28

On the Goal Line for Fit4More Joe Kaeser CFO Citigroup’s 20th Annual Global Industrial Manufacturing Conference March 6, 2007

On the Goal Line for Fit4More

Joe KaeserCFO

Citigroup’s20th Annual Global Industrial Manufacturing ConferenceMarch 6, 2007

Page 2 March 2007 Investor Roadshow

Disclaimer

This document contains forward-looking statements and information – that is, statements related to future, not past, events. These statements may be identified by words as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,”“estimates,” “will” or words of similar meaning. Such statements are based on our current expectations and certain assumptions, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Siemens’ control, affect its operations, performance, business strategy and results and could cause the actual results, performance or achievements of Siemens worldwide to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. For us, particular uncertainties arise, among others, from: changes in general economic and business conditions (including margin developments in major business areas); the challenges of integrating major acquisitions and implementing joint ventures and other significant portfolio measures; changes in currency exchange rates and interest rates; introduction of competing products or technologies by other companies; lack of acceptance of new products or services by customers targeted by Siemens worldwide; changes in business strategy; the outcome of investigations and legal proceedings as well as various other factors. More detailed information about certain of these factors is contained in Siemens’ filings with the SEC, which are available on the Siemens website, www.siemens.com and on the SEC’swebsite, www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in the relevant forward-looking statement as expected, anticipated, intended, planned, believed sought, estimated or projected. Siemens does not intend or assume any obligation to update or revise these forward-looking statements in light of developments which differ from those anticipated.

Page 3 March 2007 Investor Roadshow

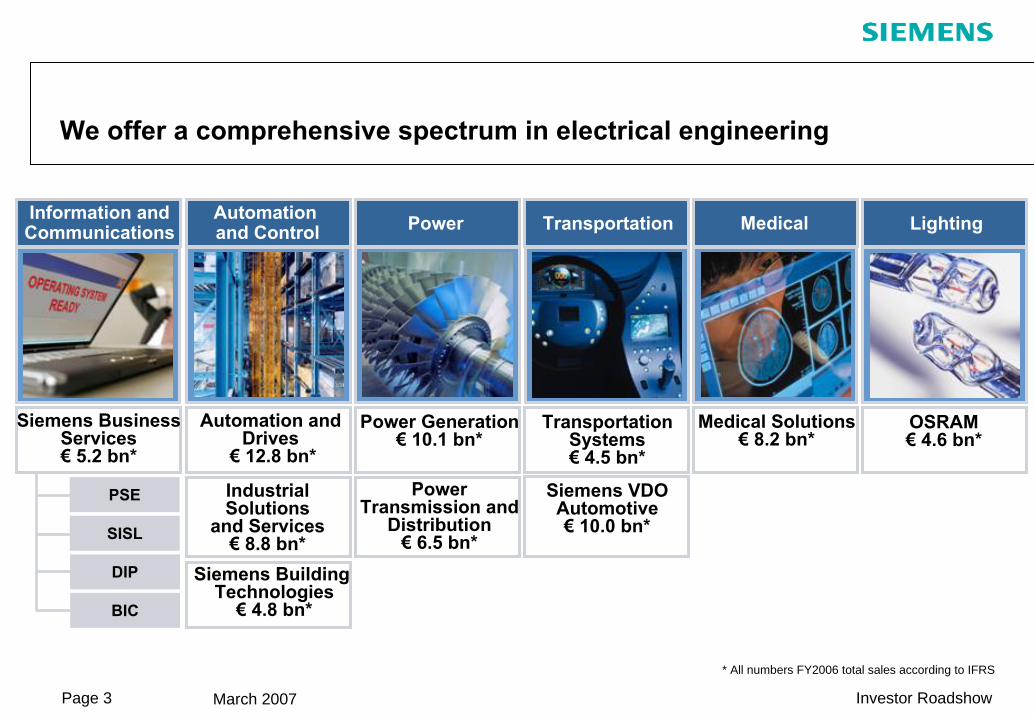

We offer a comprehensive spectrum in electrical engineering

Information andCommunications MedicalPowerAutomation

and Control LightingTransportation

Siemens BusinessServices€ 5.2 bn*

Medical Solutions€ 8.2 bn*

Power Generation€ 10.1 bn*

PowerTransmission and

Distribution€ 6.5 bn*

Automation andDrives

€ 12.8 bn*

Industrial Solutions

and Services€ 8.8 bn*

Siemens Building Technologies

€ 4.8 bn*

OSRAM€ 4.6 bn*

* All numbers FY2006 total sales according to IFRS

TransportationSystems€ 4.5 bn*

Siemens VDOAutomotive€ 10.0 bn*

PSE

SISL

DIP

BIC

Page 4 March 2007 Investor Roadshow

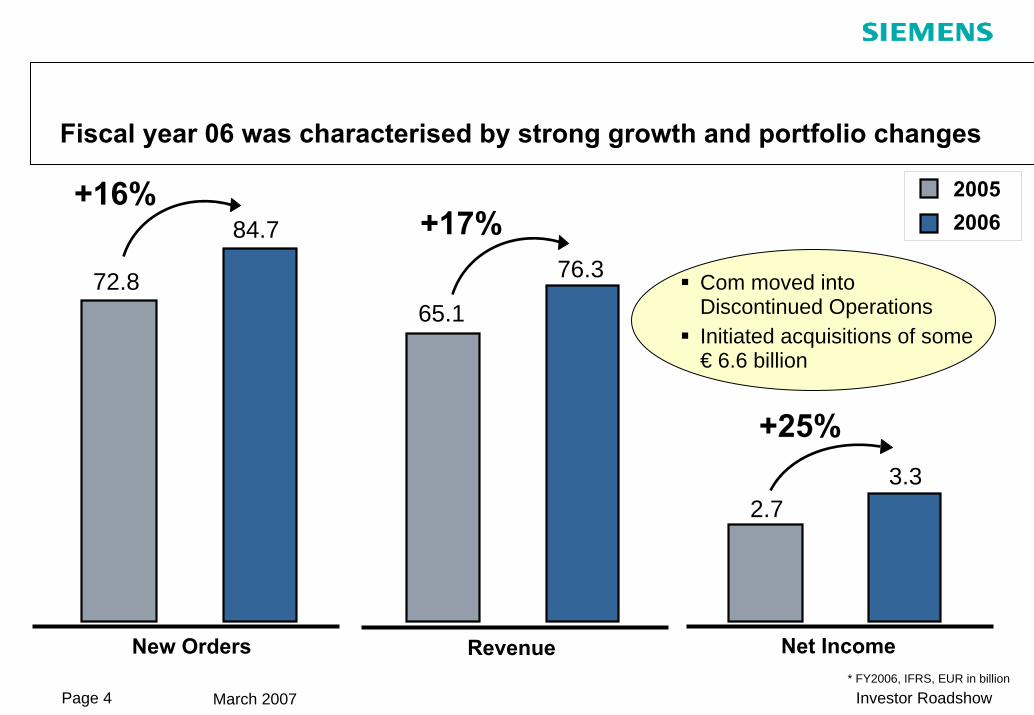

Fiscal year 06 was characterised by strong growth and portfolio changes

* FY2006, IFRS, EUR in billion

New Orders Revenue Net Income

20052006

72.8

84.7

65.1

76.3

2.73.3

+16%+17%

+25%

Com moved intoDiscontinued OperationsInitiated acquisitions of some€ 6.6 billion

Page 5 March 2007 Investor Roadshow

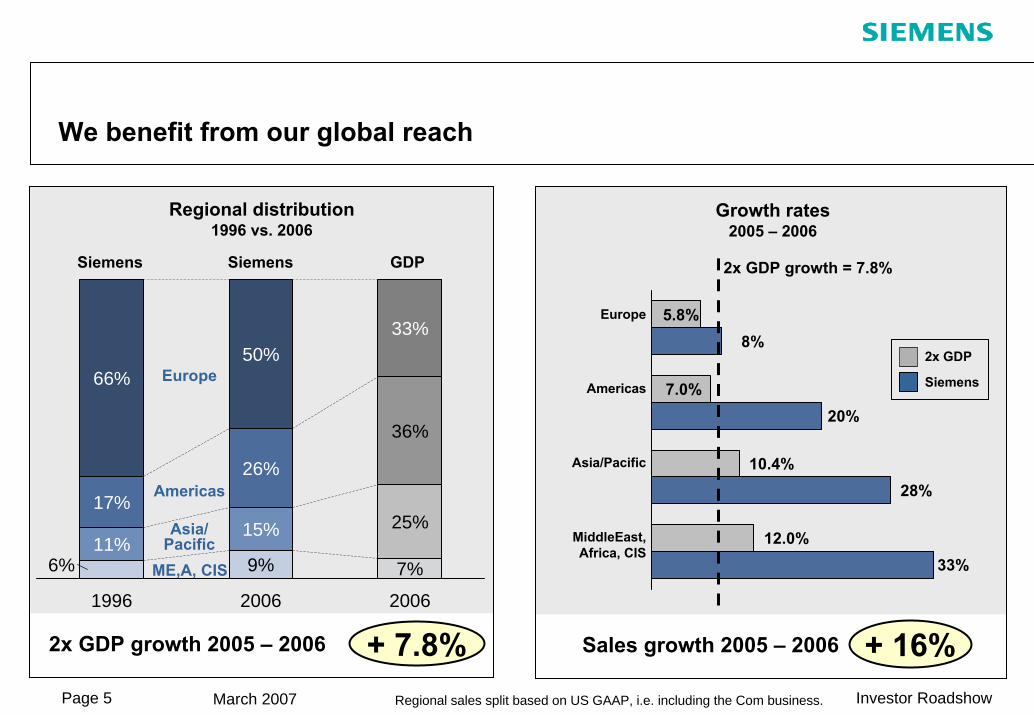

We benefit from our global reach

2x GDP growth 2005 – 2006 + 7.8% Sales growth 2005 – 2006 + 16%

Siemens

66%

17%

11%6%

1996

50%

26%

15%

9%

2006

33%

36%

25%

7%

2006

2x GDP growth = 7.8%

Europe

Americas

Growth rates2005 – 2006

Regional distribution1996 vs. 2006

GDPSiemens

ME,A, CIS

Asia/Pacific

Europe

Americas

Asia/Pacific

MiddleEast,Africa, CIS

Siemens

2x GDP

5.8%

7.0%

10.4%

12.0%

8%

20%

28%

33%

Regional sales split based on US GAAP, i.e. including the Com business.

Page 6 March 2007 Investor Roadshow

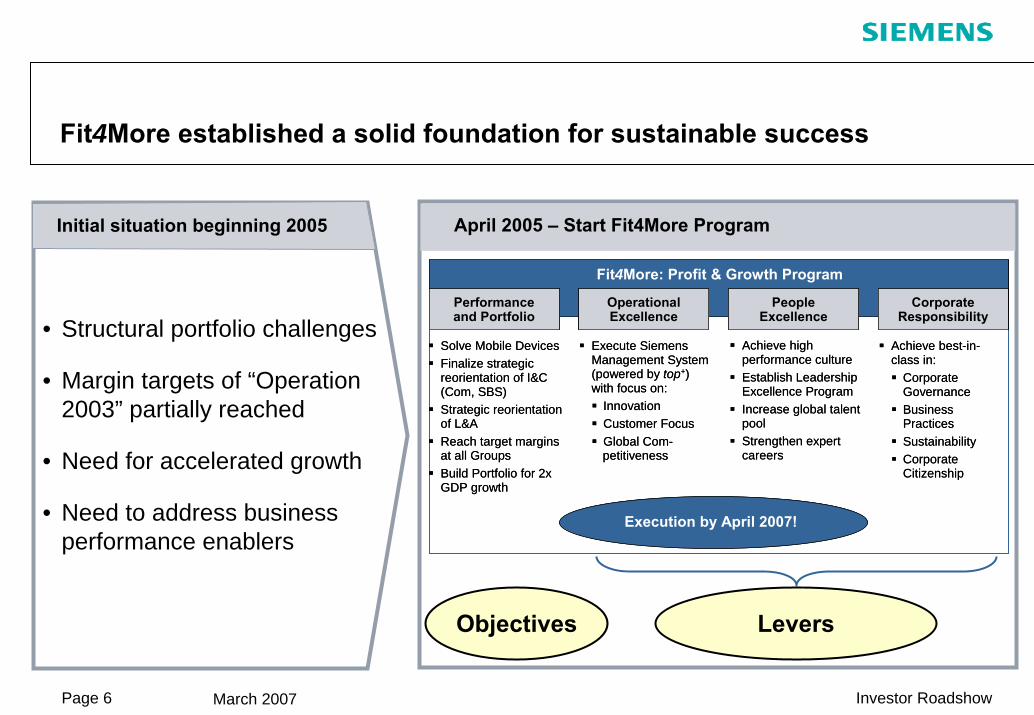

Fit4More established a solid foundation for sustainable success

• Structural portfolio challenges

• Margin targets of “Operation 2003” partially reached

• Need for accelerated growth

• Need to address business performance enablers

Initial situation beginning 2005 April 2005 – Start Fit4More Program

Objectives Levers

Execute Siemens Management System (powered by top+) with focus on:

InnovationCustomer FocusGlobal Com-petitiveness

Achieve high performance cultureEstablish Leadership Excellence ProgramIncrease global talent poolStrengthen expert careers

Solve Mobile DevicesFinalize strategic reorientation of I&C (Com, SBS) Strategic reorientation of L&AReach target margins at all GroupsBuild Portfolio for 2x GDP growth

Achieve best-in-class in:

Corporate GovernanceBusiness PracticesSustainabilityCorporate Citizenship

Fit4More: Profit & Growth Program

Performanceand Portfolio

OperationalExcellence

CorporateResponsibility

PeopleExcellence

Execution by April 2007!

Execute Siemens Management System (powered by top+) with focus on:

InnovationCustomer FocusGlobal Com-petitiveness

Achieve high performance cultureEstablish Leadership Excellence ProgramIncrease global talent poolStrengthen expert careers

Solve Mobile DevicesFinalize strategic reorientation of I&C (Com, SBS) Strategic reorientation of L&AReach target margins at all GroupsBuild Portfolio for 2x GDP growth

Achieve best-in-class in:

Corporate GovernanceBusiness PracticesSustainabilityCorporate Citizenship

Fit4More: Profit & Growth Program

Performanceand PortfolioPerformanceand Portfolio

OperationalExcellenceOperationalExcellence

CorporateResponsibility

CorporateResponsibility

PeopleExcellence

PeopleExcellence

Execution by April 2007!

Page 7 March 2007 Investor Roadshow

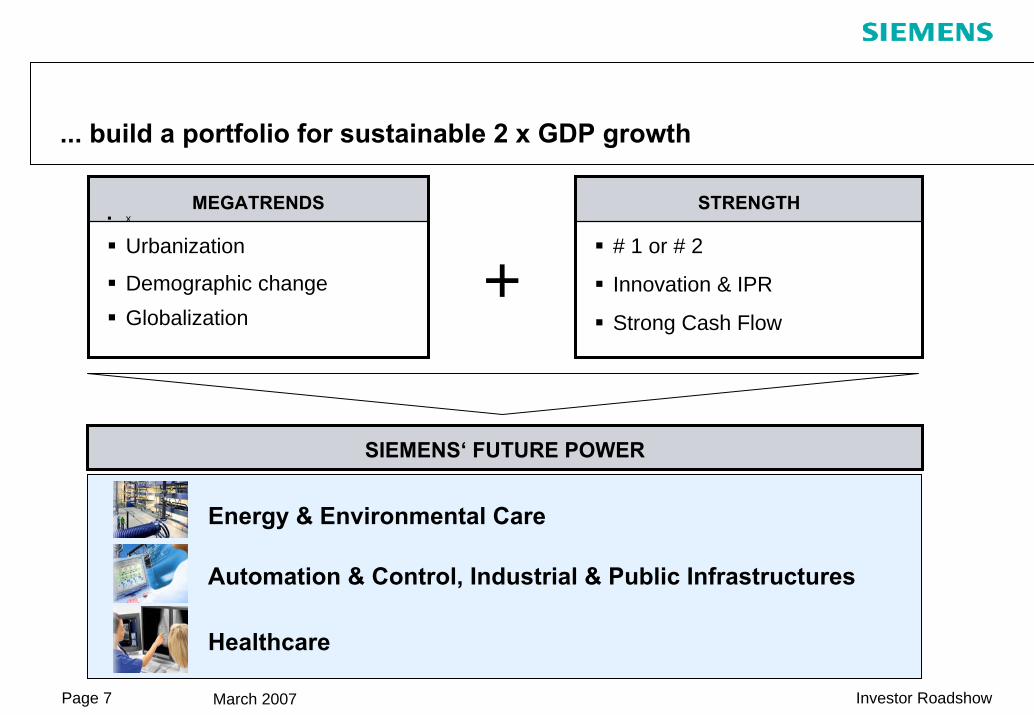

... build a portfolio for sustainable 2 x GDP growth

MEGATRENDSx

Urbanization

Demographic changeGlobalization

STRENGTH

# 1 or # 2

Innovation & IPR

Strong Cash Flow

Healthcare

Energy & Environmental Care

Automation & Control, Industrial & Public Infrastructures

SIEMENS‘ FUTURE POWER

+

Page 8 March 2007 Investor Roadshow

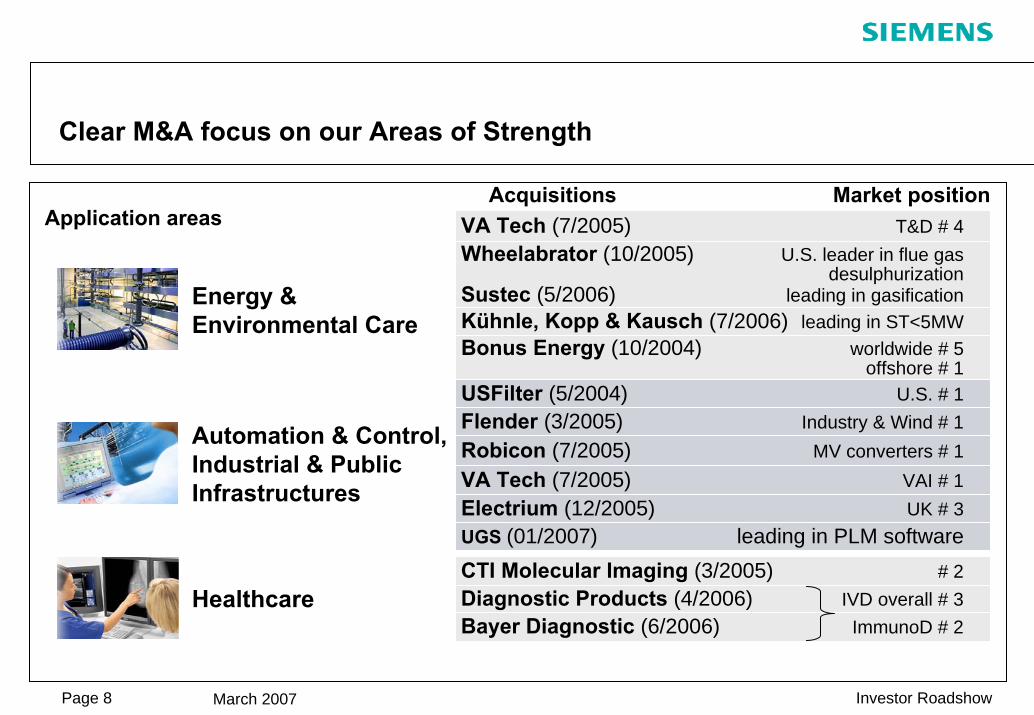

Clear M&A focus on our Areas of Strength

Market position

CTI Molecular Imaging (3/2005) # 2Diagnostic Products (4/2006) IVD overall # 3Bayer Diagnostic (6/2006) ImmunoD # 2

Healthcare

Energy & Environmental Care

Automation & Control, Industrial & Public Infrastructures

AcquisitionsVA Tech (7/2005) T&D # 4Wheelabrator (10/2005) U.S. leader in flue gas

desulphurizationSustec (5/2006) leading in gasification

Electrium (12/2005) UK # 3UGS (01/2007) leading in PLM software

Kühnle, Kopp & Kausch (7/2006) leading in ST<5MWBonus Energy (10/2004) worldwide # 5

offshore # 1USFilter (5/2004) U.S. # 1Flender (3/2005) Industry & Wind # 1Robicon (7/2005) MV converters # 1VA Tech (7/2005) VAI # 1

Application areas

Page 9 March 2007 Investor Roadshow

Key Figures Q1 FY 2007 – Operational Leverage is kicking in

in millions of eurosQ1

FY 20071) Δ

24,582 + 4%

+ 6%

+51%

+18%2)

+0.11

—

19,068

Group profit from Operations(continuing operations) 1,631

Income from continuing operations 714

Net Cash from operating and investingactivities (continuing operations)

(1,160)

0.75

New orders(continuing operations)

Revenue(continuing operations)

EPS from continuing operations (in euros)(basic, attributable to shareholders of Siemens AG)

1) Q1 FY2007 IFRS – new organization2) Includes € 423 million GIS charge. +87% year-on-year change excluding this charge.

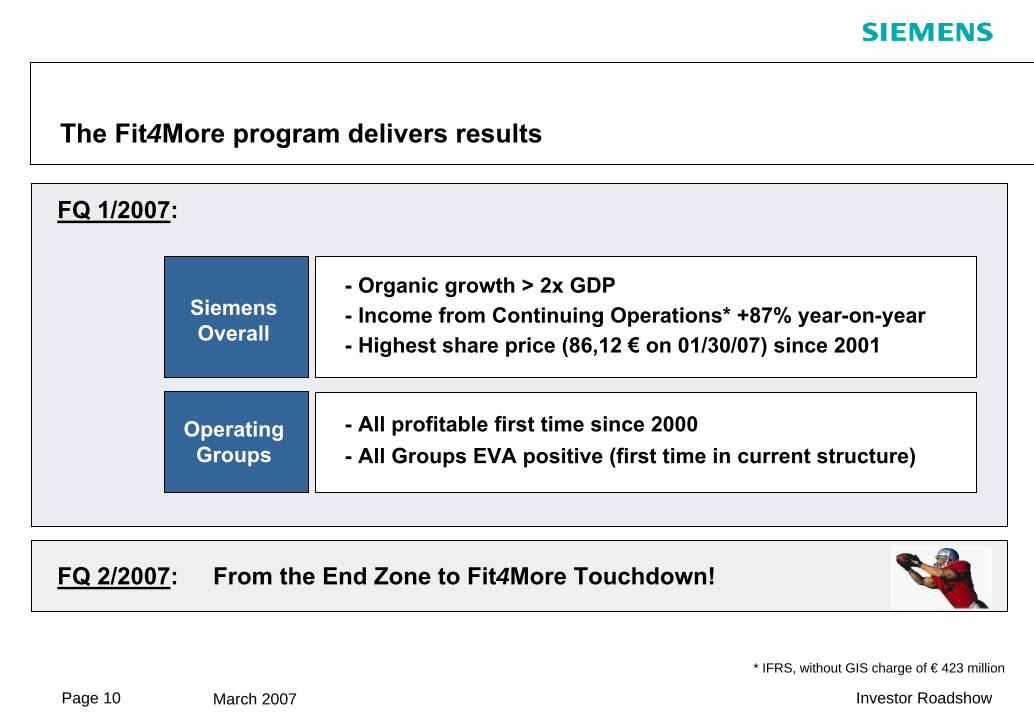

Page 10 March 2007 Investor Roadshow

The Fit4More program delivers results

- Organic growth > 2x GDP- Income from Continuing Operations* +87% year-on-year

- All profitable first time since 2000- All Groups EVA positive (first time in current structure)

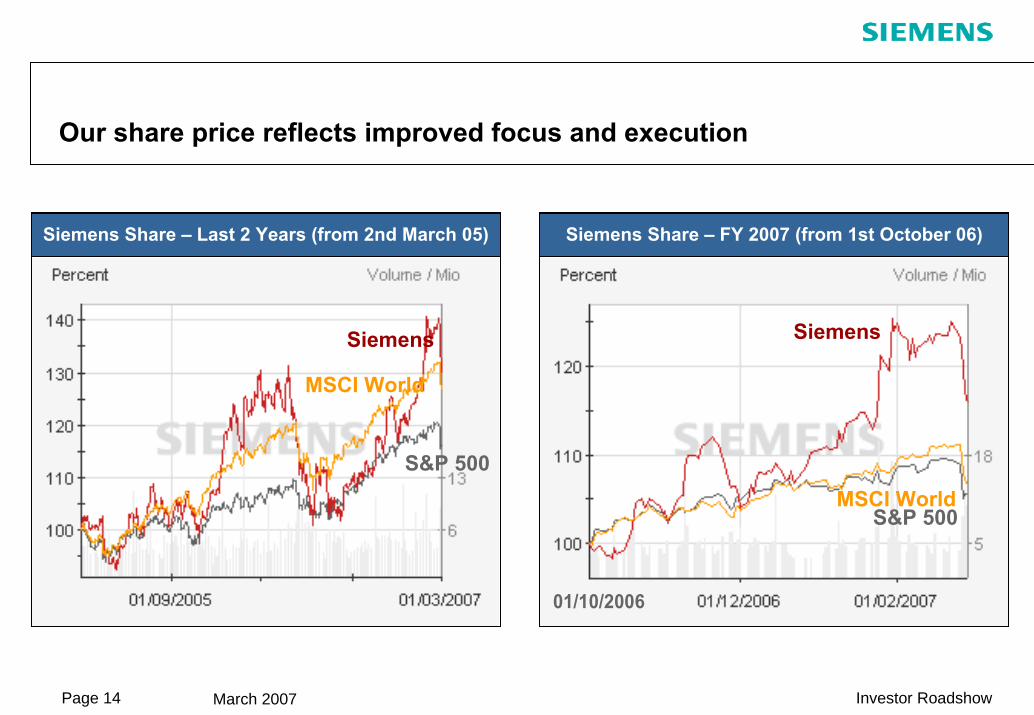

- Highest share price (86,12 € on 01/30/07) since 2001

FQ 1/2007:

FQ 2/2007: From the End Zone to Fit4More Touchdown!

* IFRS, without GIS charge of € 423 million

SiemensOverall

OperatingGroups

Page 11 March 2007 Investor Roadshow

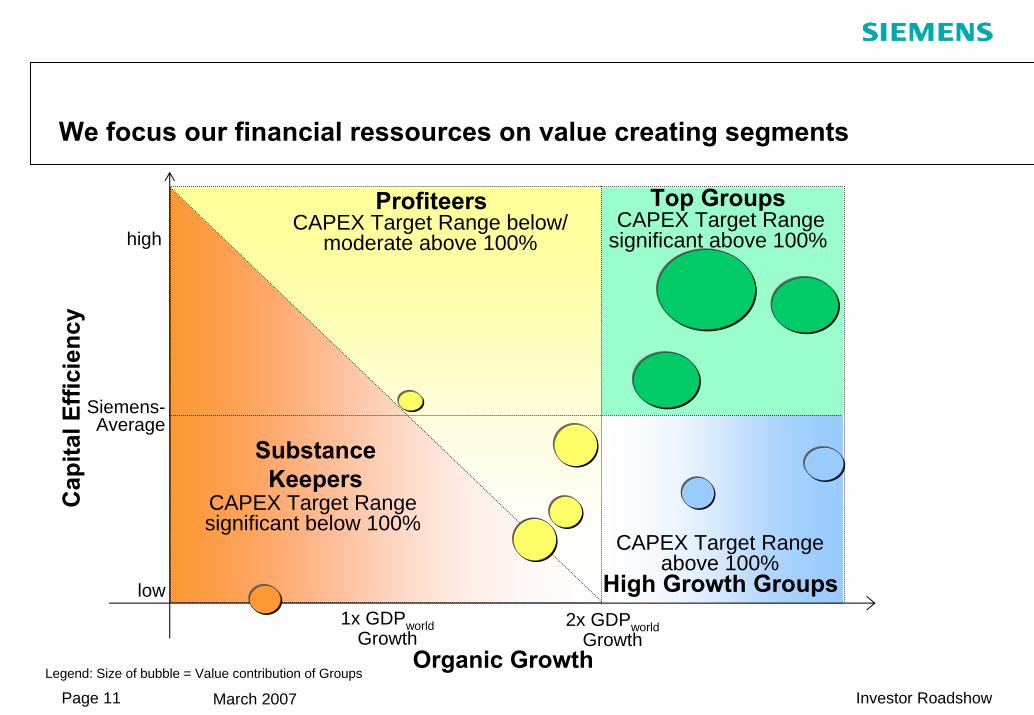

We focus our financial ressources on value creating segments

Legend: Size of bubble = Value contribution of GroupsOrganic Growth

Siemens-Average

2x GDPworldGrowth

high

low

Cap

ital E

ffici

ency

Top GroupsCAPEX Target Range

significant above 100%

High Growth Groups

Substance Keepers

CAPEX Target Range above 100%

1x GDPworldGrowth

CAPEX Target Range significant below 100%

ProfiteersCAPEX Target Range below/

moderate above 100%

Page 12 March 2007 Investor Roadshow

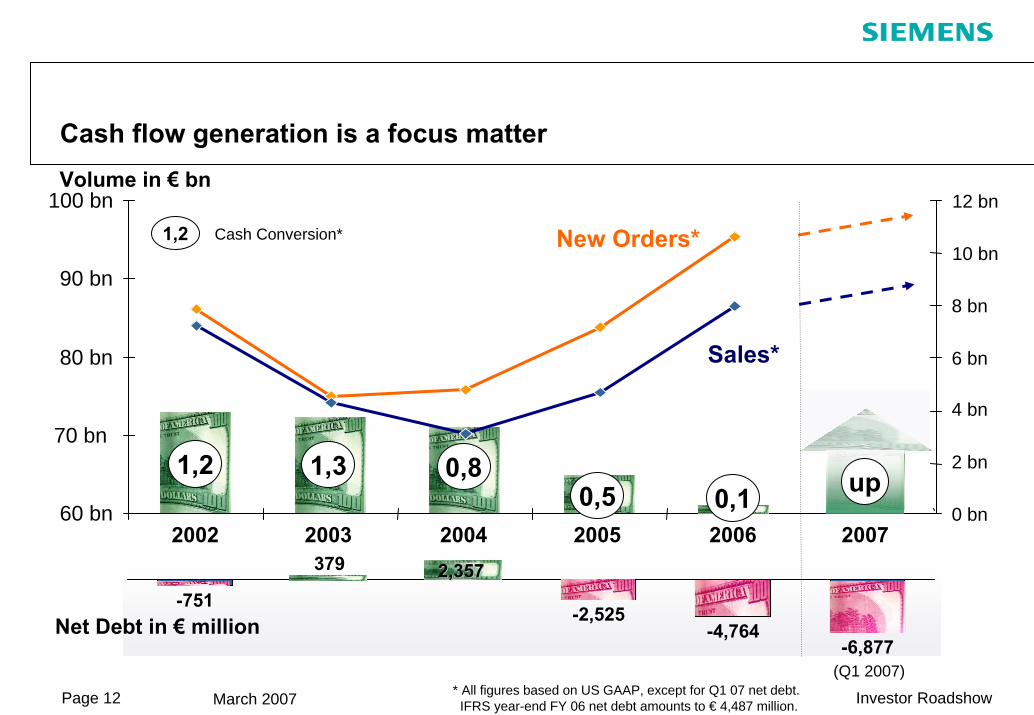

-751

379

-2,525-4,764

-6,877(Q1 2007)

Cash flow generation is a focus matterVolume in € bn

1,2 1,3 0,8

1,2 Cash Conversion*

60 bn

70 bn

80 bn

90 bn

100 bn

2002 2003 2004 2005 2006 20070 bn

2 bn

4 bn

6 bn

8 bn

10 bn

12 bn

0,10,5up

2,3572,357

up

Net Debt in € million

* All figures based on US GAAP, except for Q1 07 net debt.IFRS year-end FY 06 net debt amounts to € 4,487 million.

Sales*

New Orders*

Page 13 March 2007 Investor Roadshow

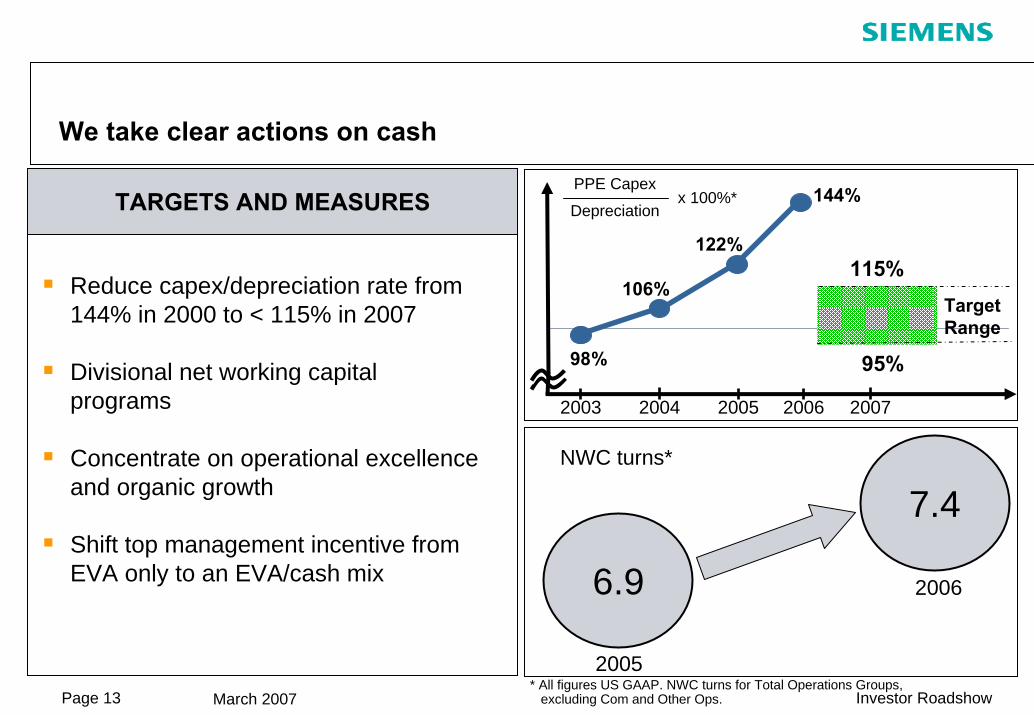

We take clear actions on cash

Reduce capex/depreciation rate from 144% in 2000 to < 115% in 2007

Divisional net working capital programs

Concentrate on operational excellence and organic growth

Shift top management incentive from EVA only to an EVA/cash mix

7.4

6.9

2005

2006

NWC turns*

* All figures US GAAP. NWC turns for Total Operations Groups,excluding Com and Other Ops.

2003 2006

TargetRange

PPE Capex

Depreciation

115%

95%

2004 2005 2007

98%

106%

x 100%*

122%

144%TARGETS AND MEASURES

Page 14 March 2007 Investor Roadshow

Our share price reflects improved focus and execution

Siemens

MSCI World

Siemens

S&P 500MSCI World

Siemens Share – FY 2007 (from 1st October 06)Siemens Share – Last 2 Years (from 2nd March 05)

S&P 500

01/10/2006

Page 15 March 2007 Investor Roadshow

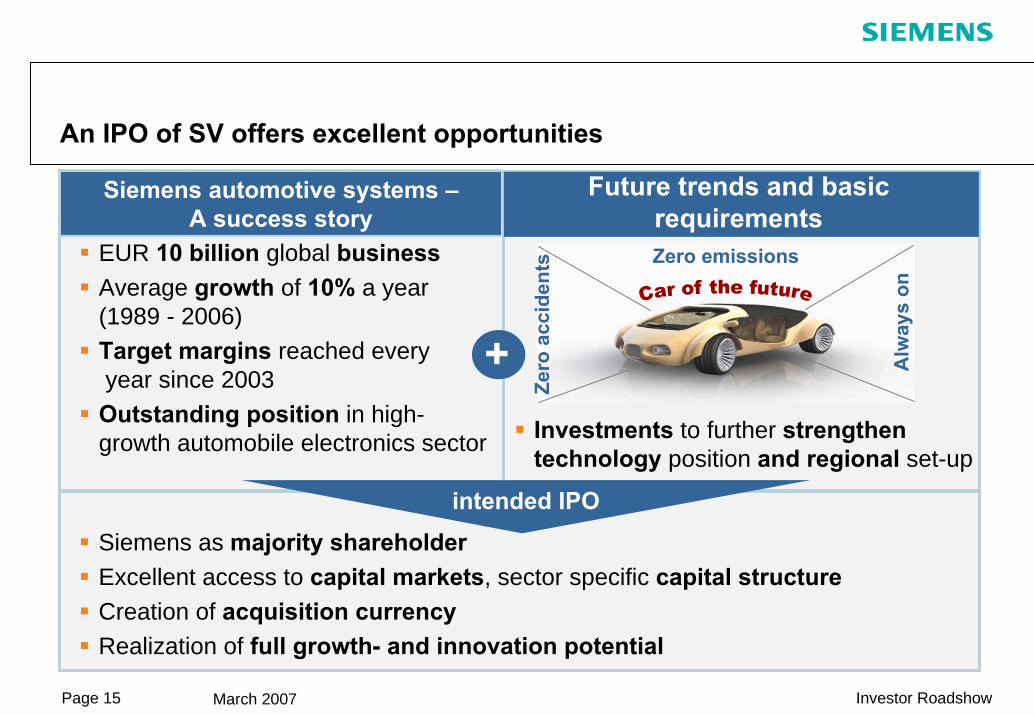

An IPO of SV offers excellent opportunities

Future trends and basic requirements

Siemens automotive systems –A success story

Investments to further strengthen technology position and regional set-up

Siemens as majority shareholderExcellent access to capital markets, sector specific capital structureCreation of acquisition currencyRealization of full growth- and innovation potential

+

intended IPO

Alw

ays

on

Zero emissions

Zero

acc

iden

tsEUR 10 billion global businessAverage growth of 10% a year (1989 - 2006)Target margins reached every year since 2003Outstanding position in high-growth automobile electronics sector

Page 16 March 2007 Investor Roadshow

Outlook for fiscal 2007

1. We will reach our Fit4More goals

Growth of 2x global GDP (w/o effects from deconsolidation)

All Groups expected to reach target margins

2. Expect a New Target System including Capital Efficiency Goal for Siemens

Page 17 March 2007 Investor Roadshow

Appendix

Page 18 March 2007 Investor Roadshow

CAGR 1977–2006: 5.9%

30 years history of continuous dividend payment

20 years of regular dividend increases

0.0

0.4

0.8

1.2

1.6

divi

dend

/ sh

are

(€)

2.0

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

special dividend€ 0.67 Infineon IPO

Page 19 March 2007 Investor Roadshow

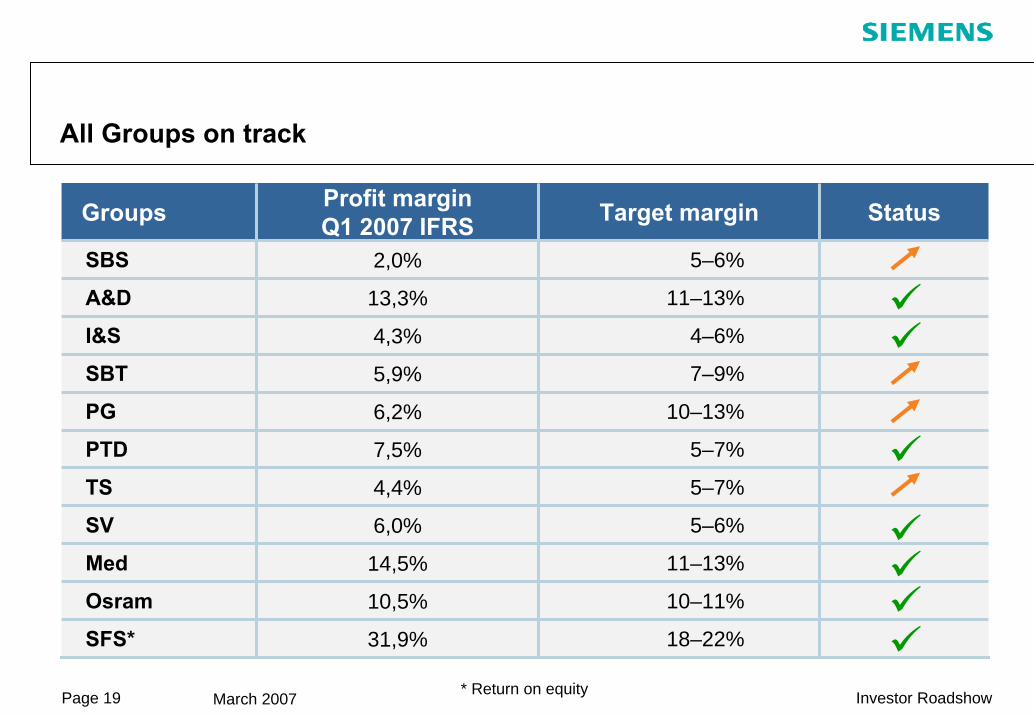

All Groups on track

Groups Profit marginQ1 2007 IFRS Target margin Status

SBS 2,0%

13,3%

4,3%

5,9%

6,2%

7,5%

4,4%

6,0%

14,5%

10,5%

31,9%

5–6%

A&D 11–13%

I&S 4–6%

SBT 7–9%

PG 10–13%

PTD 5–7%

TS 5–7%

SV 5–6%

Med 11–13%

Osram 10–11%

SFS* 18–22%

* Return on equity

Page 20 March 2007 Investor Roadshow

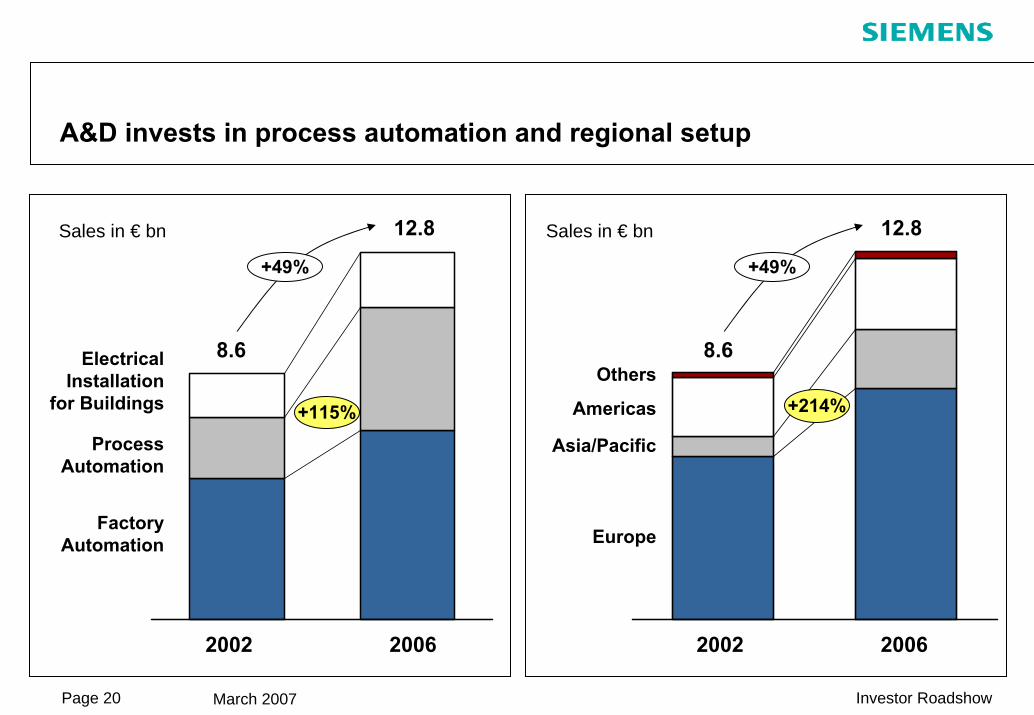

A&D invests in process automation and regional setup

2002 2006

ElectricalInstallation

for Buildings

ProcessAutomation

FactoryAutomation

+115%

Sales in € bn

8.6

12.8

+49%

Asia/Pacific

Americas

Europe

Others+214%

2002 2006

Sales in € bn

8.6

12.8

+49%

Page 21 March 2007 Investor Roadshow

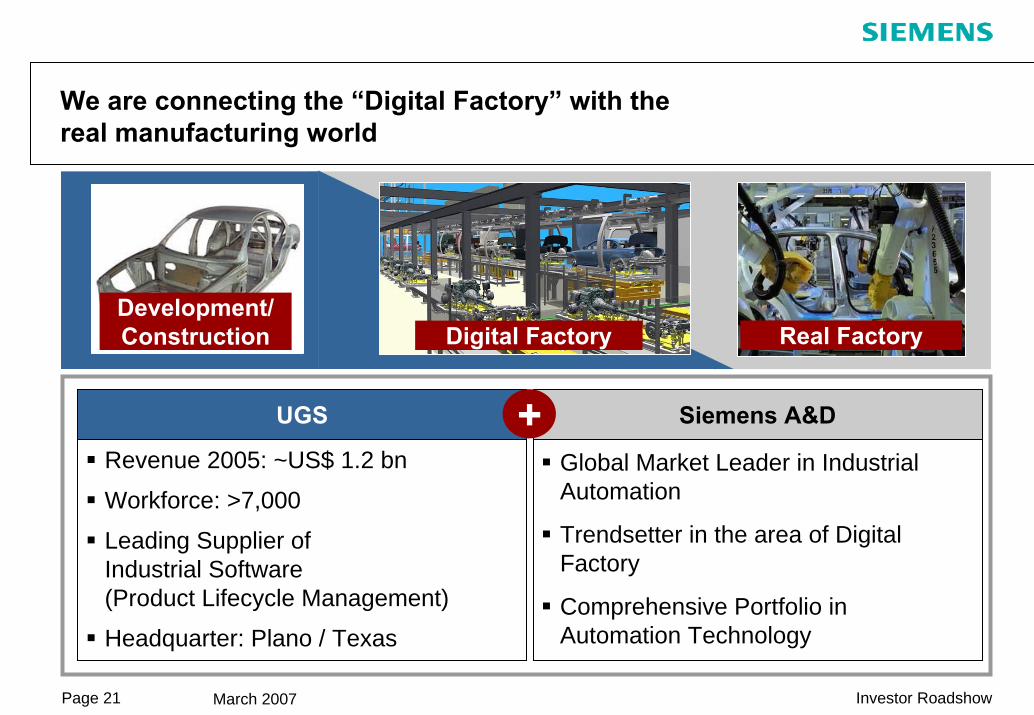

We are connecting the “Digital Factory” with the real manufacturing world

Global Market Leader in Industrial Automation

Trendsetter in the area of Digital Factory

Comprehensive Portfolio in Automation Technology

Siemens A&D

Revenue 2005: ~US$ 1.2 bn

Workforce: >7,000

Leading Supplier ofIndustrial Software (Product Lifecycle Management)

Headquarter: Plano / Texas

UGS +

Development/ Construction Digital Factory Real Factory

Page 22 March 2007 Investor Roadshow

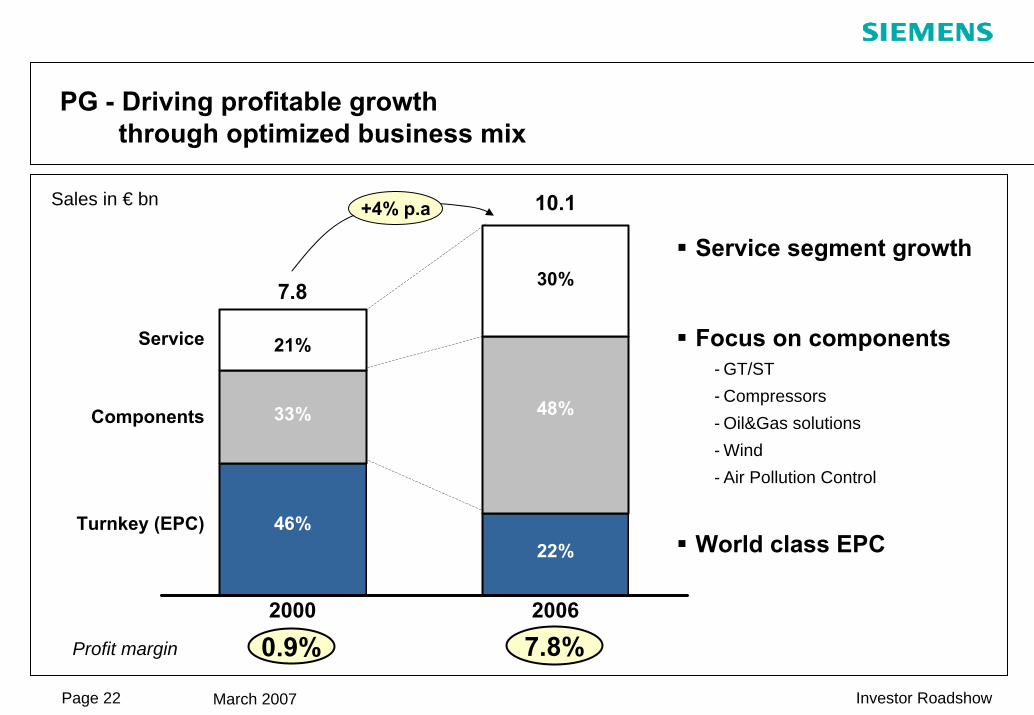

Sales in € bn

21%

33%

46%

7.8

2000

30%

48%

22%

10.1

2006

Service

Components

Turnkey (EPC)

Focus on components- GT/ST- Compressors- Oil&Gas solutions- Wind - Air Pollution Control

PG - Driving profitable growth through optimized business mix

World class EPC

Service segment growth

Profit margin 0.9% 7.8%

+4% p.a

Page 23 March 2007 Investor Roadshow

Clean energy offers multiple growth opportunities

Wind2.3 MW onshore turbine3.6 MW offshore turbine+ 195% orders+ 350% profitEurope's largest wind park€ 350 mn order value

GasificationSustec IGCCCO2-free power plant (option)Fuel flexibilityLower emissionsReduction of investment costIncrease of efficiency

CleanEnergy

Efficiency increase targets43% >50% (lignite)47% >53% (hard coal)58% >60% (CCPP)

SGT5-8000H

Air Pollution ControlWheelabratorAdvanced Burner TechnologyOrders +56%Book to Bill >2

Geothermal Power StationsConversion of heat from low-temperature springsinto electrical energyCO2-emission free base load supplyAdditional Service business opportunities

Page 24 March 2007 Investor Roadshow

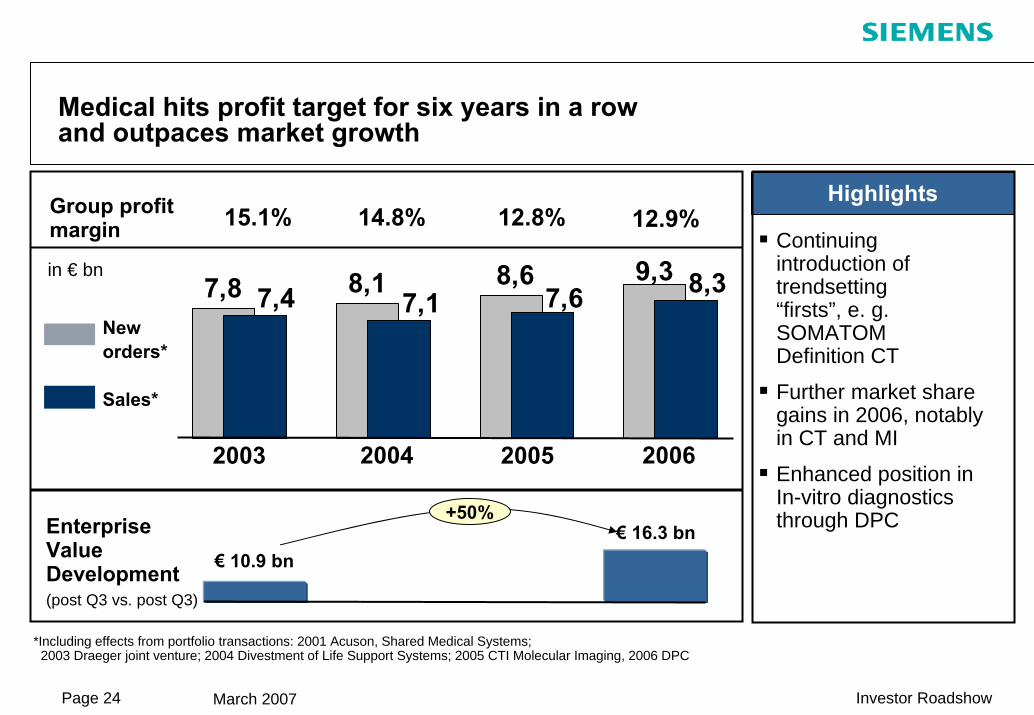

Medical hits profit target for six years in a row and outpaces market growth

Neworders*

Sales*

15.1% 14.8% 12.8%Group profitmargin Continuing

introduction of trendsetting “firsts”, e. g. SOMATOMDefinition CT

Further market share gains in 2006, notablyin CT and MI

Enhanced position in In-vitro diagnostics through DPC

*Including effects from portfolio transactions: 2001 Acuson, Shared Medical Systems; 2003 Draeger joint venture; 2004 Divestment of Life Support Systems; 2005 CTI Molecular Imaging, 2006 DPC

in € bn

12.9%Highlights

EnterpriseValueDevelopment(post Q3 vs. post Q3)

€ 10.9 bn€ 16.3 bn

+50%

9,37,8 8,1 8,67,4 7,1 7,6 8,3

2003 2004 2005 2006

Page 25 March 2007 Investor Roadshow

Pflege

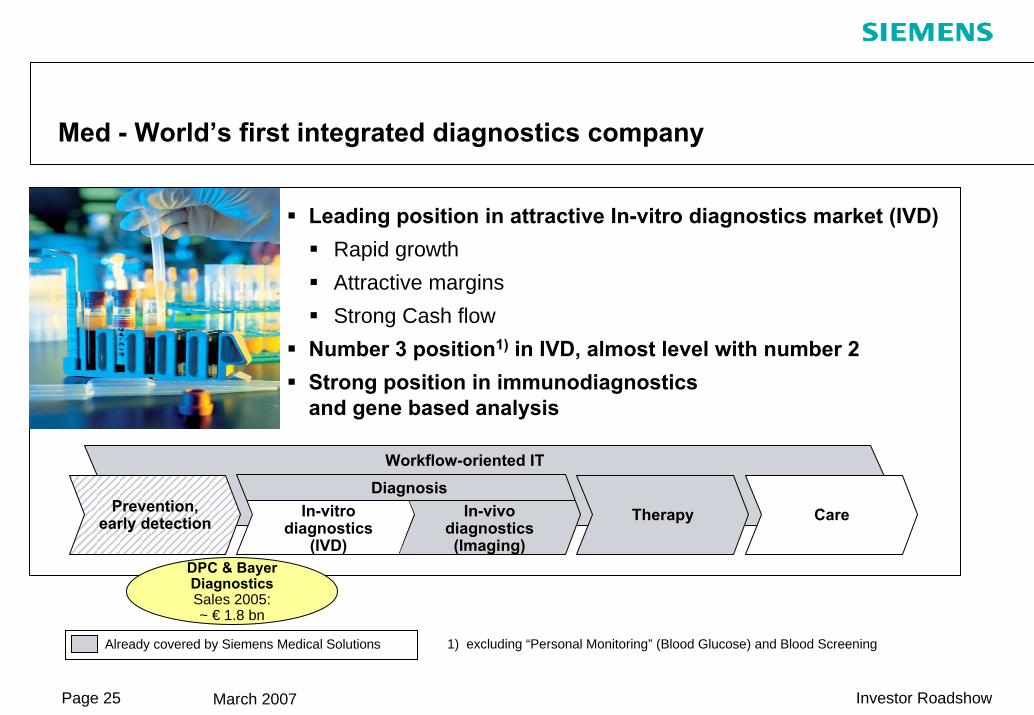

Med - World’s first integrated diagnostics company

1) excluding “Personal Monitoring” (Blood Glucose) and Blood ScreeningAlready covered by Siemens Medical Solutions

Leading position in attractive In-vitro diagnostics market (IVD)Rapid growthAttractive marginsStrong Cash flow

Number 3 position1) in IVD, almost level with number 2Strong position in immunodiagnostics and gene based analysis

CareTherapyPrevention,early detection

In-vivo diagnostics (Imaging)

DiagnosisWorkflow-oriented IT

In-vitro diagnostics

(IVD)DPC & Bayer DiagnosticsSales 2005: ~ € 1.8 bn

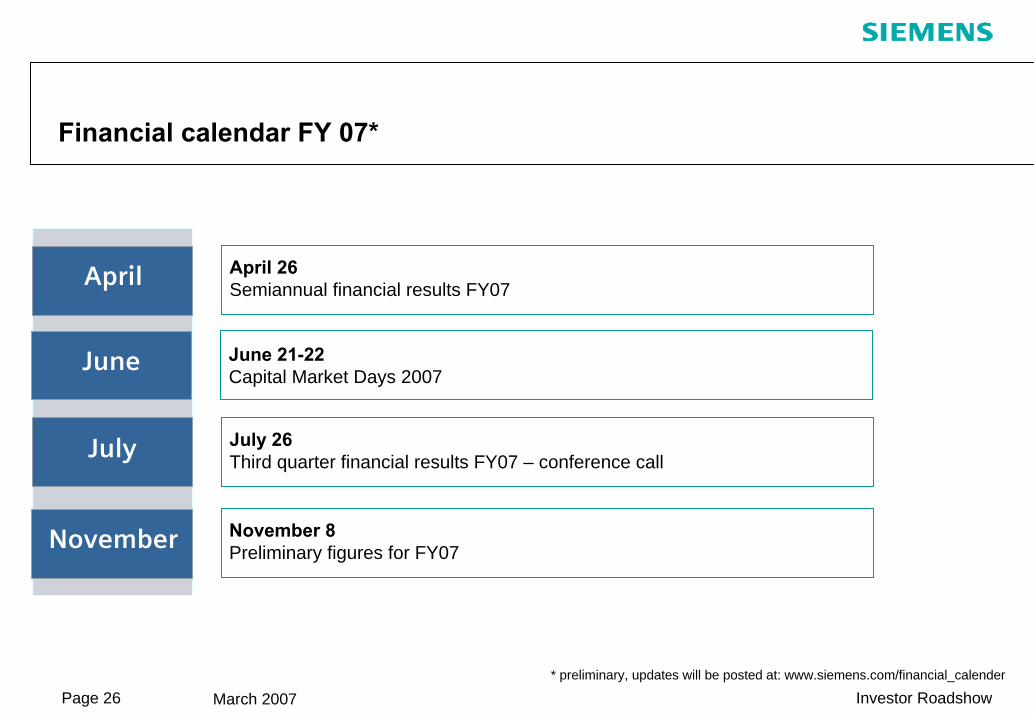

Page 26 March 2007 Investor Roadshow

June

April

June 21-22Capital Market Days 2007

April 26Semiannual financial results FY07

Financial calendar FY 07*

July July 26Third quarter financial results FY07 – conference call

November November 8Preliminary figures for FY07

* preliminary, updates will be posted at: www.siemens.com/financial_calender

Page 27 March 2007 Investor Roadshow

Reconciliations and definitions

”Group profit from Operations” is reconciled to ”Income before income taxes” of Operations under ”Reconciliation to financial statements” on the table ”Segment information”. See ”Financial Publications/Quarterly Reports, FY2007Q1, Financial Statements” at our Investor Relations website under www.siemens.com

ROE (Return on equity) margin for SFS was calculated as SFS' income before income taxes divided by the allocated equity for SFS.Allocated equity for SFS as of September 30, 2006 was € 1,131 million.

The allocated equity for SFS is determined and influenced by the respective credit ratings of the rating agencies and by the expected size and quality of its portfolio of leasing and factoring assets and equity investments and is determined annually. This allocation is designed to cover the risks of the underlying business and is in line with common credit risk management banking standards. The actual risk profile of the SFS portfolio is monitored and controlled monthly and is evaluated against the allocated equity.

Siemens ties a portion of its executive incentive compensation to achieving economic value added (EVA) targets. EVA measures theprofitability of a business (using Group profit for the Operating Groups and income before income taxes for the Financing and Real Estate businesses as a base) against the additional cost of capital used to run a business (using Net capital employed for the operations Groups and risk-adjusted equity for the Financing and Real estate businesses as a base). A positive EVA means that a business has earned more than its cost of capital, whereas a negative EVA means that a business has earned less than its cost ofcapital. Depending on the EVA development year-over-year, a business is defined as value-creating or value-destroying. Other organizations that use EVA may define and calculate EVA differently.

Page 28 March 2007 Investor Roadshow

Siemens Investor Relations Team

Webpage: http://www.siemens.com Investor Relations

e-mail: [email protected]

Telephone: +49-89-636-32474

Fax: +49-89-636-32830

Marcus Desimoni +49-89-636-32445

Roland Bischofberger +49-89-636-36165

Frank Heffter +49-89-636-34095

Irina Pchelova +49-89-636-33693

Christof Schwab +49-89-636-32677

Susanne Wölfinger +49-89-636-30639