23

On the Convergence of European Lookback Options with Floating Strike in the Binomial Model Fabien Heuwelyckx Universit´ e de Mons (Belgium) [email protected] Warsaw, June 12th 2013

On the Convergence of European Lookback Optionswith Floating Strike in the Binomial Model

Fabien Heuwelyckx

Universite de Mons (Belgium)[email protected]

Warsaw, June 12th 2013

Introduction State of the art The approximation Work in progress

1 Introduction

2 State of the art

3 The approximation

4 Work in progress

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 2 / 21

Introduction State of the art The approximation Work in progress

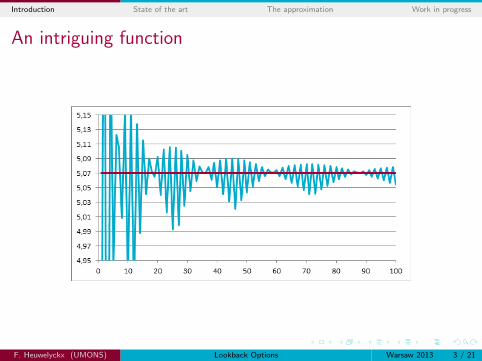

An intriguing function

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 3 / 21

Introduction State of the art The approximation Work in progress

Asymptotic expansion

Study of the behavior of the option price as a function of the number ofsteps n in the Cox-Ross-Rubinstein model. In particular, to write this priceas

Πfln = Πfl

BS +Π1√n

+Π2

n+ O

( 1

n3/2

),

where the coefficients Πi are bounded functions of n.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 4 / 21

Introduction State of the art The approximation Work in progress

Approximation for vanilla options

Diener-Diener (2004)

The evaluation of the European vanilla call in the Cox-Ross-Rubinsteinmodel satisfies the relation

CVn = CV

BS +S0e

− d212

24σ√

2πT

A− 12σ2T (∆2n − 1)

n+ O

(1

n3/2

),

with

∆n = 1− 2

{ln(S0/K)−nσ

√T/n

2σ√

T/n

},

A = −σ2T (6 + d21 + d2

2 ) + 4rT (d21 − d2

2 )− 12r2T 2.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 5 / 21

Introduction State of the art The approximation Work in progress

Other results

Results for some other options are also known:

binary options by Chang and Palmer (2007);

barrier options by Lin and Palmer (2013).

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 6 / 21

Introduction State of the art The approximation Work in progress

Lookback option with floating strike

In the case of the European option:

Payoff for the call: f (T ) = ST − min0≤t≤T

St ,

Payoff for the put: f (T ) = max0≤t≤T

St − ST ,

where St is the price of the underlying at time t and T the time tomaturity.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 7 / 21

Introduction State of the art The approximation Work in progress

Other common notations

r the risk free interest rate,

σ the volatility of the underlying,

un = eσ√

T/n the proportional upward jump,

dn = u−1n the proportional downward jump.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 8 / 21

Introduction State of the art The approximation Work in progress

Cheuk-Vorst lattice (1997)

Modified tree V .

Backward induction.

Value associated with a specific node depends only on the time andon the difference (in powers of un) between the present and thelowest value of the underlying from time t = 0 to the present time.

For the call this difference is the value j such that

Sm =(

min0≤i≤m

Si

)uj

n.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 9 / 21

Introduction State of the art The approximation Work in progress

Option evaluation

Value inside the tree is not the option price.

This value is the number by which we have to multiply the underlyingprice to obtain the corresponding option price:

Cfln (m) = Sm V (j ,m).

A previous node is the expectation of the following two nodes withrespect to the probability

qn = pnune− rT

n ,

with pn the traditional risk-neutral probability.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 10 / 21

Introduction State of the art The approximation Work in progress

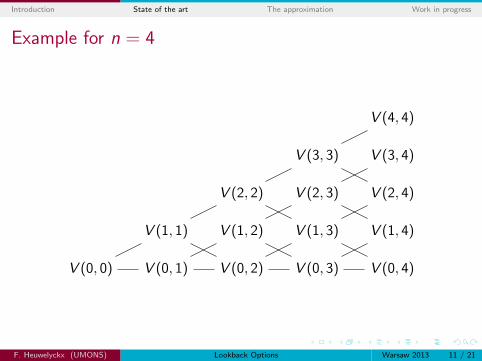

Example for n = 4

V (0, 0)

V (1, 1)

V (0, 1)

V (2, 2)

V (0, 2)

V (1, 2)

V (3, 3)

V (2, 3)

V (1, 3)

V (0, 3)

V (4, 4)

V (3, 4)

V (2, 4)

V (1, 4)

V (0, 4)

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 11 / 21

Introduction State of the art The approximation Work in progress

Value function of the lookback option

Example with S0 = 80, σ = 0.2, r = 0.08 and T = 1.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 12 / 21

Introduction State of the art The approximation Work in progress

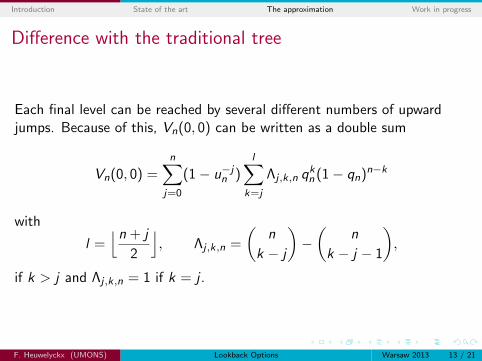

Difference with the traditional tree

Each final level can be reached by several different numbers of upwardjumps. Because of this, Vn(0, 0) can be written as a double sum

Vn(0, 0) =n∑

j=0

(1− u−jn )

l∑k=j

Λj ,k,n qkn (1− qn)n−k

with

l =⌊n + j

2

⌋, Λj ,k,n =

(n

k − j

)−(

n

k − j − 1

),

if k > j and Λj ,k,n = 1 if k = j .

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 13 / 21

Introduction State of the art The approximation Work in progress

Price for a fixed number n

The call price (with n steps) can be deduced from this construction and isS0 Vn(0, 0), with

Vn(0, 0) =Qn(1− dn)

(1− Qn)(1− Qndn)φ1 −

1

1− Qnφ2 +

e−rT

1− Qndnφ3,

where

Qn = qn

1−qn,

φ1 = Bn,qn (bn/2c)− Qn Bn,qn (bn/2c − 1),

φ2 = Qn Bn,1−qn (bn/2c)− Bn,1−qn (bn/2c − 1),

φ3 = Qndn Bn,1−pn (bn/2c)− un Bn,1−pn (bn/2c − 1),

and Bn,p the cumulative distribution function of the binomial distributionwith parameters n and p.F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 14 / 21

Introduction State of the art The approximation Work in progress

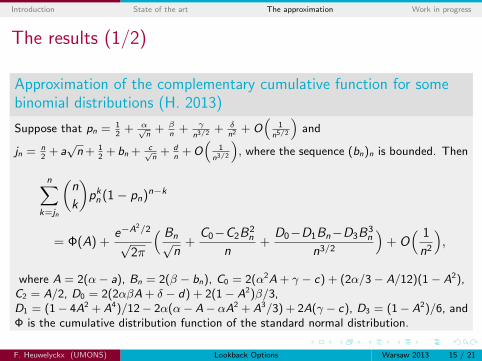

The results (1/2)

Approximation of the complementary cumulative function for somebinomial distributions (H. 2013)

Suppose that pn = 12

+ α√n

+ βn

+ γ

n3/2 + δn2 + O

(1

n5/2

)and

jn = n2

+ a√n+ 1

2+ bn + c√

n+ d

n+O

(1

n3/2

), where the sequence (bn)n is bounded. Then

n∑k=jn

(n

k

)pk

n (1− pn)n−k

= Φ(A) +e−A2/2

√2π

( Bn√n

+C0−C2B

2n

n+

D0−D1Bn−D3B3n

n3/2

)+ O

( 1

n2

),

where A = 2(α− a), Bn = 2(β − bn), C0 = 2(α2A + γ − c) + (2α/3− A/12)(1− A2),C2 = A/2, D0 = 2(2αβA + δ − d) + 2(1− A2)β/3,D1 = (1− 4A2 + A4)/12− 2α(α−A− αA2 + A3/3) + 2A(γ − c), D3 = (1−A2)/6, andΦ is the cumulative distribution function of the standard normal distribution.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 15 / 21

Introduction State of the art The approximation Work in progress

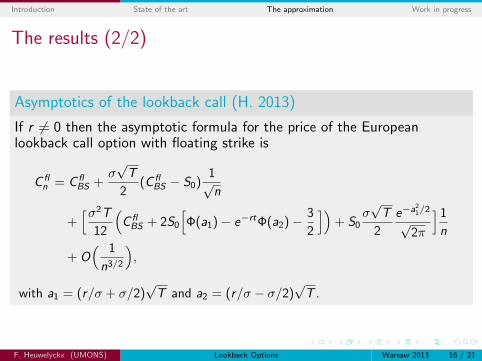

The results (2/2)

Asymptotics of the lookback call (H. 2013)

If r 6= 0 then the asymptotic formula for the price of the Europeanlookback call option with floating strike is

C fln = C fl

BS +σ√T

2(C fl

BS − S0)1√n

+[σ2T

12

(C fl

BS + 2S0

[Φ(a1)− e−rtΦ(a2)− 3

2

])+ S0

σ√T

2

e−a21/2

√2π

]1

n

+ O( 1

n3/2

),

with a1 = (r/σ + σ/2)√T and a2 = (r/σ − σ/2)

√T .

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 16 / 21

Introduction State of the art The approximation Work in progress

Work in progress

Do not restrict the evaluation to time t = 0.

At time t, we have the information for the minimal value of theunderlying between times 0 and t.

We divide the remaining time line in n steps.

The form of the previous tree changes if this minimal value is lessthan the underlying price at time t.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 17 / 21

Introduction State of the art The approximation Work in progress

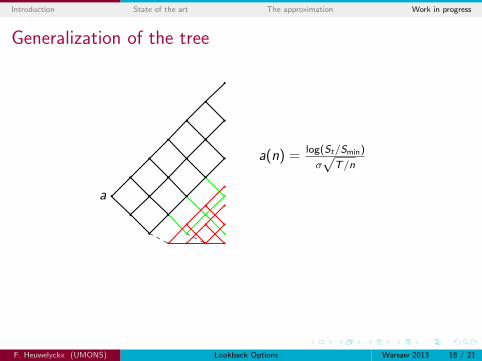

Generalization of the tree

a

a(n) = log(St/Smin)

σ√

T/n

j = a + n

j = a + n − 2bac

j = a + n − 2(bac+ 1)

j = a + n − 2b(a + n)/2c

j = n − bac − 1

j = 0

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 18 / 21

Introduction State of the art The approximation Work in progress

Generalization of the tree

a

a(n) = log(St/Smin)

σ√

T/n

j = a + n

j = a + n − 2bac

j = a + n − 2(bac+ 1)

j = a + n − 2b(a + n)/2c

j = n − bac − 1

j = 0

The number of paths to arrive at a black state can be found as in thebinomial tree.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 18 / 21

Introduction State of the art The approximation Work in progress

Generalization of the tree

a

a(n) = log(St/Smin)

σ√

T/n

j = a + n

j = a + n − 2bac

j = a + n − 2(bac+ 1)

j = a + n − 2b(a + n)/2c

j = n − bac − 1

j = 0

The number of paths to arrive at a green state can be found as in thebinomial tree without forgetting to subtract the paths that have beenabsorbed in the red tree.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 18 / 21

Introduction State of the art The approximation Work in progress

Generalization of the tree

a

a(n) = log(St/Smin)

σ√

T/n

j = a + n

j = a + n − 2bac

j = a + n − 2(bac+ 1)

j = a + n − 2b(a + n)/2c

j = n − bac − 1

j = 0

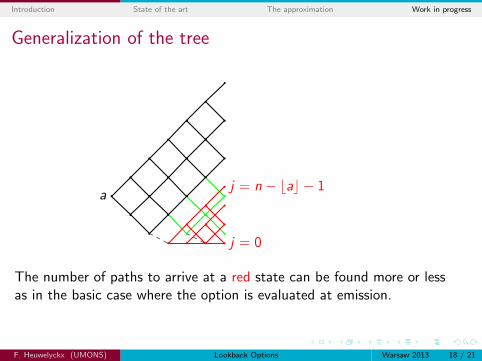

The number of paths to arrive at a red state can be found more or lessas in the basic case where the option is evaluated at emission.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 18 / 21

Introduction State of the art The approximation Work in progress

Thank you for your attention!

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 19 / 21

Introduction State of the art The approximation Work in progress

Bibliography

1 Chang L.B., and Palmer K. (2007): Smooth convergence in thebinomial model. Finance Stoch. 11, 91-105.

2 Cheuk T.H.F, and Vorst T.C.F (1997): Currency lookbackoptions and observation frequency: a binomial approach. J. Int.Money Finance 16, 173-187.

3 Diener F., and Diener M. (2004): Asymptotics of the priceoscillations of a European call option in a tree model. Math. Finance14, 271-293.

4 Heuwelyckx F. (submitted): Convergence of european lookbackoptions with floating strike in the binomial model.http://arxiv.org/abs/1302.2312.

5 Lin J., and Palmer K. (2013): Convergence of barrier optionprices in the binomial model. Math. Finance.

F. Heuwelyckx (UMONS) Lookback Options Warsaw 2013 20 / 21