OF INSIGHT 2015 KPMG Global Energy Conference Recap An event from the KPMG Global Energy Institute kpmgglobalenergyconference.com 2015 GLOBAL ENERGY CONFERENCE An event from the KPMG Global Energy Institute

Transcript

OF INSIGHT

2015 KPMG Global Energy Conference Recap

An event from the KPMG Global Energy Institute

kpmgglobalenergyconference.com

2015GLOBAL ENERGY CONFERENCE

An event from the KPMG Global Energy Institute

Table of

contents1 Introduction2 Keynote addresses

2 Jack Welch, Best-selling Author & Executive Chairman, Jack Management Institute4 Michio Kaku, Theoretical Physicist and the New York Times Best-selling Author5 Barbara Corcoran, Real Estate Mogul and Investor on ABC’s Shark Tank

6 General sessions6 Pioneering Better Business Models8 Energy’s Roles in the Global Economy from Production to Consumption

10 Panel discussions10 Women in Energy Executive Breakfast10 Engineering Success – The Science Behind Thriving STEM Organizations12 Oil and gas track12 Creating the Midstream Company of the Future14 Equipping the Future: Keys to Success for Oilfield Service Companies16 Prosperity and Purpose: Oil and Gas Corporate Citizenship17 Seeking Higher Returns: Integrating Strategic Planning and Dynamic Capital Allocation18 Power and utilities track18 The Agile Utility of Tomorrow19 Now Trending in Distributed Generation20 Winning the Race for the Customer – Strategies to Exceed the Expectations for the New Utility Customer22 Utilities Transformation: Power up the Network Integrator23 Technical track23 Tax Issues and Opportunities in a Low Commodity Price Environment24 Emerging Energy Economies: China, Mexico and Sub Saharan Africa25 Enabling Disruptive Technologies26 What’s on the Horizon? Accounting and Reporting Update

IntroductionJohn Kunasek, U.S. sector leader for Energy & Natural Resources, KPMG LLP (U.S.), and Regina Mayor, National Advisory Industry Leader, Energy & Natural Resources, KPMG (U.S.), set the stage for the conference with a discussion of the mega-trends that will affect how business gets done in the future, including global demographic shifts and disruptive technological changes that will affect the energy industry.

Mayor noted that only a year earlier the market was fundamentally different and the outlook was for higher prices. Few expected or predicted the rapid decrease in prices and now many question whether this is the “new normal.” In addition to the falling prices, the energy industry faces disruption from many other fronts. The goal of the conference, she said, was to help executives think through potential future scenarios amid these changes. “What’s the Uber for our industry?,” she asked.

Mayor discussed advancements in augmented reality and how virtual data could be simultaneously overlaid with reality. A worker could look at a piece of equipment and simultaneously review the manufacturing and maintenance detail and access multiple information sources while problem solving. Training as we currently know it today could become obsolete. In addition, she noted technology is leveraging mobility and robotics to access dangerous and remote locations without putting humans in harm’s way. The same technologies could be applied to analyzing geologic formations. “Could we get to a future with no more dry holes?”

Kunasek discussed how both economic sharing and artificial intelligence have already led to technology-driven market expansion, closed the producer-consumer gap, and improved insight through greater data availability. “We’re seeing a lot of these technologies starting to converge to do pretty remarkable things,” he said.

Kunasek noted that the future could see more collaborative organizations with increased decentralized peer-to-peer business models that can create new insight and make more effective decisions. “They’re starting to come together around tailoring an electric services offering to exactly your wants and needs,” Kunasek said. “Greener, cheaper and more reliable energy.”

Mayor discussed how 3D printing is bringing just-in-time manufacturing and supply chain costs savings through the efficient use of raw materials. She explained how this technology could remake the supply chain and transform manufacturing by reshaping the product development process. “Envision a world where your supply chain is based only on the raw materials to create the equipment and you’ve got a 3D printer to manufacture all the equipment and spare parts that you need on a real time basis.”

Kunasek stated that nanotechnology could also bring disruption to the energy industry, as more powerful and smaller smart devices become integrated into equipment. “Think small, really small!” The so-called “internet of things” could also allow for real-time communication between devices that is reducing the need for human interaction. This has already increased the quality of services with fewer failures, increased response times, and improved security. The future could bring a self-healing resilient energy grid.

Mayor noted that while it is difficult to predict the future, the goal of the conference was to get executives to start thinking about those potential scenarios. “We wanted to open your minds to those new ideas and share insights from other industries and other luminaries,” she said. Because while we have demonstrated we are not able to predict the future, perhaps with this new insight, we will have the opportunity to adapt and change as these mega-trends have more far reaching effects.

During more than 20 years as CEO of General Electric, Jack Welch helped the company grow from a market capitalization of $13 billion to over $400 billion. In 2000, he was named “Manager of the Century” by Fortune magazine. In a wide-ranging discussion, he shared with the audience some of the most important lessons he has learned during a legendary career in business.

When asked about success factors for companies, he stressed the importance of people. “Business is a game, and the team with the best players wins.” When he was an executive, he looked for people with energy, the ability to firmly say yes or no, the ability to execute on time, and the passion to win. “It’s all about getting the right talent. Talent beats strategy, and finding the right talent is the toughest job in the game.”

Once the talent is in place, Welch said, a company should maintain an atmosphere of truth and trust. “Ideally, in every conference room, you’d have a red light flashing Truth Only.” This emphasis on truth and trust is especially important in today’s digital age. “Information is no longer power. Everybody knows everything. The days when you might hold back because you thought you knew more than someone else isn’t a good game plan. Companies should be as transparent as possible.”

He also had some straight talk about business-as-usual procedures. “The budget review is one of the dumbest things ever invented.” He argued that the budgets are often a compromise between over projected costs and revenues. “The review becomes an exercise in how little a department can do.” Instead, budget holders should focus on increased performance over last year, and present an annual budget based on specific answers to five key questions:

What is the current playing field and who are the players?

What has the competition been doing over the past year?

What have we done?

What keeps us up at night worrying about the competition?

What is our checkmate move?

Answering these five questions, Welch said, helps people think in broader terms, and that is really what innovation is about. “Innovation is not a single event or introducing a new technology. It’s about finding a better way, every day, for every person to do their job. We should celebrate incremental improvements all the time, so everyone is innovating.”

Now is the time to pay your best people more than ever paid them. Great teams double up and triple up on great players in tough times.

—Jack Welch

Jack Welch, Best-selling author & Executive Chairman, Jack Management Institute

Keynote

addresses

Welch was equally frank about the popular idea of using shareholder value as a growth strategy. “Shareholder value is not a strategy. It’s simply the result of doing things right. It’s the output of everyone’s efforts.” Instead, he suggested that companies and their investors focus on employee engagement, with everyone supporting the same mission, customer satisfaction, and cash flow. “If you get these three things right, then shareholder value is going to rise.”

Welch was asked about advice for today’s global energy companies, and he underscored the need to hire people with a “global mindset” that included the ability to discern differences in how companies do business across regions. He also addressed the issue of low commodity prices, returning to his theme of supporting a company’s talent. “Everybody thinks about cutting back, but I disagree. Now is the time to pay your best people more than ever. Great teams double up on great players in tough times. You should inflict greatness on the people you need for the long haul.”

a common language—by just looking at someone who is speaking, a running translation of what they are saying would appear as subtitles under their face.

As another example, Kaku explained how 3D printers can be used by energy workers in the field to create replacement parts in a matter of minutes, eliminating the need to suspend operations for days or weeks while a new part is ordered and delivered. Equally important, computer sensors will be able to better monitor oil fields, pipelines, and refineries, providing much higher levels of information in real time to help prevent system failures, measure performance, reduce downtime, and manage safety risks. “Computer sensors can make energy self-aware,” he said, enabling the intelligent oil field, smart power grids, and new advances in battery technology—all of which can move Hubbert’s Peak forward, lower energy costs, and support a more sustainable use of our energy resources.

These predictions might seem farfetched today, but Kaku reminded us that not so long ago, the technology we now take for granted would have been considered impossible. Referring to the Apollo space missions over 40 years ago, he said, “Your cell phone today has more processing power than all of NASA in 1969.” He suggested that even greater strides are possible in the years to come.

For the energy industry, he concluded, the question of innovation is not a matter of if but when. “You ignore technology at your own risk. You need to be a surfer. You don’t resist or you’ll crash. You’ll wipe out. Ride the wave of technology, and then you can anticipate the future.”

When Michio Kaku was eight years old, he found his mission in life. Einstein had just passed away, and the boy decided that he would finish Einstein’s work to extend the theory of general relativity and unite the known forces of the universe in a Theory of Everything.

That’s a tall order for anyone, but the size and scope of Kaku’s childhood ambition shows that even at an early age he was interested in the biggest questions he could find and how science can help explain them. Since then, Kaku has become a leading theoretical physicist as well as a futurist and well-known commentator on scientific issues in the media. At this year’s conference, he shared with the audience some of his deep insights into science and technology, showing how recent innovations are already changing today’s energy industry.

Kaku argued that the world is being shaped by two megatrends of wealth: the information revolution and the energy revolution. He cited Moore’s Law as driving the information revolution—processing power is doubling every 18 months, an increase that has held steady since the 1960s. He compared this to Hubbert’s Peak, the idea that oil production follows a bell-shaped curve that peaks and declines unless new ways to identify and extract reserves are developed. Kaku argued that the two megatrends are merging to create the “digitalization of energy,” an environment where new technology based on microchips costing less than a penny will soon transform how we capture, distribute, and use energy—often in surprising ways.

In just a few years, Kaku predicted, we will see the widespread use of glasses and even contact lenses that can display complex information downloaded from the Internet. He suggested that workers in oil fields or refineries could use these devices to access technical information, blueprints, or safety information on the spot. The technology could even be used by multinational workers who do not share

Making energy self-aware, sensors everywhere...

—Michio Kaku

The world is being shaped by two megatrends of wealth: the information revolution and the energy revolution.

—Michio Kaku

Michio Kaku, Theoretical Physicist and New York Times Best-selling Author

Probably the most overlooked thing in business, small business, and big business is the fun part.

—Barbara Corcaran

Barbara Corcoran grew up in New Jersey as one of ten children in a busy household. She learned how to be organized, cooperate with others, and not be shy when she had to grab somebody’s attention, especially a parent. These were all valuable skills that she used to her advantage when she moved to Manhattan in the 1960s and started her own real estate business.

Turning a $1,000 loan into a business that she later sold for $66 million, Corcoran has become one of New York’s leading realtors, a best-selling author and a familiar face on television’s popular show “Shark Tank.” In a lively, insightful and often hilarious keynote address, Corcoran shared what she has learned over the years about reaching markets, creating teams, and building successful businesses.

One of the first lessons she learned was the importance of a business’ public image. “If you can look and act successful, you can generally get there.” Talking about her early years in the industry, she explained how hard she worked to make her agency appear larger than it was, mainly through “The Corcoran Report,” a real estate newsletter that she regularly distributed to every newspaper and radio station in town. Within a short time, she was being interviewed in the media as an authority on New York real estate—even though her agency still had less than a dozen employees. “I had to change my philosophy about getting credit before credit is due. In building the publicity, I built the brand, and by building the brand, I had to run and fill up expectations. The image came first and then the reality followed.”

Corcoran also stressed the importance of failure in her career because some of her best ideas came to her when she was facing the prospect of bankruptcy. “Be good at failure. It’s taught me a lot. It gave me great momentum to improve.” When her business was running out of money, she decided to take all her condominium

listings and stage a unique one-day sale. The result was tremendous publicity, hundreds of eager buyers, and millions in sales. At another point, she failed to deliver a convincing presentation to a group of bankers, and she recognized that she needed to improve her speaking skills. She immediately signed up to teach an 11-week business course at New York University, and this led to meeting and hiring one of her students who became one of her top performers.

Important as these lessons are, the item she stressed the most was simply having fun. “Probably the most overlooked part of building a business is being good at having fun.” Surprise parties, regular outings with coworkers, and recognizing employee contributions create an atmosphere where employees learn to trust each other and work closely together. “That’s how you create teams. You all have fun.” She added, “If you have a bunch of people in business having fun, you get a bonus card that’s called creativity.” She suggests that companies earmark five percent of revenues every year as “mad money” to try out new ideas. “This mad money doesn’t roll over to the next year. You use it or lose it. That way, people are encouraged to be creative because there’s no penalty for failing.”

Corcoran said that her mother always announced the talent of each of her children. In Corcoran’s case, it was “imagination.” Her many fans, associates, and business partners would certainly agree with her mother’s insight, especially after looking at all the ways Corcoran has used her lively and surprising imagination to succeed.

Barbara Corcoran, Real Estate Mogul and Investor on ABC’s Shark Tank

Pioneering Better Business Models

The business world is undergoing massive disruption, as technology is changing the way people work and a younger, tech-savvy generation is entering the workforce. In addition, business innovations, such as the sharing economy, and technological innovations, such as artificial intelligence, have accelerated these changes. Many businesses now need to develop improved business models in response. Steven Hill, KPMG’s Vice Chair for Strategic Investments, moderated a panel on pioneering better business models that included Rick Felts, a retired Senior Vice President for IT Operations at AT&T, Jeff Donaldson, Senior Vice President of GameStop Technology Institute, and Adam Steinberg, North American Leader for Analytics & Watson Experience at IBM.

The panel focused largely on the impact of data and analytics. Felts described data as “one of our next game changers” and noted that the data on AT&T’s network has grown by 100,000 percent since 2007. Felts said the key issues are related to governance and emphasized the importance of privacy, security, and the regulatory issues that the influx of data brings. “Building that strategy around all that really becomes the key for driving big data into your business,” he said.

Donaldson noted that while the first step in approaching this influx of data is to map the data and understand where it is located, “step zero” requires companies to completely rethink what they are doing with data. Donaldson discussed how data can be used in operational and tactical process, but he argued that the “key change is to understand how to integrate that data with your strategic processes.” He outlined three critical components of “step zero.” The first is to “collect signals and try to understand what they mean to you,” the second is to “instrument to collect that data,” and the third is “to use that data and experiment with new solutions so you can understand whether or not you’re changing behavior.”

Steinberg said data and governance “are vital to harnessing the utility of the data,” and he discussed how IBM is looking for ways to expand and change business models to take advantage of newly available data. He noted that 90 percent of new data was created in the past two years and 80 percent of that data is unstructured. Most importantly, he emphasized how this requires changes in business systems.

(L to R) Steven Hill, Vice Chair for Strategic Investments, KPMG (U.S.)Rick Felts, retired Senior Vice President, IT Operations, AT&TJeff Donaldson, Senior Vice President, GameStop Technology InstituteAdam R. Steinberg, North American Leader, Analytics & Watson Experience, IBM

The panelists also discussed the ongoing workforce changes, especially with the emergence of the millennial generation, and how those changes are affecting how workplaces are structured. “You really have to deal with different generations in the workforce today,” Felts said. He noted the different attitudes that different generations have toward offices and how the millennial generation wants flexibility and technology where they work.

The panelists each shared their company’s experience with accommodating the new preferences of a younger generation. Steinberg discussed how his company has sought to improve agility and collaboration in the workplace and how this has changed how offices are designed. Donaldson noted how the more collaborative environment has changed certain project management approaches and has led to cost savings. Felts added his views on how technology can improve the connectivity of a work group and how taking a “start-up” approach can enhance agility.

A discussion on the future of cognitive computing brought the relationship between data and the changing workforce into focus. Steinberg stressed how data does not replace human activity but actually helps people improve decision making. “If you think about the explosion of content that’s available to knowledge workers today, it’s nearly impossible for any one worker to truly harness all the information that’s available to make an informed decision,” he said.

Donaldson stated that advances in cognitive computing will change lower-paying jobs and exacerbate rising inequality, but he noted the opportunities in other areas. “At the same time, we don’t have enough engineers, we don’t have enough data scientists, we don’t have enough of the people that would be able to benefit society by developing new ideas, new products.”

It’s nearly impossible for any one worker, pick your sector, pick your section, of the workforce to truly harness all the information that’s available to make an informed decision

—Adam Steinberg, Analytics and Watson Experience Leader, IBM.

She also discussed how China and India account for more than 80% of Asia’s total energy consumption as well as more than 70% of the regions renewables consumption. She argued that coal might not play such an important part of China’s and India’s energy future and noted the breakthroughs in increased battery storage. “Not only does it make alternative fuels more viable but it increases the efficiency of the current coal fired system that we have,” she said, “which suggests that a future of electric vehicles is really not so farfetched.”

Hunter also noted how the “internet of things” will affect energy efficiency. “We’re talking about a really significant change in terms of energy distribution and energy efficiency,” she explained. “When you combine this together and you think about the growth coming out of India and China, what it suggests is that the forecasts don’t sufficiently take into account the demand for alternatives, nor do they sufficiently take into account the efficiency gains that are likely to be seen in coming decades.” Hunter discussed recent forecasts for growing energy demand in response to population and GDP growth. “What seems to be missing from these forecasts is a really deep understanding of the new technologies that are going to be game changers for the energy industry.”

Fung continued the focus on China and noted that China grew from being poorer than many African companies to one of largest economies in the world. “Even when we say it’s slowing down, the absolute growth is huge,” he said. Fung said an important factor is where growth is coming from and noted that earlier growth was from infrastructure and manufacturing. “Many of these now are not sustainable,” he said. He noted that China’s government is encouraging investment in hi-tech industries, and also stressed the effect of urbanization. “China will move 300 million people from rural areas to cities,” he said, an area equivalent to the entire U.S. population. “Imagine you move that scale of people into cities, demand for energy is going to be huge.”

I think the place to look in terms of supply is not just traditional fossil fuel supply but all of the other potential alternative supply that is coming in exponential leaps and bounds.

—Constance Hunter Chief Economist for KPMG (U.S.)

Energy’s Roles in the Global Economy from Production to Consumption

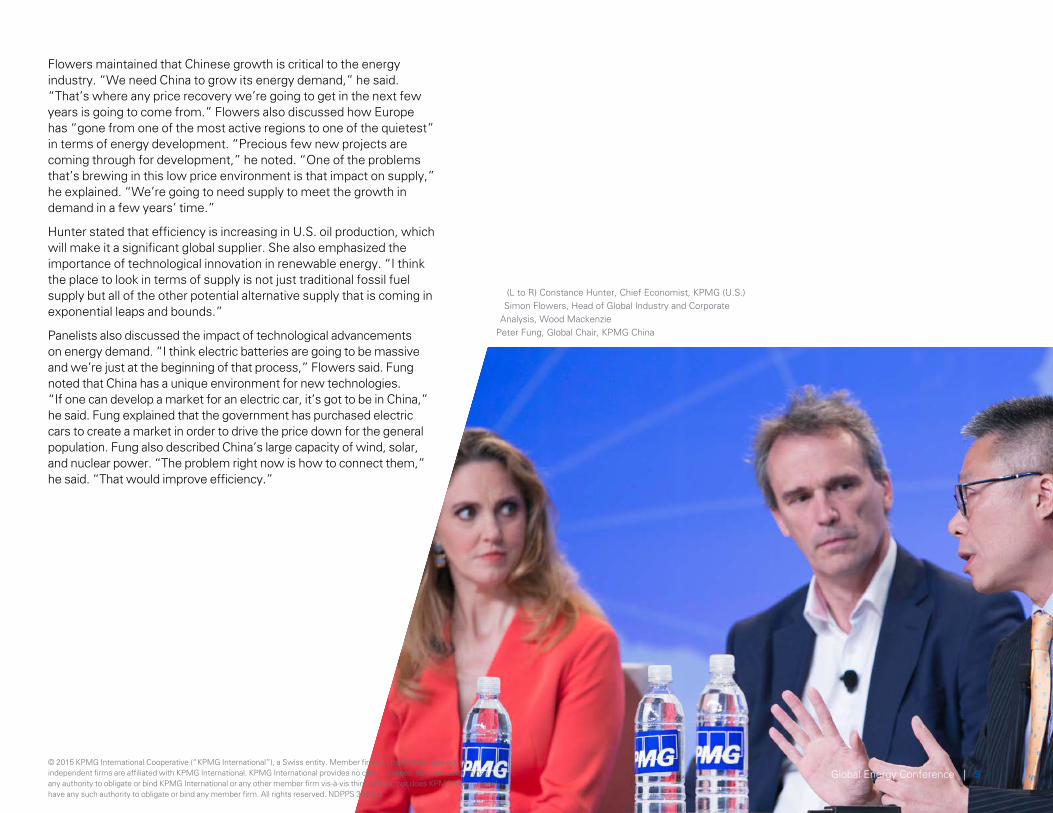

Moderated by John Kunasek, U.S. sector leader for Energy & Natural Resources, KPMG LLP (U.S.), and Regina Mayor, U.S. Energy & Natural Resources Advisory leader, KPMG LLP (U.S.) the second day of the conference opened with a panel discussion on the global impact of recent energy price volatility. Constance Hunter, Chief Economist for KPMG (U.S.), Simon Flowers, Head of Global Industry and Corporate Analysis at Wood Mackenzie, and Peter Fung, Global Chair for KPMG China, shared their views on energy demand, improvements in efficiency, and the impact of new technologies.

Hunter gave her overview of the global energy markets and focused on changes in demand from Asia. In explaining the price decline for oil, she said the increase of U.S. supplies happened around the same time that demand from China fell. This had a strong impact on global oil prices, as China’s recent significant demand growth for commodities linked the price of oil to the prices of other commodities. “This speaks to the influence that China’s demand for these commodities had on prices,” she said.

Hunter said the price of energy is historically inelastic because there was no substitute. “There’s really good reason to think that this might be starting to change, and not just because of renewables but also because of efficiency gains,” she said. Hunter argued that energy is ripe for innovation and that disruption could come in the form of energy efficiency and improved battery technology.

Economic Perspectives:

Flowers maintained that Chinese growth is critical to the energy industry. “We need China to grow its energy demand,” he said. “That’s where any price recovery we’re going to get in the next few years is going to come from.” Flowers also discussed how Europe has “gone from one of the most active regions to one of the quietest” in terms of energy development. “Precious few new projects are coming through for development,” he noted. “One of the problems that’s brewing in this low price environment is that impact on supply,” he explained. “We’re going to need supply to meet the growth in demand in a few years’ time.”

Hunter stated that efficiency is increasing in U.S. oil production, which will make it a significant global supplier. She also emphasized the importance of technological innovation in renewable energy. “I think the place to look in terms of supply is not just traditional fossil fuel supply but all of the other potential alternative supply that is coming in exponential leaps and bounds.”

Panelists also discussed the impact of technological advancements on energy demand. “I think electric batteries are going to be massive and we’re just at the beginning of that process,” Flowers said. Fung noted that China has a unique environment for new technologies. “If one can develop a market for an electric car, it’s got to be in China,” he said. Fung explained that the government has purchased electric cars to create a market in order to drive the price down for the general population. Fung also described China’s large capacity of wind, solar, and nuclear power. “The problem right now is how to connect them,” he said. “That would improve efficiency.”

(L to R) Constance Hunter, Chief Economist, KPMG (U.S.)Simon Flowers, Head of Global Industry and Corporate

Analysis, Wood MackenziePeter Fung, Global Chair, KPMG China

(L to R) Regina Mayor, National Advisory Industry Leader, Energy & Natural Resources, KPMG (U.S.)Kim Bates, Vice President Asia Pacific/Middle East, ExxonMobil Exploration Company

Dr. Bonnie Dunbar, M.D., Anderson Professor of Mechanical Engineering, Director of UH STEM Center, Aerospace Engineering Graduate Program, and SICSA Space Architecture Programs at the University of Houston

Tina V. Faraca, Vice President, U.S. Construction, Spectra EnergyLynne M. Doughtie, Chairman-elect and CEO-elect, KPMG (U.S.)

PaneldiscussionsWomen In Energy Executive Breakfast:

How can energy companies nurture budding STEM (science, technology, engineering, and mathematics) female students, attract them to their organizations, and retain and mentor them throughout their careers? This discussion kicked off the 2015 Global Energy Conference, starting with an early morning breakfast for women.

Regina Mayor, National Advisory Industry Leader for Energy & Natural Resources, KPMG (U.S.), moderated a panel of three industry women leaders—all of whom are accomplished for taking charge of highly technical, scientific, and engineering-related programs.

Lynne M. Doughtie, Chairman-elect and CEO elect of KPMG (U.S.), welcomed participants by showing her commitment to encouraging STEM initiatives and providing her own experience with her children, who are both engineers. STEM, she said, is “important to us as women leaders, in encouraging the next generation of leaders to achieve their objectives. STEM is near and dear to all of our hearts. How can we make a difference?”

The panelists shared individual stories regarding how they got interested in science as children. Dr. Bonnie Dunbar, M.D. Anderson Professor of Mechanical Engineering, Director of UH STEM Center, Aerospace Engineering Graduate Program, and SICSA Space Architecture Programs at the University of Houston, has a long list of outstanding accomplishments, including having been on five shuttle flights. Raised on a cattle ranch in Washington state, she was exposed to learning about nature, physics, and astronomy in daily life. It was her physics teacher who suggested she pursue engineering. Dr. Dunbar shared some important statistics relative to the pipeline of women in STEM programs and graduating universities.

Tina V. Faraca, Vice President, U.S. Engineering and Construction, Spectra Energy, has a distinguished career in the midstream business and received a degree in petroleum engineering. She said she always loved math and science. “I liked tinkering with things and mixing things that were under the sink that you’re not

STEM is near and dear to all of our hearts I think especially in this room. How can we make a difference?

—Lynne M. Doughtie Chairman-elect and CEO-elect, KPMG (U.S.).

supposed to mix,” she said. Her father led a very tough lifestyle on an oil rig and encouraged her to find her vocation in another industry. But she knew she wanted to follow in his footsteps somehow, but as a member of management.

Kim Bates, Vice President Asia Pacific/Middle East at ExxonMobil Exploration Company, and a geologist, has been with the company for more than 30 years. She said her dad is a mathematician, and dinner table conversation was often related to math or physics. In college, she decided to take an introduction to geology course to fulfill a science requirement. The instructor, a prominent geoscientist, gave “the most enjoyable class in my life,” she said. Bates advised the audience to make the time to be a visible role model and personally connect with young women in the organization or in school.

All the panelists agreed that when leading in predominately male working environments, younger women can take the following advice:

1. Be true to yourself

2. Understand your passions

3. Know when to lead and when to be a team player

4. Continue to learn

5. Do your best at the job you have

If you take away the engineers they’ll be sitting on a grassy hill someplace eating raw meat, with furs but no clothes.

—Tina V. Faraca Vice President, U.S. Engineering and Construction, Spectra Energy.

When you look at the statistics what is concerning to me is that only 19% of engineering graduates are women.

—Dr. Bonnie Dunbar M.D., Anderson Professor of Mechanical Engineering, Director of UH STEM Center, Aerospace Engineering Graduate Program, and SICSA Space Architecture Programs at the University of Houston.

The same number of competitors are out there, now they’re all laser-focused on the plays that work today.

—Bryan W. Neskora Chief Operating Officer & Partner at Navitas Midstream Partners

Creating the Midstream Company of the Future

Midstream companies face challenges in meeting the needs of long term demand growth, and these challenges often require them to adopt new business models and develop new capabilities. Tandra Jackson, Partner, KPMG (U.S.), moderated a panel on these issues that included Bryan W. Neskora, Chief Operating Officer & Partner at Navitas Midstream Partners, LLC; Pam Beall, President of Marathon Petroleum Pipeline (MPLX); and Heath Deneke, President, Natural Gas Business Unit, Crestwood Midstream Partners, LP.

Bryan W. Neskora of Navitas Midstream Partners discussed the changes in the industry with the fall in oil prices. “As much as it’s changed for the upstream industry, I think it has changed just as much for the midstream industry,” he said. Neskora noted that the focus is now on the “core of the core,” as there are far fewer opportunities in a low-price environment. He also said there was more competition in the market than there was a year ago, as private equity firms have not exited the market as expected. “The same number of competitors are out there, now they’re all laser focused on the plays that work today,” he said. Heath Deneke of Crestwood Midstream Partners also noted the increased competition, especially in the M&A market.

Pam Beall, President of Marathon Petroleum Pipeline (MPLX) noted that for her business there were still many opportunities in the lower price environment.

“The refining business is not really driven by the flat price of crude oil, it’s a spread business,” she explained. “Even though the crude prices are low, the margin that the refiners are able to capture has been robust.” Beall noted the volatility and difficulty in sustaining this growth. “Marathon Petroleum is focused on growing the midstream business and growing the retail business so we can offset some of that volatility in earnings and cash flow from the refining business with more steady cash flow from midstream and retail,” she said.

Regulation was also on the minds of the panelists, and Deneke discussed regulatory challenges as a form of risk management. “There’s a fair amount of time and diligence both from a government affairs standpoint all the way through to environmental permitting, through landowners to dealing with local constituencies and nongovernmental organizations,” he said. “It’s really about half the battle these days in developing organic projects.”

The panel also discussed the core capabilities that their companies must continue to focus on. Neskora noted the importance of both execution and relationships. “Having a track record around effective execution is key,” he noted. “To even get to that point, you need a very creative commercial group and long-standing relationships in the prouder community to get a foot in the door.”

Oil and gas track

Beall emphasized the importance of logistics to Marathon’s customer service focus. “It’s one continuous supply chain, and logistics is really key to getting the crude to the refineries on time, getting the products out to the market, and actually allowing the company to capitalize on dislocations in the market.”

In an environment of possible increased M&A activity, Deneke discussed the value of his company’s ability to acquire assets and integrate them quickly: “I think as Crestwood has grown from its initial investment to the platform that we have now, I think that was a key attribute and competency that we look towards.”

Sanjay Bhatia, Vice President of Corporate Development for FMC Technologies, discussed how returns for deep water projects have fallen over the past couple of years because of rising capital costs leading to project delays. “Even at $90 oil some of the projects weren’t quite flying over the hurdle in terms of a returns standpoint,” he said. “Of course, in a $60 price environment that we find ourselves in today, that just exacerbates it.”

In light of these headwinds, the panelist discussed operational improvements that have helped companies in this environment. Bhatia touted the importance of optimizing equipment design and reducing complexity. Tomlin emphasized the need for producers to decentralize procurement decision making and empower people at the well site to make key decisions. “That’s how everybody saves money; not by beating on price or driving labor costs down,” he said.

New technology also offers a means by which to differentiate a company from its competitors. Bhatia discussed the importance of integrating technology to reduce complexity and the costs of production. “There’s two buckets: what can we do with today’s technology just by integrating and driving new approaches and what can we drive in the new technology bucket mainly around increasing oil recovery.”

The panelists also agreed that the downturn could be used to improve processes and customer service. “We have a chance to really improve some of the competencies within our company because people have a chance to actually build them,” Bhatia said. “I think that a positive of having a bit of a breathing space for the next 12 – 18 months is to put some things in place to strengthen our company for the longer term.” Hajdik said his company was using the slowdown for a large ERP project that they would not have been able to do previously. “It’s a great time to do it, and we have some idle capacity.”

Finally, the possibility of increased M&A activity was also discussed as an important element in this new environment. Tomlin said there were more opportunities now than in the previous downturn but noted that there remained a disconnect between buyers’ and sellers’ valuation expectations which had limited the number of transactions closed so far this year. Overall, the panelists agreed on the need to make acquisition that fit with the company’s strategy rather than simply finding cheap deals.

Equipping the Future: Keys to Success for Oilfield Services Companies

The current downturn in oil prices and the anticipated increase in M&A activity will significantly impact the oilfield services sector. This change brings an opportunity to redefine sector strategies to be better equipped for the future. Chris A. Click, Principal, KPMG (U.S.), moderated a panel that discussed how oilfield services companies can deliver value to customers against a backdrop of potential consolidation, new competitors, technological innovation, and increasing consumer demands.

Lloyd Hajdik, Senior Vice President, Chief Financial Officer, and Treasurer for Oil States International, Inc., explained that the domestic market for oilfield services and the offshore market for production equipment each face particular challenges. “I think you have to separate deep water in the oilfield services segment against the North American onshore,” he said. “Very short cycle onshore, much longer time horizon offshore.”

Todd M. Tomlin, Partner at Turnbridge Capital, explained the impact the price decline has had on the complex supply chains and infrastructure of the onshore shale plays. “It’s been far more difficult onshore for the industry to respond to this slowdown,” he said. He noted that many of the smaller, onshore producers face more uncertainty as to what they are going to do next which creates increased volatility for the related service and equipment suppliers.

14 | Global Energy Conference

So I think that a positive of having a bit of a breathing, hopefully it’s just a bit, of a breathing space for the next 12 – 18 months is to actually put some things in place to strengthen our company for the longer term.

Flemming explained how collaboration is making a difference not only to create new jobs in industries other than oil and gas but also “to get a much better common understanding as to what the problems are.” He emphasized how this approach takes longer than the traditional corporate philanthropy.

The panelists also discussed what energy companies should have done differently if they could start over. Flemming said he would recommend a much more participatory approach and multi-stakeholder approach with the community. “If these approaches had been taken at the beginning, we wouldn’t have had these problems, and I think the region would have had the opportunity to focus a bit more attention on the non-oil-and-gas element of the economy,” Flemming said. “You’re really having to rebuild those industries over again in a region that once knew them quite well.”

Nonetheless, the panelists agreed that oil and gas companies and development agencies did not have all the answers to solving global poverty. “The people that know the most about how to develop the communities are the community members,” Flemming said. “As soon as one starts thinking that they have all the answers, that’s when they stop being effective.” Joshi agreed that no one has all the answers on how to achieve this ambitious goal. “This will require the greatest collaboration of individual and companies and civil society and government that we’ve ever seen in history.”

[Ending poverty] This will require the greatest collaboration of individuals and companies and civil society and government that we’ve ever seen in history.

—Rajiv Joshi Managing Director, The B Team

Prosperity and Purpose: Oil and Gas Corporate Citizenship

With the emergence of globalization and increased customer expectations, corporate citizenship is a standing agenda item during all shareholder meetings. Lord Dr. Michael Hastings CBE, global head of Corporate Citizenship for KPMG International, moderated a panel that discussed the importance of corporate citizenship within oil and gas activities and outlined the ways in which companies, governments, NGOs, and consultancies can achieve mutual benefit by working together.

Rajiv Joshi, Managing Director at The B Team, discussed the idea that climate change and development should be addressed together. “Many of us recognize we are in an important moment in history,” he said. “For the first time, we have all the technology, all the resources, to put an end to human suffering and poverty in the world, but at the same time human behavior also has the potential to destroy that that we find most dear.” Joshi argued that the global economy must transition to low-carbon emissions and discussed how many companies are seeing this as a business opportunity. “For us now, the opportunity, recognizing that there will be a transition, is to ensure that that transition is also an opportunity to leave no one behind,” he said.

Paula McCann Harris, Director of the Global Social Responsibility Programs and SEED at Schlumberger, explained that the attitude toward social and environmental problems “is still evolving from throwing money at the problem without a strategy and without a lot of collaboration.” She said there is a change to a more global mind set in which prosperity and purpose come together, but she cautioned that this requires increased collaboration across different groups.

Dennis Flemming, Executive Director of the Niger Delta Partnership Initiative, discussed the recognition by Chevron that it should work to benefit not only the communities close to the operations, but also the Niger Delta region as a whole. He noted that Chevron has committed money to address social and environmental issues in the region but with the idea that the company really needs to be involved in collaborations and partnerships.

(L to R) Lord Dr. Michael Hastings CBE, Global Head, Corporate Citizenship, KPMG InternationalDennis Flemming, Executive Director, Niger Delta Partnership Initiative

Paula McCann Harris, Director, Global Social Responsibility Programs and SEED, SchlumbergerRajiv Joshi, Managing Director, The B Team

Our focus is much more on being a catalyst for growth and economic development.

Seeking Higher Returns: Integrating Strategic Planning and Dynamic Capital Allocation

The boom in unconventional sources of oil and gas is changing capital planning. Companies are reassessing traditional annual capital allocation and budgeting, which often become the de facto operating plan for business units, and adopting more dynamic approaches. Angela D. Gildea, Principal, KPMG LLP (U.S.), moderated a panel on these changes that included Bill Frank, general manager, Business Development and Commercial at Chevron North America Exploration and Production Co; Richard A. Burnett, vice president, chief financial officer, and chief accounting officer for EXCO Resources, Inc.; and Greg Guidry, executive vice president, Unconventionals, Upstream Americas for Shell.

Richard Burnett discussed how the downturn, driven by increased oil supplies, has been offset by a strong supply of available capital. “Unlike the past where maybe the capital providers have not been as prevalent in the downturn, that clearly has not been the case today as we see a significant amount of capital that are still looking for opportunities within the energy sector,” he said.

Taking the point of view of an international oil company, Bill Frank discussed how Chevron’s North American business unit has traditionally funded other areas of the

company, but that has reversed this year. “That’s never happened in my tenure, and I think that’s an indication of a whole variety of geopolitical and macroeconomic forces and, of course, the unconventional boom,” he said.

Greg Guidry of Shell discussed how the capital allocation processes that work for conventional oil plays do not work very well in unconventional plays. “We stress test our processes in unconventionals, and we learn a whole lot more about them in terms of their weaknesses and their vulnerabilities and find that some of our conventional processes are not as robust as we thought,” he said. He noted that bottom-up tools used for conventionals can be very complex and unwieldy.

Guidry also discussed some of the particular challenges to capital planning from unconventionals. “The most difficult thing has been how do you simplify without being too simplistic.” he said. “How much do I model versus how much do I granular bottom build?” Guidry noted the importance of taking a different approach to this planning for unconventionals. “You do not have to do it different in conventionals, you just make less money.”

Frank noted that Chevron has had more opportunities than capital over the past few years. He described the importance of being able to react to changes in the business to reallocate capital. “If some huge project isn’t going to go this year, and we find that out in May, we might be able to do something about ramping up spend,” he said. Frank also noted the flexibility that unconventional plays can provide. “You can’t have a portfolio full of giant deepwater projects; you just don’t have enough flexibility,” he explained. “Within reason the unconventionals can provide that buffer.”

Burnett said available capital was reduced because companies are focusing on existing projects. “That forces you to put more capital into the projects than you originally thought,” he said. “We’re spending a lot of time as this process has continued to work its way through focused on what our partners are going to do.”

The panelists also discussed the importance of being nimble in the capital allocation process and changes toward shifting capital on a quarterly instead of an annual basis. “As long as we’re performing within a certain set of boundaries, we’re free to shift it around on a quarter-to-quarter basis,” Guidry noted. “That has helped a lot for unconventionals.”

Unlike in the past where maybe the capital providers have not been as prevalent in the downturn, that clearly has not been the case today as we see a significant amount of capital looking for opportunities within the energy sector.

—Richard A. Burnett Vice President, Chief Financial Officer, and Chief Accounting Officer for EXCO Resources

Global Energy Conference | 17

(L to R) Richard A. Burnett, Vice President, Chief Financial Officer and Chief Accounting Officer, EXCO Resources, Inc.

William E. (Bill) Frank, General Manager, Business Development and Commercial, Chevron North America Exploration and Production Co.

Facing unprecedented and interrelated challenges, today’s utilities, stable for a half century, will change significantly in the next 10 to 20 years. Katherine Blue, Managing Director KPMG (U.S.), Climate Change and Sustainability, KPMG, led a wide-ranging session on how this change will occur.

Changes in customer behavior is one prominent force at work. James H. Lambright, Senior Vice President of Corporate Development for Sempra Energy, observed that three categories of transformational forces—technological, policy, and market forces—interact with each other. From fracking to solar, he said, these technologies get accelerated by policy support and then lead to new kinds of customer behavior in the market.

Asked how their companies are responding to agility, panelists gave a range of examples. Carolyn J. Burke, Executive Vice President of Business Operations for Dynegy, pointed out that her company has built scale, going from a 9,000-megawatt independent power producer to 26,000 megawatts as Dynegy took advantage of utilities shedding their merchant businesses.

Lambright answered that on the nonutility side, Sempra was stripping out risk with long-term contracted cash flows. On the utility side, they are testing operational efficiencies such as unmanned aircraft to inspect disruptions. Rate reform efforts include changes to metering policy to better balance costs and to minimize cross-subsidies between those with solar on their roofs and those without. As an example of managing growth, he observed that San Diego has around 16,000 electric vehicles in use, three times the national average, yet not a lot of charging stations. His company is seeking approval to have the utility install and maintain charging stations, particularly in apartment buildings and work places.

Joe Hoagland, Vice President of Stakeholder Relations for the Tennessee Valley Authority (TVA), also sees customer behaviors as a key transformative force. TVA’s generation capability, which has evolved over the past 70 years, “may or may not be what folks want in the future.” Providing cheap, reliable electricity is still very important, but customers also want it to be cleaner; they may need it to be demonstrably sustainable, or they may even want their own microgrid structure.

Vanessa C. L. Chang, principal and independent director on the board of Edison International, said her company has seen electricity consumption go down and commercial and industrial customers leave the grid. This has meant spreading a $50 billion balance sheet among the remaining rate payers. On average, she said, only 48 percent of the electricity that is generated is used, “and yet we’ve built this asset base for peak demand.” Edison International is trying to modernize the distribution system with advanced, flexible, and two-way electric flows.

Edison International, Chang explained, has committed capital to a range of businesses, including commercial solar transmission, clean power finance, HVAC optimization for large commercial and retail installations, and an electric bus company. She emphasized that they are looking to those entrepreneurial workforces “for ways to integrate, share, and cross-fertilize the utility mindset with the venture-capital entrepreneurial mindset.”

How are companies starting to think about the future for agility? Hoagland’s example was one discussed frequently at the conference. “The reality is, if you’re a utility and somebody puts a solar panel on their house, what are you? You’re the battery,” he said. “We ought to take advantage and work with those companies, for the fact that we already provide a very robust, a very strong battery into the system.”

The reality is, if you’re a utility, and somebody puts a solar panel on their house, what are you? You’re the battery.

— Joe Hoagland, Vice President of Stakeholder Relations for the Tennessee Valley Authority

Power and utilities track

(L to R) James H. Lambright, Senior Vice President, Corporate Development, Sempra EnergyCarolyn Burke, Executive Vice President, Business Operations and Systems, Dynegy

Joe Hoagland, Vice President, Stakeholder Relations, Tennessee Valley AuthorityVanessa Chang, Principal and Independent Director, El & EL Investments, Edison International and Transocean

Matthew Smith, Principal, KPMG (U.S.), moderated a wide-ranging discussion of recent trends in distributed generation with panelists representing electric delivery, fuel cell technology, renewable energy, and energy management products and services.

“Let’s face it—energy isn’t always that sexy,” conceded Josh Richman, Vice President, Global Business, Development and Policy, Bloom Energy Corporation. Like the other panelists, however, he argued that distributed generation represents a strong and growing market. ”Customers want to have a source of personalized energy that they can control,” he said. “They want to manage this energy in different ways instead of having to take whatever they can get from the grid.” He pointed out that challenges remain involving interconnections, regulatory barriers, and installation costs, but cost reductions in solar, net thermostats, the “Bloom Box” Energy Server, and the Tesla Wall home battery are changing the face of the industry. He also pointed out innovations on the business side that are supporting new growth, including finance offerings and partnerships with utilities.

Don Clevenger, Senior Vice President, Strategic Planning, Oncor Electric Delivery, made an analogy between today’s utilities and the automotive industry in the 70s. “The car makers were telling the customers what they should need, but the customers were talking about what they wanted.” At the same time, he was clear

There’s this excitement about the ability to have a personalized source of energy that is under your control.

—Josh Richman Vice President, Global Business, Development and Policy, Bloom Energy Corporation

about the demands placed on utilities to deliver base load power across the grid. “On a given day, half of the generation in Texas sits idle. In any other industry, that would be a disaster, but that’s something we’ve come to live with.” He suggested a different scenario where natural-gas fired generation plants could charge a network of batteries during the night and then use this energy to satisfy peak demands during the day. “If we were able to use this kind of storage technology, we could really make the market more efficient.”

Gary Fromer, Senior Vice President, Energy Management Programs, Constellation, discussed the possibility of new business models for utilities. “Today, the utility is trapped in a model where revenue is based on megawatt hours sold. When customers generate their own power, this figure goes down even though the utility is still responsible for the grid. Utilities need to change their business model from being a wires company transacting a part of the megawatt hour to being a systems operator for the network.” The challenge, he said, is to convince slow-moving regulatory agencies to adopt this new model for utilities. “Technology is happening faster, much faster, than the pace of regulatory change.”

Global Energy Conference | 19

(L to R) Matthew Smith, Principal, KPMG (U.S.)Don Clevenger, Senior Vice President, Strategic Planning, Oncor Electric Delivery

Gary Fromer, Senior Vice President, Energy Management Programs, ConstellationJosh Richman, Vice President, Global Business Development and Policy, Bloom Energy Corporation

Winning the Race for the Customer – Strategies to Exceed the Expectations of the New Utility Customer

Rapidly changing dynamics are transforming the customer paradigm. This session took a close look at customer-centric strategies from three points of view. Andy Steinhubl, Principal, KPMG (U.S.), opened the discussion by pointing out that customers are being influenced by sources outside the utility’s control—online shopping, mobile apps, NEST and smart thermostats, and increasing choices around home generation. More choices, more control and higher expectations are some of the earmarks of a new consumer age. The panelists discussed how they are shaping their new approaches, customer experiences and value propositions.

NRG once sold invisible electrons, Sicily Dickenson, Senior Vice President and Chief Marketing Officer, NRG Energy, observed, and customers bought them out of need, like clothing or water. Now NRG is thinking about energy needs in terms of people’s life stages. Among NRG targets she mentioned are Millennials and pragmatic baby boomers. “For us, it really has been about looking at the full energy lifecycle from different segments of people and how we might meet their needs, wherever they are.”

Ari Sargent, Founder and Chief Executive Officer of Powershop, an energy retailer based in Australia and New Zealand, has an entirely different approach. “Our model suits behaviors rather than demographics,” he said. Customers can log on to save money, save energy, feel more in control, and be more comfortable that a winter bill is not a big surprise, he explained.

Powershop was borne of personal frustration. “I used to sit at management meetings and wonder: Why is it so hard to deliver to the customer great service? And you look at the way electricity is sold. It’s 2015, and customers don’t even know how much something is going to cost until they’ve used it. That’s just a ludicrous way to buy any product. …. Going back seven or eight years to when we started, electricity was pretty much the only thing you couldn’t buy on the internet, and it was inevitable that something was going to happen.”

In the enterprise space, Mike Troiano, Vice President, Industrial IT Solutions, AT&T Mobile & Business Solutions, described a different play in the fast-moving technology space—helping other customers, in their verticals, realize their dreams. AT&T set up foundries in Israel, Silicon Valley, Atlanta and Dallas, where the foundry specifically is focused on Internet of Things solutions. Working from a customer’s problem statement, “We‘ll take the best and brightest engineers from AT&T both of the software and hardware side as well as bring in ecosystem partners…to build prototypes” so customers can test their proof of concept in six to eight weeks to see if there is traction.

The conversation ranged to advice for incumbent utilities. Troiano remarked on the relationship shift that occurs when a tractor shipped across the world can transmit problem information to the maker. That represents not only information on product lifecycle. “Think about how that changes the customer relationship,” he said, “It’s a very different customer experience.”

Dickenson added that taking advantage of big data to create “big insights and big actions” would give customers the power, both electrical and personal, to have control over what to do next to better meet their needs. This is seen through NRG Energy’s weekly emails that differentiate the company from its competitors due to its “retention value of this communication.” She recalled a music festival that the company was a part of in which attendees could rent a portable charger to have connectivity throughout the festival. “It was a great brand moment,” said Dickenson. Her advice was to “look for those moments when you can make a difference” rather than mass communication.

So, too, do Powershop’s customers enjoy a different relationship with their energy retailer. Unlike the routine monthly electricity bill consumers expect to receive from their energy provider, Powershop works to personalize the customer experience while instilling a sense of empowerment and engagement to the consumer.

Powershop’s customers average 64 interactions a year, with mobile users averaging 100, Sargent said. What are they doing? About 20 of those interactions are purchasing. He said the company looked into gamification to increase emotional engagement, but customers already felt it was a game. “I can buy here, I can beat the system.”

Ari Sargent stressed that this opportunity to buy power and to customize the consumer’s relationship with the company leads to the consumer’s increased knowledge on their usage and energy cost. Engaging the consumer is key to developing in today’s rapidly changing technological culture and by allowing them to customize their experience, the customer feels more in control and will continue to enjoy doing business.

“It’s all about the ‘customer journey,’” concluded Dickenson. “It’s about giving power to the people.”

You look at the way electricity is sold: It’s 2015, and customers don’t even know how much they pay for something until they’ve used it. That’s just a ludicrous way to buy any product.

—Ari Sargent Founder and Chief Executive Officer, Powershop

Utilities Transformation: Powering up the Network Integrator

As utilities transform to embrace distributed generation, storage, and other disruptive technologies, the network integrator’s role gains prominence. In this session, panelists discussed that role as additional sources, technologies, and market investments transform the grid. Todd Durocher, Principal, KPMG LLP (U.S.), led the panel.

Isaac Akridge, Vice President, Regulatory Projects, ComEd, described the system integrator’s new role as a referee who not only ensures that all things interconnected and integrated don’t compromise the grid’s safety and security, but also looks for opportunities to drive efficiencies and more customer choices. “Now there are additional sources, including technologies and market interests, that are looking to leverage the grid, and we need to be prepared to address those things,” he said.

Driving the change are customers’ desire for more choices and their ability to access technology on their own, the panelists acknowledged. If utilities do not transform to provide services and choices, another business will take that space, and utilities will become irrelevant.

From the telecom perspective, Jim Kilmer, vice president, Vertical Markets, Automotive/Manufacturing/Transportation/Distribution, Verizon Enterprise Solutions, sees significant parallels. The Apple smartphone changed demand

dramatically, he observed. Also, “We made a serious bet in fiber to the household to compete against some of the cable companies. We had to change our business processes dramatically. We had to become an integrator.”

More and more retailers are coming to the table, Kenneth M. Mercado, senior vice president, Electric Operations, CenterPoint Energy, noted, with products designed to meet consumers’ needs. “That takes it to another level, because you’re discounting the focus on rates and starting to pay much of your attention on sustaining consumers and keeping them for as long as you can in a competitive environment. So the rate impact has to be almost negligible, but the service to the customer has to be magnified.” Their challenge: How to magnify the service, “but not increase their opinion about how much you charge them. Because if you’re charging them more and more over time, they’re going to get angry…and they’re going to find other solutions.”

The role of regulators in network integration is to facilitate removing barriers to the utilities making that transformation, explained Lorraine H. Akiba, commissioner, Hawaii Public Utilities Commission. Some of that involves clarification, as in the case of what a distributed energy resource is and where it fits in a resource plan, cost recovery, and, potentially, in future rate cases. “So we basically said energy storage, which I feel personally is a game changer, is a distributed energy resource and should be treated for those purposes, for resource planning alongside with energy efficiency and demand response.”

When the conversation turned to utilities’ working with third parties, Kilmer advised, “Embrace it. You’re not going to control everything. By the same token, you have the ability to really change the demand environment based on the innovation of some of these partners.”

Collaboration, Akiba observed, presents opportunities. When SolarCity partnered with Hawaiian Electric, “They found out we can get a concentration on our circuits of up to 200 percent of minimum daily load, which was never thought of before. So out of that collaboration can come some pretty specific technical ways to work together as a system integrator.”

Overall, she said, adapt, modify, implement. “I’m very confident that the grid of the future will also be the integrated grid of the future, it will be the smart grid of the future, and customers will also be partners in that effort.” She added, “The commodity is no longer the sale of kilowatt hours. The commodity in the utility of the future will be selling energy management services.”

“The commodity is no longer the sale of kilowatt hours. The commodity and the utility of the future will be selling energy management services.”

—Lorraine H. Akiba Commissioner, Hawaii Public Utilities Commission

Lorraine H. Akiba, Commissioner, Hawaii Public Utilities CommissionJim Kilmer, Vice President – Vertical Markets Automotive/Manufacturing/Transportation/Distribution,

Tax Issues and Opportunities in a Low Commodity Price Environment

“Free cash flow” was the top concern reported by attendees at a discussion on taxes moderated by Tom DeGeorgio, Partner, KPMG (U.S.). This focus on cash came as no surprise for an industry dealing with low profits, increased debts, and declining rig counts. However, DeGeorgio suggested that these issues are also accompanied by tax opportunities, and a panel of experts discussed several ways that a company’s cash position can be improved by developing more effective tax strategies.

Low commodity prices can substantially increase risks in terms of a company’s tax position, noted Cathy Douglas, Senior Vice President, Chief Accounting Officer and Controller, Anadarko Petroleum Corporation. “Transactions that might not have seemed material at a hundred dollars a barrel can now become very material to a company’s financial statement.” She also stressed the importance of the tax department to work closely with other parts of the company such as treasury, investor relations, and planning. Treasury is especially important, she said, because this department can report on current cash requirements, future spending cycles, and how the company expects to raise cash. All of these areas need to be discussed before a transaction occurs so tax positions can be optimized.

Perhaps when you entered into a particular transaction at a hundred dollar oil price the risk that we took as a company may not have seemed terribly significant, yet in today’s world that same potential outcome could be very material to a company.

— Cathy Douglas Senior Vice President, Chief Accounting Officer and Controller, Anadarko Petroleum Corporation

Jeffrey Dodson, Partner, M&A Tax, KPMG (U.S.), discussed different scenarios for tax issues and opportunities. For multinational companies, a key challenge can be to locate cash across different entities worldwide and then to repatriate this cash in an efficient manner. He noted that the United States has no participation exemption, so companies need to rely on foreign tax credits.

Companies in need of cash will look to divestitures, refinancing, or additional rounds of financing, but these strategies should be carefully structured to minimize the tax on gain. He also reviewed issues involving local country taxes. Companies should plan in advance to repatriate cash efficiently by looking at their legal entity structures in terms of tax and how that impacts their business objectives.

Leah Durner, Principal, Washington National Tax, KPMG (U.S.), discussed the importance of tax law at the state level. “Often we assume that state taxes follow federal treatments in financing and passive income, but this is not always the case.” She advised companies to check state laws and rules and review how income in different jurisdictions is broken up. “This is a good time to do a scrub-through of tax returns to see if you’re making the best decisions and getting the most out of your data to support these decisions.” She added that every dollar spent should be reviewed, including credit opportunities for areas like R&D, which are sometimes overlooked or under reported.

Technical track

(L to R) Tom DeGeorgio, Partner, KPMG (U.S.)Cathy Douglas, Senior Vice President, Chief Accounting Officer and Controller, Anadarko Petroleum Corporation

Leah Durner, Principal, Washington National Tax, KPMG (U.S.)Jeffrey Dodson, Partner, M&A Tax, KPMG (U.S.)

complicated by the lack of infrastructure, talent scarcity, an industry still dominated by privately held companies rather than equity investors, and the need to attract foreign investment. “For Mexico, the greatest investment opportunities today are in the midstream,” he said, emphasizing that the country’s growing energy needs will support significant investments in this area.

The key thing to keep in mind is that Mexico and in many state-owned enterprises, the hydrocarbons whether its water, air, minerals, both hard rock, and hydrocarbon, are owned by the state. Unlike here in the United States which has private ownership. So there is still a lot to be done at the local state level. If I was looking at where to put my money, at least initially, I would look at the midstream area.

—Al Zapanta President and Chief Executive Officer, US – Mexico Chamber of Commerce

Emerging Energy Economies: China, Mexico, and Sub-Saharan Africa

Issues and opportunities for high-growth energy markets in China, Nigeria, and Mexico were discussed in detail during a panel discussion moderated by Mark Barnes, Partner in Charge HGM KPMG (U.S.). Key topics included regulatory reform, new energy technologies such as solar, infrastructure development, and opportunities for foreign direct investment.

Recent developments in Africa were summarized by Edward Voelcker, Partner, KPMG (Nigeria). He conceded that serious challenges remain for the region, including regulatory and political reform, underdeveloped infrastructure, and a lack of local engineers, business professionals, and technocrats who can support the needs of large oil and gas production environments. In some countries like Nigeria, he said, petroleum companies have been in operation for three generations, but in Kenya, Tanzania, and Mozambique, oil and gas companies will have to find new talent and experienced personnel to support their initiatives. Nevertheless, current population growth trends and increased geopolitical stability for the region promises enormous opportunities. Referring to the recent election of Muhammadu Buhari as Nigeria’s president, he said, “That’s a good sign for the economy and for the future of democracy in Nigeria.”

Andrew Liu, Chief Financial Officer, Roc Oil Company Limited and Fosum Energy Group, discussed new developments in China. As with other industries in the country, the energy industry is in the middle of a transition from state-owned enterprises to a more mixed economy that includes privately owned companies. Traditional sectors such as petroleum are still dominated by the major national oil companies and offer fewer opportunities for foreign investment. Government regulations and cultural differences between Chinese and Western business groups also create challenges. However, Liu said that smaller companies (and especially those involved with solar and hydro power generation) are more open to working with foreign investors.

Al Zapanta, President and Chief Executive Officer, US – Mexico Chamber of Commerce, delivered an update on the energy industry in Mexico. Discussing regulatory reform, he noted that the government has passed 21 laws affecting issues ranging from the expiration of production licenses to the distribution of refined products and electric power. With only a year and a half left for the current administration, the main challenge is to implement these reforms, a task

(L to R) Andrew Liu, Chief Financial Officer, Roc Oil Company Limited and Fosum Energy GroupEdward Voelcker, Partner, KPMG Nigeria

Al Zapanta, President and Chief Executive Officer, U.S. – Mexico Chamber of Commerce

How are today’s disruptive technologies turning business models on their heads—and what is their impact on the energy industry? This question was the focus of a panel discussion by technology experts from around the world, moderated by Miriam Hernandez-Kakol, Principal, KPMG LLP (U.S.).

Ross Garrity, senior vice president, IT Solutions, Century Link, agreed with other panelists that the technology industry is now at an inflection point where science and imagination are creating a new generation of products and services. He discussed the importance of Big Data and analytics, pointing out their growing importance for petroleum exploration and production. At the same time, he stressed that analytics alone does not give us perfect predictions of the future. “Analytics is important, but it will never be everything to everybody. The key is to take all the capabilities in a business and join everything together.”

Businesses have to become more reactive. In the past you used to have the capability to sit around and see what happens. You’d have the standard adoption curve. I think that adoption curve now changes.

—Dave Wright Chief Strategy Officer, ServiceNow

Mihir Shukla discussed recent advances in robotics, drawing on his experience as chief executive officer and cofounder of Automation Anywhere. Today’s robotics provides businesses with a way to use mobile, social, and cloud technology in new combinations, citing the rapid rise of Uber as a good example. Automation is another, more familiar, use of robotics. From manufacturing to self-driving cars, robotic components are being used to augment and replace lower-skill jobs that previously existed only because of technology limitations. He also explained that even higher-skill jobs such as financial analysis can be automated and performed faster and more effectively with software tools.

Dave Wright, chief strategy officer, ServiceNow, pointed out that disruptive technology is increasing the speed of product development and adoption. “Companies need to be more proactive,” he said. “We no longer have the luxury of waiting to see if a particular technology takes off.” This accelerated business pace is driven partly by user expectations, both internally among employees and externally in retail markets. An application that requires even a few hours of training simply will not be accepted by millennials and younger consumers who have smartphones that are faster, more capable, and easier to use.

(L to R) Dave Wright, Chief Strategy Officer, ServiceNowRoss Garrity, Senior Vice President, IT Solutions, Century Link

What’s on the Horizon? Accounting and Reporting Update

Jeanne Abundis, Partner, KPMG (U.S.), moderated a panel discussion that focused on revenue recognition, recent SEC developments, and other accounting standards and disclosure requirements affecting the energy industry.

Arturis Spencer, Senior Manager, KPMG (U.S.), began the session with an update on the new revenue recognition standard that was released in May 2014 by the FASB and the IASB. In a poll of attendees at the session, most respondents indicated that their companies had not started the transition to the new standard and that they did not expect the standard to significantly change their contracting policies, business systems, or business processes. However, Spencer argued that companies should consider a number of complex issues recently highlighted by the FASB/IASB Joint Transition Resource Group, including growth versus net accounting and the identification of performance obligations. “As you go through the steps of the model,” he said, “you’ll find that there are nuances that can lead to unforeseen consequences.”

Continuing the FASB discussion, Christopher O. Champion, Partner, KPMG (U.S.), reviewed recent comments by the AICPA Task Force involved with the new FASB standard in relation to upstream oil and gas revenues. He also commented on the FASB consolidation standard and master limited partnerships and whether general partners have a significant variable interest. He concluded that the consolidation standard will not change current practice. “We will likely still consolidate these entities, but the way we document will be different.”

“There’s just some nuances in there (in the regulation) that we’ll just have to work our way through.”

—Darin Kempke Partner, KPMG (U.S.)

Representing the power and utility side of the industry, Darren Kempke, Partner, KPMG (U.S.), agreed with Champion that the new standard should not be used to make significant changes in revenue recognition. In the case of customer contracts, he said that the AICPA is questioning whether to use an average number for upstream revenues. He argued that the “as delivered” model would be the preferred approach. He also suggested that with “blend and extend” contracts, an extension should be considered as a new contract. All of these issues will require further study and discussion, he said. “The standard has a lot of nuances that we’ll just have to work our way through.”

Melanie Dolan, Partner, KPMG (U.S.), talked about recent activities at the SEC, many of which involve implementing requirements of the Dodd-Frank Act. In the area of executive pay, discussions have involved the disclosure of “compensation paid,” the ratio of compensation to company performance, and the fair value of equity rewards when these rewards are divested. She also discussed other issues addressed by the SEC such as crowd funding and capital raising opportunities, audit committee disclosures, and disclosure effectiveness.

Can you envision a world where your supply chain is based only on the raw materials to create the equipment and you’ve got a 3D printer to manufacture all the equipment and spare parts that you need on a real time basis?

—Regina Mayor U.S. Energy & Natural Resources Advisory leader, KPMG (U.S.).

We’re seeing a lot of these technologies starting to converge to do pretty remarkable things.

— John Kunasek U.S. sector leader for Energy & Natural Resources, KPMG (U.S.)