OPERATIONAL PERFORMANCE ANALYSIS OF SELECTED PUBLIC SECTOR BANKS - A STUDY Dr B Parashuramulu 1 Dr D Harikanth 2 Abstract The operational performance in commercial banks can be evaluated by using a measure, i.e., operating profit, spread, burden, net profit, and average and growth rate is taken for the present study. The information on operational performance is useful to the management for planning, decision making and control. This will enable the management to exercise control over the day to day operations with a view to ensuring maximum efficiency and adherence to the plans of management. Operating profit is the excess of operating income over operating cost. This paper an attempts to analyze the operational performance analysis of selected public sector banks a study during the period from 2008-09 to 2017-2018. The study is diagnostic and exploratory in nature and makes use of secondary data. The study finds and concludes that the operating profit, Total income, Interest income and other income of State Bank of India is improved when compare to Punjab National Bank. It can be concluded that both the banks are more depend on interest income. Hence, banks are need put efforts more to increase other income like commission, Exchange services, etc. Keywords: Operating Expenses, Operating Profit, Total Income, Spread and Burden. Introduction The Indian banking system is most popular and secular due to its structure and functions. The banking system consist a major portion in Indian financial system. Financial crisis, devaluation of money etc does not affect our banking system so badly as compared to other countries. It is also a reason for increase the operation of foreign banks in India. India is considered as best platform for banking operation. In present situation there are many commercial banks, co operative banks, rural banks operating in India. The general health of a bank is determined by health of its earnings. Earnings are considered the most sensitive of all financial indicators to change in a firm's financial health. Banks are generally considered different from general profit making enterprises.The operational performance in commercial banks can be evaluated by using a measure, i.e., 1 Assistant Professor, Department of Commerce, Satavahana University, Karimnagar, India 2 Head, Department of Commerce, Satavahana University, Karimnagar, India www.zenonpub.com Jan - Mar 2018 ISSN 2455-7331 - Vol III – Issue I International Journal of Research in Applied Management, Science & Technology

Transcript

OPERATIONAL PERFORMANCE

ANALYSIS OF SELECTED PUBLIC

SECTOR BANKS - A STUDY Dr B Parashuramulu1

Dr D Harikanth2 Abstract

The operational performance in commercial banks can be evaluated by using a

measure, i.e., operating profit, spread, burden, net profit, and average and growth rate is taken

for the present study. The information on operational performance is useful to the

management for planning, decision making and control. This will enable the management to

exercise control over the day to day operations with a view to ensuring maximum efficiency

and adherence to the plans of management. Operating profit is the excess of operating income

over operating cost. This paper an attempts to analyze the operational performance analysis

of selected public sector banks a study during the period from 2008-09 to 2017-2018. The

study is diagnostic and exploratory in nature and makes use of secondary data.

The study finds and concludes that the operating profit, Total income, Interest income

and other income of State Bank of India is improved when compare to Punjab National Bank.

It can be concluded that both the banks are more depend on interest income. Hence, banks are

need put efforts more to increase other income like commission, Exchange services, etc.

Keywords: Operating Expenses, Operating Profit, Total Income, Spread and Burden.

Introduction

The Indian banking system is most popular and secular due to its structure and

functions. The banking system consist a major portion in Indian financial system. Financial

crisis, devaluation of money etc does not affect our banking system so badly as compared to

other countries. It is also a reason for increase the operation of foreign banks in India. India is

considered as best platform for banking operation. In present situation there are many

commercial banks, co operative banks, rural banks operating in India.

The general health of a bank is determined by health of its earnings. Earnings are

considered the most sensitive of all financial indicators to change in a firm's financial health.

Banks are generally considered different from general profit making enterprises.The

operational performance in commercial banks can be evaluated by using a measure, i.e.,

1 Assistant Professor, Department of Commerce, Satavahana University, Karimnagar, India 2 Head, Department of Commerce, Satavahana University, Karimnagar, India

www.zenonpub.com Jan - Mar 2018 ISSN 2455-7331 - Vol III – Issue I

International Journal of Research in Applied Management, Science & Technology

operating profit. To study the efficiency of the banks, Financial Statements - Balance Sheet

and Profit and Loss Account –are the basis. The financial statements are indicators of two

important factors of the bank which are profitability and financial soundness. The operational

performance of banking sector has long been at the center of academic research and has

received a substantial amount of attention. The evaluation of operational performance has

always been a major concern in banking sector. It also focused on operational efficiency in

terms of cost analysis.

Review of Literature

As the present study is concerned with the “Operational Performance Analysisof

SelectedPublic Sector Banks– A Study”, an attempt is made to review in brief the earlier

studies relating to banking activities so as to gain greater insight into the subject. Some of the

relevant studies which are concerned with the Performance of Public Sector Banks - A Study

of Select banks are presented briefly.

GurpreetKaur (2015)1written an article entitled “Performance Analysis: A Study Of

Public Sector &Private Sector Banks In India”, The main objective of this article is to make

an evaluation of the financial performance of Indian Banks .The financial performance of a

bank is measured by a number of key indicators with reference to Deposits, Advances, Total

Income, Investment and Net Profit etc. Recommendations and suggestions have been given

for improving the performance of Banks in India.

CA. Ruchi Gupta (2014)2, written an article entitled “An Analysis of Indian Public

Sector Banks Using Camel Approach”, In this paper an attempt is made to discuss the

progression of an economy is significantly dependent upon deployment as well as optimum

utilization of resources and most importantly operational efficiency of the various sectors, of

which banking sector plays a very vital role. Banking sector helps in stimulation of capital

formation, innovation and monetization in addition to facilitation of monetary policy. It is

imperative to carefully evaluate and analyses the performance of banks to ensure a healthy

financial system and an efficient economy.

Shobhana (2010)3examined “Operational Efficiency of Public Sector Banks in

India”. The study revealed that out of 27 public sector banks in India, only 9 banks have

1GurpreetKaur, “Performance Analysis: A Study Of Public Sector &Private Sector Banks In India”,

ISSN No 2349-3402 Vol 2 (1) 2015

2CA. Ruchi Gupta “An Analysis of Indian Public Sector Banks Using Camel Approach” ISOR Journal of Business Management, e –ISSN: 2278-487X, p-ISSN: 2319-7668,Volume 16, Issue 1,pp 94- 102.

3. V. K. Shobhana, “Operational Efficiency of Public Sector Banks in India – A Non – Parametric Model”, Journal of Accounting and Finance, 24 (2), April-Sep 2010, p. 85-96

www.zenonpub.com Jan - Mar 2018 ISSN 2455-7331 - Vol III – Issue I

International Journal of Research in Applied Management, Science & Technology

achieved high level of efficiency in its operations with the oriental bank of commerce at the

top. It is found that factors such as size of assets, network of branches and staff strength do

not have significant influence over operational efficiency of banks

Objectives of the Study

To evaluate the operating expenses and operating profit of selected banks

To analyze the spread and burden of selected banks

Data Collection and Methodology

The study is based on secondary data collected mainly from annual reports of Punjab

National Bank and State Bank of India. The data has been suitably arranged, classified,

analysed and tabulated according to the requirements of the study. For analyzing the data

using with MS – Excel the techniques like trends, ratios, compound annual growth rate, and

averages have been used.

Period of the Study

The relevant data of the selected banks for the purpose of the study was collected for a

period of ten years from 2008-09 to 2017-18.

Scope of the Study

The present study is confined to the operational performance of selected banks only. The

study covered important operational aspects of selected banks in relation to funds, expenses,

income and profit of selected banks.

Limitation of the Study

The study used the secondary data for analysis and interpretation which is collected

from the published annual reports of the banks. Therefore, the accuracy of the data depends

on the accuracy ensured in the data presented in the annual reports.

Components of Operational Expenses

The expenses in banking operations are varying from item to item. Most of the

operating expenses in the commercial banks are fixed in nature. To know the importance of

expenditure items, an attempt has been made to examine the various components in the

operating expenses of selected banks. Broadly, the components of operating expenses in

commercial banks include compensation to employees, administration expenses, management

expenses, business promotion expenses and depreciation on assets. Compensation to

employees is composed of salaries and allowances paid to employees and also other

expenditure related to employees. The administration expenses include rent, taxes on

buildings, postage and telegrams, repairs and maintenance, printing and stationary, insurance

and other expenses. Management expenses consist of director’s fees and allowances,

www.zenonpub.com Jan - Mar 2018 ISSN 2455-7331 - Vol III – Issue I

International Journal of Research in Applied Management, Science & Technology

auditor’s fees and expenses, and legal charges. Business promotion expenses comprised of

advertisement about the banking operations, and then the depreciation on the assets consists

of the expired cost of bank’s furniture and other fixed assets of the bank.

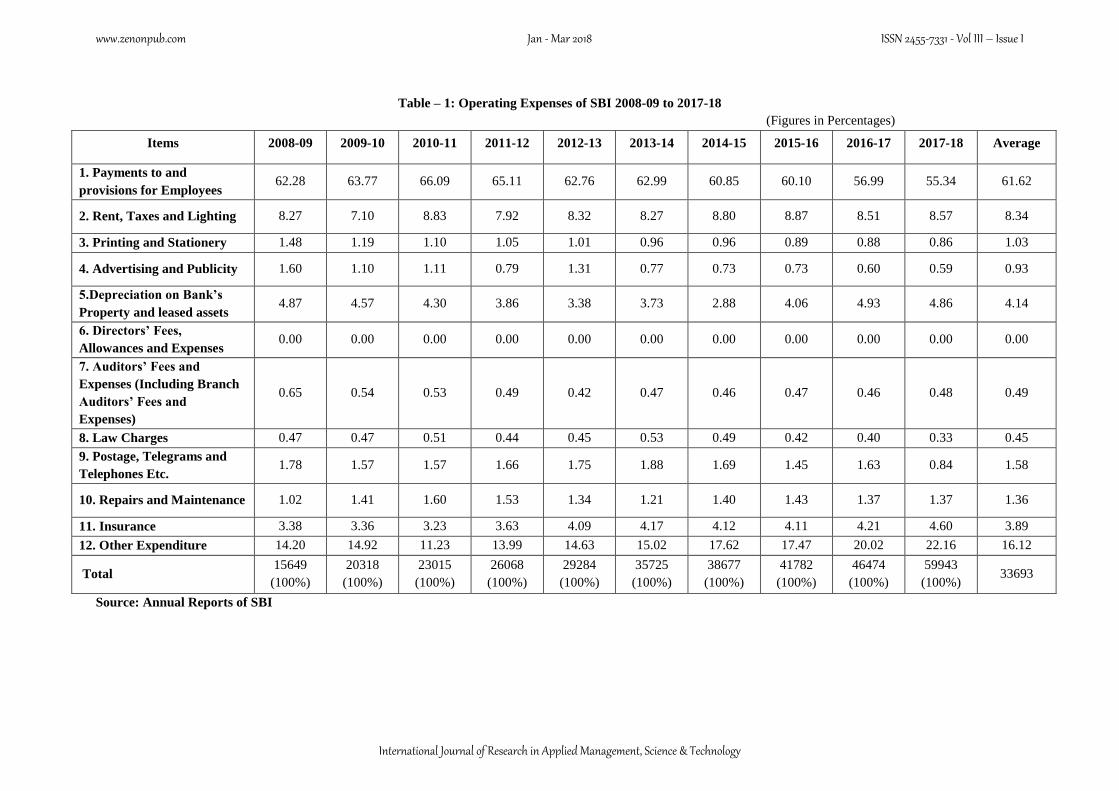

Components of Operating Expenses of State Bank of India

It can be observed from the Table – 1 that the major component of operating

expenses is compensation to employees. Its percentage ranged from 62.28 to 55.34 during the

study period and the average percentage is 61.62. This shows out of the total operating

expenses of the bank, more than 60% are relating to employees’ cost. It is observed that total

operating expenses of the bank has been raised from Rs. 15649 crores in 2008-09 to Rs.

59943 crores in 2017 -18 and the rate of increase noticed is 3.81 times. During the same

period the percentage of administrative expenses raised from 30.13 in 2008-09 to 38.40 in

2017-18 and the average percentage is 32.25. The analysis of operating expenses reveals that

the employees’ cost and administration expenses are constituted a 93.75% of the operating

expenses of the bank. The management expenses, business promotion expenses and

depreciation on assets of the bank during the study period, on an average, are 6.25% of the

operating expenses.

Components of Operating Expenses of Punjab National Bank

The details of component wise operating expenses of Punjab National Banks shown in

Table – 2 reveals that almost all the components of the operational expenses have more or

less the same proportion in the operating expenses during the study period. It is observed that

total operating expenses of Punjab National Bank has been raised from Rs. 4206 crores in

2008-09 to Rs. 13509 crores in 2017-18 and the rate of increase noticed is 3.21 times. It can

also be observed from table that the major component of operating expenses is compensation

to employees. Its percentage ranged from 57.79 to 70.09 during the study period and the

average percentage is 67.18. This shows out of the total operating expenses of the bank more

than 67% are relating to employees cost. During the same period the percentage of

administrative expenses increased from 23.95 in 2008-09 to 26.35 in 2017-18 and the average

percentage are 26.92. The management expenses, business promotion expenses and

depreciation on assets of the bank during the study period, on an average, are 6.89% of the

operating expenses. The analysis of operating expenses reveals that the employees’ cost and

administration expenses are constituted 93.11% of the operating expenses of the bank.

Out of the total operating expenses of both the banks are more than 60 percent

relating to employee cost. Banks are concentrated to reduce the employees cost,

administrative and other expenses and improve the technological development.

www.zenonpub.com Jan - Mar 2018 ISSN 2455-7331 - Vol III – Issue I

International Journal of Research in Applied Management, Science & Technology

Table – 1: Operating Expenses of SBI 2008-09 to 2017-18