31

Open Africa Power Business Development in Distribution Grids Marcelo Castillo Head of Business Development Global Infrastructure & Networks Enel Group July, 2021

Open Africa PowerBusiness Development in Distribution Grids

Marcelo Castillo

Head of Business Development

Global Infrastructure & Networks

Enel GroupJuly, 2021

Enel Group

470 TWh

Distributed

32Countries

74MEnd Users

18 Bn €

EBITDA

88GW

Installed Capacity

(56% RES)

45M

Smart Meters

2M km

lines

8Countries

8 Bn €

EBITDA

67kPeople

32kPeople

2

Enel

Group

Enel

GI&N

December 2020

ROMANIA

2.9 M customers

ITALY

31.4 M customers

SPAIN

12.3 M customers

BRAZIL

18.0 M customers

ARGENTINA

2.5 M customers

COLOMBIA

3.6 M customers

PERU

1.4 M customers

CHILE

2.0 M customers

GI&N International Experience

3

Platform-based business models Managing increasing levels of complexity

4

TSO

4. Sustainability

2. Value for

customers

3. Open

Innovation

1. Scale &

efficiency

Models to create value through GI&N platform

Direct investments in growing renewables,

networks and customers supporting

long term sustainable growth

Ownership business model Platforms as business enhancer

Provide key services, products or

know-how enabled by our platforms,

catalyzing investments of third parties

to maximize our and their value creation

Stewardship business model Platforms as business generator

Why a Platform?

Regulation knowledge

Innovation

Customer centricity

Pillars for a Sustainable DSO

Energy Access

Technologies

5

Resilience

Enabling electrification

6

Challenges for a Sustainable DSO

Network empowerment and expansion Driven by digitalization and technology

Enabling Decarbonization

Know–how, expertise, safety

Different regulatory models

Tariff reviews expertise

National/local institutions

GovernorsPrice Cap, Revenue Cap, Cost Plus

Negotiations: WACC, Totex, Losses/Quality/CollectionTargets, Digitalization, Reg. Assets recognitions

Customers

RES integrationElectric Vehicles, distributed generation

Affordability & inclusiveness

Stakeholders & local ecosystem

Traditional Grid Deployment and Microgrids solutions

Resilient

Passionate

Disruptive

BravePioneer

Dynamic

BD profile

Analytical

Argumentative

7

Patient

What does scouting mean?

Scouting at USA’s airport Scouting in Asia Scouting in Italy

8

Sustainable business (collection and losses)

Demand growth

Rewarding regulation (profit sharing)

Room for operative improvement

Digitalization

Scouting / screening criteria

1

2

3

4

5

9

List of target

countriesCountry report List of main

stakeholdersScouting pre-valuation

Projects Phases (1/2)Scouting and screening

▪ Reg. Analysis

▪ Turnaround potential

▪ Liabilities and risk analysis

▪ Site visits

▪ Upsides

▪ Competitors’ WACC

Ou

tpu

t

Countries Analysis

1 2 3 4

▪ Macroeconomics

▪ Country risk

▪ Development Indicators

▪ Competitiveness Index

▪ Regulation

▪ Private Players and/or

Privatization

▪ Privatization Stage

▪ Mkt players

▪ Government representatives

▪ Regulator

▪ Partners and competitors

190 countries on 1st analysis

Dx sector Analysis Stakeholders engagement Deep Dive

10+30 countries screened

GO / NO GO

>30 BnEUR offered

Projects Phases (2/2)Due Diligence and Execution

Ou

tpu

t

Project team set-up

5 6 7 8

Data Room management Assumption coordination Offer submission

▪ GBL involvement

▪ Regulatory & Technical

Consultants

▪ Project timeline

▪ VDR access

▪ Q&A process

▪ Documents integrity

▪ Coordination of BL/ Countries

▪ Reg. & Mkt projections

▪ Operative parameters

▪ Potential upsides

▪ Business Plan

▪ AFC financial valuation

▪ M&A committee

▪ Offer proposal

▪ Competitor’s expected bid

Project

organizationRed flags report Assumption Book Bid submission

NBO/BO11

~200 people

Example DD project:

>50k documents

>1,3k questions Q&APreparing the Assumption Book in

coordination of > 20 other areas

Company described

in the investment

proposal

Due Diligence

12

The importance of the Due Diligence

Experience in Regulatory Frameworks

America1,0 billion citizens

2X

National Benchmark / Conditioned pass through

>50% for Operator

30y / Permanent4y / 5y period

Yes

RAB x Reg. Rate Few years later / Ex-ant

Europe0,7 billion citizens

X

Actual cost Full pass through

50%

30 y4y / 6y period

Yes

RAB x Reg. Rate1 year later

Asia (India)1,4 billions citizens

25y3 y period

2X

3Y average Actual Cost

50%

Yes

RAB x Reg. Rate1 year later

Yes

Yes

Yes

Yes

Yes

Not yet

13

OPEX Remuneration

Investment remunerationTime to start remuneration

Regulated Rate

Profit sharing

Concession durationReg Period Length

Inflation adjustment

Commercial IncentivesQuality Incentives

Resilience Incentives No NoNo

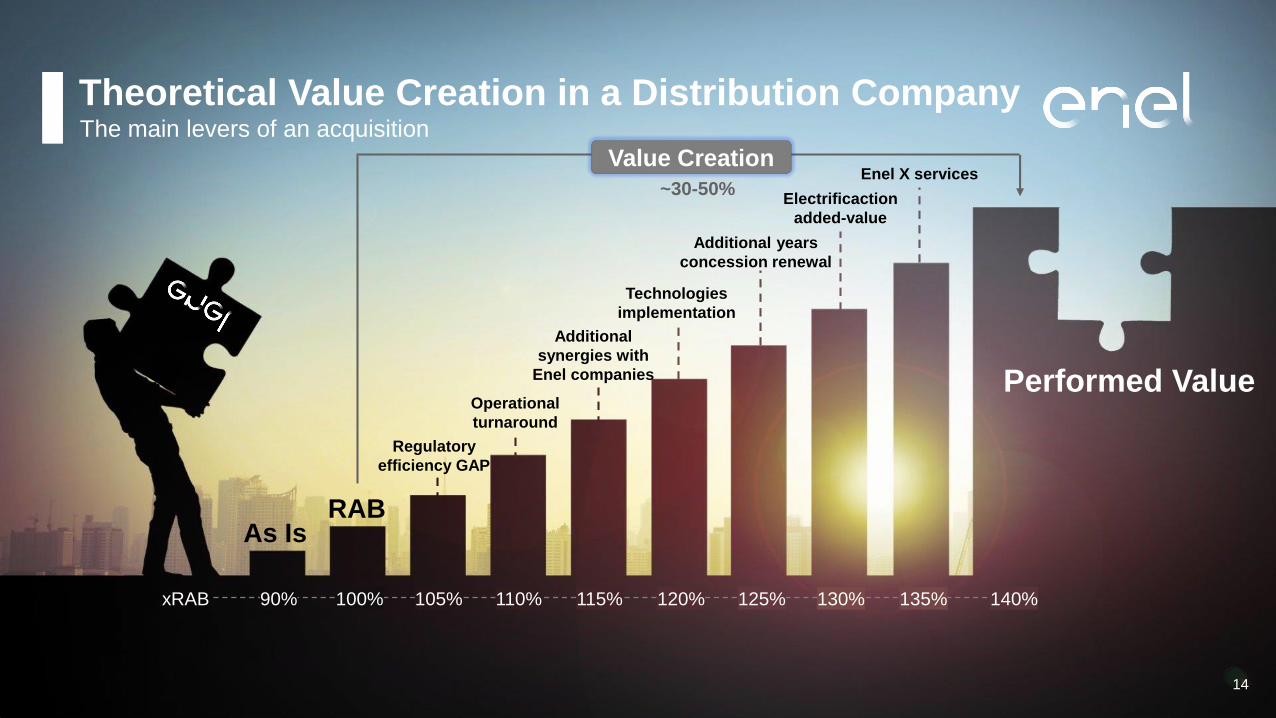

1

2

3

4

5

6

7

8

Regulatory

efficiency GAP

Theoretical Value Creation in a Distribution CompanyThe main levers of an acquisition

Operational

turnaround

Technologies

implementation

Enel X services

Additional years

concession renewal

As Is

14

Value Creation

RAB

Performed Value

Additional

synergies with

Enel companies

Electrificaction

added-value

~30-50%

90%xRAB 100% 105% 110% 115% 120% 125% 130% 135% 140%

Private investments socio-economic impactSustainable infrastructure investments

Infrastructure needs in Africa from 130-170bn$ a year with a financing gap up to ≈60%

▪ Creation of up to 20.000 new direct

jobs with 1bn$ investment in grids

(Based on private experiences, in Sub-

Saharan Africa)

Sources: McKinsey & Company, African Development Bank, others

▪ Energy transition acceleration

▪ Quality of life improvement

▪ Social education promotion

▪ Higher health/safety levels

Other benefitsJob creation impact

“Infrastructure has a socioeconomic rate of return around 20%: $1 of

investment can raise GDP by 20 cents in the long run”

15

Possible approach for success in developing countries

16

1. Public-private partnership

2. Subsidies divided between the utility, government and client

3. Ten years of stable rules

5. Involving the community from the beginning

4. Sustainable Funds with patient approach

Top 10 Megacities in 2035 – UN Data

Shanghai – CHI 34 M

Tokyo – JAP 36 M

Delhi – IND 43 M

Dhaka – BAN 31 M

Cairo –EGY28 M

Mumbai – IND 27 M

Kinshasa – CON 27M

Mexico city – MEX 25M

Beijing– CHI 25M

Private-owned

State-owned

San Paulo – BRA 24M

17

Sustainable models for colaboration

18

1

2

3

4

18

5

Fundación Pachacútec

19

Proyecto CSV – Carrera de Electricidad Industrial

Training young people who will work in the

future in the company or in our value chain,

mainly in the quality of service and safety

Description

Partner IES Privado Nuevo Pachacútec

BenefitedFrom 2006 to 2020, 310 students

successfully completed their studies.

92% job placement, including womenMain results

Quality education

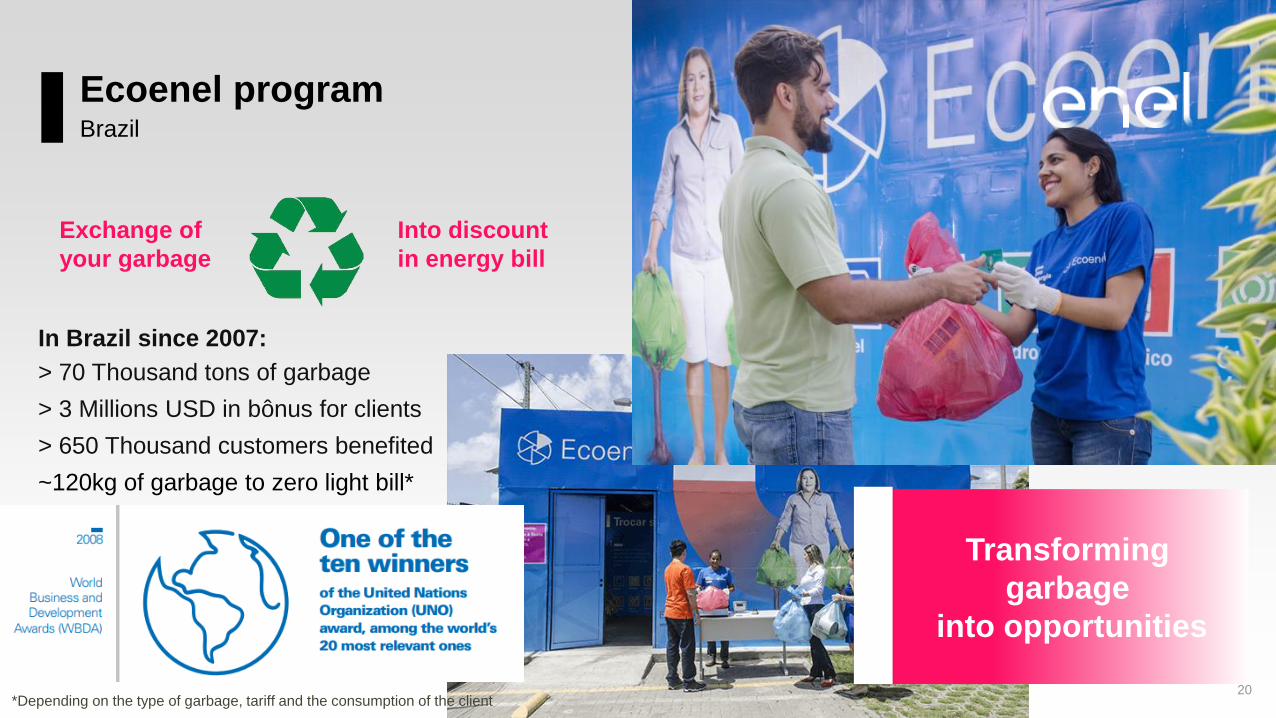

Ecoenel program

20

Brazil

In Brazil since 2007:

> 70 Thousand tons of garbage

> 3 Millions USD in bônus for clients

> 650 Thousand customers benefited

~120kg of garbage to zero light bill*

Transforming

garbage

into opportunities

Exchange of

your garbage

Into discount

in energy bill

*Depending on the type of garbage, tariff and the consumption of the client

“Luz para Todos” programBrazil

Public measures to bring electrification to remote

areas, with tariffs subsidized by the governments

and distributors

>15 Million people beneficiated in the country

21

“Tarifa Social”

22

Brazil

Public measure in which low-income

clients can have discounts in their light bill

The lower the consumption, the

greater the proportional discount

EXTERNAL WALLSUBESTATION COMPARTIR COLOMBIA

Substation Compartir Colombia

SOLID WASTE INTO FURNITURES 23

SOCIO-ECONOMIC CONTEXT

✓ The south of Bogotá and the municipality of Soacha

had a fast population growth: from 40k to 500k in

last 30yrs (DANE)

✓ High migration to the municipality as a result of the

armed conflict, displacement, search for

opportunities, residence at a lower cost and close

to the capital of the Country.

SUSTAINABILITY PLAN

1 Reforesting Soacha and Street art valorization

JAC* strengthening2

More than 700 plants planted and decoration of substation Compartir with local art

14 training sessions on politics, organizational management, project formulation

3 Photovoltaic System Lighting

Solid waste management4More than 2,500 kg of wood transformed into 743 pieces of furniture

8 poles and led lights (Danube) + 10 led lights and 38 lights switch (Tejares)

*JAC = Juntas de Accion Comunal (non-profit organizations made up of residents)

More energy for the economic development of the Region

24

Copacabana - Rio

24

25

Rio de Janeiro - Brazil

What does the cat in

the picture mean?

Spaghetti?

15,7%14,6%

12,6%

10,7%9,8%

8,0%

9,0%

10,0%

11,0%

12,0%

13,0%

14,0%

15,0%

16,0%

17,0%

Privatization y1 y2 y3 y4

Lima

20,4%18,8%

16,1%

13,6% 13,3%

19,5%

13,5%

10,5%11,4%

10,3%8,0%

10,0%

12,0%

14,0%

16,0%

18,0%

20,0%

22,0%

Privatization y1 y2 y3 y4

Santiago Bogotá

25,6%24,0%

23,0%22,0%

20,0%

26,0%

22,1%

16,2%

12,0% 11,2%9,0%

11,0%

13,0%

15,0%

17,0%

19,0%

21,0%

23,0%

25,0%

27,0%

Privatization y1 y2 y3 y4

Rio de Janeiro Buenos Aires

Losses Track Record Enel after privatization in Latam

1 2

1987

1998

1995

1996

3

1995

Energy Losses reduction in 4Y

Dx M clients Reduction

Buenos Aires (ARG) 2,5 -57%

Bogotá (COL) 3,5 -47%

Lima (PER) 1,4 -38%

Santiago (CHI) 2,0 -35%

Rio de Janeiro (BRA) 2,9 -22%

▪ Inspections

▪ Normalization

▪ Armouring

Main Actions

Today22,1% 18,9%

Today 8,8%

Today5,2% 7,6%

26

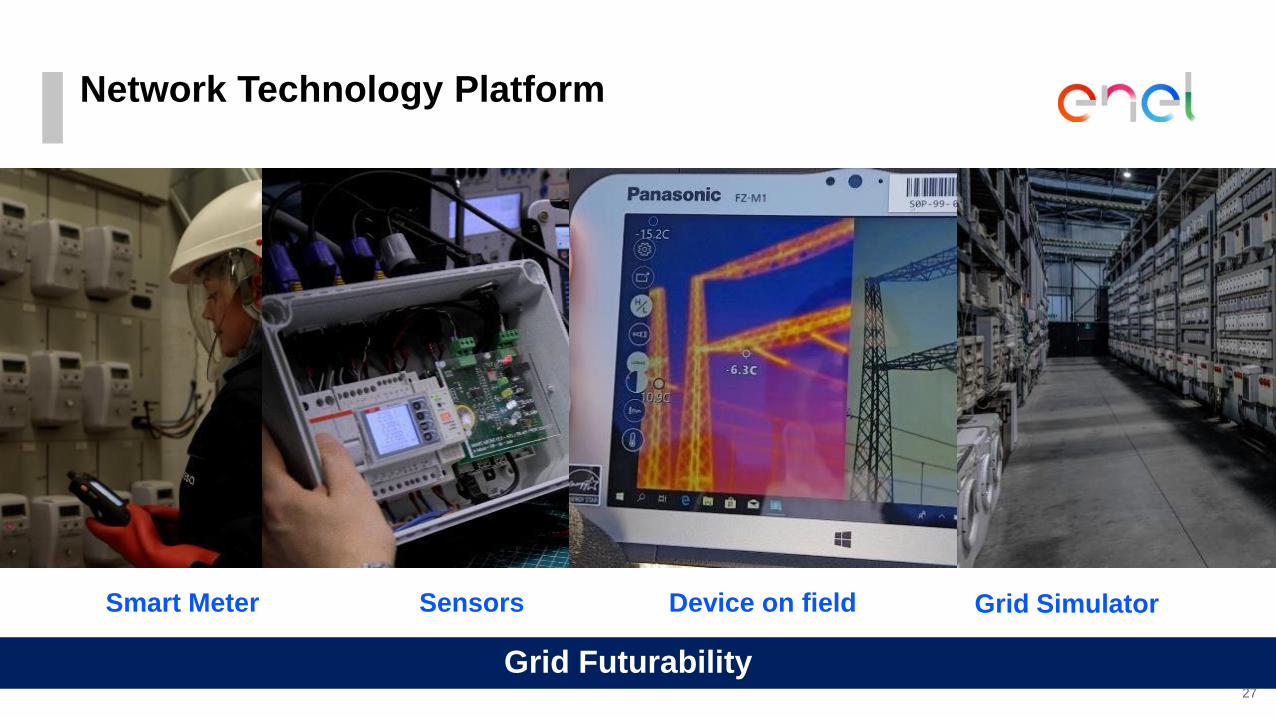

Smart Meter Sensors Grid Simulator

Network Technology Platform

Device on field

27

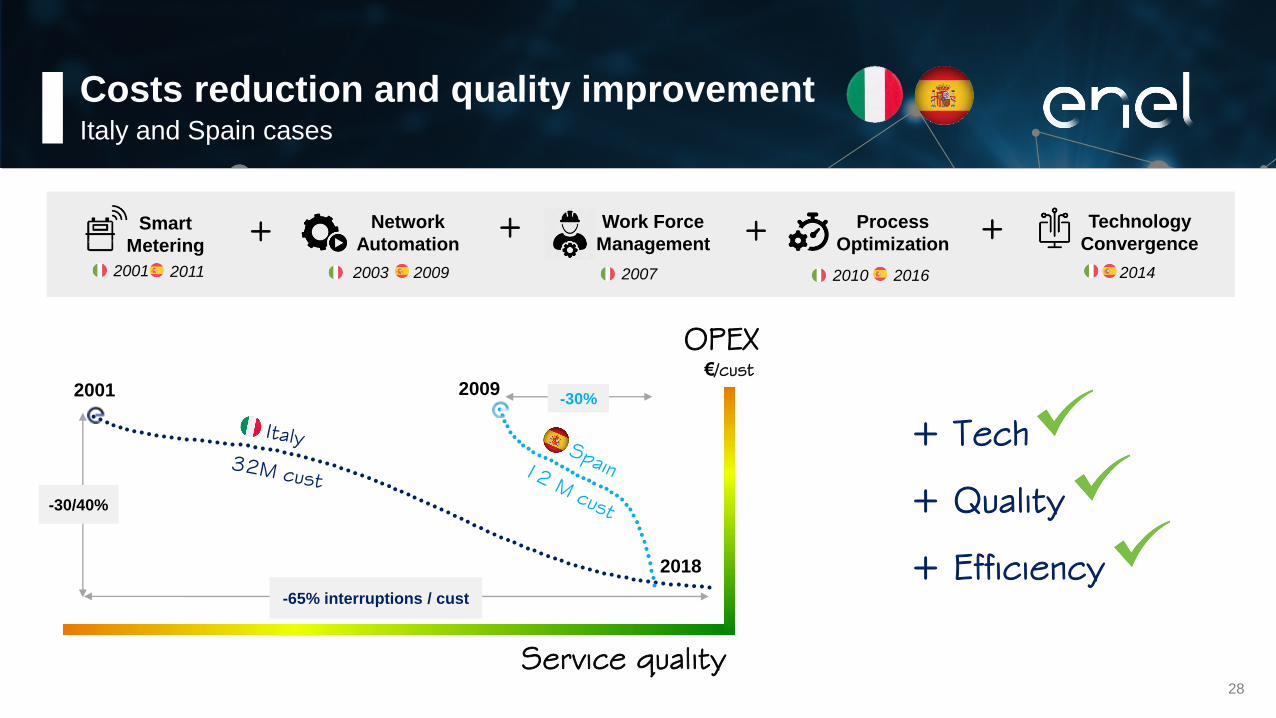

Grid Futurability

2001 2011

Network

Automation

2003 2009

Work Force

Management

2007

Process

Optimization

20162010

Technology

Convergence

2014

40

45

50

55

60

65

70

75

80

35455565758595105115125135

2001 2009

2018

OPEX

€/cust

Service quality

Smart

Metering

+ Tech

+ Quality

+ Efficiency

Costs reduction and quality improvementItaly and Spain cases

28

-30/40%

-65% interruptions / cust

-30%

+ +++

São Paulo and Goiás Opex optimizationTotal 10 M of customers related to recent Dx acquisitions

-60% Goias

-60% interruptions / cust

OPEX

€/cust

Service quality

-50% SP

-45% interruptions / cust

29*2024 Expected

2016

2020

2024 2024

2017

2018

Main actions

▪ Increasing CAPEX

By 2x - 3x the companies’ historic

▪ Processes optimization

▪ Fighting losses

▪ Opex Recognition negotiation

▪ A Good and Fair Asset Base

negotiation with regulator

▪ Increasing Digitalization

▪ Network resilience

São Paulo – urban area with ≈1.600 cust./Km2

Goiás – rural area with ≈9 cust./Km2

GI&N Stewardship for dummiesStewardship and Sustainability

Accelerate the

energy transition

Minimize

level of risk

Disseminate Enel’s

sustainable model

30

Reach new

countries

Stewardship

Offer Enel

Global expertise

Surpass Regulatory

restrictions

Leverage in our Platform

business models

31

THANK YOU