OIL MARKET OUTLOOK AND OIL MARKET OUTLOOK AND OIL MARKET OUTLOOK AND OIL MARKET OUTLOOK AND WHAT NEXT FOR THE SOUTH WHAT NEXT FOR THE SOUTH WHAT NEXT FOR THE SOUTH WHAT NEXT FOR THE SOUTH EAST ASIAN EAST ASIAN EAST ASIAN EAST ASIAN OFFSHORE OFFSHORE OFFSHORE OFFSHORE MARKET MARKET MARKET MARKET VIJAY KRISHNAN

Transcript

OIL MARKET OUTLOOK AND OIL MARKET OUTLOOK AND OIL MARKET OUTLOOK AND OIL MARKET OUTLOOK AND WHAT NEXT FOR THE SOUTH WHAT NEXT FOR THE SOUTH WHAT NEXT FOR THE SOUTH WHAT NEXT FOR THE SOUTH

EAST ASIAN EAST ASIAN EAST ASIAN EAST ASIAN OFFSHORE OFFSHORE OFFSHORE OFFSHORE MARKETMARKETMARKETMARKET

VIJAY KRISHNAN

rystad energyrystad energyrystad energyrystad energy

introduction

Office locations• Rystad Energy is an independent

databases and consulting services firm, started in 2004, headquartered in Oslo, Norway.

• Provides a range of upstream E&P and oilfield service business intelligence data solutions built from a bottom up perspective across every single asset

• A leading advisor within strategy, market analysis and business development

• Publishing standard and customized research reports on high impact industry topics

• Insight and deliveries based on proprietary, fundamental research from primary sources

Core content:

• 65,000 assets globally

• 100% of Global Supply

• Asset Level Economic Model

• Monthly Global Update

• 3,200 companies

• Time span 1900-2100

• Production & Reserves

• Costs & Tax models

• Breakeven prices

• Asset factsheets

• M&A data

Core benefits:

• Complete

• Consistent

• Micro to Macro

• Best in class GUI

Core usage:

• Market/company/asset

analysis

• Benchmarking

• BD & target screening

• Valuation

ucube - the core of what we do

INSIGHT THROUGH BUSINESS DATA SOLUTIONSBUILT ON SAME, CONSISTENT DATA STRUCTURE AND PLATFORM

Complete and consistent E&P business intelligence data from macro to micro level with global coverage

North America shale analysis package with volumes, economics, well data and maps for all key plays and players

Global oil services market analysis data by industry segments, geography and supplier companies

Regional strategy & business development tool kit incl. regional E&P database, license activity atlas, asset reports and economical modelling spreadsheets

regional

e&p

solutions

regional

e&p

solutions

global

e&p

solutions

global

e&p

solutions

global

oil service

solutions

global

oil service

solutions

north

america

shale

solutions

north

america

shale

solutions

Rystad EnergyOil & gas

knowledge house

NOCs

Majors

E&Ps

Investment banks

Investors

Consulting firms

Oilfield service

Governments/Organizations

SERVING ALL OIL & GAS CLIENT SEGMENTS

JW19

Slide 5

JW19 Work more on colour coding here and use company specific coloursJulia Weiss, 30/11/2016

How we got here: the generic commodity cycle

Higher

reinvestment

increases

production

Production

outpaces

demand

Demand

outpaces

productionLow reinvestment

hurts production

Prices drop,

hurting cash

flow and

returns

Cash flow

declines,

spending

cuts, lay offs

Increased

investment,

capacity

issues

Higher prices

improve cash

flows

A commodity market with no “price maker” endlessly repeats this cycle

The cycle begins: in 2014, a large imbalance between supply and demand was looming

Stocks draw in 2017 on cuts, in medium term still tight Stocks draw in 2017 on cuts, in medium term still tight Stocks draw in 2017 on cuts, in medium term still tight Stocks draw in 2017 on cuts, in medium term still tight market due to lack of sanctioningmarket due to lack of sanctioningmarket due to lack of sanctioningmarket due to lack of sanctioning

Source: Rystad Energy research and analysis

• Global liquids supply and demand

• Million bbl/d

11

82

84

86

88

90

92

94

96

98

100

102

104

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Total Demand

Total Supply

ForecastHistorical

9.0

9.2

9.4

9.6

9.8

10.0

10.2

10.4

10.6

10.8

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-

14

Se

p-1

4

No

v-1

4

Jan

-15

Ma

r-1

5

Ma

y-1

5

Jul-

15

Se

p-1

5

No

v-1

5

Jan

-16

Ma

r-1

6

Ma

y-1

6

Jul-

16

Se

p-1

6

No

v-1

6

Jan

-17

Ma

r-1

7

Ma

y-1

7

Jul-

17

Se

p-1

7

No

v-1

7

KSA RE base case

KSA Target cut

KSA prepared to force compliance and we expect KSA prepared to force compliance and we expect KSA prepared to force compliance and we expect KSA prepared to force compliance and we expect production to be cut below target in 1H 17production to be cut below target in 1H 17production to be cut below target in 1H 17production to be cut below target in 1H 17

• KSA base case crude production, monthly

• Million bbl/d

12

• * This is the scenario called «Full 2017 Cuts + Natural Decline» in the OPEC scenarios on slide 4.

• Source: Rystad Energy research and analysis

ForecastHistorical

Full compliance through maintenance, while Iran Full compliance through maintenance, while Iran Full compliance through maintenance, while Iran Full compliance through maintenance, while Iran increases production through Augincreases production through Augincreases production through Augincreases production through Aug----17171717

Source: Rystad Energy research and analysis

• Selected OPEC countries crude production base case vs. OPEC agreement 30-Nov target production

Six OPEC members struggle to maintain production Six OPEC members struggle to maintain production Six OPEC members struggle to maintain production Six OPEC members struggle to maintain production regardless of the OPEC agreementregardless of the OPEC agreementregardless of the OPEC agreementregardless of the OPEC agreement

*Rest OPEC = Qatar, Ecuador and Gabon. Source: Rystad Energy research and analysis

• Selected OPEC countries crude production base case vs. OPEC agreement 30-Nov target production

• Million bbl/d

14

ForecastHistorical

Production Production Production Production to to to to drop by 260 drop by 260 drop by 260 drop by 260 kbblkbblkbblkbbl/d in 1H 17 against the /d in 1H 17 against the /d in 1H 17 against the /d in 1H 17 against the reference reference reference reference level, level, level, level, mostly through mostly through mostly through mostly through declinesdeclinesdeclinesdeclines

Source: Rystad Energy research and analysis

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Jun

-16

Jul-

16

Au

g-1

6

Se

p-1

6

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Fe

b-1

7

Ma

r-1

7

Ap

r-1

7

Ma

y-1

7

Jun

-17

Jul-

17

Au

g-1

7

Se

p-1

7

Oct

-17

No

v-1

7

De

c-1

7

ForecastHistorical

Mexico

Kazakhstan

Oman

Azerbaijan

Malaysia

Other non-OPEC

• .

• Liquids production profile for non-OPEC countries

• Million bbl/d

1

5

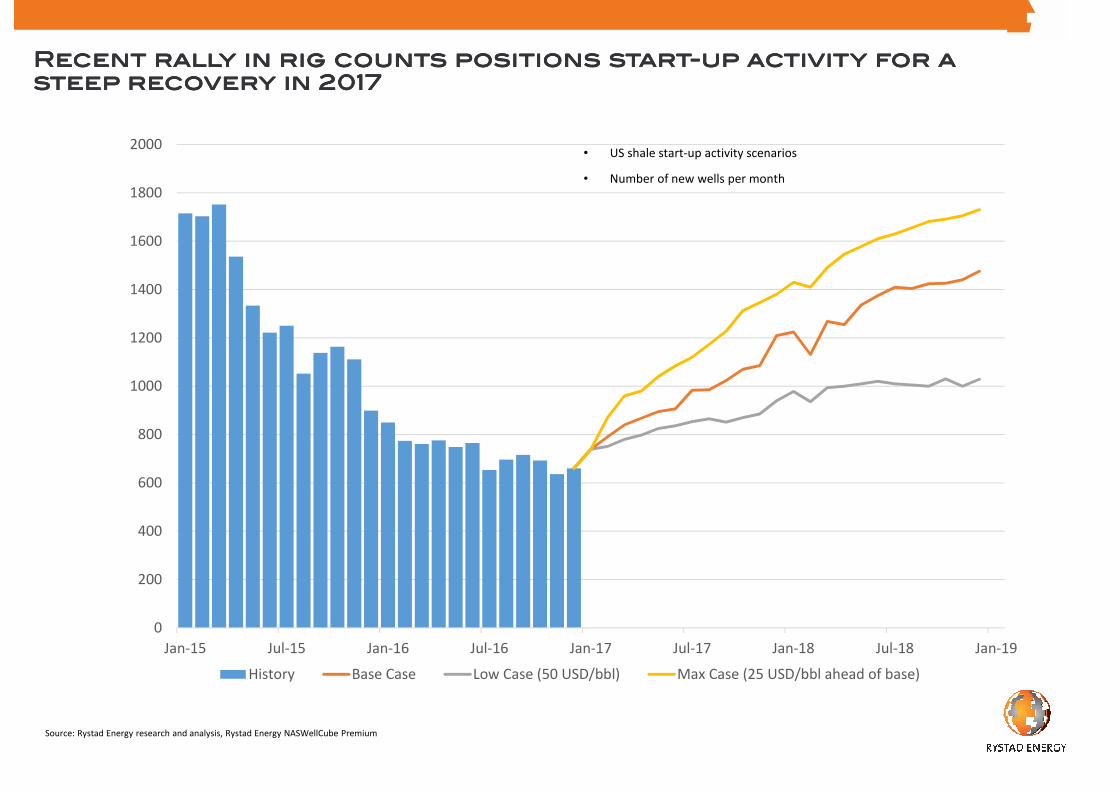

Recent rally in rig counts positions startRecent rally in rig counts positions startRecent rally in rig counts positions startRecent rally in rig counts positions start----up activity for a up activity for a up activity for a up activity for a steep recovery in 2017steep recovery in 2017steep recovery in 2017steep recovery in 2017

Source: Rystad Energy research and analysis, Rystad Energy NASWellCube Premium

History Base Case Low Case (50 USD/bbl) Max Case (25 USD/bbl ahead of base)

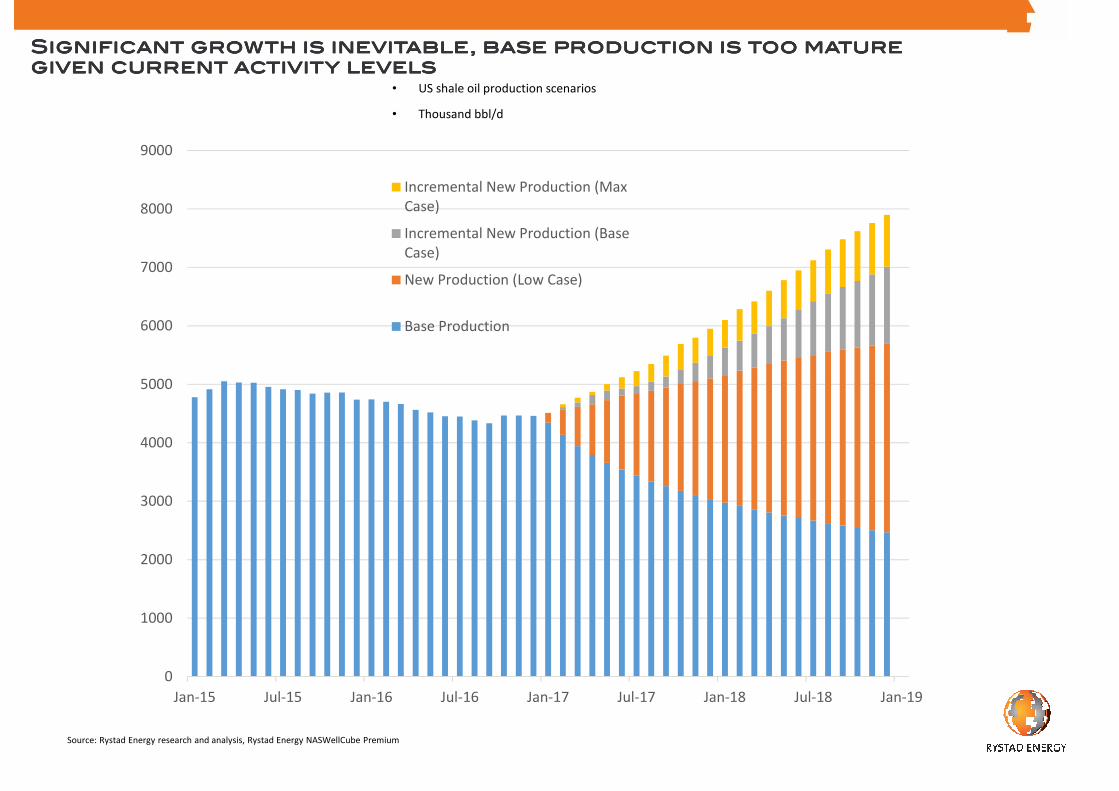

Significant growth is inevitable, base production is too mature Significant growth is inevitable, base production is too mature Significant growth is inevitable, base production is too mature Significant growth is inevitable, base production is too mature given current activity levelsgiven current activity levelsgiven current activity levelsgiven current activity levels

Source: Rystad Energy research and analysis, Rystad Energy NASWellCube Premium

Weaker 1Q and stronger remainder of the year demand Weaker 1Q and stronger remainder of the year demand Weaker 1Q and stronger remainder of the year demand Weaker 1Q and stronger remainder of the year demand result in overall higher 2017 growthresult in overall higher 2017 growthresult in overall higher 2017 growthresult in overall higher 2017 growth

Source: Rystad Energy research and analysis

• World liquids demand growth y/y

• Million bbl/d

1

8

ICE Brent crude historical front month price, latest five ICE Brent crude historical front month price, latest five ICE Brent crude historical front month price, latest five ICE Brent crude historical front month price, latest five year futures curve and UCube base caseyear futures curve and UCube base caseyear futures curve and UCube base caseyear futures curve and UCube base case

4560

67

59

62

0

20

40

60

80

100

120

140

Nov-10 Nov-11 Nov-12 Nov-13 Nov-14 Nov-15 Nov-16 Nov-17UCube base case Futures curve Brent front month

Source: Bloomberg, Rystad Energy research and analysis

E&P companies to keep investment flat E&P companies to keep investment flat E&P companies to keep investment flat E&P companies to keep investment flat in 2017 with some positive in 2017 with some positive in 2017 with some positive in 2017 with some positive upside riskupside riskupside riskupside risk

revision of the short and long termservice market. This is the effect of

more clarity around oil supply and

E&P companies being cautious

before the OPEC meeting.

The short term service segment

purchases from 2015-2017 is now at

-9.5%, down from -8.8%.

Long term we still see an average

growth of 10%.

Source: Rystad Energy DCube

Purchases of oilfield servicesUSD Billion

Average 62 USD/Average 62 USD/Average 62 USD/Average 62 USD/bblbblbblbbl oil price in 2017 suggests broadly flat growth oil price in 2017 suggests broadly flat growth oil price in 2017 suggests broadly flat growth oil price in 2017 suggests broadly flat growth for the OFS marketfor the OFS marketfor the OFS marketfor the OFS market

2015 2017 2021Short term Long term

CAGR-9.5%

CAGR10.0%

100

5447

62

75

8897

105

0

20

40

60

80

100

120

2014 2016 2018 2020

Brent Oil Price with Rystad Forward CurveUSD/bbl

Floater fixture volumes and rig rates have been trending Floater fixture volumes and rig rates have been trending Floater fixture volumes and rig rates have been trending Floater fixture volumes and rig rates have been trending downwardsdownwardsdownwardsdownwards

14 12

38

1629

4533

54

3750

78

39

123

58

101

57

2939

1728

7

28

14

27

7 11 10 13 13 11 60

20

40

60

80

100

120

140

160

180

200

0

100

200

300

400

500

600

1Q09 1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16

Rig Supply Years (rhs)

Rig Rate USD (lhs)

Rig rates (kUSD/day) # fixed rig years

The same situation for The same situation for The same situation for The same situation for jackupsjackupsjackupsjackups but lower activitybut lower activitybut lower activitybut lower activity

*As of 22.09.2016Source: RigCube September 2016

- 30

- 20

- 10

0

10

20

30

40

50

60

70

80

90

100

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Construction

Retired

Jackup construction and retirement

Number of units

19 units retired in 2015

20 units retired in 2016*

Jackups

2015 & 2016 with largest number of retired rigs in more than 40 years2015 & 2016 with largest number of retired rigs in more than 40 years2015 & 2016 with largest number of retired rigs in more than 40 years2015 & 2016 with largest number of retired rigs in more than 40 years

*As of 22.09.2016Source: RigCube September 2016

Floaters

Floater construction and retirement

Number of units

- 30

- 25

- 20

- 15

- 10

- 5

0

5

10

15

20

25

30

35

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Semisubmersible

Drillships

Retired Semisubmersible

Retired Drillship

28 units retired in 2015

22 units retired in

2016*

Utilization will start to recover during 2018 assuming no further Utilization will start to recover during 2018 assuming no further Utilization will start to recover during 2018 assuming no further Utilization will start to recover during 2018 assuming no further retirementsretirementsretirementsretirements

* Total supply is gross supply for the fleet and includes all rigs, including ready stacked and cold stacked.Source: RigCube September 201625

• Global supply* and demand for floating drilling rigs

• Number of rigs

Implied77% 81% 84% 86% 84% 81% 79% 82% 85% 82%

73%57% 51% 53% 60% 65%

0

50

100

150

200

250

300

350

400

2005 2010 2015 2020

Demand Total supply

Historical average 83%

Utiliz

ation

Tota

l fleet

Floaters

Recovery from 2018 for all segments Recovery from 2018 for all segments Recovery from 2018 for all segments Recovery from 2018 for all segments

Source: DCube November 2016

• Purchases of oilfield services

• Annual change

6%5%

-20%

-18%

0%

9% 9%10%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2013 2014 2015 2016 2017 2018 2019 2017-2021

CAGR

Maintenance and Operations

EPCI

Subsea

Drilling Contractors

Well Services and Commodities

Seismic

All OFS Purhases

But the rebound varies across regions and segments in 2017 But the rebound varies across regions and segments in 2017 But the rebound varies across regions and segments in 2017 But the rebound varies across regions and segments in 2017 Oilfield service growth

Source: DCube

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2015 2016 2017 2018

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2015 2016 2017 2018

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2015 2016 2017 2018

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2015 2016 2017 2018

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2015 2016 2017 2018

North America

South America Africa and Middle East Asia and CIS

Europe

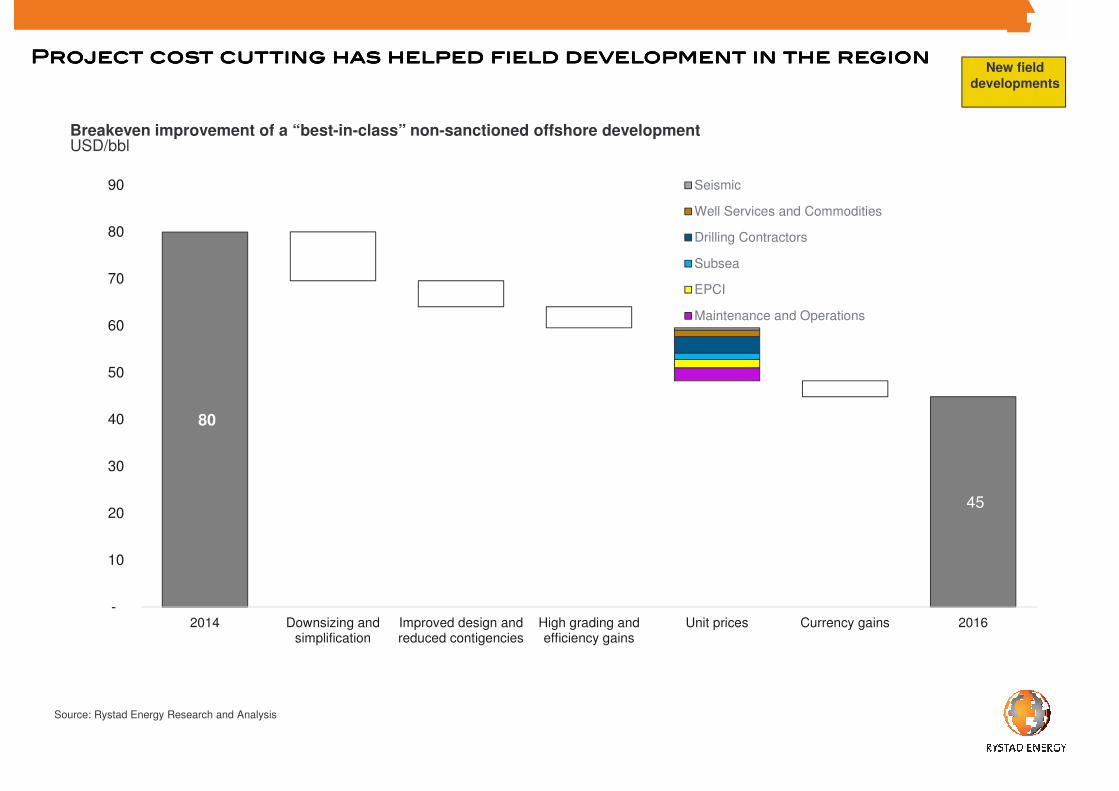

Project cost cutting has helped field development in the regionProject cost cutting has helped field development in the regionProject cost cutting has helped field development in the regionProject cost cutting has helped field development in the region

Source: Rystad Energy Research and Analysis

Breakeven improvement of a “best-in-class” non-sanctioned offshore developmentUSD/bbl

80

45

-

10

20

30

40

50

60

70

80

90

2014 Downsizing andsimplification

Improved design andreduced contigencies

High grading andefficiency gains

Unit prices Currency gains 2016

Seismic

Well Services and Commodities

Drilling Contractors

Subsea

EPCI

Maintenance and Operations

49.3

7.3

New field

developments

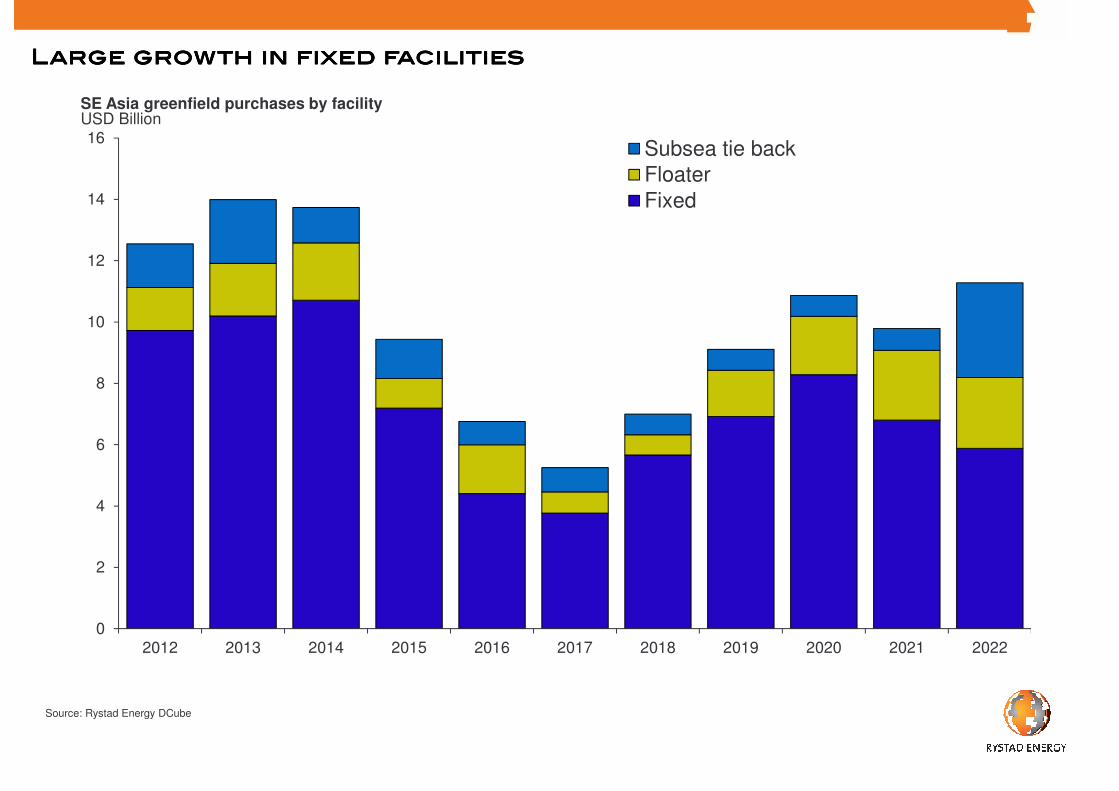

Shallow water investments drive the decline in Southeast Asia, but Shallow water investments drive the decline in Southeast Asia, but Shallow water investments drive the decline in Southeast Asia, but Shallow water investments drive the decline in Southeast Asia, but also the rebound…also the rebound…also the rebound…also the rebound…

Offshore purchases from investments by supply segmentUSD billions

- 26%

- 33%CAGR: 16%

Southeast Asian growth will come from new developments and Southeast Asian growth will come from new developments and Southeast Asian growth will come from new developments and Southeast Asian growth will come from new developments and Brownfield investmentBrownfield investmentBrownfield investmentBrownfield investment

Source: Rystad Energy DCube

SE Asia purchases of offshore oilfield servicesUSD Billion

SE Asia purchases of offshore oilfield servicesUSD Billion

Although lower volumes, there are still exciting opportunities Although lower volumes, there are still exciting opportunities Although lower volumes, there are still exciting opportunities Although lower volumes, there are still exciting opportunities around the world!around the world!around the world!around the world!

Mozambique:

•Coral FLNG

•Area 1 LNG

•Area 4 LNG

Brazil:

•Libra Pilot

•Sepia

•Buzios

•Marlim revitalization

West Africa:

•Bonga SW

•Zabazaba/Etan

GoM:

•Appomattox

•Mad Dog Phase 2

•Shenandoah

North Sea:

• Johan Castberg

•Wisting

•Alta/Gotha

•Culzean

Australia:

• Browse FLNG

India:

•KG-DWN-98/2

Indonesia:

•Abadi FLNG/onshore

•Gendalo-Gehem

Mediterranean:

•Leviathan

•Zohr

Legend

Size of circle =

1 BUSD

Offshore capex 2017-2022USD billion

Source: Rystad Energy research and analysis, DCube

Spending in Offshore Southeast AsiaSpending in Offshore Southeast AsiaSpending in Offshore Southeast AsiaSpending in Offshore Southeast Asia

3

3

Greenfield

Exploration

Brownfield

33

Greenfield

Exploration

Brownfield

Petronas, Shell, Chevron and Total are the biggest spenders Petronas, Shell, Chevron and Total are the biggest spenders Petronas, Shell, Chevron and Total are the biggest spenders Petronas, Shell, Chevron and Total are the biggest spenders during the recoveryduring the recoveryduring the recoveryduring the recovery

Source: Rystad Energy DCube

SE Asia purchases of offshore oilfield servicesUSD Billion

Investment in greenfield projects favors large fieldsInvestment in greenfield projects favors large fieldsInvestment in greenfield projects favors large fieldsInvestment in greenfield projects favors large fields