9

Organic Cotton Demand Insights Report 2021

Organic Cotton Demand Insights Report 2021

Organic Cotton Demand Insights Report•• 3

This report summarises the findings of a survey Textile Exchange carried out in early 2021 to provide a snapshot of the current and future demand for organic cotton worldwide. The survey was sent to all Textile Exchange Members as well as members of the wider Organic Cotton Round Table (OCRT) Community.

The survey asked questions about current sourcing of organic cotton, future needs for both organic and in-conversion, and perceived barriers for reaching organic sourcing goals.

The majority of respondents were brands and included companies responsible for at least half of the 2018/19 organic cotton uptake.

Introduction

Contents

2 Textile Exchange © 2021 Cover photo: Organic cotton held by farmer in Brazil © Charlotte Lapalus for VEJA

Summary of Results 4

Who Took Part in the Survey? 6

Future Demand 8

Current & Future Sourcing Locations 9

Obstacles & Opportunities 12

Conclusion 14

4 ••Textile Exchange © 2021 Organic Cotton Demand Insights Report•• 5

Summary of Results

• Overall, the findings represent an 84% increase in forecasted organic cotton demand by 2030 compared to a 2019/20 baseline

• Of the 116 respondents, only 16 (14%) provided forecast data. While this doesn’t necessarily mean that brands aren’t forecasting future needs, demand signals and commitments will need to be clearer so that farmers can plan to plant.

• The 16 respondents that provided forecast data are companies that represented 60% uptake of the 2019/20 global organic cotton production.

• For the companies that were able to project future organic cotton needs, they projected an average 10% increase in uptake each year until 2025 and a 15% increase between 2025 and 2030.

• Only one company provided anticipated demand data for in-conversion cotton. This may indicate that some companies don’t have detailed plans for how they intend to meet their future organic cotton needs, nor understand the important role that in-conversion cotton plays in the journey to organic.

• The majority (72%) of respondents knew which country or region their organic cotton came from, but there were variations in how far down the value chain they were able to trace it, with 36% able to trace to yarn level, and just 12% to seed cotton.

• There were marginal differences between current and intended sourcing regions suggesting that most intend to build on existing supply networks. However, within regions there were some variations – particularly in sub-Saharan Africa.

• The current price of organic cotton and the lack of in-conversion cotton in the pipeline to meet future organic cotton needs were considered the primary barriers for companies meeting organic cotton sourcing goals.

• Companies are predominantly addressing these challenges by entering into long-term relationships with suppliers or incorporating in-conversion cotton into their sourcing strategies.

Photo: Organic cotton farmer in Uganda © Klaus Mellenthin for Cotonea

6 ••Textile Exchange © 2021 Organic Cotton Demand Insights Report•• 7

Who Took Part in the Survey?

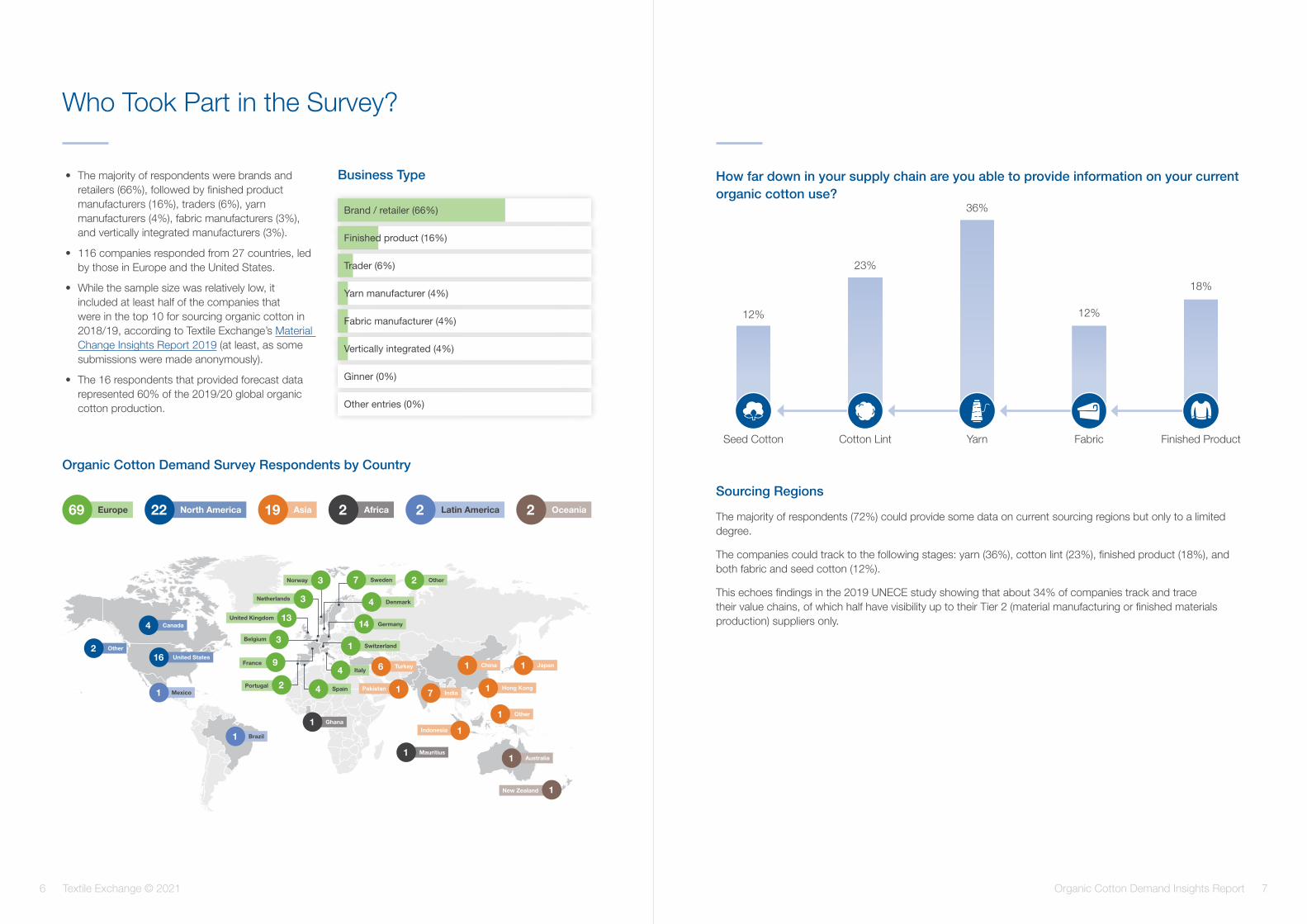

• The majority of respondents were brands and retailers (66%), followed by finished product manufacturers (16%), traders (6%), yarn manufacturers (4%), fabric manufacturers (3%), and vertically integrated manufacturers (3%).

• 116 companies responded from 27 countries, led by those in Europe and the United States.

• While the sample size was relatively low, it included at least half of the companies that were in the top 10 for sourcing organic cotton in 2018/19, according to Textile Exchange’s Material Change Insights Report 2019 (at least, as some submissions were made anonymously).

• The 16 respondents that provided forecast data represented 60% of the 2019/20 global organic cotton production.

Business Type

Organic Cotton Demand Survey Respondents by Country

Belgium

Indonesia

Pakistan

United Kingdom

Netherlands

France

Portugal

New Zealand

Canada

United States

Mexico

Brazil

Ghana

Mauritius

Sweden

Denmark

Germany

Switzerland

Italy

Spain

China

Hong KongIndia

Turkey Japan

Australia

Norway

4

Other2

Other1

Other216

1

1

1

1

1

1

17

6 1

1

1

1

Asia19Europe69 Latin America2Africa2North America22 Oceania2

2

94

4

14

1

3

3

3 7

4

13

Sourcing Regions

Finished product (16%)

Fabric manufacturer (4%)

Trader (6%)

Vertically integrated (4%)

Yarn manufacturer (4%)

Ginner (0%)

Other entries (0%)

Brand / retailer (66%)

The majority of respondents (72%) could provide some data on current sourcing regions but only to a limited degree.

The companies could track to the following stages: yarn (36%), cotton lint (23%), finished product (18%), and both fabric and seed cotton (12%).

This echoes findings in the 2019 UNECE study showing that about 34% of companies track and trace their value chains, of which half have visibility up to their Tier 2 (material manufacturing or finished materials production) suppliers only.

How far down in your supply chain are you able to provide information on your current organic cotton use?

Seed Cotton Yarn Finished ProductCotton Lint Fabric

12%

18%

23%

36%

12%

8 ••Textile Exchange © 2021 Organic Cotton Demand Insights Report•• 9

Textile Exchange gathers data on cotton uptake annually through our Corporate Fiber and Materials Benchmark (CFMB) program’s annual Material Change Index survey. This demand survey was an additional “temperature check’” survey carried out in early 2021 and is the first time we have gathered data on future demand as opposed to past use. Data gleaned from this demand survey was cross-checked against the CFMB data provided by companies to resolve any reporting inconsistencies.

Of the 116 respondents, only 16 (14%) provided forecast data. The reasons for this lack of data were not given, so it would be inaccurate to assume that it reflects a lack of forward planning. However, what is certain is that if brands want to secure future supply of organic cotton, farmers will need clearer demand signals and commitments so that they can plan to plant, given that conversion to organic can take up to 36 months.

However, responding companies project an average 10% increase uptake each year through to 2025 and a 15% increase between 2025 and 2030.

Overall, this represents an 84% increase in organic cotton demand by 2030 compared to the 2019/20 baseline of responding companies.

Future Demand Current & Future Sourcing Locations

Percentage of respondents providing organic cotton sourcing data

72+28 Providing data (72%)Not providing data (28%)

72

28

Future organic cotton sourcing regions2

South & South East Asia (30%)

Europe, Middle East, North Africa & Central Asia (23%)

Sub-Saharan Africa (11%)

Latin America & the Caribbean (11%)

North America (8%)

China (8%)

No answer (9%)

23

30

9

8

8

11

11

Current organic cotton sourcing regions1

South & South East Asia (34%)

Europe, Middle East, North Africa & Central Asia (22%)

China (11%)

Sub-Saharan Africa (9%)

Latin America & the Caribbean (8%)

North America (7%)

No answer (8%)

34

2211

9

8

78

20202020

84% increase from 2019/2020 baseline

20302030

1. Survey question was: From which countries/regions are you currently sourcing your organic cotton?

2. Survey question was: Are you interested in sourcing organic cotton produced in other countries/regions?

10 ••Textile Exchange © 2021 Organic Cotton Demand Insights Report•• 11

Current & Future Sourcing Locations (cont.)

Europe, Middle East, North Africa & Central Asia

South & South East Asia

Sub-Saharan Africa

Latin America & the Caribbean

Future organic cotton sourcing regions2

India (76%)

Brazil (40%)

Benin (30%)

Bangladesh (3%)

Colombia (10%)

Uganda (13%)

Senegal (4%)

Pakistan (15%)

Peru (40%)

Burkina Faso (17%)

Ivory Coast (4%)

Myanmar (6%)

Haiti (10%)

Tanzania (13%)

Mali (4%)

Thailand (<1%)

Argentina (<1%)

Ethiopia (9%)

Cameroon (4%)

Turkey (72%)

Kyrgyzstan (4%)

Egypt (8%)

Greece (8%)

Tajikistan (4%)

Israel (4%)

Spain (0%)

Central African Republic (0%)

Current organic cotton sourcing regions1

Bangladesh (0%)

Senegal (0%)

Ivory Coast (0%)

Turkey (61%)

Egypt (5%)

Kyrgyzstan (18%)

Israel (2%)

Tajikistan (8%)

Spain (4%)

Greece (3%)

Tanzania (53%)

Cameroon (5%)

Ethiopia (<1%)

Uganda (21%)

Mali (5%)

Burkina Faso (11%)

Benin (<1%)

Central African Republic (5%)

Peru (70%)

Argentina (<1%)

Brazil (20%)

Colombia (10%)

Haiti (<1%)

India (85%)

Thailand (<1%)

Pakistan (13%)

Myanmar (2%)

Photo: Truck of organic cotton at new organic gin in Burkina Faso © Organic & Fairtrade Cotton Coalition West Africa

Approximately 72% of respondents were able to provide data on their current organic cotton sourcing regions. There were marginal differences in the proportions of cotton coming from current versus future/anticipated-sourcing regions, suggesting that most companies intend to build on existing supply networks.

However, within regions there were some significant variations suggesting that companies plan to focus on scaling up sourcing in some countries. Notable examples include:

Sub-Saharan Africa:

The results indicate a growing interest in West African organic cotton, as well as significant potential for expansion in Ethiopia.

• From 0% to 30% in Benin

• From 11% to 17% in Burkina Faso

• From 0% to 9% in Ethiopia

Latin America & the Caribbean:

• From 20% to 40% in Brazil

• From 0% to 10% in Haiti

Growing interest in Turkey:

• From 61% to 72%

Note that these figures relate to proportions of the share of cotton within regions, not predicted increases in absolute volumes. This data should build confidence about increased interest in certain countries, but doesn’t tell us the extent or scale of the interest. Due to the sample size and the lack of data provided, projected volume data was not complete enough to make detailed projections about volume increases.

12 ••Textile Exchange © 2021 Organic Cotton Demand Insights Report•• 13

The primary barrier to meeting organic cotton sourcing goals cited was the cost of organic cotton (40%). However, the second greatest barrier was that there is not enough in-conversion cotton in the pipeline to meet demand (19%), demonstrating there is a keen interest in expanding despite the current price challenges. The two other primary concerns were that suppliers were not connected to producer groups (16%), and organic cotton of the desired quality was not available (13%).

The category of ‘other reasons’ included answers with similar themes related to price, availability, and lack of supply chain experience related to organic cotton.

Respondents are addressing the barriers to organic cotton sourcing in a number of ways, including entering into long-term commitments with farm groups, or suppliers working closely with the farmers (29%) and by incorporating in-conversion cotton into their sourcing strategies (27%). Many are taking several of the actions listed and more. For example, 17% of respondents listed other actions that they are taking, which included booking capacity in advance. However, some saw the solution as choosing other preferred cottons instead of organic or incorporating more recycled cotton into their sourcing strategy.

Obstacles & Opportunities

Obstacles and opportunities for meeting organic cotton sourcing goals

Barriers to organic cotton sourcing

How respondents intend to address barriers to organic cotton sourcing

There is not enough in-conversion cotton in the pipeline to meet our needs (19%)

Other entries (11%)

My suppliers are not connected to producer groups (16%)

I cannot find the quality of organic cotton that I'm looking for (13%)

Organic cotton is too expensive (40%)

Incorporating in-conversion cotton into our sourcing strategy (27%)

Other entries (17%)

Being/becoming part of a program that helps sourcing directly at the farm level (15%)

Sourcing directly at the farm level on a 1-to-1 basis (11%)

Entering into a long-term commitment to farm groups or suppliers working closely with farmers (29%)

Photo: SysCom research station © bioRe India Ltd.

14 ••Textile Exchange © 2021 Organic Cotton Demand Insights Report 15

Conclusion

This report is intended as a ‘temperature check’ to build a picture of the demand for organic cotton over the next ten years. While the source data doesn’t capture the whole sector, it is robust enough to provide some clear indications:

• Demand is strong, and growing

• More needs to be done to facilitate the journey to organic by supporting in-conversion cotton

• Unless proactive steps are taken there will be a missed opportunity to scale organic cotton and the positive impacts it brings.

The future for organic cotton use looks promising but there is room for greater ambition. By working together to address challenges and amplify solutions, the organic cotton sector can exceed the current projections.

It is clear that demand is growing. The industry has a sense of the challenges to scaling organic cotton and many companies are showing leadership in overcoming these. To realise growth, farmers need to have commitments so they can plan to plant and brands can feel confident about meeting their future needs. Forward planning and looking at ways to incorporate in-conversion cotton into companies’ fiber strategies will be vital.

Textile Exchange's Organic Cotton Round Table (OCRT) will build on the lessons learnt from this report by:

• Highlighting and showcasing business models that help support farmers through the conversion period.

• Addressing the price paradigm

• Showing innovative ways to market and label in-conversion cotton

For more information on the OCRT visit TextileExchange.org/organic-cotton-round-table

Textile Exchange continues to gather information on the uptake of organic cotton as well as production, and appreciates the cooperation of all producers, brands, retailers, and other stakeholders in sharing usage and production information via our surveys.

In addition, brands, retailers, manufacturers, and suppliers are invited to track their progress with organic cotton (and other preferred fiber and materials) by participating in the annual Material Change Index (MCI) survey (open through September; email: [email protected]).

New this year are questions regarding product sales figures and forecasted demand through 2025 – information vital to understanding the market.

What do these results mean for me?

16 ••Textile Exchange © 2021

For more information on the Organic Cotton Round Table (OCRT):

Visit: TextileExchange.org/organic-cotton-round-table

To learn more about in-conversion cotton:

Visit: TextileExchange.org/in-conversion-transitional-cotton