44

Office Market Dashboards 2009 Colliers International | Greater Toronto Area Q2 | SECOND QUARTER

| Date post: | 14-Mar-2016 |

| Category: |

Documents |

| Upload: | chris-fyvie |

| View: | 218 times |

| Download: | 1 times |

Office Market Dashboards

2009Colliers International | Greater Toronto Area Q2 | SECOND QUARTER

Table Of Contents

1 GTA Regional

2 GTA Central 3 Downtown 4 Financial Core 5 Downtown East6 Downtown West7 Downtown South8 Downtown North

9 GTA Midtown10 Yonge & St. Clair11 Airport West12 Airport East13 Airport Corporate Centre14 Sheridan

15 GTA North16 North Yonge Corridor17 Dufferin-Finch18 Yorkdale19 Vaughan20 Richmond Hill21 Yonge & Eglinton22 Yonge & Bloor

23 GTA West24 Oakville25 Mississauga City Centre26 Meadowvale27 Hurontario & Highway 40128 Cooksville29 Burlington30 Brampton31 Highway 427 & Bloor-Islington

32 GTA East33 Woodbine-Steeles34 Toronto East35 Pickering-Oshawa36 Markham37 Highway 404 & 40738 Duncan Mill39 Don Mills & Eglington40 Consumers Road41 Scarborough Town Centre

Greater Toronto AreaOffice Market Dashboard

REGIONAL INDICATORS MAP OF REGION

Q1 2009 Q2 2009 Trend

Office Inventory* 180,142,712 180,664,489

Net Absorption (432,214) 657,589

Vacancy Rate 5.5% 5.7%

Average Asking Net Rent $17.66 $17.58

Average Additional Rent $15.86 $15.94

AVAILABLE SPACE OPTIONS

AVAILABLE SUPPLY SPLIT

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 1626 664 406 333 53 24

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

505 16,985 Cadillac Fairview

600 16,630 The Last Minute Club

301 15,00090 Eglinton Ave

Holdings

GROSS RENT & AVAILABILITY BY BUILDING CLASS Date Address Price Vendor Purchaser Size $/PSF

6/18/2009 415 Yonge Street $32,100,000 Anthem

Properties

Crown Realty

Partners 191,880 $172.00

100 Wellington Street W

150 Ferrand Drive

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 2045 office buildings surveyed in the GTA office region.

Q2-09

Number of units on the regional market by size brackets

Tenant

TOP Office Sale Transactions by Price

Office Region Dashboard: Greater Toronto Area

90 Eglinton Avenue E ThinData Inc.

TOP Office Lease Transactions by Size

Address

N/A

N/A

Available Direct80%

Available Sublease20%

Total Available Office Space: 15285487 sf

80,000,000 $70

Avail. Office Space Not Avail. Office Space Gross Rent

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

ua

re F

ee

t

Sublease Direct Sublease as % of Total Available

6/18/2009 415 Yonge Street $32,100,000 Properties Partners

191,880 $172.00

5/27/20096700 Century

Avenue$7,000,000

A Private

Individual Sanyo Co. 56,607 $124.00

6/15/200921 Randolph

Avenue$5,765,000

Don Valley

Storage Inc Canadian Red Cross 59,000 $98.00

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

155 Wellington

Street West1,223,891 Q2 2009

333 Bay Street 1,127,986 Q3 2009

25 York Street 780,000 Q3 2009

REGIONAL CHARACTERISTICS

Source: Colliers International, Q2 2009

RBC Dexia, Fairmont

Menkes

Brookfield Properties

Developer Anchor Tenant

Telus, Kinross,

Cadillac Fairview

KPMG, Goodmans,

Available Direct80%

Available Sublease20%

Total Available Office Space: 15285487 sf

$63.22

$34.55

$29.27

$23.43

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class AAA Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$17.58

5.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

(5)

(3)

(1)

1

3

5

7

9

11

13

15

17

19

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (100,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

17%

Data,Publishing, Broadcasting Services 11%

Finance 27%

Professional Services 22%

Public Service & Private Sector

Services20%

Others3%

* The GTA is Canada's largest urban economic region in terms of size in population, economy andoffice space.* Built on strong foundations that include world-renowned educational and health institutions, adiversity of internationally competitive sectors and clusters, and a highly-skilled, well-educated andgrowing population.* GTA includes the City of Toronto plus & surrounding regional municipalities, which are comprised of25 local municipalities of which 11 have populations greater than 100,000 (as of 2008).* Over time Toronto has maintained its position as Canada's financial and industrial center.* Economic strength and dominance of the area is reflected in its concentration of corporateheadquarters.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

ua

re F

ee

t

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we

Available Direct80%

Available Sublease20%

Total Available Office Space: 15285487 sf

$63.22

$34.55

$29.27

$23.43

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class AAA Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$17.58

5.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

(5)

(3)

(1)

1

3

5

7

9

11

13

15

17

19

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (100,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

17%

Data,Publishing, Broadcasting Services 11%

Finance 27%

Professional Services 22%

Public Service & Private Sector

Services20%

Others3%

* The GTA is Canada's largest urban economic region in terms of size in population, economy andoffice space.* Built on strong foundations that include world-renowned educational and health institutions, adiversity of internationally competitive sectors and clusters, and a highly-skilled, well-educated andgrowing population.* GTA includes the City of Toronto plus & surrounding regional municipalities, which are comprised of25 local municipalities of which 11 have populations greater than 100,000 (as of 2008).* Over time Toronto has maintained its position as Canada's financial and industrial center.* Economic strength and dominance of the area is reflected in its concentration of corporateheadquarters.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

ua

re F

ee

t

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

MARKET INDICATORS MAP OF MARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 84,971,884 84,997,879

Net Absorption 196,322 85,909

Vacancy Rate 4.6% 4.7%

Average Asking Net Rent $22.99 $22.49

Average Additional Rent $21.40 $21.17

AVAILABLE SUPPLY SPLIT AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 717 317 144 127 0 1

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord Tenant

505 16,985 Cadillac Fairview

301 15,000 90 Eglinton Ave

Holdings

500 13,091 N/A

GROSS RENT & AVAILABILITY BY BUILDING CLASS

Date Address Price Vendor Purchaser Size $/PSF

6/18/2009415 Yonge

$32,100,000 Anthem

Crown Realty Partners 191,880 $172

Q2-09

Number of units on the market by size brackets

ThinData Inc.

N/A 100 Wellington Street W

90 Eglinton Avenue E

TOP Office Sale Transactions by Price

Office Market Dashboard: GTA Central

85 Richmond Street W N/A

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 724 office buildings surveyed in this market.

TOP Office Lease Transactions by Size

Address

35,000,000

40,000,000

$60

$70

Avail. Office Space Not Avail. Office Space Gross Rent

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

6/18/2009415 Yonge

Street$32,100,000

Anthem

Properties Crown Realty Partners 191,880 $172

6/15/200921 Randolph

Avenue$5,765,000

Don Valley

Storage Inc Canadian Red Cross 59,000 $98

5/6/2009860 - 862

Richmond St W$4,356,000

City of

Toronto Allied Properties REIT 27,317 $159

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.155 Wellington

Street West1,223,891 Q2 2009

333 Bay Street 1,127,986 Q3 2009

25 York Street 780,000 Q3 2009

MARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

RBC Dexia, Fairmont

Menkes

Brookfield Properties

Anchor TenantDeveloper

Telus, Kinross,

Cadillac Fairview

KPMG, Goodmans,

$63.22

$36.54

$28.66

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$22.49

4.7%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

(3)

(1)

1

3

5

7

9

11

13

15

17

19

21

23

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (100,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

7%

Data,Publishing, Broadcasting Services 11%

Finance 33%

Professional Services 25%

Public Service & Private Sector

Services21%

Others3%

* Largest office market in the GTA with the lowest vacancy rate* GTA top annual rental rates of $70.39 are asked for at the Royal Bank Plaza* Market is in high demand by users looking for a prestige urban location and modern, state-of-the-art architecture* Limited parking, but great access to public transit and the PATH system, Toronto's underground walkway* Proximity to multiple amenities and services add convenience for employees and customers* Vacancy rates are fairly stable at a low value as this market is in high demand by companies looking to locate in this well located office market* Abundance of amenities are in walking distance in all three submarkets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

$63.22

$36.54

$28.66

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$22.49

4.7%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

(3)

(1)

1

3

5

7

9

11

13

15

17

19

21

23

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (100,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

7%

Data,Publishing, Broadcasting Services 11%

Finance 33%

Professional Services 25%

Public Service & Private Sector

Services21%

Others3%

* Largest office market in the GTA with the lowest vacancy rate* GTA top annual rental rates of $70.39 are asked for at the Royal Bank Plaza* Market is in high demand by users looking for a prestige urban location and modern, state-of-the-art architecture* Limited parking, but great access to public transit and the PATH system, Toronto's underground walkway* Proximity to multiple amenities and services add convenience for employees and customers* Vacancy rates are fairly stable at a low value as this market is in high demand by companies looking to locate in this well located office market* Abundance of amenities are in walking distance in all three submarkets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

MARKET INDICATORS MAP OF MARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 67,957,121 67,983,116

Net Absorption 86,529 (49,185)

Vacancy Rate 4.2% 4.4%

Average Asking Net Rent $24.83 $24.26

Average Additional Rent $22.30 $22.02

AVAILABLE SUPPLY SPLIT

AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 506 255 101 119 0 1

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

505 16,985 Cadillac Fairview

GROSS RENT & AVAILABILITY BY BUILDING CLASS 500 13,091 N/A

1000 11,908 N/A

Q2-09

Number of units on the market by size brackets

Tenant

Office Market Dashboard: Downtown

401 Bay Street N/A

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 559 office buildings surveyed in this market.

TOP Office Lease Transactions by Size

Address

N/A

N/A100 Wellington Street W

85 Richmond Street W

30,000,000 $70

Avail. Office Space Not Avail. Office Space Gross Rent

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

1000 11,908 N/A

Date Address Price Vendor Purchaser Size $/PSF

6/18/2009 415 Yonge Street $32,100,000 Anthem

Properties

Crown Realty

Partners 191,880 $172

6/15/200921 Randolph

Avenue$5,765,000

Don Valley

Storage Inc

Canadian Red

Cross 59,000 $98

5/6/2009860 - 862

Richmond St W$4,356,000 City of Toronto

Allied Properties

REIT 27,317 $159

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.155 Wellington

Street West1,223,891 Q2 2009

333 Bay Street 1,127,986 Q3 2009

25 York Street 780,000 Q3 2009

MARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

KPMG, Goodmans,

RBC Dexia, Fairmont

Menkes

Brookfield Properties

Developer Anchor Tenant

Telus, Kinross,

401 Bay Street N/A

TOP Office Sale Transactions by Price

Cadillac Fairview

$63.22 $45.54

$37.78

$28.20

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class AAA Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$24.26

4.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

(3)

1

5

9

13

17

21

25

29

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (100,000's)

Absorption Asking Net Rent Vacancy Rate Manufacturing & Distribution

6%

Data,Publishing, Broadcasting Services 12%

Finance 34% Professional

Services 24%

Public Service & Private Sector

Services21%

Others3%

* Largest office market in the GTA with the lowest vacancy rate* GTA top annual rental rates are achieved in buildings located in this market* Market is in high demand by users looking for a prestige urban location and modern, state-of-the-artarchitecture* Limited parking, but great access to public transit and the PATH system, Toronto's undergroundwalkway* Proximity to multiple amenities and services add convenience for employees and customers

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we

$63.22 $45.54

$37.78

$28.20

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class AAA Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$24.26

4.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

(3)

1

5

9

13

17

21

25

29

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (100,000's)

Absorption Asking Net Rent Vacancy Rate Manufacturing & Distribution

6%

Data,Publishing, Broadcasting Services 12%

Finance 34% Professional

Services 24%

Public Service & Private Sector

Services21%

Others3%

* Largest office market in the GTA with the lowest vacancy rate* GTA top annual rental rates are achieved in buildings located in this market* Market is in high demand by users looking for a prestige urban location and modern, state-of-the-artarchitecture* Limited parking, but great access to public transit and the PATH system, Toronto's undergroundwalkway* Proximity to multiple amenities and services add convenience for employees and customers

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

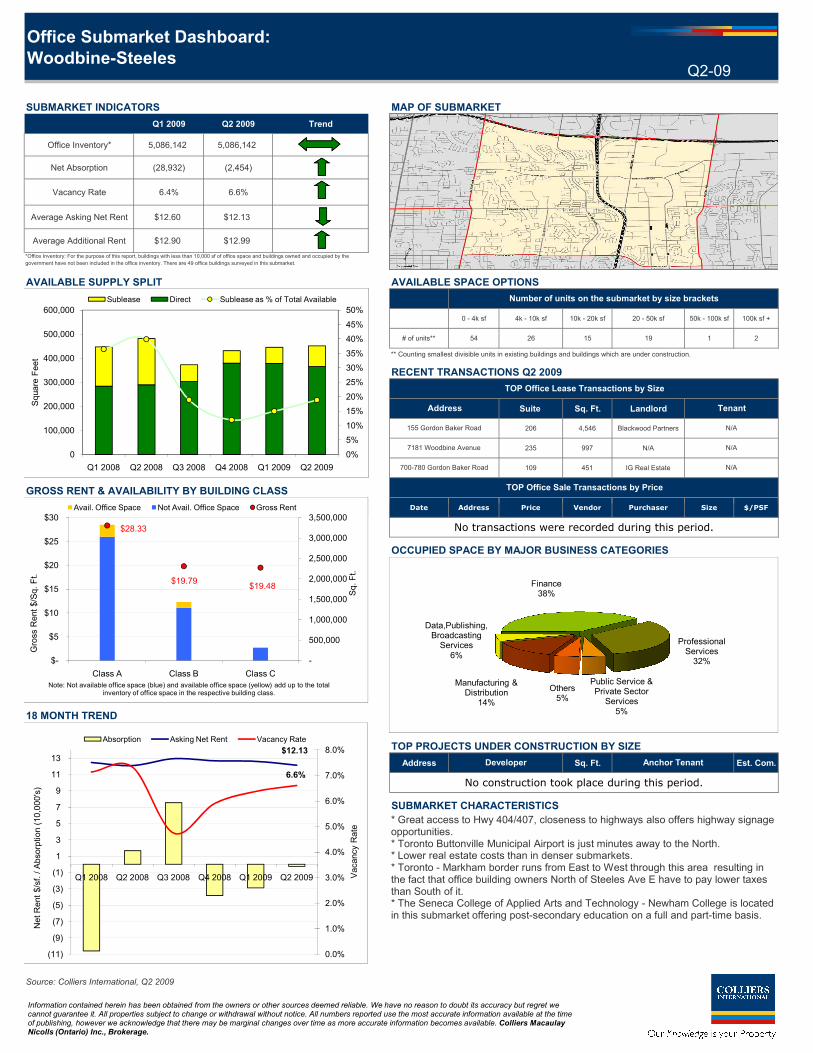

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend AVAILABLE SPACE OPTIONS

Office Inventory* 30,410,745 30,411,232

Net Absorption (11,549) (55,215)

Vacancy Rate 3.4% 3.5%

Average Asking Net Rent $27.82 $27.66 0 - 4k sf

Average Additional Rent $27.29 $27.31 4k - 10k sf

10k - 20k sf

AVAILABLE SUPPLY SPLIT 20 - 50k sf

50k - 100k sf

100k sf +

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

505 16,985 Cadillac Fairview

Corporation

500 13,091 N/A

1000 11,908 N/A

Date Address Price Vendor Purchaser Size $/PSF

** Counting smallest divisible units in existing

buildings and buildings under construction.

TenantAddress

N/A

N/A

No transactions took place during this period.

0

TOP Office Sale Transactions by Price

N/A

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 105 office buildings surveyed in this submarket. 70

128

Number of units

on the

submarket by

size brackets

100 Wellington Street W

85 Richmond Street W

Office Submarket Dashboard: Financial Core

401 Bay Street

# of units**

TOP Office Lease Transactions by Size

85

Q2-09

0

166

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

GROSS RENT & AVAILABILITY BY BUILDING CLASS OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

155 Wellington

Street West1,223,891 Q2 2009

333 Bay Street 1,127,986 Q3 2009

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

Developer Anchor Tenant

No transactions took place during this period.

Cadillac Fairview

KPMG, Goodmans,

RBC Dexia, Fairmont

Brookfield Properties

$63.22

$55.51

$44.94

$35.92

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class AAA Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$27.66

3.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

(20)

(16)

(12)

(8)

(4)

-

4

8

12

16

20

24

28

32

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

5%

Data,Publishing, Broadcasting Services

5%

Finance 47%

Professional Services 25%

Public Service & Private Sector

Services16%

Others2%

* Most dense office submarket in the GTA with one of the lowest vacancy rates* GTA top annual rental rates are achieved in buildings located in this market* Majority of tenants occupy 4,000 sf or less* Prestige urban location and modern, state-of-the-art architecture* Limited parking, but great access to public transit and the PATH system, Toronto's underground walkway* Proximity to multiple amenities and services add convenience for employees and customers

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we

$63.22

$55.51

$44.94

$35.92

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

$-

$10

$20

$30

$40

$50

$60

$70

Class AAA Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$27.66

3.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

(20)

(16)

(12)

(8)

(4)

-

4

8

12

16

20

24

28

32

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

5%

Data,Publishing, Broadcasting Services

5%

Finance 47%

Professional Services 25%

Public Service & Private Sector

Services16%

Others2%

* Most dense office submarket in the GTA with one of the lowest vacancy rates* GTA top annual rental rates are achieved in buildings located in this market* Majority of tenants occupy 4,000 sf or less* Prestige urban location and modern, state-of-the-art architecture* Limited parking, but great access to public transit and the PATH system, Toronto's underground walkway* Proximity to multiple amenities and services add convenience for employees and customers

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 4,512,403 4,527,403

Net Absorption 31,082 23,683

Vacancy Rate 3.7% 3.8%

Average Asking Net Rent $15.83 $17.27

Average Additional Rent $4.71 $7.90

AVAILABLE SUPPLY SPLIT

AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 69 26 4 14 0 1

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

GROSS RENT & AVAILABILITY BY BUILDING CLASS 200 9,174 Alliance Entertainment

300 3,245 Tippin Capital

200 2,555 Tippin Capital

145 King Street E

N/A

Office Submarket Dashboard: Downtown East

105-109 King Street E

Q2-09

Address

N/A

N/A

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 107 office buildings surveyed in this submarket.

105-109 King Street E

Number of units on the submarket by size brackets

TOP Office Sale Transactions by Price

TOP Office Lease Transactions by Size

Tenant

$32.50

$32.62

2,500,000

3,000,000

$30

$35

Avail. Office Space Not Avail. Office Space Gross Rent

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Date Address Price Vendor Purchaser Size $/PSF

4/14/200971 Front Street

East$4,940,000

Front

Esplanade

Holdings

Pajelle Investments

Ltd. N/A N/A

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

125 Queen's

Quay East550,000 Q1 2010

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

TEDCO, Corus

Developer Anchor Tenant

Aecon

TOP Office Sale Transactions by Price$32.50

$32.62

$1.84

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

$-

$5

$10

$15

$20

$25

$30

$35

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$17.27

3.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

(2)

-

2

4

6

8

10

12

14

16

18

20

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

9%

Data,Publishing, Broadcasting Services 38%

Finance 7%

Professional Services 22%

Public Service & Private Sector

Services14%

Others10%

* Includes original 10 blocks of Toronto and historic buildings allow for remarkable office space features (Brick&Beam)* Northern part of submarket well connected to downtown & rest of the GTA through public transportation and Gardiner Expressway & Don Valley Parkway* With new residential high-rise developments (e.g. Corktown, Distillery District), the labour pool will increase, expand and diversify* George Brown College's third main Toronto campus will support growth of up to 4,000 new students per year and energize the new East Bay lakefront development by Fall 2011

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

$32.50

$32.62

$1.84

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

$-

$5

$10

$15

$20

$25

$30

$35

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$17.27

3.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

(2)

-

2

4

6

8

10

12

14

16

18

20

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

9%

Data,Publishing, Broadcasting Services 38%

Finance 7%

Professional Services 22%

Public Service & Private Sector

Services14%

Others10%

* Includes original 10 blocks of Toronto and historic buildings allow for remarkable office space features (Brick&Beam)* Northern part of submarket well connected to downtown & rest of the GTA through public transportation and Gardiner Expressway & Don Valley Parkway* With new residential high-rise developments (e.g. Corktown, Distillery District), the labour pool will increase, expand and diversify* George Brown College's third main Toronto campus will support growth of up to 4,000 new students per year and energize the new East Bay lakefront development by Fall 2011

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend

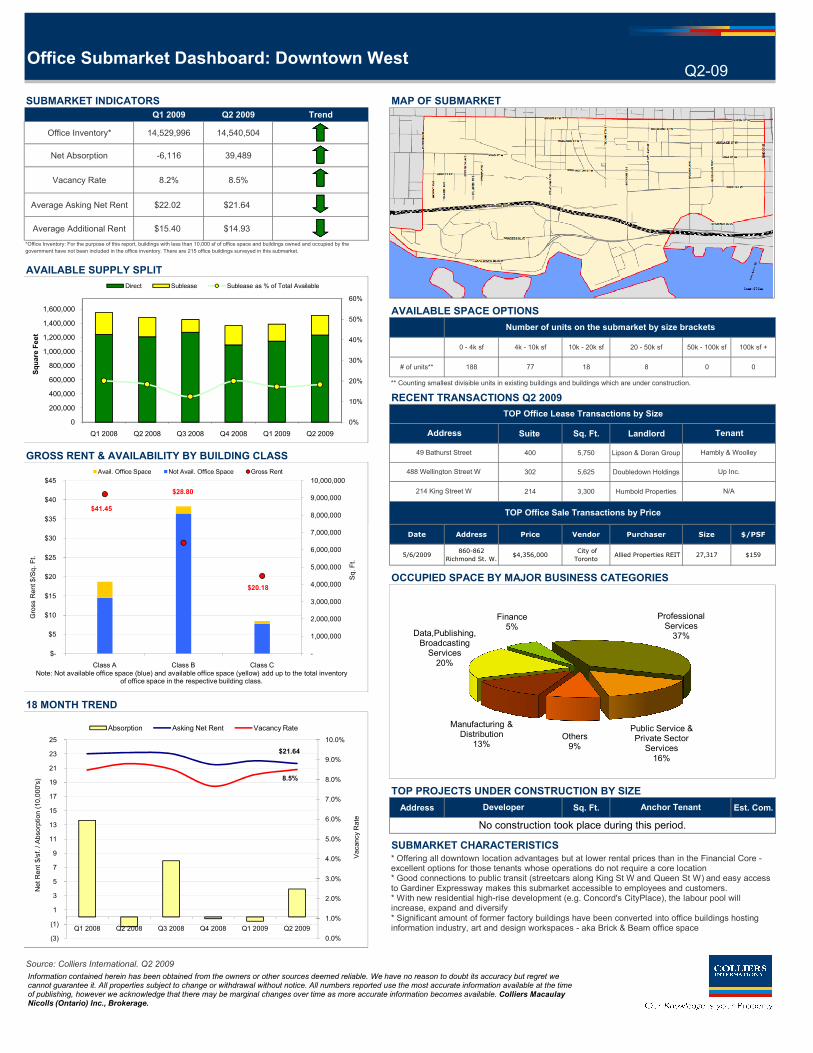

Office Inventory* 14,529,996 14,540,504

Net Absorption -6,116 39,489

Vacancy Rate 8.2% 8.5%

Average Asking Net Rent $22.02 $21.64

Average Additional Rent $15.40 $14.93

AVAILABLE SUPPLY SPLIT

AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 188 77 18 8 0 0

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

GROSS RENT & AVAILABILITY BY BUILDING CLASS 400 5,750 Lipson & Doran Group

302 5,625 Doubledown Holdings

214 3,300 Humbold Properties

Number of units on the submarket by size brackets

Tenant

TOP Office Lease Transactions by Size

Address

Up Inc.

Hambly & Woolley49 Bathurst Street

Office Submarket Dashboard: Downtown West

214 King Street W N/A

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 215 office buildings surveyed in this submarket.

Q2-09

488 Wellington Street W

$41.45

$28.80

8,000,000

9,000,000

10,000,000

$35

$40

$45

Avail. Office Space Not Avail. Office Space Gross Rent

0%

10%

20%

30%

40%

50%

60%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Date Address Price Vendor Purchaser Size $/PSF

5/6/2009860-862

Richmond St. W.$4,356,000

City of

Toronto Allied Properties REIT 27,317 $159

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

No construction took place during this period.

Developer Anchor Tenant

TOP Office Sale Transactions by Price$41.45

$28.80

$20.18

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$21.64

8.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

(3)

(1)

1

3

5

7

9

11

13

15

17

19

21

23

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate Manufacturing & Distribution

13%

Data,Publishing, Broadcasting Services 20%

Finance 5%

Professional Services 37%

Public Service & Private Sector

Services16%

Others9%

* Offering all downtown location advantages but at lower rental prices than in the Financial Core -excellent options for those tenants whose operations do not require a core location* Good connections to public transit (streetcars along King St W and Queen St W) and easy access to Gardiner Expressway makes this submarket accessible to employees and customers.* With new residential high-rise development (e.g. Concord's CityPlace), the labour pool will increase, expand and diversify* Significant amount of former factory buildings have been converted into office buildings hosting information industry, art and design workspaces - aka Brick & Beam office space

0%

10%

20%

30%

40%

50%

60%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

$41.45

$28.80

$20.18

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$21.64

8.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

(3)

(1)

1

3

5

7

9

11

13

15

17

19

21

23

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate Manufacturing & Distribution

13%

Data,Publishing, Broadcasting Services 20%

Finance 5%

Professional Services 37%

Public Service & Private Sector

Services16%

Others9%

* Offering all downtown location advantages but at lower rental prices than in the Financial Core -excellent options for those tenants whose operations do not require a core location* Good connections to public transit (streetcars along King St W and Queen St W) and easy access to Gardiner Expressway makes this submarket accessible to employees and customers.* With new residential high-rise development (e.g. Concord's CityPlace), the labour pool will increase, expand and diversify* Significant amount of former factory buildings have been converted into office buildings hosting information industry, art and design workspaces - aka Brick & Beam office space

0%

10%

20%

30%

40%

50%

60%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 2,453,525 2,453,525

Net Absorption (2,065) (11,467)

Vacancy Rate 2.9% 3.2%

Average Asking Net Rent $22.06 $22.28

Average Additional Rent $17.94 $17.99

AVAILABLE SUPPLY SPLIT

AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 12 9 5 27 0 0

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

GROSS RENT & AVAILABILITY BY BUILDING CLASS Date Address Price Vendor Purchaser Size $/PSF

Address

No transactions were recorded during this period.

Number of units on the submarket by size brackets

Office Submarket Dashboard: Downtown South

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 15 office buildings surveyed in this submarket.

TOP Office Lease Transactions by Size

Tenant

TOP Office Sale Transactions by Price

Q2-09

0%

10%

20%

30%

40%

50%

60%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

ua

re F

ee

t

Direct Sublease Sublease as % of Total Available

GROSS RENT & AVAILABILITY BY BUILDING CLASS Date Address Price Vendor Purchaser Size $/PSF

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

25 York Street 780,000 Q3 2009

18 York Street 650,000 Q1 2011

15 York Street 207,000 Q1 2010

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

N/A TBD

Menkes

PricewaterhouseCoopers

Cadillac Fairview

Great West Life

No transactions were recorded during this period.

Developer

Telus, Kinross,

Anchor Tenant

$49.38

$31.88

$-

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

$-

$10

$20

$30

$40

$50

$60

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$22.28

3.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

(3)

(1)

1

3

5

7

9

11

13

15

17

19

21

23

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

19%

Data,Publishing, Broadcasting Services 32% Finance

13%

Professional Services 23%Public Service &

Private Sector Services10%

Others3%

* Offering many downtown location advantages but at lower rental prices than in the Financial Core along the city's waters' edge* Good connections to public transit and easy access to Gardiner Expressway & DVP makes this submarket accessible to employees and customers.* Submarket is part of the Waterfront Revitalization project will continue to change the area into a more urban community in the years to come* With new residential high-rise development (e.g. Pier 27/Quay West), the labour pool will increase, expand and diversify

0%

10%

20%

30%

40%

50%

60%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

ua

re F

ee

t

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay

$49.38

$31.88

$-

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

$-

$10

$20

$30

$40

$50

$60

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$22.28

3.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

(3)

(1)

1

3

5

7

9

11

13

15

17

19

21

23

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

19%

Data,Publishing, Broadcasting Services 32% Finance

13%

Professional Services 23%Public Service &

Private Sector Services10%

Others3%

* Offering many downtown location advantages but at lower rental prices than in the Financial Core along the city's waters' edge* Good connections to public transit and easy access to Gardiner Expressway & DVP makes this submarket accessible to employees and customers.* Submarket is part of the Waterfront Revitalization project will continue to change the area into a more urban community in the years to come* With new residential high-rise development (e.g. Pier 27/Quay West), the labour pool will increase, expand and diversify

0%

10%

20%

30%

40%

50%

60%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

ua

re F

ee

t

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 14,740,192 14,740,192

Net Absorption 105,869 (43,109)

Vacancy Rate 1.8% 2.4%

Average Asking Net Rent $18.14 $18.71

Average Additional Rent $18.49 $20.34

AVAILABLE SUPPLY SPLIT

AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 70 19 8 9 0 0

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

400 9,223 Milcan Enterprises

GROSS RENT & AVAILABILITY BY BUILDING CLASS 1422 626 Northam Realty

Q2-09Office Submarket Dashboard: Downtown North

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 73 office buildings surveyed in this submarket.

TOP Office Lease Transactions by Size

Number of units on the submarket by size brackets

229 Yonge Street

2 Carlton Street

TenantAddress

St Michael's Hospital

N/A

0%

10%

20%

30%

40%

50%

60%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

GROSS RENT & AVAILABILITY BY BUILDING CLASS

Date Address Price Vendor Purchaser Size $/PSF

6/18/2009415 Yonge

Street$32,100,000

Anthem

Properties Crown Realty 191,880 $172

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

TOP Office Sale Transactions by Price

No Construction took place during this period

Developer Anchor Tenant

$42.87 $36.55

$33.66

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$18.71

2.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

(5)

-

5

10

15

20

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

1%

Data,Publishing, Broadcasting Services

2%

Finance 17%

Professional Services

9%

Public Service & Private Sector

Services69%

Others2%

* Offering all downtown location advantages but at lower rental prices than in the Financial Core* Great connections to public transit and road system makes this submarket accessible toemployees and clients/customers.* Great proximity to an educated and productive labour force* With new residential high-rise development, residential development will increase and expand anddiversify labour pool* Incorporates Toronto Discovery District a 2.5 square km research park with a highly concentratedmix of research, bio-medical companies, finance and business support services

0%

10%

20%

30%

40%

50%

60%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we

$42.87 $36.55

$33.66

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$18.71

2.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

(5)

-

5

10

15

20

25

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

1%

Data,Publishing, Broadcasting Services

2%

Finance 17%

Professional Services

9%

Public Service & Private Sector

Services69%

Others2%

* Offering all downtown location advantages but at lower rental prices than in the Financial Core* Great connections to public transit and road system makes this submarket accessible toemployees and clients/customers.* Great proximity to an educated and productive labour force* With new residential high-rise development, residential development will increase and expand anddiversify labour pool* Incorporates Toronto Discovery District a 2.5 square km research park with a highly concentratedmix of research, bio-medical companies, finance and business support services

0%

10%

20%

30%

40%

50%

60%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Direct Sublease Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

MARKET INDICATORS MAP OF MARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 17,014,763 17,014,763 AVAILABLE SPACE OPTIONS

Net Absorption 109,794 135,095

Vacancy Rate 6.1% 5.5%

Average Asking Net Rent $16.45 $16.40 0 - 4k sf

Average Additional Rent $18.17 $18.25 4k - 10k sf

10k - 20k sf

AVAILABLE SUPPLY SPLIT20 - 50k sf

50k - 100k sf

100k sf +

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

301 15,000 Madison Group

1100 4,588 Manulife Financial

2601 3,141 Oxford Properties

GROSS RENT & AVAILABILITY BY BUILDING CLASS

62

211

** Counting smallest divisible units in existing

buildings and buildings under construction.

0

0

8

43

45 St Clair Avenue W

Tenant

TOP Office Sale Transactions by Price

N/A

ThinData Inc.90 Eglinton Avenue E

Q2-09Office Market Dashboard: GTA Midtown

2 Bloor Street W N/A

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 165 office buildings surveyed in this market.

TOP Office Lease Transactions by Size

Address

Number of units

on the market by

size brackets

# of units**

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

GROSS RENT & AVAILABILITY BY BUILDING CLASS

Date Address Price Vendor Purchaser Size $/PSF

4/15/2009327 Eglinton

Avenue East$1,200,000

A Private

Individual

The Cosmetic Surgery

Institute 2,329 $515

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

MARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

Anchor TenantDeveloper

No construction occurred during this period

$38.70

$33.73

$29.42

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$16.40

5.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

(11)

(7)

(3)

1

5

9

13

17

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

9%

Data,Publishing, Broadcasting Services 14%

Finance 23% Professional

Services 24%

Public Service & Private Sector

Services28%

Others2%

* Well established office market in a continuously densifying urban area consitsting of three office submarkets: Yonge-Bloor, Yonge-St.Clair and Yonge-Eglinton* Lower real estate costs than in Downtown Toronto* Vacancy rates are fairly stable at a low value as this market is in high demand by companies looking to locate in this well located office market* Great access to public transit and highly educated labour force* Abundance of amenities are in walking distance in all three submarkets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay

$38.70

$33.73

$29.42

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$16.40

5.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

(11)

(7)

(3)

1

5

9

13

17

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

9%

Data,Publishing, Broadcasting Services 14%

Finance 23% Professional

Services 24%

Public Service & Private Sector

Services28%

Others2%

* Well established office market in a continuously densifying urban area consitsting of three office submarkets: Yonge-Bloor, Yonge-St.Clair and Yonge-Eglinton* Lower real estate costs than in Downtown Toronto* Vacancy rates are fairly stable at a low value as this market is in high demand by companies looking to locate in this well located office market* Great access to public transit and highly educated labour force* Abundance of amenities are in walking distance in all three submarkets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 2,851,688 2,851,688

Net Absorption 21,583 20,397

Vacancy Rate 1.6% 1.4%

Average Asking Net Rent $15.96 $16.83

Average Additional Rent $18.57 $18.67

AVAILABLE SUPPLY SPLIT

AVAILABLE SPACE OPTIONS

0 - 4k sf 4k - 10k sf 10k - 20k sf 20 - 50k sf 50k - 100k sf 100k sf +

# of units** 33 10 2 2 0 0

** Counting smallest divisible units in existing buildings and buildings which are under construction.

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord Tenant

1100 2,879 Manulife Financial

GROSS RENT & AVAILABILITY BY BUILDING CLASS

Date Address Price Vendor Purchaser Size $/PSF

Address

TOP Office Sale Transactions by Price

No transactions took place during this period.

Q2-09

Number of units on the submarket by size brackets

N/A45 St. Clair Avenue W

Office Submarket Dashboard: Yonge & St. Clair

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 37 office buildings surveyed in this submarket.

TOP Office Lease Transactions by Size

1,800,000

2,000,000

$40

$45

Avail. Office Space Not Avail. Office Space Gross Rent

-5%

5%

15%

25%

35%

45%

55%

65%

75%

0

50,000

100,000

150,000

200,000

250,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

No transactions took place during this period.

Developer Anchor Tenant

No construction took place during this period.

$39.87 $33.67

$31.79

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$16.83

1.4%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

(1)

1

3

5

7

9

11

13

15

17

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

10%

Data,Publishing, Broadcasting Services

8%

Finance 15%

Professional Services 24%

Public Service & Private Sector

Services41%

Others2%

* Smallest office submarket of the Midtown office market* Due to small total inventory submarket usually doesn’t have many space options available* Vacancy Rate remains below the 9% threshold and Rental costs are fairly stable due to this fact* Great access to public transit and proximity to local labour force* Most buildings in this submarket have been built between 1960-1990 with some of them being renovated in the 1990s

-5%

5%

15%

25%

35%

45%

55%

65%

75%

0

50,000

100,000

150,000

200,000

250,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we

$39.87 $33.67

$31.79

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Avail. Office Space Not Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$16.83

1.4%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

(1)

1

3

5

7

9

11

13

15

17

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Vacancy Rate

Net Rent $/sf. / Absorption (10,000's)

Absorption Asking Net Rent Vacancy Rate

Manufacturing & Distribution

10%

Data,Publishing, Broadcasting Services

8%

Finance 15%

Professional Services 24%

Public Service & Private Sector

Services41%

Others2%

* Smallest office submarket of the Midtown office market* Due to small total inventory submarket usually doesn’t have many space options available* Vacancy Rate remains below the 9% threshold and Rental costs are fairly stable due to this fact* Great access to public transit and proximity to local labour force* Most buildings in this submarket have been built between 1960-1990 with some of them being renovated in the 1990s

-5%

5%

15%

25%

35%

45%

55%

65%

75%

0

50,000

100,000

150,000

200,000

250,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Sq

uare

Feet

Sublease Direct Sublease as % of Total Available

Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

SUBMARKET INDICATORS MAP OF SUBMARKET

Q1 2009 Q2 2009 Trend

Office Inventory* 4,108,253 4,456,253

Net Absorption (21,457) 315,860

Vacancy Rate 3.7% 4.6%

Average Asking Net Rent $14.40 $14.68 0 - 4k sf

Average Additional Rent $10.59 $10.29 4k - 10k sf

10k - 20k sf

AVAILABLE SUPPLY SPLIT 20 - 50k sf

50k - 100k sf

100k sf +

RECENT TRANSACTIONS Q2 2009

Suite Sq. Ft. Landlord

Date Address Price Vendor Purchaser Size $/PSF

GROSS RENT & AVAILABILITY BY BUILDING CLASS

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

TOP Office Lease Transactions by Size

Address

** Counting smallest divisible units in existing

buildings and buildings under construction.

0

0

Tenant

31

8

2

0

TOP Office Sale Transactions by Price

No transactions were recorded during this period.

*Office Inventory: For the purpose of this report, buildings with less than 10,000 sf of office space and buildings owned and occupied by the

government have not been included in the office inventory. There are 56 office buildings surveyed in this submarket.

Q2-09

AVAILABLE SPACE OPTIONSNumber of units

on the

submarket by

size brackets

# of units**

No transactions were recorded during this period.

Office Submarket Dashboard: Airport West

Not Avail. Office Space Avail. Office Space Gross Rent

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Square Feet

Sublease Direct Sublease as % of Total Available

OCCUPIED SPACE BY MAJOR BUSINESS CATEGORIES

18 MONTH TREND

TOP PROJECTS UNDER CONSTRUCTION BY SIZE

Address Sq. Ft. Est. Com.

75 Courtneypark

West70,721 Q3 2009

SUBMARKET CHARACTERISTICS

Source: Colliers International, Q2 2009

Anchor Tenant

Higgens Development N/A

Developer

$30.22 $25.27

$16.42

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

$-

$5

$10

$15

$20

$25

$30

Class A Class B Class C

Sq. Ft.

Gross Rent $/Sq. Ft.

Not Avail. Office Space Avail. Office Space Gross Rent

Note: Not available office space (blue) and available office space (yellow) add up to the total inventory of office space in the respective building class.

$14.68

4.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%