24

DNV GL © 2016 02 April 2016 SAFER, SMARTER, GREENER DNV GL © 2016 OIL & GAS Offshore Pipeline Outlook 1 Asle Venas Global Director Pipelines DNV GL

DNV GL © 2016

Ungraded

02 April 2016 SAFER, SMARTER, GREENER DNV GL © 2016

Ungraded

OIL & GAS

Offshore Pipeline Outlook

1

Asle Venas

Asle Venas

Global Director Pipelines

DNV GL

DNV GL © 2016

Ungraded

02 April 2016

Onshore and Offshore (Pipeline and Gas Journal)

3

191901 189829 186939

150520 160182

151568

0 0 0

50000

100000

150000

200000

250000

2011 2012 2013 2014 2015 2016 2017 2018

K

M

o

f

p

i

p

e

l

i

n

e

s

Year

Global pipelines Planned and under Construction

Global

Do not distinguish between onshore and offshore

But major part is onshore

DNV GL © 2016

Ungraded

02 April 2016

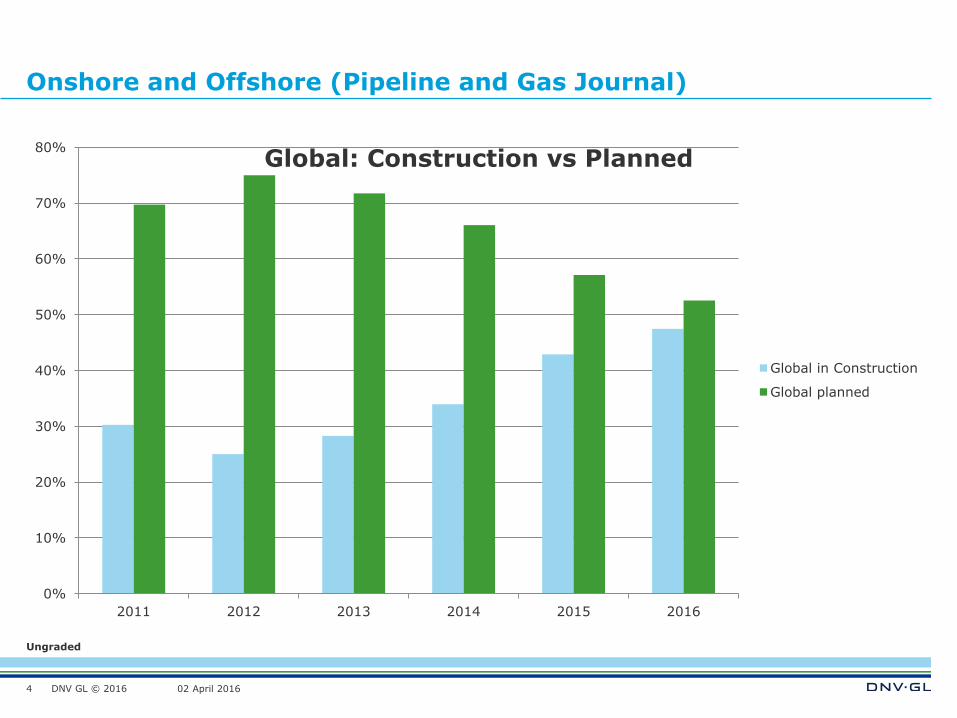

Onshore and Offshore (Pipeline and Gas Journal)

4

0%

10%

20%

30%

40%

50%

60%

70%

80%

2011 2012 2013 2014 2015 2016

Global: Construction vs Planned

Global in Construction

Global planned

DNV GL © 2016

Ungraded

02 April 2016

Onshore and Offshore (Pipeline and Gas Journal)

5

0

10000

20000

30000

40000

50000

60000

70000

80000

2011 2012 2013 2014 2015 2016

Global trends per region

North America

Asia Pacific

South America

Eastern Europe

Africa

Middle East

Western Europe

DNV GL © 2016

Ungraded

02 April 2016

EIC global data base (Sep. 2016):

Midstream pipeline projects: planned and under construction

All midstream pipeline projects:

Pipeline projects (nos.): 893

Total value all projects ($million): 1,241,089

Total length (km): 404,066 (P&G J-jan2016: 151,568)

All midstream offshore pipelines:

Pipeline projects (nos.): 99 (10% of all)

Total value all projects ($million): 281,749 (23% of all)

Total length (km): 43,688 (10% of all)

6

Note: Upstream projects contains loads of pipelines that are not included here

DNV GL © 2016

Ungraded

02 April 2016

EIC - Offshore pipelines - North and South America

Major offshore midstream pipeline projects: 25

Total value: 14,200 $million

Total length: 4,189 Km

Examples:

South Texas - Tuxpan Subsea Natural Gas

Pipeline

Eastern Caribbean Gas Pipeline Network

(Caricom Pipeline)

7

DNV GL © 2016

Ungraded

02 April 2016

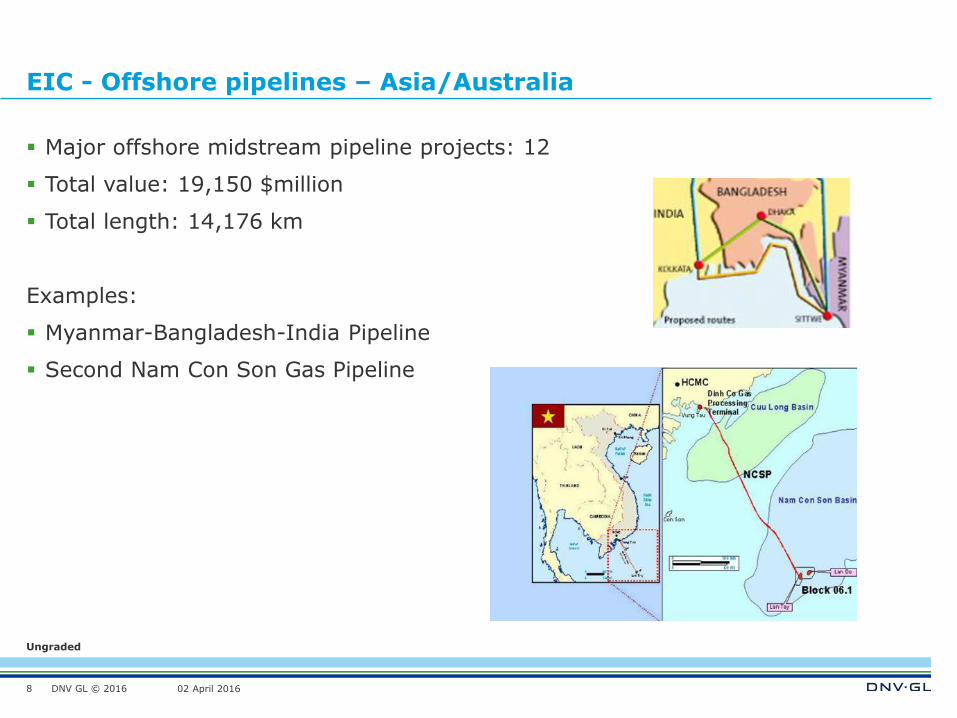

EIC - Offshore pipelines – Asia/Australia

Major offshore midstream pipeline projects: 12

Total value: 19,150 $million

Total length: 14,176 km

Examples:

Myanmar-Bangladesh-India Pipeline

Second Nam Con Son Gas Pipeline

8

DNV GL © 2016

Ungraded

02 April 2016

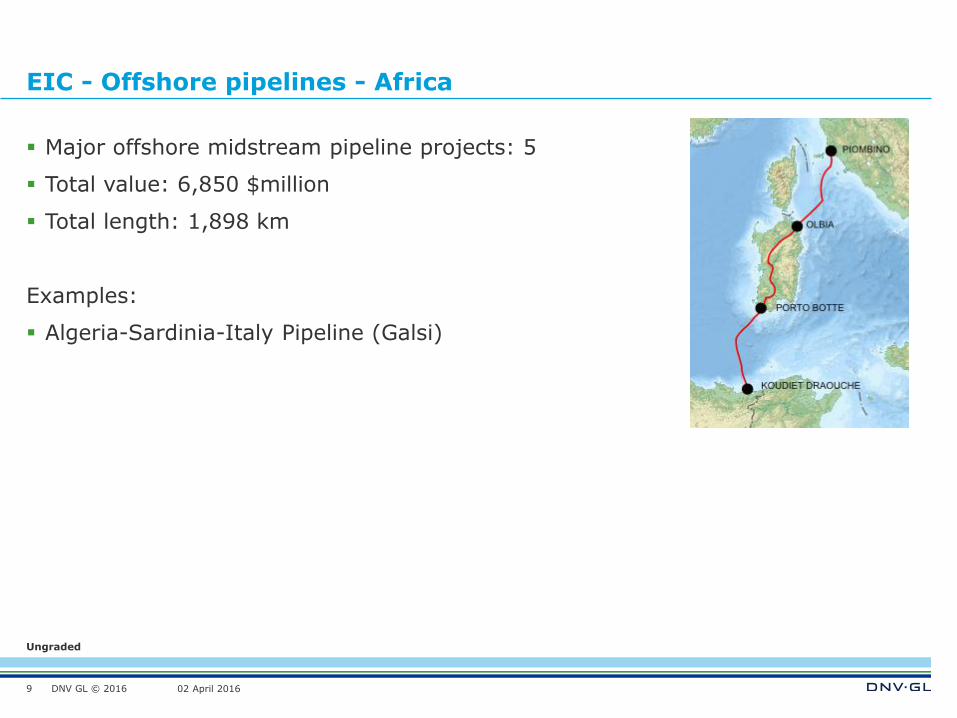

EIC - Offshore pipelines - Africa

Major offshore midstream pipeline projects: 5

Total value: 6,850 $million

Total length: 1,898 km

Examples:

Algeria-Sardinia-Italy Pipeline (Galsi)

9

DNV GL © 2016

Ungraded

02 April 2016

EIC - Offshore pipelines - Europe

Major offshore midstream pipeline projects: 17

Total value: 21,931 $million

Total length: 8,442

Examples:

Johan Sverdrup Oil Export

Trans Adriatic Pipeline

10

DNV GL © 2016

Ungraded

02 April 2016

EIC - Offshore pipelines – Indian sub-continent

Major offshore midstream pipeline projects: 9

Total value: 5,431 $million

Total length: 1,220

Examples:

Colombo - Kolonnawa Oil Pipeline

Kochi-Kayamkulam Subsea Pipeline

11

DNV GL © 2016

Ungraded

02 April 2016

EIC - Offshore pipelines – Middle East

Major offshore midstream pipeline projects: 15

Total value: 25,395 $million

Total length: 6449

Examples:

Iran to Oman Gas Pipeline

Middle East to India Deepwater Gas Pipeline

(SAGE)

12

DNV GL © 2016

Ungraded

02 April 2016

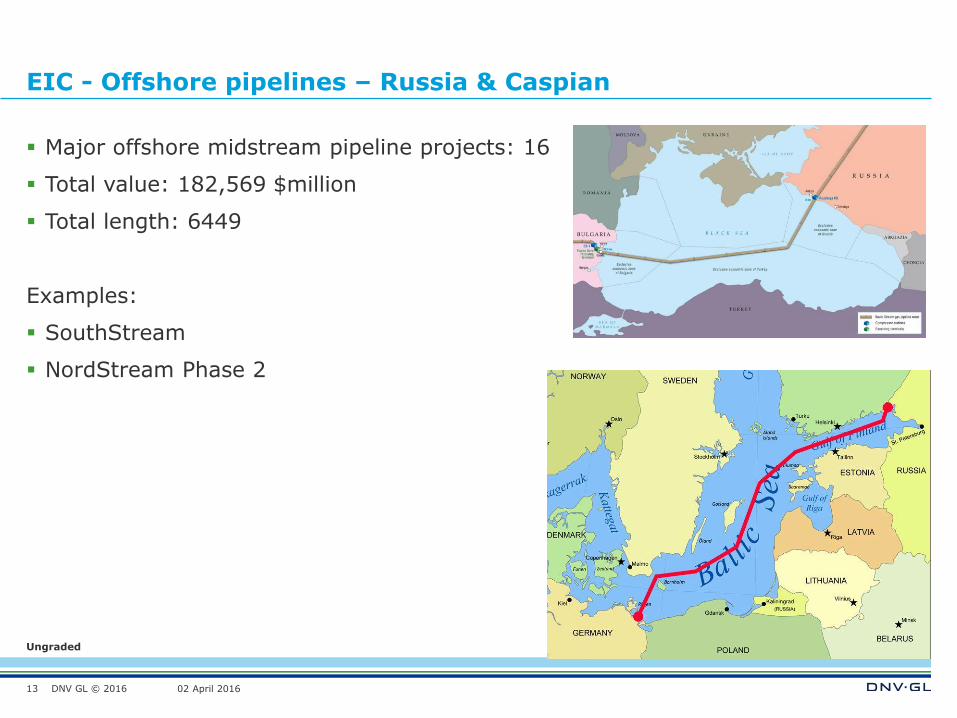

EIC - Offshore pipelines – Russia & Caspian

Major offshore midstream pipeline projects: 16

Total value: 182,569 $million

Total length: 6449

Examples:

SouthStream

NordStream Phase 2

13

DNV GL © 2016

Ungraded

02 April 2016

What can affect future activity

14

DNV GL © 2016

Ungraded

02 April 2016

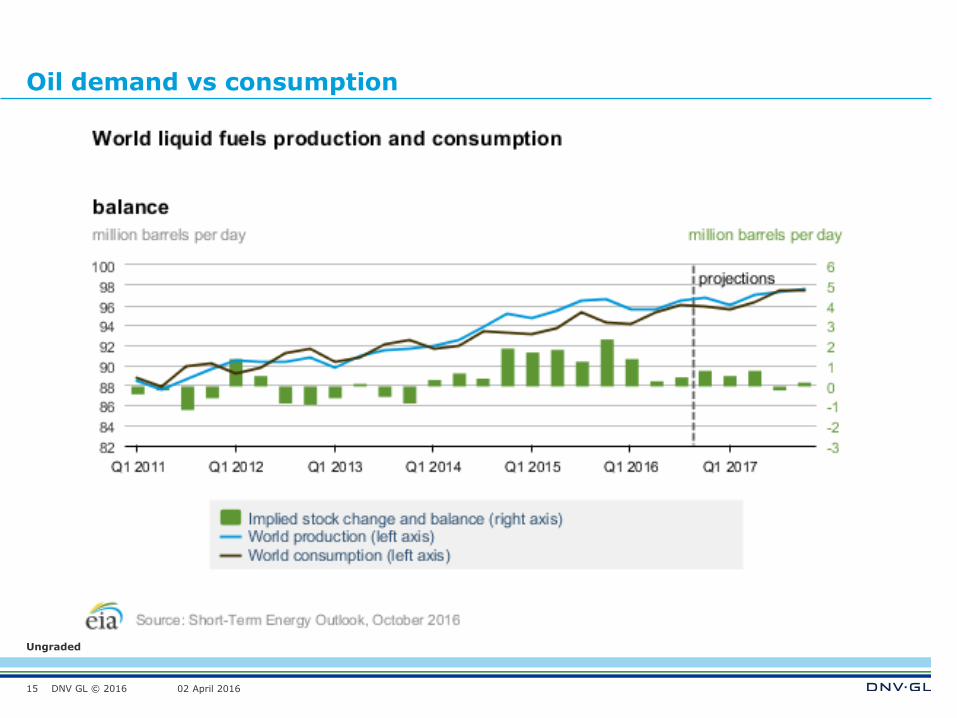

Oil demand vs consumption

15

DNV GL © 2016

Ungraded

02 April 2016

World liquid fuel consumption

16

DNV GL © 2016

Ungraded

02 April 2016

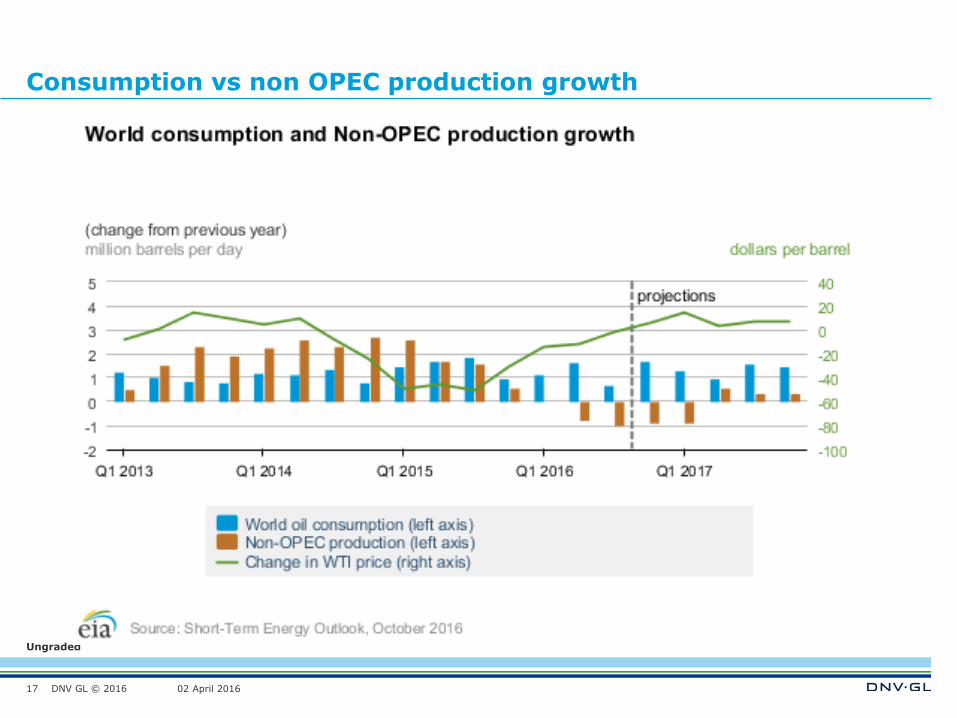

Consumption vs non OPEC production growth

17

DNV GL © 2016

Ungraded

02 April 2016

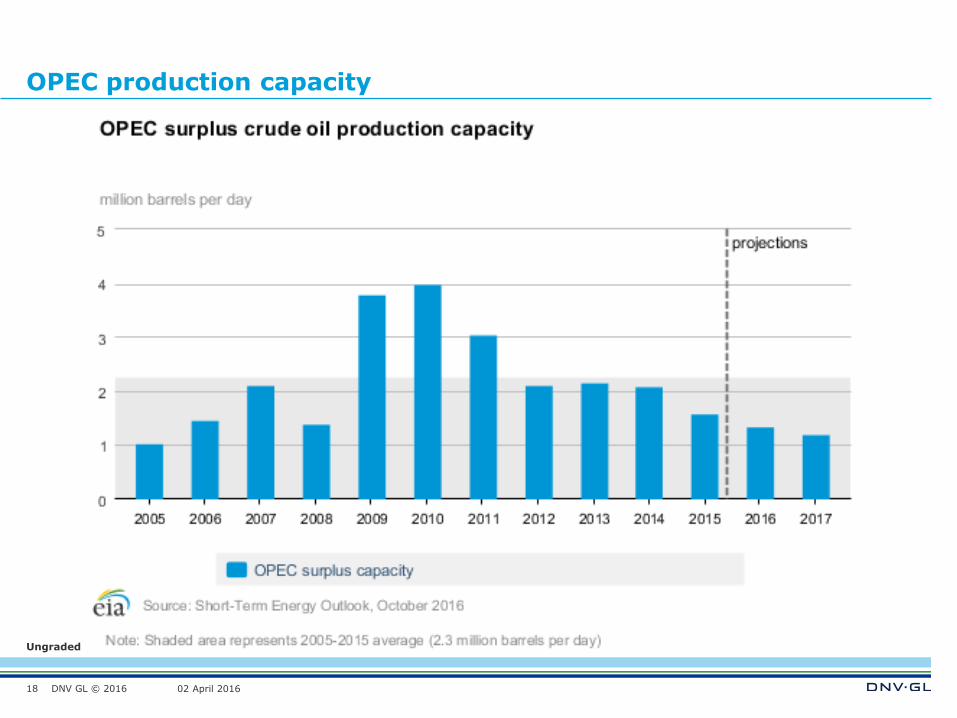

OPEC production capacity

18

DNV GL © 2016

Ungraded

02 April 2016

Where is the oil price going?

19

Source: Offshore, September 2016

DNV GL © 2016

Ungraded

02 April 2016

What have happened last 2 years

Drilling rigs rates reduced 60-70%

Other cost significant reduced

Example:

Johan Castberg 2014: Break even oil price 80 $/bbl

Johan Castberg 2016: Break even oil price 40 $/bbl

20

Is 60$/bbl the new 100$/bbl

DNV GL © 2016

Ungraded

02 April 2016

21

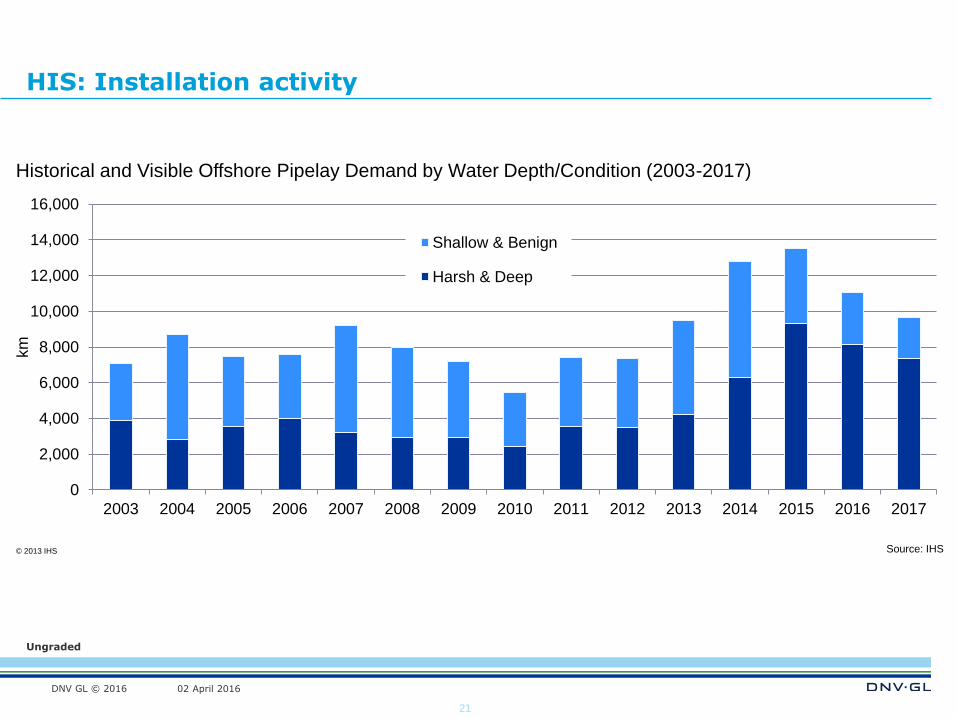

HIS: Installation activity

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

km

Historical and Visible Offshore Pipelay Demand by Water Depth/Condition (2003-2017)

Shallow & Benign

Harsh & Deep

© 2013 IHS Source: IHS

DNV GL © 2016

Ungraded

02 April 2016

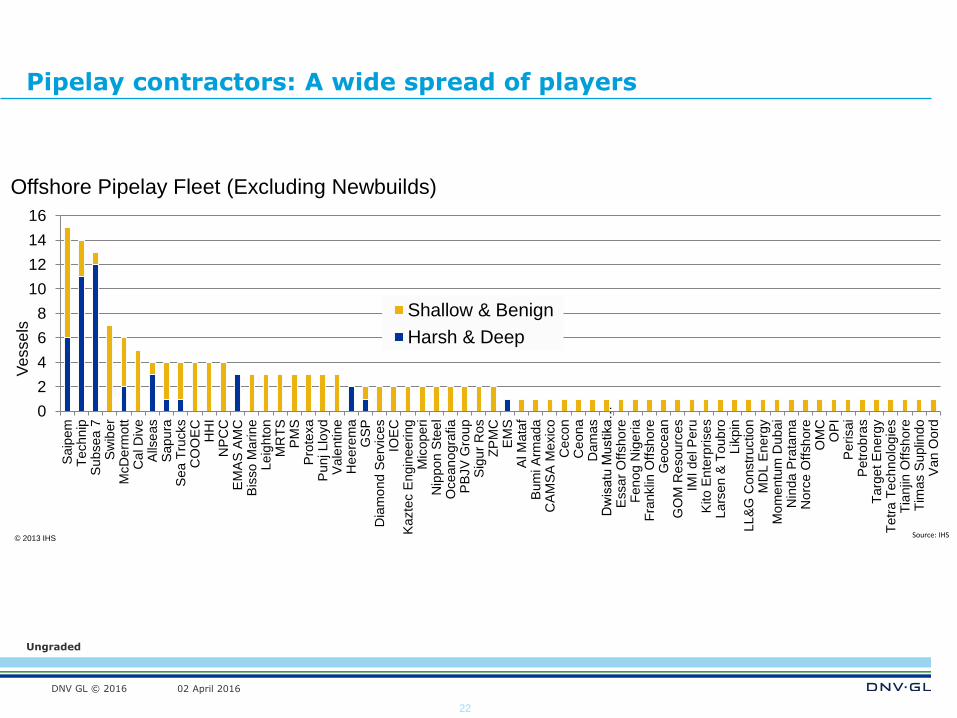

22

Pipelay contractors: A wide spread of players

0

2

4

6

8

10

12

14

16

Saip

em

Techn

ipS

ubsea

7S

wib

er

McD

erm

ott

Ca

l D

ive

Alls

eas

Sapu

raS

ea T

rucks

CO

OE

CH

HI

NP

CC

EM

AS

AM

CB

isso

Ma

rine

Le

ighto

nM

RT

SP

MS

Pro

texa

Punj Llo

yd

Vale

ntine

He

ere

ma

GS

PD

iam

ond S

erv

ices

IOE

CK

azte

c E

ngin

ee

ring

Mic

ope

riN

ippo

n S

tee

lO

cean

ogra

fia

PB

JV

Gro

up

Sig

ur

Ros

ZP

MC

EM

SA

l M

ata

fB

um

i A

rmada

CA

MS

A M

exic

oC

eco

nC

eona

Da

mas

Dw

isatu

Mustika

…E

ssar

Offsho

reF

en

og N

ige

ria

Fra

nklin

Off

sh

ore

Geo

ce

an

GO

M R

eso

urc

es

IMI de

l P

eru

Kito

En

terp

rise

sLa

rsen

& T

oub

roLik

pin

LL

&G

Co

nstr

uctio

nM

DL E

nerg

yM

om

entu

m D

ub

ai

Nin

da

Pra

tam

aN

orc

e O

ffsh

ore

OM

CO

PI

Perisai

Petr

ob

ras

Ta

rge

t E

nerg

yT

etr

a T

echno

log

ies

Tia

njin

Off

sh

ore

Tim

as S

uplin

do

Van O

ord

Vesse

ls

Offshore Pipelay Fleet (Excluding Newbuilds)

Shallow & Benign

Harsh & Deep

© 2013 IHS Source: IHS

DNV GL © 2016

Ungraded

02 April 2016

23

…although newbuilds will change the picture

0

2

4

6

8

10

12

14

16

18

20

Te

ch

nip

Su

bse

a 7

Sa

pu

ra

Sa

ipe

m

Alls

eas

EM

AS

AM

C

McD

erm

ott

Ce

co

n

He

ere

ma

EM

S

GS

P

Se

a T

rucks

Ce

ona

DO

F S

ub

se

a

Oce

an

Insta

ller

Rie

be

r

Ve

sse

ls

Harsh & Deep Pipelay Fleet (Including Newbuilds)

© 2013 IHS Source: IHS

DNV GL © 2016

Ungraded

02 April 2016

Conclusion: Is 60$ the new 100$?

24

DNV GL © 2016

Ungraded

02 April 2016

SAFER, SMARTER, GREENER

www.dnvgl.com

END

25

Asle Venås

+47-93605054