MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

MENA Summit 2013:

Enabling innovation, driving profitability

6 November 2013

EVENT PARTNERS:

Operator strategies to address the

OTT threat

Stephen Sale

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat 2

Changing business models in communication services

Operator responses to the OTT threat

Outlook for the MENA region

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

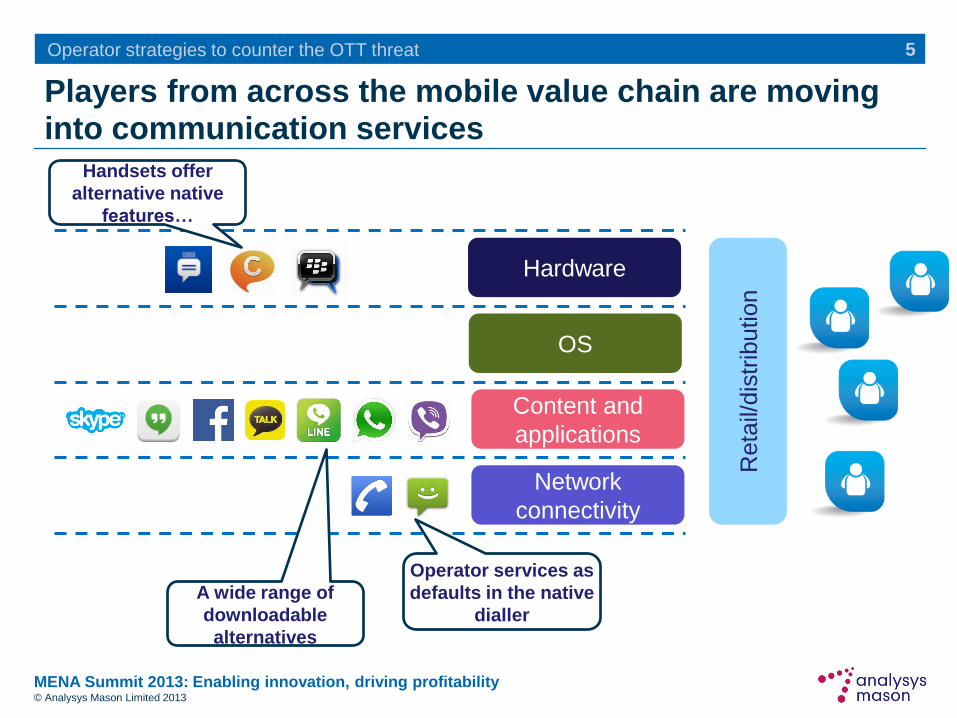

Players from across the mobile value chain are moving into communication services

3

Network

connectivity

Content and

applications

OS

Hardware

Reta

il/dis

trib

ution

Operator services as

defaults in the native

dialler

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Players from across the mobile value chain are moving into communication services

4

Network

connectivity

Content and

applications

OS

Hardware

Reta

il/dis

trib

ution

Operator services as

defaults in the native

dialler

A wide range of

downloadable

alternatives

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Players from across the mobile value chain are moving into communication services

5

Network

connectivity

Content and

applications

OS

Hardware

Reta

il/dis

trib

ution

Operator services as

defaults in the native

dialler

Handsets offer

alternative native

features…

A wide range of

downloadable

alternatives

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Players from across the mobile value chain are moving into communication services

6

Network

connectivity

Content and

applications

OS

Hardware

Reta

il/dis

trib

ution

Operator services as

defaults in the native

dialler

Handsets offer

alternative native

features…

A wide range of

downloadable

alternatives

…increasingly

presented as default

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Players from across the mobile value chain are moving into communication services

7

Network

connectivity

Content and

applications

OS

Hardware

Reta

il/dis

trib

ution

Operator services as

defaults in the native

dialler

Handsets offer

alternative native

features…

A wide range of

downloadable

alternatives

Tighter integration

forthcoming?

…increasingly

presented as default

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Case study: Facebook

8

Facebook Messenger and Home screenshots

• SMS handling in Android

• „Chat heads‟ avatars in other apps

• VoIP (in some countries)

Features

• 874 million mobile MAUs (no

Messenger figures available)

Installed base

• Standalone messaging app launched in 2011

• Improving access by dropping Facebook login

and partnering with operators

• Extending with Facebook Home

Overview

• Messenger: 4.5* (Android), 4* (iOS); Home:

2.5* (Android)

Rating

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Case study: Google

9

Google Hangouts and KitKat screenshots

• Group chat features; emoticons

• Location and picture sharing

• SMS and MMS integration with Hangouts

Features

• 540 million MAUs for Google+

(300 million „in-stream‟)

Installed base

• Google Hangouts now focus for

disparate comms initiatives, including

Google Voice; expanding numbering

• Integrated more closely with Android

4.4; Hangouts replaces „Messages‟ icon

Overview

• 3.5* (Android), 2* (iOS)

Rating

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

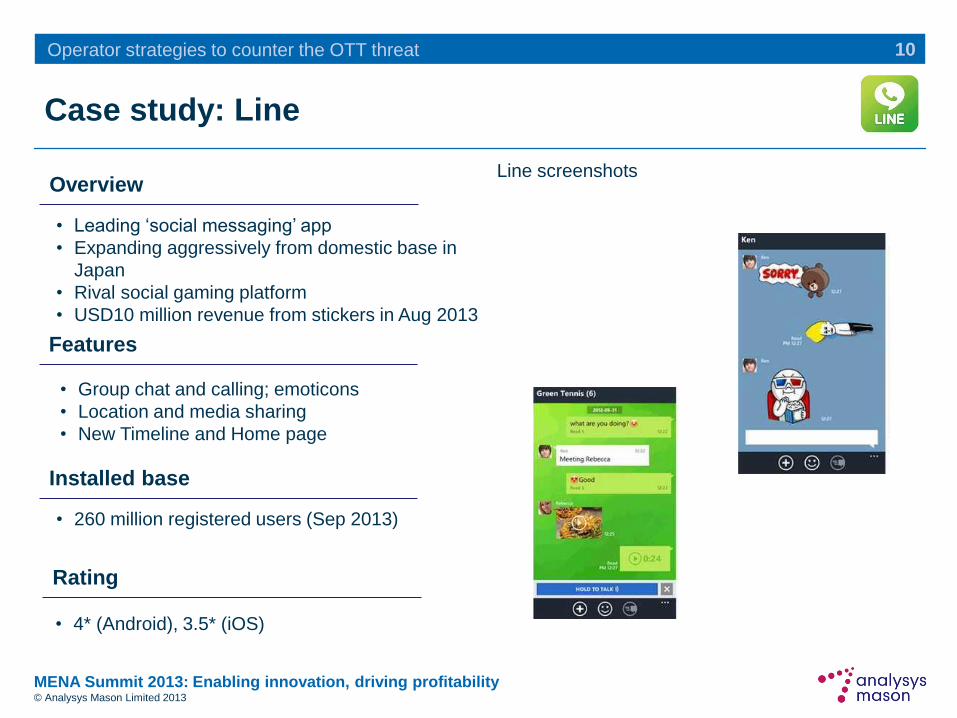

Case study: Line

10

Line screenshots

• Group chat and calling; emoticons

• Location and media sharing

• New Timeline and Home page

Features

• 260 million registered users (Sep 2013)

Installed base

• Leading „social messaging‟ app

• Expanding aggressively from domestic base in

Japan

• Rival social gaming platform

• USD10 million revenue from stickers in Aug 2013

Overview

• 4* (Android), 3.5* (iOS)

Rating

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Case study: WhatsApp

11

WhatsApp Messenger screenshot

• Group chat features

• Media sharing

• Audio messaging

Features

• 350 million MAUs (Sep 13)

Installed base

• First cross-platform app to easily integrate

address book

• 27 billion messages per day

• No ads: first year free, then USD0.99

Overview

• 4.5* (Android), 4* (iOS)

Rating

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

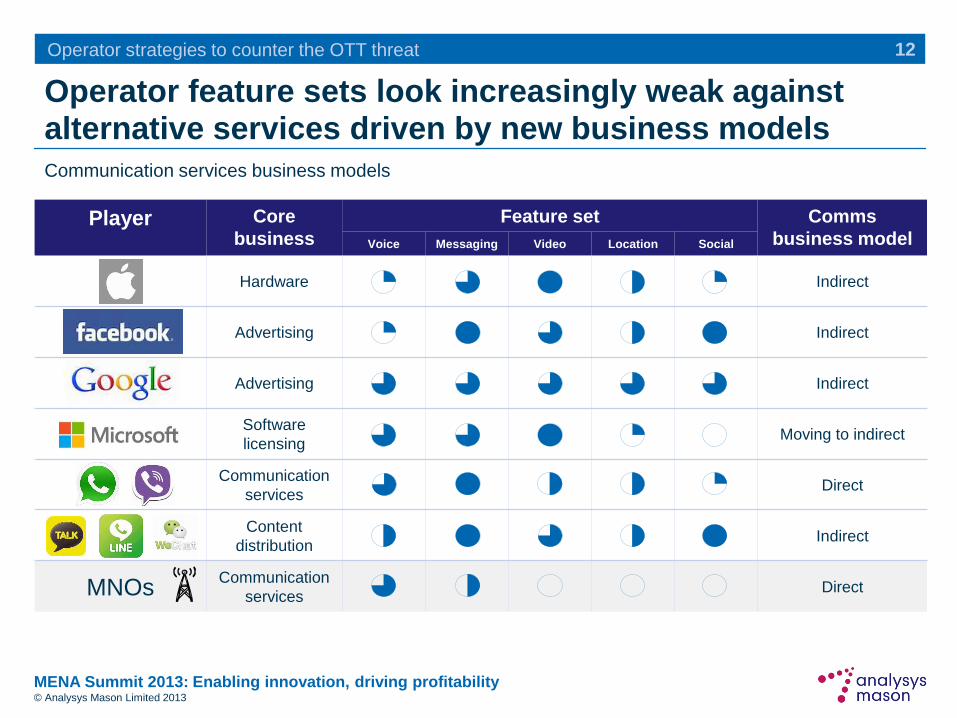

Operator strategies to counter the OTT threat 12

Player Core

business

Feature set Comms

business model Voice Messaging Video Location Social

Hardware Indirect

Advertising Indirect

Advertising Indirect

Software

licensing Moving to indirect

Communication

services Direct

Content

distribution Indirect

MNOs Communication

services Direct

Operator feature sets look increasingly weak against alternative services driven by new business models

Communication services business models

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat 13

Player Core

business

Feature set Comms

business model Voice Messaging Video Location Social

Hardware Indirect

Advertising Indirect

Advertising Indirect

Software

licensing Moving to indirect

Communication

services Direct

Content

distribution Indirect

MNOs Communication

services Direct

Operator feature sets look increasingly weak against alternative services driven by new business models

Communication services business models

Value of communication services increasingly co-opted

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat 14

Player Core

business

Feature set Comms

business model Voice Messaging Video Location Social

Hardware Indirect

Advertising Indirect

Advertising Indirect

Software

licensing Moving to indirect

Communication

services Direct

Content

distribution Indirect

MNOs Communication

services Direct

Operator feature sets look increasingly weak against alternative services driven by new business models

Communication services business models

Increasing overlap between communication services and social networking

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

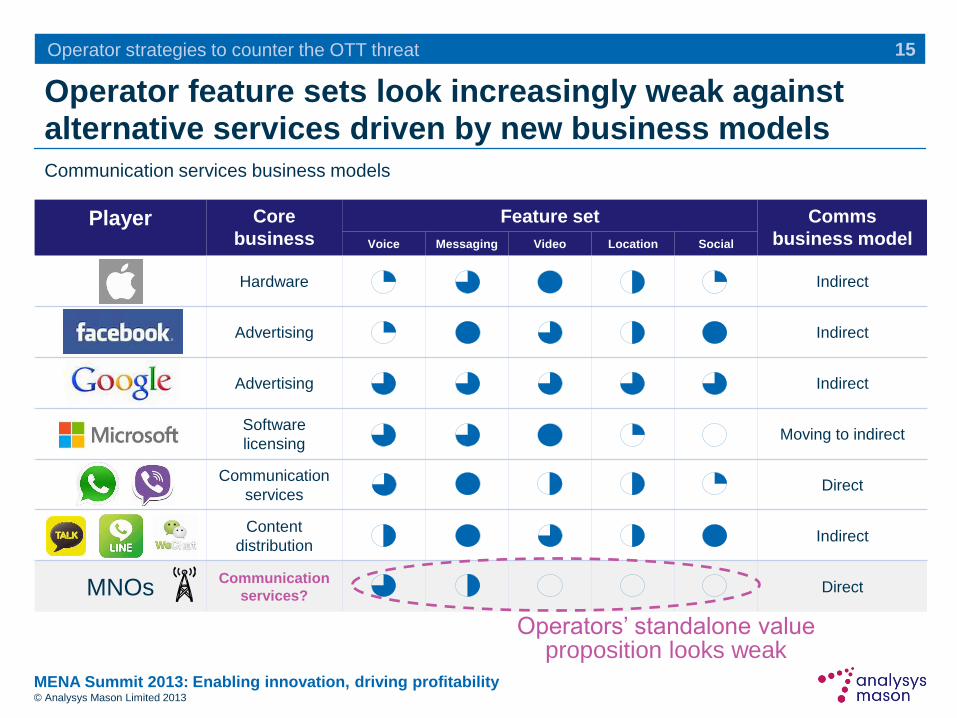

Operator strategies to counter the OTT threat 15

Player Core

business

Feature set Comms

business model Voice Messaging Video Location Social

Hardware Indirect

Advertising Indirect

Advertising Indirect

Software

licensing Moving to indirect

Communication

services Direct

Content

distribution Indirect

MNOs Communication

services? Direct

Operator feature sets look increasingly weak against alternative services driven by new business models

Communication services business models

Operators‟ standalone value proposition looks weak

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat 16

Changing business models in communication services

Operator responses to the OTT threat

Outlook for the MENA region

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Operator responses

17

Block OTT services

Stimulate usage

Partner with OTT

Offer RCS

Offer ‘telco OTT’

Strategy Objective Examples

• Prevent OTT becoming mainstream

• Gain value from high-end bundles

• Defend legacy communication

services

• Buy time

• Attract young smartphone users

• Support core data business with

move to bundles

• Improve operator messaging

• „Retain relevance‟ as a

communications provider

• Differentiate own services

• „Retain relevance‟ as a

communications provider

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

0%

10%

20%

30%

40%

50%

60%

70%

80%

Avera

ge

Fra

nce

Ge

rma

ny

Pola

nd

Sp

ain

UK

US

A

Pe

netr

ation

Voice Messaging

Tariff rebalancing can serve to stimulate usage of legacy services

18

Tariff rebalancing is already underway

Voice and messaging are becoming

cheaper

Many markets are moving towards

unlimited plans

Examples:

SingTel migrated customers from

unlimited data plans (with small

voice and messaging allowances) to

a tiered portfolio (with large

allowances).

In France: “everyone has SMS

unlimited for free … We don‟t see a

big strength of WhatsApp…”

Figure: Penetration of unlimited bundles in

selected countries

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Globe Telecom is pursuing an aggressive partnership strategy

19

Many operators already have productive

partnerships with OTT players –

Facebook, for example.

In the Philippines, Globe Telecom

launched a partnership with Viber in July

2013 to prepaid customers (98% of base).

GoUnli25 includes free Viber usage.

Viber10 (for USD0.23) and Viber20

plans for unlimited messaging and HD

voice.

Extended to Facebook Messenger,

KakaoTalk, Line, WeChat and WhatsApp

in August (GoUnli30).

Other examples include Airtel, 3 and

Reliance.

Promotional image for Globe‟s GoUnli30 service

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

RCS is the collective industry response

20

RCS services have now been launched by

17 operators in 11 countries:

Notably France, Germany, South Korea,

Spain and USA (boosted by América

Móvil).

Available as a downloadable app and

native on 23 ranged devices.

The main features are:

IM and group chat (with SMS integration)

file-sharing/video-streaming.

Data usage is typically zero-rated on

specific tariff plans.

Service has yet to be marketed strongly,

even in early launch markets.

Rhetoric shifting towards hybrid clients, and

RCS as an enabler.

Screenshot of joyn

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Telefónica is offering a telco OTT toolset to its opcos

21

TU Go is a communications app from

Telefónica Digital that:

focuses on voice over Wi-Fi,

adding network selection and

virtualisation of service across

devices.

The first launch was with Telefónica

UK (O2) in March 2013. Initially it is

only available to contract customers;

prepaid to follow.

Usage of TU Go services is drawn

down from customers‟ bundles of

minutes and messages.

Screenshot of O2 UK‟s TU Go service

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

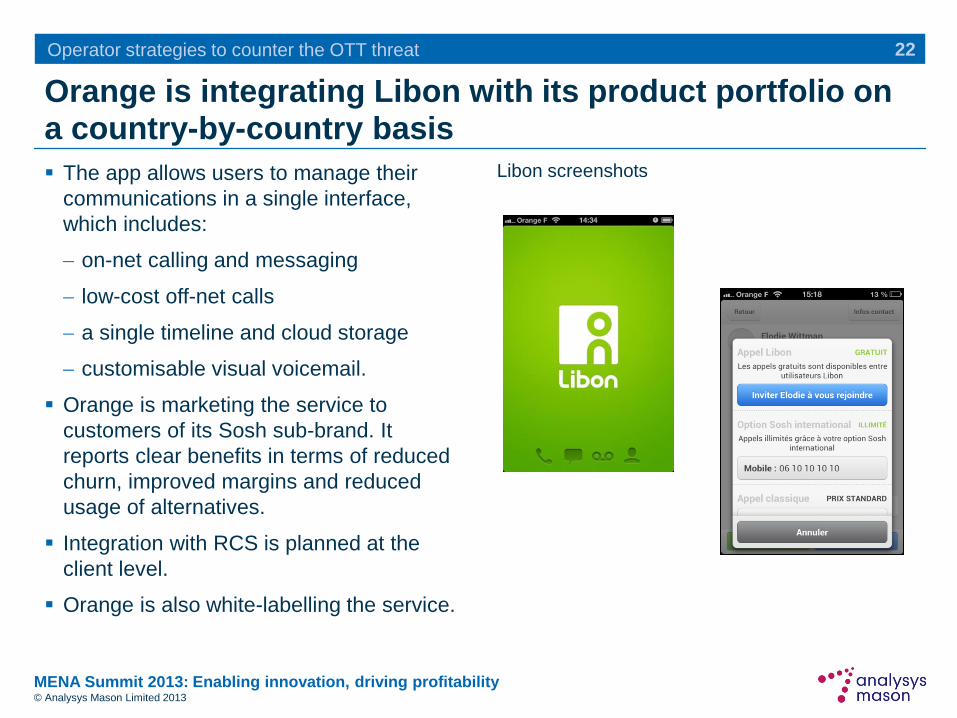

Orange is integrating Libon with its product portfolio on a country-by-country basis

22

The app allows users to manage their

communications in a single interface,

which includes:

on-net calling and messaging

low-cost off-net calls

a single timeline and cloud storage

customisable visual voicemail.

Orange is marketing the service to

customers of its Sosh sub-brand. It

reports clear benefits in terms of reduced

churn, improved margins and reduced

usage of alternatives.

Integration with RCS is planned at the

client level.

Orange is also white-labelling the service.

Libon screenshots

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

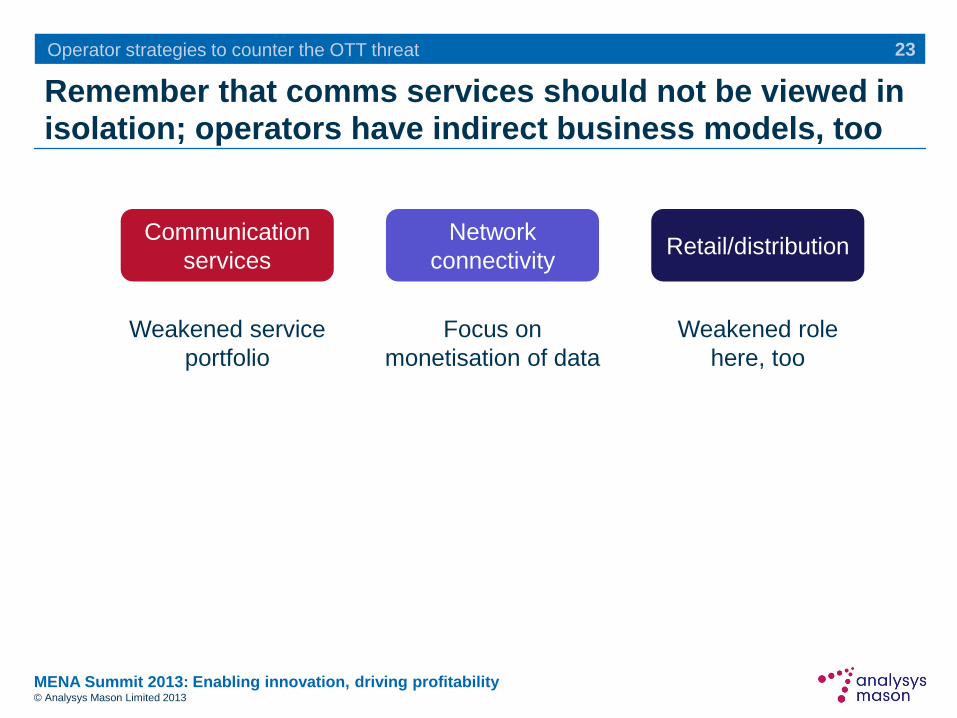

Remember that comms services should not be viewed in isolation; operators have indirect business models, too

23

Network

connectivity

Communication

services Retail/distribution

Weakened service

portfolio

Focus on

monetisation of data

Weakened role

here, too

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Remember that comms services should not be viewed in isolation; operators have indirect business models, too

24

Improved service

portfolio

Network

connectivity

Communication

services Retail/distribution

Weakened service

portfolio

Focus on

monetisation of data

Weakened role

here, too

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Remember that comms services should not be viewed in isolation; operators have indirect business models, too

25

Improved service

portfolio

Helps slow

commoditisation

and maintain ARPU

Network

connectivity

Communication

services Retail/distribution

Weakened service

portfolio

Focus on

monetisation of data

Weakened role

here, too

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Remember that comms services should not be viewed in isolation; operators have indirect business models, too

26

Improved service

portfolio

Helps slow

commoditisation

and maintain ARPU

And supports

initiatives here

Network

connectivity

Communication

services Retail/distribution

Weakened service

portfolio

Focus on

monetisation of data

Weakened role

here, too

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat 27

Changing business models in communication services

Operator responses to the OTT threat

Outlook for the MENA region

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

We forecast users/traffic/revenue (where appropriate) for operator and non-operator communication services

28

CS voice CS voice SMS/MMS

Traditional

operator

services

VoBB VoIP/VoLTE IP messaging

Next-generation

operator

services

OTT VoIP OTT VoIP OTT IP

messaging

Non-operator

provided

services

Fixed voice Mobile voice Messaging

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

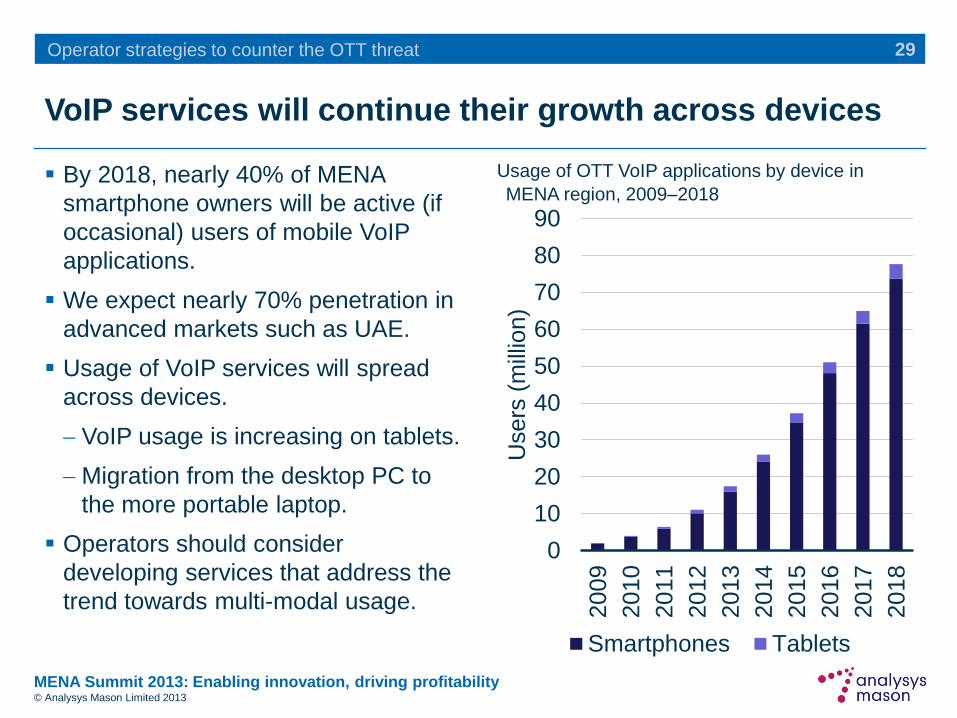

VoIP services will continue their growth across devices

29

By 2018, nearly 40% of MENA

smartphone owners will be active (if

occasional) users of mobile VoIP

applications.

We expect nearly 70% penetration in

advanced markets such as UAE.

Usage of VoIP services will spread

across devices.

VoIP usage is increasing on tablets.

Migration from the desktop PC to

the more portable laptop.

Operators should consider

developing services that address the

trend towards multi-modal usage.

Usage of OTT VoIP applications by device in

MENA region, 2009–2018

0

10

20

30

40

50

60

70

80

90

2009

2010

20

11

20

12

2013

2014

2015

2016

20

17

20

18

Users

(m

illio

n)

Smartphones Tablets

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Operators will remain the dominant force in mobile voice but will be significantly weakened

A growing proportion of smartphone

owners will use VoIP as their primary

voice service. However, full service

substitution will be very limited.

By 2018, we forecast that non-

operator-provided VoIP services will

generate 21% of smartphone users‟

voice traffic.

In the UAE we expect this figure to

be much higher: 33%

Exposure of international call

volumes

Higher smartphone penetration

fuels network effect

Availability of Wi-Fi.

30

Voice traffic originated from smartphones in

MENA region, 2009–2018

0

50

100

150

200

250

300

350

400

20

09

20

10

20

11

201

2

20

13

20

14

20

15

20

16

201

7

20

18

Min

ute

s (

bill

ion

)

OTT IP voice

Operator IP voice

Circuit-switched voice

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Operators are much more vulnerable in messaging

31

OTT messaging services will

continue to grow strongly. We expect

service penetration of smartphones

to increase to over 60% by 2018.

Full service substitution is much

more viable in messaging; SMS is

not a universal service and usage is

strongly clustered.

Partnerships look likely dominate in

many markets and appetite for

operators to compete head-on for the

mass-market limited.

Messaging volumes on smartphones in MENA

region by type of service, 2009–2018

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Messages (

trill

ion)

SMS/MMS Operator IP

Non-operator IP

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

The revenue outlook is providing a challenge for standard investment models

32

Investment decisions typically based

on NPV/DCF assume revenue

growth.

The value of the communication

services business is currently

unknown.

But some of its value is in supporting

other parts of the business:

Chiefly connectivity

But also distribution, identity

management, authentication,

billing, location, etc.

Some opportunities for incremental

revenue but, importantly, also

defence of key links in value chain.

Handset ARPU in MENA region, 2012–2018

0

5

10

15

20

12

20

13

20

14

20

15

20

16

20

17

20

18

US

D p

er

month

Voice Messaging Data

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Summary

33

The value of communication services is increasingly „indirect‟

• Dominant Internet players each have their own business model

• Smaller start-ups also developing new models

Operators are experimenting with a range of approaches

• „Free‟ voice and messaging are increasingly the default

• Voice over Wi-Fi the clearest service enhancement

Continued uncertainty about long-term role of communication services

• Difficulty of investment case in context of long-term revenue decline

• Clearer argument for supporting voice services

• No „one size fits all‟ solution; different solutions for different segments?

MENA Summit 2013: Enabling innovation, driving profitability © Analysys Mason Limited 2013

Operator strategies to counter the OTT threat

Thank you for your attention.

Any questions?

34

Stephen Sale

Principal Analyst

[email protected]