13

OPPORTUNITIES IN INDIAN POWER SECTOR BUSINESS SWEDEN India April 2015

OPPORTUNITIES IN INDIAN

POWER SECTOR

BUSINESS SWEDEN

India

April 2015

THE INDIAN ECONOMY HAS WITNESSED RAPID GROWTH IN THE PAST

DECADE AND TO SUSTAIN A SIMILAR GROWTH TRAJECTORY OF 9%,

THE POWER SECTOR NEEDS TO GROW AT ATLEAST 8.1 % PER

ANNUM

Planning Commission

‘ ‘

2 BUSINESS SWEDEN

INDIA – THE WORLDS LARGEST DEMOCRACY

WORLD BANK DATABASE, INTERNETLIVESTATS.COM

Parameters India Sweden

Area: 3,287,000 sq. km 450,000 sq. km

Population:

2013

1,252 million 9.5 million

Population growth:

2013

1.2% 0.8%

Adult literacy rate:

2011

74% 99%

GDP total:

2013

USD 1,877 billion USD 579

billion

GDP per capita:

2013

USD 960 USD 56,690

GDP per capita in

PPP:

2013

USD 5,410 USD 45,150

GDP growth:

2005-13

7.3% 0.9%

Internet

penetration:

19.2%, 243

million

89%, 8.5

million

New Delhi

Capital: New Delhi

Form of State: Federal republic, Parliamentary

democracy

Official language: Hindi and English

Currency: 23/03/2015, 1 SEK= 7.27 INR

Number of bordering countries: 6

Time zone: GMT+ 4:30h

3 BUSINESS SWEDEN

310

615

1230

2270

0

500

1000

1500

2000

2500

1990 2004 2015 2030

COAL TO REMAIN THE MAJOR SOURCE

INDIA PROJECTED TO QUADRUPLE ITS ELECTRICITY

OUTPUT BETWEEN 2004 AND 2030

SOURCE: CEA.NIC.IN, IBEF, MINISTRY OF POWER

Growth in Electricity Generation

1990 – 2030 in TWH

Growth

370%

Percentage Wise Split by Source of Electricity

1990 - 2030

0%

20%

40%

60%

80%

100%

1990 2004 2015 2030

Coal Hydro Gas Oil

Nuclear Biomass Other

4 BUSINESS SWEDEN

A few players also exist in the private sector.

While some industries have captive plants that supply the

surplus to the power grid (e.g. Triveni) others are dedicated

generators (e.g. Reliance)

Power generation is also taken up at a state government level

Power generated by the state is usually for use within the state

or shared with a partner state

Private

State

Centre

The central government takes up generation projects on a

national level

Power generated through central projects are shared between

various states through the central power grid

STATE GOVERNMENTS ARE THE LARGEST

CONTRIBUTORS TO POWER GENERATION IN INDIA

SOURCE: CEA.NIC.IN, IBEF, MINISTRY OF POWER

38%

33%

29%

State Private Centre

Share of Generation Capacity

2014

5 BUSINESS SWEDEN

India is the fourth largest producer and electricity

consumer in the world

Thermal energy is the largest source of electricity

generation in India, contributing to more than 60% of

electricity generation

Power produced through hydro sources is highest in

northeast and southern India owing to rivers

THERE ARE REGIONAL DIFFERENCES IN INDIA’S

ENERGY MIX

SOURCE: CEA.NIC.IN, IBEF, MINISTRY OF POWER

Nuclear power is mainly

generated in north, due to

government policies

favoring these areas

The proportion of renewable energy

is highest in south and west India

due to government investment,

incentives and suitability of the

coastal areas to wind energy

Relative utilization of

thermal energy is

highest in eastern

India

Region Wise Split of Source of Power Generation

2013-14

0%

25%

50%

75%

100%

North West South East North East

Thermal Nuclear Hydro RES

Distribution of the Sources of Power between Different

Parts of the Country

North

West

South

East

North

East

6 BUSINESS SWEDEN

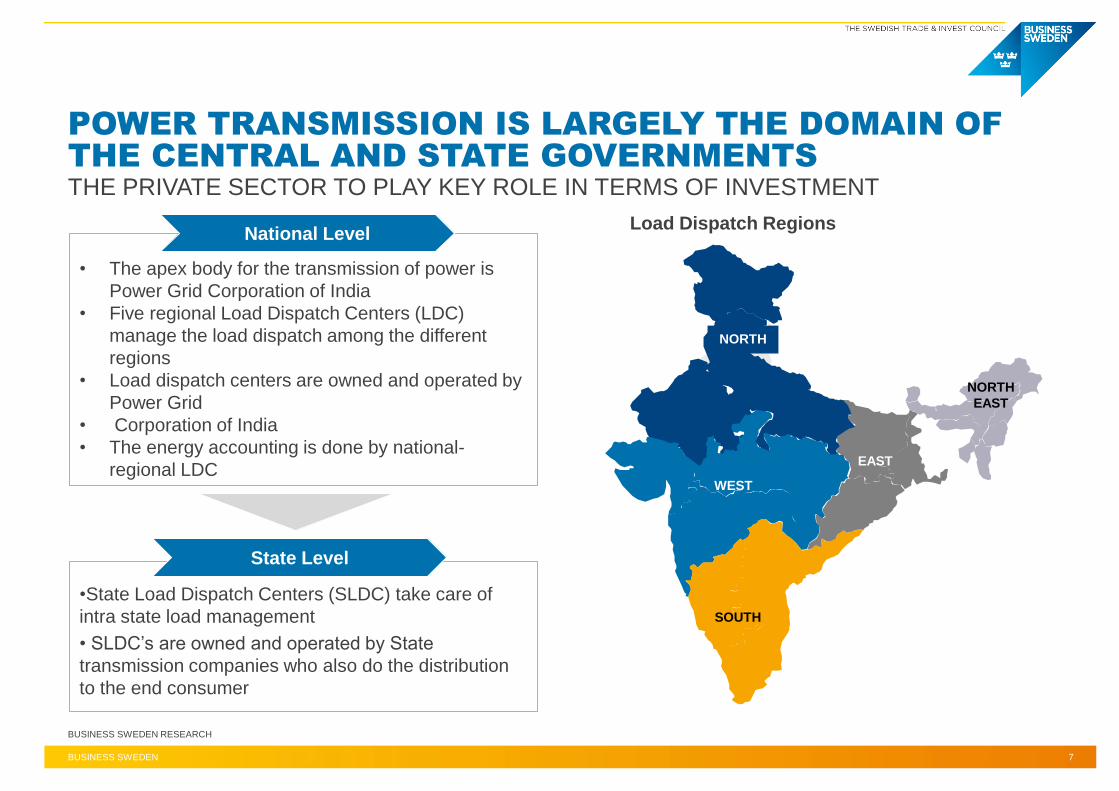

THE PRIVATE SECTOR TO PLAY KEY ROLE IN TERMS OF INVESTMENT

POWER TRANSMISSION IS LARGELY THE DOMAIN OF

THE CENTRAL AND STATE GOVERNMENTS

BUSINESS SWEDEN RESEARCH

•State Load Dispatch Centers (SLDC) take care of

intra state load management

• SLDC’s are owned and operated by State

transmission companies who also do the distribution

to the end consumer

• The apex body for the transmission of power is

Power Grid Corporation of India

• Five regional Load Dispatch Centers (LDC)

manage the load dispatch among the different

regions

• Load dispatch centers are owned and operated by

Power Grid

• Corporation of India

• The energy accounting is done by national-

regional LDC

SIL

NORTH

WEST

EAST

NORTH

EAST

SOUTH

Load Dispatch Regions National Level

State Level

7 BUSINESS SWEDEN

PRIVATE SECTOR TO CONTRIBUTE THE MOST IN THERMAL POWER GENERATION

THERMAL POWER IS MAJOR CONSTITUENT OF

PLANNED CAPACITY ADDITION BETWEEN 2012-2017

SOURCE: MINISTRY OF POWER

82% 72340

12% 10897

6% 5300

Thermal Hydro Nuclear

Split of the Planned Capacity Addition

2012-2017(88537 MW)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Thermal Hydro Nuclear

Centre State PrivateAchieved

so far 44% 11% 0%

8 BUSINESS SWEDEN

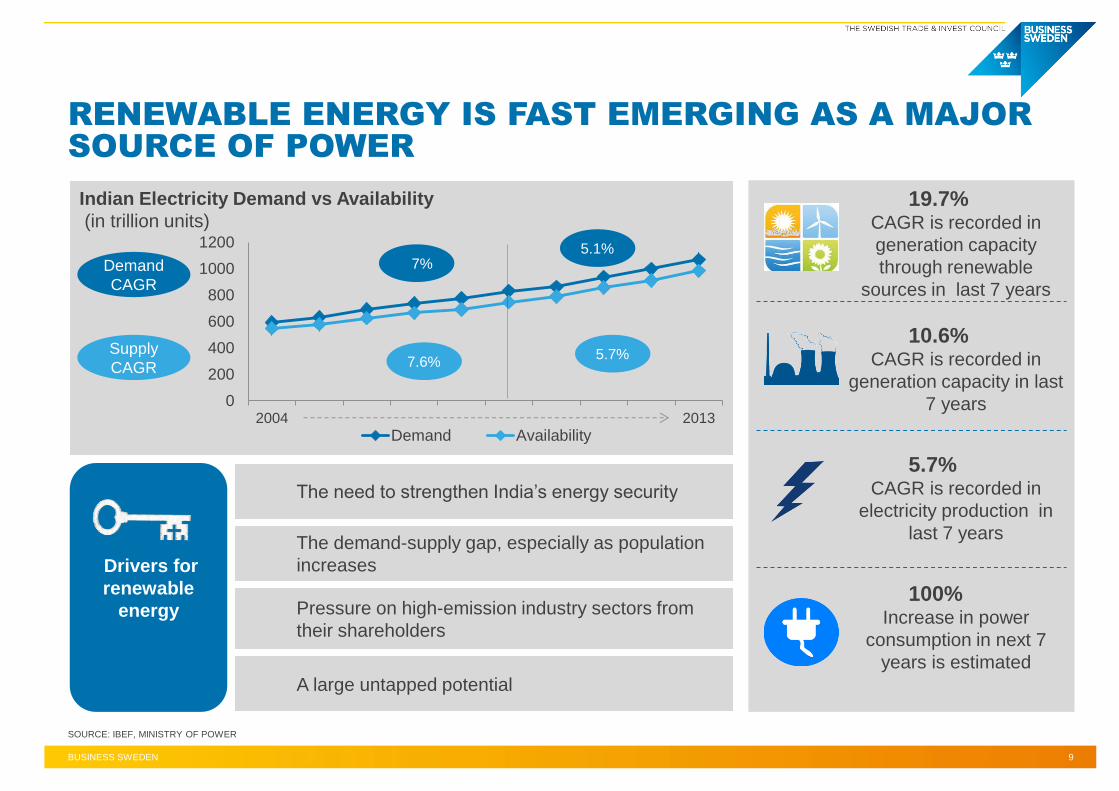

0

200

400

600

800

1000

1200

2004 2013

Demand Availability

7%

5.7%

5.1%

7.6%

RENEWABLE ENERGY IS FAST EMERGING AS A MAJOR

SOURCE OF POWER

SOURCE: IBEF, MINISTRY OF POWER

Indian Electricity Demand vs Availability

(in trillion units)

100% Increase in power

consumption in next 7

years is estimated

5.7% CAGR is recorded in

electricity production in

last 7 years

10.6% CAGR is recorded in

generation capacity in last

7 years

19.7% CAGR is recorded in

generation capacity

through renewable

sources in last 7 years

Drivers for

renewable

energy

The demand-supply gap, especially as population

increases

Pressure on high-emission industry sectors from

their shareholders

A large untapped potential

The need to strengthen India’s energy security

Demand

CAGR

Supply

CAGR

9 BUSINESS SWEDEN

INDIA HAS VAST UNTAPPED RENEWABLE ENERGY

RESOURCES

SOURCE: NATIONAL INSTITUTE OF SOLAR ENERGY IN INDIA, MAKEININDIA.COM

“India is a key market for us. We have a fully-dedicated team, a manufacturing

capacity and a solid services set up in India”...

Maxine Ghavi

Head-Solar Business, ABB

Solar Energy Wind Energy Bio-Power

Estimated

Potential

(in GW)

Installed

Capacity

(in GW)

3

750

21

103

4,1

22,5

0.4% 20% 18%

2017

2022

30 GW of renewable

capacity would be added

• 15 GW - wind power

• 10 GW - solar power

• 2.9 GW - biomass

power

• 2.1 GW - small hydro

power

100 GW of solar

power capacity to

be added

10 BUSINESS SWEDEN

MAJOR PLAYERS IN THE POWER SECTOR

BUSINESS SWEDEN RESEARCH

11 BUSINESS SWEDEN

FOREIGN INVESTORS IN INDIAN POWER SECTOR

BUSINESS SWEDEN RESEARCH

CLP Holdings (Hong Kong) GE Energy (USA) AES (USA)

Kosep (South Korea) Abellon Clean Energy (Canada) GDF SUEZ (France)

12 BUSINESS SWEDEN

NEW DELHI

Business Sweden

Embassy of Sweden, Nyaya Marg,

Chanakya Puri, New Delhi-110021, INDIA

T +91 11 46067100

www.business-sweden.se/indien

CONTACT US

BUSINESS SWEDEN IN INDIA

BANGALORE

Business Sweden

Kheny Chambers, 4/2 Cunningham

Road, Bangalore 560052

T: +91 80 415 29100

www.business-sweden.se/indien

We are located in India since

1995 and have offices in

Bangalore and New Delhi.

From our offices in India, we also

cover Afghanistan, Bangladesh,

Bhutan, Maldives, Nepal,

Pakistan and Sri Lanka