79

Annual Report 2011 One world...

| Date post: | 31-Mar-2018 |

| Category: |

Documents |

| Upload: | truongkhue |

| View: | 219 times |

| Download: | 3 times |

Annual Report 2011

One world...

Orascom Telecom Holdings Annual Report 2011 03Orascom Telecom Holdings Annual Report 2011B

Financial highlights

Strong performance across the board

Contents :

Financial highlights 03OTH at a glance 04Letter from the Chairman and CEO 06Business review 08Social responsibility 18Board of directors 20Governance 22Financial review 24Financial statements 42

Orascom Telecom is a leading integrated telecommunications services company operating GSM networks in the Middle East, Africa, Canada and Asia. OTH’s core belief is that communication is the essence of life, and the inherent right of every human. Being a borderless company, OTH seeks to provide the means of communication to people wherever they are in the world.

Communication empowers people to tell their stories, enhance their lives and advance their communities. OTH believes and strives to osition itself as the primary provider of communication services in its countries of operation. Integrating the most suitable and best technological innovation for each country enables OTH operator companies to facilitate and enrich their subscribers’ lives.

...one voiceFinancial data (IFRS)

in US$ millions 2009 2010 2011

Revenue 3760 3565 3636

EBITDA 1518 1496 1647

EBITDA margin (%) 40% 42% 45%

Net income 379 781 661

Earnings per GDR 0.36 0.73 0.63

CAPEX 761 782 816

Net Debt* 5113 4008 3022

Subscribers

78m

201120102009

78

69

61

Revenue

3,636m

201120102009

363635653760

EBITDA

1,647m

201120102009

1647

14961518

*Net Debt is calculated as a sum of short term debt, long term debt, less cash and cash equivalents.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 0504

Orascom Telecom at a glance

Diverse marketsOTH operates in countries on three continents, serving a population of 415 million customers with an average penetration of 48%.

Our operations

Country Population Mobile penetration Subscribers Market PositionContribution

to Group revenue

Algeria 35 million 83% 16.6 million 1 51%

Pakistan 190 million 58% 34.2 million 1 32%

Bangladesh 162 million 49% 23 million 2 14%

Telecel Global

Burundi 11 million 24% 1.2 million 1

Central African Republic

5 million 19% 0.4 million 1 2%

Zimbabwe 13 million 56% 1.5 million 2

Canada 34 million 70% 0.4 million n/aEquity

Consolidation

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 0706

A year of progress

Strategic Milestones

Janu

ary

2011

Orascom Telecom Holdings Annual Report 2011

Letter from the Chairman and Chief Executive

Jo Lunder, Chairman,“Given the strategic importance of Orascom Telecom Holding after the successful merger between VimpelCom Ltd. and Wind Telecom, I am very excited to have been appointed Chairman of the company. Our focus will be on executing our operational strategy which will deliver an increase in cash flows through driving profitable growth, operational excellence and capital efficiency.

Ahmed Abou Doma, Chief Executive Officer,“After an incredibly exciting year, Orascom Telecom ends 2011 poised to capture the growth momentum across its dynamic markets. With our operators showing impressive growth for 2011, Orascom Telecom now counts over 78 million customers, an increase of almost 13% compared to the closing base of 2010. While the depreciation of local currencies in Algeria, Pakistan, Bangladesh and Burundi impacted US dollar revenues for the quarter, performance indicators show expansion and development in most of our operations. Additionally, EBITDA growth surpassed revenue growth in most operations as a result of our focus on driving profitable growth, as well as our operational excellence and capital efficiency programs.

In Algeria, OTA continues to lead the market with a growth in subscribers of 10% over the course of 2011. While revenues were up by 5% in local currency, EBITDA increased 11% YoY as a result of Opex savings. Despite the healthy margin, the Algerian unit continues to face severe limitations, such as the ban on foreign currency transfers,

June

201

1

0706

which challenges network expansion and capacity needs.

In Pakistan, the subscriber base of over 34 million has contributed to a healthy revenue growth of 4% in local currency terms compared to the previous year. Mobilink’s EBITDA increased 7% YoY, as a result of lower sales costs, leading to an improved EBITDA margin for 2011.

In Bangladesh, banglalink’s aggressive focus on VAS has helped drive subscriber growth. A 23% increase in subscribers was reflected by 19% revenue growth in local currency compared to the same period last year.

Telecel Globe subscribers have exceeded 3 million, with high additions to the networks in Burundi and Zimbabwe.

In Canada, WIND Mobile subscribers have continued to grow, as a result of innovative offerings and an expanded coverage across Canada’s urban centers.”

In my new capacity as Chairman of OTH, I look forward to working closely with Ahmed Abou Doma and the management team to deliver maximum value to all our shareholders and contribute to OTH’s successful role as a major player in the global telecommunications arena.”

OTH Senior Secured Lenders support further financial flexibility from representation, warranties, and covenants related to OTA M

arch

201

1

VimpelCom Ltd. voted in their Special General Meeting in favor of the combination with WIND TELECOM, OTH’s parent company, to create a new global telecom group

Ap

ril 2

011

OTH’s EGM approves Demerger, Refinancing Plan and Internal Reorganization M

ay 2

011

Appointment of new Chief Executive Officer, Mr. Ahmed Abou Doma

OTH announces the sale of Powercom Ltd. in Namibia to Investec and Nedbank

Successful Refinancing of OTH’s capital structure, through the purchase by VimpelCom in full of the interests of the creditors under the Senior Credit Facility, and the interest of the holder of the Equity Linked Notes followed by the redemption of the High Yield Notes and the termination and close out the hedging transactions

Sep

tem

ber

201

1

Orascom Telecom Bangladesh receives its 2G license renewal guidelines. OTB is to pay approximately BDT 19.8 Billion (equivalent to approximately US$ 263 Million*) over three years as spectrum and license renewal fees. In addition, according to the received guidelines, the validity of the license renewal is for 15 years

Appointment of new Chief Financial Officer, Mr. Khalid Ellaicy

No

vem

ber

201

1

Appointment of new Chairman elected by the Board of Directors, Mr. Jo Lunder

Dec

emb

er 2

011

OTH completes Demerger after receiving approval from the Egyptian Financial Supervisory Authority. As a result of the Demerger, during November and December 2011, ownership of the Spin-Off Assets were transferred from OTH to Orascom Telecom Media and Technology (OTMT)O

cto

ber

201

1

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 0908

Business review

Financial Data

FY 2010 FY 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Revenues (DZD bn) 129 136 5.4%

EBITDA (DZD bn) 73 80 9.6%

EBITDA Margin 56.6% 58.8% 2.2p.p

Capex (US$ m) 90 40 (56%)

Operational Data

Dec 2010 Dec 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Subscribers 15,087,393 16,595,233 10.0%

Market Share 57.6% 55.5% (2.1%)

ARPU (DZD) (3 months) 724 673 (7.0%)

MOU (3 months) 288 278 (3.5%)

Churn (3 months) 5.7% 5.5% (0.2) p.p

Key priorities

• Balanced value pricing strategy

• Focus on data opportunity

• Consolidate Djezzy brand leadership and strengthen emotional bonding with customers

• Increase quality and control over the distribution channel

• Define leaner site configurations

Company Strategy

OTA’s main focus during 2011 has been on maintaining company value through key strategic pillars. These strategic pillars mainly focus on Value Segmentation, Distribution Control, Operational Excellence, New Revenue Streams & Assets Monetization, Control of Regulatory Risks, and finally retaining our key staff members as well as introducing new talent development programs.

The year in review

Brand

Orascom Telecom Algeria SPA (“OTA”) operates a GSM network in Algeria and provides a range of prepaid and postpaid products encompassing voice, data and multimedia, using the corporate brand “Orascom Telecom Algerie” and the dial commercial brand of “Djezzy” and “Allo”. OTA was awarded the second GSM license in Algeria in 2001 and launched its operations in February 2002. OTA commenced its operations under the brand “Djezzy” and introduced a second prepaid brand “Allo” in August 2004. Despite having launched its GSM operation approximately three years after the launch by the incumbent, Algerian Mobile Network (“AMN” conducting business under the brand name “Mobilis”), OTA was able to rapidly grow into Algeria’s leading and preferred telecommunications operator.

Market share

During 2011 OTA succeeded in managing to the best of its ability a very challenging year amidst extreme and adverse conditions, closing with 16.6m subscribers, maintaining its market leadership position with a 56% market share, controlling the largest distribution network with 20,000 POS selling SIM cards and over 65,000 selling airtime across all 48 Wilayas. During 2011 competition has intensified in form of network roll-out, channel incentives, consumer pull activities and BTL activities, compensating for the resulting gap out of OTA’s blockage situation.

Regulatory environment

The Algerian telecommunication regulator (ARPT) continues to classify OTA as a dominant operator and hence applying much tighter rules in evaluating its proposed tariffs and promotions compared to the other two operators. The regulator introduced new promotional rules during 1Q 2011, with respect to the duration of prepaid promotions, which were reduced from one month to fifteen days, and with respect to the required time period between prepaid promotions within any given month.

Algeria

Success Story

During 2011 OTA continued to reinforce its brand leadership through several new initiatives launched during the year. Main actions undertaken were the launch of a new communication platform and campaign for High Value Customers supported by new postpaid offers, the consolidation of OTA brand architecture supported by a national equity campaign and several campaigns during major yearly festivities, a leadership campaign (Being number one) reinforcing OTA’s leadership on network, products and customer relationship, as well as the launch of new products and services like Scoop or Ring Back Tones. OTA also focused on capturing leadership on the digital media front through targeting the online community by improved presence on social media such as Facebook and YouTube. Finally, OTA launched a new yearly initiative called “Prodiges” aiming to promote young Algerian talents active in all disciplines (music, cinema, writing, sport, dance, entrepreneurship) involving famous Algerian ambassadors (like Yasmina Khadra) and broadcasted on radio, billboard and press.

Leveraging Revenue Streams

Voice

At close to 100% penetration, subscriber growth in the mobile market has slowed considerably, and the attention is shifting to maintaining or improving the average revenue per user (ARPU), which has continued to decline under intensifying price competition. New postpaid pricing plans (Control 900 & 1900) were launched during this first half of 2011 supported by an initial 50% reduction in subscription fee and the first monthly fee. Other promotions included a recharge bonus for the “Allo” prepaid product. In the future, OTA’s main focus will be to reinforce the segmented approach.

Value Added Services

During 2011 OTA’s focus was on launching new products as well as improving the performance of current top value added service. OTA distinguished itself in the marketplace through the launch of the Arabic version of “Scoop”, OTA information services as well as the re-launch of “Ranati”, the ring back tone service, through a strong communication campaign. Finally a large SMS educational campaign was launched to increase SMS penetration among non-users, the campaign leveraged on a “free SMS” upon recharge promotion and was communicated through all media channels, including TV.

Data

In a market where voice and 2G services are saturated, OTA has entered the underdeveloped internet market by launching basic mobile data services. The licensing of a third generation (3G) spectrum has been delayed, which has made it difficult for OTA to fully compete in the broadband sector. However, 3G licenses are now expected to be issued in 2012.

Opportunities for the Future

Algeria has resolutely embarked on the process of developing a digital economy based on the knowledge and the integration of IT and communication technologies in all the aspects of daily life. It is therefore expected that the high speed mobile internet that will be brought by 3G mobile telephony will highly contribute to spreading the usage of IT and communication technologies. Future opportunities will come from mobile broadband and mobile internet services in the long run, while in the medium term opportunities lie in connectivity and the low penetration rate given by the fixed line operator (Algerie Telecom).

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 1110

Success Story

Mobilink launched the first of its kind “App store” by the name of Jazz Bananas in Pakistan on September 26th, 2011. This “App store” features comprehensive library of ready-to-download applications, games and other value added content services such as wallpapers, full tracks, videos, ringtones etc supporting all the popular handsets and devices available in the market.

The Jazz Bananas store is accessible via WAP and WEB interface, and includes the Handset Agnostic store, which supports all the popular handsets and devices in the market. There are over 5000 different apps and games for all major operating systems, including Android, Symbian, Java & BlackBerry. The Apps consist of various genres such as productivity, location based, social networking & eBooks. A further feature of Jazz Bananas is UGC (User Generated Content), which allows developers and third-party-vendors to upload their own apps and games, and benefit from the revenue share model.

The store will also be accessible via an on-device portal soon, which will be a small program installed on a user’s handset to facilitate access to the store at the touch of a button.

Business review

Financial Data

FY 2010 FY 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Revenues (PKR bn) 94 98 4.3%

EBITDA (PKR bn) 37 40 8.1%

EBITDA Margin 39.4% 40.8% 1.4 p.p

Capex (US$ m) 143 261 83%

Operational Data

Dec 2010 Dec 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Subscribers 31,794,292 34,213,552 7.6%

Market Share 31.4% 30.3% (1.1%)

ARPU (PKR) (3 months) 245 235 (4.0%)

MOU (3 months) 221 209 (5.4%)

Churn (3 months) 8.2% 7.2% (1) p.p

Key priorities

• Leverage the large subscriber base in order to unlock revenue potential from non-voice services

• Enhance margin through capturing mobile data opportunities

• Increase EBITDA through network OPEX reduction initiatives

• Adopt innovative technology solutions in order to enable a more efficient use of resources

• Infrastructure sharing

• Network modernization

Company Strategy

Mobilink is steadfast and focused on retaining and strengthening its market share to achieve revenue growth, whilst continuing to reduce operational costs. The company has the largest cellular network in Pakistan and this coverage advantage has been maintained with regular network expansion plans to meet the demands of the population’s horizontal growth.

The year in review

Ouer Brand

Pakistan Mobile Company Limited (PMCL) was founded in 1990 and began operations in August, 1994. Since that time, the company’s flagship brand, Mobilink, has established itself as a market leader amongst Pakistan’s GSM network operators, providing prepaid and postpaid voice and data services to individuals and corporate clients across Pakistan.

Mobilink’s brand portfolio includes Jazz and Jazba for prepaid customers and Indigo for postpaid customers, whereas broadband services are marketed under the brand name of Infinity. Jazz has established itself as a mass market brand, offering multiple packages, specially tailored to meet the demands of a diverse customer base. Jazba has been developed to cater to the youth segment, which has become an increasingly important segment in the industry. Indigo has become Pakistan’s premier postpaid cellular service and the brand of choice for both individuals and corporate clients.

Market share

During 2011 the cellular industry remained very competitive, with all operators introducing multiple campaigns with heavy media support. Mobilink also kept its product portfolio competitive by introducing new products and investing in various platform capacities to address the growing demand in services from its subscriber base. By the end of 2011 Mobilink served over 34 million customers, retaining its market leadership in a five player market with a 30.2% share.

Regulatory environment

Pakistan Telecommunication Authority (PTA) serves as the licensing and regulatory authority in Pakistan. During 2011, PTA’s major initiatives included a Quality of Service Survey and a Subscriber Authentication Process. After launching the Subscriber Verification System 789 in 2009, PTA introduced the SIM Ownership Verification system, in this drive 16 million unregistered connections were targeted, the majority of SIMs were regularized, while the remaining were made inoperative.

Pakistan

Leveraging Revenue Streams

Voice

The Voice segment, which is the major source of revenue for all the operators, remained an area of intense competition. With multiple products and promotions, Mobilink not only improved customers’ perception but also maintained its competitive portfolio. In 2011, the industry focus shifted towards location based charging (LBC) offers, with all operators, including Mobilink, introducing aggressive on-net discount offers across multiple cities. Aggressive hourly calls offers with daily subscription fees continued to be popular. Mobilink maintained its focus on subscriber acquisition by introducing periodic new sales promotions for both prepaid and postpaid connections during 2011.

Value Added Services

Mobilink has continued to exhibit significant growth in the VAS segment. Ring Back Tones, along with other services, remained popular among subscribers during 2011. Entertainment services, such as Mobile Music and Mobile Radio, continued to gain popularity among the youth segment and showed high engagement. During the

year Mobilink introduced multiple innovative services, resulting in an improved customer experience.

Data

In 2011, the data portfolio also underwent exponential growth after the launch of daily unlimited bundles on the back of enhanced network capacities. In addition to building a well-rounded data product portfolio for addressing all the needs of customers, Mobilink has also been focused on building requisite network capacities to fulfill growing demand.

Opportunities for the Future

The uptake of data services and 3G will allow Mobilink to unlock value and revenue streams from its large subscriber base, thus supplementing voice revenues.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 1312

Business review

Financial Data

FY 2010 FY 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Revenues (BDT bn) 32 38 18.8%

EBITDA (BDT bn) 9 13 44.4%

EBITDA Margin 28.1% 34.2% 6.1 p.p

Capex (US$ m) 235 161 (31%)

Operational Data

Dec 2010 Dec 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Subscribers 19,327,005 23,753,552 22.9%

Market Share 28.5% 27.9% (0.6%)

ARPU (BDT) (3 months) 149 140 (5.8%)

MOU (3 months) 221 207 (6.3%)

Churn (3 months) 46.9% 5.4% 0.8 p.p

Key priorities

• Tap into mobile data opportunities

• Leverage large base by unlocking mass-market value potential

• Apply a dual market strategy providing tailored services for high-end segments, as well as optimized services for lower-end segments in the market

• Capture technology synergies by introducing and swapping into outdoor sites and implementing innovative hybrid solutions

• Site sharing

Company Strategy

Orascom Telecom Bangladesh Limited (OTB) is a GSM telecommunications operator in Bangladesh and providing wide range of voice and data services.

OTB’s marketing strategy focused on targeting different consumer segments with specially designed products and services that are tailored to the needs of these segments.

OTB aggressively enhanced its network since inception, and has consistently increased its capital expenditures to build an efficient and dependable network.

The year in review

Brand

OTB provides its services under two brand names: “banglalinkTM” and “icon”. OTB’s prepaid brand, “banglalink desh”, is perceived as the best prepaid package in the country with innovative tariff and value for money features. “banglalink business”, “banglalink SME” and “banglalink PCO” cater the needs of the business segment including the thriving SME sector where OTB has been the pioneer in the country. The premium brand ‘icon’ has already created awareness and acceptability within its target market.

Market share

Telecommunications services in Bangladesh are provided by 5 GSM and 1 CDMA operators, and 8 fixed-line operators. Among the GSM operators, OTB stands as the second largest operator.

As of December 31st, 2011, OTB’s network covered 97% population of Bangladesh with 23.75 million subscribers and a market share of 27.9%. This phenomenal growth was attributable to overwhelming response of subscribers to OTB’s innovative products, strong brand equity, extensive distribution network, and continuous improvement in service quality.

Telenor Mobile Communications AS owns 55.8% shares of Grameenphone the only operator in Bangladesh which is a publicly listed company. Axiata Bangladesh Ltd (Robi), the third largest player is a joint venture company in which Axiata holds 70% and NTT DoCoMo holds a 30% stake. Teletalk Bangladesh Ltd is the state owned mobile operator while Airtel Bangladesh is a subsidiary of Bharti Airtel Limited. Pacific Bangladesh Telecom Ltd. (“Citycell”), is the only CDMA operator, in which SingTel acquired a minority interest. The Bangladesh Telecommunications Company Limited (“BTCL”) is the incumbent state-owned fixed-line operator.

Bangladesh

Success Story

OTB is a pioneer in launching mobile financial services in Bangladesh, being the first operator in South Asia to launch international remittance over mobile. OTB won an award from the International Association of Money Transfer Networks (IAMTN) for this first-ever service in Bangladesh. OTB also launched several other mobile financial services, such as train ticketing, utility bill pay, concert ticketing and domestic remittance services with Bangladesh Post Office.

OTB received several awards in 2011. ‘Krishi Bazaar 2474’ has won the World Communication Award 2011, while OTB Mobile Cash service won the mBillionth South Asia Award 2011. In addition, OTB won the ICMAB (an association of leading professional accountants’ of Bangladesh) best corporate award 2011 for publication of its annual report 2010.

Regulatory environment

2G licenses awarded by the Government of Bangladesh to four mobile operators including OTB, expired on 11 November 2011. OTB along with Grameenphone, Axiata and Pacific Telecom deposited the license renewal fees within the stipulated payment schedule. The Government of Bangladesh is currently processing the renewal of the 2G licenses of the four operators, including OTB.

Leveraging Revenue Streams

Voice

Under the flagship brand “banglalink desh”, the prepaid products have been introduced with features such as flat tariff, 1 sec pulse and long call benefit, to address different usage needs of the 2.2 million prepaid consumers. “banglalink business”, “banglalink SME” and “banglalink PCO” cater to the needs of the business segment, including the thriving SME sector. In 2011, OTB introduced “banglalink inspire”, targeting different professional groups of society with a variety of special features.

Value Added Services

OTB subscribers enjoy a wide range of innovative and superior services including caller ring-back tone, music station, voice portal, voice chat, news alerts etc. In recent years, OTB has been leading the industry in offering new and enhanced services for business customers, namely premium field force locator, corporate SMS broadcast and mobile advertising to name a few examples.

Opportunities for the future

OTB has started to strengthen it’s footsteps by consolidating a nationwide EDGE/GPRS network with competitive mobile internet products, aiming to monetize small screen mobile internet usage. Moreover, OTB’s value-added service continues be a value driver for maintaining and enhancing the overall value proposition of OTB’s product offering.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 1514

Business review

Financial Data

FY 2010 FY 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Revenues ($US m) 102 94 (7.8%)

EBITDA ($US m) 24 8 (66.7%)

EBITDA Margin 23.5% 8.5% (15.0) p.p

Operational Data

Dec 2010 Dec 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Subscribers 2,974,000 3,140,000 5.6%

Key priorities

• Derive profitability by reaching the critical mass in the underlying markets while capitalizing on our market leadership

• Maintain value-driven pricing

• Increase coverage footprint through cautious investment in rural areas by deploying low CAPEX sites suitable for rural environments

• Introduce low-cost outdoor sites in order to manage CAPEX demands

• Employ hybrid solutions

Telecel CARTelecel is the market leader in CAR with an approximate market share of 50%. It operates a GSM/GPRS/EDGE/WIMAX network. For historical reasons Telecel holds a special place in Central Africans’ hearts. This bond is reflected in the company’s communication with the use of the emotive phrase “Biani, Biani”, which translated from Sango is “all of us, together”. Among all four international mobile phone operators in CAR, Telecel boasts the biggest VAS portfolio, the largest network coverage and the most extensive distribution network. With its recent rebranding to the color red, it has also become the country’s most visible network, reflecting its dominant market position. Having now consolidated its lead in the capital Bangui, Telecel CAR is preparing for the next stage of its growth; developing the vast and underserved rural market. With only 20% penetration, there is still plenty of room for growth.

leo BurundiU-Com Burundi S.A. trading under the brand name ‘leo’ is the leading telecommunications operator in Burundi. It started providing analog services in 1993 and moved to GSM protocol in the year 2000. GPRS/EDGE data services were launched commercially in 2009 along with WIMAX broadband (fixed internet) services. ‘Leo’ has launched a 3G network in October 2011 along with fiber-optic backhaul connectivity in its strategic drive to commercialize broadband data services to all segments (mass-market as well as SME and corporate) at competitive prices in this landlocked country.

‘leo’ has a subscriber base of 1.2 million customers with the highest market share amongst 5 other mobile and fixed operators of 59%. Current GSM (SIM) penetration is 25% and therefore there is still significant scope for growth especially in rural areas and leo has firmly positioned itself as the telecommunications operator of choice in terms of coverage, accessibility, products, services, customer care and brand values.

Telecel Globe

Telecel ZimbabweTelecel Zimbabwe has been part of the Orascom Group since 2000. It currently operates a GSM/GPRS/EDGE/3G network. Telecel Zimbabwe serves a growing customer base and constantly demonstrates its core values of simplicity, value for money, innovation and trust and care for which it has become well known for in the Zimbabwean market. It’s attractive voice and data bundle offerings, effective marketing communications, improved distribution network, enhanced network quality and coverage all complement each other and help in reaching customers everywhere and in providing them with world-class telecommunication services. TZIM currently operates in a three-player market and at the end of 2011 held the 2nd position with a market share of 22.2% and total subscriber base of 1.52 million customers. With a fairly low market penetration at the end of 2011 (56%), growth still lies ahead! TZIM’s focus is to bring smart choices to customers with best value for money offers in a young, friendly and responsible way. The opportunities for the future reside in strengthening our distribution network to fuel the anticipated growth, developing segmentation capabilities to grow the value from our existing customers, capturing the data opportunity through 3G, enhancing the brand image to further strengthen the customer bond, and to continue to roll-out our network.

Success Story

Orascom Telecom’s three African operators are key players in the efforts to make mobile data services available to the masses in the countries where they operate.

The Central African Republic and Burundi were the first operators to offer high speed Internet using WIMAX. Telecel Zimbabwe was the first to offer 3G services, followed by leo Burundi. Telecel Central Africa currently provides mobile Internet using GPRS / EDGE but will soon be joining its African sister companies offering 3G.

3G has proved to be extremely popular and Telecel Zimbabwe and leo Burundi are seeing strong demand for their 3G

offerings. Between November 2011 and March 2012, data revenues for both these operations combined have experienced an amazing four-fold increase!

Both Zimbabwe and Burundi gained access to the sea cables in 2010-2011 and CAR is to connect to the Central African backbone by mid-2013. As a result, the cost of bandwidth has fallen dramatically. Along with cheaper high-speed data via the undersea cables, low cost smart phones are being developed, making it easier for middle class Africans to access the Internet and connect to the digital world.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 1716

Business review

Operational Data

Dec 2010 Dec 2011

Inc/(dec)Dec 2011 vs.

Dec 2010

Subscribers 232,641 403,000 73.2%

ARPU (CAD) (3 months) 29.0 26.4 (9.0%)

Regional strategy

dam aut hit a volesto ma nime si culparunti doluptae resequas ius, alibus sequam, ent, ad qui dis eum ime que omnis quod quatquos sit vitatusam fuga. Nam faccuscipis aliti id qui dolorum, volenist expercipis sunt offic totae expe volut vidusci ligent.

Key priorities

• Capture market share

• Expand network coverage

• Grow distrubution network

• Continue providing value for money services

Company Strategy

WIND continued to play a significant role in shaping the wireless market in Canada, WIND’s adjusted its strategy targeting the “Value Plus” customer segment in the Canadian market offering a variety of voice services, including a mix of simple and feature-rich service plans, typically with an unlimited voice component.

WIND continued its commitment to the prepaid market in Canada, but reflected a conscious and disciplined mandate not to “race to the bottom” following unreasonably aggressive pricing waves adopted by low end market entrants proven to have no financial feasibility and in fact unsustainable in the mid-term.

Also, fixed line businesses operate under numerous brands with services including long distance, operator services, billing clearinghouse services, reservation-less conferencing and VoIP to small and medium-sized businesses.

WIND successfully executed on its new postpaid strategy, “Value Plus”, by extending its handset subsidy program (“TAB”) to a new TAB+ program. This new program includes larger subsidies and a broader range of high-end Android, Blackberry and Windows 7 handsets. The effect has been positive, as greater than 50% of WIND Canada’s gross additions in Q4 2011 were postpaid sales.

The year in review

Brand

WIND’s re-launched “WIND Mobile” brand targeting the “Value Plus” customer segment in the Canadian market.

Market share

Wind Mobile launched in December 2009, by the end of 2011 it had a market share of 2.0% of licensed population and 4.28% market share normalized to its coverage. The Canadian market has primarily been served by three large facilities-based providers, Rogers Communications, which had 36% of the wireless subscribers in 2011, followed by Bell Group at (29%), TELUS Communications Company (28%), and other providers, principally MTS Allstream and SaskTel. In 2010, three other new service providers commenced operations to offer mobile service using spectrum acquired as part of the AWS auction in 2008; Mobilicity, Public Mobile and Videotron.

Regulatory environment

Two major announcements from the Canadian Government came in Q1 2012 These are:

• Policy regarding the upcoming auction (expected to take place in H1 2013) of 700MHz spectrum; and

• Long-awaited decision to lift (for at companies with less than 10% market share) the existing restrictions on non-Canadian ownership and control of telecommunications companies operating in Canada.

Canada

Leveraging Revenue Streams

Data

WIND offers a variety of data products and value added services ranging from mobile internet, mobile broadband data sticks, blackberry and social media add-ons.

Value Added Services

Value added services include text, multimedia messaging, web portal, voice mail and call control features, and premium apps through various content providers.

Opportunities for the future

WIND will continue its focus on network rollout with a clear goal to expand coverage, increase quality, and data speed to support its Value Plus strategy. Special focus is assigned to growing distribution network on the dealer and indirect channels. WIND is exploring a number of strategic alliances to strengthen its position as Canada’s fourth national player.

Success Story

WIND’s success has been built on simple, transparent, and feature-rich postpaid and prepaid talk, text, and data plans that offering unlimited features with no term contracts. WIND’s re-launched “WIND Mobile” brand targeting “Value Plus” customer segment in the Canadian market. The successful execution of its new strategy increased the share of postpaid voice subscribers to +60% of net additions. The strategy shift entails carefully managing prepaid segment economics. WIND managed a 73% growth in 2011 Subscribers base over 2010 in its second year of operations after increasing its coverage reaching more than 12.7 million people (37% of the total population and 47% of the ‘licensed’ population), WIND covers five of the top six populated areas in Canada.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 1918

CSR

Corporate Responsibility Orascom Telecom Holding S.A.E’s approach to corporate social responsibility is based on decentralization and the consequential delegation of a number of tasks. Decentralization has been a key element of our corporate culture and is also the basis of our success in implementing group recommended social, governance and environmental initiatives that are tailored to meet local market needs.

Over the past two years, we have made progress on our sustainability priorities by improving the energy efficiency of our network and increasing our paper-less billing methods across our operating companies. We have also completed our environmental management 14001 and occupational health and safety 18001 systems for OTH headquarters in Cairo.

In 2011 Orascom Telecom Holding S.A.E and its local operating companies achieved a number of awards. Orascom Telecom was ranked third on the EGX ESG index for 2011.

The assessment was based on our environmental, social and corporate governance activities disclosed through our annual sustainability report. In 2011, banglalink received the World Communication Award for the banglalink krishi bazaar service.

Orascom Telecom is proud to be a pioneer in the industry’s efforts to improve responsible business practices in emerging markets. We continue to support the United Nations Global Compact and its principles on human rights, labor rights, the environment and anti-corruption. We participate in the national quarterly roundtable discussions and our annual sustainability report meets the criteria of the UN global compact communication on progress requirements.

For more information, please read our annual sustainability report available on www.otelecom.com /responsibility

Social Investment

Orascom Telecom provides support to programs and projects that contribute to the social development and improves the standard of living through direct financial donations, in kind, as well as employee donations and volunteering. Across our operating companies and through our products and social investment program, we contribute to the achievement of the United Nations Millennium Development Goals. Below are some examples.

Table 1: Total Subscribers1

MDG Goal Country Example of our Contribution

Eradicate extreme poverty

Bangladesh & Zimbabwe

The launch of mobile-banking is helping people access to banking service anytime and anywhere which will boost rural economy and national output by scaling up money circulation in villages in Bangladesh and Zimbabwe.

Achieve universal primary education Zimbabwe

In Zimbabwe, Burundi and Central African Republic, we have been supporting primary school education by providing bursary schemes and financial support to help students who can’t afford enroll in schools and continue their education.

Promoting gender equality and empower women Pakistan

In partnership with UNESCO Mobilink in Pakistan has been empowering women and young ladies through the provision of literacy to adolescent girls using mobile phones.

Reduce child mortality Pakistan

Mobilink has partnered with the Polio Eradication Fraternity including UNICEF and Ministry of Health, to help create awareness of this disease.

Improve maternal health Egypt

Our services can improve maternal healthcare services considerably especially in remote areas where access to health units is difficult. Mobinil has piloted a new service “Mobile baby” in partnership with Great Connections.

Combat HIV/AIDS, malaria and other diseases Burundi

Leo Burundi provides direct financial donation to children schools and orphanages. The target beneficiaries are children whom are whose parents are HIV positive.

Ensure Environmental sustainability

Across the Group

Across our operations, we reduce our carbon emissions and energy consumptions by using alternative energy generation techniques such as solar power and wind energy.

Egypt- Orascom Telecom Holding

Orascom Telecom sponsors Cairo University to compete in SIFE World Cup

Orascom Telecom Holding S.A.E proudly sponsored the SIFE Egypt team from Cairo University to compete in SIFE 2011 World Cup. The competition took place in Kuala Lumpur, Malaysia, October 3rd -5th where 40 national champion university teams representing 40 countries presented their civic engagement projects.

SIFE (Students In Free Enterprise) an international non-profit organization that brings together the leaders of today and tomorrow to create a better, more sustainable world through the positive power of business. Founded in 1975, SIFE has active programs on more than 1,500 college and university campuses in over 40 countries. For more information contact SIFE World Headquarters at 417-831-9505 or visit www.sife.org.

Through SIFE, students around the world are discovering that “doing well” and “doing good” can be accomplished simultaneously throughout college and career. More than 400 global business leaders assembled at the Kuala Lumpur Convention Center October 3-5 to evaluate the outreach projects of 40 national champion teams. The teams were judged on how successful they’ve been at using business solutions to create economic opportunity for others.

Pakistan – Mobilink

Flood Relief Efforts for 2011

Mobilink in collaboration with the Armed Forces and Torchbearers reached out to 7000 families in flood hit regions of Sindh with essential food items. Mobilink ration bags were designed to feed a family of 7 for 15 days. Through this initiative, Mobilink provided food and clean drinking water to about 50,000 people. Mobilink also distributed 126,000 liters of clean drinking water

Mobilink torchbearers and franchises helped identify areas that were in need of help and were active in distributing ration items in those areas with the help of the armed forces. As a result Mobilink was able to reach out to villages where no aid had been distributed and villages which were ignored by traditional NGOs and international aid agencies.

Mobilink was the first company to set up an SMS code to raise funds from external sources for flood relief. Mobilink also launched an internal

fundraising drive. Mobilink Employees at all levels donated generously from their salaries and we were able to raise Rs. 700,000 in the first four weeks of fundraising.

While many other organizations just donated funds, Mobilink not only donated funds and goods but the time of its personnel and encouraged its staff to volunteer in the field, to visit places and identify underserved regions. Mobilink torchbearers sacrificed over one thousand hours towards flood relief including weekends.

Mobilink remains committed to providing relief to flood victims. With funds raised by employees and commitments made by the management, Mobilink is going to expand its flood relief efforts in the near future. Mobilink will continue to provide relief goods and will also be constructing homes for people who lost their homes to the floods in Sindh.

Burundi – Leo

Education Assistance Program

Leo Burundi’s Educational Assistance Program began in March 2009 and it has benefited 1643 schoolchildren. The programme provides assistance with the education of disadvantaged children, including orphans and children with disabilities, channelling its assistance through eight institutions. The programme contributes to the educational development of children in both urban and rural communities who are unable to afford basic educational facilities. Assistance includes school fees, uniforms, and stationary items, such as pencils and exercise books, and equipment for handicapped students.

The institutions to which Leo Burundi has provided assistance are: Association RET (Association Regard à l’Enfant Traumatise), which takes care of children traumatised by the war in Burundi, Association ASENBU (Association pour L’Enfant Non Acompagné de Buyengero), which takes care of children in the Buyengero region affected by the war, École EPHPHATA, which is a school in Bujumburu for the deaf and mute, CESDA (Centre Spécialisé pour Deficients Auditifs), which is a school in Gitega province for children who are deaf or have hearing difficulties, Ecole KANURA, a school for the blind, Ecole RUMURI, which is a school for the blind in Gitega Province, Association Solidarité pour Aider les Sinistrés Burundais, and Centre Handicapé de Kiganda.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 2120

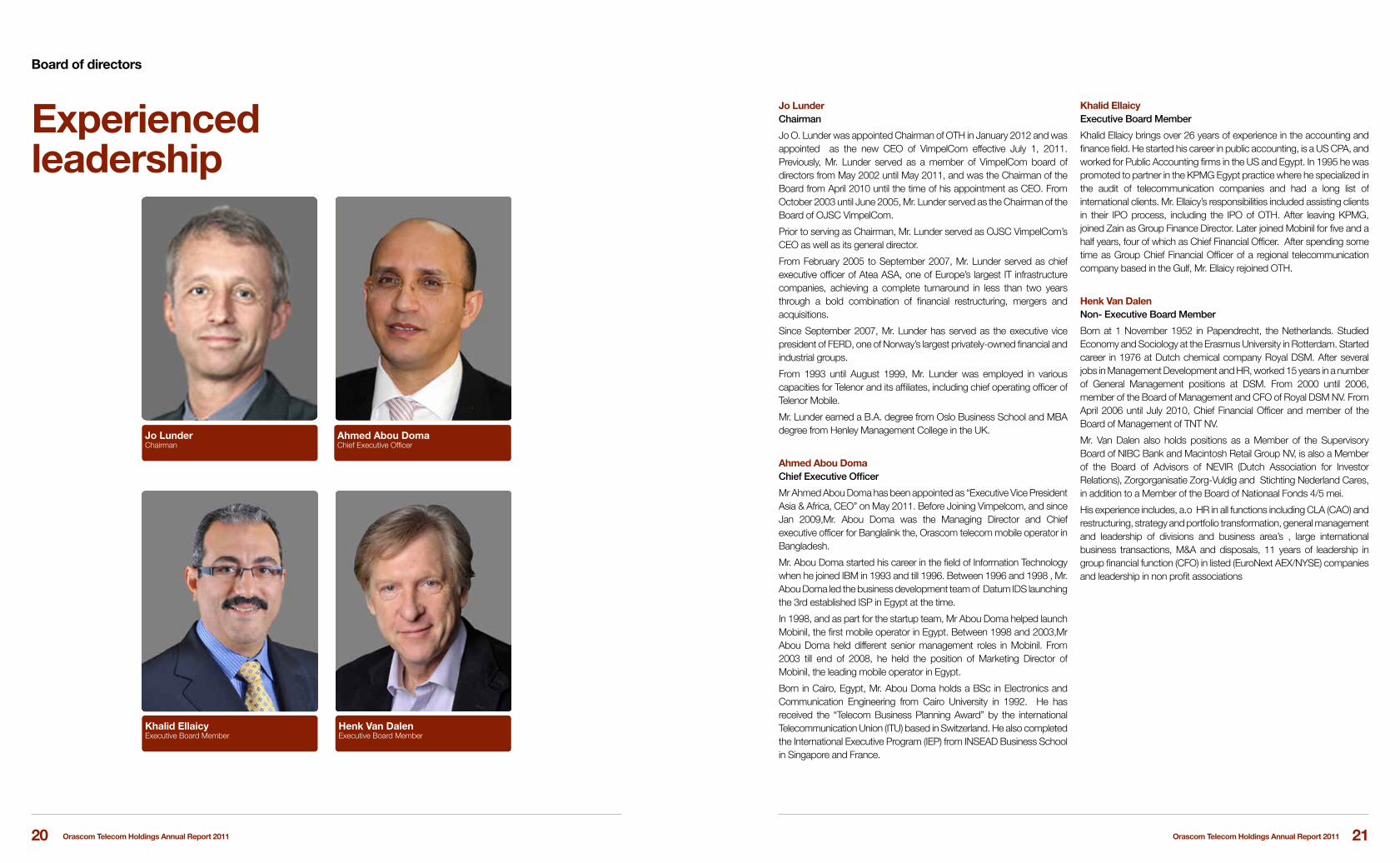

Board of directors

Experienced leadership

Jo Lunder Chairman

Ahmed Abou Doma Chief Executive Officer

Jo Lunder Chairman

Jo O. Lunder was appointed Chairman of OTH in January 2012 and was appointed as the new CEO of VimpelCom effective July 1, 2011. Previously, Mr. Lunder served as a member of VimpelCom board of directors from May 2002 until May 2011, and was the Chairman of the Board from April 2010 until the time of his appointment as CEO. From October 2003 until June 2005, Mr. Lunder served as the Chairman of the Board of OJSC VimpelCom.

Prior to serving as Chairman, Mr. Lunder served as OJSC VimpelCom’s CEO as well as its general director.

From February 2005 to September 2007, Mr. Lunder served as chief executive officer of Atea ASA, one of Europe’s largest IT infrastructure companies, achieving a complete turnaround in less than two years through a bold combination of financial restructuring, mergers and acquisitions.

Since September 2007, Mr. Lunder has served as the executive vice president of FERD, one of Norway’s largest privately-owned financial and industrial groups.

From 1993 until August 1999, Mr. Lunder was employed in various capacities for Telenor and its affiliates, including chief operating officer of Telenor Mobile.

Mr. Lunder earned a B.A. degree from Oslo Business School and MBA degree from Henley Management College in the UK.

Ahmed Abou DomaChief Executive Officer

Mr Ahmed Abou Doma has been appointed as “Executive Vice President Asia & Africa, CEO” on May 2011. Before Joining Vimpelcom, and since Jan 2009,Mr. Abou Doma was the Managing Director and Chief executive officer for Banglalink the, Orascom telecom mobile operator in Bangladesh.

Mr. Abou Doma started his career in the field of Information Technology when he joined IBM in 1993 and till 1996. Between 1996 and 1998 , Mr. Abou Doma led the business development team of Datum IDS launching the 3rd established ISP in Egypt at the time.

In 1998, and as part for the startup team, Mr Abou Doma helped launch Mobinil, the first mobile operator in Egypt. Between 1998 and 2003,Mr Abou Doma held different senior management roles in Mobinil. From 2003 till end of 2008, he held the position of Marketing Director of Mobinil, the leading mobile operator in Egypt.

Born in Cairo, Egypt, Mr. Abou Doma holds a BSc in Electronics and Communication Engineering from Cairo University in 1992. He has received the “Telecom Business Planning Award” by the international Telecommunication Union (ITU) based in Switzerland. He also completed the International Executive Program (IEP) from INSEAD Business School in Singapore and France.

Khalid EllaicyExecutive Board Member

Khalid Ellaicy brings over 26 years of experience in the accounting and finance field. He started his career in public accounting, is a US CPA, and worked for Public Accounting firms in the US and Egypt. In 1995 he was promoted to partner in the KPMG Egypt practice where he specialized in the audit of telecommunication companies and had a long list of international clients. Mr. Ellaicy’s responsibilities included assisting clients in their IPO process, including the IPO of OTH. After leaving KPMG, joined Zain as Group Finance Director. Later joined Mobinil for five and a half years, four of which as Chief Financial Officer. After spending some time as Group Chief Financial Officer of a regional telecommunication company based in the Gulf, Mr. Ellaicy rejoined OTH.

Henk Van Dalen Non- Executive Board Member

Born at 1 November 1952 in Papendrecht, the Netherlands. Studied Economy and Sociology at the Erasmus University in Rotterdam. Started career in 1976 at Dutch chemical company Royal DSM. After several jobs in Management Development and HR, worked 15 years in a number of General Management positions at DSM. From 2000 until 2006, member of the Board of Management and CFO of Royal DSM NV. From April 2006 until July 2010, Chief Financial Officer and member of the Board of Management of TNT NV.

Mr. Van Dalen also holds positions as a Member of the Supervisory Board of NIBC Bank and Macintosh Retail Group NV, is also a Member of the Board of Advisors of NEVIR (Dutch Association for Investor Relations), Zorgorganisatie Zorg-Vuldig and Stichting Nederland Cares, in addition to a Member of the Board of Nationaal Fonds 4/5 mei.

His experience includes, a.o HR in all functions including CLA (CAO) and restructuring, strategy and portfolio transformation, general management and leadership of divisions and business area’s , large international business transactions, M&A and disposals, 11 years of leadership in group financial function (CFO) in listed (EuroNext AEX/NYSE) companies and leadership in non profit associations

Khalid Ellaicy Executive Board Member

Henk Van Dalen Executive Board Member

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 2322

Jeffrey D. McGhieNon- Executive Board Member

Jeffrey D. McGhie is General Counsel of VimpelCom Ltd. Mr McGhie held the position of Vice President, General Counsel of OJSC VimpelCom since June 2007, he served as Chief Legal Officer since March 2006.

Prior to joining VimpelCom, he held the position of associate in the Moscow office of Akin Gump Strauss Hauer & Feld LLP from September 2002 until December 2004, and counsel from January 2005 until March 2006.

From December 1999 until August 2002, Mr. McGhie was an associate at Kirkland & Ellis in Chicago, Illinois.

Mr. McGhie graduated with a B.A.in Russian from Brigham Young University (Provo, Utah USA) in 1995 and received a J.D. magna cum laude and MBA from Indiana University (Bloomington) in 1999 (Bloomington, Indiana USA).

Iskandar Shalaby Non- Executive Board Member

On September 1, 2008 Alex Shalaby was appointed Chairman of the Egyptian Company for Mobile Services (Mobinil) by Board consensus; prior to that he was its President and CEO since 2005.

Shalaby came to Mobinil from Washington, DC where he was AT&T Director for Public Affairs, serving as the company’s link to lawmakers on Capitol Hill and lobbying the executive branch of the U.S. government. He helped in achieving more liberalization of the telecoms sector internationally for the emerging nations of the Middle East, Africa, and Eastern Europe through the relevant bi-lateral and multi-lateral agencies. During these years, he served on the boards of the American Chamber of Commerce becoming its president during the period (1991 – 1992), the Bi-national Fulbright Commission, and Seeds of Peace; he currently chairs the board of Injaz & SIFE in Egypt.

In 1966 Shalaby graduated with a Bachelors of Science degree in Electrical Engineering from the University of Alexandria and earned a Masters of Science degree in Electrical Engineering and Computer Science from San Jose State University in California.

Mohamed Shaker Non- Executive Board Member

Ambassador Shaker is Chairman of the Egyptian Council for Foreign Affairs (ECFA) since its inception in 1999 and again since 2009. As of 2002, he is Chairman of the Board of the Regional Information Technology Institute (RITI). He is also Chairman of the Board of Trustees of the National Center for Middle East Studies since 2006. As of 2009, He was designated member of the Board of The Diplomatic Institute, Egyptian Foreign Ministry.

He is also Chairman of the Board of Trustees of the Sawiris Foundation for Social Development as of 2001. In 2008, he was elected as Chairman of the Board of Trustees of Magdi Yacoub Foundation for Heart Research. As of June 2009, he is a member of the Board of the Nuclear Power Plants Authority.

Ambassador Shaker served as ambassador to the UK, Austria, the IAEA and the UN.

Ambassador Shaker completed his studies as Docteur es Sciences Politiques at the Graduate Institute of International Studies, University of Geneva, in 1975, after having acquired the Licence en Droit (LLB) from Cairo University in 1955. Amb Shaker chaired two major conferences on peaceful uses of nuclear energy and nonproliferation in 1985 and 1987. Among Ambassador Shaker’s major works is a book on The Nuclear Non-Proliferation Treaty.

Elena ShmatovaNon- Executive Board Member

Elena Shmatova has served as Executive Vice President and Chief Financial Officer of OJSC VimpelCom since October 2005. She has also served as Vice President since June 2004 and as Chief Financial Officer of VimpelCom since January 2003. Ms. Shmatova served as Director of Treasury of VimpelCom from March 2002 until January 2003 and as Financial Controller of VimpelCom from December 1999 until March 2002. From 1992 until 1999, Ms. Shmatova served as Deputy Finance Director, Finance Director and Vice President of Finance at the Sprint Communications/GlobalOne Group of companies in Russia. Prior to 1992, Ms. Shmatova served as a Financial Director of “Express Mail Service-Garantpost” and was an economist at the Ministry of Telecommunications of the USSR and the Center of International Accounting of the Ministry of Telecommunications of the USSR.

In June 2010 Elena Shmatova was appointed the General Director of OJSC “VimpelCom” and lead the Russia business unit till December 2011. In January 2012 she joined VimpelCom’s finance team in Amsterdam as Group Director Business Control, Development and M&A.

Ms. Shmatova received a bachelor’s degree in economics from the Moscow Telecommunications University.

Jeffrey D. McGhie Non- Executive Board Member

Iskandar Shalaby Non- Executive Board Member

Mohamed ShakerNon- Executive Board Member

Elena ShmatovaNon- Executive Board Member

Experienced leadership

Board of directors

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 2524

Governance

Committed to the highestglobal standardsThe Company is committed to achieving and maintaining the highest standards of corporate governance. The Company considers effective corporate governance essential to enhancing shareholders’ value and protecting stakeholders’ interests. Accordingly, the Board attributes a high priority to identifying and implementing appropriate corporate governance practices to ensure transparency, accountability and effective internal controls. The Board continued to further its commitment to corporate governance through reviewing existing processes and, where appropriate, developing new ones. The Company substantially complies with the practices enunciated in the Egypt Code of Corporate Governance and will strive to comply with these and other appropriate standers and governance guidelines. The key corporate governance principles and practices are as follows:

The General Assembly The General Assembly (”GA”) of the Company is the ultimate governing body of the Company. In summary, the (”GA”):

• includes all the shareholders of the Company; • takes its decision by voting among shares represented in the meeting. The voting rule is: 1 share = 1 vote for all shares indifferently;• holds at least one ordinary meeting per year and may have an extra-ordinary meeting as needed;• The responsibilities of the GA are based on the laws and Company Statues; • it appoints the board, approves the financial results, appoints the external auditors, and approves dividends distribution. Board of Directors The Board has the responsibility to work to enhance the value of the Company in the interest of the Company and its shareholders. In summary, the Board:

• is engaged in active and continuous strategic planning and approves corporate strategies, including the approval of transactions relating to acquisitions and divestments, and capital expenditure above delegated authority limits;

• reviews and approves the corporate plan for the forthcoming year and following two years, including the capital expenditure and operating budget, and reviews performance against strategic objectives;

• assesses business opportunities and risks on an ongoing basis and oversees the Company’s control and accountability systems; • monitors and approves the Company’s financial reporting and dividend policies; • appoints and has the authority to remove the Chief Executive Officer and approves the recommendations of the Human Resources;• ratifies the appointment and has the authority to remove the Chief Financial Officer and Group General Counsel and appoints the

Company Corporate Secretary; and • oversees succession planning for the Chief Executive Officer and senior management.

The Chairman and the Chief Executive Officer establish meeting agendas to ensure adequate coverage of key issues during the year. In addition workshops and strategy meetings take place. Executives and other senior people regularly attend Board meetings and are also available to be contacted by Directors between meetings.

The Board met ten times in 2011.

Composition of the Board of Directors

ChairmanJo Lunder

Board MembersJo Lunder (Chairman)Ahmed Abou Doma (Chief Executive Officer)Khalid Ellaicy (Executive Board Member)Iskandar Shalaby (Non-Executive Board Member)Mohamed Shaker (Non-Executive-Board Member)Henk Van Dalen (Non-Executive-Board Member)Jeffery McGhie (Non-Executive-Board Member)Elena Shmatova (Non-Executive-Board Member)

The above Board Members classification is based on the Egyptian Corporate Governance code. The latter did not specify the criteria for independent directors that would allow the Company to benchmark against, yet in our opinion and based on internationally recognized best practices, a number of our directors would qualify as independent directors bringing to the company the highest possible standing from both a personal and professional standpoint.

Secretary to the Board David DobbieThe company Secretary is responsible to the Board and is available to individual Directors in respect of Board procedures. The Company Secretary was appointed in March 2012. He joined the Group in October 2008. Board Committees• The Board has established a number of committees which are

the most important tools for the management and the operational integration of the Company and provides sufficient resources to enable them to undertake their duties. Executive Directors are not members of the Audit Committee, although they may be invited to attend meetings.

It has recently been revised to:• Monitor the implementation of strategies and the development of

plans and results. • Ensure the overall coordination of business actions and the

management of the relative cross-over business issues. • Build up the necessary operating synergies between the various

functions involved in the technological, business and support processes.

• Support the integrated development of the innovation processes of the Company.

• In particular, the Committee System of the Board includes:

Investment CommitteeThe objective of the Investment Committee is to assist the Board in reviewing the Company’s investment policies, strategies, transactions and performance. This C. also oversees the Company’s capital and financial resources. The Committee has appropriate resources and authority to discharge its responsibilities, including the authority to retain experts or consultants.

Audit CommitteeThe objective of the Audit Committee is to assist the Board in fulfilling its oversight responsibilities by reviewing (i) proposed financial plans; (ii) the financial information provided to shareholders and others; (iii) systems of internal controls which management and the Board of Directors have established; and (iv) the audit process, including both internal and external audits. The Audit Committee interacts directly with the independent auditor to ensure the independent auditor’s ultimate accountability to the Board and the Committee, as representatives of the shareholders, and is directly responsible for the appointment, compensation and oversight of the independent auditor.

Remuneration CommitteeThe objective of the Remuneration Committee is to ensure that the company has a formal process of considering management’s and directors’ remuneration: that is, executive directors should play no part in decisions regarding their own remuneration. There should be an alignment of the remuneration schemes and the performance objectives of the Company, and the remuneration schemes should attract and retain talented individuals.

Management CommitteesManagement committees have ultimate responsibility for directing the activities of the Company, ensuring that it is well run and delivering the expected outcomes.

The management committees should provide leadership to the Company by:• Setting the strategic direction to guide and direct the activities of

the Company; • Ensuring the effective management of the Company and its

activities; and • Monitoring the activities of the Company to ensure that they are

complying with the founding principles, objects and values. • In particular, the Committee System of the Company consists of:

Executive Committee The objective of the Executive Committee is to review and, where appropriate, authorize corporate action with respect to most matters concerning the Company’s and its subsidiaries’ interests. This committee is also in charge of the day-to-day activities on the Operating and Holding level.

24 Orascom Telecom Holdings Annual Report 2011

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 2726

Financial review

Table 1: Total Subscribers1

Subsidiary31 Dec 2010US$ (3 months)

30 Sept 2011 US$ (3 months)

31 Dec 2011 US$ (3 months)

Inc/(dec)

Dec 2011 vs. Dec 2010

Djezzy (Algeria) 15,087,393 16,288,615 16,595,233 10.0%

Mobilink (Pakistan) 31,794,292 33,415,696 34,213,552 7.6%

banglalink (Bangladesh) 19,327,005 22,139,953 23,753,552 22.9%

Telecel Globe2 2,974,000 2,825,000 3,140,000 5.6%

Total 69,182,690 74,669,264 77,702,337 12.3%

Operations accounted for under the equity method31 Dec 2010 US$(3 months)

30 Sept 2011 US$(3 months)

31 Dec 2011 US$(3 months)

Inc/(dec)Dec 2011 vs. Dec 2010

Wind Canada (Canada) 232,641 358,000 403,000 73.2%

Total 232,641 358,000 403,000 73.2%

Grand Total 69,415,331 75,027,264 78,105,337 12.5%

1. For comparative purposes, the subscriber figures for 2010 and September 2011 have been adjusted to reflect the demerger of Mobinil, koryolink and Alfa2. Global ARPU is calculated on a year to date basis, taking into account the weighted average subscribers for calculation.2 Including Zimbabwe; after excluding Powercom Ltd (Namibia) subscribers in December 2010

The Demerger has already been reflected in the consolidated balance sheet as of December 31, 2011, whilst, for income statement purposes, the results of operations have been classified as discontinued operations.

Operating performance

SubscribersOrascom Telecom ended the year 2011 with a subscriber base of over 78 million, showing an increase of almost 13% compared to the previous year. For comparative purposes, the subscriber figure for 2010 has been adjusted to reflect the demerger of Mobinil, koryolink and Alfa, as well as the sale of Powercom Ltd in Namibia.

Algeria’s subscribers increased 10% in comparison to December 2010, as a result of controlling churn alongside successful customer acquisitions.

In Pakistan, Mobilink’s subscriber base grew almost 8% YoY after expanding its portfolio of location-based promotions and focusing on high-quality acquisitions by introducing new pre-paid and post-paid sales promotions. In addition, reactivation promotions were launched to help control churn, which culminated in successful customer retention.

In Bangladesh the subscriber base showed an impressive growth of 23% compared to the previous year, driven by an aggressive acquisition strategy following the SIM Tax reduction in June 2011, as well as loyalty programs and reactivation promotions.

Telecel Globe subscribers showed an increase of 6% in comparison to December 2010, as well as an improvement in subscriber growth QoQ. The subscriber growth is mostly driven by a surge in Burundi’s and Zimbabwe’s customer bases, as a result of increased penetration into rural areas, as well as improved sales and distribution channels performance. It is also worth noting the impressive growth in subscribers compared to 3Q 2011, which was boosted by Zimbabwe’s recapturing of subscribers after a dip in 1H 2011.

In Canada, WIND Mobile subscribers increased 73% compared to the closing base of 2010.

ARPU

In Algeria, ARPU for 4Q 2011 showed a decline of 7% in US$ and local currency terms as compared to 4Q 2010. The decrease is due to the penetration of lower income segments within the customer base, in addition to an accounting provision concerning the “Imtiyaz” loyalty program.

In Pakistan, Mobilink’s ARPU decreased by 7% YoY in US$ terms and by 4% in local currency terms amidst a highly competitive environment. The decline is due to the penetration of lower-end segments in the market through location based promotions in most of the major cities in Pakistan. It is worth noting that ARPU levels were stable in comparison

to the previous quarter.

In Bangladesh, ARPU showed a decline in both US$ and local currency terms, decreasing 14% and 6% respectively. Accelerated growth of subscribers in rural and youth market segments led to some ARPU dilution, while the continuing devaluation of the local currency against the US$ also had an adverse impact on ARPU for 4Q 2011.

In Canada, WIND Mobile experienced a 13% decline in ARPU YoY, while showing stability compared to the previous quarter.

A year of record performance

Highlights

• Total subscribers exceeded 78 million, an increase of 13% over the same period last year, after the exclusion of Alfa, Mobinil and koryolink subscribers for comparative purposes.

• Revenues reached US$ 896 million1, decreasing by 2% compared to 4Q 2010, as a result of the liquidation of the handset business of “Ring” as well as unfavourable currency movements. GSM revenues showed almost 2% growth for the quarter. Revenues for the full year showed an increase of 2% compared to 31 December 2010.

• EBITDA reached US$ 346 million1, a decrease of 4% compared to the same period last year, mainly driven by an increase in corporate contingent liability provisions at the OT Holding level, in addition to unfavourable currency movements. GSM EBITDA increased by 4% YoY. EBITDA for the full year increased 10% compared to the previous year, driven by strong GSM performance of 11%.

• Group EBITDA margin stood at 38.7%, stable over 4Q 2010. EBITDA margins for the major subsidiaries were: Djezzy 58.6%, Mobilink 41.4%, and banglalink 19.2%.

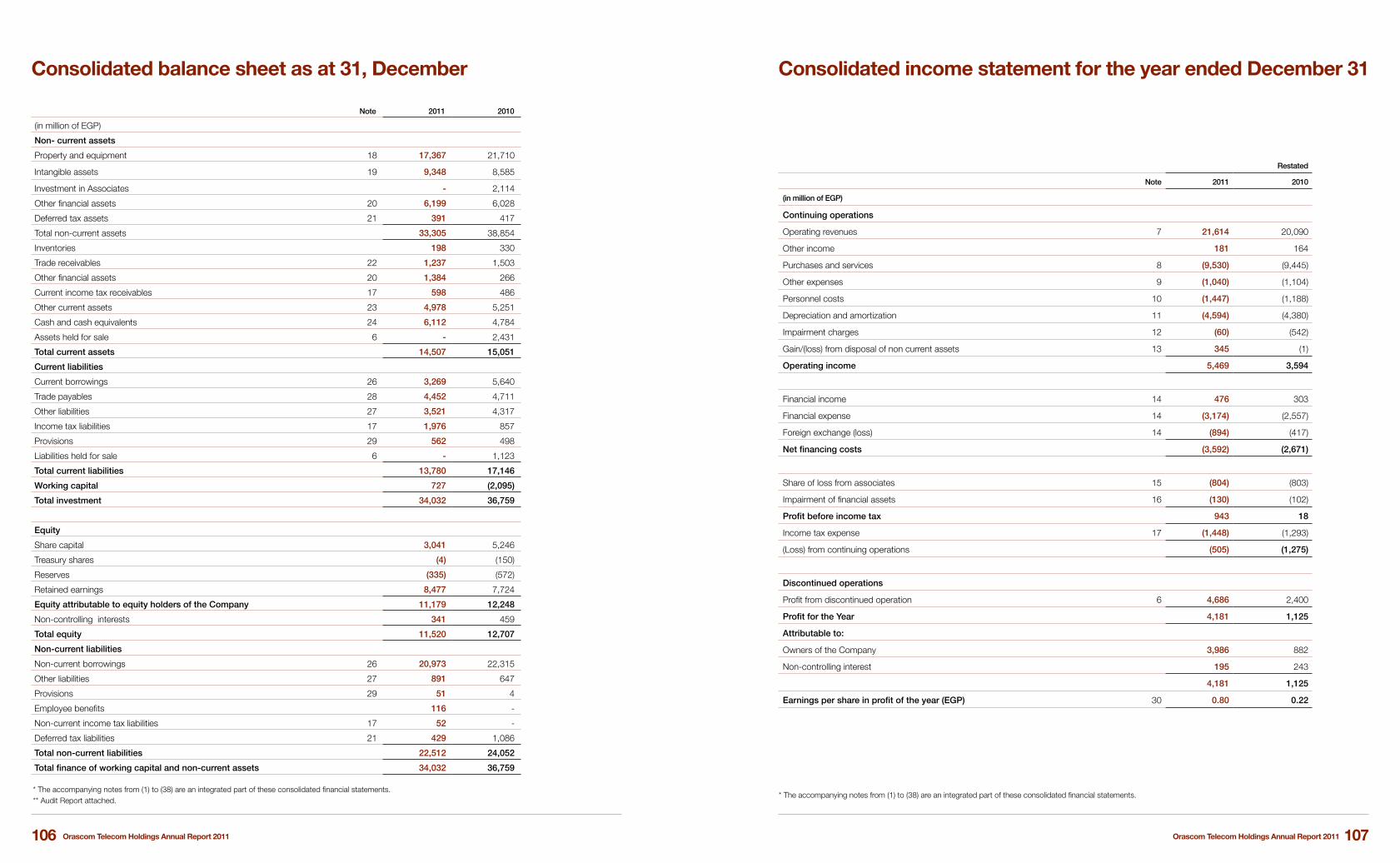

• Net Income before minority interest for the quarter was negative for US$ 83 million1 compared to a loss of US$ 170 million recorded during the same period last year. The improvement is due to a three-fold boost in operating income, which was adversely impacted by the impairment of the company’s assets in Namibia the previous year. Net income attributable to equity holders for the year 2011 was US$ 661 million1.

• Net Debt2 as of December 31, 2011 stood at US$ 3,022 million1, a decrease of over 25% compared to 31 December 2010; with a Net Debt/EBITDA of 1.8x.

Table 2: Blended Average Revenue Per User (ARPU)1

Operations accounted for under the equity method31 Dec 2010 US$ (3 months)

30 Sept 2011 US$ (3 months)

31 Dec 2011 US$ (3 months)

Inc/(dec) Dec 2011 vs. Dec 2010

Djezzy (Algeria) 9.7 9.9 9.0 (7.2%)

Mobilink (Pakistan) 2.9 2.7 2.7 (6.9%)

banglalink (Bangladesh) 2.1 1.9 1.8 (14.3%)

Wind Canada (Canada) 30.0 25.9 26.0 (13.3%)

Global ARPU (YTD)2 4.2 4.2 4.1 (2.8%)

Global ARPU (3 months) 4.2 4.2 4.1 (2.8%)

1. After excluding Mobinil and koryolink subscribers from December 2010.2. Global ARPU is calculated on a year to date basis, taking into account the weighted average subscribers for calculation.

1. US$ financial figures in the Income Statement & Balance Sheet are according to the International Financial Reporting Standards (IFRS).

2. Net Debt is calculated as a sum of Short Term Debt, Long Term Debt, less Cash and Cash Equivalents.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 2928

Market Share & Competition

During the fourth quarter of 2011, Orascom Telecom continued to lead in its core operating markets, with the exception of Bangladesh where banglalink continues to maintain its second largest market share position.

In Algeria, market share declined by 2.2 p.p. in comparison to 3Q 2011 as a result of aggressive competitive pressures surrounding channel acquisitions, and the ongoing adverse operating conditions resulting from the ban on foreign currency transfers and other Government

actions, which have restricted the import of essential equipment, and the undertaking of critical network maintenance.

In Pakistan, the market share of Mobilink dropped 0.2 p.p. as measured on internal traffic patterns, as a result of the continued market-wide focus on MNP and aggressive competitive pressures.

In Bangladesh, banglalink witnessed an increase in market share of 0.7 p.p. as a result of its successful customer acquisition strategy.

CAPEX

Total consolidated capital expenditures for 4Q 2011 showed a 24% increase compared to the previous year, in line with strategic investment plans.

In Algeria, CAPEX declined 41% in comparison to 4Q 2010, as a result of the ongoing ban on foreign currency transfers preventing the payment of essential suppliers, as well as the importing of equipment critical to network maintenance and necessary expansion.

In Pakistan, CAPEX increased 129% YoY due to the continued focus on network and IT development for Mobilink.

In Bangladesh, CAPEX decreased 16% in comparison to the aggressive network roll-out plan of the previous year. It is worth noting that the 2G license renewal fee was booked as accrued (accounting) CAPEX since the company received the title for the license while the payment will be made in instalments. From a cash flow perspective, however, the actual amount paid in Q4 was US$118 million and the remaining part of approximately US$138 million is deferred.

“Other” CAPEX increased by 112% compared to the same period last year. The increase is mainly due to investments made in

Table 4: Market Share & Competition

Country Brand Name Market Share (%) Market Position Names of additional network operations

30 Sept 2011 31 Dec 2011

Algeria Djezzy 57.7% 55.5% 1 AMN, Qtel

Pakistan1 Mobilink 30.3% n.a2 1 U-Fone, Paktel, Telenor, Al Warid

Bangladesh1 banglalink 27.2% 27.9% 2 Grameen, Aktel, Citycell, BTTB, Airtel

1. Market share, as announced by the national Regulator is based on information disclosed by the other operators which use different subscriber recognition policies. 2. Market share for December 2011 had not been disclosed by the Pakistani Regulator prior to this release.

Telecel Globe for the purpose of network expansion and 3G.

Table 5: Capital Expenditure of OTH Subsidiaries1

Subsidiary 4Q 2010 4Q 2011 inc / (dec)

TotalUS$ Million2010

TotalUS$ Million2011 inc / (dec)

Djezzy (Algeria) 35 21 (41%) 90 40 (56%)

Mobilink (Pakistan) 48 110 129% 143 261 83%

banglalink (Bangladesh) 82 69 (16%) 235 409 74%

Other2 6 13 112% 27 28 2%

Total Consolidated 172 213 24% 495 738 49%

Consolidated Capex/Sales 18.7% 23.8% 5 p.p. 13.9% 20.3% 6.4 p.p.

1.CAPEX figures excluding license fees.2. “Other” companies include OT Holding, Ring and Telecel Globe.

Table 3: Blended Average Revenue Per User (ARPU) (Local Currency)

Subsidiary31 Dec 2010 US$(3 months)

30 Sept 2011 US$(3 months)

31 Dec 2011 US$(3 months)

Inc/(dec) Dec 2011 vs.Dec 2010

Djezzy (Algeria) (DZD) 724.1 714.9 673.1 (7.0%)

Mobilink (Pakistan) (PKR) 244.6 235.6 234.9 (4.0%)

banglalink (Bangladesh) (BDT) 148.9 147.1 140.3 (5.8%)

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 3130

Financial Review

Revenues

Total Consolidated Revenues for 4Q 2011 declined by 2% compared to the previous year, as a result of modest growth in GSM revenues countered by the liquidation of the handset business of “Ring”, as well as local currency devaluation against the US$ in OTH’s main operating countries. For the full year, consolidated revenues improved by 2%, driven by nearly 6% increase in GSM revenues.

In Algeria, revenues remained stable for the quarter showing 1% growth in comparison to 4Q 2010. In local currency terms, revenues increased 3% YoY, mostly driven by the growth in OTA’s subscriber base.

In Pakistan, revenues increased 1.5% in US$ terms, impacted by currency devaluation. In local currency terms, revenues were up 4% in 4Q 2011 compared to the previous year, mainly due to an increase in

subscribers, steady VAS uptake, as well as higher administrative fees on scratch cards.

In Bangladesh, the ongoing devaluation of the local currency against the US$ was responsible for the difference in revenue growth in US$ vs. local currency, up 5% and 16.5% respectively for the quarter. The growth in revenues is attributable to tariff revisions, aggressive competitive moves, and a strong focus on VAS, which contributed to solid additions to the subscriber base of banglalink.

Telecel Globe revenues declined by 5% in comparison to 4Q 2010 as a result of the sale of the operation in Namibia, in addition to currency devaluation in Burundi. On a comparable basis, excluding the sale of Powercom Ltd. in Namibia, revenues display an increase of 8.6% YoY.

Table 6: Consolidated Revenues YoY

Subsidiary

Represented4Q - 20101

(3 months)US$ (000)

4Q - 2011(3 months)US$ (000)

Inc/(dec)

Represented 31 Dec 20101

US$ (000

31 Dec2011US$ (000)

Inc/(dec)

GSM

Djezzy (Algeria) 452,911 457,085 0.9% 1,746,566 1,859,804 6.5%

Mobilink (Pakistan) 280,863 285,175 1.5% 1,107,067 1,133,704 2.4%

banglalink (Bangladesh) 122,285 128,278 4.9% 456,984 511,291 11.9%

Telecel Globe (Africa)2 25,007 23,743 (5.1%) 101,830 93,683 (8.0%)

Total GSM 881,068 894,282 1.5% 3,412,447 3,598,482 5.5%

Telecom Services

Ring 37,121 1,432 (96.1%) 152,278 37,096 (75.6%)

Total Telecom Services 37,121 1,432 (96.1%) 152,278 37,096 (75.6%)

Total Consolidated 918,188 895,714 (2.4%) 3,564,725 3,635,578 2.0%

1. 2010 figures have been represented to reflect the completion of the demerger process.2. As per IFRS rules, Telecel Globe figures have not been represented in 2010 and H1 2011to reflect the disposal of Powercom Ltd. in 2Q 2011.

Table 7: Consolidated Revenues QoQ

Subsidiary Represented 4Q - 2010 (3 months) US$ (000) 4Q - 2011 (3 months) US$ (000) Inc/ (dec)

GSM

Djezzy (Algeria) 486,671 457,085 (6.1%)

Mobilink (Pakistan) 281,490 285,175 1.3%

banglalink (Bangladesh) 129,306 128,278 (0.8%)

Telecel Globe (Africa) 21,340 23,743 11.3%

Total GSM 918,807 894,282 (2.7%)

Telecom Services

Ring 6,644 1,432 (78.4%)

Other 27,931 - n.a.

Total Telecom Services 6,644 1,432 (78.4%)

Total Consolidated 925,451 895,714 (3.2%)

Total consolidated revenues for 4Q 2011 decreased 3% compared to 3Q 2011, mostly impacted by a drop in GSM revenues for the quarter.

In Algeria, revenues declined 6% in US$ terms and 4% in local currency terms. The decrease is a result of an accounting provision concerning the “Imtiyaz” loyalty program.

In Pakistan, revenues increased 1% in US$ terms and 2% in local currency terms, in line with subscriber usage and VAS growth.

In Bangladesh, revenues increased 3% in local currency terms, mostly due to tariff revisions, VAS and MFS offerings, as well as additions to the subscriber base. Revenues were partially slowed by disconnection regulations concerning the post-paid base.

Telecel Globe revenues grew by 11% compared to the previous quarter, driven by increases in the ARPU of CAR, as well as a significant subscriber increase in Burundi for 4Q 2011.

Table 8: Proforma Consolidated Revenues (Local Currency)1

Subsidiary4Q - 2010(3 months)

4Q - 2011(3 months) Inc/ (dec)

3Q - 2011(3 months) Inc/ (dec) 31 Dec 2010 31 Dec. 2011 Inc/ (dec)

GSM

Djezzy (Algeria) (DZD bn) 32.84 33.86 3.1% 35.4 (4.3%) 129.24 135.64 5.0%

Mobilink (Pakistan) (PKR bn) 23.94 25.00 4.3% 24.5 2.0% 94.34 97.90 3.8%

banglalink (Bangladesh)(BDT) 8.47 9.87 16.5% 9.6 2.9% 31.82 37.88 19.0%

1. Un-audited Figures.

Orascom Telecom Holdings Annual Report 2011Orascom Telecom Holdings Annual Report 2011 3332

EBITDA

Consolidated EBITDA for 4Q 2011 decreased 4% YoY, mainly driven by an increase in corporate contingent liability provisions at the OT Holding level, in addition to unfavourable currency movements. GSM EBITDA increased by 4% YoY. On a year-to-date basis, consolidated EBITDA increased over 10%, as a result of the operational excellence program, which helped boost GSM EBITDA by nearly 11%.

In Algeria, EBITDA increased 11% in US$ terms while showing an 18% increase in local currency terms, as a result of currency devaluation against the US$. The increase is mainly attributable to OPEX savings coupled with strong top line performance in the quarter.