Oregon Oregon Renewable Renewable Energy Energy Standard Standard Cost issues of new energy technologies Community Renewable Community Renewable Energy Association Energy Association Paul R. Woodin Paul R. Woodin pwoodin@communityrenewables .org 509.261.0219 509.261.0219

Transcript

Oregon Oregon Renewable Renewable

Energy StandardEnergy Standard

Cost issues of new energy technologies

Community Renewable Community Renewable Energy AssociationEnergy Association

New energy will come from three likely sourcesNew energy will come from three likely sources• CoalCoal

• Pulverized with modern emission standardsPulverized with modern emission standards• New technologies like GasificationNew technologies like Gasification

• Natural GasNatural Gas• RenewablesRenewables

• The traditional methods of procuring long term power contracts for load The traditional methods of procuring long term power contracts for load growth are undergoing major paradigm shifts growth are undergoing major paradigm shifts

• Pricing uncertainties exist in long term power contracts for coal plants due Pricing uncertainties exist in long term power contracts for coal plants due to ever more stringent green house gas regulationsto ever more stringent green house gas regulations

• Pricing uncertainties exist for long term power contracts for Natural Gas Pricing uncertainties exist for long term power contracts for Natural Gas power plants due to uncertainties in long term fuel supplies.power plants due to uncertainties in long term fuel supplies.

Fossil Fuels – the base load options

• Coal• Older technologies are

inexpensive but polluting

• Western States are passing ever more stringent criteria on green house gasses and carbon standards

• New technologies like IGCC are promising but unproven

• Difficult to get long term firm power contracts due to unknown future carbon costs

• Natural Gas• Least polluting fossil fuel

• Supply has been under pressure leading to very high market prices

• Despite hope in discovery of new fields and LNG, experts are pessimistic in long term viability of Natural Gas as an energy fuel source.

• Almost impossible to get long term power contracts due to variability of fuel futures.

Renewables

Wind• Most cost effective of large scale

renewables – can be 100’s of MW per project

• Intermittent in nature – needs to be firmed• Costs raising due to shortage of turbines

and inflation• Can be priced for long term power

contracts with known costs• A good mix with base load but can not be

the total solution to utility needs

Small Hydro• Generally small sized projects – 1-3 MW• Seasonal runoffs can vary output• Difficult to site and permit

Solar• Normally net metering but moving into

the power generation size

• Geothermal• Can provide base load• Some sites can be multi-megawatt

locations• Generally more expensive than wind

• Biomass• Can provide base load• Can be cost effective as combined

cycle for existing loads i.e. - lumber mills.

• Has not proven cost effective for pure power sales without some value added product

• New technologies coming on the market that could change the cost dynamics

Coal• Good base load powerGood base load power

• Under pressure for greenhouse gases and carbon generationUnder pressure for greenhouse gases and carbon generation

• Carbon Sequestration an unproven technologyCarbon Sequestration an unproven technology

• Gasification of coal is promising however has never been done on a commercial Gasification of coal is promising however has never been done on a commercial scalescale

• NWPUD states Utah prices for a new pulverized coal plant at $49.91/MW and a new NWPUD states Utah prices for a new pulverized coal plant at $49.91/MW and a new IGCC cost of $53.60/MW. Unfortunately, neither plant will be built until 2013 and IGCC cost of $53.60/MW. Unfortunately, neither plant will be built until 2013 and these prices do not contain any costs for carbon cap and trade, sequestration, or other these prices do not contain any costs for carbon cap and trade, sequestration, or other regulated carbon costs. These prices are not firm and do not represent the potential regulated carbon costs. These prices are not firm and do not represent the potential for long term power contract with known prices.for long term power contract with known prices.

• It is unlikely that the Utah pulverized coal plant would qualify for California or It is unlikely that the Utah pulverized coal plant would qualify for California or Washington Green House gasWashington Green House gas

•

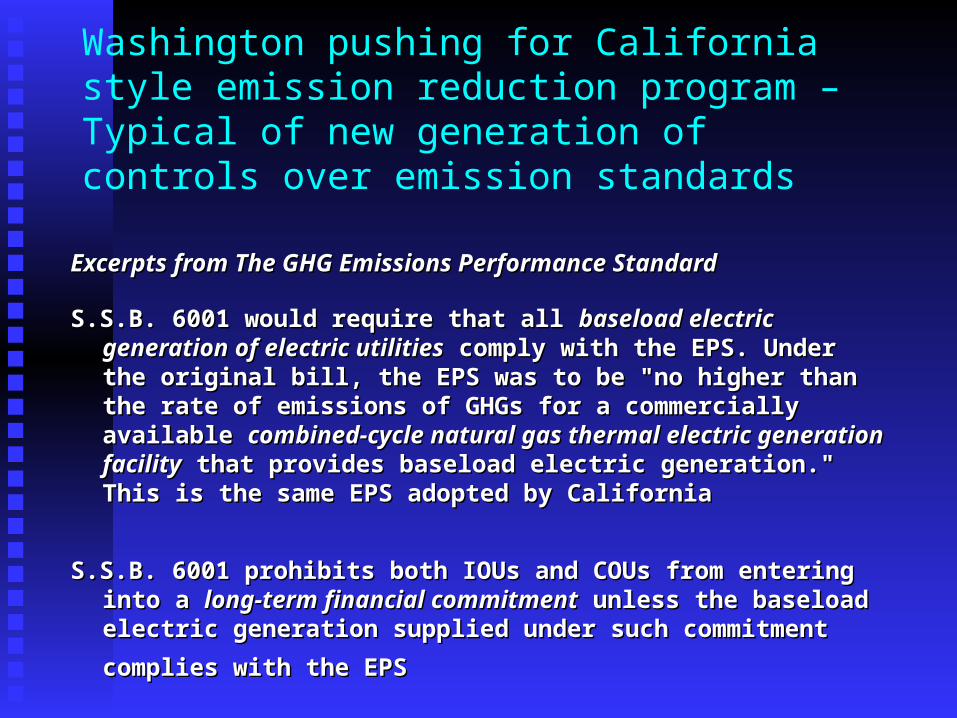

Washington pushing for California style emission reduction program – Typical of new generation of controls over emission standards

Excerpts from The GHG Emissions Performance StandardExcerpts from The GHG Emissions Performance Standard

S.S.B. 6001 would require that all S.S.B. 6001 would require that all baseload electric generation of electric baseload electric generation of electric utilitiesutilities comply with the EPS. Under the original bill, the EPS was to comply with the EPS. Under the original bill, the EPS was to be "no higher than the rate of emissions of GHGs for a be "no higher than the rate of emissions of GHGs for a commercially available commercially available combined-cycle natural gas thermal electric combined-cycle natural gas thermal electric generation facilitygeneration facility that provides baseload electric generation." This that provides baseload electric generation." This is the same EPS adopted by Californiais the same EPS adopted by California

S.S.B. 6001 prohibits both IOUs and COUs from entering into a S.S.B. 6001 prohibits both IOUs and COUs from entering into a long-long-term financial commitmentterm financial commitment unless the baseload electric generation unless the baseload electric generation

supplied under such commitment complies with the EPSsupplied under such commitment complies with the EPS

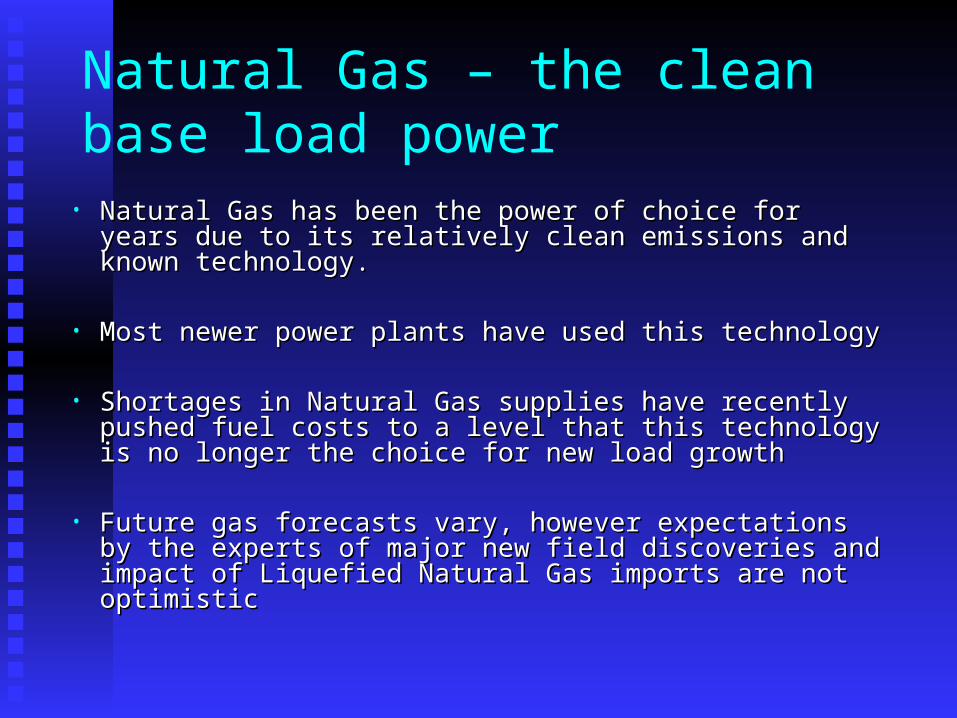

Natural Gas – the clean base load power

• Natural Gas has been the power of choice for years due to its Natural Gas has been the power of choice for years due to its relatively clean emissions and known technology.relatively clean emissions and known technology.

• Most newer power plants have used this technologyMost newer power plants have used this technology

• Shortages in Natural Gas supplies have recently pushed fuel Shortages in Natural Gas supplies have recently pushed fuel costs to a level that this technology is no longer the choice costs to a level that this technology is no longer the choice for new load growthfor new load growth

• Future gas forecasts vary, however expectations by the Future gas forecasts vary, however expectations by the experts of major new field discoveries and impact of experts of major new field discoveries and impact of Liquefied Natural Gas imports are not optimisticLiquefied Natural Gas imports are not optimistic

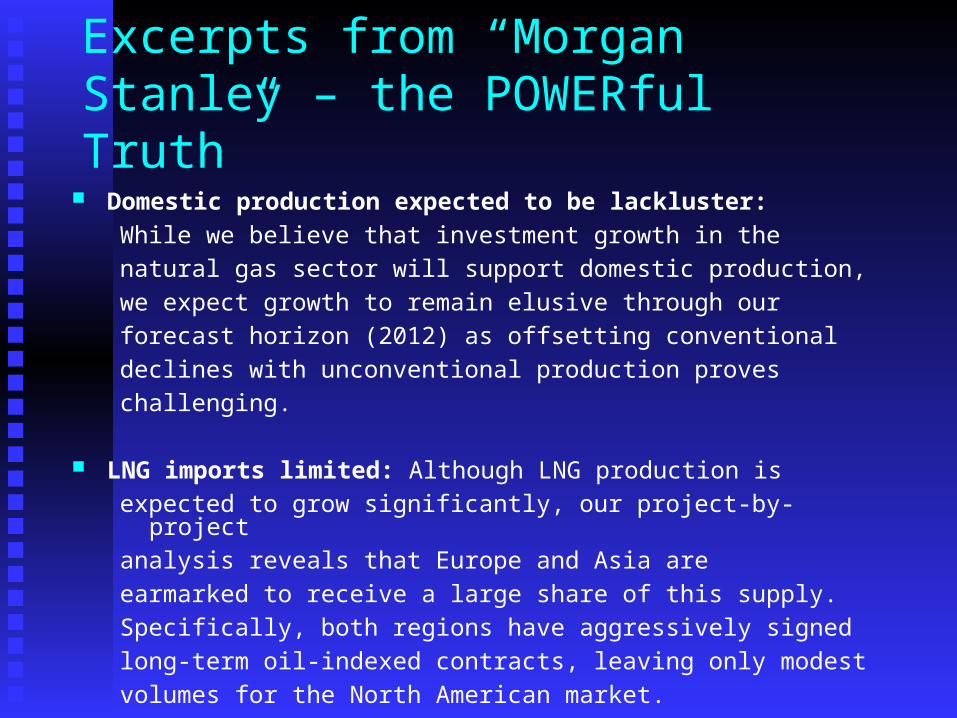

Excerpts from “Morgan Stanley – the POWERful Truth”

Domestic production expected to be lackluster:

While we believe that investment growth in the

natural gas sector will support domestic production,

we expect growth to remain elusive through our

forecast horizon (2012) as offsetting conventional

declines with unconventional production proves

challenging.

LNG imports limited: Although LNG production is

expected to grow significantly, our project-by-project

analysis reveals that Europe and Asia are

earmarked to receive a large share of this supply.

Specifically, both regions have aggressively signed

long-term oil-indexed contracts, leaving only modest

volumes for the North American market.

Excerpts from “Morgan Stanley – the POWERful Truth”

Our base case scenario points to a consistentNorth American Gas Balance Deficit:

At current crude oil prices, natural gas prices show upside of10% and 16% in 2009 and 2010, respectively, withnatural gas prices rising to above $8.75/mmBtu.

However, as our subsequent scenario analysisreveals, natural gas prices could increase intodouble-digit territory, potentially trading up to heatingoil, in order to reduce demand growth, stimulatehigher-cost domestic production, and attractadditional LNG spot cargoes.

Forecasting long term power costs is proving much more difficult than past years

• There is concern in the market place for the cost of new load There is concern in the market place for the cost of new load growth powergrowth power

• Will RPS’s raise power costs?Will RPS’s raise power costs?• Will coal, gas, or renewables be the best choice?Will coal, gas, or renewables be the best choice?

• The answers appear to be complexThe answers appear to be complex• All new load growth will raise pricesAll new load growth will raise prices• Utilities that actively buy power in the market are finding Utilities that actively buy power in the market are finding

renewables to be cost effective against more traditional renewables to be cost effective against more traditional fossil fuel choicesfossil fuel choices

• A prudent mix of fossil fuel and renewables appear to be A prudent mix of fossil fuel and renewables appear to be the choice of the larger utilitiesthe choice of the larger utilities

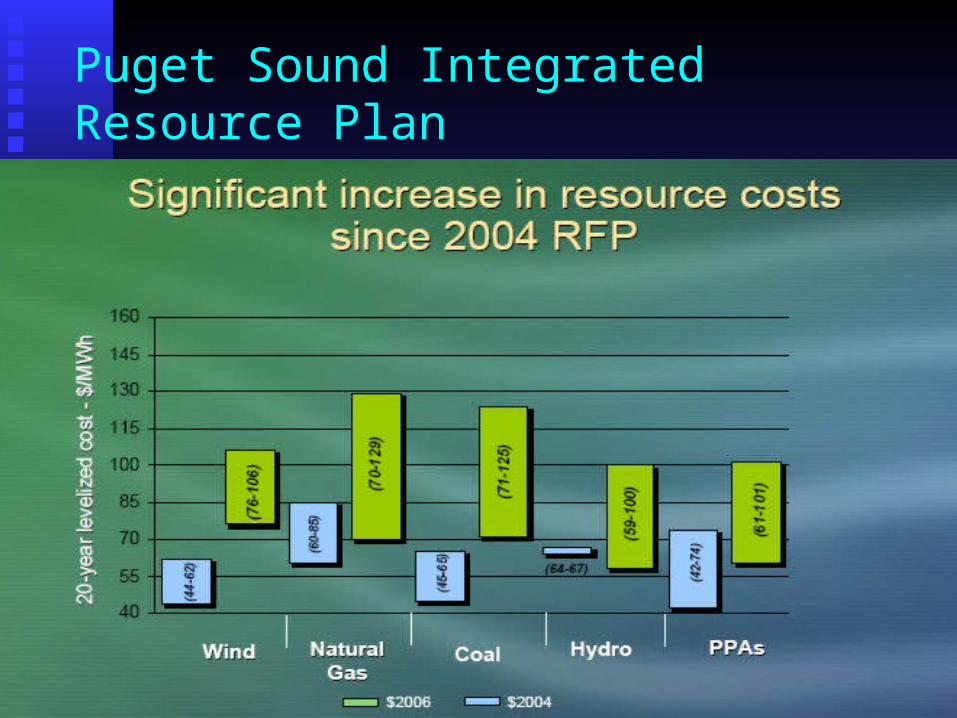

Puget Sound Integrated Resource Plan

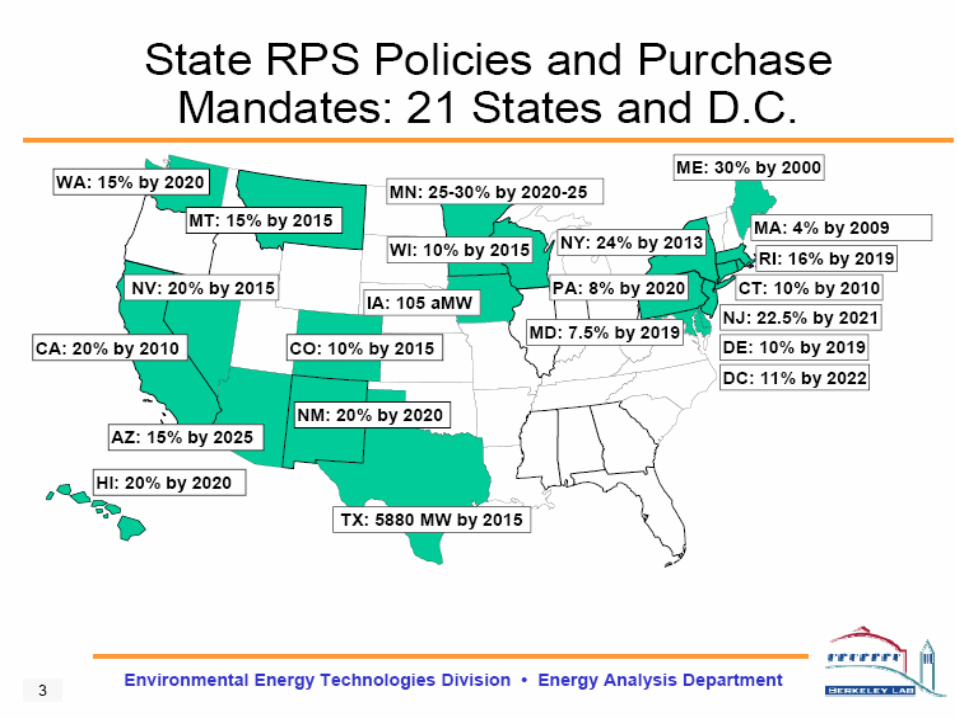

Weighing the Costs and Benefits of State Renewables Portfolio Standards:A Comparative Analysis of State-Level Policy Impact ProjectionsLawrence Berkeley National Laboratory

• • Project scope• – Survey of 28 state RPS cost impact projections in 18 states• – Sample includes state and utility-level (not federal) analyses in the

U.S.• – Studies present projected (not actual) costs and benefits

• • Comparison of key results• – Direct or inferred projected retail rate impacts• – Projected renewable deployment by technology• – Scenario analysis; secondary cost impacts; and benefits• – All results presented here are taken from the first year that each RPS• hits its ultimate target level (e.g. 2013 for New York, 2010 for