34

OPM Critical Skills Gap Initiative 0511 Auditing Focus Group Results April Davis Manager, Classification and Assessment Policy U.S. Office of Personnel Management September 3, 2014

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| Upload: | julian-williamson |

| View: | 213 times |

| Download: | 0 times |

OPMCritical Skills Gap Initiative

0511 Auditing Focus Group Results

April DavisManager, Classification and Assessment Policy

U.S. Office of Personnel Management September 3, 2014

Background On August 1, 2013*, Office of Personnel

Management (OPM) met with representatives of the Closing the Skill Gap (CSG), Auditor Mission Critical Occupation (MCO) group to discuss the challenges facing the auditing series within the Office of Inspector General (OIG) government-wide.

The Auditor Focus Group study is a response to a request by Jon Rymer, Inspector General (IG), Department of Defense, Chair of the Audit Committee of the Council of Inspectors General on Integrity and Efficiency (CIGIE), and CSG Auditor MCO Sub-goal leader (SGL).

OPM (RH and SWP) - SGL 8/1/13 Meeting Notes2

Background (con’t) Specifically, as the Auditor MCO Sub-goal

leader, Mr. Rymer has asked OPM to consider†:– working with the Inspector General (IG) community

to create a new standard that better fits their standards for conducting the work auditors do as required under the Inspector General Act of 2008, or

– modify the existing standard (0511) with amending text to allow for more connections to performance-based auditor work.

†OPM (SWP) Correspondence

3

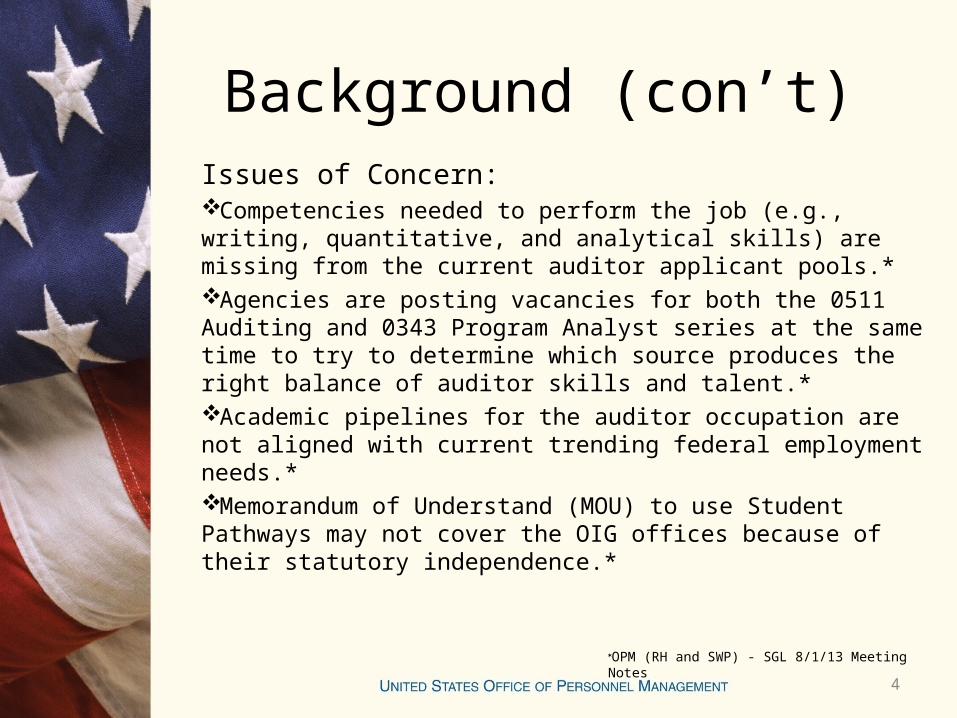

Background (con’t)Issues of Concern:Competencies needed to perform the job (e.g., writing, quantitative, and analytical skills) are missing from the current auditor applicant pools.* Agencies are posting vacancies for both the 0511 Auditing and 0343 Program Analyst series at the same time to try to determine which source produces the right balance of auditor skills and talent.* Academic pipelines for the auditor occupation are not aligned with current trending federal employment needs.*Memorandum of Understand (MOU) to use Student Pathways may not cover the OIG offices because of their statutory independence.*

OPM (RH and SWP) - SGL 8/1/13 Meeting Notes

4

Background (con’t)Issues of Concern:Communications with the Chief Human Capital Officer (CHCO) contacts, for the most part, does not reach the OIG offices.*Positive education requirement of a degree in Accounting or related field with 24 semester hours in accounting may not align with employment needs for performance-based auditor work.‡

*OPM (RH and SWP) - SGL 8/1/13 Meeting Notes‡Pre-focus group meeting 9/23/13 and FAEC GS 511 Position Paper

5

GoalThe purpose of this study was to identify and understand from CIGIE and the 0511 Auditor community •some baseline information for possible improvements on vacancy announcements, better defining agency-specific “specialized experience” requirements, and the barrier root causes;•how changes to the OPM classification and/or qualification standards will address issues experienced in identifying qualified applicants for agencies’ auditor positions; and •the potential impact on current 0511s government wide.

6

CIGIE Information Auditing and Human Resources (HR) IG

Representative Contacts Federal Audit Executive Council (FAEC)

Professional Development Committee Survey FAEC group Position Paper Pre-Focus Group Meeting w/ CIGIE Audit

Committee members and Key Stakeholder agencies

7

Methodology Review of relevant literature and information.

• Federal data sources (e.g., FedScope Database)• Other sources (e.g., FAEC position paper, ARC’s Issue

paper, GAO Government Auditing Standards)

Qualitative analysis of focus group information. Summary of information provided by focus groups,

agency comments, CIGIE, and other data collected.

8

Methodology (con’t) Human-Centered Design (HCD) Focus Group

Format In-person discussion and interactive design format

o Journal Discussiono What’s on your Radar?o Rose-Bud-Thorn/Affinity Clustero Statement Starters/Creative Matrix

Forty agencies invited to participate 13 out of 40 (33%) agencies attended sessions

(Cabinet-level, large, and excepted service included)

Conduct Focus Groups (HCD Methods) Four in-person focus groups were held; 27

participants from 13 agencies attended Auditor-IG and HR-IG Subject Matter Experts (SMEs)

participated

9

Participants Demographics

Agency List(N= 13)

HR SME

(Count)

Auditor SME

(Count)DHS 0 1DOC 1 1DOD 0 1DOE 0 1DOS 1 1FDIC 0 1FRB 0 1GSA 1 3HHS 1 2HUD 1 0SSA 2 1Treasury 1 3USDA 2 1

Total 10 17

Total number of 0511 Auditor and HR SME focus group participants (in-person only)

SME Count of Agencies that Participated

10

Agency Breakdown of 0511sGovernment wide – Part 1

11

Agency Breakdown of 0511s Government wide – Part 2

12

GS-Level Breakdown of 0511s Government wide

Grade Count Percent

GS-1 0 0%

GS-2 0 0%

GS-3 0 0%

GS-4 0 0%

GS-5 2 0%

GS-6 0 0%

GS-7 148 1%

GS-8 0 0%

GS-9 354 3%

GS-10 0 0%

GS-11 631 5%

GS-12 4,715 39%

GS-13 3,945 32%

GS-14 1,546 13%

GS-15 485 4%

N/A 326 3%

TOTAL 12,152 100%

Source: OPM, FedScope Database, March 2014

13

Educational Breakdown of 0511s Government wide

Source: OPM, FedScope Database, March 2014

14

Length of Service Breakdown of 0511s Government wide

15

Focus Groups OPM’s Classification and Assessment Policy

(CAP) conducted focus groups to discuss performance auditing work throughout the government.

The purpose of the meetings were to discuss agencies’ experiences with using the current classification and qualifications standards for identifying applicants from which to select and fill performance auditor positions.

16

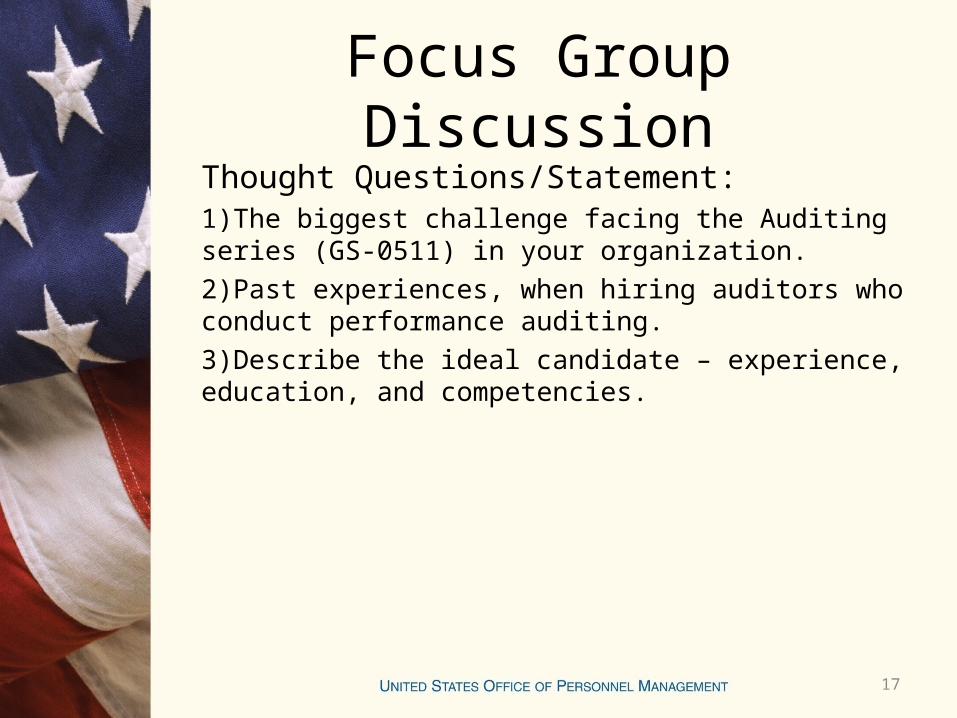

Focus Group DiscussionThought Questions/Statement:1)The biggest challenge facing the Auditing series (GS-0511) in your organization.

2)Past experiences, when hiring auditors who conduct performance auditing.

3)Describe the ideal candidate – experience, education, and competencies.

17

Results Classification Competencies Recruitment Qualifications Assessments Hiring Retention Training and Development

18

Classification Professional versus Administrative Work

– Most agree that a degree is needed for the auditing position; however, many questioned the need for it to be an accounting degree only.

– Mixed support that candidates need knowledge of Government Auditing Standards, also known as the “The Yellow Book.”

Financial versus Performance Auditing– Primary focus of IG Auditors is on performance audits;

efficiency and effectiveness studies are their typical responsibilities.

– A clearer distinction needed between financial accounting and performance auditing skill sets to assist agencies in classifying performance auditing positions.

19

Classification Position Management

– The use of both the GS-0511 and GS-0343 positions to perform performance audit work.

20

CompetenciesList of competencies identified to “successfully perform the job” by focus group SMEs

Demonstrated by the ideal candidate to successfully perform the job

Lacked by recent candidates to successfully perform the job

Needed by the ideal candidate at entry level

Analytical skills Data analysis Data manipulation Critical thinking/ evidence-based Communication skillsInterpersonal skills Oral communication Writing Other characteristicsAmbitious, motivated, initiative Willing to learnTeamwork Technical expertise

Analytical thinking

Critical thinking Data manipulation Problem solving by going

out and meeting people to discuss the issues

Interpersonal skills

Oral communication Writing

Initiative Diverse experience Team work Legal research

Analytical skills Oral communication Writing

21

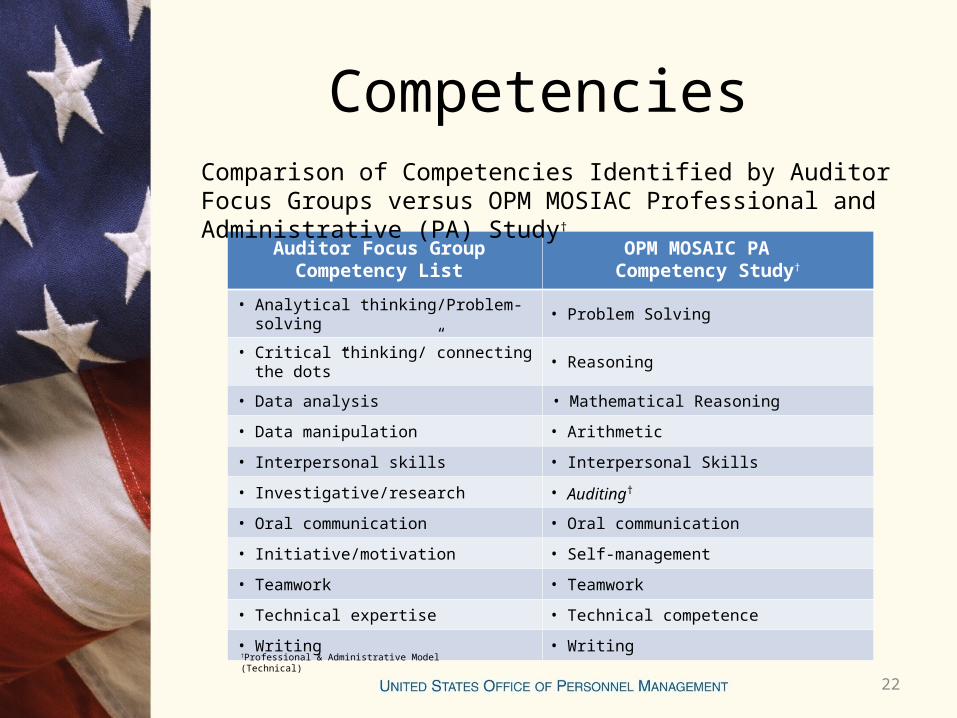

Competencies

Auditor Focus Group Competency List

OPM MOSAIC PA Competency Study†

• Analytical thinking/Problem-solving • Problem Solving

• Critical thinking/”connecting the dots” • Reasoning

• Data analysis • Mathematical Reasoning

• Data manipulation • Arithmetic

• Interpersonal skills • Interpersonal Skills

• Investigative/research • Auditing†

• Oral communication • Oral communication

• Initiative/motivation • Self-management

• Teamwork • Teamwork

• Technical expertise • Technical competence

• Writing • Writing

Comparison of Competencies Identified by Auditor Focus Groups versus OPM MOSIAC Professional and Administrative (PA) Study†

†Professional & Administrative Model (Technical)

22

Recruitment Recruitment Strategy

– Identify the “right” talent pool– Attract a diverse applicant pool– Develop a better “marketing pitch”

Partnerships– Human Resources/Hiring Manager collaboration– Build university relationships

Budget/Incentives– Private sector firms (e.g. “Big 4”) more “attractive” – Internships underdeveloped– Salary rate lower; need special salary rate reinstated

Job Opportunity Announcements (JOAs)– Accurately describing the work to target performance

auditing vs financial auditing

23

Qualifications Education

– Limitations of the 24 hour accounting course requirement

– Broaden the degree requirement to include Business, Criminal Justice, etc.

Certification– Relevance of Certified Public Accountant (CPA) and

other certifications (i.e., CIA, CFE, CGFM)

Minimum Qualifications– Include needed competencies in the minimum

qualifications– Use specialized experience effectively

24

Assessments Applicant Integrity

– Disconnect between resume and self-reporting assessment tools, and in-person assessments (structure interview, writing exercises)

Occupational Questionnaire– Applicants are “gaming the process” – HR should verify applicant responses– Need to develop more effective screening questions

Assessment Design– Aligning assessment strategy to assess needed

competencies– Assistance with developing more “sophisticated”

assessment tools

25

Hiring Hiring Programs

– FCIP replaced by Pathways, agencies preferred old program

– Veteran’s preference

Hiring Authorities– Direct Hire given to agencies, but not to IG office

Hiring Process– JOA not specific enough– Time-to-hire too long– USAJobs cumbersome

Best Qualified– Category rating, candidates “look good” on paper– Veteran’s preference candidates

26

Retention Lack competitive benefits

– Private sector salary is much higher– Quasi- government agencies offer nice “perks” (e.g., gym

membership, spa days)

Turnover– Work is not of interest to new hires, expect to perform

financial auditing – Agencies “stealing” talent from each other– Need Succession Planning in preparation for retirement

eligible

Career Ladders– Seek career mobility for 0343 Program Analysts

27

Retention Possible incentives

– Re-institute Special Salary Rate– Develop good internships/details– Give awards

28

Training and Development On-the-Job-Training (OJT)

– Need auditors that can “hit the ground running”– Need shadowing and coaching from more

experienced colleagues

Funding– No training budget

Skill gaps– Training courses can only do so much– Need close supervision and feedback

29

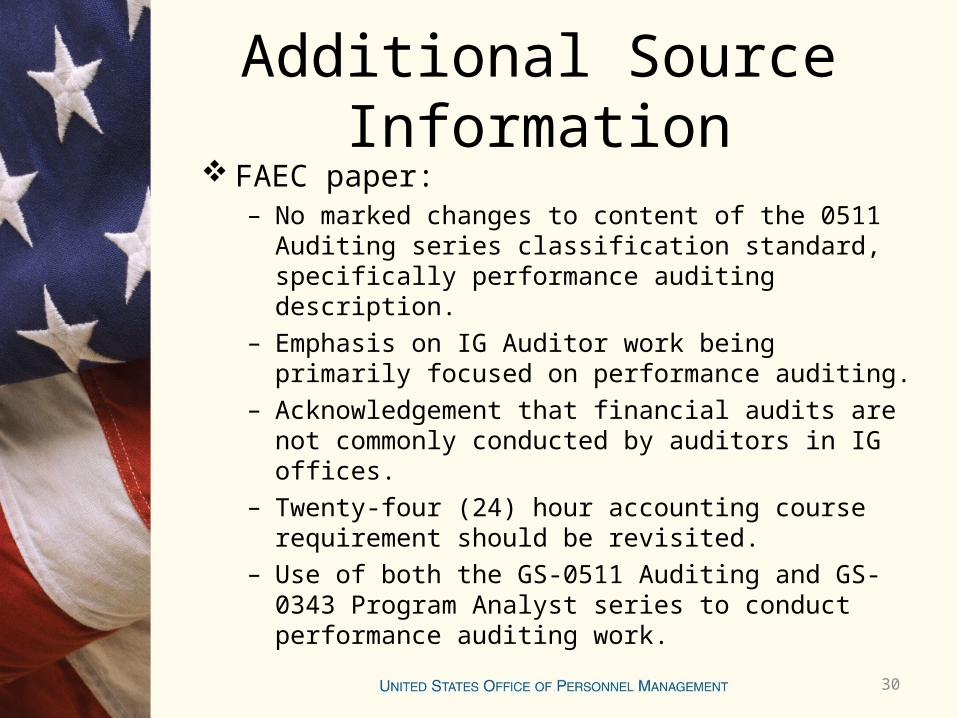

Additional Source Information FAEC paper:

– No marked changes to content of the 0511 Auditing series classification standard, specifically performance auditing description.

– Emphasis on IG Auditor work being primarily focused on performance auditing.

– Acknowledgement that financial audits are not commonly conducted by auditors in IG offices.

– Twenty-four (24) hour accounting course requirement should be revisited.

– Use of both the GS-0511 Auditing and GS-0343 Program Analyst series to conduct performance auditing work.

30

Findings In response to creating a new standard or

modifying current standard to include current performance requirements:

– OPM may need to review the GS-0511 Auditing classification and qualification standards to simplify distinctions between 0511 “performance” and 0511 “financial” audit work.

– OPM guidance may be needed to ensure that organizations are aware of their ability to utilize organizational titles such as Performance Auditor to recruit and hire.

– Other opportunities exist to partner with OPM’s Recruitment and Hiring team to assist in closing the 0511 Auditing Series skills gap

31

OPM’s Recommendations Work with OPM to revisit Classification and Qualification

Standards – to simplify distinctions between performance audit work and

financial audit work– Review 24 hour account course criteria

Establish strategic partnerships for recruitment and hiring– Promote University Partnerships (e.g., Pathways) – Strengthen HR/SME Partnership – Develop “Realistic Job Preview” to describe the work

Re-assess hiring processes– Revisit assessment strategy – Identify specialized skills and targeted competencies in the JOAs

Develop training and development strategies to close skill gaps

– Crowdsourcing to create training – Establish a Community of Practice – Develop Career Paths

32

SummaryTogether we can implement strategies to ensure Federal agencies can attract, recruit, and retain skilled Auditor employees to accomplish agency and Government wide performance-related work.

33