on balance sheets and volatile pension expenses

Higher administrative costs of DB plans*Clark, G.L & Monk, A.H.B., University of Oxford, 2006; **Standard&Poors 2005

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 17

Privatising Pensions –DC, individual control and responsibility for old age provision

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 18

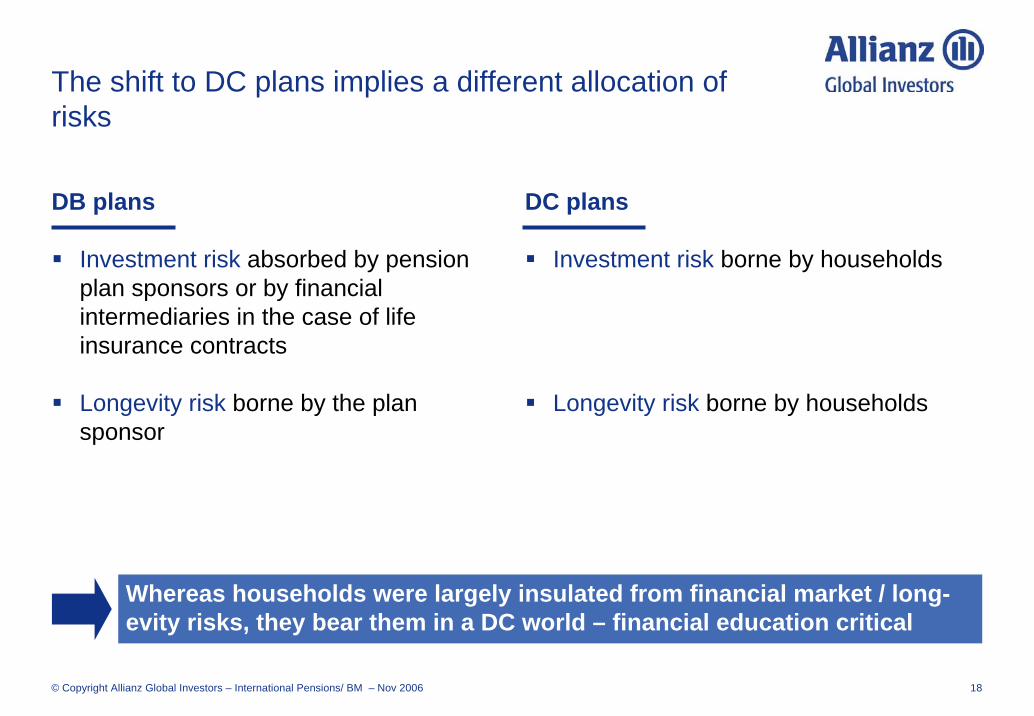

The shift to DC plans implies a different allocation of risks

DB plans

Investment risk absorbed by pension plan sponsors or by financial intermediaries in the case of life insurance contracts

Longevity risk borne by the plan sponsor

DC plans

Investment risk borne by households

Longevity risk borne by households

Whereas households were largely insulated from financial market / long-evity risks, they bear them in a DC world – financial education critical

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 19

Privatising pensions – an illusion of control?

DC schemes are intended to increase the individual’s responsibility and control for pensions- employees are increasingly expected to make financial decisions that will

determine their standard of living in old age

DC schemes imply the assumption of- rational behaviour of individuals with regard to investment decisions- efficient markets protecting investors from systematic pricing errors

But research on Behavioural Economics indicates the “homo oeconomicus’ “ departures from rational behaviour

cognitive biases influence decisionslack of understanding of financial markets impair investment decisions personal discretion – people tend to overestimate their abilities

Source: Kahnemann et al., 2005

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 20

Implications for the design of DC pension plans

Pension plans with an ‘autopilot’:Automatic enrollment: participation in corporate pension plans increases considerably. Plans should discourage active trading.If savings rates are optional, default rates should be set adequately high, possibly with an automatic increase of pension savings on a regularly scheduled basis or at prespecified future dates.Plans should offer well-diversified, low-fee mutual funds as default choices.Workers who wish to make other choices may do so – but good options should be available to those who do not choose.Choice overload reduces plan participation.

If we are going to make people fly their own planes, we should expect them to rely onthe autopilot, and it must be designed accordingly.*

Source: *Kahnemann et al., 2005; Mitchell / Utkus 2003: Lessons from Behavioral Finance for Retirement Plan Design

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 21

Thank you for your attention!

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 22

Back up

© Copyright Allianz Global Investors – International Pensions/ BM – Nov 2006 23

Definitions OECD (2006) Defined Contribution plans are those where the plan sponsor has no obligations over and above paying contributions.

Two main types- Defined Contribution (unprotected): A personal pension plan or occupational defined

contribution pension plan where the pension plan/fund itself or the pension provider does not offer any investment return or benefit guarantees or promises covering the whole plan/fund

- Defined Contribution (protected): A personal pension plan or occupational defined contribution pension plan other than an unprotected pension plan. The guarantees or promises may be offered by the pension plan/fund itself or the plan provider (e.g. deferred annuity, guaranteed rate of return)

Defined Benefit: Occupational plans where the plan sponsor has obligations over and above paying contributions, other than in defined contribution plans.

Three main types- Traditional: DB plan where benefits are linked through a formula to the members’ wages or

salaries, length of employment, or other factors- Hybrid: DB plan where benefits depend on a rate of return credited to contributors, where this

rate of return is either specified in the plan rules, independently of of the actual return of any supporting assets or is calculated with reference to the actual return of any supporting assets and a minimum return guarantee specified in the plan rules

- Mixed: A DB plan that has two separate DB and DC components but which are treated as part of the same plan