www.eia.gov U.S. Energy Information Administration Independent Statistics & Analysis Oil and natural gas: market outlook and drivers for 2016 Intellectual Capital Conference May 25, 2016 | Baltimore, MD by Howard Gruenspecht, Deputy Administrator

Transcript

www.eia.govU.S. Energy Information Administration Independent Statistics & Analysis

Oil and natural gas: market outlook and drivers

for

2016 Intellectual Capital Conference

May 25, 2016 | Baltimore, MD

by

Howard Gruenspecht, Deputy Administrator

world supply and demand

million barrels per day

implied stock change

million barrels per day

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Global supply has consistently exceeded demand since the start of 2014;

EIA forecasts a return to market balance in the second half of 2017

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

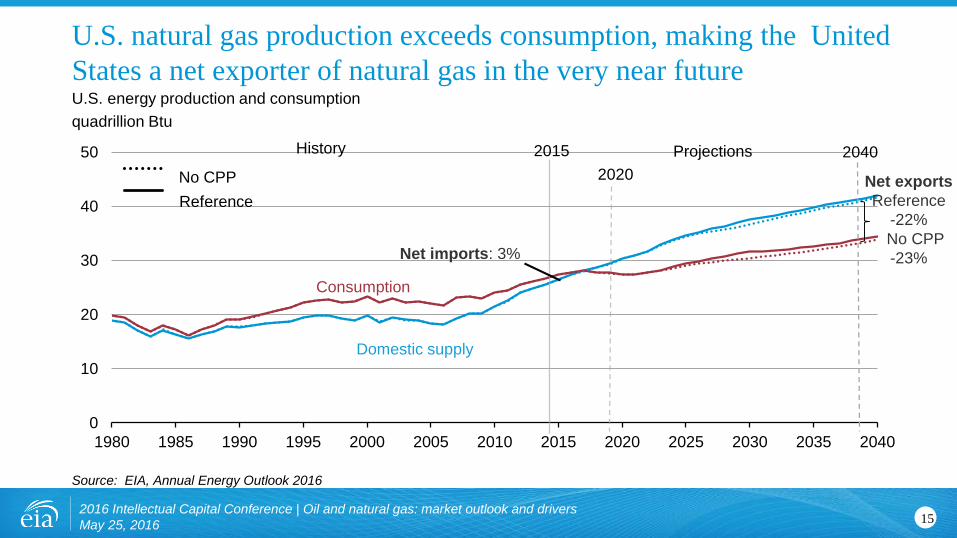

U.S. natural gas production exceeds consumption, making the United

States a net exporter of natural gas in the very near future

Source: EIA, Annual Energy Outlook 2016

15

History Projections2015

Net exports

Reference

-22%

No CPP

-23%

Consumption

Domestic supply

Net imports: 3%

2020

2040

Reference

No CPP

Shale resources remain the dominant source of U.S. natural gas

production growth

16

0

20

40

60

80

100

120

0

5

10

15

20

25

30

35

40

45

1990 2000 2010 2020 2030 2040

U.S. dry natural gas production

trillion cubic feet

Source: EIA, Annual Energy Outlook 2016

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Tight gas

Coalbed methane

Other lower 48

onshore

Shale gas and

tight oil plays

AlaskaLower 48 offshore

History2015

Projections

AEO2016 Reference

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

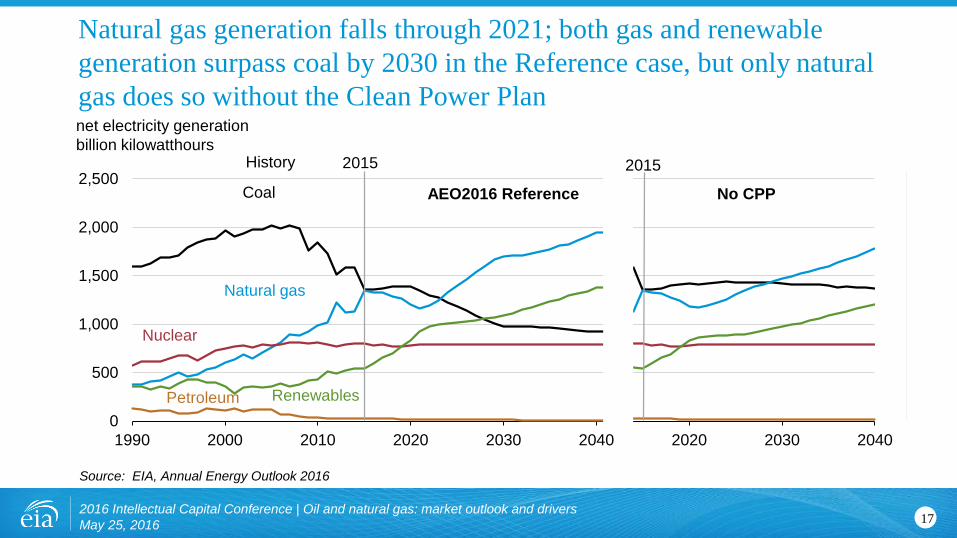

Natural gas generation falls through 2021; both gas and renewable

generation surpass coal by 2030 in the Reference case, but only natural

gas does so without the Clean Power Plan

17

0

500

1,000

1,500

2,000

2,500

1990 2000 2010 2020 2030 2040 2020 2030 2040

AEO2016 Reference No CPP

2015History 2015

Nuclear

Petroleum

Natural gas

Coal

Renewables

net electricity generation

billion kilowatthours

Source: EIA, Annual Energy Outlook 2016

Natural gas consumption growth is led by electricity generation and

industrial uses; natural gas use rises in all sectors except residential

18

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

2005 2015 Reference No CPP Reference No CPP Reference No CPP

U.S. dry gas consumption

trillion cubic feet billion cubic feet per day

Source: EIA, Annual Energy Outlook 2016

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

ProjectionsHistory

Electric powerIndustrial*Residential Transportation**

12.6

4.6

1.7

11.2

3.7

9.1

4.6

0.9

9.6

3.2

*Includes combined heat-and-power and lease, plant, and export liquefaction fuel

Commercial

12.5

4.6

1.7

12.0

3.7

20402020 2030

**Includes pipeline fuel

Global crude oil prices

Nominal dollars per barrel, monthly average

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

World oil prices move together due to arbitrage

Sources: Bloomberg, Thomson Reuters

19

select global natural gas and crude oil prices with average monthly LNG prices in Japan

U.S. dollars per million British thermal unit

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

North American natural gas prices are low compared to prices in the

rest of the world, although spreads have narrowed recently

Source: EIA, Bloomberg L.P.

20

Global Energy Outlook

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 201621

Key findings in the IEO2016 Reference case

• World energy consumption increases 48% increase (1.4% compound annual growth rate) between 2012 and 2040. Non-OECD Asia (including China and India) account for more than half of the increase.

• The industrial sector continues to account for the largest share of delivered energy consumption; the world industrial sector still consumes over half of global delivered energy in 2040.

• Renewable energy is the world’s fastest-growing energy source, increasing by 2.6%/year; nuclear energy grows by 2.3%/year, from 4% of the global total in 2012 to 6% in 2040.

• Fossil fuels continue to supply more than three-fourths of world energy use in 2040.

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 201622

Many global issues increase uncertainty…

• Economic growth in key economies (China, Brazil, Russia, among others)

• Implementation and strength of climate policies

• Technology improvement rates (both supply and demand)

• Unrest in oil producing countries

• OPEC production

• Future of nuclear generating capacity

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 201623

-4

-2

0

2

4

6

U.S. OECDEurope

Japan SouthKorea

China India Brazil MiddleEast

Africa Russia

Energy Intensity GDP per capita Population

average annual percent change (2012–40)

percent per year

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Economic activity and population drive increases in energy use; energy

intensity (E/GDP) improvements moderate this trend

Source: EIA, International Energy Outlook 2016

24

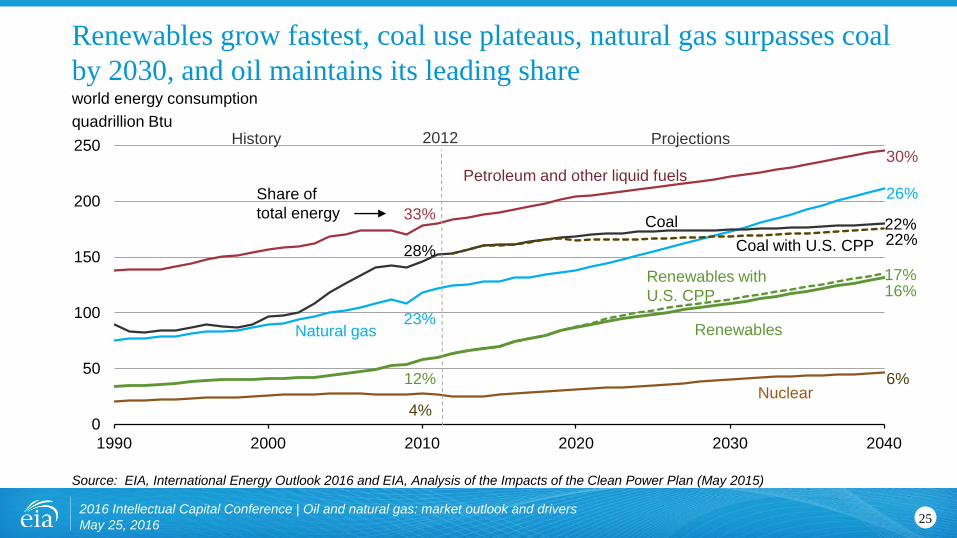

0

50

100

150

200

250

1990 2000 2010 2020 2030 2040

Coal

Petroleum and other liquid fuels

Natural gas Renewables

Nuclear

Coal with U.S. CPP

Renewables with

U.S. CPP

Share of

total energy

world energy consumption

quadrillion Btu

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Renewables grow fastest, coal use plateaus, natural gas surpasses coal

by 2030, and oil maintains its leading share

Source: EIA, International Energy Outlook 2016 and EIA, Analysis of the Impacts of the Clean Power Plan (May 2015)

25

History Projections2012

33%

30%

28%

22%

23%

26%

12%

17%

4%

6%

22%

16%

40

50

60

70

1990 2000 2010 2020 2030 2040

Non-OECD

OECD

carbon intensity of energy consumption, 1990-2040

kilograms CO2 per million Btu

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Projected carbon intensity of energy use (CO2/E) declines through 2040

in both OECD and non-OECD; non-OECD CO2/E rose over 2000–12

Source: EIA, International Energy Outlook 2016

26

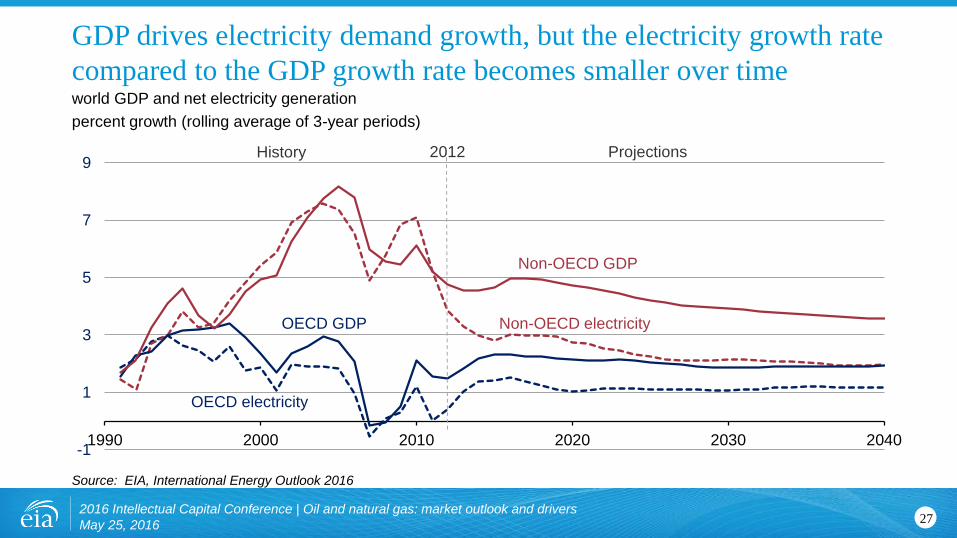

History Projections2012

-1

1

3

5

7

9

1990 2000 2010 2020 2030 2040

Non-OECD electricity

Non-OECD GDP

OECD GDP

OECD electricity

world GDP and net electricity generation

percent growth (rolling average of 3-year periods)

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

GDP drives electricity demand growth, but the electricity growth rate

compared to the GDP growth rate becomes smaller over time

Source: EIA, International Energy Outlook 2016

27

History Projections2012

0

10

20

30

40

2012 2020 2025 2030 2035 2040

world net electricity generation by source

trillion kilowatthours

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Renewables, natural gas, and coal all contribute roughly the same

amount of global net electricity generation in 2040

Source: EIA, International Energy Outlook 2016

28

Liquids

Other renewables

Natural gas

Coal

Nuclear

Hydropower

passenger-miles per capita (left-axis) and GDP per capita (horizontal-axis) for

selected country groupings 2010–40

2016 Intellectual Capital Conference | Oil and natural gas: market outlook and drivers

May 25, 2016

Passenger-miles per person will rise as GDP per capita grows; travel