21

OECD Multilateral Instrument status tracker Current as of 1 June 2019

OECD Multilateral Instrument status tracker Current as of 1 June 2019

Introduction 1

Status of the MLI as at 1 June 2019 2

World heat map 2

Europe 3

Asia-Pacific and the Middle East 4

Americas 5

Africa 6

Matrices of CTAs 7

Appendices 15

Contacts 18

OECD Multilateral Instrument status tracker | Introduction

1

Introduction

Scope

This document is a status tracker for the implementation of the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting generally referred to as the Multilateral Instrument or MLI. This MLI status tracker is intended to consolidate general information on the application of the treaty. The tracker has been reviewed and updated as of 1 June 2019.

As at 1 June 2019, 88 jurisdictions have signed the MLI, and 26 of those jurisdictions have also deposited their instruments of ratification with the OECD.

Please note the following definitions used in the document:

• Base Erosion and Profit Shifting (BEPS) refers to tax planning strategies that may be used to exploit gaps and mismatches in the tax rules of different countries to artificially shift profits to low or no-tax locations where there is little or no economic activity.

• BEPS Action Plan – This plan, published by the OECD, includeds 15 actions to address BEPS in a comprehensive manner.

• OECD BEPS Project – The BEPS project supported by the G20 now includes over 100 countries. Countries are able to take part in the ongoing work if they commit to implementation of the agreed minimum standards.

• OECD Model Tax Convention – The OECD Model Tax Convention on Income and on Capital is the model traditionally used by developed economies when negotiating double tax conventions.

• Tax treaty – A tax convention between two jurisdictions for the avoidance of double taxation with respect to taxes on income and on capital.

The MLI status tracker is intended to be a quick reference guide, and is not an exhaustive overview of all information relating to the MLI. It should not be relied upon for making business decisions, and experienced tax professionals should be consulted before taking any action. For more information regarding the application of the MLI in specific countries, and about Deloitte’s tax practice in those jurisdictions, please contact your usual Deloitte tax adviser.

The MLI status tracker will be updated when additional information becomes available; please check our website for the latest updates.

OECD Multilateral Instrument status tracker | Status of the MLI as at 1 June 2019

2

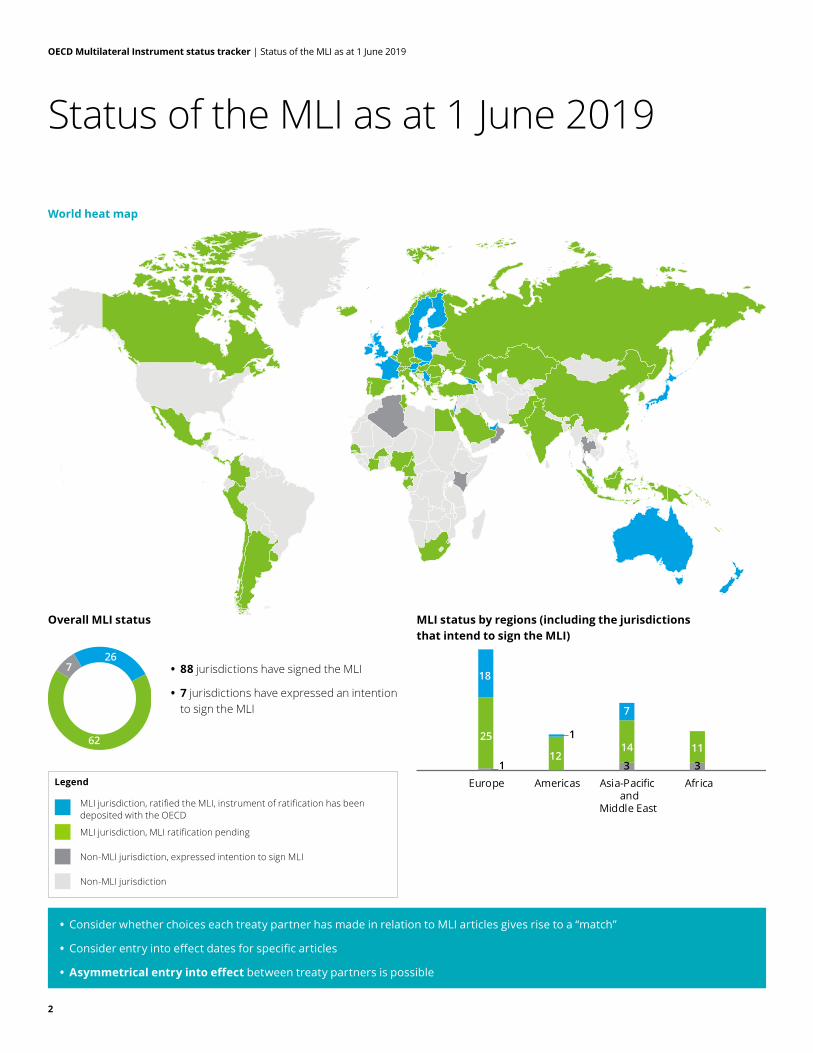

Status of the MLI as at 1 June 2019

World heat map

Overall MLI status

• 88 jurisdictions have signed the MLI

• 7 jurisdictions have expressed an intention to sign the MLI

26

62

7

MLI status by regions (including the jurisdictions that intend to sign the MLI)

• Consider whether choices each treaty partner has made in relation to MLI articles gives rise to a “match”

• Consider entry into effect dates for specific articles

• Asymmetrical entry into effect between treaty partners is possible

3

111

25

18

12

1

3

14

7

Europe Americas Asia-Pacificand

Middle East

AfricaLegend

MLI jurisdiction, ratified the MLI, instrument of ratification has been deposited with the OECD

MLI jurisdiction, MLI ratification pending

Non-MLI jurisdiction, expressed intention to sign MLI

Non-MLI jurisdiction

OECD Multilateral Instrument status tracker | Status of the MLI as at 1 June 2019

3

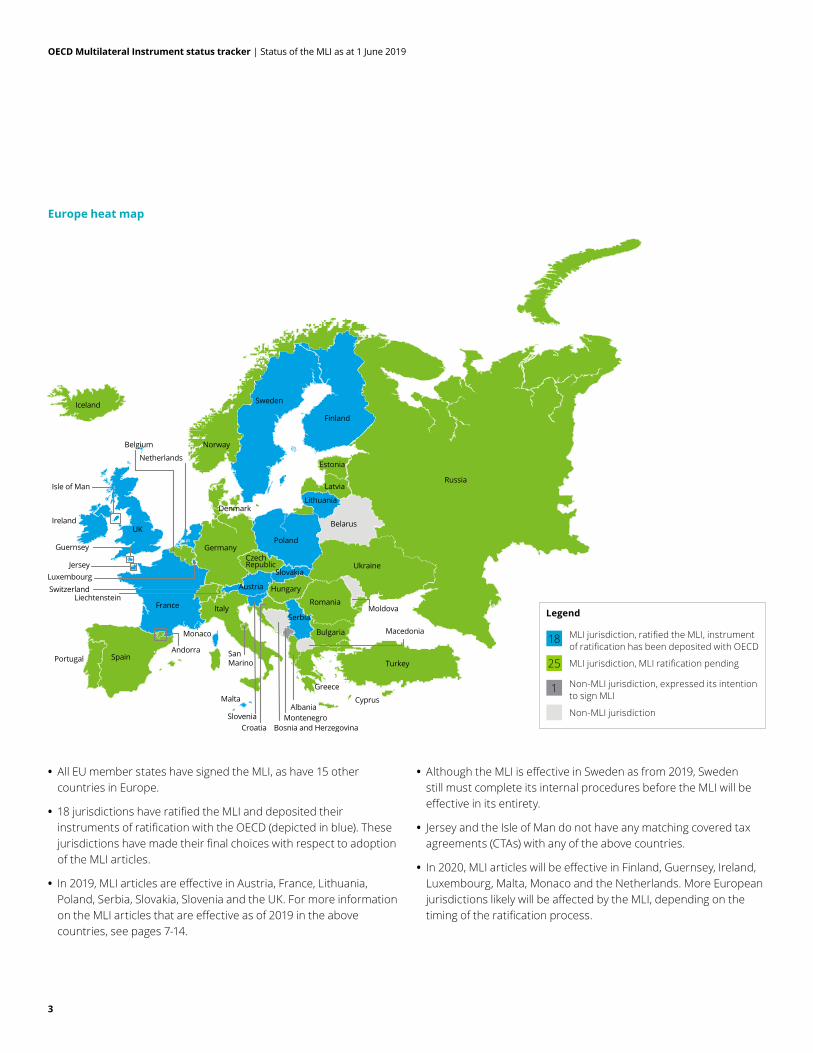

Europe heat map

Sweden

Finland

France

Spain

Poland

Italy

Germany

Romania

UK

Latvia

Ireland

Isle of Man

Bulgaria

Hungary

Greece

Lithuania

Portugal

Estonia

Slovakia

Belgium

Denmark

Malta

San Marino

Netherlands

Cyprus

Russia

CroatiaSlovenia

Ukraine

Belarus

Moldova

Norway

Macedonia

AlbaniaMontenegro

Bosnia and Herzegovina

Turkey

Austria

Czech Republic

Serbia

Iceland

LuxembourgJersey

Guernsey

SwitzerlandLiechtenstein

Monaco

Andorra

• All EU member states have signed the MLI, as have 15 other countries in Europe.

• 18 jurisdictions have ratified the MLI and deposited their instruments of ratification with the OECD (depicted in blue). These jurisdictions have made their final choices with respect to adoption of the MLI articles.

• In 2019, MLI articles are effective in Austria, France, Lithuania, Poland, Serbia, Slovakia, Slovenia and the UK. For more information on the MLI articles that are effective as of 2019 in the above countries, see pages 7-14.

• Although the MLI is effective in Sweden as from 2019, Sweden still must complete its internal procedures before the MLI will be effective in its entirety.

• Jersey and the Isle of Man do not have any matching covered tax agreements (CTAs) with any of the above countries.

• In 2020, MLI articles will be effective in Finland, Guernsey, Ireland, Luxembourg, Malta, Monaco and the Netherlands. More European jurisdictions likely will be affected by the MLI, depending on the timing of the ratification process.

Legend

MLI jurisdiction, ratified the MLI, instrument of ratification has been deposited with OECD

MLI jurisdiction, MLI ratification pending

Non-MLI jurisdiction, expressed its intention to sign MLI

Non-MLI jurisdiction

18

25

1

OECD Multilateral Instrument status tracker | Status of the MLI as at 1 June 2019

4

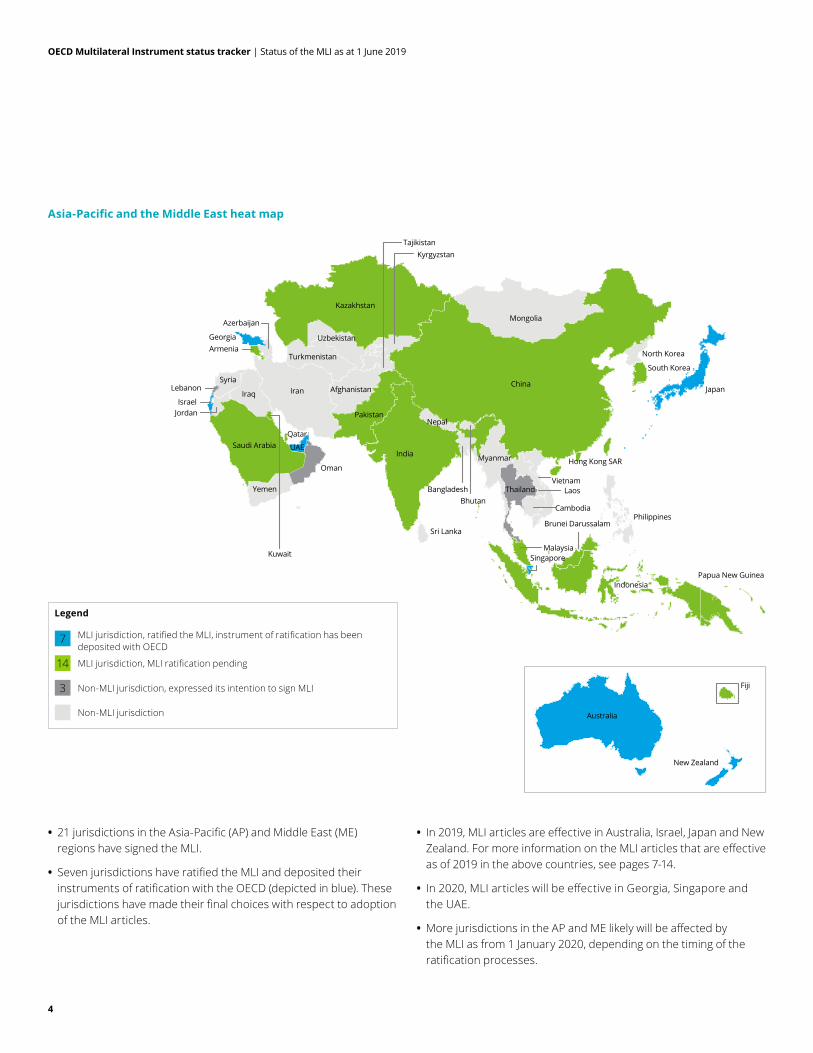

Asia-Pacific and the Middle East heat map

ChinaJapan

North Korea

Mongolia

Kazakhstan

Uzbekistan

TajikistanKyrgyzstan

Georgia

Azerbaijan

Syria

Iraq

Saudi Arabia

Yemen

Kuwait

JordanIsrael

Lebanon

Oman

Qatar

UAE

Iran

Pakistan

India

BangladeshBhutan

VietnamLaos

Nepal

Myanmar

Thailand

Hong Kong SAR

Philippines

IndonesiaPapua New Guinea

Sri Lanka

Afghanistan

TurkmenistanSouth Korea

Armenia

Cambodia

Malaysia

Brunei Darussalam

Singapore

Australia

New Zealand

Fiji

• 21 jurisdictions in the Asia-Pacific (AP) and Middle East (ME) regions have signed the MLI.

• Seven jurisdictions have ratified the MLI and deposited their instruments of ratification with the OECD (depicted in blue). These jurisdictions have made their final choices with respect to adoption of the MLI articles.

• In 2019, MLI articles are effective in Australia, Israel, Japan and New Zealand. For more information on the MLI articles that are effective as of 2019 in the above countries, see pages 7-14.

• In 2020, MLI articles will be effective in Georgia, Singapore and the UAE.

• More jurisdictions in the AP and ME likely will be affected by the MLI as from 1 January 2020, depending on the timing of the ratification processes.

Legend

MLI jurisdiction, ratified the MLI, instrument of ratification has been deposited with OECD

MLI jurisdiction, MLI ratification pending

Non-MLI jurisdiction, expressed its intention to sign MLI

Non-MLI jurisdiction

7

14

3

OECD Multilateral Instrument status tracker | Status of the MLI as at 1 June 2019

5

Americas heat map

Curaçao

St Maarten

Barbados

GuyanaSuriname

French Guiana

Canada

United States

Brazil

Venezuela

Paraguay

Bolivia

Peru

Ecuador

Colombia

ArgentinaUruguay

Chile

Bahamas

Bahamas

Dominican Rep.

Puerto RicoJamaica

Belize

HondurasNicaragua

Guatemala

Costa Rica

PanamaEl Salvador

Mexico

• 13 jurisdictions in the Americas region have signed the MLI.

• Only Curacao has ratified the MLI and deposited its instrument of ratification with the OECD. Curacao has made its final choices with respect to adoption of the MLI articles.

• Other jurisdictions can change their initial MLI positions before ratifying the MLI.

• The MLI will not be effective in the Americas region in 2019.

• The MLI will be effective in Curacao as from 2020.

Legend

MLI jurisdiction, ratified the MLI, instrument of ratification has been deposited with OECD

MLI jurisdiction, MLI ratification pending

Non-MLI jurisdiction, expressed its intention to sign MLI

Non-MLI jurisdiction

1

12

0

OECD Multilateral Instrument status tracker | Status of the MLI as at 1 June 2019

6

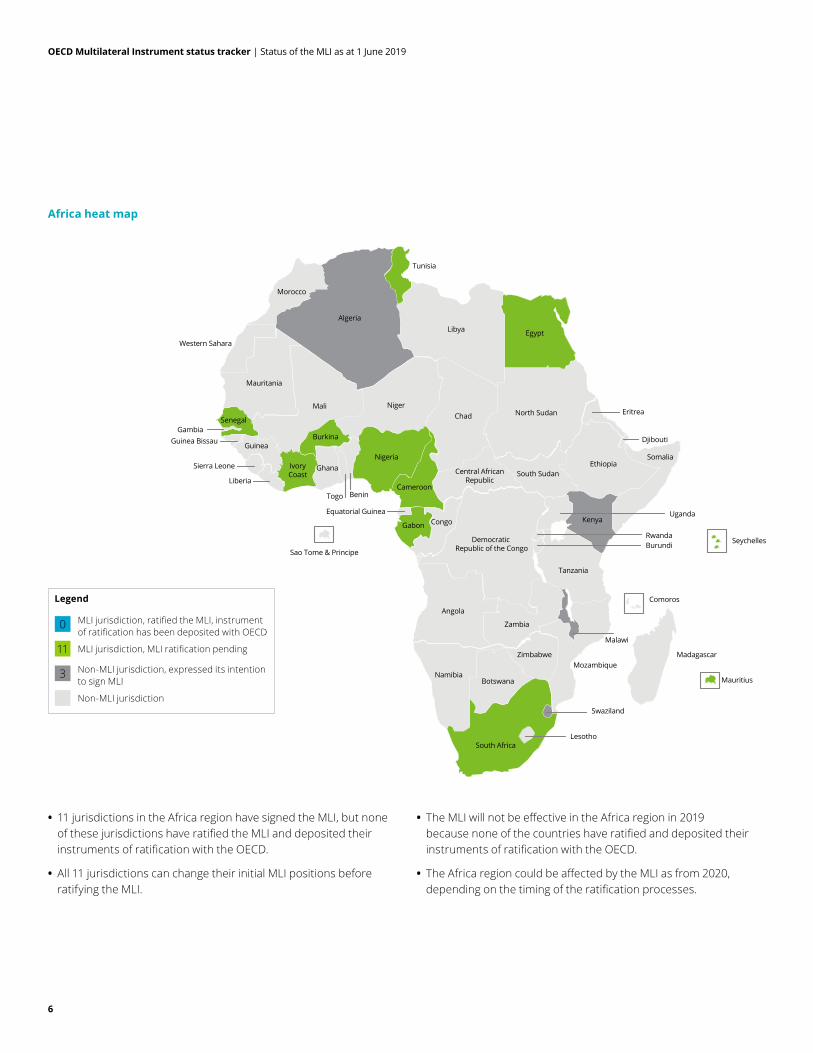

Africa heat map

Algeria

Tunisia

Libya Egypt

North Sudan Eritrea

SomaliaEthiopia

Djibouti

South Sudan

Congo

Democratic Republic of the Congo

Angola

Namibia

South Africa

MadagascarMozambique

Malawi

Uganda

RwandaBurundi

Mauritius

Seychelles

Comoros

Lesotho

Botswana

Zimbabwe

Zambia

Tanzania

Kenya

Central AfricanRepublic

Gabon

Cameroon

Nigeria

Sao Tome & Principe

ChadNigerMali

Mauritania

SenegalGambia

Guinea Bissau GuineaBurkina

IvoryCoast

Ghana

BeninTogo

Equatorial Guinea

Sierra Leone

Liberia

Western Sahara

Morocco

Swaziland

• 11 jurisdictions in the Africa region have signed the MLI, but none of these jurisdictions have ratified the MLI and deposited their instruments of ratification with the OECD.

• All 11 jurisdictions can change their initial MLI positions before ratifying the MLI.

• The MLI will not be effective in the Africa region in 2019 because none of the countries have ratified and deposited their instruments of ratification with the OECD.

• The Africa region could be affected by the MLI as from 2020, depending on the timing of the ratification processes.

Legend

MLI jurisdiction, ratified the MLI, instrument of ratification has been deposited with OECD

MLI jurisdiction, MLI ratification pending

Non-MLI jurisdiction, expressed its intention to sign MLI

Non-MLI jurisdiction

0

11

3

OECD Multilateral Instrument status tracker | Matrices of CTAs

7

Matrices of CTAs

MLI impact as at 1 January 2019

• As at 1 January 2019, the MLI applies in the following 15 jurisdictions in Europe, Asia-Pacific and the Middle East since these countries ratified the MLI and deposited their instruments of ratification with the OECD by 1 October 2018: Australia, Austria, France, Isle of Man, Israel, Japan, Jersey, Lithuania, New Zealand, Poland, Serbia, Slovakia, Slovenia, Sweden and the UK. The MLI is not yet in effect in any countries in Africa or the Americas as at 1 January 2019 because no jurisdiction has ratified the MLI and deposited its instrument of ratification with the OECD.

• The following pages provide more information on the impact of the MLI as at 1 January 2019 on certain CTAs showing: – Where the MLI entered into force on or before 1 January 2019;

– Where the MLI entered into effect with respect to withholding tax (WHT) as from 1 January 2019;

– Where the MLI will enter or has entered into effect with respect to other taxes during 2019; and

– Where the MLI is effective with respect to mutual agreement provisions (MAP). The entry into effect dates for MAP could be different from WHT and other taxes.

Note:

• Jersey and the Isle of Man have not listed tax treaties with any of the other jurisdictions that have deposited their instruments of ratification with the OECD by 1 October 2018 so there are no CTAs for these jurisdictions to be covered by the MLI articles as per 1 January 2019.

• Curacao, Finland, Georgia, Guernsey, Ireland, Luxembourg, Malta, Monaco, Netherlands, Singapore and the UAE are not included in the matrices because the MLI articles, with the exception of dispute resolution, will enter into effect as from 2020 in these countries.

OECD Multilateral Instrument status tracker | Matrices of CTAs

8

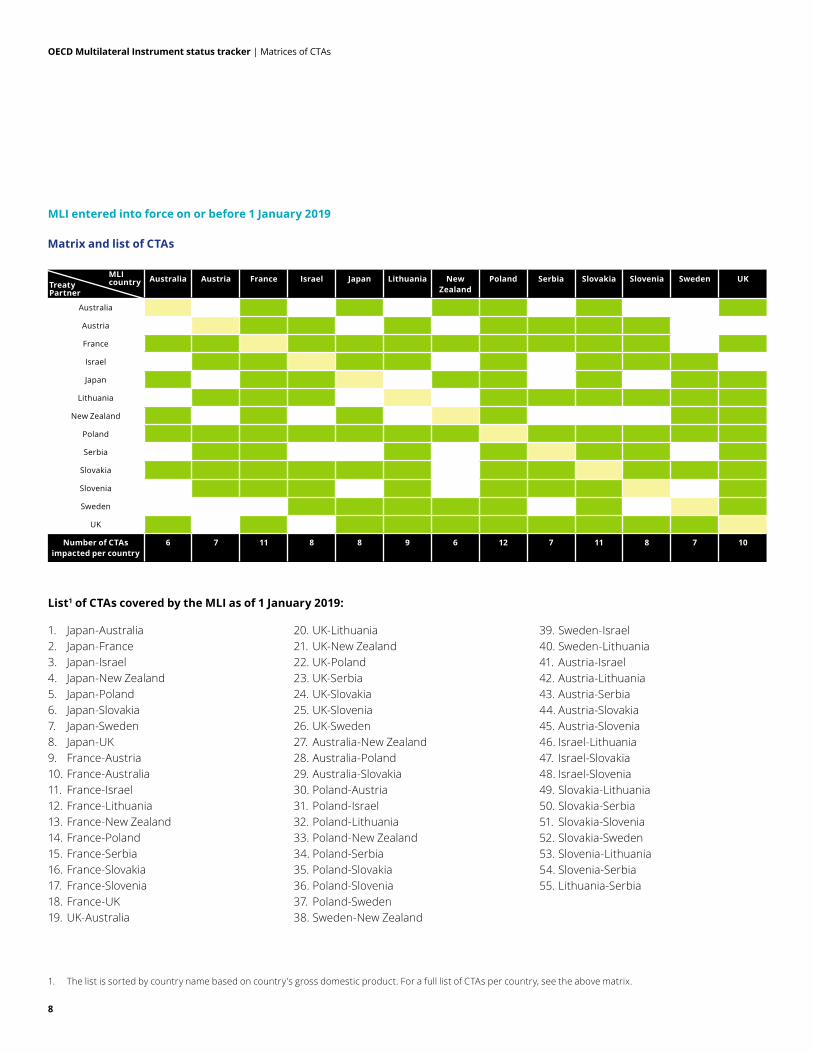

MLI entered into force on or before 1 January 2019

Australia Austria France Israel Japan Lithuania New Zealand

Poland Serbia Slovakia Slovenia Sweden UK

Australia

Austria

France

Israel

Japan

Lithuania

New Zealand

Poland

Serbia

Slovakia

Slovenia

Sweden

UK

Number of CTAs impacted per country

6 7 11 8 8 9 6 12 7 11 8 7 10

List1 of CTAs covered by the MLI as of 1 January 2019:

1. Japan-Australia2. Japan-France3. Japan-Israel4. Japan-New Zealand5. Japan-Poland6. Japan-Slovakia7. Japan-Sweden8. Japan-UK9. France-Austria10. France-Australia11. France-Israel12. France-Lithuania13. France-New Zealand14. France-Poland15. France-Serbia16. France-Slovakia17. France-Slovenia18. France-UK19. UK-Australia

20. UK-Lithuania21. UK-New Zealand22. UK-Poland23. UK-Serbia24. UK-Slovakia25. UK-Slovenia26. UK-Sweden27. Australia-New Zealand28. Australia-Poland29. Australia-Slovakia30. Poland-Austria31. Poland-Israel32. Poland-Lithuania33. Poland-New Zealand34. Poland-Serbia35. Poland-Slovakia36. Poland-Slovenia37. Poland-Sweden38. Sweden-New Zealand

39. Sweden-Israel40. Sweden-Lithuania41. Austria-Israel42. Austria-Lithuania43. Austria-Serbia44. Austria-Slovakia45. Austria-Slovenia46. Israel-Lithuania47. Israel-Slovakia48. Israel-Slovenia49. Slovakia-Lithuania50. Slovakia-Serbia51. Slovakia-Slovenia52. Slovakia-Sweden53. Slovenia-Lithuania54. Slovenia-Serbia55. Lithuania-Serbia

1. The list is sorted by country name based on country's gross domestic product. For a full list of CTAs per country, see the above matrix.

MLI countryTreaty

Partner

Matrix and list of CTAs

OECD Multilateral Instrument status tracker | Matrices of CTAs

9

Key takeaways

Mutual agreement procedure (application of Article 16 of the MLI)

General: The MAP allows the competent authorities of the governments of both Contracting Jurisdictions to attempt to resolve cross-border tax disputes. Such disputes may involve cases of double taxation (juridical and economic), as well as inconsistencies in the interpretation and application of a tax treaty.

Status:

• The MLI generally enters into effect for dispute resolution immediately after the MLI enters into force for both countries.

• As Article 16 covers one of the BEPS minimum standards, jurisdictions that sign the MLI must incorporate this article into their CTAs.

• Therefore, Article 16 of the MLI is effective in all 13 jurisdictions (see page 8 for the tax treaties covered by the MLI and, therefore, impacted by Article 16).

• It should be noted that there may be complexity as to whether disputes from earlier years can benefit from an extended MAP period introduced by Article 16 because the entry into effect provisions in Article 35 specifically exclude cases that “were not eligible to be presented” before a CTA was modified.

Other considerations:

• Mandatory binding arbitration may apply after a case has spent two years in a MAP. However, many jurisdictions have opted out of the arbitration provisions (Articles 18-26 of the MLI) as these are not part of the BEPS minimum standard.

OECD Multilateral Instrument status tracker | Matrices of CTAs

10

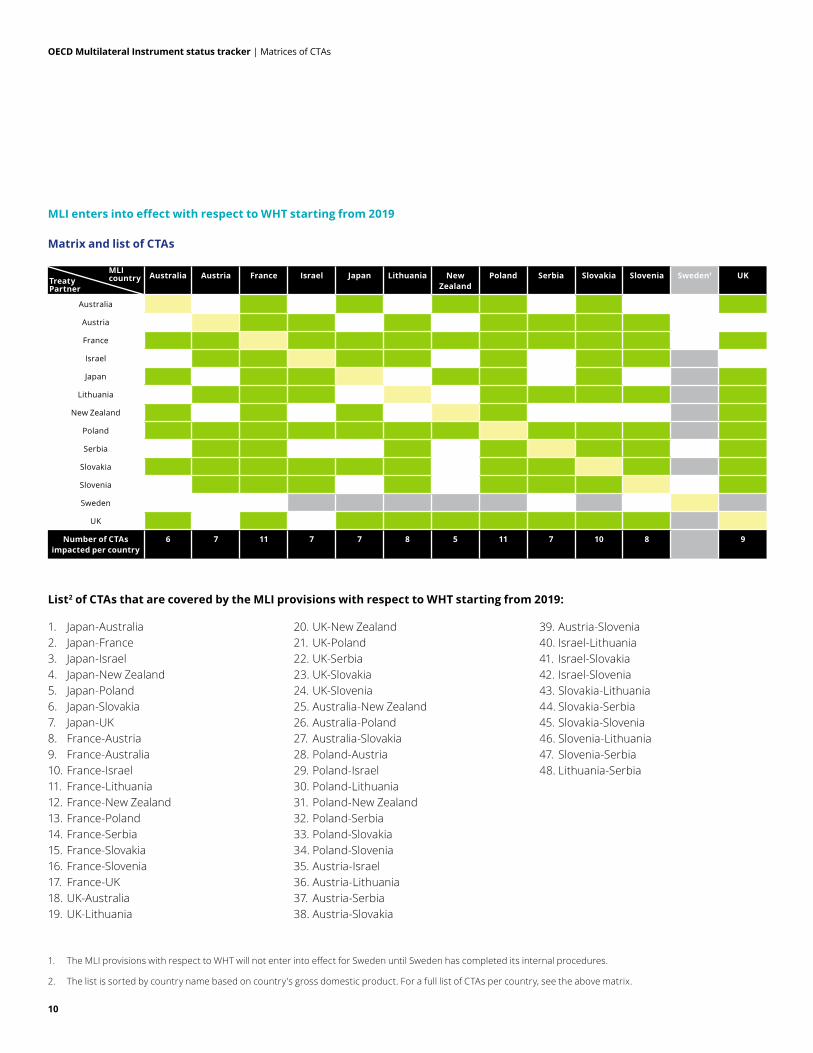

MLI enters into effect with respect to WHT starting from 2019

Australia Austria France Israel Japan Lithuania New Zealand

Poland Serbia Slovakia Slovenia Sweden1 UK

Australia

Austria

France

Israel

Japan

Lithuania

New Zealand

Poland

Serbia

Slovakia

Slovenia

Sweden

UK

Number of CTAs impacted per country

6 7 11 7 7 8 5 11 7 10 8 9

List2 of CTAs that are covered by the MLI provisions with respect to WHT starting from 2019:

1. Japan-Australia2. Japan-France3. Japan-Israel4. Japan-New Zealand5. Japan-Poland6. Japan-Slovakia7. Japan-UK8. France-Austria9. France-Australia10. France-Israel11. France-Lithuania12. France-New Zealand13. France-Poland14. France-Serbia15. France-Slovakia16. France-Slovenia17. France-UK18. UK-Australia19. UK-Lithuania

20. UK-New Zealand21. UK-Poland22. UK-Serbia23. UK-Slovakia24. UK-Slovenia25. Australia-New Zealand26. Australia-Poland27. Australia-Slovakia28. Poland-Austria29. Poland-Israel30. Poland-Lithuania31. Poland-New Zealand32. Poland-Serbia33. Poland-Slovakia34. Poland-Slovenia35. Austria-Israel36. Austria-Lithuania37. Austria-Serbia38. Austria-Slovakia

39. Austria-Slovenia40. Israel-Lithuania41. Israel-Slovakia42. Israel-Slovenia43. Slovakia-Lithuania44. Slovakia-Serbia45. Slovakia-Slovenia46. Slovenia-Lithuania47. Slovenia-Serbia48. Lithuania-Serbia

1. The MLI provisions with respect to WHT will not enter into effect for Sweden until Sweden has completed its internal procedures.

2. The list is sorted by country name based on country's gross domestic product. For a full list of CTAs per country, see the above matrix.

MLI countryTreaty

Partner

Matrix and list of CTAs

OECD Multilateral Instrument status tracker | Matrices of CTAs

11

Key takeaways

Prevention of treaty abuse (application of Article 7 of the MLI)

General: CTAs must include an anti-abuse rule to prevent treaty benefits from being granted in unintended circumstances. The anti-abuse rule may take one of two forms: (i) a principle purpose test (PPT) or (ii) a simplified LOB rule, supplemented by a PPT. The PPT will have the effect of denying treaty benefits (e.g., a reduction in WHT on dividends, interest and royalties) where it is reasonable to conclude, having regard to all relevant facts and circumstances, that obtaining a treaty benefit is one of the principal purposes of the party seeking to rely on the relevant treaty.

Status:

• For Article 7 of the MLI to take effect from 1 January 2019, countries generally would have had to ratify and deposit their instruments of ratification before 1 October 2018.

• As at 1 January 2019, the MLI entered into effect with respect to WHT in almost all jurisdictions that had ratified the MLI and deposited their instruments of ratification before 1 October 2018, except for Sweden, which still must complete its internal procedures before the MLI will be effective. All 12 jurisdictions that completed the ratification process before 1 October 2018 have chosen to incorporate the PPT only (see page 10 for the tax treaties that are covered by the MLI and, therefore, impacted by Article 7 of the MLI as it applies to WHT, from 1 January 2019).

Other considerations:

• Many existing bilateral tax treaties already may include anti-abuse provisions, but the scope may be narrower than the PPT.

• Some jurisdictions have domestic-anti abuse provisions that target artificial structures or those that lack substance; these provisions may prevent access to tax treaties even before consideration can be given to the application of a PPT.

• In addition, jurisdictions may have tightened or otherwise revised their domestic anti-abuse rules (e.g. domestic implementation of the general anti-abuse rule in the EU Anti-Tax Avoidance Directive or amended their domestic rules on the basis of the recommendations of the OECD Report on Preventing the Granting of Treaty Benefits in Inappropriate Circumstances (BEPS Action 6)).

OECD Multilateral Instrument status tracker | Matrices of CTAs

12

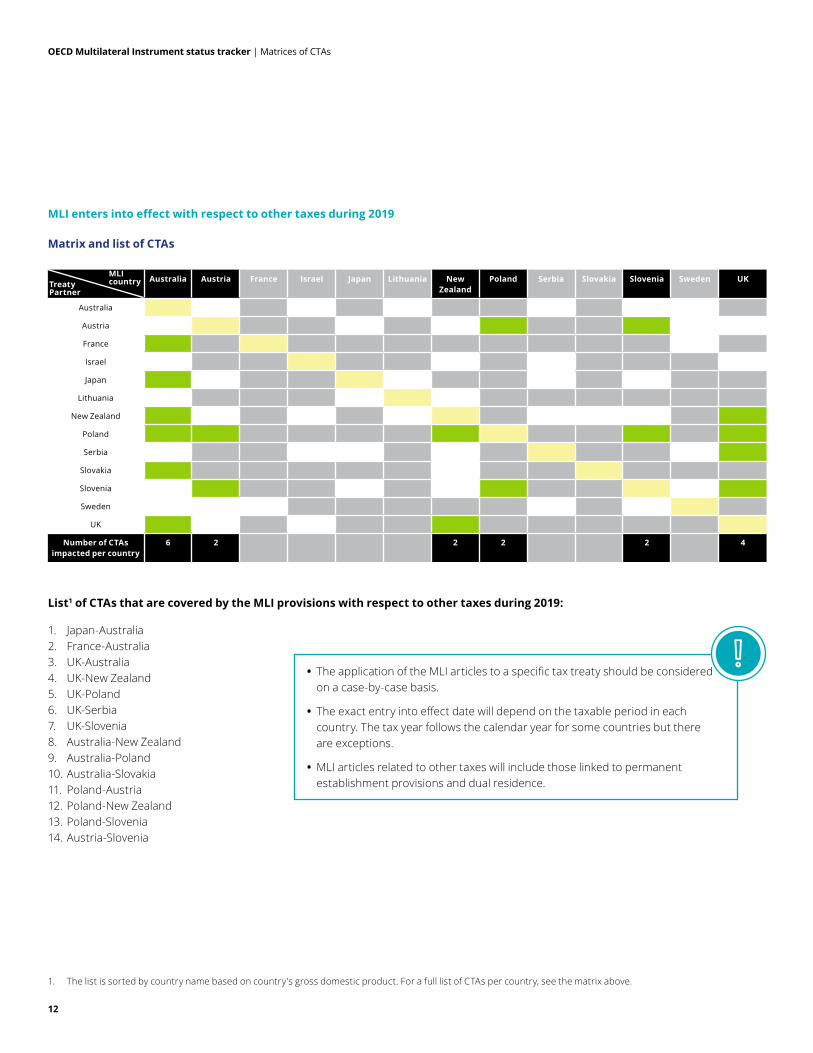

MLI enters into effect with respect to other taxes during 2019

Australia Austria France Israel Japan Lithuania New Zealand

Poland Serbia Slovakia Slovenia Sweden UK

Australia

Austria

France

Israel

Japan

Lithuania

New Zealand

Poland

Serbia

Slovakia

Slovenia

Sweden

UK

Number of CTAs impacted per country

6 2 2 2 2 4

List1 of CTAs that are covered by the MLI provisions with respect to other taxes during 2019:

1. Japan-Australia2. France-Australia3. UK-Australia4. UK-New Zealand5. UK-Poland6. UK-Serbia7. UK-Slovenia8. Australia-New Zealand9. Australia-Poland10. Australia-Slovakia11. Poland-Austria12. Poland-New Zealand13. Poland-Slovenia14. Austria-Slovenia

1. The list is sorted by country name based on country's gross domestic product. For a full list of CTAs per country, see the matrix above.

MLI countryTreaty

Partner

• The application of the MLI articles to a specific tax treaty should be considered on a case-by-case basis.

• The exact entry into effect date will depend on the taxable period in each country. The tax year follows the calendar year for some countries but there are exceptions.

• MLI articles related to other taxes will include those linked to permanent establishment provisions and dual residence.

Matrix and list of CTAs

OECD Multilateral Instrument status tracker | Matrices of CTAs

13

Key takeaways

Artificial avoidance of permanent establishment status through commissionnaire arrangements and similar strategies (application of Article 12 of the MLI)

Countries that opted for Article 12: Countries that opted out of Article 12:

General: A permanent establishment will arise not only where a dependent agent concludes contracts in the name of the enterprise, but also contracts for the transfer of, or for the granting of the right to use, property owned by that enterprise, or for the provision of services by that enterprise, where the agent habitually concludes contracts, or habitually plays the principal role leading to the conclusion of contracts that are routinely concluded without material modification by the enterprise.

Status:

• For Article 12 of the MLI to take effect as from 1 January 2019, countries generally would have had to ratify the MLI and deposit their instruments of ratification before 1 April 2018 where their tax period aligns with the calendar year. However, some countries have taxable periods that are not based on a calendar year: Australia (from 1 July), New Zealand (from 1 April), the UK (from 1 April for corporate taxes).

• During 2019, the MLI enters into effect with respect to other taxes in Australia, New Zealand, Poland, Slovenia and the UK. Out of these jurisdictions, only New Zealand and Slovenia have opted to apply Article 12 of the MLI; the other jurisdictions opted out of this article. As at 1 January 2019, there is no tax treaty between New Zealand and Slovenia, so no tax treaty will be affected by Article 12 as from 2019.

Other considerations:

• The definition of a permanent establishment is set out in Article 5 of the OECD Model Tax Convention (2017 version), and the text included in Article 12 of the MLI is consistent with the language used there. As a result of the update to the OECD model, some newer tax treaties already may contain the revised language. In addition, some jurisdictions may choose to align their domestic law on permanent establishment with this definition, irrespective of whether they have signed the MLI or opted to apply Article 12.

1. France 2. Israel

3. Japan 4. Lithuania

5. New Zealand 6. Serbia

7. Slovakia 8. Slovenia

1. Australia 2. Austria

3. Poland 4. Sweden

5. UK

Jurisdictions where the MLI is applied in 2019 are shown in bold.

OECD Multilateral Instrument status tracker | Matrices of CTAs

14

Artificial avoidance of permanent establishment status through the specific activity exemptions (application of Article 13(4) of the MLI)

Countries that opted for Article 13(4): Countries that opted out of Article 13(4):

About: Prevention of the fragmentation of a cohesive operating business into several small operations in order to fall within the “preparatory or auxiliary” exemption of the permanent establishment definition.

Status:

• For Article 13(4) to take effect as from 1 January 2019, countries generally would have had to ratify the MLI and deposit their instruments of ratification before 1 April 2018 where the tax period aligns with the calendar year. However, as noted above, some countries have taxable periods that are not based on a calendar year, i.e., Australia (from 1 July), New Zealand (from 1 April) and the UK (from 1 April for corporate taxes).

• During 2019, the MLI enters into effect with respect to other taxes only in Australia, New Zealand, Poland, Slovenia and the UK. Out of these countries, Australia, New Zealand, Slovenia and the UK have opted for Article 13 (4) and Poland have opted out of this article. See page 12 for treaties that are covered by the MLI and, therefore, are impacted by Article 13(4) during 2019.

Other considerations:

• Due to differences in taxable periods, there may be asymmetrical entry into effect dates in respect of Article 13(4) between Contracting Jurisdictions.

• The anti-fragmentation rule is also set out in Article 5 of the 2017 version of the OECD Model Tax Convention, and the text included in Article 13(4) of the MLI is in line with that rule. Due to the revision to the OECD model, some newer tax treaties already may contain anti-fragmentation language. In addition, some jurisdictions may align their domestic law with this change to the definition of permanent establishment, irrespective of whether they have signed the MLI or opted to apply Article 13(4) of the MLI.

1. Australia 2. France

3. Israel 4. Japan

5. Lithuania 6. New Zealand

7. Serbia 8. Slovakia

9. Slovenia 10. UK

1. Austria 2. Poland

3. Sweden

Jurisdictions where the MLI is applied in 2019 are shown in bold.

OECD Multilateral Instrument status tracker | Appendices

15

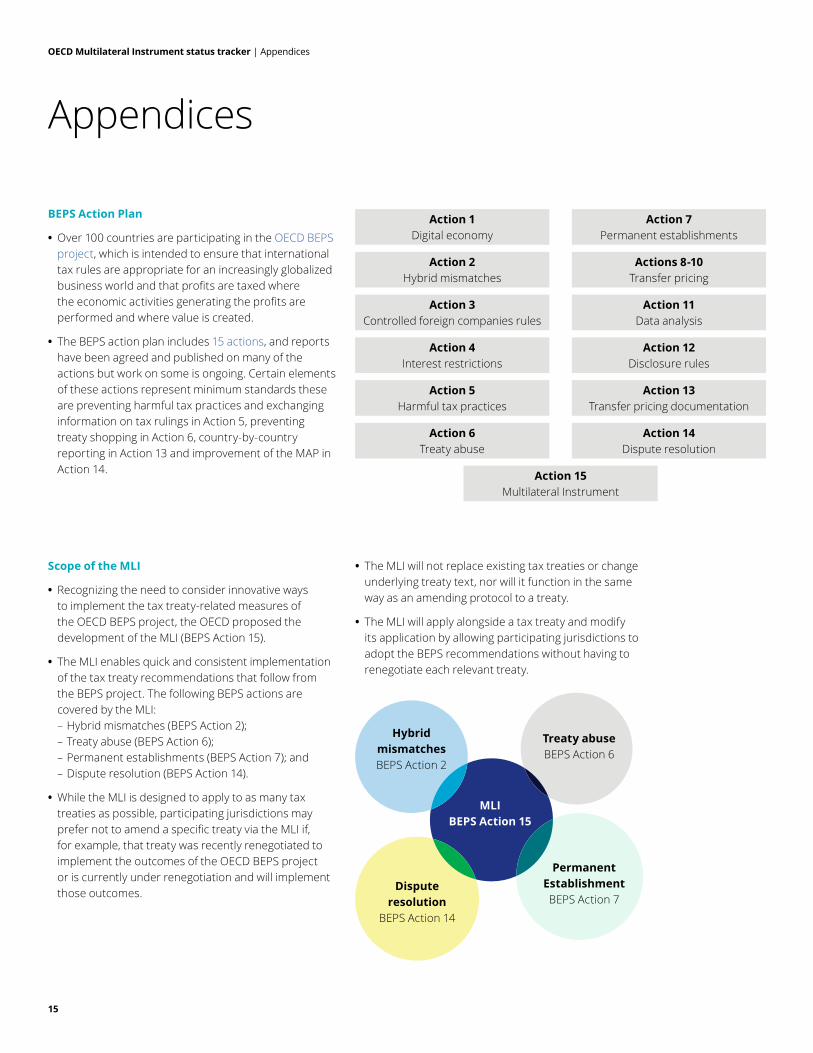

BEPS Action Plan

• Over 100 countries are participating in the OECD BEPS project, which is intended to ensure that international tax rules are appropriate for an increasingly globalized business world and that profits are taxed where the economic activities generating the profits are performed and where value is created.

• The BEPS action plan includes 15 actions, and reports have been agreed and published on many of the actions but work on some is ongoing. Certain elements of these actions represent minimum standards these are preventing harmful tax practices and exchanging information on tax rulings in Action 5, preventing treaty shopping in Action 6, country-by-country reporting in Action 13 and improvement of the MAP in Action 14.

Scope of the MLI

• Recognizing the need to consider innovative ways to implement the tax treaty-related measures of the OECD BEPS project, the OECD proposed the development of the MLI (BEPS Action 15).

• The MLI enables quick and consistent implementation of the tax treaty recommendations that follow from the BEPS project. The following BEPS actions are covered by the MLI: – Hybrid mismatches (BEPS Action 2); – Treaty abuse (BEPS Action 6); – Permanent establishments (BEPS Action 7); and – Dispute resolution (BEPS Action 14).

• While the MLI is designed to apply to as many tax treaties as possible, participating jurisdictions may prefer not to amend a specific treaty via the MLI if, for example, that treaty was recently renegotiated to implement the outcomes of the OECD BEPS project or is currently under renegotiation and will implement those outcomes.

Appendices

Action 1Digital economy

Action 7Permanent establishments

Action 2 Hybrid mismatches

Actions 8-10Transfer pricing

Action 3Controlled foreign companies rules

Action 11Data analysis

Action 4Interest restrictions

Action 12Disclosure rules

Action 5Harmful tax practices

Action 13Transfer pricing documentation

Action 6Treaty abuse

Action 14Dispute resolution

Action 15Multilateral Instrument

• The MLI will not replace existing tax treaties or change underlying treaty text, nor will it function in the same way as an amending protocol to a treaty.

• The MLI will apply alongside a tax treaty and modify its application by allowing participating jurisdictions to adopt the BEPS recommendations without having to renegotiate each relevant treaty.

Hybrid mismatchesBEPS Action 2

Treaty abuseBEPS Action 6

MLI BEPS Action 15

Dispute resolution

BEPS Action 14

Permanent EstablishmentBEPS Action 7

OECD Multilateral Instrument status tracker | Appendices

16

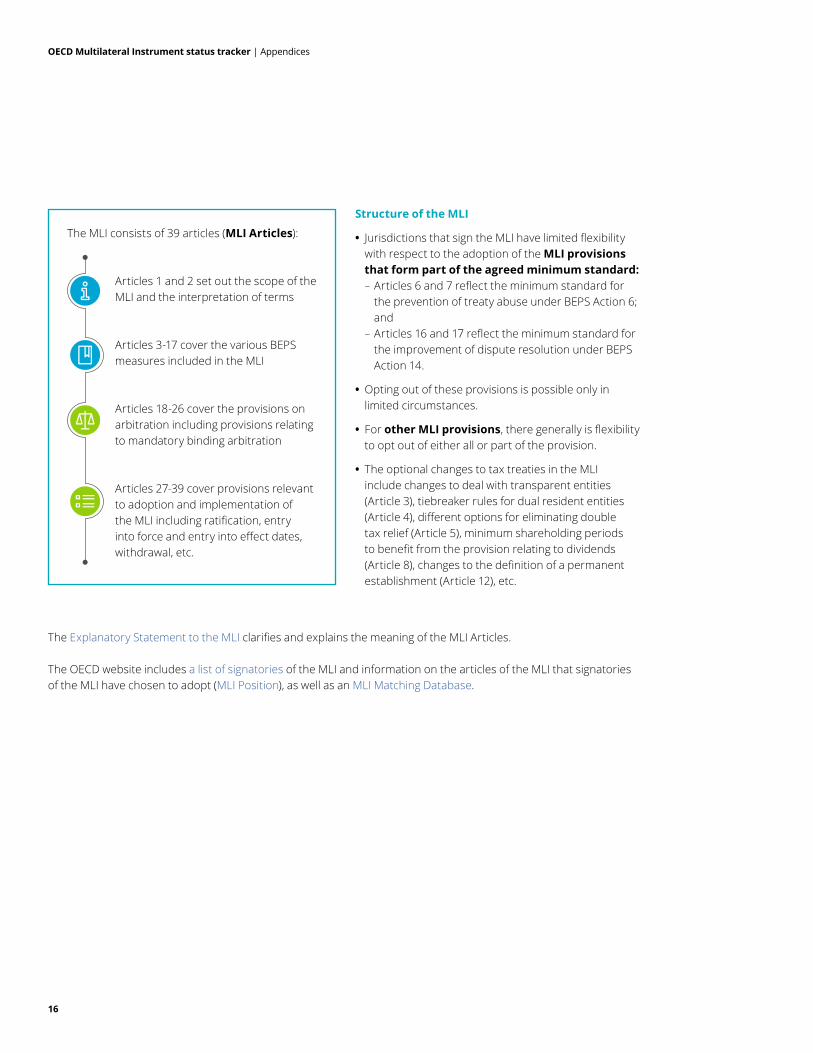

Structure of the MLI

• Jurisdictions that sign the MLI have limited flexibility with respect to the adoption of the MLI provisions that form part of the agreed minimum standard: – Articles 6 and 7 reflect the minimum standard for the prevention of treaty abuse under BEPS Action 6; and

– Articles 16 and 17 reflect the minimum standard for the improvement of dispute resolution under BEPS Action 14.

• Opting out of these provisions is possible only in limited circumstances.

• For other MLI provisions, there generally is flexibility to opt out of either all or part of the provision.

• The optional changes to tax treaties in the MLI include changes to deal with transparent entities (Article 3), tiebreaker rules for dual resident entities (Article 4), different options for eliminating double tax relief (Article 5), minimum shareholding periods to benefit from the provision relating to dividends (Article 8), changes to the definition of a permanent establishment (Article 12), etc.

The Explanatory Statement to the MLI clarifies and explains the meaning of the MLI Articles.

The OECD website includes a list of signatories of the MLI and information on the articles of the MLI that signatories of the MLI have chosen to adopt (MLI Position), as well as an MLI Matching Database.

The MLI consists of 39 articles (MLI Articles):

Articles 1 and 2 set out the scope of the MLI and the interpretation of terms

Articles 3-17 cover the various BEPS measures included in the MLI

Articles 18-26 cover the provisions on arbitration including provisions relating to mandatory binding arbitration

Articles 27-39 cover provisions relevant to adoption and implementation of the MLI including ratification, entry into force and entry into effect dates, withdrawal, etc.

OECD Multilateral Instrument status tracker | Appendices

17

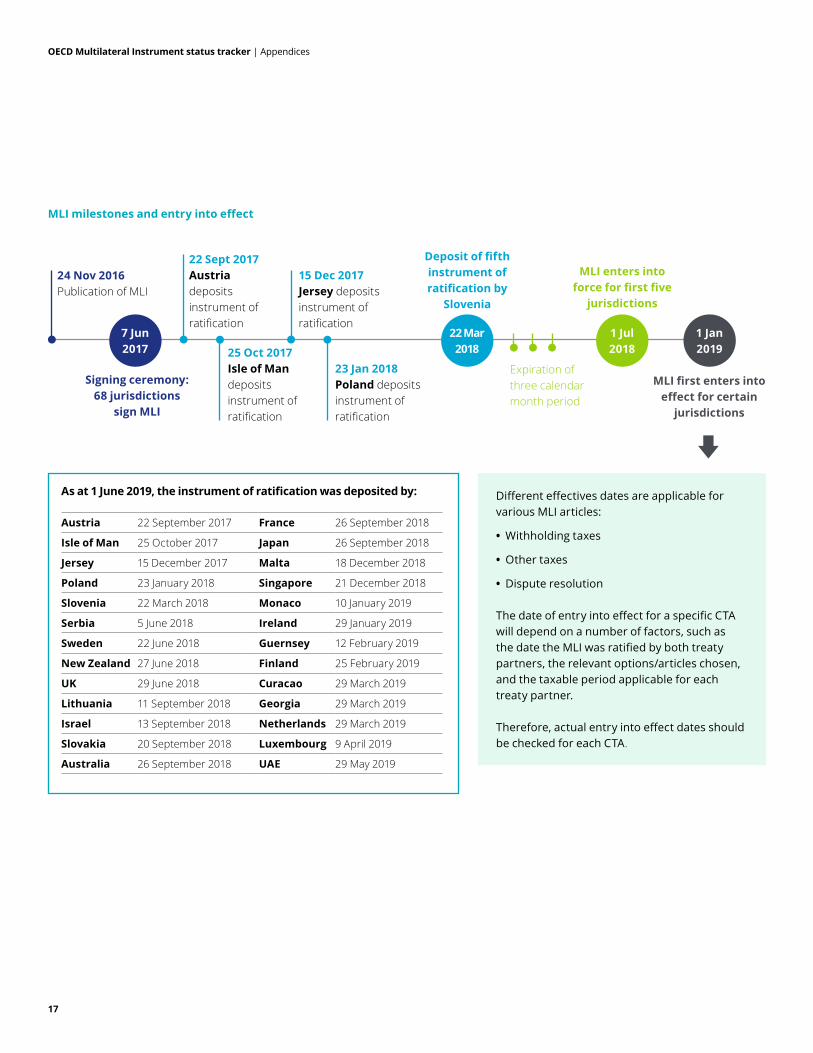

MLI milestones and entry into effect

24 Nov 2016Publication of MLI

22 Sept 2017Austria deposits instrument of ratification

25 Oct 2017Isle of Mandeposits instrument of ratification

23 Jan 2018Poland deposits instrument of ratification

Expiration of three calendar month period

Deposit of fifth instrument of ratification by

Slovenia

MLI enters into force for first five

jurisdictions

MLI first enters into effect for certain

jurisdictions

Signing ceremony: 68 jurisdictions

sign MLI

15 Dec 2017Jersey deposits instrument of ratification

7 Jun 2017

22 Mar 2018

1 Jul2018

1 Jan 2019

As at 1 June 2019, the instrument of ratification was deposited by:

Austria 22 September 2017 France 26 September 2018

Isle of Man 25 October 2017 Japan 26 September 2018

Jersey 15 December 2017 Malta 18 December 2018

Poland 23 January 2018 Singapore 21 December 2018

Slovenia 22 March 2018 Monaco 10 January 2019

Serbia 5 June 2018 Ireland 29 January 2019

Sweden 22 June 2018 Guernsey 12 February 2019

New Zealand 27 June 2018 Finland 25 February 2019

UK 29 June 2018 Curacao 29 March 2019

Lithuania 11 September 2018 Georgia 29 March 2019

Israel 13 September 2018 Netherlands 29 March 2019

Slovakia 20 September 2018 Luxembourg 9 April 2019

Australia 26 September 2018 UAE 29 May 2019

Different effectives dates are applicable for various MLI articles:

• Withholding taxes

• Other taxes

• Dispute resolution

The date of entry into effect for a specific CTA will depend on a number of factors, such as the date the MLI was ratified by both treaty partners, the relevant options/articles chosen, and the taxable period applicable for each treaty partner.

Therefore, actual entry into effect dates should be checked for each CTA.

OECD Multilateral Instrument status tracker | Contacts

18

Aart NoltenGlobal BEPS [email protected]

Tom DriscollNorth America BEPS [email protected]

Eduardo Barron Latin America BEPS [email protected]

Claudio CimettaAsia Pacific BEPS [email protected]

Lisa Scott Global International Tax [email protected]

John HenshallTransfer Pricing Expert,Deloitte Representative to the [email protected]

Alison LobbTransfer Pricing Expert, Deloitte Representative to the [email protected]

Kate RammDeloitte OECD [email protected]

Contacts

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms are legally separate and independent entities. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our network of member firms in more than 150 countries and territories serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 264,000 people make an impact that matters at www.deloitte.com.This communication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member firms and their related entities (collectively, the “Deloitte network”). None of the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2019. For information, contact Deloitte Touche Tohmatsu Limited.RITM0258424 CoRe Creative Services