36

OIL AND GAS RESERVES ESTIMATING WE HAVE MET THE ENEMY, AND HE IS US Peter R. Rose Senior Associate, Rose & Associates, LLP., and President AAPG Austin, Texas

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | kristian-melton |

| View: | 220 times |

| Download: | 0 times |

OIL AND GAS RESERVES ESTIMATING

WE HAVE MET THE ENEMY, AND HE IS US

Peter R. Rose

Senior Associate, Rose & Associates, LLP., and President AAPG

Austin, Texas

1. Write your name on the form

2. Follow instructions

3. Try hard to answer objectively

4. Write your answers down

5. No joint ventures -- work independently

6. P90 is a small number; P10 is a large number

RULES OF THE GAME

DETERMINISTIC ESTIMATE

A single number (best guess) among a wide range of possible real outcomes.

Low confidence in being precisely correct.

Amount of uncertainty affects willingness to invest in your estimate.

FOR $20, HOW MUCH ARE YOU PREPARED TO BET THAT YOUR BEAN-ESTIMATE IS EXACTLY CORRECT?

$10?$5?

$2?$1?

50¢?20¢?

10¢?5¢?

Chance of estimating

the exact number of beans?

!REMOTE!

UNCERTAINTY & CONFIDENCE

EXPRESSING CONFIDENCE I

• Traditional Engineering Convention -- ±10%?

• Ranges of Numbers Corresponding to Confidence:

Confidence (=,>)

> 10 beans

> 100 beans

> 1,000 beans

> 200 beans

> 2,000 beans

> 20,000 beans

very, very high

high

moderate

fairly high

low

very, very low

Confidence (=,>)

EXPRESSING CONFIDENCE II

LET US SPECIFY:

“High Confidence” = 90% sure =, > P90 value

“Low Confidence” = 10% sure =, > P10 value

“50/50 Confidence” = 50% sure =, > P50 = Median

Superiority Of Probabilistic Method

“. . . still just estimates cloaked in probabilities?”

Advantages:

1. Measure our estimating accuracy by comparing probabilistic forecasts against actual outcomes

2. Use statistical principles to make better estimates (lognormal expectation, calculate mean of distribution, defined low-side & high-side criteria

P1 Geologically possible; but extremely unlikely P10 Reasonable Maximum P50 Half below, Half above, the Median P90 Reasonable MinimumP99 As small as it could be . . . Yet detectable

PRACTICAL ATTRIBUTES OF KEY PARAMETERS

Boundary Conditions

80% confidence level

Superiority Of Probabilistic Method

“. . . still just estimates cloaked in probabilities?”

Advantages:

1. Measure our estimating accuracy by comparing probabilistic forecasts against actual outcomes

2. Use statistical principles to make better estimates (lognormal expectation, calculate mean of distribution, defined low-side & high-side criteria

3. Reality-checks -- natural limits, unrealistic extremes, analog distributions

4. Faster, more efficient

Compare your original “best estimate” (circled number, item 2, colored form) with your neighbor

Does anyone in the audience have a circled number that is EXACTLY

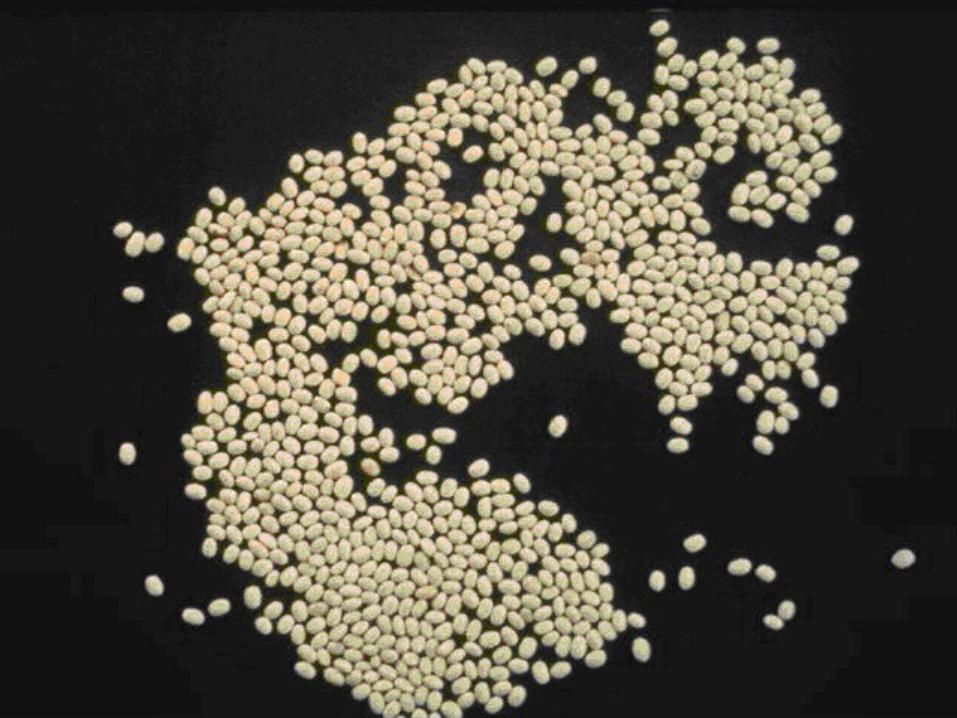

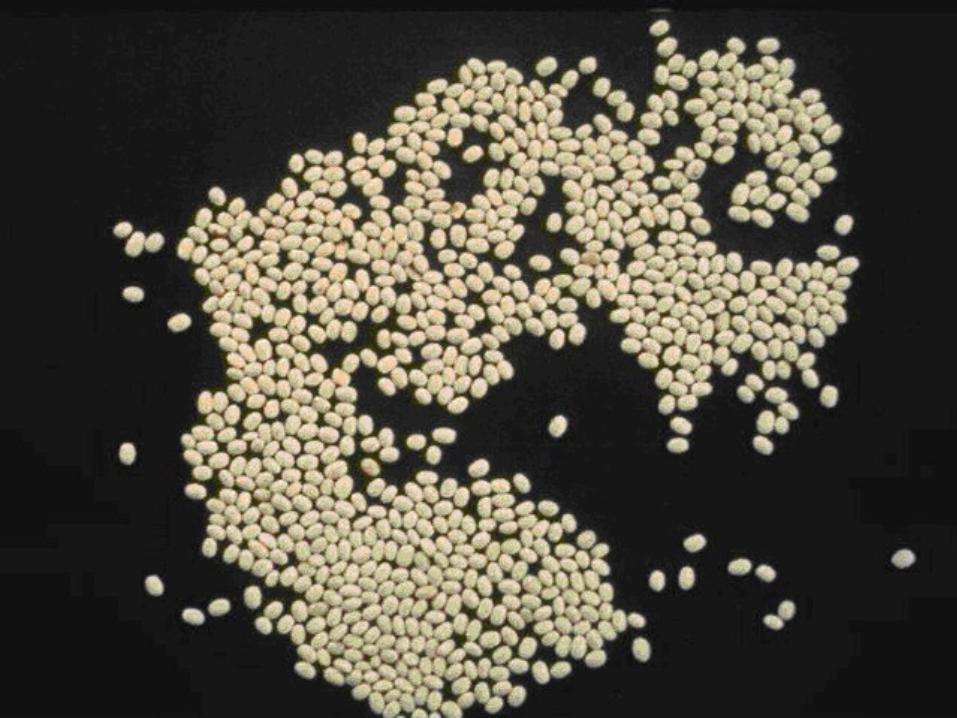

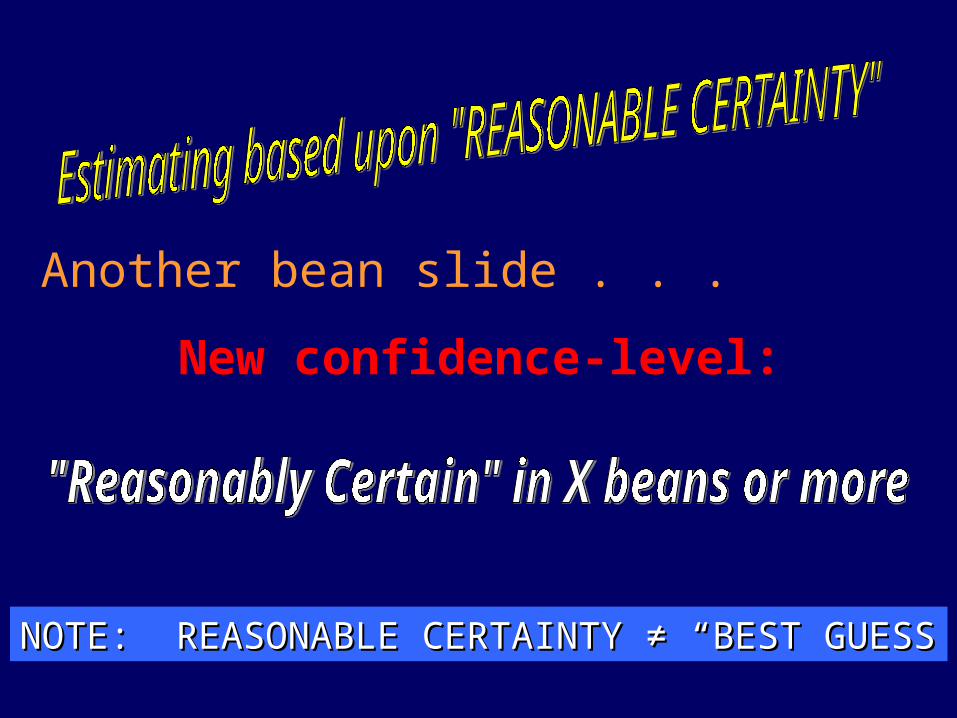

Another bean slide . . .

New confidence-level:

NOTE: REASONABLE CERTAINTY NOTE: REASONABLE CERTAINTY ≠ “BEST GUESS≠ “BEST GUESS

I am “Reasonably Certain” that there are ________ beans or more.

NOTE: THIS IS A PROBABILITY STATEMENT, ALTHOUGH NO PROBABILITY (= CONFIDENCE LEVEL) IS SPECIFIED

WHAT IS YOUR REASONABLE CERTAINTY?50%? 67%? 75%? 80%? 90%? 95%? 99%?

HOW CAN YOU MEASURE YOUR ESTIMATING HOW CAN YOU MEASURE YOUR ESTIMATING ABILITY USING AN UNDEFINED CRITERION?ABILITY USING AN UNDEFINED CRITERION?

444466

COMPLICATIONS

1. A larger estimate may be in your personal interest

2. Your boss may prefer larger to smaller estimates

3. Possible consequences if actual result is less than your estimate

a) Negative Press

b) Employer Disciplines

c) State Penalizes

U.S. SEC REFUSES TO SPECIFY THE CONFIDENCE-LEVEL OF“REASONABLE CERTAINTY”

99%?

80%?

95%?

67%?

90%?75%?

98%?

50%?

. . . BUT SEC will not specify confidence level assigned to “PROVED”

“Proved” Reserves

. . . are the estimated quantities which geological and engineering data demonstrate with reasonable certainty to be recoverable. . .

.sec.gov / divisions / corpfin / forms / regsx. htm

This is the foundational statement of what we think is an outdated (1978) system.

Let’s take a look at the evolution of the wording

reas

onab

le c

erta

inty

www

1936

Every reasonable probability

1964

Reasonable certainty

1976

CapenSPE 5579

1981

Revised def.for proved

1987

Provedprobable &possible

1978

Proved w reasonable

certainty

APIYergin and Hobbs, 2005 ogj

SPE

US SEC 1982

Year-endpricing

1997

Probabilistic methods

guidelinespublished

“Proved” Reservesre

ason

able

cer

tain

ty

DETERMINISM GETS INCREASINGLY COMPLEX

• Proved, Probable, Possible

• Developed & Undeveloped

• Weighting schemes to account for uncertainty

• ? Applicability to Undrilled Prospects and Plays?

PROBABILISTIC ESTIMATING COMES TO PETROLEUM EXPLORATION (≈ 1985 )

• Exploration is a “repeated-trials game” of many uncertain ventures

• Statistical treatment is appropriate

• Statistics = “Language of Uncertainty”

• Aids to Improved Estimating -- LognormalityReality ChecksProject post-audits improved estimating skills

• Leads to Portfolio Management

PROBABILISTIC ESTIMATING: STANDARD EXPLORATION PRACTICE

• Tipping Point mid-1990s

• SPE/WPC acknowledged in 1997, recognizing both Deterministic and Probabilistic approaches

• SPE/WPC recommendation:

Proved = 90% Confidence

Reserves Estimating: A Divided Industry

Exploration:Fully Probabilistic

Production: Mostly Deterministic (Proved, Probable, Possible,

Developed, Undeveloped, etc.)

TWO VIEWS OF E&P WORK:Deterministic View: Probabilistic

View:

TIM

E &

$$

← UNCERTAINTY →T

IME

& $

$← UNCERTAINTY →

“THE ANSWER”

(Determinism)P

90

P50

P10

STOP!

Use this time & $$ to find other

prospects

Determinism Promotes Unaccountability

Attempts to represent highly uncertain parameters with a single, “precise” number, and without expressing how much uncertainty surrounds it.

Proved, Probable, Possible: terms not defined quantitatively, so impossible to measure and calibrate estimating abilities objectively

So the Deterministic Method is unaccountable to:

Professionals

Clients and Employers

Investors

General Public

PROBABILISTIC METHODS PROMOTE ACCOUNTABILITY

All possible outcomes are assigned likelihood of occurrence

Compare estimates with outcomes:

• Detects and measures bias

• Encourages learning and improved estimating

Compatible with Portfolio Management

Adaptable to considerations of Chance of Success

Can be universally applied to all E&P projects

(Plays, Prospects, Developments, Workovers, EOR’s, etc.)

? Resistance to change?? Resistance to change?

? Propped up by SEC?? Propped up by SEC?

? Accountants can’t deal with uncertainty?? Accountants can’t deal with uncertainty?

? Encourages false confidence?? Encourages false confidence?

? Desire to remain unaccountable?? Desire to remain unaccountable?

DETERMINISM ENCOURAGES UNREALISTIC THINKING ABOUT HIGHLY

UNCERTAIN RESOURCE VALUES

• Executives, Board Members, Bankers, Analysts, Stockholders

• Enables Decision-makers to maintain unwarranted confidence

• Discourages realistic assessments of uncertainty and risk

One Simple Remedy to Start Fixing the Problem

A unified statement from the E&P professional community that “Proved” = 90% confidence.

•Imposed Definition on SEC

•Support of Professional Societies?

•Support of Influential Companies?

Industry professionals created this problem -- Industry professionals created this problem --

Why don’t we, as responsible Professionals, change it?Why don’t we, as responsible Professionals, change it?

(Walt Kelly, POGO)

OIL AND GAS RESERVES ESTIMATING

WE HAVE MET THE ENEMY, AND HE IS US

Peter R. Rose

Senior Associate, Rose & Associates, LLP., and President AAPG

Austin, Texas