15

Options for Reducing Property Taxe David L. Sjoquist Towards a Better Understanding of Property Taxes & Proposed Policies September 11, 2008 Atlanta, Georgia

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | kiersten-nels |

| View: | 24 times |

| Download: | 1 times |

Options for Reducing Property Taxes

David L. Sjoquist

Towards a Better Understanding ofProperty Taxes & Proposed Policies

September 11, 2008Atlanta, Georgia

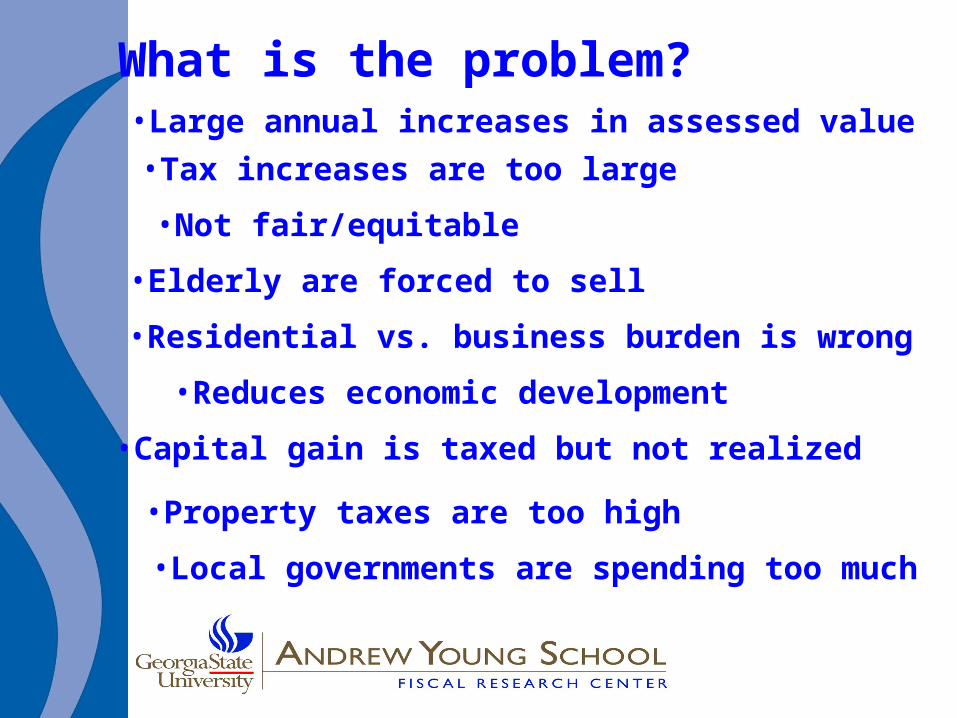

What is the problem?

•Local governments are spending too much

•Property taxes are too high

•Large annual increases in assessed value•Tax increases are too large

•Not fair/equitable

•Elderly are forced to sell

•Residential vs. business burden is wrong

•Reduces economic development

•Capital gain is taxed but not realized

Three Options for ReducingProperty Tax Burden

• State funding of education

• Grants to local governments • Targeted tax credits

I. State funding of education

• Increase QBE to $8,000 per FTE

• Districts under $8,000: eliminate PT

• Districts over $8,000: allow supplement

• Set an allowable annual increase

• Districts assured of annual increase:• From the state• From prop tax

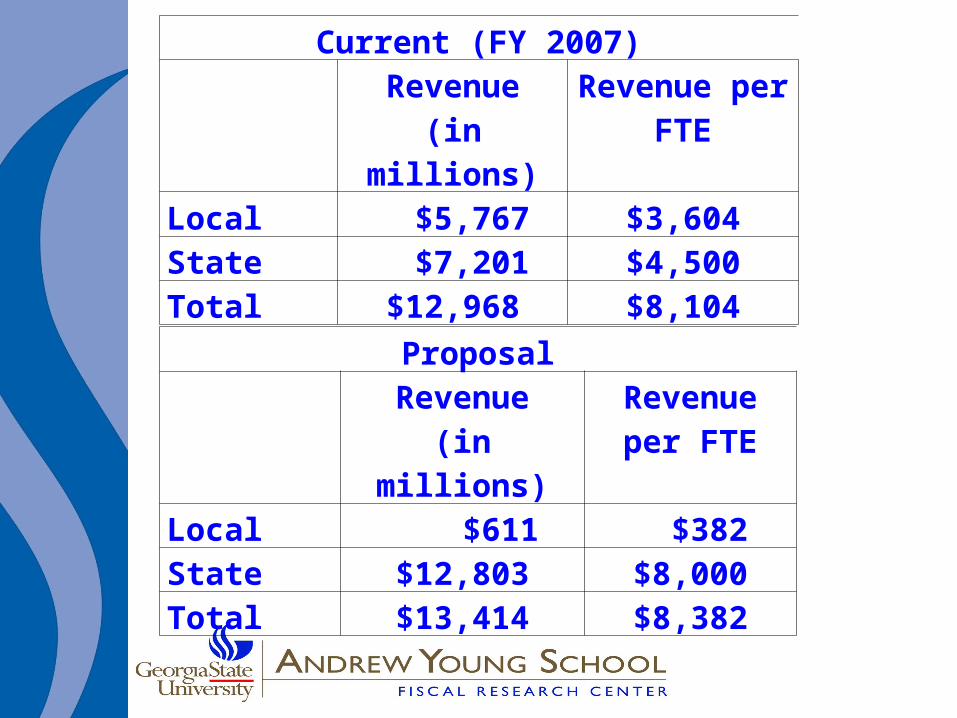

Current (FY 2007)Revenue

(in millions)Revenue per FTE

Local $5,767 $3,604State $7,201 $4,500Total $12,968 $8,104

ProposalRevenue

(in millions)Revenue per FTE

Local $611 $382State $12,803 $8,000Total $13,414 $8,382

Prop Tax Reduction = $5,156 millionIncreased funding = $445 million

% reduction in local rev: 89%Districts with 0 tax: 109

II. Matching Grant

•State grant = fraction of prop tax

•Require an equal cut in prop tax

•Set a limit for increase in grant

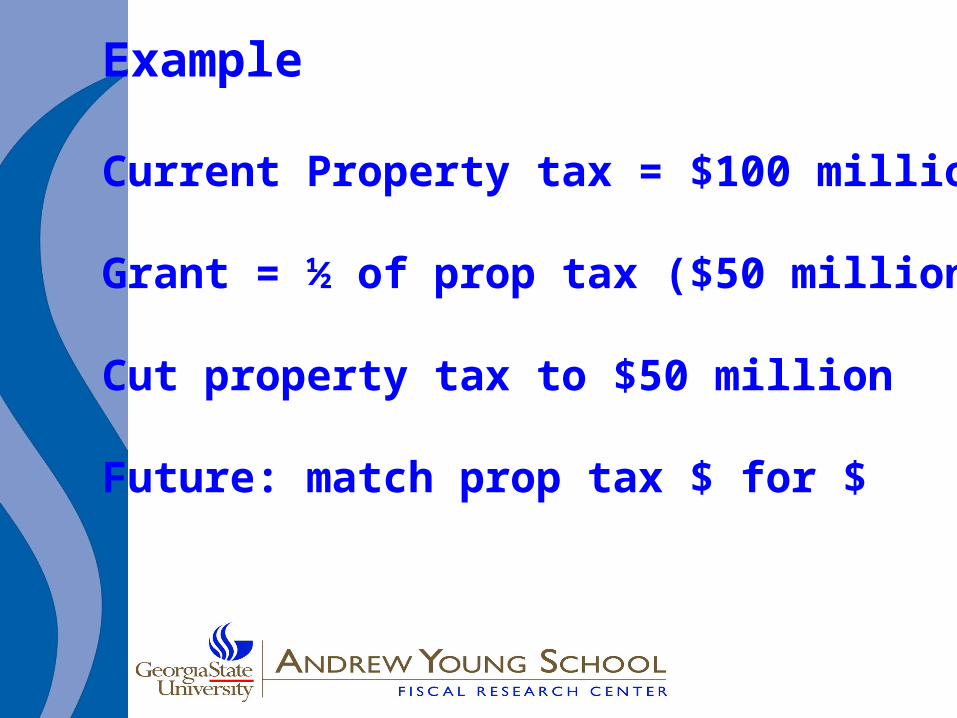

Example

Current Property tax = $100 million

Grant = ½ of prop tax ($50 million)

Cut property tax to $50 million

Future: match prop tax $ for $

What about the 2nd year?

Suppose increase is limited to 5%

Case A:Prop tax stay at $50 millionMatching Grant is $50 million

Case B:Prop tax increases to $52.5 millionMatching Grant is $52.5 million

Case C:Prop tax increases to $54 millionMatching grant is $52.5 million

III. Targeted Tax Credit

Credit = Property Tax in excessof some fraction of income

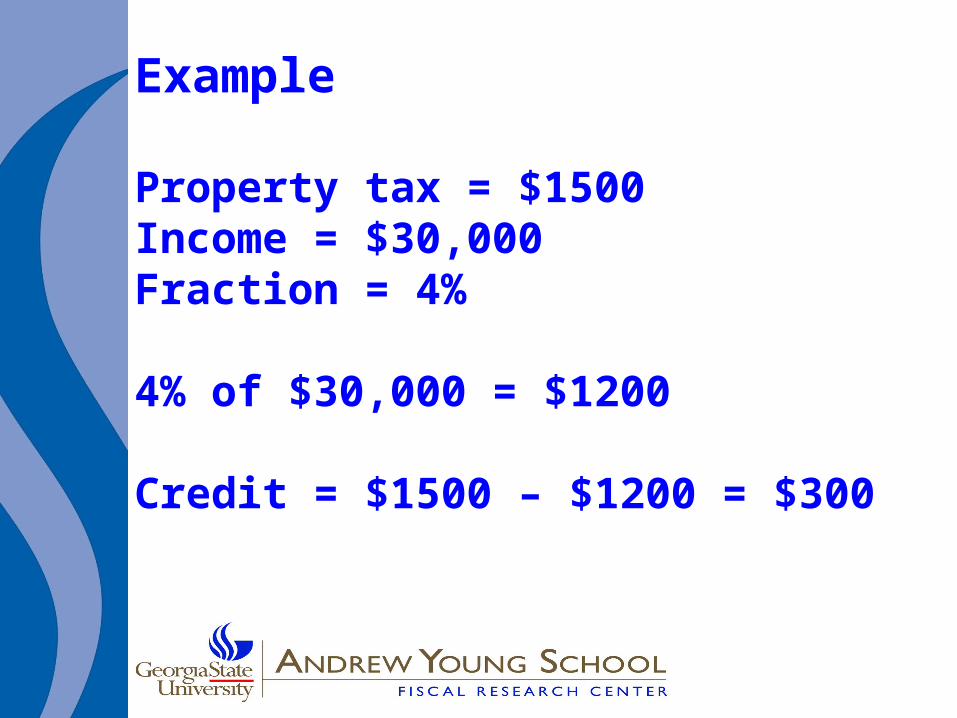

Example

Property tax = $1500Income = $30,000Fraction = 4%

4% of $30,000 = $1200

Credit = $1500 – $1200 = $300

Eligibility and Limitations

• Age• Income• Owner-Renter• Maximum credit

Relief with 4%Homeowners only

Maximum

Income

AgeLimit

Property Tax Relief(in millions)

% of Owners

None None $400 17.0%$50,000 None $247 12.4%$50,000 62 $98 5.0%

Fiscal Research CenterAndrew Young School of Policy StudiesGeorgia State UniversityAtlanta, GA FRC Report No. 182August 2008

For copies of reports,see the FRC website:

http://FRC.GSU.EDU

A Brief History of the Property Tax in Georgia

David L. Sjoquist