Market Data / Supplier Selection / Event Presentations / User Experience Benchmarking / Best Practice / Template Files / Online Measurement and Strategy Report 2011 in association with Lynchpin

Transcript

Market Data / Supplier Selection / Event Presentations / User Experience Benchmarking / Best Practice /

Template Files /

Online Measurement and Strategy Report 2011

in association with Lynchpin

Online Measurement and Strategy Report 2011 in association with Lynchpin

Online Measurement and Strategy Report 2011in association with Lynchpin

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Online Measurement and Strategy Report 2011in association with Lynchpin

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 1

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Econsultancy is a digital publishing and training group used by more than 200,000 Internet professionals every month.

The company publishes practical and time-saving research to help marketers make better decisions about the digital environment, build business cases, find the best suppliers, look smart in meetings and accelerate their careers.

Econsultancy has offices in New York and London, and hosts more than 100 events every year in the US and UK. Many of the world's most famous brands use Econsultancy to educate and train their staff.

Some of Econsultancy‟s members include: Google, Yahoo, Dell, BBC, BT, Shell, Vodafone, Virgin Atlantic, Barclays, Deloitte, T-Mobile and Estée Lauder.

Join Econsultancy today to learn what‟s happening in digital marketing – and what works.

Call us to find out more on +1 212 699 3626 (New York) or +44 (0)20 7269 1450 (London). You can also contact us online.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 2

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 3

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

3. Executive Summary and Highlights This is the fourth annual Online Measurement and Strategy Report published by

Econsultancy in association with Lynchpin.

The research is based on a survey of more than 800 companies (including both „client-side‟ organisations and agencies) which was carried out in March and April 2011.

Key findings:

Companies continue to wrestle with a joined-up approach to data collection and

analysis, which incorporates web data into broader business strategy. Only a

minority of companies have common KPIs (key performance indicators) for

online and offline data.

– Disappointingly, fewer companies than last year say they have a company-wide strategy in

place that ties data collection and analysis to business objectives (22% compared to 25%

last year). Only 28% of respondents say that web analytics definitely drive actionable

recommendations that make a difference to their organisation, down from 31% last year.

– 41% of companies say they have common key performance indicators (KPIs) for web and

non-web data, while just 19% have common teams and processes for web and non-web

data.

– Only 22% of companies have a framework for analysing customer journeys that cross

online and offline, while a similar proportion (24%) of responding organisations carry out

attribution modelling to give more insight into the relationship between different

channels.

– But it is encouraging to see that more companies than last year (46% versus 41%) are

analysing data which sheds light on the interaction between online and offline.

Reliance on Google Analytics (GA) continues to grow, but many companies still

prefer to use their other analytics vendor for a range of reporting requirements.

– The proportion of companies using Google exclusively for web analytics now stands at 44%,

up from 38% in 2010 and only 23% in 2009. Only 13% of responding companies don’t use

Google Analytics, while the remainder continue to use Google and a paid-for analytics tool

simultaneously.

– Those companies using both Google and a paid-for analytics tool are more likely to use GA

for PPC optimisation, site search usage and campaign tracking.

– But these companies are more likely to use their other, paid-for vendor for traffic and

management reporting, content influence, rich media / flash / video tracking and product

/ cross-sell analysis.

– This group of companies are split evenly in terms of whether they use Google Analytics

(43%) or their other vendor (43%) more frequently.

– Nearly half (48%) of companies using a paid-for tool as well as Google say they do so

because the free tool isn’t sophisticated enough for their requirements.

Companies plan to bolster their resourcing of data analysis for both in-house

staff and outsourced analysts. Companies are more likely than last year to be

increasing budgets for consulting and other third-party services relating to web

analytics.

– 42% of companies are planning to increase the number of employees dedicated to data

analysis over the next 12 months, while a third (31%) are planning for more outsourced

analysis.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 4

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

– Those outsourcing analytics functions are most likely to do so for analysis and

optimisation (52%), strategic consultancy (47%) and implementation support (41%).

– The proportion of companies spending more than £100,000 a year on web analytics has

increased from 9% to 14%.

– 38% of companies are planning to increase web analytics technology spend over the next

year, down slightly from 41% who answered this way in 2010. Some 40% of companies are

planning to increase spending on internal staff, also down slightly on 2010 (44%).

However, the proportion of companies planning to increase budget for consulting and

services now stands at 37%, up from 30% last year.

The number of companies interested in measuring their online reputation and

social media activity continues to grow.

– The proportion of companies who say they analyse reputation, buzz and social media

metrics has significantly increased. Over half of companies (55%) are now analysing this,

compared to 45% of responding organisations in 2010.

– More companies are interested in listening to the voice of the customer, and in measuring

and benchmarking social media activity. The proportion of companies who have paid for

buzz monitoring tools has increased significantly, up to 41% in 2011 from 30% in 2010.

– Companies are also starting to take a more integrated approach to social media

measurement, in terms of the tools they use. A third of companies (33%) now say they use a

combination of tools (including buzz monitoring software and web analytics technology) to

measure online reputation and social media activity. Last year only a quarter of companies

(24%) said they used a mixture of tools.

Financial and resourcing constraints still present the biggest problems, along

with a lack of co-ordination and absence of strategy.

– The biggest barrier preventing companies from having an effective online measurement

strategy is still lack of budget and resources, though significantly fewer companies than

last year cite this as one of the three most significant issues (48% compared to 57%).

– The next most widely cited barriers (as was the case last year) are lack of co-ordination /

siloed organisation (27%) and lack of strategy (also 27%).

– Difficulty in reconciling data (17%), finding staff (13%) and poor technology (16%) are all

significantly more widespread problems than they were a year ago.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 5

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 6

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Lynchpin is proud to sponsor this ongoing research into online measurement and strategy, a topic

naturally close to our hearts as a web analytics consultancy.

The results of this year‟s survey continue a story of great opportunity matched with a fair dose of

practical frustration.

As a discipline, web analytics is still experiencing some growing pains. The expectations for

insight on demand are ever-increasing; meanwhile data volumes continue to grow and start to

spread themselves across disparate sources, presenting new challenges to overcome.

With headcount of dedicated analysts growing, the focus now increasingly turns to process: how

to keep information flowing effectively around a business to drive decisions. Coordinating

technology and people remains a key point of friction in driving value from web data.

Getting the basics right is still a challenge equally worthy of focus. In the value chain of raw data

to actionable insight, the two most frequent points of failure tend to be failure to align KPIs with

business performance, and not collecting the right data in the first place through poor technology

implementation.

The first phase of consolidation of web analytics technology vendors looks to be reaching its

logical conclusion, with the number of major paid web analytics vendors yet again reduced by

mergers and acquisitions.

Google remains a powerful force in the analytics market. The extent of overlap and

complementary usage of Google Analytics alongside paid for tools hints at continuing functional

weaknesses in the paid-for toolsets set against increasing attention to data ownership.

Online measurement needs to reflect the significant growth of multichannel businesses, and here

we start to see the next phases of the market develop. Web analytics vendors are historically poor

at data flexibility. Meanwhile, traditional Business Intelligence vendors historically lack the mind-

set to deal effectively with clickstream data.

As web analytics comes of age, it needs to join-up both the online and the offline, and the

technical and the strategic. We look forward to playing our part in that process over the coming

year.

Andrew Hood

Managing Director

Lynchpin Analytics

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 7

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 8

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.1. Information requirements The chart below shows the different types of information analysed by organisations. Broadly

speaking, organisations are now analysing more data than they were previously and this might

account for the lack of progress companies are making when it comes to translating data into

actionable next steps [See Figure 44]. The more data there is, the harder it is to make sense of

everything within a coherent framework.

The results show that interaction between different online channels (70%) is still the most

common type of data analysed by companies. However, the proportion of companies analysing

this type of data has slightly fallen from 76% since 2010.

Almost two-thirds of companies (65%) are analysing customer survey data, a slight increase since

last year‟s survey, when 60% of companies were analysing this type of data.

The proportion of companies now monitoring reputation / buzz / social media metrics has

significantly increased. Over half of companies (55%) are now analysing such data, compared to

45% of respondents last year. Slightly fewer companies are now analysing competitor

information compared to last year. Some 52% of respondents say their company analyses this,

compared to 57% in 2010.

It is encouraging to see that more companies than last year (46% versus 41%) are analysing the

interaction between online and offline.

Companies

Figure 1: What types of data does your organisation analyse?

2011 response: 382 2010 response: 227

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 9

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Over three-quarters of supply-side respondents (76%) say their clients are analysing the

interaction between different online channels, a significant increase from 2010, when only 64%

of companies were analysing this type of data [Figure 2].

Only 45% of agencies say their clients are analysing customer survey data, compared to 60% of

organisations surveyed.

The proportion of agencies who say their clients are analysing CRM / customer profiling data has

slightly fallen to 45% in 2011, down from 50% in 2010. However, more than half of supply-side

respondents (51%) say their clients are now analysing the interaction between online and offline,

compared to 44% in 2010.

The proportion of clients who are looking at third-party research data has also significantly

increased. Over a third of clients (37%) now analyse this type of data according to the agencies

surveyed. For comparison, in 2010, only 29% of agencies reported their clients analysed this type

of data.

Agencies (supply-side)

Figure 2: What types of data do your clients typically analyse?

2011 response: 274

2010 response: 195

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 10

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.1.1. Which data requirements are business priorities?

The chart below indicates the extent to which different information requirements are regarded as

a business priority.

More than half of companies (57%) report that the cost of acquiring a customer or lead is high-

priority information, while just under half (49%) say that the impact of content on acquisition is

high priority.

It is interesting to note that businesses are most interested in understanding cost-per-acquisition,

which is an important but relatively short term metric. A fuller understanding of the customer

journey and lifetime value is less of a priority.

Just over a quarter of respondents (26%) say the relationship between online and offline is high

priority, while 30% say this is low priority.

Customer behaviour on partner sites is thought to be low priority by just under half of

responding companies (46%). Only 15% say this is high priority and, as Figure 3 shows, this has

fallen by 7% since last year‟s survey.

Information relating to drop-off across key site processes is deemed to be high priority by some

49% of companies, and thought to be medium priority by 39%. This is regarded as less important

in 2011 than last year, with the proportion of respondents saying this is a high priority having

dropped by 10% [Figure 4].

Benchmarking traffic has dropped down the list of business priorities. Some 7% fewer companies

than last year report this to be a high priority.

Companies

Figure 3: How much of a business priority are the following information

requirements?

Response: 385

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 11

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 4: Proportion of respondents reporting information requirement is high

priority – change since 2010

The supply-side responses below show that 61% of agencies report the cost of acquiring a lead to

be a high business priority for clients. The impact of content on acquisition is deemed to be less

important for agency clients than companies themselves indicate.

Some 36% report this type of information as high priority for their clients, compared to just under

half (49%) of companies surveyed.

Only 17% of agencies deem customer behaviour on partner sites to be high priority for clients,

while 38% say this is medium priority and 44% say it is low priority.

Figure 6 shows the change since last year. The proportion of agencies deeming information

relating to performance versus competitors to be high priority for their clients has increased by

6%. The proportion of supply-side respondents reporting information about the customer

journey over multiple visits to be high priority has increased by 5%.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 12

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 5: Typically, how much of a business priority are the following information

requirements for clients?

Response: 273

Figure 6: Proportion of respondents reporting information requirement is high

priority – change since 2010

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 13

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The chart below shows that businesses are more likely to be paying for a range of tools which

measure and optimise business performance. The availability of so many optimisation and

measurement tools is a great opportunity for businesses, but also presents challenges for

companies who want to have an integrated strategy for improving performance and measuring

progress.

As discussed above, an increase in data sources is not in itself useful for businesses, unless

information is harnessed effectively and seen in the context of robust, top-level KPIs.

Looking at the chart in more detail, more than two-thirds (67%) of companies have paid for

online survey tools as shown below. Over half of companies (57%) are now paying for media

planning or tools related to competitor analysis.

The proportion of companies who have paid for buzz monitoring tools has increased significantly,

up to 41% in 2011 from 30% in 2010. This indicates that more companies are interested in

listening to the voice of the customer, and in measuring and benchmarking social media activity.

Companies may also be beginning to see value from undertaking reputation monitoring.

On-site optimisation through feedback and testing is also becoming a more significant priority for

companies. Some 29% are now paying for multivariate testing, compared to 26% last year. The

proportion of companies paying for on-site feedback tools has risen to 29%, up from 20% in 2010.

This reinforces the trend of the increased importance of optimising the on-site experience by

listening to the voice of the customer.

Companies

Figure 7: Has your organisation paid for any of the following types of tools?

2011 response: 280 2010 response: 221

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 14

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The supply-side responses [Figure 8] indicate media analysis and buzz monitoring to be the

types of tool that clients are most likely to pay for. Over half of agencies (56%) say their clients are

now paying for online survey tools, slightly fewer than the proportion of companies.

Buzz and social media monitoring is deemed to be even more important for agencies than for

clients; some 60% of supply-side respondents say their clients are now paying for this technology,

compared to 41% of companies.

Agencies are seeing more evidence of paid-for mobile analytics with a fifth (20%) of supply-side

respondents saying their clients are now paying for this, up from 13% in 2010. Only 13% of

companies this year say they pay for mobile analytics tools, up just a single percentage point since

2010.

Agencies

Figure 8: Do your clients pay for any of the following types of tools?

2011 response: 225 2010 response: 186

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 15

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.2.2. Measuring online reputation and social media activity

It is clear that more companies are beginning to focus on benchmarking and measurement of

social media. Fewer companies now say they don’t measure their online reputation or social

media activity; this has fallen from 27% in 2010 to 21% in 2011.

Companies are also starting to take an integrated approach to social media measurement. Only

12% of companies use their web analytics tool exclusively to measure online reputation and social

media activity, compared to 19% in 2010.

In comparison, a third of companies (33%) say they use a combination of paid-for reputation

monitoring tools, free tools and their web analytics software to measure social media activity. The

proportion of companies using a combination of tools has increased from 24% in 2010.

Companies

Figure 9: How does your organisation measure online reputation and social

media activity?

2011 response: 379

2010 response: 221

Figure 10 indicates that just under half of agencies (47%) say their clients use a combination of

different tools to measure online reputation and social media activity, up from 40% in 2011.

In comparison to the companies surveyed, only 15% of agencies say their clients do not measure

social media activity, compared to 21% of companies.

The proportion of agencies who say their clients now use paid-for monitoring tools has slightly

increased to 18%, up from 14% in 2010. Correspondingly, fewer clients are now using free tools

exclusively, as this has fallen to 13%, down from 18% in last year‟s survey.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 16

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 10: How do your clients measure online reputation and social media

activity?

2011 response: 256

2010 response: 186

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 17

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.2.3. Use of enterprise web analytics technologies

The chart below shows the state of the web analytics market in 2011, indicating that Adobe /

Omniture and Webtrends dominate the industry. Some 35% of companies use Adobe, while 32%

currently using Webtrends.

There has been much M&A activity in the web analytics industry in the past year. The acquisition

of analytics vendors by companies such as Adobe (i.e. Omniture) and IBM (i.e. Unica and

Coremetrics) makes it difficult to directly compare the results to 2010.

The agency findings are shown separately in Figure 12. According to supply-side respondents,

Webtrends is now the most frequently used technology.

Companies

Figure 11: If any, which of the following web analytics vendors do you use?

Response: 207

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 18

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 12: If any, which of the following web analytics vendors do your clients

use?

Response: 200

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 19

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.2.4. Selecting an appropriate web analytics tool

The results below show that agencies still largely take responsibility for recommending the right

tool for their clients to use. Some 63% of agencies said they recommend a tool, while 17% said

they make the decision on behalf of the client. Almost the same proportion (16%) said they use

whatever tool the client has.

Agencies

Figure 13: Who typically takes the lead in selecting the most appropriate web

analytics tool for a given purpose?

2011 response: 258

2010 response: 189

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 20

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

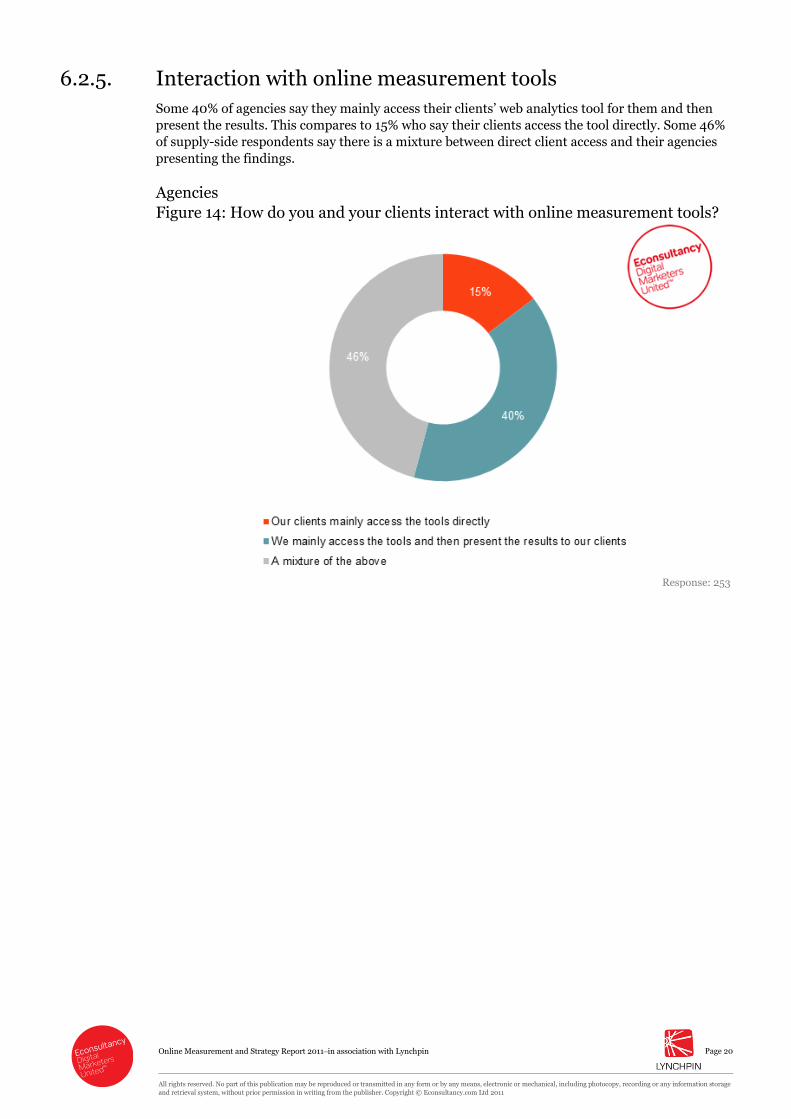

Some 40% of agencies say they mainly access their clients‟ web analytics tool for them and then

present the results. This compares to 15% who say their clients access the tool directly. Some 46%

of supply-side respondents say there is a mixture between direct client access and their agencies

presenting the findings.

Agencies

Figure 14: How do you and your clients interact with online measurement tools?

Response: 253

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 21

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Supply-side respondents were asked to what extent they share online measurement data with

their clients. The majority (55%) said that they did not share as much data with their clients as

they would like.

However, it is more encouraging to see that over a third of agencies (38%) say they share online

measurement data to a great extent.

Agencies

Figure 15: To what extent do you and your clients share online measurement

data?

Response: 255

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 22

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The proportion of companies exclusively using Google Analytics (44%) has increased again this

year, up from 38% in 2010 and only 23% in 2009. This is accompanied by a drop in the

proportion of companies using Google Analytics in addition to other analytics tools.

Companies

Figure 16: Does your organisation use Google Analytics?

2011 response: 385

2010 response: 227

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 23

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The supply-side responses are shown separately below, with more evidence that companies are

more likely to be using Google Analytics as their sole web analytics tool. Some 35% of agencies say

their clients use Google Analytics exclusively, while 62% say their clients use this in conjunction

with another tool.

Agencies

Figure 17: Do your clients typically use Google Analytics?

2011 response: 261

2010 response: 191

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 24

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Of the clients who are exclusively using Google Analytics, some 87% use the platform for

understanding traffic and conversion KPIs. Over two-thirds of companies (68%) are using

campaign tracking, while 60% are using it for management reporting.

At the lower end of the scale, only 17% of company use Google for reporting related to product

and cross-sell analysis, while 9% use Google Analytics for rich media, flash and video tracking.

Companies

Figure 18: Do you use Google Analytics for any of the following types of reporting

or insight? [Companies exclusively using Google Analytics]

Response: 167

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 25

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.3.3. Frequency of Google Analytics usage (compared to other

tool)

Looking at the use of different analytics tools, it is apparent that there is an even spread between

how frequently companies use Google Analytics versus another analytics provider. Some 43% of

responding companies said they use Google Analytics more frequently, while the same proportion

said they use another analytics provider more often.

The proportion of companies who say they use Google Analytics more frequently has slightly

increased to 43%, up from 38% in 2010. Some 15% of companies report the same level of usage

between Google and another analytics provider.

Companies Figure 19: Which do you use more frequently? [Companies not exclusively using Google Analytics]

2011 response: 150

2010 response: 108

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 26

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.3.4. Reasons for using additional paid-for analytics tools

Of companies who use another tool in addition to Google Analytics, just under half (48%) say this

is because Google is not sophisticated enough for their requirements. This compares to 41% in

2010.

Companies are less concerned about a dependence on Google, as only 14% said they don’t want to

be completely reliant on Google, down from 30% of respondents in last year‟s survey. Some 14%

are still assessing whether Google Analytics alone is sufficient.

Some 20% of companies stated „other‟. Reasons include the fact that Google only promises to keep

data for up to a year, and some companies require the data to be stored for a longer time period

than this. The lack of competitor benchmarking tools on Google also leads to some companies

using additional analytics tools.

Companies are also concerned with security issues and vulnerabilities in the cloud. One

respondent also mentioned that Google was thought to be unreliable on its own.

A handful of companies only use Google for quick measurements on their microsites, rather than

as a tool to measure their entire main website activity.

Companies

Figure 20: What is the main reason you continue to use a paid-for tool as well as Google Analytics? [Companies not exclusively using Google Analytics]

2011 response: 147

2010 response: 103

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 27

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The chart below shows responses from companies who do not use Google Analytics. Some 42% of

companies say the main reason they do not use Google‟s technology is because they are happy

with their existing web analytics supplier.

A fifth of companies (19%) say they do not want Google to have data about their site, while 15%

say the platform is not sophisticated enough for their requirements. However, it is worth noting

that proportion of companies who now say Google is not sophisticated enough has fallen

considerably, down from 23% in 2010.

There has also been an increase in the proportion if companies who state „other‟. This mainly

relates to legal issues, and concerns about data privacy, as well as restrictions imposed by the

company‟s IT departments.

Note: sample sizes for this chart are small

Companies

Figure 21: What is the principal reason you don't use Google Analytics?

[Companies not using Google Analytics]

2011 response: 53

2010 response: 26

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 28

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

content influence, rich media / flash / video tracking and product / cross-sell analysis.

Some 43% of responding companies use Google for PPC or AdWords optimisation, while 21% use

another analytics vendor. Over a third of companies (36%) use Google for site search usage data,

while 31% use their other vendor. There is a fairly even split between companies who use Google

and other vendors for campaign tracking. While a third (33%) use Google, some 32% use other

vendors. This compares to over a quarter (28%) who use both Google and other vendors.

Companies are most likely to use other vendors for management reporting (41%) compared to

22% of companies who use Google exclusively. Around a third (30%) say they use Google as well

as another vendor for this requirement.

Companies

Figure 22: Which tool do you use for the following types of reporting or insight?

[Companies not exclusively using Google Analytics]

Response: 153

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 29

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Supply-side respondents indicate their clients are more likely to use Google Analytics than

another vendor for the full range of reporting needs, except for rich media and video tracking.

Some 68% say their clients are using Google for PPC optimisation, while only 11% use other

vendors.

Over half of agencies (57%) say their clients use Google exclusively for site search metrics.

A quarter (26%) of agencies say their clients use Google for rich media tracking, while 32% say

clients use another vendor for this purpose.

Some 32% of companies use Google Analytics for product and cross-sell analysis, while 27% use

another vendor. Just 16% say they do not use any tool for tracking this, while 24% are using a

mixture of Google Analytics and another vendor for tracking this.

Agencies

Figure 23: Which tool do your clients typically use for the following types of

reporting or insight?

Response: 257

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 30

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

For companies that are not using Google Analytics, some 84% use their current analytics tool for

campaign tracking, while 82% use their tool for traffic and conversion KPIs.

Some 71% of companies are using their tool for management reporting, while over two-thirds

(67%) are using web analytics technology for funnel and conversion optimisation.

At the other end of the scale, only 29% are using their tool for tracking rich media or video, while

the same proportion use technology for gauging content influence.

Companies

Figure 24: Do you use your web analytics tool for any of the following types of

reporting or insight? [Companies not using Google Analytics]

Response: 49

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 31

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

For companies who are using Google Analytics in conjunction with another tool, half (50%) feel

that they are getting ROI from their paid-for analytics tool. The proportion of companies who are

getting ROI has fallen, down from 58% in 2010.

Some 11% of companies say they are not getting value. Over a third of respondents (39%) say they

do not know if they are reaping ROI.

Figure 25: Do you get return on investment from your paid-for analytics tool?

[Companies also using Google Analytics]

2011 response: 155

2010 response: 105

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 32

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

A third of respondents (35%) say they have one dedicated web analyst, a significant drop from

2010, when 42% had a single employee dedicated to analysis of web data.

Although the proportion of companies with no dedicated web analysts has slightly increased from

22% in 2010 to 25% in 2011, more companies this year say they have a team of three dedicated

web analysts. Some 9% of companies now have three dedicated web analysts compared 4% in

2010.

Companies

Figure 26: How many dedicated employees does your organisation have doing

analysis of web data?

2011 response: 364 2010 response: 217

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 33

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Just under two-thirds of companies (62%) have no regular contractors for analysis of web data,

down from 73% in 2010.

The proportion of companies with one regular contractor has slightly increased since last year.

Just under a quarter of companies (23%) now have one regular contractor, compared to 15% last

year.

Companies

Figure 27: How many regular contractors does your organisation have doing analysis of web data?

2011 response: 364

2010: response: 217

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 34

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Most companies (65%) do not take any days of outsourced analysis from agencies or third parties.

Some 10% say their companies take one day of outsourced analysis from agencies per month,

compared to 7% who take two days per month.

Companies

Figure 28: How many days per month of outsourced analysis does your

organisation take from agencies or other third parties?

2011 response: 369

2010: response: 216

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 35

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

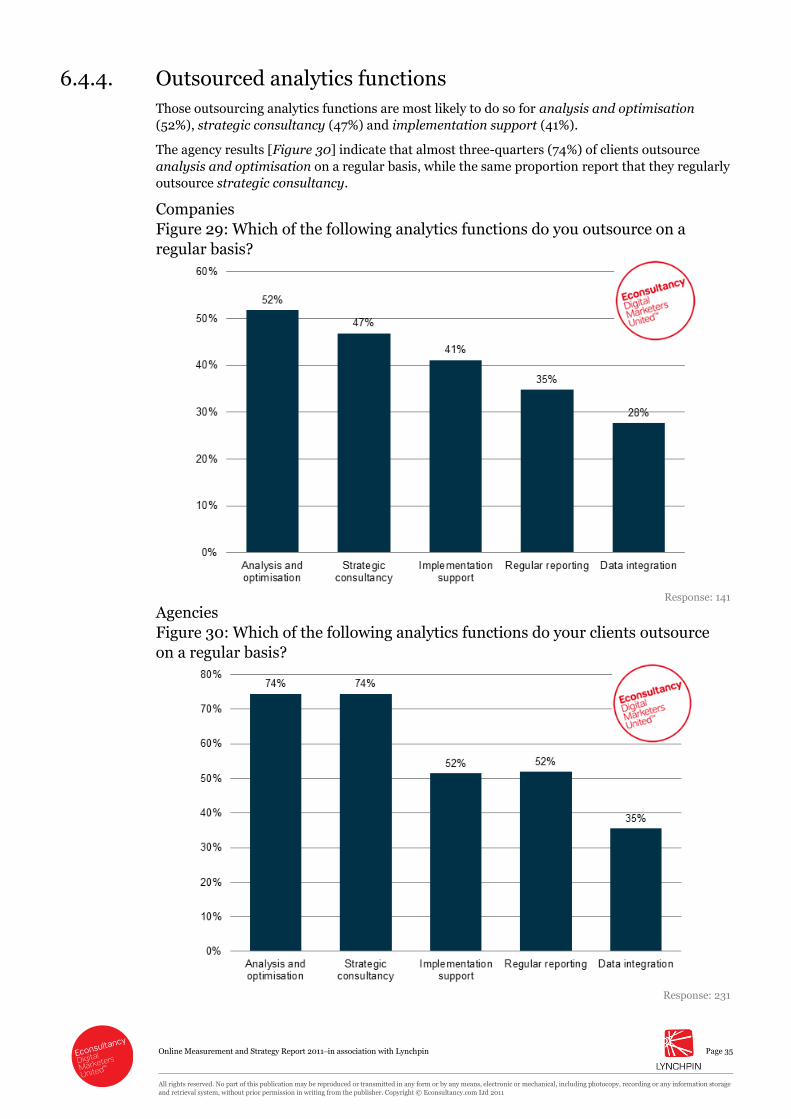

Those outsourcing analytics functions are most likely to do so for analysis and optimisation

(52%), strategic consultancy (47%) and implementation support (41%).

The agency results [Figure 30] indicate that almost three-quarters (74%) of clients outsource

analysis and optimisation on a regular basis, while the same proportion report that they regularly

outsource strategic consultancy.

Companies

Figure 29: Which of the following analytics functions do you outsource on a

regular basis?

Response: 141

Agencies

Figure 30: Which of the following analytics functions do your clients outsource

on a regular basis?

Response: 231

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 36

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.4.5. Web analytics resourcing (increase or decrease)

The majority of companies are planning to keep resourcing of data analysis the same, as indicated

by the chart below. While some 42% are planning to increase resources for dedicated employees,

57% say they will keep this the same.

Almost three-quarters of respondents (73%) plan to keep regular contractors the same, while 61%

say they plan to keep resourcing for outsourced analysis the same.

Companies

Figure 31: Over the next 12 months, are you planning to increase or decrease your

resourcing of data analysis in these areas?

Response: 360

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 37

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The proportion of companies spending more than £100,000 a year on web analytics has increased

from 9% last year to 14% this year. Some 42% of companies are spending £5,000 or less on web

analytics per year, the same proportion as 2010.

Generally speaking, the results below show that spending on web analytics technology has not

dramatically changed in the last year, and has remained fairly consistent. Some 8% say they

spend between £100,000 and £200,000 on web analytics, while 6% now spend £200,000 or

more.

Companies

Figure 32: In total, how much do you spend on web analytics each year?

2011 response: 365 2010 response: 215

Some 39% of agencies suggest their clients are spending up to £5,000 on web analytics per year, a

slight increase from 2010. Similarly, the proportion of agency clients spending between £5,000

and £10,000 per year has increased to 24%, up from 15% in 2010.

Agencies

Figure 33: On average, how much do your clients spend on web analytics each

year?

2011 response: 244 2010 response: 181

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 38

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

On average, more than half of web analytics expenditure (52%) is now spent on internal staff,

while 29% is spent on technology. Almost a fifth of investment (19%) is spent on consulting and

services.

According to supply-side respondents [Figure 35], spending on analytics is heaviest for consulting

and services.

Companies

Figure 34: How is your web analytics expenditure split between the following areas?

2011 response: 303 2010 response: 182

Agencies

Figure 35: Typically, how is a client's web analytics expenditure split between the following areas?

2011 response: 214 2010 response: 148

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 39

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

In terms of where companies will be increasing their analytics-related spending over the next

year, there is a fairly even split between spend on technology, consulting or services and internal

staff. Some 40% plan to increase expenditure on internal staff, while a similar proportion plan to

do the same for technology (38%) and consulting (37%). Some 58% plan to keep spending on

these three areas the same over the next 12 months.

The results from 2010 are shown in Figure 37, and highlight that more companies this year are

planning to increase spending on consulting and services, up from 30% in 2010.

Conversely, the percentages for companies increasing investment in technology and internal staff

have slightly fallen.

Companies – 2011 results

Figure 36: Over the next 12 months, are you planning to increase your web

analytics budget in the following areas?

Response: 356

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 40

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 37: Over the next 12 months, are you planning to increase your web

analytics budget in the following areas?

Response: 211

Supply-side responses are shown in Figure 38. Over half of agencies (57%) say their clients plan

to increase spend on consulting and services, while 37% say their clients plan to keep this the

same.

More agencies than the companies themselves report clients are increasing consulting budgets

Some 42% say their clients plan to increase spend on technology, while 41% report their clients

are increasing budgets for internal staff.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 41

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 38: Over the next 12 months, are your clients planning to increase their

web analytics budget in the following areas?

Response: 243

Results from 2010

Figure 39: Over the next 12 months, are your clients planning to increase their

web analytics budget in the following areas?

Response: 148

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 42

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The chart below indicates who within the organisation is most likely to take responsibility for the

budget, and indicates this is most likely to be the remit of senior management or online

marketing.

While some 28% of respondents say senior management owns the budget, a quarter (25%) say

online marketing takes responsibility for this. Some 16% say a mixture of departments takes

charge of managing online measurement budget.

The agency results [Figure 41] also show that the responsibility for online measurement budget

within client organisations usually lies with senior management or online marketing.

The proportion of agencies who say that senior management take responsibility for the online

measurement budget has significantly jumped this year to 30%, up from 18% in 2010. This is

encouraging as it indicates that senior managers increasingly understand the value of online

measurement and reporting.

Companies

Figure 40: Who 'owns' the budget for online measurement within your

organisation?

2011 response: 364

2010 response: 213

Note: ‘mixture of the above’ means a mixture of departments

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 43

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 41: Who is most likely to 'own' the budget for online measurement within

a client company?

2011 response: 243

2010 response: 178

Note: ‘mixture of the above’ means a mixture of departments

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 44

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.5.1. Company-wide strategy Only 22% of companies say they have a company-wide strategy for collecting and integrating data

analysis with business objectives, while almost two-thirds (63%) say they are working on this.

Some 15% do not have a strategy in place for this at all.

Disappointingly, there hasn‟t been any improvement since last year. We believe this is because the

growing number of data sources and tools available make it harder for companies to decide top-

level KPIs which reflect business objectives.

The lack of improvement in this area may also be due to increased expectations. There is now

more understanding around what goes into a company-wide strategy and increased realisation

that they are further away from this than they originally thought, despite moving in the right

direction.

The agency results [Figure 43] indicate that only 16% of respondents say their clients have a

company-wide strategy in place, while 61% say they are working on this. Just under a quarter

(23%) of respondents say their clients do not have a company-wide strategy in place.

Companies

Figure 42: Do you have a company-wide strategy that ties data collection and

analysis to business objectives?

2011 response: 362

2010 response: 213

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 45

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 43: Do your clients typically have a company-wide strategy that ties data

collection and analysis to business objectives?

2011 response: 244

2010 response: 179

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 46

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.5.2. Driving actionable recommendations from analytics

Over three-quarters of companies (85%) say that web analytics drive actionable recommendations

within their organisation. But only 28% say that analytics definitely drive actionable

recommendations, while 57% say they sometimes drive actionable recommendations.

Again, there has sadly not been any improvement since last year which can be attributed to an

increase of data and reporting requirements, which can obfuscate the bigger picture about what is

important and what needs to be done.

Companies

Figure 44: Do web analytics drive actionable recommendations that make a

difference to your organisation?

2011 response: 362

2010 response: 211

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 47

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Almost two-thirds of supply-side respondents (62%) say web analytics sometimes drive

actionable recommendations for clients, while 27% say this is definitely the case. Only 10% of

agencies responded with „No – not really’. There has been little change since last year, as Figure

45 shows.

Agencies

Figure 45: Do web analytics typically drive actionable recommendations that

make a difference to your clients' organisations?

2010 response: 246

2011 response: 180

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 48

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The chart below shows the average amount of web analytics data that is thought to be useful for

driving business decision-making. Some 62% of companies say that less than half of web analytics

data is useful, the same percentage as last year.

The 2010 Online Measurement and Strategy Report showed a positive movement of respondents

from the 0-25% to the 26-50% category compared to 2009, which was encouraging.

This year, more respondents have shifted back to the lower percentage band which is

disappointing. More companies now report that less than a quarter of web analytics data is useful

for decision-making (27% this year compared to 22% last year).

As mentioned above, this can be attributed to an increase in available data which is outpacing the

speed at which businesses can translate information into actionable insights.

From this chart, we have worked out the average amount of web analytics data thought to be

useful for driving decision-making is approximately 43%. The average amount of useful data in

2010 was 44%.

Companies

Figure 46: Approximately, what percentage of the web analytics data you collect

is useful to your organisation for driving decision-making?

2011 response: 363 2010 response: 213

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 49

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The agency results below show that over a third of respondents (35%) say that between 26% and

50% of analytics data is useful for their clients. This compares to 37% last year. Some 61% of

supply-side respondents report that up to half of analytics data is useful for client decision-

making.

Agencies

Figure 47: Approximately, what percentage of the web analytics data your clients

collect is useful to their organisations for driving decision-making?

2011 response: 242 2010 response: 181

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 50

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The results below show the extent to which companies integrate web analytics data into a broader

business strategy. Some 41% of companies have common KPIs for both web and non-web data.

The reality is that, despite a wealth of good intentions, most businesses aren‟t yet at the stage

where they have agreed high-level business intelligence metrics which feed off online and offline

data.

The chart also shows that only a fifth of companies (19%) have common teams and processes for

web and non-web data. Some 11% have a common technology platform for web and non-web

data.

Some 30% of responding companies say their web analytics are not integrated at all into their

business intelligence strategy, while 15% do not have a business intelligence strategy at all.

Companies

Figure 48: To what extent are web analytics integrated into your broader

business intelligence strategy?

Response: 357

Note: respondents could check multiple options

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 51

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

As shown in Figure 49, 43% of agencies report that their clients have common KPIs, while just

over a fifth (22%) say they have common teams and processes. Just 8% say their clients have a

common technology platform.

Agencies

Figure 49: Do your clients typically integrate web analytics into their broader

business intelligence strategies?

Response: 240

Note: respondents could check multiple options

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 52

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.5.5. Integration of analytics data with data from other sources

Some 59% of companies integrate analytics with data from other sources, while 41% do not

integrate with other types of data.

The agency results are shown in Figure 51. Some 52% of agencies say their clients integrate web

analytics with other data sources, while 48% say their clients are not yet doing this.

Companies

Figure 50: Do you integrate web analytics with data from other sources?

Response: 365

Agencies

Figure 51: Do your clients typically integrate web analytics with data from other

sources?

Response: 247

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 53

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The chart below shows how companies are integrating data. Hhalf (50%) are manually collating

data, while 45% say this is semi-automated, for example using spreadsheets and macros.

The extent to which companies are manually manipulating data explains much of the difficulty

involved with implementing an over-arching business intelligence framework which is accurate

and credible within the organisation.

Around a quarter of companies (26%) say they export data from their analytics tool into another

analysis platform. A fifth (20%) choose to import other data sources into their own analytics

platform.

Some 16% say they collate all data from their analytics platform and other sources into their own

data warehouse for further analysis.

Companies

Figure 52: How do you integrate web analytics with other data sources?

Response: 183

Note: respondents could check multiple options

The agency results [Figure 53] suggest that fewer companies are performing manual collation of

output data. Only 39% of agencies report manual collation, compared to half of companies

surveyed. Significantly more agencies (some 59%) than companies report their clients are

performing semi-automated collation.

More than a third of agencies (36%) say their clients integrate data by exporting data from their

analytics tool, while the same proportion say clients are importing data into their web analytics.

Just under a fifth (19%) say clients integrate analytics data by collating data from all sources and

storing in a data warehouse.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 54

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Figure 53: How do your clients integrate web analytics with other data sources?

Response: 94

Note: respondents could check multiple options

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 55

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.5.6. Analysing customer journeys that cross online and offline

Tying up digital and offline data relating to individual customers is a major challenge for

businesses trying to become truly multichannel.

Only around a fifth of companies (22%) report their organisation has a framework for analysing

customer journeys that cross online and offline. Over half (55%) say this is not in place. Some

22% of respondents do not know if their organisation has this type of framework.

Some 28% of agencies [Figure 55] report their clients have a framework in place, while just under

half (46%) say their clients do not have framework for online and offline journey analysis.

Companies

Figure 54: Does your organisation have a framework for analysing customer

journeys that cross online and offline?

Response: 365

Agencies

Figure 55: Do your clients typically have a framework for analysing customer

journeys that cross online and offline?

Response: 247

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 56

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.5.7. Barriers preventing frameworks for analysing online and

offline data

In an open-ended question, companies were asked about the main barriers to having a consistent

framework for analysing online and offline data. The tag cloud below summarises the responses.

Time, lack of understanding, budget constraints and lack of resources are frequently cited as

significant barriers.

Powered by Wordle

The lack of resources was frequently cited by respondents. Many companies are unsure of how to

put an appropriate framework in place, and some companies do not see the value of doing this.

Lack of resources – time, budget and skills

“Lack of resources, lack of awareness of the potential value in doing this.”

“Lack of resources (not currently a main priority) - we have some systems in place but none which would

constitute a consistent framework.”

“We don't have enough resources in-house and suppliers don't offer that but mostly specialised in one or the

other [i.e. online and offline].”

“Not a high priority for the moment.”

Company and agency respondents

Some respondents also reported that the lack of quality data was preventing their organisation

from putting an appropriate framework in place.

Lack of quality data

“The different systems and data sources aren't connected so any tracking between online/offline is done

manually. We simply don't have the resources to do this on a large scale.”

“Tools and data sources, quality of data.”

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 57

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

“Offline data is incompatible with online. Television commercials TVRs and media stats are square pegs, online

analytics are round holes.”

Company and agency respondents

The lack of senior management buy-in is also holding back many companies, as they do not see

the value of having such a framework in place. This relates to a lack of understanding, as well as

company culture.

Senior management buy-in and company culture

“The business not understanding why or how this works. Senior Management don't have time to listen to how

the relationship between online and offline is so important and what we can gain from it.”

“Lack of understanding of importance/ relevance from senior management.”

“Company culture, lack of understanding, resistance to truly integrate all departments.”

“Organisational culture. However several things are coming together at present that should change this over the

next 12 months.”

“An antiquated business culture based upon the view that online only serves for low-end customer browsing

while in-store is high-end purchase (fashion industry).”

Company and agency respondents

A handful of respondents also referred to technology restraints, which prevent them from joining

up the data properly.

Technology

“Internal structures and processes; technology barriers.”

“Different agency partners responsible for different channels.”

“Technology limitations.”

Company and agency respondents

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 58

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Just under a quarter of companies (24%) perform some kind of attribution modelling, while over

half (56%) are not yet doing this. Figure 57 shows the agency responses.

Note: for more information on attribution, please refer to Econsultancy’s Marketing Attribution

Management Buyer’s Guide.

Companies

Figure 56: Do you (or a supplier on your behalf) do any kind of attribution

modelling to give more insight into the relationship between different channels?

Response: 362

Agencies

Figure 57: Do your clients do any kind of attribution modelling to give more

insight into the relationship between different channels?

Response: 247

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 59

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.6.1. Barriers preventing an effective online measurement strategy

The main barrier to an effective online measurement strategy is still the lack of budget and

resources, which is one of the three biggest problems for 48% of organisation surveyed. However,

it is encouraging that there has been a slight drop in the proportion of companies citing this, as

this has fallen from 57% last year.

Organisational silos or lack of co-ordination are reported to be a problem for 27% of companies

this year compared to 30% in 2010. Although this has fallen slightly, it is clear that companies still

need to do more to remove these silos.

A lack of strategy still holds back 27% of companies surveyed, and 23% do not know what to

measure. It is clear that there is still a need for further training and investment to bridge the skills

gap. More companies than last year report that finding staff is a problem; this had increased to

13%, up from 8% in 2010.

While fewer respondents in last year‟s report than in 2009 said that the poor technology was a

problem, there has been a reversal in the last year. The proportion of companies reporting

technology to be a top-three problem has increased by 10% since 2010, as some 16% now cite this

as a barrier, compared to just 6% in 2010.

Companies

Figure 58: What are the barriers that prevent you from having an effective online

measurement strategy?

2011 response: 349 2010 response: 210

Note: respondents could check up to three options.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 60

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

The supply-side responses indicate that the biggest problem for their clients relates to a lack of

understanding about what to measure. Over half of agencies (51%) reported this to be a problem

for their clients.

The next most significant barrier is thought to be a lack of budget and resources, according to

40% of agencies. Over a third of supply-side respondents (36%) said a lack of strategy is a major

barrier, slightly higher than the companies themselves suggest.

A third of agencies (33%) also note that the lack of senior management buy-in is preventing their

clients from having an effective online measurement strategy. Only 23% of companies reported

this to be an issue, and it may be that agencies are better placed to assess whether this is a

significant barrier to measurement.

Agencies

Figure 59: What are the barriers which prevent your clients from having an

effective online measurement strategy?

2011 response: 245 2010 response: 177

Note: respondents could check up to three options.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 61

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

6.6.2. Main frustrations involved in managing web analytics

Companies were asked about their main frustrations associated with managing analytics. From

this, it is apparent that a lack of understanding about the data, issues with senior management

buy-in and the lack of time and budget are all significant barriers to managing web analytics.

Powered by Wordle

Many respondents cited information over-load or lack of time to process and understand the

information. Some companies report an undue focus on simply the data itself, rather than the

interpretations and insights that analytics provides.

Too much data / lack of time

“It's so time consuming.”

“Too much data. Too much emphasis by senior management on reporting everything, while refusing to actually

align KPIs directly to business objectives. Senior managers don't really understand analytics but believe that

these tools are some kind of silver bullet. They don't put enough focus on the offline processes and joined up

thinking that is required to ensure analytical tools can give us useful, measurable actionable insights against our

goals.”

“There's so much data it's often difficult to decide where to focus and be confident in numbers that are simply

contradicted by other figures.”

“Too much data.”

“Volume of data and lack of synthesis. Issues with tagging, tracking and dependence on IT.”

Company and agency respondents

As well as too much data, some respondents also feel that they cannot trust the data, particularly

if the tools are using multiple analytics tools which all give different benchmarks and metrics.

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 62

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

“Confidence in data; not enough time to tag all events on a content heavy site.”

“Amount of data, data not matching between different data sources, digital competences in overall marketing.”

“Accuracy and customer data.”

“Complexity of multiple data sets and consolidation. Analysis of data benchmarking.”

“Conflicting data, especially when using more than one tool.”

Company and agency respondents

Problems related to a lack of understanding about analytics, and consequently, a lack of senior

management buy-in, were also frequently cited. To rectify this, there is an on-going need to better

educate senior-level executives about measurement, and to translate the value of analytics into

metrics that impact the bottom line. Setting up dedicated teams and hiring people with the right

mix of skills would also help to address the issue of senior management buy-in.

Lack of understanding and senior management buy-in.

“A more robust understanding of what to measure. Why do our sites exist? Very few people if any can agree or

even have the answer to that question. They approach analytics through what is the tool capable of measuring

which means there is less analysis and more reporting and therefore very little context to the numbers which

doesn't help anyone.”

“Lack of internal buy-in.”

“Need dedicated resource to have the time to educate senior teams and then get the investment.”

“Gaining senior buy in and coordinating between departments.”

“Not understanding what you are doing.”

“Not having a strategy in the first place.”

“The gap between what is possible and what we can really do today considering IT blockage, lack of real

understanding of the needs and lack of implementation within the strategy.”

Company and agency respondents

Some respondents also mention the lack of budget, which is an on-going problem. However, as

companies address the issue of senior management buy-in and are able to demonstrate the value

of measurement tools, naturally this will result in more budget being shifted towards web

analytics.

Lack of budget

“Lack of training and limits of current technology/budget.”

“Getting budget and understating within the business of its value.”

“Complexity of requirements conflict with budget available. Lack of follow-on budget to allow action to occur

after insight.”

Company and agency respondents

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 63

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

7.1. Respondent profiles The figure below indicates that 59% of respondents in this survey are client-side, and some 41%

work for an agency, vendor or consultant who offer web analytics or related services.

Figure 60: Which of the following most accurately describes your job role?

Response: 840

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 64

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage

Some 43% of respondents report they have an annual turnover of under £10 million, including a

fifth (20%) who have a turnover of under £1 million. At the other end of the scale, almost a third

of respondents (32%) report an annual turnover of over £150 million, while 15% have a turnover

or more than £1 billion.

Figure 61: What is your annual company turnover?

Response: 346

Online Measurement and Strategy Report 2011–in association with Lynchpin

Page 65

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage