337

#oilgasict Welcome to

| Date post: | 10-Jan-2017 |

| Category: |

Technology |

| Upload: | ray-bugg |

| View: | 956 times |

| Download: | 5 times |

#oilgasict

Welcome to

#oilgasict

Mark StephenBBC Scotland

#oilgasict

Conference App & Wi-Fi on badges

#oilgasict

Richard Higgsbrightsolid

5Information Classification: Open All Rights recognised

Collaborating locally to lead the way globally in deflationary digital services

The next 20 minutes

The 7 critical cloud considerations

Future ready technology and emerging trends for 2020

Ensuring IT remains deflationary and returns agility

7Information Classification: Open All Rights recognised

The board have concerns and down the list is IT

8Information Classification: Open All Rights recognised

Security, operational reliability, cost cuts and

collaboration are on our minds for today

9Information Classification: Open All Rights recognised

7 critical cloud considerations

10Information Classification: Open All Rights recognised

Cost Assurance: Price matching

Hardware operational budget of

<£1m

Azure cost

estimator tool

Azure £250K per year

brightsolid£185K

per year

brightsolid includes: service desk, remote back-ups and DDoS protection

11Information Classification: Open All Rights recognised

Be confident and expert in Security

Hosting up to Government level ‘Official Sensitive’

12Information Classification: Open All Rights recognised

Critical connectivity…..

13Information Classification: Open All Rights recognised

DR has to be guaranteed…. at a third of the price of your primary cloud

14Information Classification: Open All Rights recognised

Contention and neighbours?

15Information Classification: Open All Rights recognised

International & Utility cloud connection

16Information Classification: Open All Rights recognised

Future ready and proofed

18Information Classification: Open All Rights recognised

Welcome……to hybrid cloud

19Information Classification: Open All Rights recognised

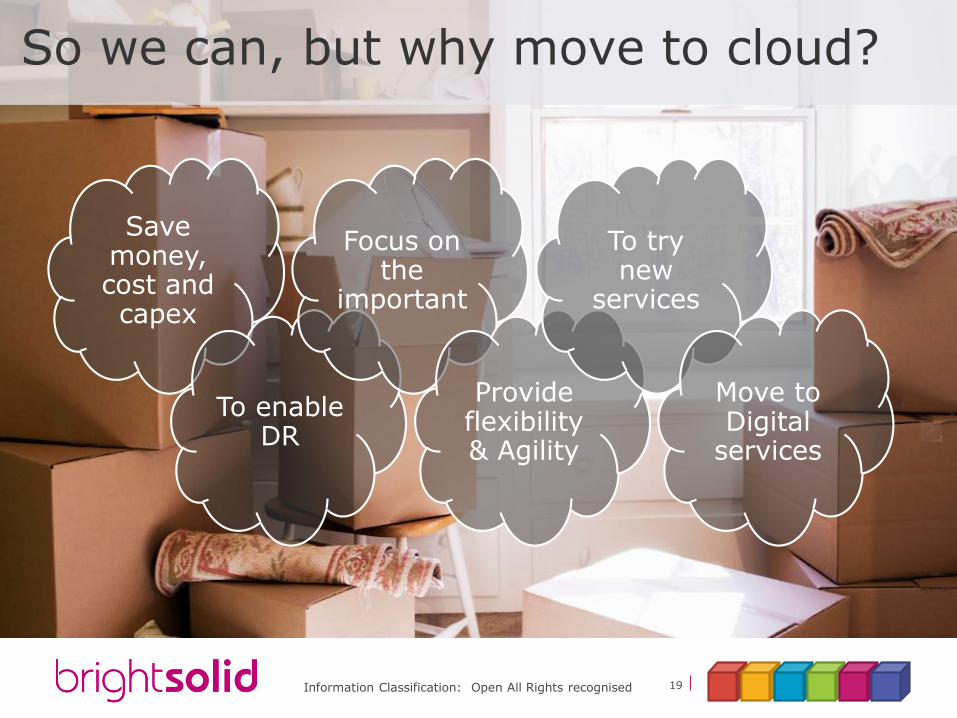

Save money, cost and capex

To enable DR

Focus on the

important

Provide flexibility & Agility

To try new

services

Move to Digital

services

So we can, but why move to cloud?

20Information Classification: Open All Rights recognised

Everyone can now embrace the cloud

21Information Classification: Open All Rights recognised

Positive spiral through technology

22Information Classification: Open All Rights recognised

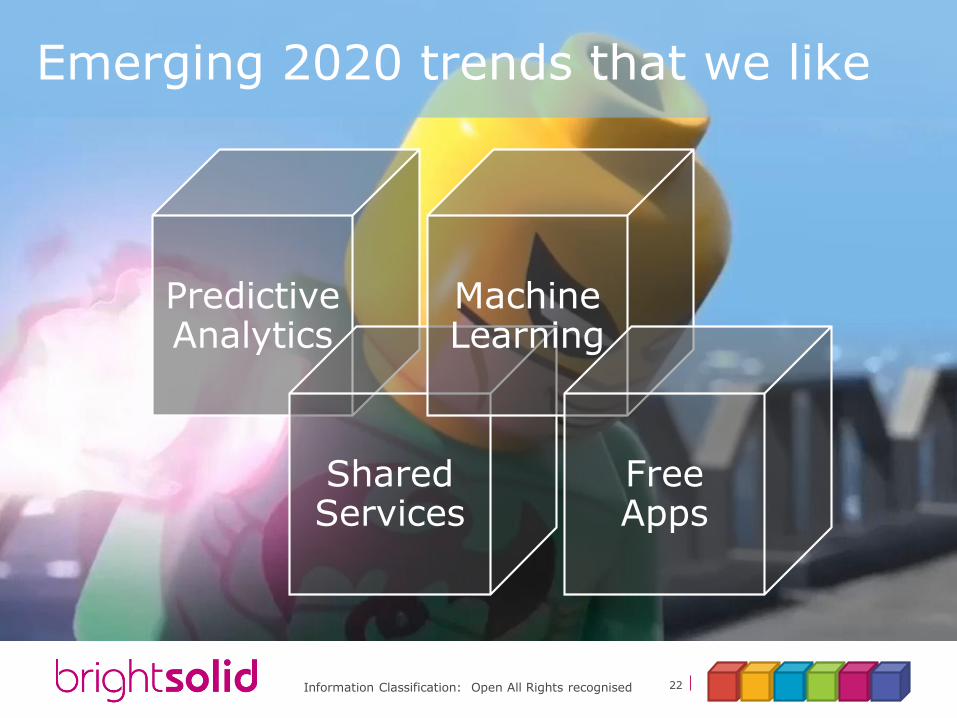

Emerging 2020 trends that we like

Predictive Analytics

Shared Services

Machine Learning

Free Apps

23Information Classification: Open All Rights recognised

24Information Classification: Open All Rights recognised

Free applications and infinite development opportunities

In micro services in open source application layers

25Information Classification: Open All Rights recognised

Shared services vision and local collaboration

26Information Classification: Open All Rights recognised

Shared services vision and local collaboration

27Information Classification: Open All Rights recognised

How much could you actually save?

28Information Classification: Open All Rights recognised

£350K a year -the best we’ve achieved

since opening our Aberdeen Facility

29Information Classification: Open All Rights recognised

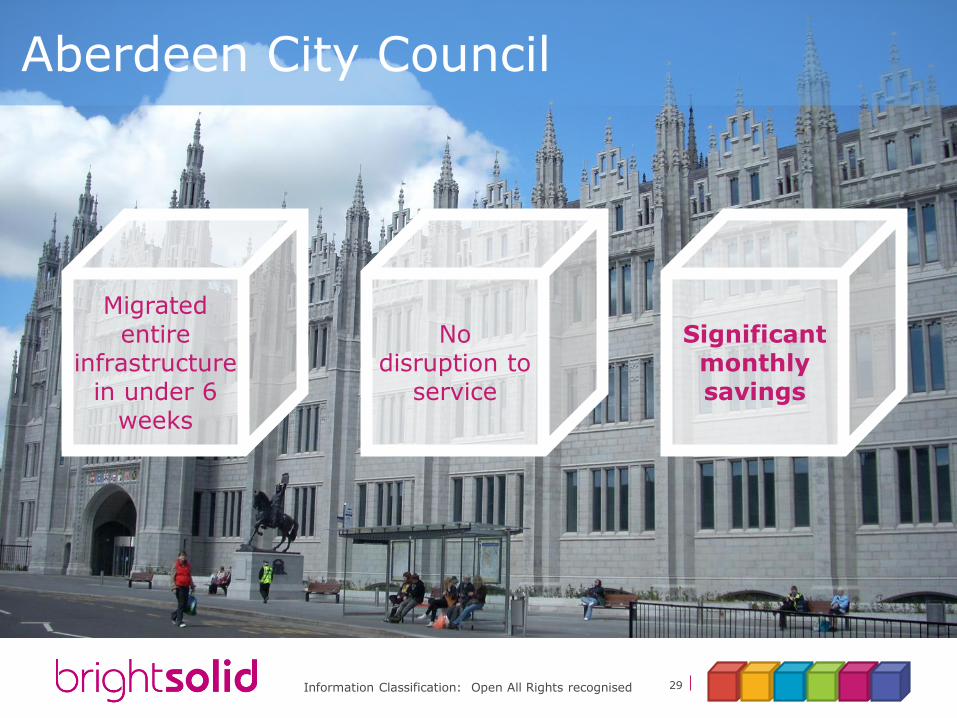

Aberdeen City Council

Migrated entire

infrastructure in under 6

weeks

No disruption to

service

Significant monthly savings

30Information Classification: Open All Rights recognised

“In brightsolid, we have found a partner with whom we can

innovatively work as we digitally transform our council

services whilst also reducing our operational costs.” Aberdeen City Council Finance

Policy and Resources Convenor Councillor

Willie Young

Technical Innovation with Personal Service

31Information Classification: Open All Rights recognised

How?Critical Attributes, Choices, Outcomes

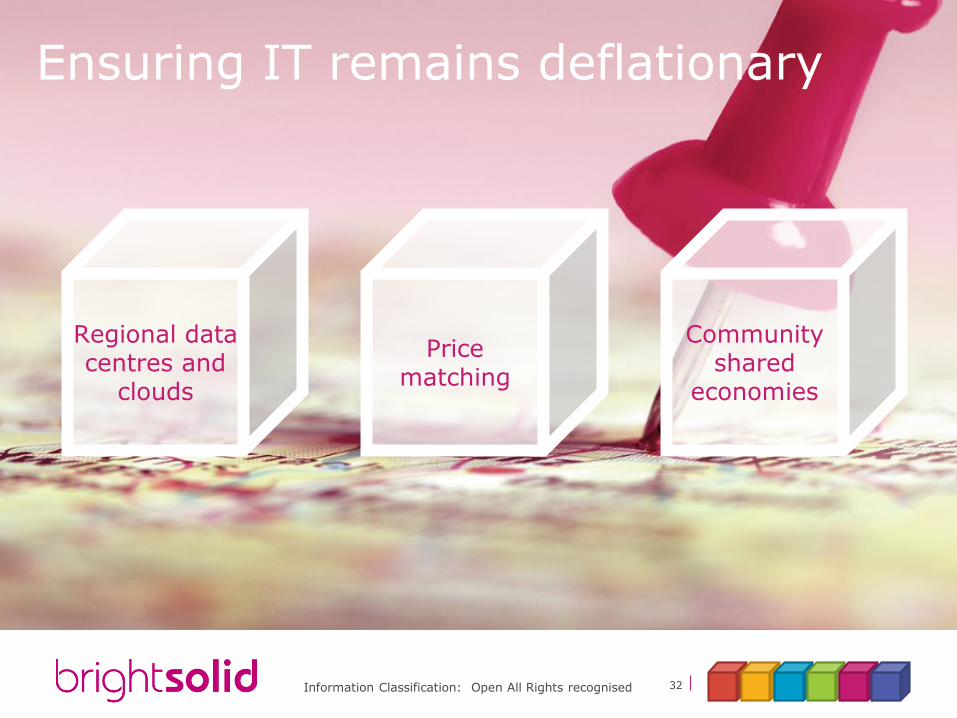

32Information Classification: Open All Rights recognised

Regional data centres and

clouds

Price matching

Community shared

economies

Ensuring IT remains deflationary

33Information Classification: Open All Rights recognised

Ecofris PUE sub 1.2525 Kw per

rack

Efficiency cooling the price

34Information Classification: Open All Rights recognised

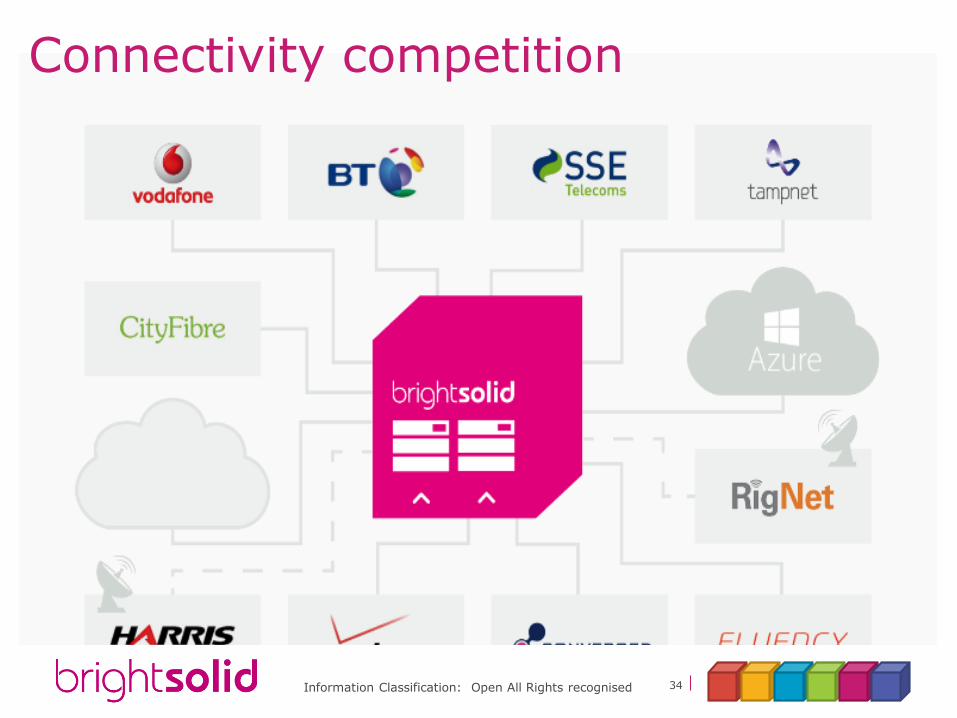

Connectivity competition

35Information Classification: Open All Rights recognised

Bundling essential services…….back-ups are boring but included

36Information Classification: Open All Rights recognised

So is support………….

37Information Classification: Open All Rights recognised

And Awards and AccreditationsSecurity is at the heart of everything we do

38Information Classification: Open All Rights recognised

ButCould we just dip a toe in the water…

39Information Classification: Open All Rights recognised

We can continue to drive down cost whilst adhering to our Values

42Information Classification: Open All Rights recognised

Enough about us, we want to hear from you

#oilgasict

Ard de BruijneShell

Copyright of Shell International BV

ADOPTING AN OPEN STANDARD FOR

MANAGING IT

Ard de Bruijne

Strategy, Planning & Architecture Manager Global Functions

Copyright of Shell International BV

DEFINITIONS AND CAUTIONARY NOTE

Reserves: Our use of the term “reserves” in this presentation means SEC proved oil and gas reserves.

Resources: Our use of the term “resources” in this presentation includes quantities of oil and gas not yet classified as SEC proved oil and gas reserves. Resources are consistent

with the Society of Petroleum Engineers 2P and 2C definitions.

Organic: Our use of the term Organic includes SEC proved oil and gas reserves excluding changes resulting from acquisitions, divestments and year-average pricing impact.

Resources plays: Our use of the term ‘resources plays’ refers to tight, shale and coal bed methane oil and gas acreage.

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate entities. In this presentation “Shell”, “Shell group” and “Royal Dutch Shell” are

sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer

to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying the particular company or companies.

‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this presentation refer to companies in which Royal Dutch Shell either directly or indirectly has control.

Companies over which Shell has joint control are generally referred to as “joint ventures” and companies over which Shell has significant influence but neither control nor joint control

are referred to as “associates”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held by Shell in a venture, partnership or

company, after exclusion of all third-party interest.

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than

statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on

management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ

materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Royal

Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are

identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘intend’’, ‘‘may’’, ‘‘plan’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘probably’’, ‘‘project’’,

‘‘will’’, ‘‘seek’’, ‘‘target’’, ‘‘risks’’, ‘‘goals’’, ‘‘should’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could

cause those results to differ materially from those expressed in the forward-looking statements included in this presentation, including (without limitation): (a) price fluctuations in

crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and

industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful

negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and

regulatory developments including potential litigation and regulatory measures as a result of climate changes; (k) economic and financial market conditions in various countries and

regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of

projects and delays in the reimbursement for shared costs; and (m) changes in trading conditions. All forward-looking statements contained in this presentation are expressly

qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional

factors that may affect future results are contained in Royal Dutch Shell’s 20-F for the year ended 31 December, 2014 (available at www.shell.com/investor and www.sec.gov ).

These factors also should be considered by the reader. Each forward-looking statement speaks only as of the date of this presentation, 15 March, 2016. Neither Royal Dutch Shell

nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In

light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this presentation. There can be no assurance

that dividend payments will match or exceed those set out in this presentation in the future, or that they will be made at all.

We use certain terms in this presentation, such as discovery potential, that the United States Securities and Exchange Commission (SEC) guidelines strictly prohibit us from including

in filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov. You can also

obtain this form from the SEC by calling 1-800-SEC-0330.

Copyright of Shell International BV

AGENDA

The environment

What is IT4IT anyway?

The Shell IT4IT Journey

Copyright of Shell International BV

THE ENVIRONMENT –

SHELL AND IT

Company name appears here

ABOUT SHELL IN 2014

$1.2 billion

Amount we spent

on R&D

70+

Number of countries

in which we operated

$160 million

Spent on voluntary social

investment worldwide

$13.7 billion

Spent in lower

income countries

10%

Our share of the world’s LNG

sold

40+

Number of LNG vessels we

manage and operate

3.1 million

Our equity production in

barrels of oil equivalent a day

51.8%

Share of our production that

was natural gas

94,000

Average number

of people we employed

24 million

Tonnes of LNG we sold

$45 billion

Cash flow from operating

activities

2%

Our share of the world’s

oil production

3%

Our share of the world’s

gas production

Copyright of Shell International BV

NAVIGATING A DISRUPTIVE ENVIRONMENT

49

EVERYTHING

TO CLOUD

INFORMATION FROM

DATA &

ANALYTICS

COLLABORATION

ACROSS ALL

(MOBILE) DEVICES

CONTROLS, LEGAL,

REGULATORY &

CYBER DEFENCE

BUSINESS PLATFORMS

GUIDE INVESTMENT

DECISIONS

DIGITALISATION

AND INTERNET

OF THINGS

Copyright of Shell International BV

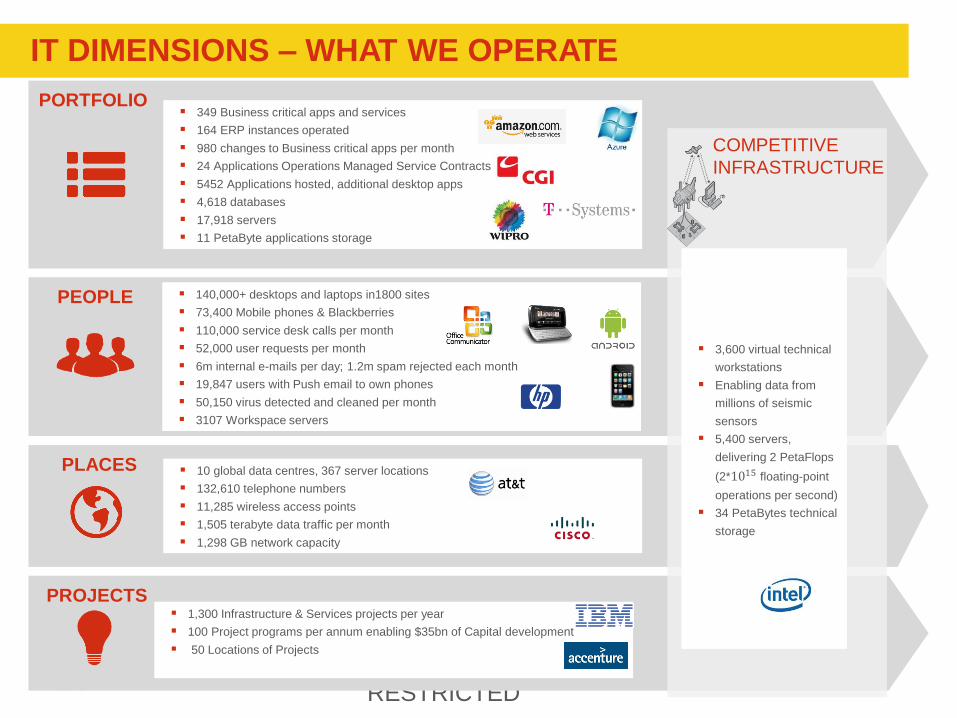

IT DIMENSIONS – WHAT WE OPERATE

RESTRICTED

PLACES 10 global data centres, 367 server locations

132,610 telephone numbers

11,285 wireless access points

1,505 terabyte data traffic per month

1,298 GB network capacity

PEOPLE 140,000+ desktops and laptops in1800 sites

73,400 Mobile phones & Blackberries

110,000 service desk calls per month

52,000 user requests per month

6m internal e-mails per day; 1.2m spam rejected each month

19,847 users with Push email to own phones

50,150 virus detected and cleaned per month

3107 Workspace servers

PORTFOLIO 349 Business critical apps and services

164 ERP instances operated

980 changes to Business critical apps per month

24 Applications Operations Managed Service Contracts

5452 Applications hosted, additional desktop apps

4,618 databases

17,918 servers

11 PetaByte applications storage

PROJECTS 1,300 Infrastructure & Services projects per year

100 Project programs per annum enabling $35bn of Capital development

50 Locations of Projects

COMPETITIVE

INFRASTRUCTURE

3,600 virtual technical

workstations

Enabling data from

millions of seismic

sensors

5,400 servers,

delivering 2 PetaFlops

(2*1015 floating-point

operations per second)

34 PetaBytes technical

storage

Copyright of Shell International BV

WHAT IS IT4IT ANYWAY?

Copyright of Shell International BV

IT4IT - THE BUSINESS OF MANAGING IT

“Would you run a listed company without

an integrated IT solution like an ERP?”

October 20, 2015 52© Shell International BV March 15, 201652

Copyright of Shell International BV

IT SERVICE

IT’S CORE ISSUE: MOST OF OUR FOCUS GOES INTO

DELIVERY, NOT NEARLY ENOUGH INTO OUTCOME

Manage Capabilities People, Process, Information, Tools

Measure Outcomes Metrics, Actions, Improvements

Plan BuildOperat

eDeploy Retire

Copyright of Shell International BV

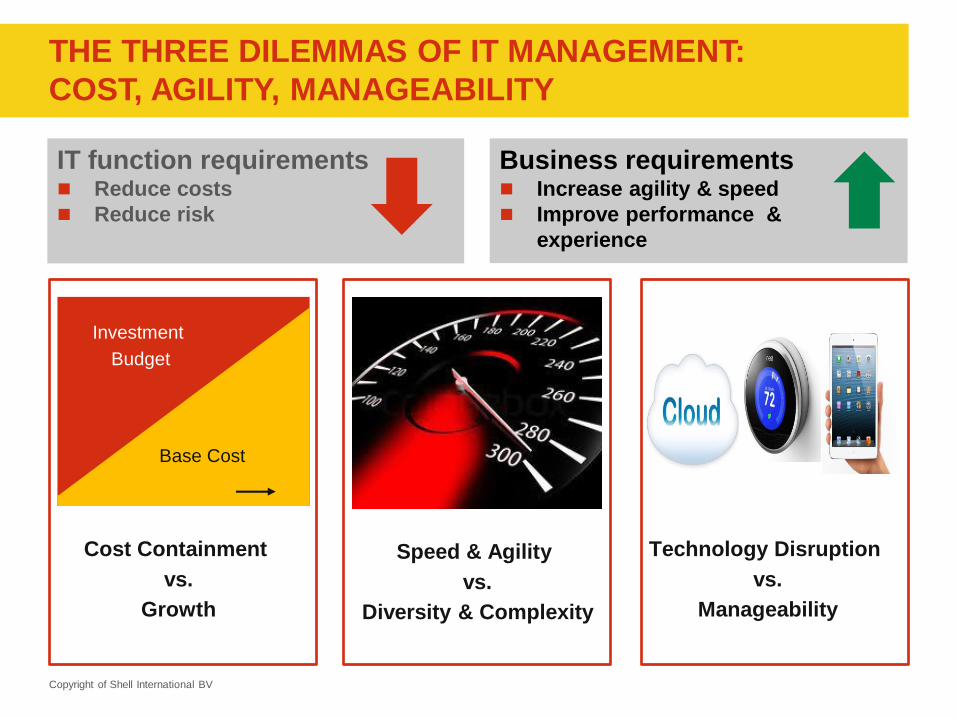

THE THREE DILEMMAS OF IT MANAGEMENT:

COST, AGILITY, MANAGEABILITY

Speed & Agility

vs.

Diversity & Complexity

Technology Disruption

vs.

Manageability

Cost Containment

vs.

Growth

Base Cost

Investment

Budget

IT function requirements Reduce costs

Reduce risk

Business requirements Increase agility & speed

Improve performance &

experience

Copyright of Shell International BV

CONSORTIUM CREATED END-TO-END VALUE CHAINS

plan build deploy run

Copyright of Shell International BV

SUMMARY: BETTER, FASTER, AFFORDABLE,

CONTROLLED

• Integrated workflows improving the quality of delivery

• Reduced downtime

• Operations become a “broker of services”

BETTER

• Agile development and DEVOPS

• Improved Project execution

• More self-service

FASTER

• Reduces cost for IT4IT (integration / sourcing options)

• Reduce overall IT costAFFORDABLE

• Improved understanding of and response to risks & threats

• Enhanced monitoring and exception handlingCONTROLLED

And we believe we can achieve this through a holistic approach to IT4IT

Copyright of Shell International BV

SHELL IT4IT JOURNEY

Copyright of Shell International BV

COMMUNITY DEVELOPMENT – AN EVOLUTIONARY

MODEL

Shell proprietary Standard Open Industry Standard

2010: Delivery Model 2012: Segment Architecture 2014: Reference Architecture

2012/09: Consortium kicked off PWC, HP-IT, ING, Munich Re, HP-SW,

Achmea, later extended with AT&T,

Accenture, USF

2013-2016: Continued Growth of

consortiumOver 40 Members at time of this presentation

2013/10: Open Group First affiliation discussions

2014/10: Public launch at

The Open Group IT4IT

forum and standard

2015/06: V2.0

Copyright of Shell International BV

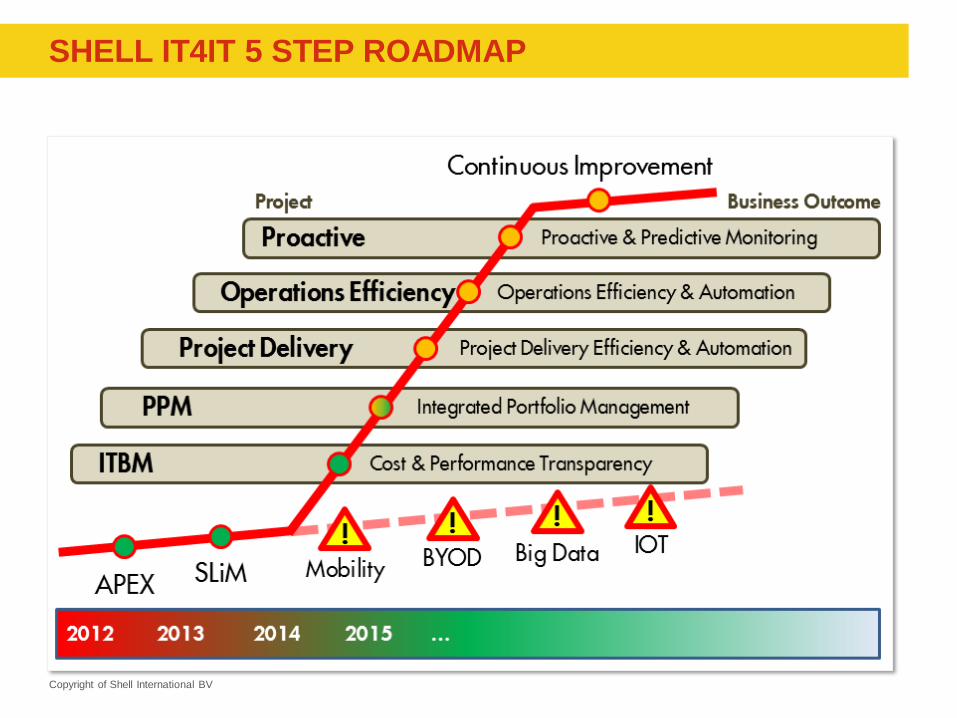

SHELL IT4IT 5 STEP ROADMAP

Copyright of Shell International BV

RETURN TO THE ‘COMPACT IT ESTATE’ WITH COST

TRANSPARENCY

IT BUSINESS MANAGEMENT

Application

overview

IT Management Information

Project

Overview

Infrastructure

overview

Infrastructure

optimization

TRUSTED DATA SOURCES

Config

ManagementApplications/

ServicesProjects

Application/

service costs

Infra

Invoice DataUtilization

Budget

ActualsERP

#oilgasict

Christopher RivinusTullow Oil

Culture Eats Strategy for Breakfast

March 2016

“Culture Eats Strategy for Breakfast”- Mark Fields – 2006

Background in Anthropology

Characteristics of Culture

• Pernicious: acts through people who come and go

• Rewards those who protect it and perpetuate it

• Culture tolerates policy, governance, new process

• …Or rejects it

• Has mechanisms that help it evolve/survive

• Has trigger points for change

• Culture and policy dual for influence….unless they are aligned.

Framing the Problem Set

IS Leadership Group is diverse

Varied IT savvy

Cultures from 3 continents

Domain of expertise vary

Not culture of statistics

Few time motion studies

No framework for ROI

Executives don’t have time

We have them for 1 hour per month

Don’t have time for homework

Decision culture dominated by desire for broad/input consensus

67

Tullow IS Solution

Has to start good debate - at a glance

Has to provide right contextual understanding for decisions/debate

Has to enable a decision at the right level of specificity

Can’t imply scientific process where it doesn’t exist

Must empower appropriate challenge between executives

Must place the executives in complete control

Not asking for their opinion

Asking them for approval to spend their money

All plots must have narrative about notional 125% ROI

No hard ROI calculation required

But a good narrative is

68

Scoring Strategic Fit

69

Scoring Strategic Fit – Cont.

70

Scoring Ease of Implementation (Risk)

71

Basic Result

72

Why It Worked

Right level of detail for contextual understanding Considering the time available

Considering varied IT savvy

Provides confidence to act

Compares RELATIVE strategic fit and RELATIVE ease of implementationGroup chooses spending limits

Produces quadrant to focus attention/debate

Ensures debate leads directly to spend decisions

VisualAbility to focus quickly on areas for debate and decision

Matches their allotted time to the task

Forum allows for broad participation

Decision method infers consensus

Format minimizes time investment required

73

Take-Away – Guiding Principles

• Simplicity– Level of specificity must match the level of accuracy

– Use only attributes that the group can make decisions on

• “Snap-shot” decision making– Visual with data and text detail as backup

– If they haven’t read anything….can they still contribute to a decision?

• Trust their gut– Create ability to do a deep dive into areas that don’t “feel right”

– Details can (not always by any means) confound judgement

– IT facilitates decision making – leads from the back

Hidden value: nearly all initiatives have some IT component… our solution brings the strategy debate to IT, as opposed to asking for a seat at a table in the next room.

74

#oilgasict

Questions & Discussion

#oilgasict

Breakout SessionsPlease check

back of badge

#scotsecure

Our Next Event

#oilgasict

James McLeanConocoPhillips

IT StrategyDeveloping an IT Strategy for a low cost environment

James McLeanIT Manager, UK

March 17, 2016

80

Content

Drivers for a strategy formation

• Business outcome driven: Are you aligned to your business strategy?

• Understand your capabilities: Are you able to deliver?

• Sourcing strategies: How do you deliver whilst remaining agile and scalable?

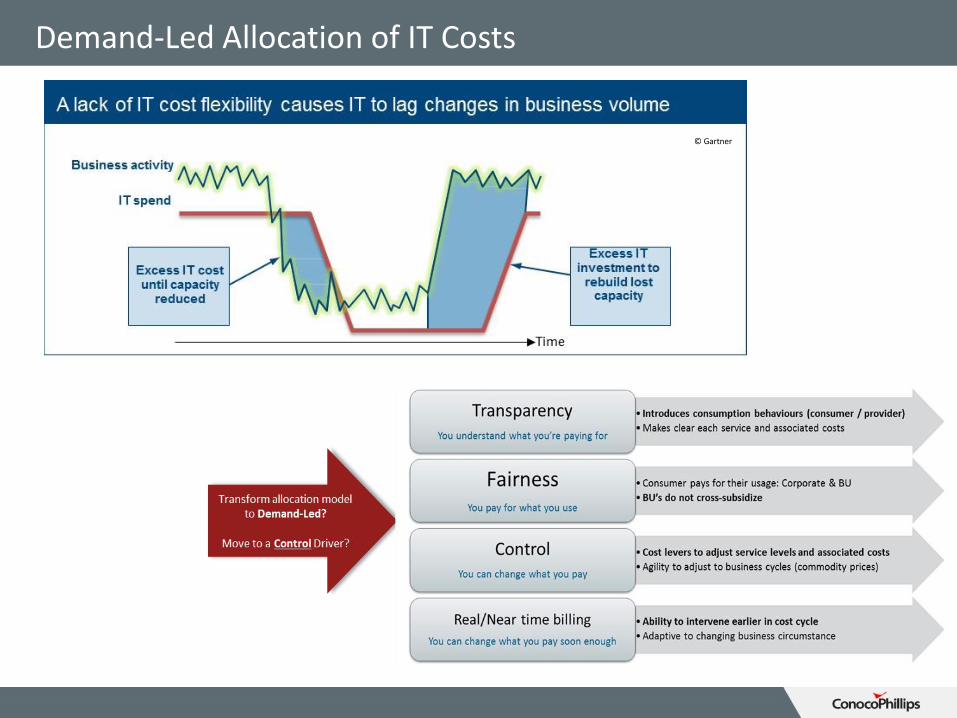

• Demand led: Should your charge model reflect cost dynamics?

Drivers for an new IT Strategy Formation

• Industry Drivers

• Oil price volatility

• Decommissioning is essentially a new business in the UK industry

• Steadily Declining Production

• Aging fields/assets

• Successive cost reduction rounds and the need to operate differently

• IT Drivers

• Headcount and Cost constraints

• Doing more with less

• IT Industry driving to the Cloud as a transformative capability

• Drivers for a strategy formation

Business outcome driven: Are you aligned to your business strategy?

• Understand your capabilities: Are you able to deliver?

• Sourcing strategies: How do you deliver whilst remaining agile and scalable?

• Demand led: Should your charge model reflect cost dynamics?

An Approach for Developing Strategic Alignment

Business change well understood

IT implications identified

Understand Business Demand

Business Capabilities

IT Implications

Business & Market Context

Determine Strategic Direction

Vision

Strategic Objectives

Change Requirements

Vision and strategic objectives

Role of IT

IT operating model

Assess Capabilities

People

Process

Technology

Current state understood and aligned internally

Determine Required Actions

Control

Supply

Risks & Issues

Future state described in terms of impacts on the Business of IT capabilities

Imp

lem

ent

Develop Roadmap

Projects/Program

Timeline and Resources

Communication

Roadmap and action plan defined

Strategic direction communicated and accepted within business and IT

The Enterprise Context serves as a strategic planning tool for summarising, agreeing upon and analyzing the consequences of the main business strategies and their consequences on business change

Understand Business Demand

Business Capabilities

IT Implications

Business & Market Context

Gartner Nexus of Forces Model

© Gartner

Approach to Understanding Business Demand

• Interviews with the key business stakeholders

• CFO

• BU/department heads

• ...

Business change well understood

IT implications identified

Understand Business Demand

Business Capabilities

IT Implications

Business & Market Context

Anchor model of the businessBusiness capability model

Guiding Principals

© Gartner

• Drivers for a strategy formation

• Business outcome driven: Are you aligned to your business strategy?

Understand your capabilities: Are you able to deliver?

• Sourcing strategies: How do you deliver whilst remaining agile and scalable?

• Demand led: Should your charge model reflect cost dynamics?

Approach to Assessing Capabilities

Assess Capabilities

People

Process

Technology

Current state understood and aligned internally

ITIL framework can provide structure

Deliver Change

Business Relationship Management

Service Operation

Operational Management

Service Desk

Capacity

Management

(design)

Request fulfilment

Change

Management

(FSOC)

Config/Asset Mgmt

Identity

Management

Security Monitoring

Incident Control

2nd/3rd line support

Apps Dev/ SDLC

Boundary &

Feasibility

PPM

PMO

Impact AssessmentIM-enabled

Business Change

Delivery Portfolio

Planning

Event Management

IM Management

Design

Solution Delivery

Strategic Alignment

TfL IM Demand

Harmonisation

Reporting and

Communication

Establish IM

Success Criteria

IM Budget setting

Transition

Applications

TTO/ Service

Introduction

Operational

Testing

Apps Maintenance

Services (AMS)

Apps Mgmt (SAM)

Financial and Commercial

Performance and Resourcing

Security, Risk, Compliance

Strategy and EA

Procurement/

Sourcing

Workforce

Management

IM Function

Financial Planning

Vendor

Management

Service KM

IM Strategic Planning EA

Cyber Security

(policy/

requirements)

Risk Management and

Control

Performance

monitoring

Projects and Change

BRM/ demand

management

(projects)

Demand sensing/

shaping Business Analysis

Business As Usual BRM

Requests for

Service

Capacity

Management

(forecast)

IM-based

Changes

Problem

Management

Incident

Management

Fin Mgmt for IM

Services

Agree IM Strategy

Service Portfolio

ManagementStandards

Compliance and Audit

BU Investment

Portfolio Management

High Level Example: Capability view of an IT Organisation Level 0+1

Application Support

Consultancy

Application Development

Application Support

Database Support

Enterprise Content Management

Project Management

Administration

Application Development

Application Development

Business Intelligence

Application Support

Project Management

Administration

Business Partner

Business Analysis

Project Management

Change Management

Asset Management

Administration

Data Services

Data Management

Physical and Digital Record Management

Compliance

Advisory

Strategy

Project Management

Technical Reprographics

Administration

Planning, Control and Compliance

Service Portfolio Management

Stakeholder Management

Governance

Strategy

Planning and Control

Compliance

Administration Support

Infrastructure Operations

Compliance

Consultancy

Strategy

Operational Support

Project Management

Administration

Project Management

Solution Design

Project Planning

Budget Management

Project Delivery

L0

L1

Future State Example of IT Capabilities – Level 0 + 1

Strategy and Planning Service Development Service Management Business Relationship

Management

Information Management

Business

Enablement

Strategy

Business

Performance

Planning

Demand

Management

Communications

Planning

Stakeholder

Management

Business

Performance

Management

Information

Management

Strategy

Information

Architecture

Information

Resource

Management

Content

Management

Business

Intelligence

Record

Management

Project & Program

Management

Enterprise

Architecture

Portfolio

Management

Human Resources

Management

IT Financial

Management

Vendor

Management

IT Strategy

Management

Service

Architecture

Service Operation

Solutions

Development

Infrastructure

Development

Service Transition

Service Delivery

Service Design

Service Strategy

IT Risk &

Compliance

L0

L1

Strategy and Planning

Enterprise

Architecture

Portfolio

Management

Human Resources

Management

IT Financial

Management

Vendor

Management

IT Strategy

Management

IT Risk &

Compliance

• Drivers for a strategy formation

• Business outcome driven: Are you aligned to your business strategy?

• Understand your capabilities: Are you able to deliver?

Sourcing strategies: How do you deliver whilst remaining agile and scalable?

• Demand led: Should your charge model reflect cost dynamics?

How to Deliver and Remain Agile

• Flexible to adapt to volatility• Use of small boutique companies on turnkey activities

• Identify commodity services and execute at lowest costs possible

• Never sacrifice stable IT operations

• Is it differentiating?

• Know what you are investing in for the long term• Long term planning allows for strategic adjustments through volatility periods

• Stay the course on the differentiating services

• Flexible workforce• Agile

• Scalable +/-

• Drivers for a strategy formation

• Business outcome driven: Are you aligned to your business strategy?

• Understand your capabilities: Are you able to deliver?

• Sourcing strategies: How do you deliver whilst remaining agile and scalable?

Demand led: Should your charge model reflect cost dynamics?

Demand-Led Allocation of IT Costs

© Gartner

#oilgasict

Alex NicholsonNetApp

Internet of Things

Supporting Business Objectives in the Oil and Gas Industry

Alex Nicholson

Business Development Manager

15th March 2016

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use9

6

Made in a minute….

From the beginning of recorded time until 2003, 5 billion gigabytes of data was created

In 2011, the same amount was created every two days

In 2013, the same amount is created every 10 minutes

Today the same amount is created every minute of every day

DATA NEVER SLEEPS 2.0 (DOMO)

Source: DOMO https://www.domo.com/blog/2014/04/data-never-sleeps-2-0/© 2015 NetApp, Inc. All rights reserved.

NetApp Proprietary – Limited Use Only9

7

http://www.internetlivestats.com/

Change is essential…

Only 12% survived from 1955 to 2016

© 2015 NetApp, Inc. All rights reserved.

NetApp Confidential – Limited Use 9

8

Fortune 500 in 2016 but not in 1955

Fortune 500 in both 1955 and 2016

Fortune 500 in 1955 but not in 2016

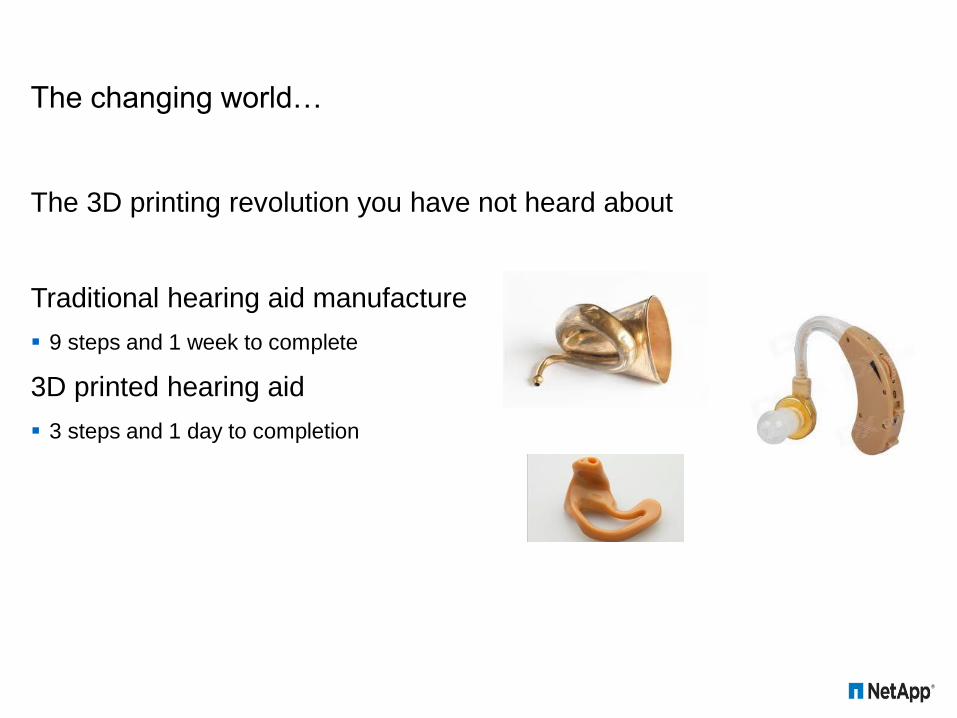

The changing world…

The 3D printing revolution you have not heard about

Traditional hearing aid manufacture

9 steps and 1 week to complete

3D printed hearing aid

3 steps and 1 day to completion

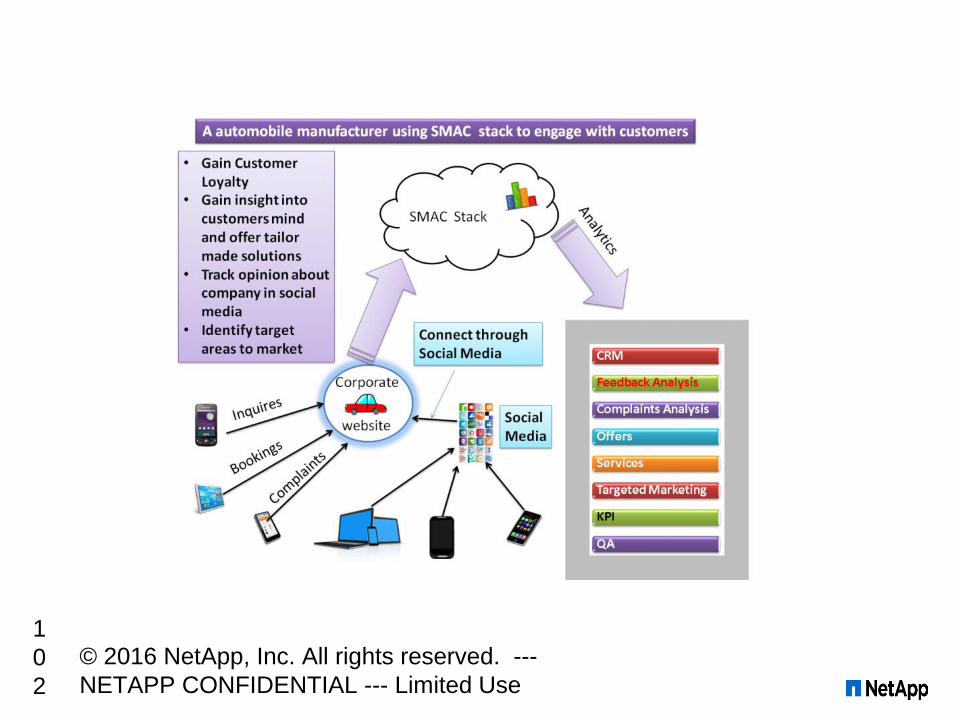

The changed world…

New business for new business

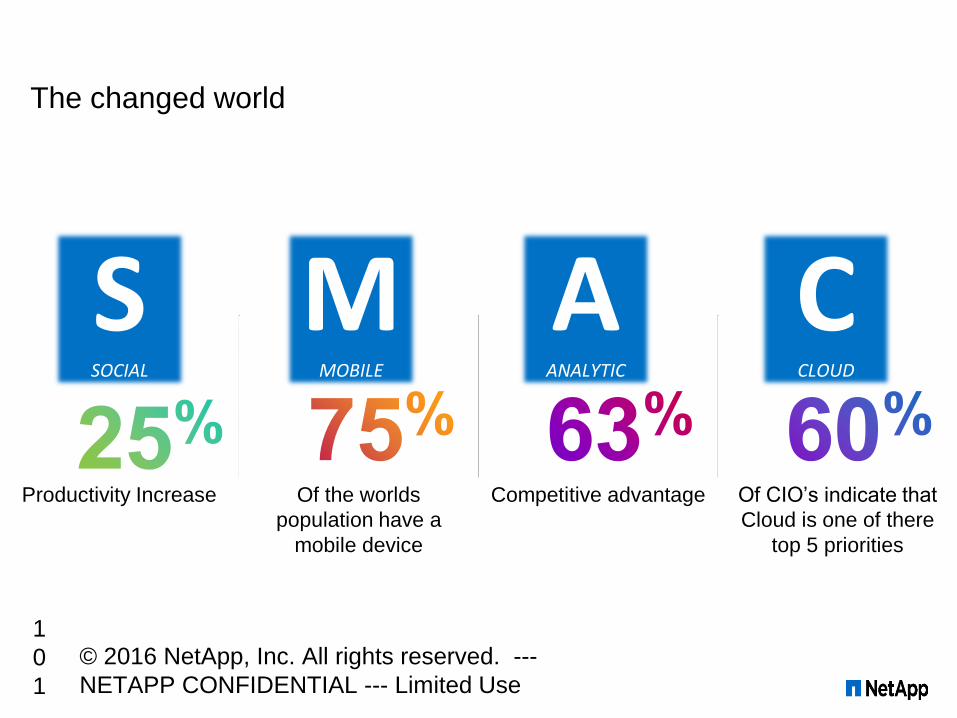

The changed world

Productivity Increase Of CIO’s indicate that

Cloud is one of there

top 5 priorities

Competitive advantageOf the worlds

population have a

mobile device

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use

1

0

1

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use

1

0

2

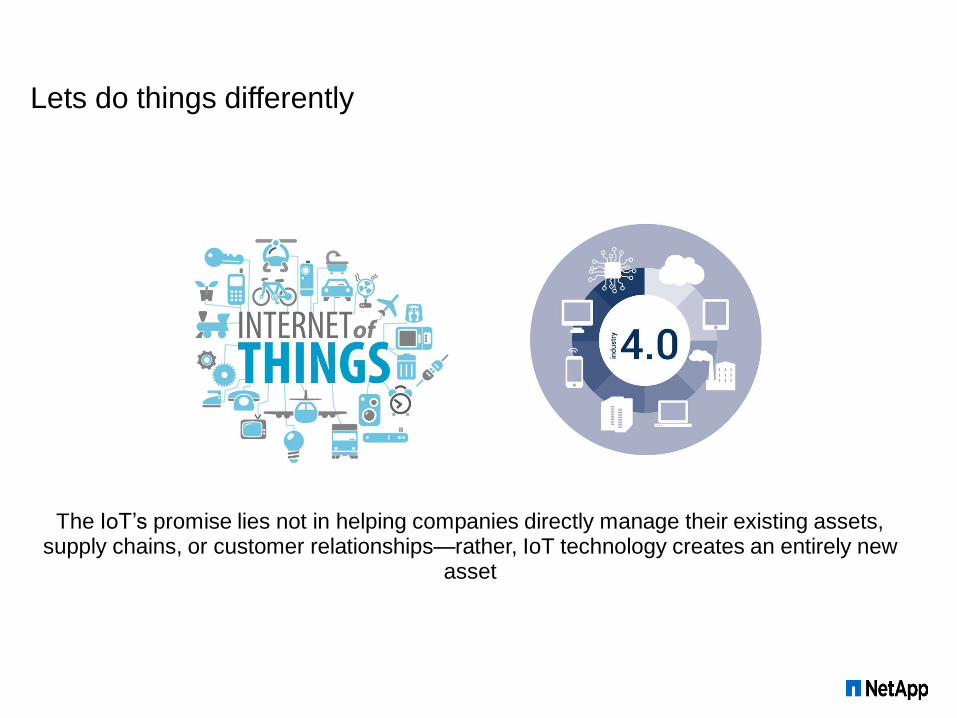

Lets do things differently

The IoT’s promise lies not in helping companies directly manage their existing assets, supply chains, or customer relationships—rather, IoT technology creates an entirely new

asset

What are “things”50 Sensor Applications for a Smarter World

http://www.libelium.com/top_50_iot_sensor_applications_ranking/© 2015 NetApp, Inc. All rights reserved.

NetApp Proprietary – Limited Use Only

1

0

4

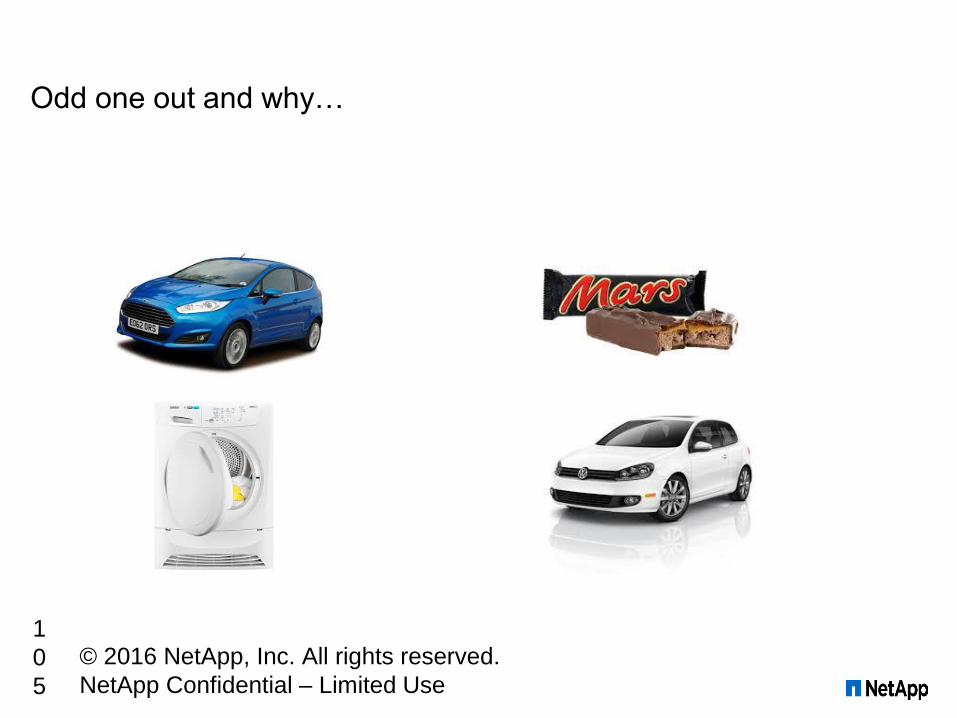

Odd one out and why…

© 2016 NetApp, Inc. All rights reserved.

NetApp Confidential – Limited Use

1

0

5

Connected Barrel

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use

1

0

6

If Carlsberg did IoT

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use

1

0

7

Have I got news for you…Odd one out and why…

© 2015 NetApp, Inc. All rights reserved.

NetApp Confidential – Limited Use

1

0

8

Right turn policy introduced in 2004

Increased profits, reduced emissions and accidents

Increased number of parcels delivered on an annual basis by 15.8 million

Reduced vehicle travel by 20.4 million miles

Reduced gas consumption by 10 million gallons

Reduced emissions by 20,000 metric tonnes each year.

Supply chain managementRight turn policy

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use

1

0

9

Have I got news for you…Odd one out and why…

© 2015 NetApp, Inc. All rights reserved.

NetApp Confidential – Limited Use

1

1

0

Final thoughts…Odd one out and why…

© 2015 NetApp, Inc. All rights reserved.

NetApp Confidential – Limited Use

1

1

1

© 2016 NetApp, Inc. All rights reserved. ---

NETAPP CONFIDENTIAL --- Limited Use

1

1

2

Thank You.

#oilgasict

Welcome Back

#oilgasict

Angus MurrayTAQA

Progressing the vision for change

Angus Murray, Head of IT, TAQA @RamblingGeek

Alan Norrie, IT Lead – Infrastructure and EUC @Alan_Norrie

115©tampnet

Recap from 2015 – ICT as an enabler

The Levers for Change

Challenging the Statics – Upgrade or Die

Enabling Technologies

Collaboration – Supply Chain

Timing is everything.

March 2016 @RamblingGeek 116

The Results…

• Operational IT costs

• 2015 actuals vs 2014 actuals, 30% reduction

• 2016 forecast vs 2015 actuals, 9% further reduction

• Forecast 2016 vs original 2014 budget, 40% reduction

March 2016 @RamblingGeek 117

• CAPEX Reduction

• 2015 actuals vs 2014 actuals, 50% reduction

• Risk Management is key – technology debt.

What we didIdentification – Own it, push the limits.

March 2016 @RamblingGeek 118

Identifying the LEVERS

High Cost items/Scope to change

Supply Chain Partnering –the limits of hammering rates-squeezing the balloon

Retendering -time to deliver

Timing is everything

Challenging the statics

Ownership

DO-IT, Measure it. What gets measured gets done

Taking 6 months just doubled your target!

10% cut straight away ( same as 20% in June!) – get after it

Upgrade or die… manage your risks

Software and maintenance, license count….

Bottom up, own the cost, own the saving

10/20/30%... 30 % option key – imagine the impossible

Not waiting for the axe to fall… own it

Savings tangible, SMART, linked to budget codes

Examples

Offshore bandwidth – Work Smarter

Market Test – Do more with less

In-source, out-source, right source-take control

Sub Surface Licencing

Discretionary effort

Retender – if your not willing to work with us, we check the market

Shift Left – Challenge the norm.

March 2016 @RamblingGeek 119

Alan Norrie

IT Lead – Infrastructure & EUC

@alan_norrie

#ShiftLeft

Market Test – Thinking outside the box

March 2016 @Alan_Norrie 121

Service Desk

Desktop Support

Server/Storage

Support

Networks Support

Applications Support

Software VendorsSoftware Vendors

Software Vendors

Software VendorsSoftware Vendors

Hardware Vendors

ERP Support

Database Support

1st Line Support 2nd Line Support 3rd Line Support

Operations Centre

Telecoms Support

Renegotiate Retender

Commodity

Strategic/Core Strategic/Core

Commodity

Shift Left – A smart way to drive down cost

March 2016 @Alan_Norrie 122

1st Line 2nd Line 3rd Line

Shift Left

Commodity Commodity/Strategic Strategic/Core

The Business

Strategic/Core

• Worked with our supplier to implement the change, not at them

• Merged Service Desk and Desktop Support – Technical Service Desk

• Established SMEs within Service Desk – Infrastructure, Apps & Networks

• Formalised KB Framework for 2nd and 3rd line teams

• Prioritise workloads (Do less, better)

Incidents, requests, problems, CSIs

• Continual Service Improvement – Objective is to reduce incidents.

2015 – The Numbers

March 2016 @Alan_Norrie 123

0%

20%

40%

60%

80%

100%

120%

£-

£0

£0

£0

£0

£0

£0

£0

1 2 3 4 5 6 7 8 9 10 11 12

Perf

orm

an

ce

Co

st

Series2 Series1 Series3 Series4

IT Leadership Meeting

Transitioned from Managed Service to ‘Hybrid’ T&M

Formalised ‘Shift Left’ & Established Technical Service Desk

The Customers

February 2016 124

2014

2015

Shifting Left

Conclusions

There are savings there, but we all need to make the effort

Rate cuts don’t cut it! Part of the solution, but not game changing

Right sourcing will be key (complicated managed services-tail wagging the dog)

Ownership (bottom up) is key to most sustainable savings

Need to make this a sustainable industry

Aberdeen bubble needs to burst

IT more susceptible to global players

We are all competing Globally

February 2016 125

#oilgasict

Steven WardIT Consultant

Leadership in Times of Crisis:

How to avoid unnecessary casualties

Steven Ward BSc(Hons) PgDip MBCS MCMI

Agenda :

• In times of crisis, what makes the right sort of leader

• The importance of avoiding stress for your team...and you

• “Directors are Divas”

• Learning from other industries

• In the eye of the storm

• Generous applause (possible standing ovation)

Fit’s the loon sayin?

Famous Geordies

Bryan Johnson – singer with AC/DC

Famous Geordies

Bryan Johnson – singer with AC/DC

This former English teacher

Famous Geordies

Bryan Johnson – singer with AC/DC

This former English teacher

Cheeky scamps - Ant and Dec or Ant

Famous Geordies

Bryan Johnson – singer with AC/DC

This former English teacher

Cheeky scamps - Ant and Dec or Ant

And of course ... Jimi Hendrix

Famous Geordies

OK, not Jimi Hendrix – Jimmy Nail

Famous Geordies

OK, not Jimi Hendrix – Jimmy Nail

...but definitely this great man

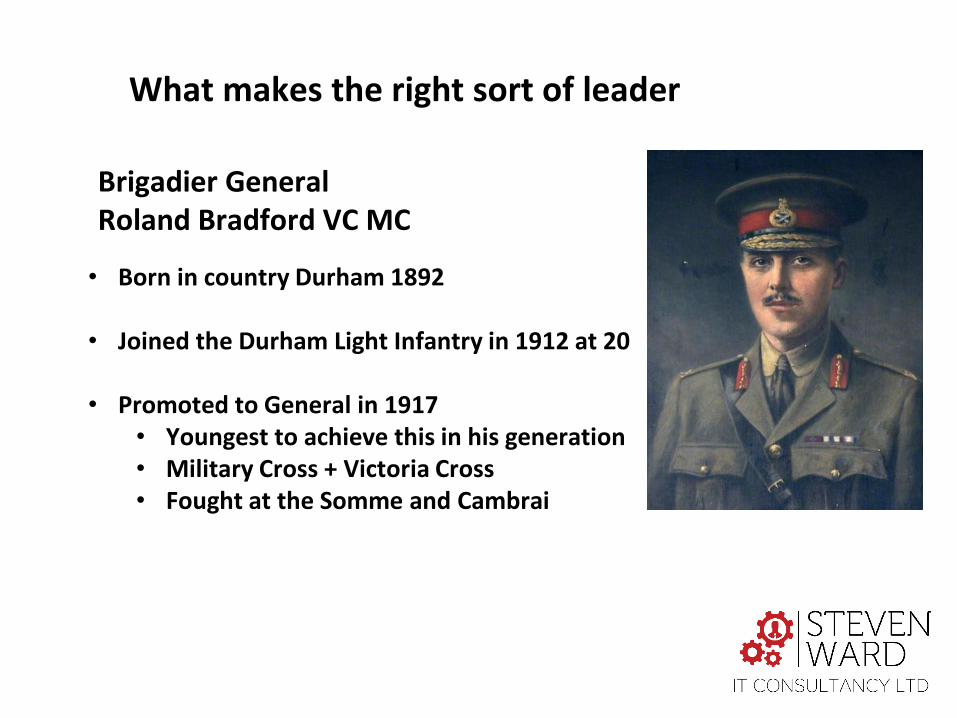

What makes the right sort of leader

What makes the right sort of leader

Brigadier GeneralRoland Bradford VC MC

• Born in country Durham 1892

• Joined the Durham Light Infantry in 1912 at 20

• Promoted to General in 1917• Youngest to achieve this in his generation• Military Cross + Victoria Cross• Fought at the Somme and Cambrai

The importance of avoiding stress for your team ...and you

The importance of avoiding stress for your team ...and you

Effects of Stress

Combatting Stress

Combatting Stress

Supporting your team

Supporting your team

Supporting your team in 1917

“Directors are Divas” Knowing how and why to protect your budget

What is it you do anyway?

Roland’s Directors

Learning from other industries

Learning from other industries

Learning from other industries

Recall of 1 million tyres

Learning from other industries

Recall of 1 million tyres

Daruma Doll

Learning from other industries

Recall of 1 million tyres

Daruma Doll

Learning from other industries

Learning from other industries

Blackmailed

In the eye of the storm – what should you be doing right now

Sound advice

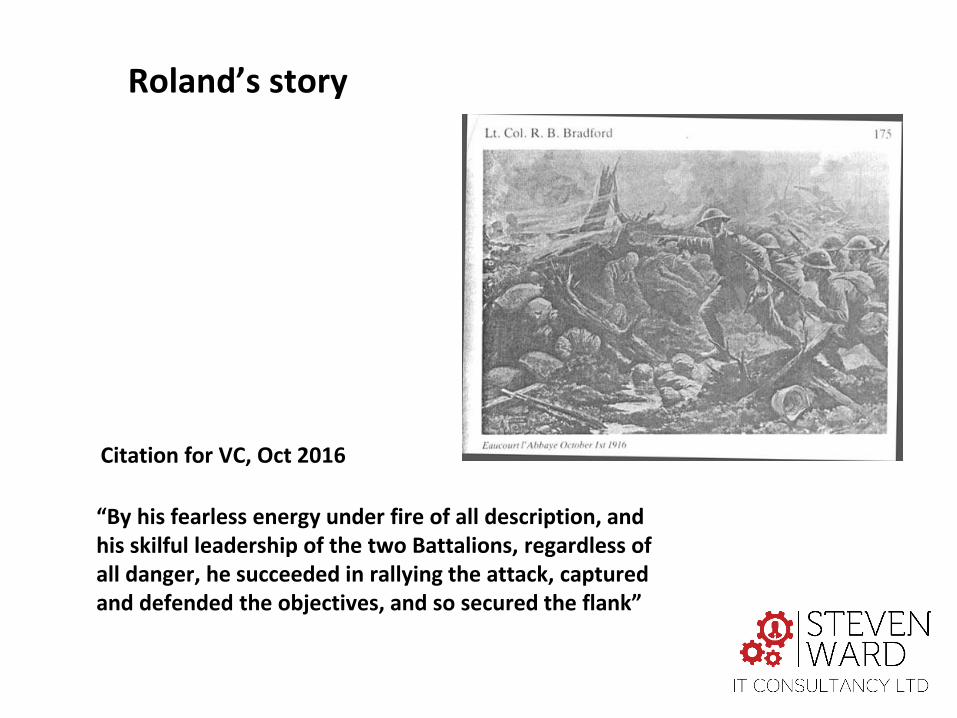

Roland’s story

“By his fearless energy under fire of all description, and his skilful leadership of the two Battalions, regardless of all danger, he succeeded in rallying the attack, captured and defended the objectives, and so secured the flank”

Citation for VC, Oct 2016

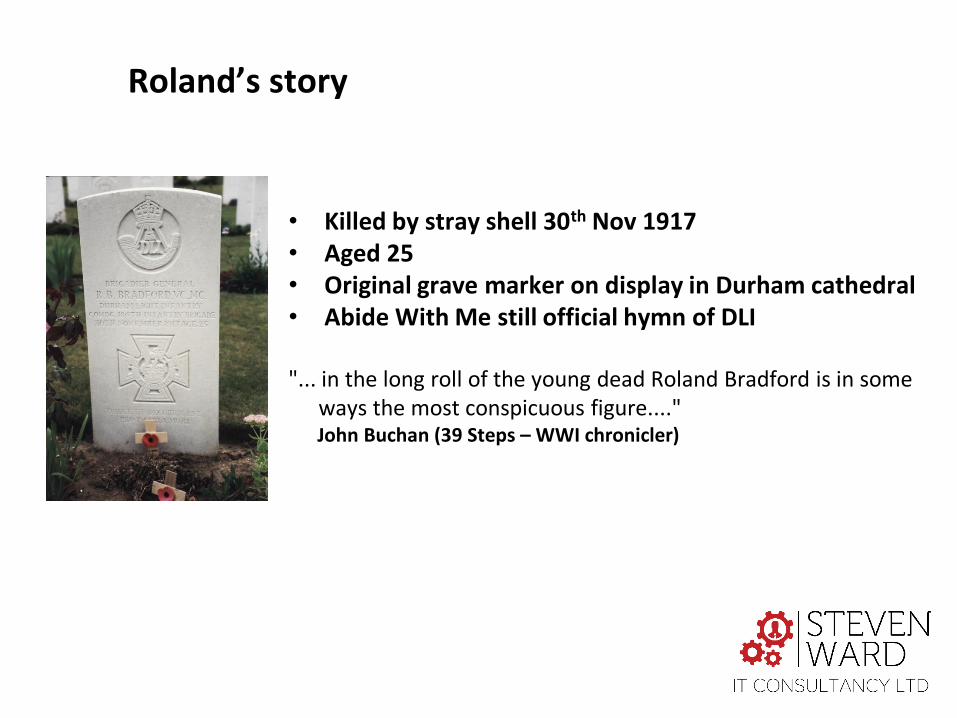

Roland’s story

• Killed by stray shell 30th Nov 1917• Aged 25• Original grave marker on display in Durham cathedral• Abide With Me still official hymn of DLI

"... in the long roll of the young dead Roland Bradford is in some ways the most conspicuous figure...." John Buchan (39 Steps – WWI chronicler)

Thank You

(Graciously accept polite applause / standing ovation)

Blatant plug……

You’ve been a great audience

#oilgasict

Chris PlessCAN Offshore

#oilgasict

Questions & Discussion

#oilgasict

Drinks & Networking sponsored by

#oilgasict

Paul PhillipsNutanix

Oil & Gas ICT Summit

Paul Phillips – Regional Vice President – Western Europe

167

No Business is Immune to the Winds of Change

• 2015 has been a difficult year

• Increased pressure on budgets

• Industry is changing, continued acquisitions and mergers

• Innovation more important than ever

• Infrastructure refresh drives efficiency

168

• IT is touching end-users directly, like never before, IT has to become a business enabler.

No Business is Immune to the Winds of Change

169

Is it possible to escape the winds of change?

170

Is Hyper-convergence enough?

• IT has to innovate continuously and relentlessly

171

iPhone Converged Several Consumer Devices

172

=

For the Data Center

The Nutanix Opportunity

173

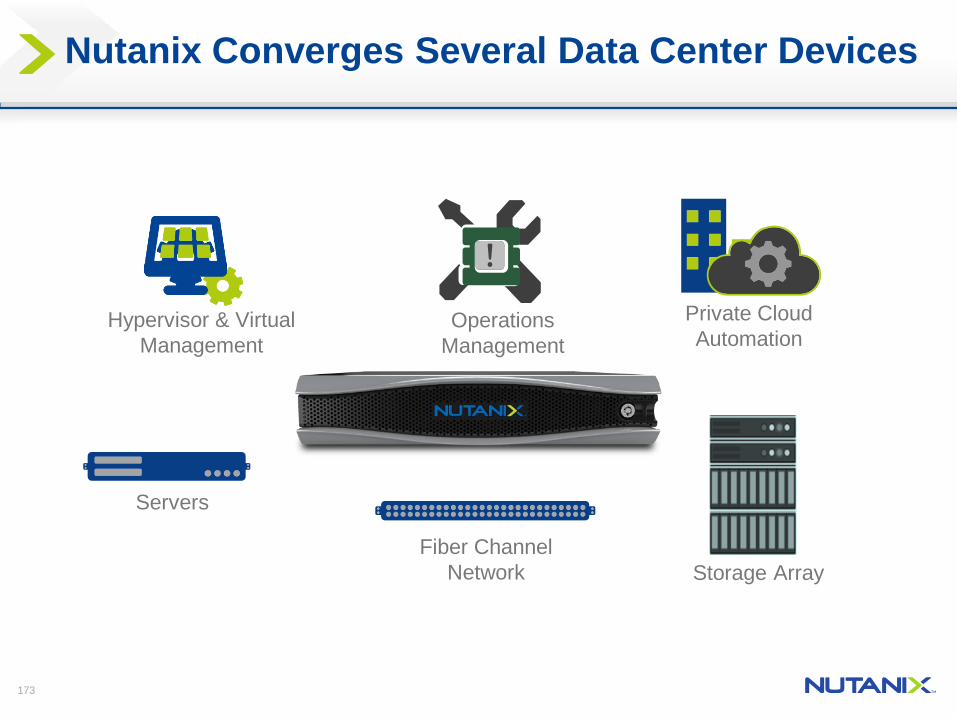

Nutanix Converges Several Data Center Devices

Private Cloud

Automation

Fiber Channel

Network Storage Array

Servers

Operations

Management

Hypervisor & Virtual

Management

174

Just Works

Invisible …

175

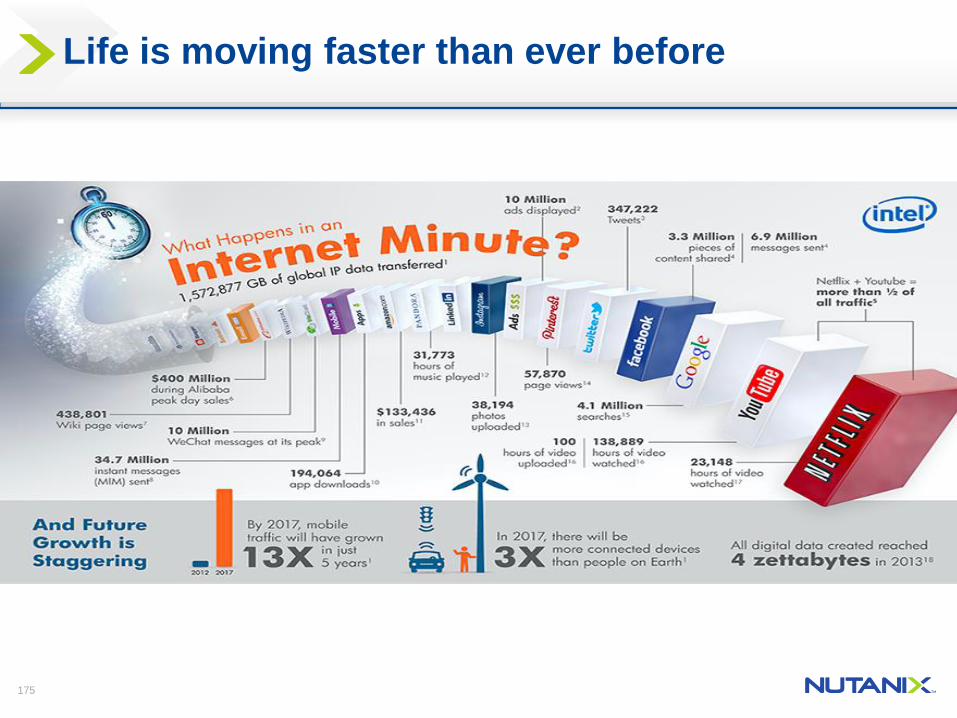

Life is moving faster than ever before

176

Web-Scale DatacentersSimple, Scalable, Efficient

Design Principles

• Unbranded x86 servers: fail-fast systems

• No special purpose appliances

• All intelligence and services in software

• Extensive automation and rich analytics

• Distributed everything

Benefits

• Linear, predictable scale-out

• Always-on systems

• Fast innovation in software

• Operational simplicity

• Lower TCO

177

LUNs

Zoning

Masking

FCoE

Backplane

Blade chassis

FCAL

Multipathing

HBA

FC SwitchvC

ente

r

Ora

cle

SQ

L S

erv

er

vR

ealiz

e

Auto

mation

SR

M,

SR

A

vR

ealiz

e O

ps

Manag

em

ent

EV

O:R

AIL

Isilon

VSPEX Blue

Vblock

EVO:RACK

XtremeIO

VNXViPR

VxRACK

ScaleIO

DSSD

VMAX ECS

The Journey Towards Invisible Infrastructure

Complex is Competent, Simple Genius

178

Legacy Infrastructure Is Not Invisible

1. Inherent Complexity

2. Inefficient Silos

3. Forklift Scaling

179

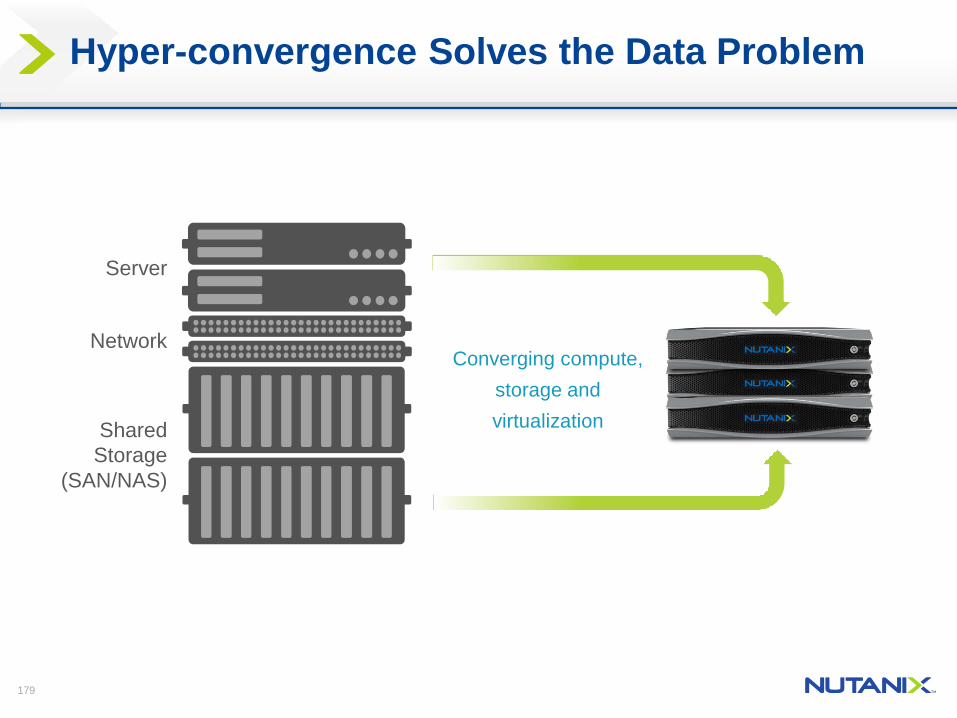

Hyper-convergence Solves the Data Problem

Converging compute,

storage and

virtualization

Server

Network

Shared

Storage

(SAN/NAS)

180

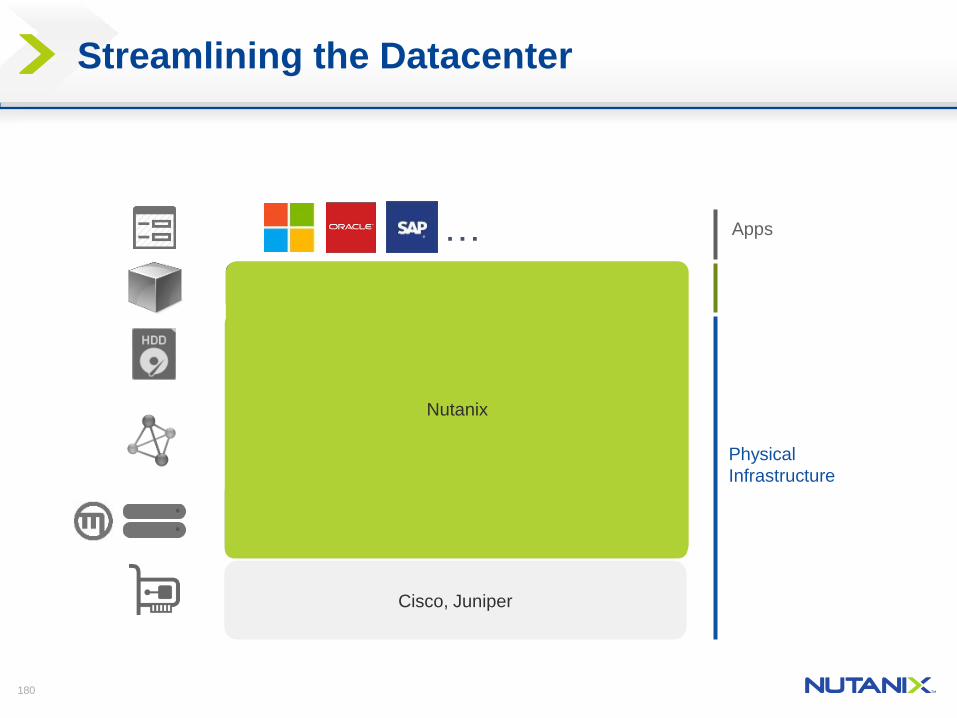

Streamlining the Datacenter

Cisco, Juniper

HP, Dell, Cisco

NetApp,EMC

Qlogic, Emulex

Vmware, Microsoft, Redhat

Cisco, BrocadePhysical

Infrastructure

Apps…

Nutanix

Nutanix

181

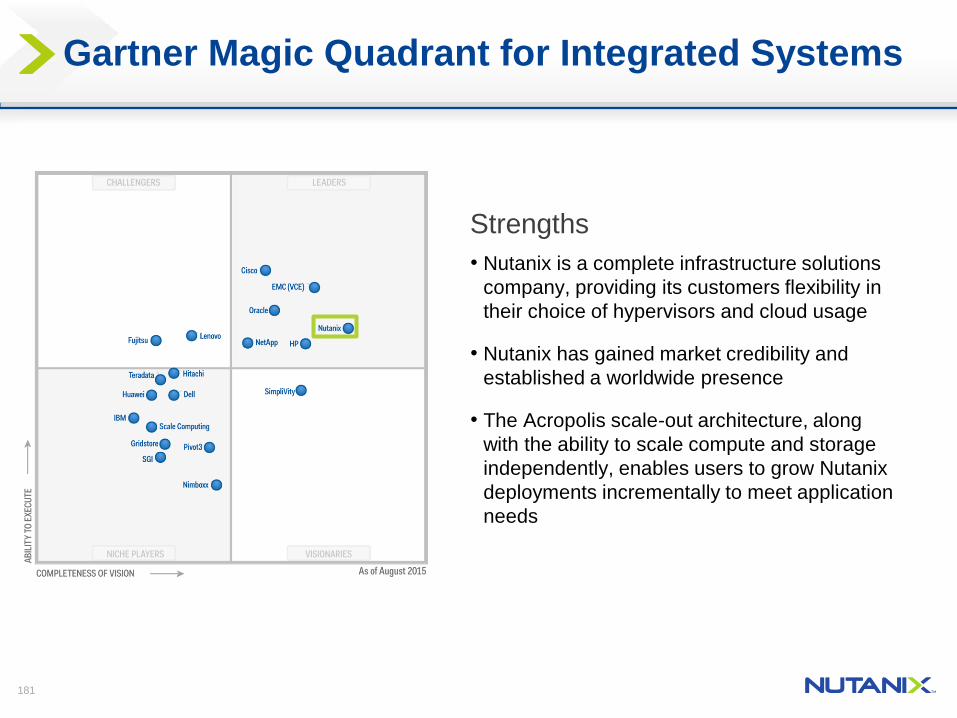

Gartner Magic Quadrant for Integrated Systems

Strengths

• Nutanix is a complete infrastructure solutions

company, providing its customers flexibility in

their choice of hypervisors and cloud usage

• Nutanix has gained market credibility and

established a worldwide presence

• The Acropolis scale-out architecture, along

with the ability to scale compute and storage

independently, enables users to grow Nutanix

deployments incrementally to meet application

needs

182

Nutanix Xtreme Computing Platform

Make Cloud Invisible

Make Virtualization Invisible

Make Storage Invisible

The Journey To Invisible Infrastructure

183

Nutanix Product Families

Distributed Storage Fabric

App Mobility Fabric

Azure

VMware

ESXi

Microsoft

Hyper-VAWS

Acro

polisInfrastructure

Management

Operational

Insights

RemediationAcropolis

Hypervisor

Three Product Families: Nutanix Acropolis and Nutanix Prism

Xtreme Computing Platform

Prism

184

Tomorrow’s Hybrid App could live on Nutanix

Staging DRProductionDev/Test

Hybrid App Lifecycle

On-Premise On-PremiseCloud Cloud

The Need for a Web-Scale Operating System

185

75%

vs

Elasticity Predictability

25%

The Right Cloud for the Right Workload

186

Cloud

VMVM VM

Application Mobility Fabric

Public Cloud

On-prem

Owning vs renting

187

Nutanix in 30 Seconds

Invisible Infrastructure

Why What

Hyperconvergence

How

Web-Scale

Just

Works

Eliminates

Guesswork

Removes

Constraints

188

Brand Adoption in Energy

189

Support That Delivers

24X7X365

97%Customer

Satisfaction

45+Spare Parts

Depots

90+Net Promoter Score

“Follow the Sun” support

24X7X365

78Countries

12Languages

6Support Centers

1K Annual

Part Shipments

20K+Servers Supported

Thank You

#oilgasict

Welcome to Day 2

#oilgasict

Mark StephenBBC Scotland

#oilgasict

Prof John McCallRobert Gordon University

Data Analytics for Oil and Gas: Challenges and Opportunities

John McCallSmart Data Technologies Centre

Robert Gordon University

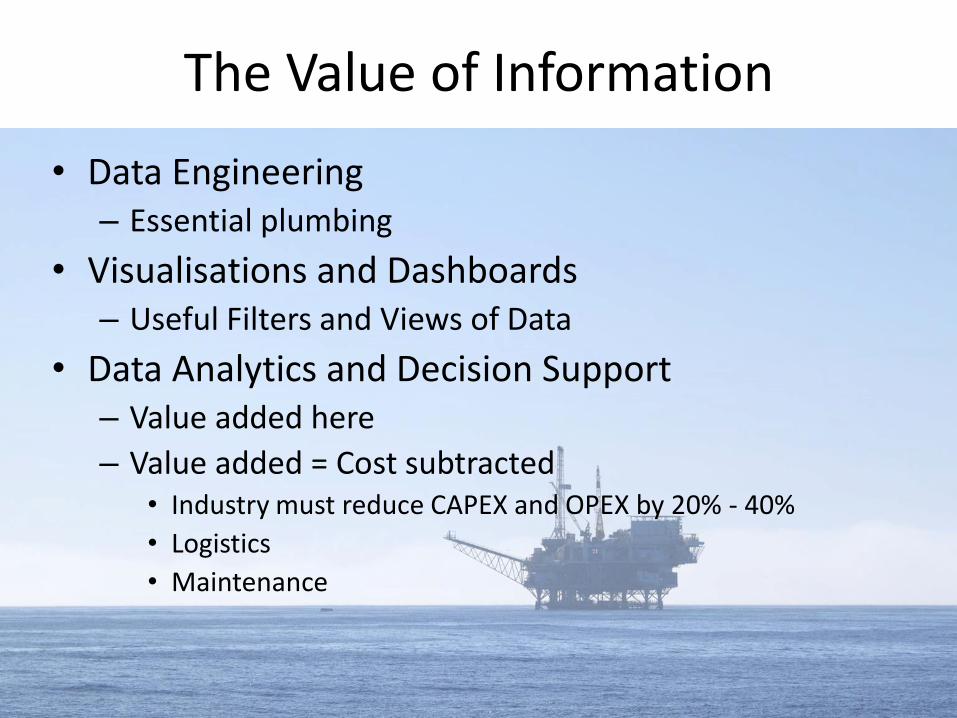

The Value of Information

• Data Engineering– Essential plumbing

• Visualisations and Dashboards– Useful Filters and Views of Data

• Data Analytics and Decision Support– Value added here

– Value added = Cost subtracted• Industry must reduce CAPEX and OPEX by 20% - 40%

• Logistics

• Maintenance

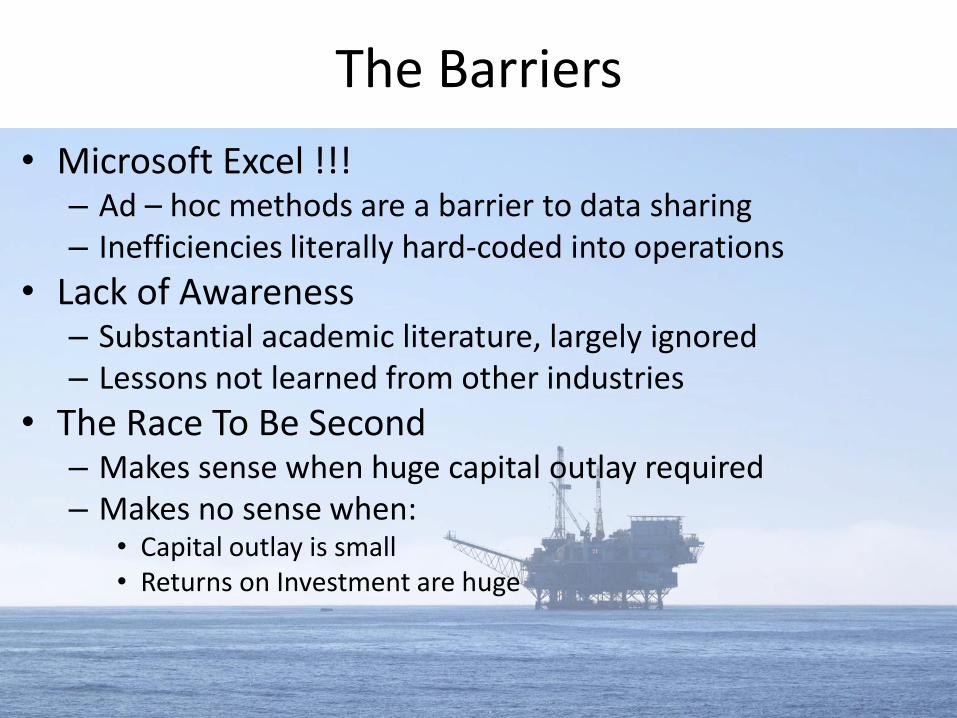

The Barriers

• Microsoft Excel !!!– Ad – hoc methods are a barrier to data sharing– Inefficiencies literally hard-coded into operations

• Lack of Awareness– Substantial academic literature, largely ignored– Lessons not learned from other industries

• The Race To Be Second– Makes sense when huge capital outlay required– Makes no sense when:

• Capital outlay is small• Returns on Investment are huge

Dashboards Can Be A Useful Filter

Now, just drill down …

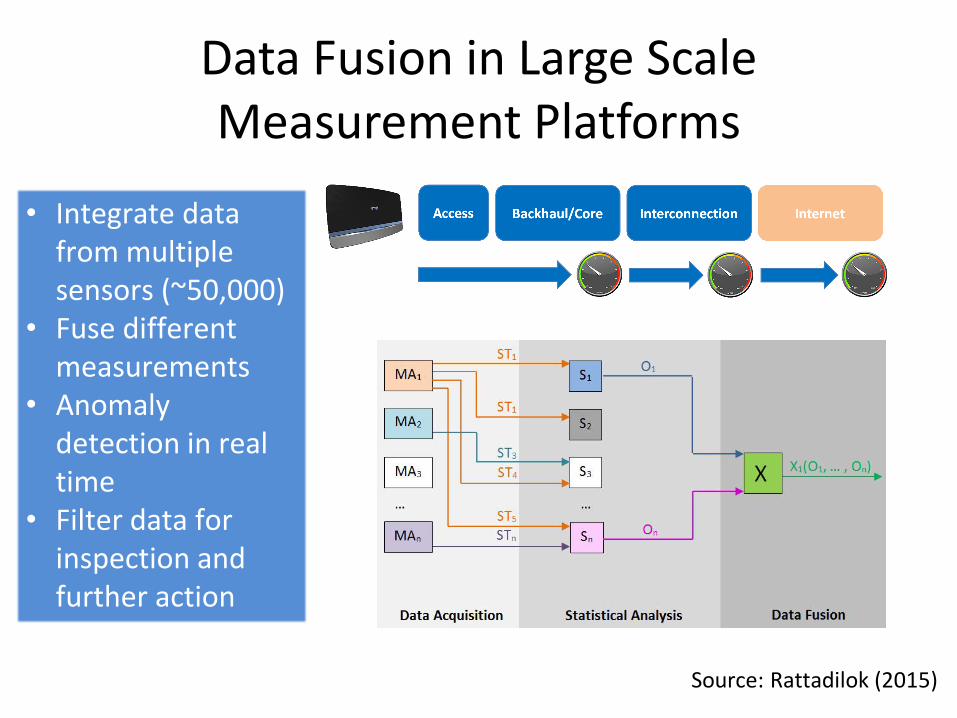

Data Fusion in Large Scale Measurement Platforms

• Integrate data from multiple sensors (~50,000)

• Fuse different measurements

• Anomaly detection in real time

• Filter data for inspection and further action

Source: Rattadilok (2015)

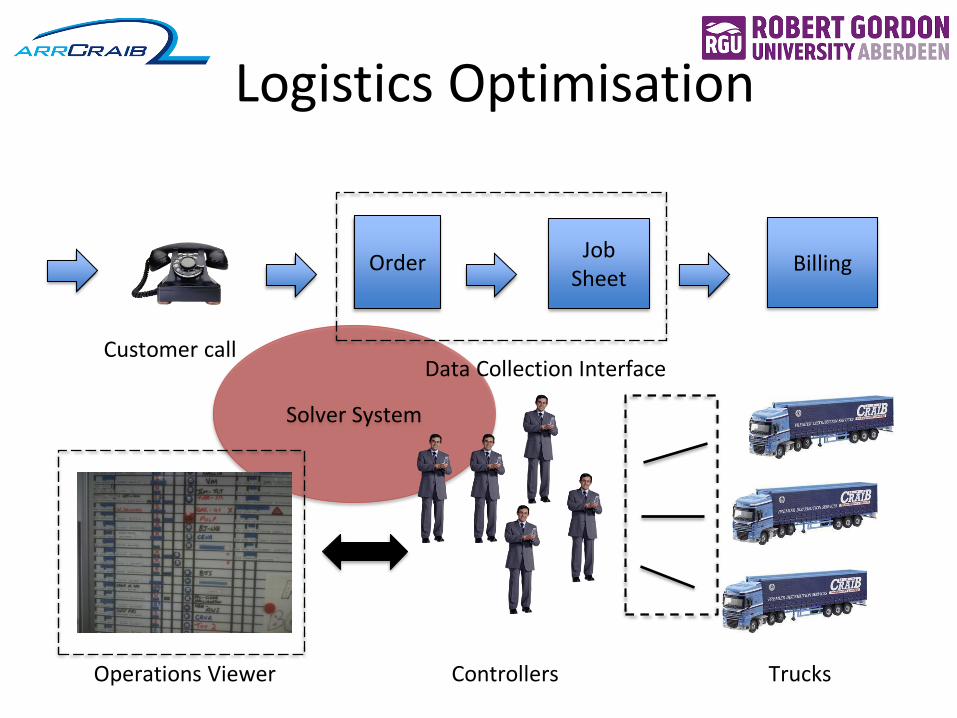

Logistics Optimisation

• Highly complex supply chain

– People, parts, trucks, vessels, helicopters, cranes

• Operational uncertainty

– Weather, equipment failures, non-productive time

• Primitive information systems

– Excel, email, bits of paper, …

• Over-resourcing traditionally affordable

Solver System

Logistics Optimisation

OrderJob

SheetBilling

Customer call

Operations Viewer Controllers Trucks

Data Collection Interface

Logistics Optimisation: Benefits

• Optimise KPIs– Manage trade-offs effectively

• Typical resources savings 20% - 40% – supply vessel @ £15K/day hire

– Each vessel saved = £4.5M per year

– 20% x 150 vessels x £4.5M = £135M

• Similar savings can be realisedthroughout the supply chain.

• This is standard in some industries

Maintenance

• Corrective maintenance– Classic “fail and fix”

– Fixing may be hugely expensive or impossible

• Preventative and Predictive Maintenance– Maintain before failure

– Schedule maintenance based on prediction

• Value added = Cost subtracted– Reduced maintenance requirement

– Planned, not reactive activity

– Fewer, faster, more productive shutdowns

Analytics Layer

Sensors Layer

Storage Layer

Decision LayerHealth MonitoringPredictive ModelsMaintenance PlansLogistics Scheduling

OptimiseKPIs

Predictive Maintenance

Industry Future

• New analysis techniques from academic literature

– e.g. Dynamic Bayesian Networks

• Modern CMSs integrate with SCADA

– Relate operating condition and performance

• Model features of individual systems

• More sophisticated multivariate analyses

• Automation of analysis

Where to Start?

• Identify main areas of pain– Target rich environment!

• Seek partners– Data/experience sharing within / outside industry– Vendors – logistics and analytics platforms– Academic researchers

• Help is available– Data Lab– CENSIS– OGIC– Scottish Enterprise

Conclusion

• Data Analytics can significantly enhance:– Offshore Logistics

– Predictive Maintenance

• Needs to be embedded in operations

• There is no shortage of techniques!– Academic literature sizeable and growing

– Gap with industry practice

• Combined industry and academic collaboration can make transformative step changes

#oilgasict

Steve HarrisonScottish Enterprise

Last year....

Digital Offshore

2016

Data Science

Who is in the room?

Who is in the room?

Do you make your living selling data?

Who is in the room?

Do you make your living analysing data?

Who is in the room?

Do you make your living creating data?

Who is in the room?

Do you make your living helping others ?

A Quick Survey

A Quick Survey

Who thinks the oil price will never rise >$100 again?

A Quick Survey

Has heard of the term Digital Mesh?

A Quick Survey

Has used the term Industry 4.0 in a presentation?

Steve H & Scottish Enterprise

• An Engineer – 15 years in a Multinational – Oil & Gas Services

• A Business Professional - Strategy, M&A, Operations, HR, Business Development, Innovation.

• A coach, mentor & advisor

• A facilitator – helping to make things happen

Overview

1. SE Supports individual companies to grow ...grants/expertise/networks

2. SE develops, invests & manages projects to help sectors to grow

– Creating conditions to encourage growth

– Removing barriers / obstacles that prevent growth

– Identifying opportunities and investing in resources to realise them.

“We identify and exploit opportunities for Scotland's economic growth by supporting Scottish companies to compete, helping to build globally competitive sectors, attracting new investment and creating a world-class business environment.”

Predict, Prevent, Produce More

TopicsWednesday 16th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Objectives

1. Share with you our thinking about the Data Science opportunity

2. Encourage you to volunteer your companies, data, resources to exploring these opportunities

3. Update you on our plans to consult with you about this opportunity and to seek your active involvement both today and later on.

Can Data Science Help Maximise Economic Recovery?

Schematic to Help Facilitate Discussions

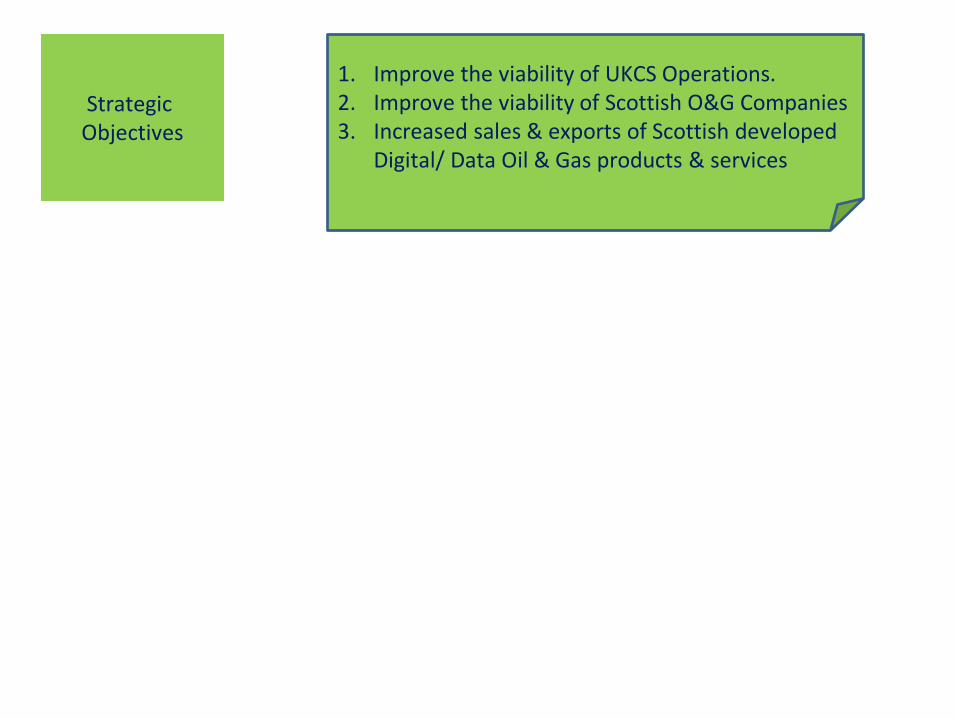

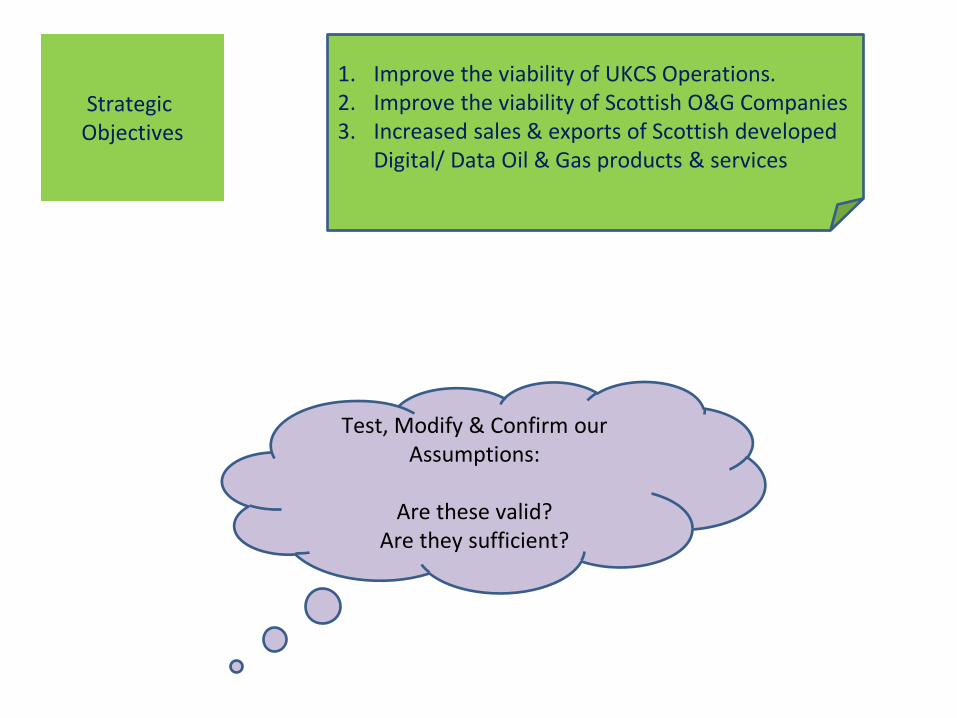

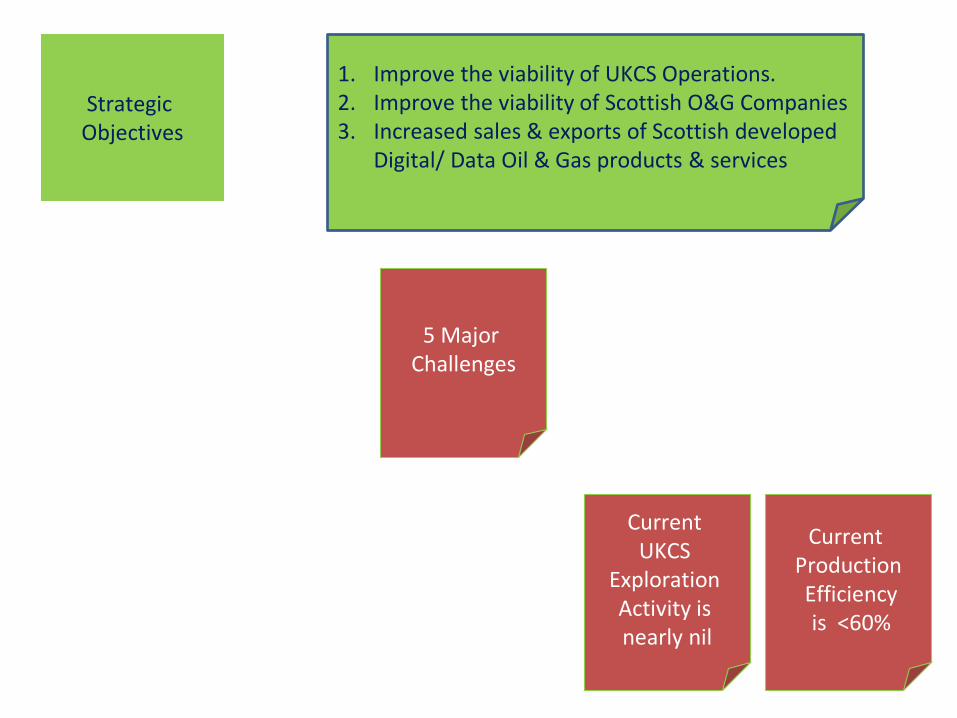

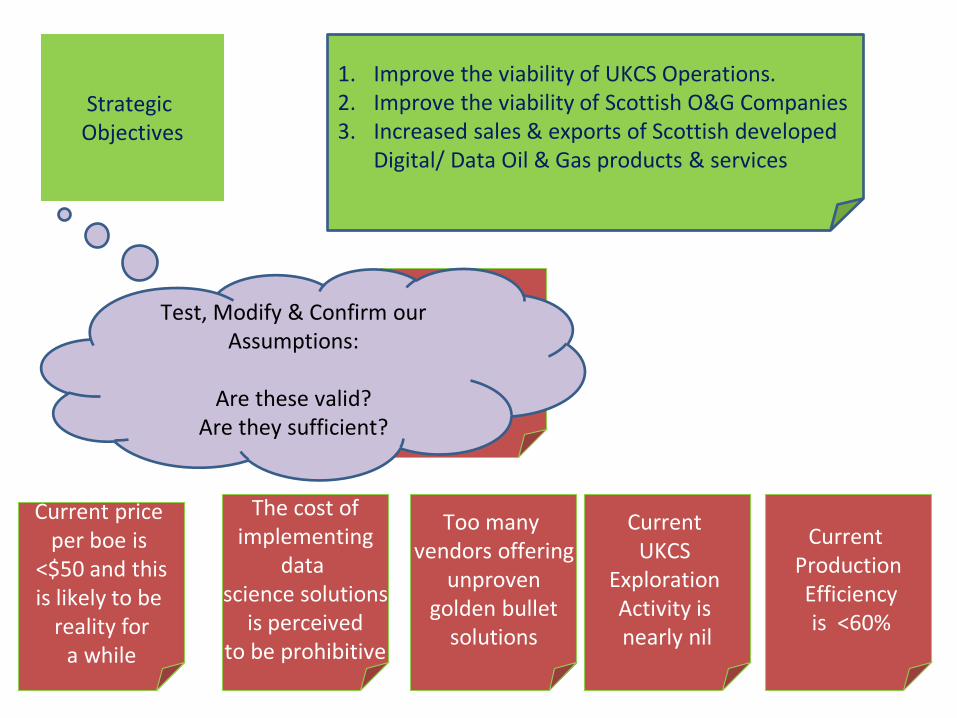

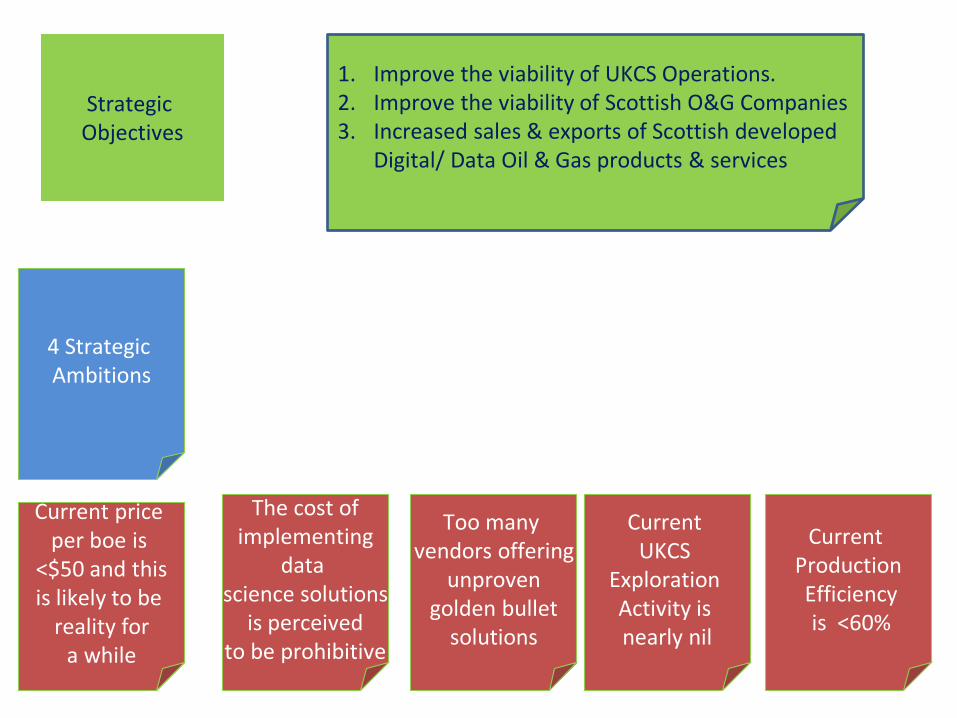

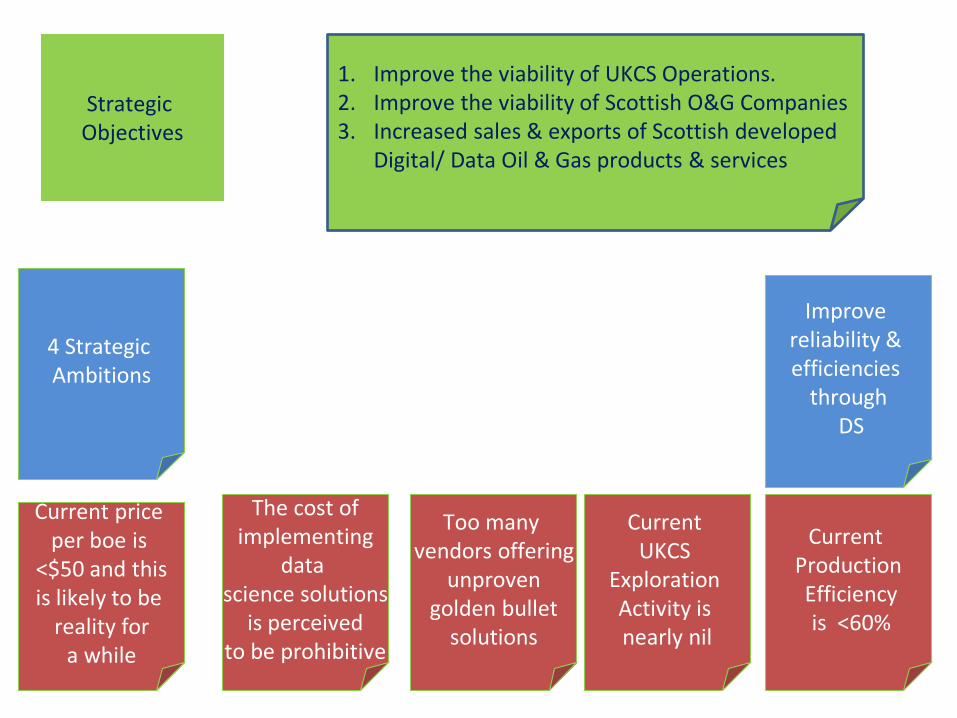

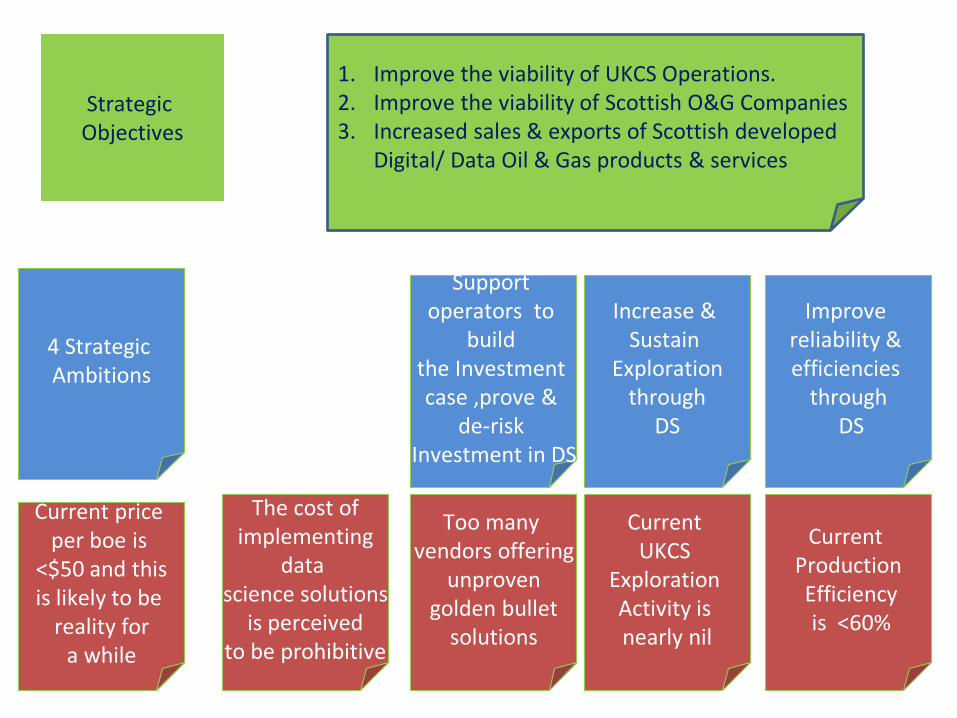

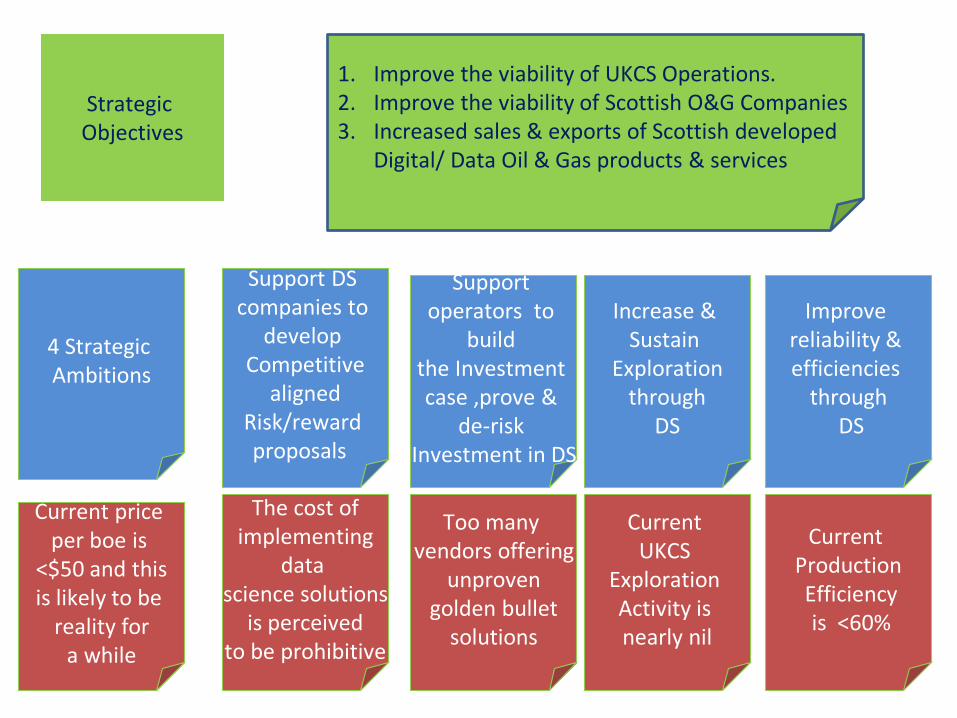

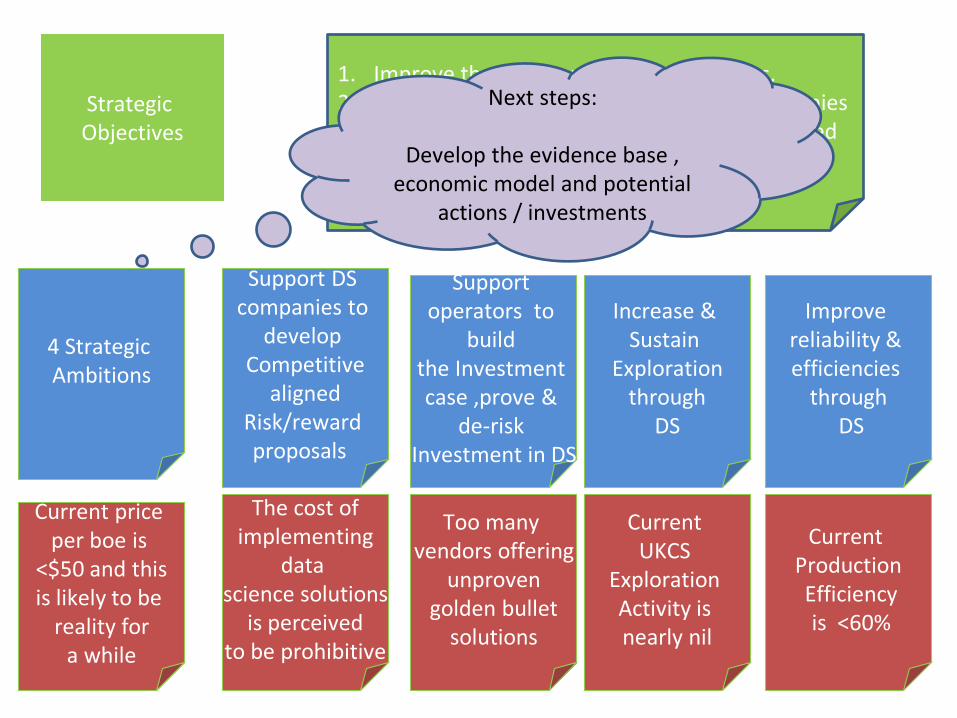

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Test, Modify & Confirm our Assumptions:

Are these valid?Are they sufficient?

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

5 Major Challenges

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

5 Major Challenges

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

5 Major Challenges

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Too many vendors offering

unprovengolden bullet

solutions

5 Major Challenges

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

5 Major Challenges

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

5 Major Challenges

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

5 Major Challenges

Test, Modify & Confirm our Assumptions:

Are these valid?Are they sufficient?

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

4 Strategic Ambitions

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

4 Strategic Ambitions

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

Increase & Sustain

Explorationthrough

DS

4 Strategic Ambitions

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

Increase & Sustain

Explorationthrough

DS

Support operators to

build the Investment case ,prove &

de-risk Investment in DS

4 Strategic Ambitions

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

Increase & Sustain

Explorationthrough

DS

Support operators to

build the Investment case ,prove &

de-risk Investment in DS

4 Strategic Ambitions

Support DS companies to

develop Competitive

alignedRisk/reward proposals

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

Increase & Sustain

Explorationthrough

DS

Support operators to

build the Investment case ,prove &

de-risk Investment in DS

Support DS companies to

develop Competitive

alignedRisk/reward proposals

4 Strategic Ambitions

Test, Modify & Confirm our Assumptions:

Are these valid?Are they sufficient?

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

Increase & Sustain

Explorationthrough

DS

Support operators to

build the Investment case ,prove &

de-risk Investment in DS

Support DS companies to

develop Competitive

alignedRisk/reward proposals

4 Strategic Ambitions

Next steps:

Develop the evidence base , economic model and potential

actions / investments

1. Improve the viability of UKCS Operations.2. Improve the viability of Scottish O&G Companies3. Increased sales & exports of Scottish developed

Digital/ Data Oil & Gas products & services

Strategic Objectives

Current ProductionEfficiencyis <60%

Current UKCS

Exploration Activity is nearly nil

Current price per boe is

<$50 and this is likely to be

reality fora while

Too many vendors offering

unprovengolden bullet

solutions

The cost ofimplementing

data science solutions

is perceived to be prohibitive

Improve reliability & efficiencies

throughDS

Increase & Sustain

Explorationthrough

DS

Support operators to

build the Investment case ,prove &

de-risk Investment in DS

Support DS companies to

develop Competitive

alignedRisk/reward proposals

4 Strategic Ambitions

Next steps:

Develop the evidence base , economic model and potential

actions / investments

Co-ordinated Team

Approach

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Activity

1. On Line

2. We need your help to help us build the evidence of need and demand for support & investment.

Predict, Prevent, Produce More

In Development….

1. A case for Digital / Data as a TLB theme

2. Digital / Data to be a part of the appropriate solution centres within the OGTC

…connected to….

3. A Data Science for O&G Centre

4. A support programme

Activity

1. On Line

2. We need your help to help us build the evidence of need and demand for support & investment.

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Can Data Technology Help

improve Productivity?

Find the Missing Platform?

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Can Data

Technology

Help find &

recover

hydrocarbons?

Predict the

Predictable?

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Can Data Technology help to

reduce lift cost?

Prevent the Preventable?

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Can Data Technology inform

Capital Investment decisions?

Increase ROI

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Opportunity

1. Can Data Technologies increase uptime and improve efficiency?

2. Can Data Technologies improve prediction and reservoir modelling accuracies?

3. Can Data Technologies better inform capital investment decisions?

4. Can Data Technologies reduce lift cost?

However “they” have been saying that for decades...

Data2Text

Founded 2009,

3 scientist’s + 1

entrepreneur

Merged to form

Arria NLG in

2013

Floated on AIM

in 2014 for

£100M

Current trading

at £35M and 50

data scientists

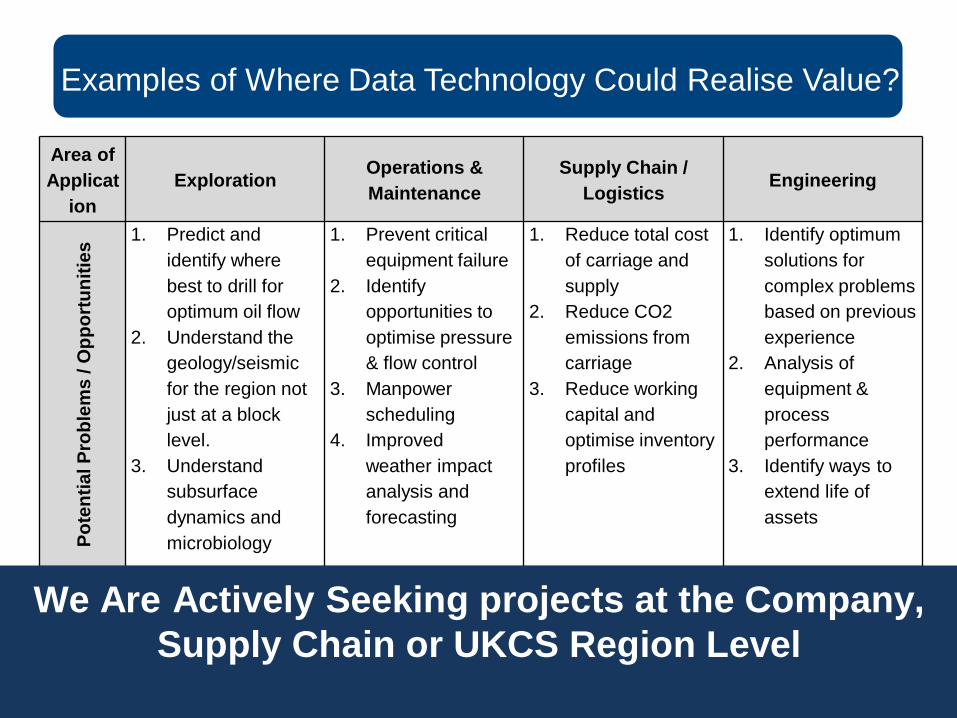

Examples of Where Data Technology Could Realise Value?

Area of

Applicat

ion

ExplorationOperations &

Maintenance

Supply Chain /

LogisticsEngineering

Po

ten

tial P

rob

lem

s / O

pp

ort

un

itie

s

1. Predict and

identify where

best to drill for

optimum oil flow

2. Understand the

geology/seismic

for the region not

just at a block

level.

3. Understand

subsurface

dynamics and

microbiology

1. Prevent critical

equipment failure

2. Identify

opportunities to

optimise pressure

& flow control

3. Manpower

scheduling

4. Improved

weather impact

analysis and

forecasting

1. Reduce total cost

of carriage and

supply

2. Reduce CO2

emissions from

carriage

3. Reduce working

capital and

optimise inventory

profiles

1. Identify optimum

solutions for

complex problems

based on previous

experience

2. Analysis of

equipment &

process

performance

3. Identify ways to

extend life of

assets

Examples of Where Data Technology Could Realise Value?

Area of

Applicat

ion

ExplorationOperations &

Maintenance

Supply Chain /

LogisticsEngineering

Po

ten

tial P

rob

lem

s / O

pp

ort

un

itie

s

1. Predict and

identify where

best to drill for

optimum oil flow

2. Understand the

geology/seismic

for the region not

just at a block

level.

3. Understand

subsurface

dynamics and

microbiology

1. Prevent critical

equipment failure

2. Identify

opportunities to

optimise pressure

& flow control

3. Manpower

scheduling

4. Improved

weather impact

analysis and

forecasting

1. Reduce total cost

of carriage and

supply

2. Reduce CO2

emissions from

carriage

3. Reduce working

capital and

optimise inventory

profiles

1. Identify optimum

solutions for

complex problems

based on previous

experience

2. Analysis of

equipment &

process

performance

3. Identify ways to

extend life of

assets

We Are Actively Seeking projects at the Company,

Supply Chain or UKCS Region Level

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Will this secure, protect or grow

jobs...or will we lose more jobs?

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Create / Attract &

Anchor New High

Growth Data Technology

Ventures

7 Years

From

zero to

$10Bn

Val and

$1.7Bn

Sales

Business

Model

Innovation

Can we

learn &

apply?

Digital Founders

Cohort 1 April – Sept 15

Next Cohort Live Now - March to Sept 16

Applications now open for early stage

A 20 week programme built around USA best practice

designed to accelerate investor readiness and growth

plans.

Digital Founders

Cohort 1 April – Sept 15

Next Cohort March to Sept 16

Applications now open for early stage

A 20 week programme built around USA best practice

designed to accelerate investor readiness and growth

plans.

We need people with ambition, big ideas,

hungry to change the world....

Digital Founders

Cohort 1 April – Sept 15

Next Cohort March to Sept 16

Applications now open for early stage

A 20 week programme built around USA best practice

designed to accelerate investor readiness and growth

plans.

And we need mentors, investors, problem owners to

support...

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Support Companies to

Grow, Innovate &

Internationalise

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Develop Innovative,

Novel Methods,

Technologies, Services...

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Pathfinders Wanted

1. Do you have a datastream or data

set that you think might have hidden

value within it?

2. Do you have a problem where you

need a business case to validate

investment in technology?

3. Do you have a digital technology or

usage case that you would like us to

test and evaluate?

We are looking for bold pathfinders .

We have resources , we want your

problems so we can prove value.

Contact: [email protected]

or [email protected] to

arrange a discussion.

Myth Busting

1. We don’t have time

2. We can’t spare the people

3. We don’t have the data

4. We can’t afford it

5. It can’t be that good

6. Lets wait

Predict, Prevent, Produce More

Pathfinders Wanted

1. Do you have a datastream or data

set that you think might have hidden

value within it?

2. Do you have a problem where you

need a business case to validate

investment in technology?

3. Do you have a digital technology or

usage case that you would like us to

test and evaluate?

We are looking for bold pathfinders .

We have resources , we want your

problems so we can prove value.

Contact: [email protected]

or [email protected] to

arrange a discussion.

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

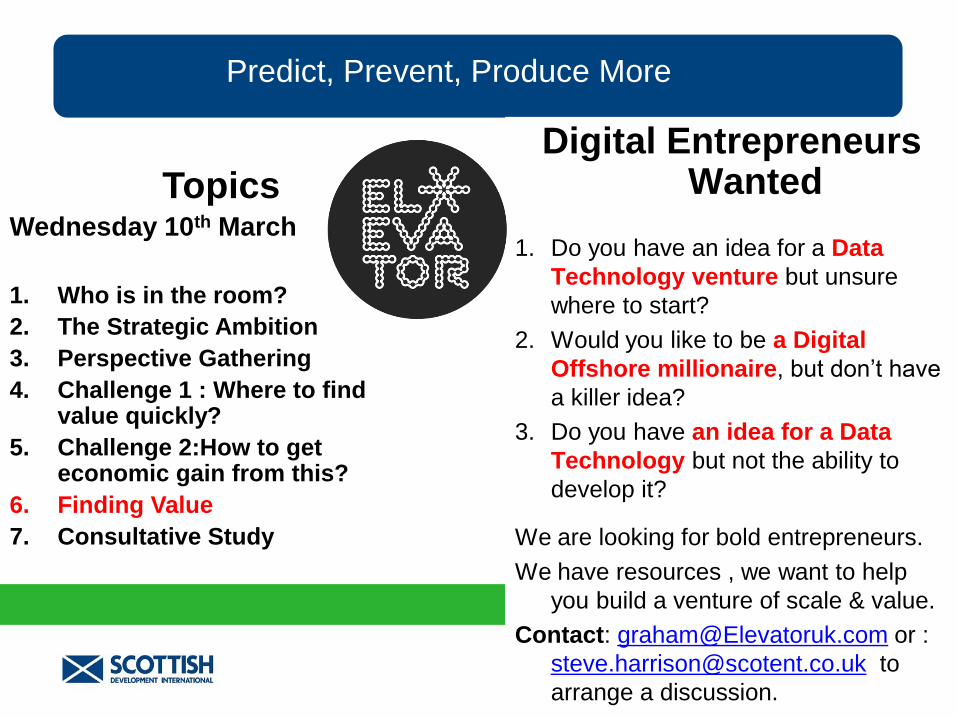

Digital Entrepreneurs Wanted

1. Do you have an idea for a Data

Technology venture but unsure

where to start?

2. Would you like to be a Digital

Offshore millionaire, but don’t have

a killer idea?

3. Do you have an idea for a Data

Technology but not the ability to

develop it?

We are looking for bold entrepreneurs.

We have resources , we want to help

you build a venture of scale & value.

Contact: [email protected] or :

arrange a discussion.

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

8. FAMA

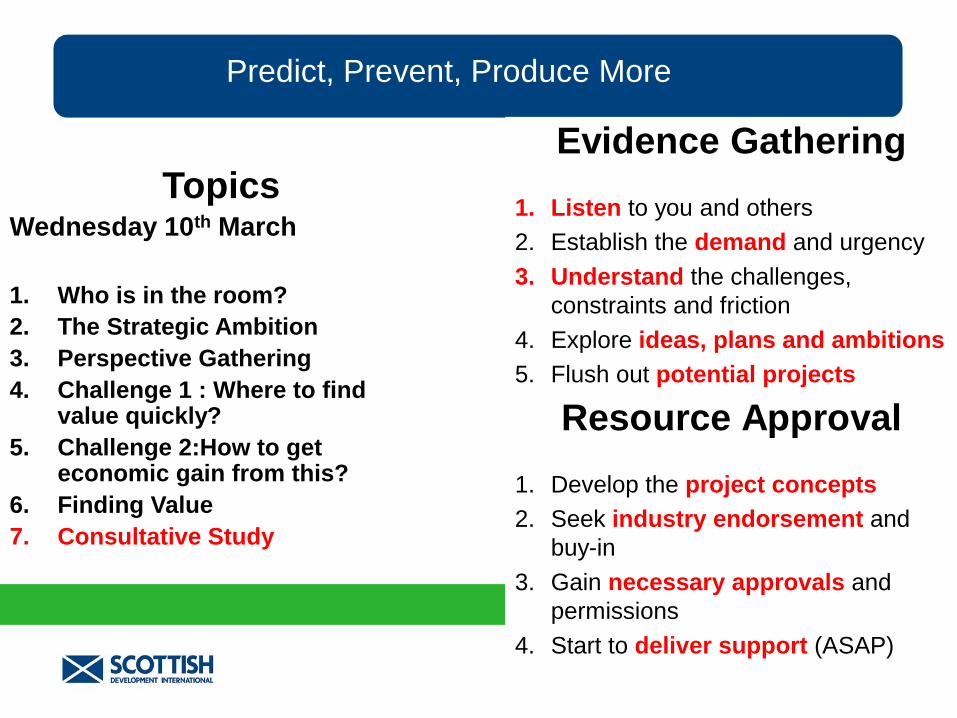

Evidence Gathering

1. Listen to you and others

2. Establish the demand and urgency

3. Understand the challenges,

constraints and friction

4. Explore ideas, plans and ambitions

5. Flush out potential projects

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Evidence Gathering

1. Listen to you and others

2. Establish the demand and urgency

3. Understand the challenges,

constraints and friction

4. Explore ideas, plans and ambitions

5. Flush out potential projects

Resource Approval

1. Develop the project concepts

2. Seek industry endorsement and

buy-in

3. Gain necessary approvals and

permissions

4. Start to deliver support (ASAP)

Predict, Prevent, Produce More

TopicsWednesday 10th March

1. Who is in the room?

2. The Strategic Ambition

3. Perspective Gathering

4. Challenge 1 : Where to find value quickly?

5. Challenge 2:How to get economic gain from this?

6. Finding Value

7. Consultative Study

Review

1. Share with you our thinking about the Data Science opportunity

2. Encourage you to volunteer your companies, data, resources to exploring these opportunities