24

CA T. N. CA T. N. Manoharan Manoharan 6 th June, 2014 6 th June, 2014 Bombay Chartered Accountants’ Society A 2-Day Summit on Networking Within and Across Professions

CA T. N. CA T. N. ManoharanManoharan

6th June, 20146th June, 2014

Bombay Chartered Accountants’ Society

A 2-Day Summit on Networking Within and Across ProfessionsA 2-Day Summit on Networking Within and Across Professions

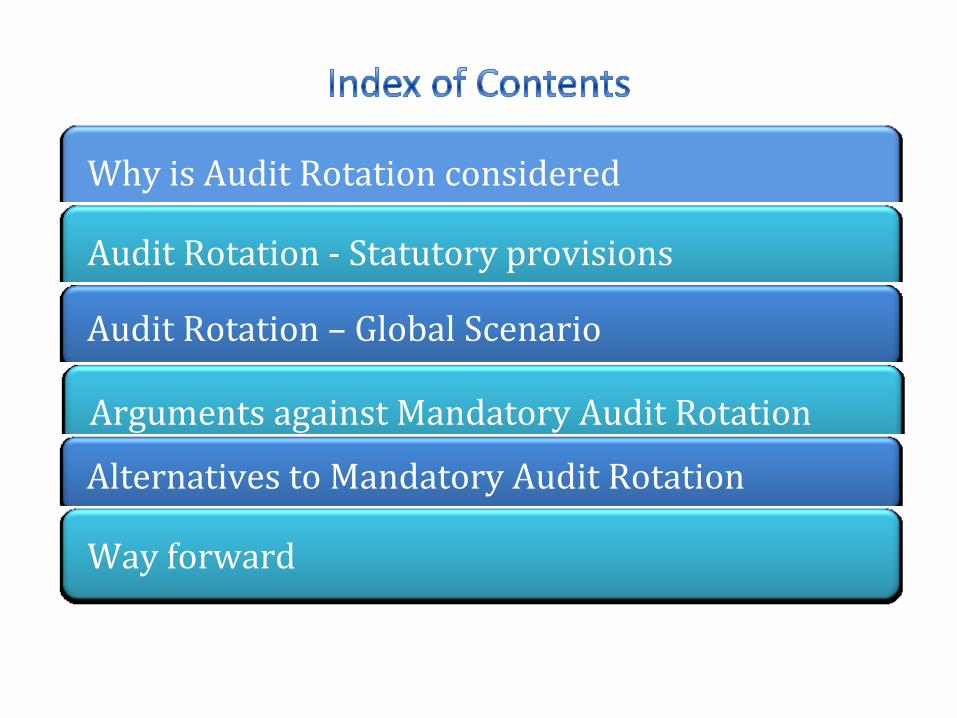

Why is Audit Rotation considered

Audit Rotation - Statutory provisions

Audit Rotation – Global Scenario

Arguments against Mandatory Audit Rotation

Alternatives to Mandatory Audit Rotation

Way forward

Over familiarity with the management can result in loss of professional skepticism

Pressure to maintain a commercial relationship may undermine the quality of the audit

Fresh Eyes are more likely to spot issues than an incumbent audit firm

Would help in opening up and eliminating concentration in the upper part of the market

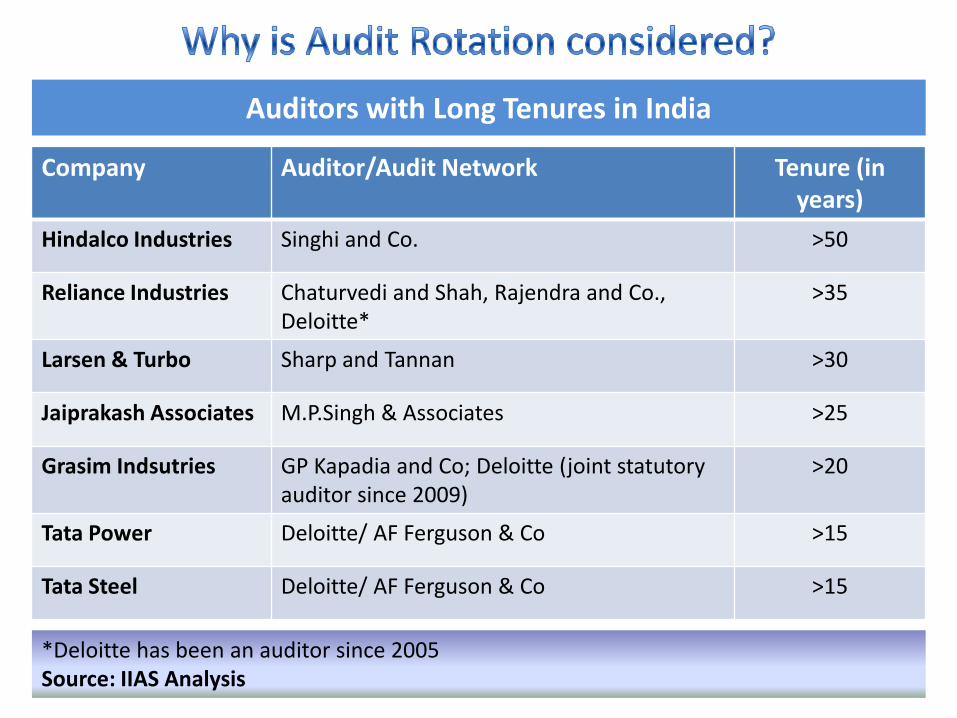

Auditors with Long Tenures in India

Company Auditor/Audit Network Tenure (in years)

Hindalco Industries Singhi and Co. >50

Reliance Industries Chaturvedi and Shah, Rajendra and Co., Deloitte*

>35

Larsen & Turbo Sharp and Tannan >30

Jaiprakash Associates M.P.Singh & Associates >25

Grasim Indsutries GP Kapadia and Co; Deloitte (joint statutory auditor since 2009)

>20

Tata Power Deloitte/ AF Ferguson & Co >15

Tata Steel Deloitte/ AF Ferguson & Co >15

*Deloitte has been an auditor since 2005Source: IIAS Analysis

Statutory provisions governing the Rotation of Auditors

Chapter X of the

Companies Act, 2013

The Companies (Audit and

Auditors) Rules, 2014 w.e.f 01.04.2014

Section 139(2) of the Companies Act, 2013

Audit being done byIndividual

AuditorAudit Firm

One term of 5 consecutive

years

Two terms of 5 consecutive

years

Includes LLPs, incorporated under

Includes LLPs, incorporated under

LLP Act, 2008

Cooling period - 5 years after completing the tenure

Transition Period from1.04.20143 years

Transition Period from1.04.20143 years

Class of companies Covered

as per Rule 5 of The Companies (Audit and Auditors) Rules, 2014 r/w S. 139(2):

All Unlisted public companies having

Paid up Share Capital of

Rs. 10 Crore or more

All private limited companies having

Paid up Share Capital of

Rs. 20 Crore or more

Other companies having public borrowings from

financial institutions, banks or public deposits of Rs 50 crore or more.

“One Person Company” and “Small Company” as defined under Section 2(62) and 2(85) respectively are excluded from this provision

Section 139(3) of the Companies Act, 2013

Members of the Company may resolve to provide that:

In the firm appointed:

Audit partner and team must be rotated at intervals as resolved by members

The audit must be

conducted by more than one auditor

Nothing contained inSection shallaffect• the

an

• auditor

Nothing contained inSection 139(2) shallaffect :• the right of the

company to remove anauditor or

• the right of the auditorto resign

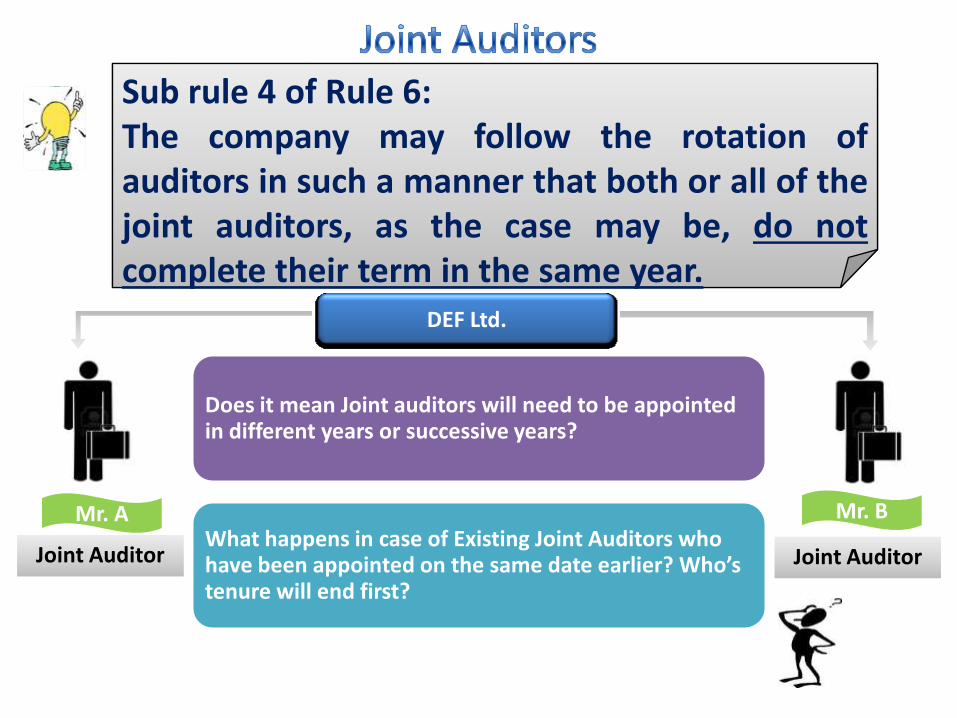

Mr. A

Joint AuditorJoint Auditor

Mr. B

Joint AuditorJoint Auditor

Sub rule 4 of Rule 6:T ofauditors thejoint notcomplete their term in the same year.

Sub rule 4 of Rule 6:The company may follow the rotation ofauditors in such a manner that both or all of thejoint auditors, as the case may be, do notcomplete their term in the same year.

Does it mean Joint auditors will need to be appointed in different years or successive years?Does it mean Joint auditors will need to be appointed in different years or successive years?

What happens in case of Existing Joint Auditors who have been appointed on the same date earlier? Who’s tenure will end first?

What happens in case of Existing Joint Auditors who have been appointed on the same date earlier? Who’s tenure will end first?

DEF Ltd.

European UnionEuropean Union

November 2011 Crisis” proposed a requirement for audit firm rotation.November 2011 - Green paper “Audit Policy: Lessons from the Crisis” proposed a requirement for audit firm rotation.

European Parliament voted in favor of this recentlyEuropean Parliament voted in favor of this recently

Europeanmust appoint a new auditor European-listed companies, banks and financial institutions must appoint a new auditor every 10 years

Extension of Tenure : If companies put their audit contract up for bid at the decade mark (10 more years) or in case of a jointaudit (14 more years).

Extension of Tenure : If companies put their audit contract up for bid at the decade mark (10 more years) or in case of a joint-audit (14 more years).

U.S.AU.S.A

November 2003 - The U.S Government Accountability Office issued its study – “Public Accounting Firms: Required Study on the Potential Effects of Mandatory Audit Firm Rotation”

November 2003 - The U.S Government Accountability Office issued its study – “Public Accounting Firms: Required Study on the Potential Effects of Mandatory Audit Firm Rotation” - as part of the Sarbanes-Oxley Act.

Congress dismissed Mandatory Auditor rotation in favor of mandatory engagement partner rotationCongress dismissed Mandatory Auditor rotation in favor of mandatory engagement partner rotation

Public Company Accounting Oversight Board (PCAOB) encountered fierce resistance to the mandatory auditor rotation idea, which never got beyond the concept release stage.

Public Company Accounting Oversight Board (PCAOB) encountered fierce resistance to the mandatory auditor rotation idea, which never got beyond the concept release stage.

At present, lead audit partners are rotated At present, lead audit partners are rotated every 5 years.

The US is of the view that this system captures substantially all the benefits of mandatory auditThe US is of the view that this system captures substantially all the benefits of mandatory audit-firm rotation in a cost-effective manner.

ChinaChina

China adopted mandatory auditor rotation rules in 2010China adopted mandatory auditor rotation rules in 2010

Global dominance of the Big Four has been broken hereGlobal dominance of the Big Four has been broken here

Financial institutions and stateundertake an audit tender process every 3 yearsFinancial institutions and state-owned enterprises must undertake an audit tender process every 3 years

An auditor cannot serve the same client for more than 5 consecutive years.An auditor cannot serve the same client for more than 5 consecutive years.

What’s happening in the Other Countries?What’s happening in the Other Countries?

Audit firm rotation only forcompanies areassuchlisted financialinstitutions, insurancecompanies governmentcompanies

Audit firm rotation only forcompanies in specific areassuch aslisted companies, financialinstitutions, banks, insurancecompanies and governmentcompanies.

Pakistan, Italy, Paraguay, Pakistan, Italy, Paraguay, Peru, Poland, Portugal and

Oman

Previously implementedbut abolishedmandatory auditorrotation

Previously implementedbut have now abolishedmandatory auditorrotation.

Canada, Czech Republic, Korea, Latvia, and Slovak

Canada, Czech Republic, Korea, Latvia, Singapore and Slovak Republic

Audit Quality

• Experience and credibilitydevelop over longer tenure

• Knowledge and understanding of company developed over long term - leads to increase in audit quality

• Longer tenure results in greater respect for auditors judgment while challenging management decisions

Cumulative Knowledge

• Removing experienced professionals from the audit team results in loss of knowledge and expertise, accumulated over the years

Concentration of Audits will persistConcentration of Audits will persist

• Few firms have the resources to take up large sophisticated clients

• Internal Company Policies - require Audit to be carried out by the Big 4 firms only

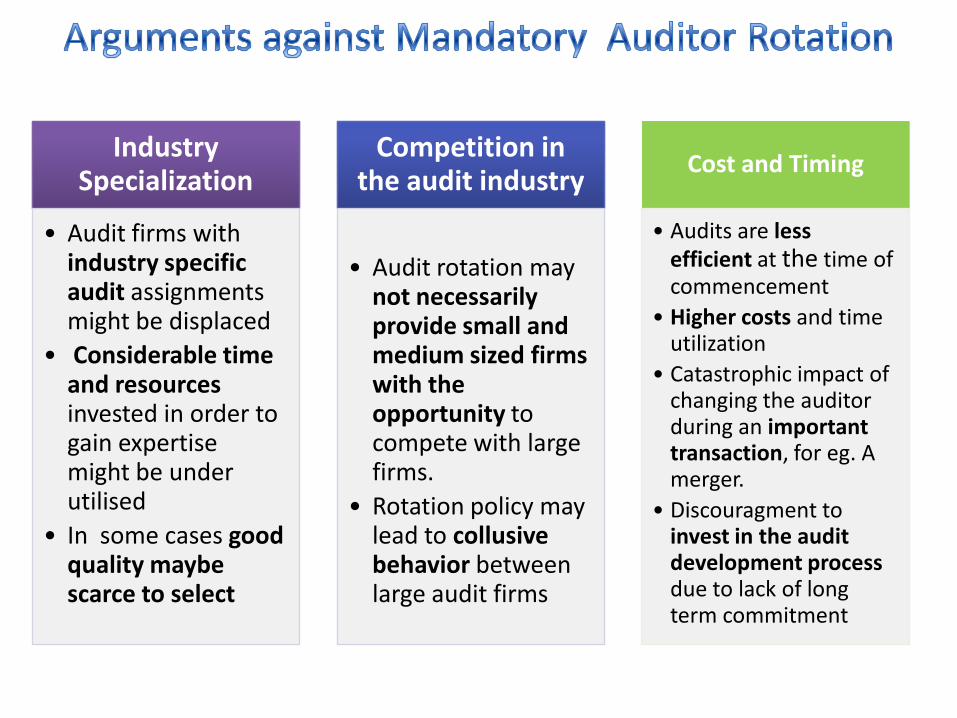

Industry Industry Specialization

• Audit firms with industry specific audit assignments might be displaced

• Considerable time and resources invested in order to gain expertise might be under utilised

• In some cases good quality maybe scarce to select

Competition in Competition in the audit industry

• Audit rotation may not necessarily provide small and medium sized firms with the opportunity to compete with large firms.

• Rotation policy may lead to collusive behavior between large audit firms

Cost and TimingCost and Timing

• Audits are less efficient at the time of commencement

• Higher costs and time utilization

• Catastrophic impact of changing the auditor during an important transaction, for eg. A merger.

• Discouragment to invest in the audit development process due to lack of long term commitment

Global Environment

• For Multinational companies using a single audit network for all their branches- rotation would cause hardship and complexities.

• Variances in the time limit as well as the category of companies to which such policies would apply would be difficult to cope with and comply

Undermines corporate governance structureUndermines corporate governance structure

• Independent audit committees - best placed to determine whether the current auditor is acting with independence and producing a high-quality audit or should be replaced.

• Rotation diminishes this role.

Adverse Effects on the audit professionAdverse Effects on the audit profession

• Increase in costs of recruiting and retaining quality audit personnel

• Partners would have to switch engagements regularly

• Firms would face significant capacity and utilization challenges

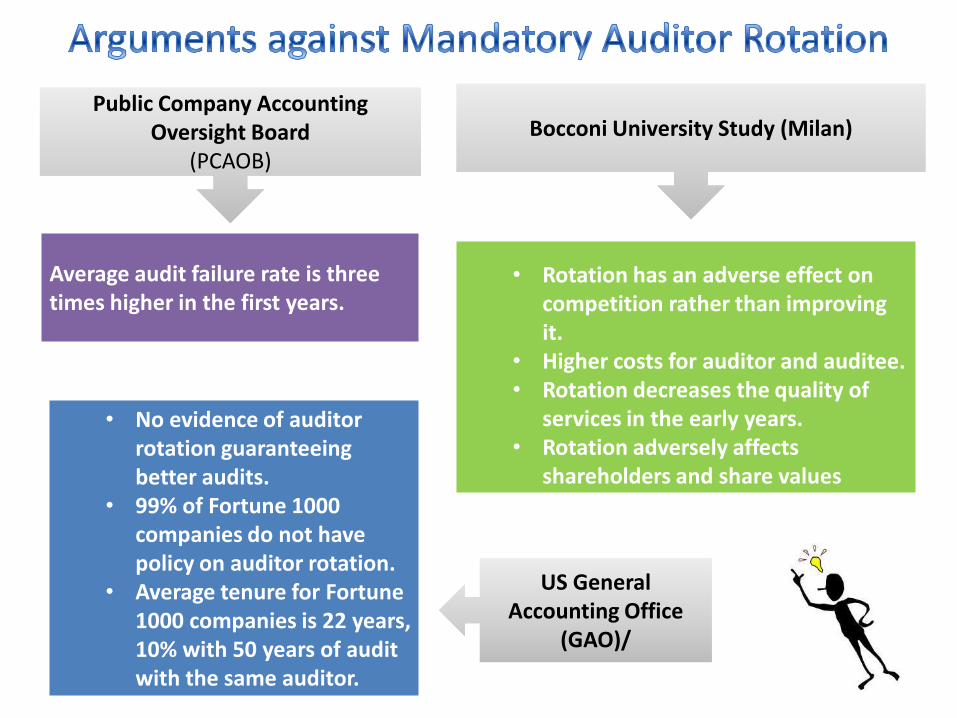

Public Company Accounting Oversight Board

(PCAOB)

Public Company Accounting Oversight Board

(PCAOB)

Average audit failure rate is three times higher in the first years.Average audit failure rate is three times higher in the first years.

• No evidence of auditor

Average tenure for Fortune 1000 companies is 22 years,

• No evidence of auditor rotation guaranteeing better audits.

• 99% of Fortune 1000 companies do not have policy on auditor rotation.

• Average tenure for Fortune 1000 companies is 22 years, 10% with 50 years of audit with the same auditor.

Higher costs for auditor and auditee.

• Rotation has an adverse effect on competition rather than improving it.

• Higher costs for auditor and auditee.• Rotation decreases the quality of

services in the early years.• Rotation adversely affects

shareholders and share values

Bocconi University Study (Milan)Bocconi University Study (Milan)

US General Accounting Office

(GAO)/

US General Accounting Office

(GAO)/

Period In years No. of Members

1949 – 2004 55 1,61,091

2004 – 2014 10 1,14,599

Total 65 2,30,690

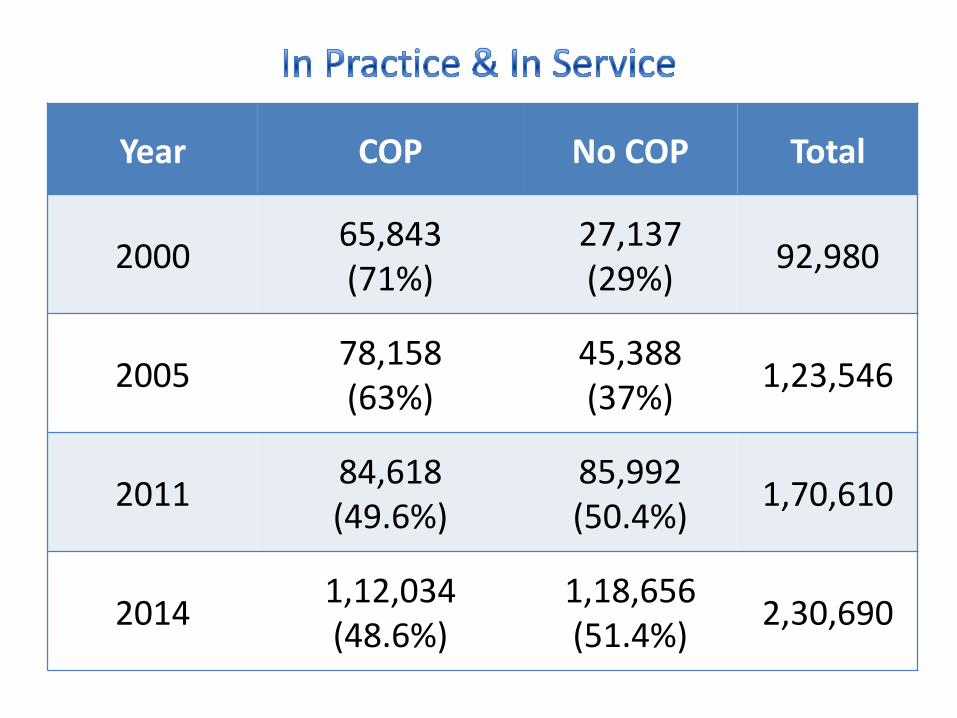

Year COP No COP Total

200065,843(71%)

27,137(29%)

92,980

200578,158(63%)

45,388(37%)

1,23,546

201184,618(49.6%)

85,992(50.4%)

1,70,610

20141,12,034(48.6%)

1,18,656(51.4%)

2,30,690

Partners 2003 2013 2014

Proprietary 33,561 40,903 41,022

2 Partners 7,464 8,742 8,981

3 to 5 3,629 6,579 6,941

6 to 9 824 1,322 1,414

10 to 15 104 291 316

16 to 20 25 56 57

Total 45,607 57,893 58,731

Audit Partner RotationAudit Partner Rotation

Natural turnover of personnel at companies for which audit work isperformedNatural turnover of personnel at companies for which audit work isperformed ensures the relationship is not too cozy

Effective Audit Committees And Greater Transparency Of Their AuditorOversightEffective Audit Committees And Greater Transparency Of Their AuditorOversight

External auditor oversight regimesExternal auditor oversight regimes

Globally consistent auditor independence requirementsGlobally consistent auditor independence requirements

Prohibition of certain non audit consulting services/cap on such fee Prohibition of certain non audit consulting services/cap on such fee

Cap in terms of % of fee from any auditee to the total income of the AuditorCap in terms of % of fee from any auditee to the total income of the Auditor

Appointment of joint auditors – rotation of scope of workAppointment of joint auditors – rotation of scope of work

V/sV/s

ChallengeChallenge OpportunityOpportunity

![Untitled-1 [hclinfosystems.in] · The Company has tied up long term borrowings during the year and repaid a part of its short term borrowings. Net Borrowings ` crores Particulars](https://static.documents.pub/doc/80x56/5e7f6cd958ba933e346222ff/untitled-1-the-company-has-tied-up-long-term-borrowings-during-the-year-and.jpg)