36

OSFI ANNUAL REPORT 2016-2017

OSFIANNUAL REPORT 2016-2017

Office of the Superintendent of Financial Institutions Canada255 Albert Street, 16th floor, Ottawa, ON K1A 0H2Telephone: 613-990-7788 Facsimile: 613-952-8219Toll-free line: 1-800-385-8647 Website: www.osfi-bsif.gc.caCat. No. IN1-2017E-PDF ISSN 1701-0810© Minister of Public Services and Procurement Canada

• OSFI is an independent federal government agency established in 1987.

• OSFI regulates and supervises more than 400 federally regulated financial institutions (FRFIs) and 1,200 private pension plans to determine whether they are in sound financial condition and meeting their regulatory and supervisory requirements.

• Although OSFI plays an essential oversight role, it does not manage the operations of institutions or pension plans. Their executive management, boards of directors and trustees are responsible for their success or failure.

• OSFI’s approach to supervision is risk-based to reflect the nature, size, complexity and risk profile of an institution. Financial institutions must be allowed to take reasonable risks and compete effectively. OSFI’s goal is to balance competitiveness with financial stability, and international standards with Canadian market realities.

• OSFI’s oversight does not include consumer-related issues or the securities industry, which are the responsibility of other agencies, both federal and provincial.

• OSFI reports to Parliament through the Minister of Finance and works closely with its federal partners, including the Department of Finance, the Bank of Canada, the Canada Deposit Insurance Corporation and the Financial Consumer Agency of Canada.

• OSFI recovers its costs, which in 2016-2017 totalled $150.5 million. OSFI is funded mainly through assessments on the financial institutions and private pension plans it regulates and a user-pay program for legislative approvals and other select services.

• The Office of the Chief Actuary, which is an independent unit within OSFI, provides actuarial valuation and advisory services for the Canada Pension Plan, the Old Age Security program, the Canada Student Loans program, and other public sector pension and benefit plans.

• OSFI’s regulation and supervision activities play a key role in contributing to public confidence in the Canadian financial system.

• As of March 31, 2017, OSFI employed some 700 people in offices located in Ottawa, Montréal, Toronto and Vancouver.

1 OSFI ANNUAL REPORT 2016-2017

OSFI at a Glance

2

A Balanced Approach

Regulating and supervising financial institutions and pension plans is a difficult balancing act. OSFI must find the right balance between protecting depositors, policyholders and other creditors, and allowing federally regulated financial institutions (FRFIs) to compete effectively and take reasonable risks. OSFI must also protect the rights of pension plan members and other beneficiaries by ensuring plans are meeting their funding requirements and managing their risks effectively.

Taking a balanced approach is one of our five compass points for success – a vision that sets out who we are and who we want to become. The other points are: we are risk-based; we are principles-based; we are results-oriented; and we set the benchmark for prudential regulation and supervision. We are proud of these strengths and determined to build on them because they will help us to be the best organization we can be, both now and in the future.

Superintendent’s Message

We are Risk-based

2016-2017 was another year of continuing low interest rates, growing levels of household debt and stubbornly slow economic growth. OSFI undertook a number of activities to address developing risks in these areas, and others, to further strengthen Canada’s system of prudential regulation and supervision.

Given record levels of household debt in Canada, combined with extremely active residential real estate markets, OSFI enhanced supervisory oversight around mortgage underwriting and insurance, tightened our expectations around due diligence, and reinforced our existing guidance. We will continue to respond to developments that pose additional risk.

In January 2017, our advisory, Capital Requirements for Federally Regulated Mortgage Insurers, defined a new, more risk-sensitive approach to the regulatory capital requirements for mortgage insurance. It incorporated such measures as borrower creditworthiness, outstanding loan balance, loan-to-value ratio, and remaining amortization. It also contained provisions that allow it to be adaptable to future changes.

In addition to our work on the housing file, after several years in the making, OSFI unveiled the Life Insurance Capital Adequacy Test (LICAT). The LICAT represents an evolution in OSFI’s regulatory capital expectations and is designed to take account of significant changes in the nature and management of risk within the insurance industry that will continue to protect policyholders, while fostering competition.

We are Principles-basedWhile OSFI plays a prudential oversight role in the Canadian financial system, it is boards of directors and senior management who are ultimately responsible for the safety and soundness of their institutions and compliance with the governing legislation.

OSFI launched a comprehensive review of our expectations around corporate governance practices of FRFIs. The feedback received through these targeted consultations will guide revisions to our Corporate

OSFI ANNUAL REPORT 2016-2017

3

Governance Guideline, which outlines our expectations for boards of directors and senior management.

We are Results-orientatedOSFI has a legislated mandate that describes what we do and why. But how is success defined and how are results achieved?

Everything OSFI does is aimed at improving the safety and soundness of financial institutions and private pension plans, and increasing confidence in the Canadian financial system. We do this through developing guidance on risk management and mitigation, assessing the risks and risk management of financial institutions, and intervening promptly when corrective actions need to be taken.

We focus on current and emerging risks that have the potential to have a material impact on FRFIs, and whether they have effective controls in place. It is not always certain which emerging risks or triggers will create substantial disturbances and shocks to the financial system. What is relatively certain, however, is that if controls and risk management in institutions are robust, and strong capital and liquidity shock absorbers are in place, the ability to deal with such events is greatly improved.

In general, federally regulated financial institutions are managing their risks appropriately and their performance has been strong. Indeed, Canada’s banks and insurers are considered among the safest in the world, and public confidence remains very high. And OSFI continues to develop and improve its guidance and supervisory tools to build upon this success.

OSFI also conducted a survey of FRFIs and respondents rated us highly for our effectiveness in supervising their institutions. They said we focus on appropriate areas of risk and respond in a timely manner to market changes.

The results also revealed a few areas for improvement, including the scalability of our guidance for small and medium-sized institutions, and our understanding of an institution’s business practices. We welcome this feedback and will make the necessary corrections where required.

We Set the BenchmarkTo be a world-leading regulator and supervisor, it is not enough to only set high standards for the entities

we regulate; we must also establish high standards for ourselves. We continued our Supervision Training Initiative, a multi-year plan to ensure our supervisors have the skills and knowledge necessary to perform their work. We created a new group − Common Supervisory Services − to improve the consistency of support activities across supervision groups. We also continued work on a new human capital strategy and a cyber security action plan.

Our People and Partners During the year, we welcomed two new executive members. Carolyn Rogers was appointed Assistant Superintendent, Regulation Sector. Ms. Rogers came from the Financial Institutions Commission (FICOM), the integrated financial services regulator of British Columbia, where she served as Superintendent and CEO. Michelle Doucet was appointed Assistant Superintendent, Corporate Services Sector. Ms. Doucet came from the Privy Council Office, where she served as Assistant Deputy Minister, Corporate Services Branch.

In closing, I would like to recognize the valuable contributions of my OSFI colleagues. Regulating and supervising financial institutions and private pension plans is indeed a balancing act − one that relies on the dedication of employees who are knowledgeable, skilled, passionate and determined to help maintain OSFI’s reputation as a world-class regulator and supervisor.

One of the unique aspects of Canada’s world-class system of effective prudential regulation is the strong partnership among the federal agencies that contribute to financial stability and confidence in the financial system. These partners include the Department of Finance, the Bank of Canada, the Financial Consumer Agency of Canada and the Canada Deposit Insurance Corporation. Our strong cooperation with our regulatory partners will continue as we work through issues that impact Canadians.

As we mark OSFI’s 30th anniversary year in 2017-2018, we – and those who came before us – can all be proud of this organization and its important role in contributing to public confidence in the Canadian financial system.

Jeremy Rudin

OSFI ANNUAL REPORT 2016-2017

4 OSFI ANNUAL REPORT 2016-2017

Priority B: Strengthen our ability to anticipate and respond to severe but plausible risks to the Canadian financial system

Steps Taken

• Developed and implemented a more risk-based regulatory capital framework for mortgage guarantee insurance.

• Amended bank capital rules to introduce more risk sensitivity and address greater uncertainty in housing collateral valuations when prices are rising rapidly.

• Designed and tested a proposed risk-based stand-alone capital metric to replace the current asset-based metric.

• Initiated industry-wide stress tests for mortgage insurers and presented a macro stress test vision and five-year roadmap for large banks.

• Implemented a more consistent approach to assessing liquidity risk for small and medium-sized banks based on a revised liquidity framework.

• Published the Life Insurance Capital Adequacy Test (LICAT) guideline in September 2016 for implementation in January 2018.

Performance against Priorities 2016-2017

OSFI identified five priorities for 2016-2017 through which to achieve its mandate. This section reports key accomplishments under each priority. OSFI achieved its goals for the

reporting year and continues to work on these multi-year priorities. More details are available in subsequent chapters of this report. Two new objectives to achieve our priorities were added in 2016-2017: enhance our ability to identify, analyze and respond to macroeconomic and geopolitical uncertainty; and re-examine our role and approach to enhancing cyber security at federally regulated financial institutions (FRFIs).

Priority A: Tighten the link between effort at OSFI and results in the field

Steps Taken

• Created a new unit called Common Supervisory Services (CSS) to improve the delivery of support activities across all supervisory groups.

• Completed the second phase of the Supervisory Tools and Technology Review project, including reviewing, streamlining and documenting supervisory processes.

• Compiled information on regulated entities to support assessments on risk culture and other drivers of behaviour that may undermine effective risk management.

• Collaborated with partner agencies to prioritize regulatory data requests and minimize filing required by FRFIs.

5 OSFI ANNUAL REPORT 2016-2017

• Conducted directed consultations on the international long-term liquidity metric (Net Stable Funding Ratio), slated for implementation in 2019.

• Implemented Basel III standards for the application of countercyclical capital requirements.

Priority E: Set and meet high standards for managing our own resources

Steps Taken

• Built a new enterprise document and records management system (eSpace) to enable better information sharing, improve organizational information management and accentuate cross-team collaboration. This initiative is on track to be completed in the first quarter of 2017-2018.

• Developed a Human Capital Strategy to ensure human resources programs, policies and practices are strategically aligned in support of OSFI’s objectives and mandate.

• Devised a cyber security technology roadmap, an enhanced vulnerability assessment and a cyber security policy suite.

• Designed a modular training program to establish core and specialized learning for supervisors.

• Strengthened the organizational structure through enhancements to governance and leadership and a realignment of roles, responsibilities and accountabilities.

• Converted our accounting standards from IFRS to Public Sector Accounting Standards (PSAS) following revisions by the Public Sector Accounting Board requiring OSFI to adopt PSAS as its basis for accounting.

• Enhanced financial planning, forecasting, monitoring and reporting approaches to provide greater flexibility to redeploy resources in response to evolving business needs, while respecting overall budgetary limits.

The five priority areas will also guide the achievement of strategic outcomes for 2017-2018. Details can be found in the Reports and Accountability section of OSFI’s website.

Priority C: Reinforce our principles-based guidance and supervision

Steps Taken• Issued a letter notifying industry that OSFI would be

enhancing its supervisory oversight and reinforcing its expectation that FRFIs engage in prudent underwriting of residential mortgage loans.

• Issued a guideline outlining OSFI’s expectations regarding the application of IFRS 9 − Financial Instruments and Disclosures, which replaces a series of accounting and disclosure-related guidelines.

• Conducted a pre-implementation review of Expected Credit Loss (ECL) for internal ratings-based (IRB) banks to review the impact of the ECL component of IFRS 9.

• Completed targeted consultations on a Total Loss Absorbency Capacity (TLAC) guideline in time for the release of bail-in regulations by the Department of Finance.

• Launched a comprehensive review of OSFI’s expectations for boards of directors, which began with targeted discussions with FRFI directors and senior officials.

• Established a CEO roundtable from small and medium-sized financial institutions to discuss issues of interest.

Priority D: Influence international guidance, standards and reforms with a view to implementing them in the context of what is best for Canada

Steps Taken

• Led the Financial Stability Board (FSB) Working Group on Governance Frameworks to address misconduct risk, with a view to developing a supervisory toolkit in this area.

• Worked to advance the implementation of G20 financial sector reforms, including in the areas of resolution regimes and over-the-counter derivatives.

• Participated in the efforts of the International Association of Insurance Supervisors (IAIS) to develop guidance for insurance regulators and to design and implement a new international Insurance Capital Standard (ICS).

6 OSFI ANNUAL REPORT 2016-2017

Corporate Overview

Role and Mandate

OSFI was established in 1987 by an Act of Parliament: the Office of the Superintendent of Financial Institutions Act (OSFI Act). OSFI supervises and regulates all banks in Canada and all federally incorporated or registered trust and loan companies, insurance companies, cooperative credit associations, fraternal benefit societies and private pension plans. Under the OSFI Act, the Superintendent is solely responsible for exercising OSFI’s authorities and is required to report to the Minister of Finance from time to time on the administration of the financial institutions legislation.

OSFI’s mandate:

Fostering sound risk management and governance practices

OSFI advances a regulatory framework designed to control and manage risk.

Supervision and early intervention

OSFI supervises federally regulated financial institutions and pension plans to determine whether they are in sound financial condition and meeting regulatory and supervisory requirements.

OSFI promptly advises financial institutions and pension plans if there are material deficiencies, and takes corrective measures, or requires that they be taken to expeditiously address the situation.

Environmental scanning linked to safety and soundness of financial institutions

OSFI monitors and evaluates system-wide or sectoral developments that may have a negative impact on the financial condition of federally regulated financial institutions.

Taking a balanced approach

OSFI acts to protect the rights and interests of depositors, policyholders, financial institution creditors and pension plan beneficiaries, while having due regard for the need to allow financial institutions to compete effectively and take reasonable risks.

OSFI recognizes that management, boards of directors and pension plan administrators are ultimately responsible for risk decisions, and that financial institutions can fail and pension plans can experience financial difficulties resulting in the loss of benefits.

In fulfilling its mandate, OSFI supports the government’s objective of contributing to public confidence in the Canadian financial system.

Financial Resources

OSFI recovers its costs, as stipulated under the OSFI Act. OSFI is funded mainly through assessments on the financial institutions and private pension plans it regulates and a user-pay program for legislative approvals and other select services. A very small portion of OSFI’s revenue is received through an appropriation from the Government of Canada, primarily for actuarial valuation and advisory services relating to the Canada Pension Plan, the Old Age Security program, the Canada Student Loans program and various public sector pension and benefit plans.

Human Resources

Given that we work in a knowledge-based environment, we count on the expertise of our staff to meet our mandate and maintain our position as a world-class financial regulator. At March 31, 2017, OSFI had some 700 employees in offices located in Ottawa,

OSFI ANNUAL REPORT 2016-2017 7

Montréal, Toronto and Vancouver. OSFI employees have a wide range of skills, including financial services experience, regulatory expertise and risk management backgrounds. They use these skills in positions ranging from accountants and actuaries to economists, risk managers and other professionals supporting corporate activities.

Accountability

Auditing

OSFI’s Audit Committee, comprised of three independent members and the Superintendent, provides objective advice and recommendations regarding the adequacy and functioning of OSFI’s governance, risk management and control practices. The Committee held four meetings in 2016-2017 and

provided advisory services with respect to key activities such as Enterprise Risk Management, quarterly and annual financial statements, the IM/IT strategy and the Internal Audit function.

Surveys and Consultations

OSFI routinely undertakes surveys and consultations with federally regulated financial institutions (FRFIs) to help assess its performance and effectiveness.

• In fall 2016, Environics Research Group conducted the Financial Institutions Survey, an online tracking survey of CEOs across all FRFIs.

• In winter 2017, Nielsen conducted the Life Insurance Sector Consultation, a qualitative research survey consisting of interviews with senior executives.

Remy Dagher Junior Human Resources Advisor, Human Resources Operations, Corporate Services Sector

Sean HopkinSupport Officer, Infrastructure and Technology Services Division,Corporate Services Sector

8 OSFI ANNUAL REPORT 2016-2017

The results of these surveys were positive and show improvement in overall satisfaction with OSFI. The Financial Institutions Survey showed positive momentum on OSFI’s performance in most areas across guidance, approvals and supervision. The Life Insurance Sector Consultation highlighted the transparent and collaborative approach that OSFI has established in its interactions, and commended OSFI on its efforts to consult on guidance development. Some areas for improvement were identified and, where appropriate, OSFI developed action plans to address these.

Neville Henderson, Assistant Superintendent, Insurance Supervision Sector • Michelle Doucet, Assistant Superintendent, Corporate Services Sector • Jeremy Rudin, Superintendent of Financial Institutions • Carolyn Rogers, Assistant Superintendent, Regulation Sector • Jamey Hubbs, Assistant Superintendent, Deposit-taking Supervision Sector

Summaries of the results of these surveys are available on OSFI’s website.

Benefits to Canadians

OSFI’s strategic outcomes, supported by our plans and priorities, are intrinsically aligned with broader government priorities. A properly functioning financial system makes a material contribution to Canada’s economic performance, and inspires a high level of confidence among consumers and others who deal with financial institutions.

9 OSFI ANNUAL REPORT 2016-2017

Federally Regulated Financial Institutions

Risk Assessment and Intervention

OSFI supervises federally regulated financial institutions (FRFIs), monitors the financial and economic environment to identify issues that may have a negative impact

on these institutions, and intervenes in a timely manner to protect depositors and policyholders from loss. In doing so, OSFI recognizes that management and boards of directors of FRFIs are ultimately responsible and that those institutions can fail.

In 2016-2017, sustained high levels of domestic household indebtedness, low interest rates, and ongoing global political and financial uncertainty continued to be seen as sources of potential systemic vulnerability. OSFI took action to address the possible impact of these challenges and achieve its strategic priorities. It communicated its expectations for risk management to FRFIs and conducted reviews in several areas. Areas under review included corporate and commercial lending, mortgage and other retail lending, risk data aggregation and risk reporting, risk management, and compliance. OSFI continued to develop supporting guidance for its Supervisory Framework and other programs to enhance its supervisory processes and tools.

Review by Sector

Deposit-taking Supervision

The Canadian deposit-taking industry is comprised of six large domestic banks designated as domestic systemically important banks (D-SIBs) and many smaller deposit-taking institutions (DTIs). The six largest banks account for about 90% of total assets held by federally regulated DTIs. Their diversified business lines extend beyond traditional deposit-taking and lending activities to trading, investment banking,

Colleen Ng Senior Supervisor, SMSB,Deposit-taking Supervision Sector

David Gourlay Manager, SMSB,Deposit-taking Supervision Sector

10 OSFI ANNUAL REPORT 2016-2017

wealth management and insurance. In addition to their primary domestic focus, these large banks operate in many countries around the world.

The remaining 10% of assets are held by small and medium-sized institutions with various market and business strategies, such as mortgage lending, commercial real estate lending and credit card lending.

OSFI fully implemented the Basel III capital rules in 2013, at which time banks began reporting new Common Equity Tier 1 (CET1) capital adequacy ratios. Canadian banks continued to report capital ratios well above the minimum CET1 requirements. The D-SIBs remained above the CET1 8% capital requirement (reflecting the 1% D-SIBs capital surcharge

requirement), while small and medium-sized banks reported capital ratios well above the target level of 7%.

Overall, return on equity for the industry was about 15% in 2016, similar to 2015, primarily due to continued solid net income generation and a mainly favourable credit environment. In the first half of 2016, some increase was observed in impairments and loan loss provisions due to the impacts of low oil prices; however, this moderated in the last two quarters of the year.

OSFI continued to closely monitor economic, financial and other risks facing deposit-taking institutions. One key risk is the potential that a pronounced economic downturn could lead to a meaningful housing price correction. This, in turn, could then translate into significant losses for lenders.

Mortgage rates have been at historically low levels for a number of years, which has led to significant increases in household debt, particularly mortgage debt. Recognizing the elevated financial risks and vulnerabilities facing financial institutions, OSFI advised the banking industry of tightened expectations and its intent to increase scrutiny around residential mortgage underwriting practices. OSFI took steps in 2016 to make capital requirements for residential mortgages more risk-sensitive, and to more accurately reflect market conditions.

Insurance Supervision

Life Insurance

The life insurance industry consists of three conglomerate institutions and more than 70 domestic companies and foreign branches. The conglomerates account for over 90% of the assets for the sector and have operations in Canada, the United States, Europe and Asia. They offer a broad range of wealth management, life and health insurance products through a number of distribution channels. The non-conglomerates are more restricted in product breadth and distribution.

The key metric used to assess capital adequacy for Canadian supervisory purposes is the Minimum Continuing Capital and Surplus Requirement (MCCSR) ratio. This metric is to be replaced by the Life Insurance Capital Adequacy Test (LICAT) ratio in January 2018.

The LICAT represents an evolution in OSFI’s regulatory capital expectations and is designed to take account of significant changes in the nature and management

Margarita Taqvi Principal Analyst, Common Supervisory Services, Deposit-taking Supervision Sector

Jenny Ge Actuarial Specialist, Actuarial Division,Insurance Supervision Sector

OSFI ANNUAL REPORT 2016-2017 11

of risk within the insurance industry. It improves the overall measurement of the quality of available capital and incorporates refined techniques in risk measurement.

OSFI released the final version of the LICAT guideline on September 12, 2016. Since then, life insurers have carried out a test run, performed sensitivity tests and developed implementation plans for a smooth transition.

The macro-economic environment has continued to be a challenge for life insurers since the 2008 financial crisis. Life insurers have ceased or reduced sales of products with high-risk market guarantees, de-risked and re-priced product offerings, increased their hedging of product risks, divested themselves of high-risk blocks of business, and strengthened their governance and risk management practices. As a result, life insurers have significantly decreased their sensitivity to interest rate and equity fluctuations.

Market volatility and persistently low interest rates have had an effect on in-force product profitability as investment yields have declined below yields anticipated when these products were originally priced. However, companies have set up additional balance sheet provisions to meet their future obligations to policyholders.

The aggregate capital ratio for the life insurance industry remains above OSFI’s minimum requirements but declined to 227% at year-end 2016, compared to 237% for 2015, driven largely by market impacts. The aggregate level has been well above OSFI’s minimum requirements for the last several years as companies built up capital in response to market volatility.

Return on equity for the industry was 10% and net income was $9.8 billion in 2016, compared to 9% and $8.8 billion, respectively, in 2015. About 75% of the industry’s net income is attributable to the three large conglomerates. The increases in net income and return on equity were largely due to favourable investment gains and credit experience, along with the strengthening of the U.S. dollar. Regardless of favourable financial results in 2016, challenges remain as persistently low interest rates make asset/liability management more difficult and strain in-force product profitability given that many products cannot be re-priced due to contractual provisions. OSFI is monitoring changes in risk policies to ensure companies adopt appropriate mitigation practices and controls if they move up the risk curve.

Property and Casualty Insurance (excluding mortgage insurance)

Catastrophes and weather-related losses continued to be a key risk for the property and casualty (P&C) insurance industry and a major driver of earnings volatility over the last year. The industry reported $1.5 billion of net income in 2016, a significant decline of 67% from the previous year, mainly as a result of catastrophe-related losses.

The 2016 wildfires in and around Fort McMurray, Alberta, are considered to be the costliest catastrophic event in Canadian history, resulting in about $4 billion of insured losses. While the event had a significant negative impact on industry profitability, most insurers have geographically diversified portfolios and adequate reinsurance strategies in place. Other catastrophes resulted in an additional $1 billion of losses in 2016, consistent with losses experienced in recent years.

A key measure of the industry’s core profitability is the ‘combined ratio,’ which measures the revenue from premiums relative to the sum of claims and expenses. A combined ratio under 100% indicates that underwriting profits as premium income exceed claims and expenses.

The P&C industry’s aggregated combined ratio deteriorated to 101% in 2016 from 96% in the previous year. Meanwhile, the low interest rate environment continues to impact the investment results as a significant portion of the investment portfolios are in bonds and debentures.

The Minimum Capital Test (MCT) is the capital metric for Canadian P&C insurance companies, while the Branch Adequacy of Assets Test (BAAT) is used for foreign-owned P&C branch operations in Canada. The industry continued to be well capitalized, with a relatively stable capital ratio of 269% in 2016, well above OSFI’s supervisory target of 150%.

OSFI is conducting an expanded review of industry reinsurance practices. The objective is to ensure that institutions appropriately balance their financial resources in Canada when compared to their insurance exposures, and have comprehensive risk management practices to avoid over-reliance on reinsurance and concentrated counterparty credit risks. OSFI plans to consult with the industry once its initial review has been completed. The review may result in revisions to existing OSFI guidelines.

12 OSFI ANNUAL REPORT 2016-2017

Mortgage Insurance

The mortgage insurance industry in Canada is composed of three participants: two private sector insurers regulated by OSFI, and the Canada Mortgage and Housing Corporation (CMHC), which is a Crown corporation also subject to OSFI oversight.

The private sector mortgage insurers continued to display improving financial performance during 2016, with total after-tax net income rising 10% to $539 million, reflecting higher earned premiums and stronger underwriting income. The average MCT capital ratio at year-end rose by seven points to 240%, which is above OSFI’s supervisory requirement of 150% and the companies’ planned operating level of 220%.

For CMHC, after-tax net income decreased by 6% to $1,183 million, reflecting lower earned premiums and a decrease in underwriting income, partly offset by an increase in investment earnings. CMHC’s MCT capital ratio at year-end rose by 30 points to 384%.

Despite the currently favourable financial results, the mortgage insurers remain vulnerable to rising consumer debt levels, the risk of a housing price correction in certain markets, and the potential employment impact given sustained low oil and gas prices in energy-producing regions of the country.

Supervisory Tools

Managing Risk Effectively

OSFI maintains internal assessment guidance to support its risk-based Supervisory Framework, which considers an institution’s inherent business risks, risk management practices (including corporate governance) and financial condition.

OSFI again held annual risk management seminars in 2016-2017 for the industries it regulates (DTIs, life insurance, P&C insurance and mortgage insurance) to reinforce the need for strong risk management and to share lessons learned. The goal of these seminars is to communicate OSFI’s expectations in key risk management areas based on detailed work OSFI has undertaken during the year, and to share information on issues being discussed internationally by regulators. The seminars also provide participants with the opportunity to ask questions of OSFI’s senior supervisory and regulatory teams.

Continuing the practice of holding Colleges of Supervisors, in 2016-2017 OSFI hosted a college for two of Canada’s five largest banks. In line with Financial Stability Board recommendations, the colleges bring together executives from Canadian banks with supervisors from jurisdictions where they do business. OSFI also hosted a supervisory college for a large life insurance company. In conjunction with the Canada Deposit Insurance Corporation, Crisis Management Groups (CMGs) were again held for two of the largest deposit-taking institutions.

Composite Risk Ratings

The Composite Risk Rating (CRR) represents OSFI’s overall assessment of an institution’s safety and soundness. There are four possible risk ratings: ‘low,’ ‘moderate,’ ‘above average’ and ‘high.’ The CRR is reported to most institutions at least once a year (certain inactive or voluntary wind-up institutions may not be rated). Supervisory information regulations prohibit institutions or OSFI from publicly disclosing their ratings. As at the end of March 2017, OSFI had assigned CRR ratings of low or moderate to more than 95%, and above average or high to less than 5% of all CRR-rated institutions.

Beginning in 2013-2014, a Branch Risk Rating (BRR) – rather than a CRR − was assigned to Foreign Bank Branches (FBBs) operating in Canada, thereby better reflecting OSFI’s approach to assessing the safety and soundness of FBBs.

Intervention Ratings

As described in OSFI’s guides to intervention for FRFIs, financial institutions are also assigned an intervention (stage) rating, which determines the degree of supervisory attention they receive. Broadly, these ratings are categorized as: normal (stage 0); early warning (stage 1); risk to financial viability or solvency (stage 2); future financial viability in serious doubt (stage 3); and non-viable/insolvency imminent (stage 4). As at March 31, 2017, there were 20 staged institutions. With a few exceptions, most of the staged institutions were in the early warning (stage 1) category.

Regulation and GuidanceOSFI provides a regulatory framework of guidance and rules that reflects international minimum standards for federally regulated financial institutions

OSFI ANNUAL REPORT 2016-2017 13

(FRFIs). In addition to issuing guidance, OSFI provides input to the development of federal legislation and regulations affecting FRFIs. It comments on accounting, auditing and actuarial standards development, including determining how to incorporate those standards in its regulatory framework. OSFI also participates in a number of international and domestic rule-making activities.

DOMESTIC RULE MAKING

Accounting, Auditing and Actuarial Standards

OSFI is a member of the Canadian Accounting Standards Board’s (AcSB) User Advisory Council and is an observer on its Insurance Accounting Task Force. With respect to auditing standards, OSFI is a non-voting member of the Auditing and Assurance Standards Oversight Council, which oversees the activities of the Canadian Auditing and Assurance Standards Board (AASB). OSFI also holds a seat on the Canadian Public Accountability Board (CPAB) Council of Governors, which carries out an annual high-level assessment of the CPAB against its mandate.

OSFI works closely with the Canadian Institute of Actuaries (CIA) and the Actuarial Standards Board (ASB) to ensure that actuarial standards are appropriate and lead to acceptable practice in areas such as valuation, risk and capital assessment at insurance and pension plan entities regulated by OSFI. In 2016-2017, we continued to participate on several CIA practice committees and joined the ASB designated group updating actuarial standards related to the implementation of the Life Insurance Capital Adequacy Test (LICAT).

In addition, through 2016-2017, OSFI agreed with the CIA to focus initial efforts on changes to the Dynamic Capital Adequacy Testing (DCAT) opinion as a way to better integrate DCAT with insurance companies’ Own Risk and Solvency Assessments (ORSA).

OSFI also works with the International Actuarial Association (IAA) and supports the profession by establishing guidance related to initiatives on insurance company valuation for International Financial Reporting Standards (IFRS), and the International Association of Insurance Supervisors’ (IAIS) Insurance Capital Standard (ICS).

Capital and Liquidity Guidance

Deposit-taking Institutions

During 2016-2017, OSFI amended its Capital Adequacy Requirements (CAR), the framework for assessing the capital adequacy of federally regulated deposit-taking institutions. This was done to introduce more risk sensitivity and to address greater uncertainty in housing collateral valuations when housing prices have been rising rapidly. These amendments came into effect in the first quarter of 2017 and helped ensure that capital requirements kept pace with developments in the Canadian mortgage market and were more sensitive to the underlying risks.

Julie Kennedy Manager, Approvals, Approvals and Precedents Division,Regulation Sector

Jeams Cherestal Correspondence Officer, Communications and Consultations Division, Corporate Services Sector

14 OSFI ANNUAL REPORT 2016-2017

OSFI also communicated its expectations to industry on the domestic implementation of two global capital adequacy standards issued by the Basel Committee in recent years.

Life Insurance Companies

In September 2016, OSFI published the guideline for the Life Insurance Capital Adequacy Test (LICAT). Effective January 1, 2018, the LICAT will replace the current insurance capital guideline, Minimum Continuing Capital and Surplus Requirements. The LICAT represents an evolution in OSFI’s regulatory

capital expectations and takes into account developments in life insurance accounting and actuarial standards, lessons from evolving capital frameworks in other jurisdictions, and the global financial crisis.

A test run took place in late 2016 whereby each life insurer assimilated the concepts of the LICAT and assessed its volatility. Test run results were received in January 2017 and may trigger further refinements and calibration adjustments to the LICAT prior to its effective date.

Property and Casualty Insurance Companies

The Property and Casualty (P&C) MCT Advisory Committee continued to develop a framework for the use of company-specific models to determine capital requirements for P&C insurance companies.

Mortgage Insurance Companies

A new regulatory capital framework for residential mortgage insurance came into effect in January 2017. Work to refine the framework, including the development of a separate capital guideline and reporting forms for mortgage insurers, will continue in 2017 and 2018, with implementation of these refinements planned for January 2019.

Other Guidance

Operational Risk Management

In June 2016, OSFI released the final version of its Operational Risk Management Guideline E-21, which sets out expectations regarding operational risk management for FRFIs using a principles-based approach. Full implementation of the principles within the guideline is expected to be achieved no later than June 2017.

Margin Requirements for Non-centrally Cleared Derivatives (E-22)

In February 2017, OSFI provided transitional relief to those FRFIs subject to the mandatory exchange of variation margin on non-centrally cleared derivatives effective March 1, 2017, based on the requirements of Guideline E-22. This guidance establishes minimum standards for the exchange of margin to secure performance on non-centrally cleared derivative transactions undertaken by covered entities. Given the global nature of the derivatives market,

Carole Carrière Translator-Editor, Communications and Consultations Division, Corporate Services Sector

Elizabeth Côté Senior Manager, Operational Risk DivisionRisk Support Sector

OSFI ANNUAL REPORT 2016-2017 15

OSFI acknowledged that a Canadian implementation schedule that recognizes the transitional measures taken in other major jurisdictions was appropriate.

Pillar 3 Disclosure Requirements

In August 2016, OSFI issued a letter on the deferred implementation of the revised Basel Pillar 3 standard to reporting periods ending in fiscal 2018. A final guideline will be issued in 2017 to provide clarification on the domestic implementation for FRFIs.

IFRS 9 Financial Instruments and Disclosures

In June 2016, OSFI issued the final guideline on IFRS 9 − Financial Instruments and Disclosures. The guideline outlines OSFI’s expectations for Federally Regulated Financial Institutions (FRFIs) regarding the application of IFRS 9, and is effective for reporting periods beginning in fiscal 2018.

Deferral of IFRS 9 for Federally Regulated Life Insurers

In March 2017, OSFI released a final advisory on the deferral of IFRS 9 for federally regulated life insurers. The advisory is in response to the September 2016 approval by the International Accounting Standards Board (IASB) of an amendment to IFRS 4 − Insurance Contracts. The amendment allows companies whose activities are predominantly connected with insurance to defer the application of IFRS 9 until January 1, 2021.

OSFI supports the improved standard IFRS 9 over the existing International Accounting Standard (IAS) 39 − Financial Instruments Standard. However, a deferral of IFRS 9 for life insurers is needed given the 2018 introduction of OSFI’s new Life Insurance Capital Adequacy Test (LICAT).

Anti-Money Laundering (AML) and Anti-Terrorism Financing (ATF)

During 2016-2017, OSFI continued its support of the Financial Action Task Force (FATF) standard-setting on money laundering/terrorist financing risks and risk management. At the international level, ongoing work to strengthen the financial system against money laundering and terrorism financing is led by the FATF. OSFI’s AML/ATF supervisory assessment program was reviewed by FATF as part of the mutual evaluation of Canada’s regime, and the report was released in September 2016. Overall, the message regarding

OSFI’s contribution to the Canadian AML/ATF regime was positive.

During 2016-2017, OSFI continued its AML/ATF supervisory assessment program and regular follow-up work at a wide variety of financial institutions. This was conducted collaboratively with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). During the year, OSFI continued discussions with FINTRAC to move to a more coordinated approach for onsite assessments.

OSFI monitors compliance by FRFIs with sanctions imposed on designated persons under the Criminal Code and United Nations Act regulations. Through its website, OSFI also continued its role as lead communicator in helping to ensure that the Canadian financial sector is promptly notified of sanctions imposed by the United Nations Security Council (UNSC) and the Government of Canada on terrorists and terrorist organizations, as well as UNSC sanctions against Iran and North Korea.

Compliance

Since the November 2014 revision of OSFI Guideline E-13 − Regulatory Compliance Management (RCM), financial institutions have improved their RCM frameworks. OSFI has seen demonstrable support for chief compliance officers in the provision of their opinions to boards, including verification of key information supporting their opinions.

INTERNATIONAL ACTIVITIESInternational organizations play a key role in the development of regulatory frameworks for banks and insurers. OSFI is an active participant in a number of these groups, including the Financial Stability Board, the Basel Committee on Banking Supervision, and the International Association of Insurance Supervisors.

Financial Stability Board (FSB)

The FSB was established in April 2009 to coordinate the work of national financial authorities and international standard-setting bodies. It develops and promotes the implementation of effective regulatory, supervisory and other financial sector policies.

Canadian representation on the FSB is shared among the Department of Finance, the Bank of Canada and OSFI. During 2016-2017, OSFI

16 OSFI ANNUAL REPORT 2016-2017

continued its involvement with the FSB through membership on the FSB Plenary, Steering Committee, and Standing Committee on Supervisory and Regulatory Cooperation.

Some of the work in which OSFI and its Canadian partners participated during 2016-2017 included:

• Releasing the final policy recommendations in January 2017 to address structural vulnerabilities in asset management activities;

• Leading the FSB Working Group on Corporate Governance Frameworks to address misconduct risk, with a view to determining whether the development of additional guidance or other supervisory tools is necessary;

• Developing a framework to guide post-implementation evaluations of the effects of

G20 reforms, with the aim of publishing the framework in July 2017; and

• Working to finalize implementation of G20 financial sector reforms, including in the areas of resolution regimes and over-the-counter derivatives.

Basel Committee on Banking Supervision (BCBS)

OSFI is an active member of the BCBS, which provides a forum for international rule-making and cooperation on banking supervisory matters.

In 2016-2017, a major area of focus for the BCBS was completing the final chapter of Basel III with a substantive set of proposals to reduce excessive variability in the calculation of minimum capital requirements across banks and across jurisdictions. G20 finance ministers have endorsed the BCBS use of the guiding principle that changes should not result in a significant increase in regulatory capital requirements for the global banking system as a whole. A Basel III standard for bank capital that increases risk sensitivity and reduces variability of estimate of risk has not achieved a final agreement. OSFI is preparing a plan for adopting elements of the draft standard that will improve domestic regulation of capital consistent with our principles for regulation and supervision.

International Accounting and Auditing Standards (IAIS)

As all FRFIs in Canada are required to follow International Financial Reporting Standards (IFRS) and International Standards on Auditing (ISA), OSFI interprets and assesses international rules that may apply to Canadian financial institutions. OSFI works with the International Accounting Standards Board (IASB) and International Auditing and Assurance Standards Board (IAASB) through active participation and leadership in the Accounting Experts Group of the BCBS and the Accounting and Auditing Working Group of the International Association of Insurance Supervisors (IAIS).

In 2016-2017, OSFI worked through the BCBS and IAIS to provide comments to the IAASB on projects of key interest, such as Enhancing Audit Quality in the Public Interest, Strategic Objectives and Work Plan for 2017-2018, and the development of revisions to ISA 540 − Auditing Accounting Estimates and Related Disclosures.

Janet Law Manager, Supervision Tools and Technology Renewal,Deposit-taking Supervision Sector

Robert DougallDirector, Risks, Surveillance, and Analytics Division,Risk Support Sector

OSFI ANNUAL REPORT 2016-2017 17

Active participation in the development of these initiatives promotes a set of high-quality global standards and enhances our understanding of key IFRSs and ISAs that impact FRFIs. Significant changes to accounting and auditing standards require early involvement and close consultation and communication with standard setters, other regulators and both international and domestic firms. OSFI collaborates closely with all stakeholders as key accounting and auditing standards are developed.

International Association of Insurance Supervisors (IAIS)

OSFI participates in the work of the IAIS, whose membership includes insurance regulators and supervisors from approximately 140 countries. IAIS objectives are to contribute to the improved supervision of the insurance industry for the protection of policyholders worldwide, to promote the development of well-regulated insurance markets, and to contribute to global financial stability.

OSFI is a member of the IAIS Executive Committee and the Financial Stability and Technical Committee, as well as the Supervisory Forum and several working groups. As an example, OSFI actively participates in the Capital Solvency and Field Testing Working Group and its many work streams that are tasked with developing the Insurance Capital Standard (ICS), which is a risk-based global insurance standard. The IAIS plans to issue the first version of the ICS and updated technical specifications for testing purposes in 2017. A second version of ICS is planned for completion in 2019.

Through its membership on the IAIS Accounting and Auditing Working Group, OSFI continues to monitor key developments and contribute to international policy work on issues of concern, such as the IASB’s insurance contracts project that will result in a final standard in mid-2017 called IFRS 17 − Insurance Contracts.

APPROVALS AND PRECEDENTSThe Bank Act, Trust and Loan Companies Act, Insurance Companies Act, and Cooperative Credit Associations Act require FRFIs to seek regulatory approval from the Superintendent or the Minister of Finance (after receiving the recommendation of

the Superintendent) prior to engaging in certain transactions or business undertakings.

Regulatory approvals are also required by persons wishing to incorporate a FRFI, and by foreign banks or foreign insurance companies wishing to establish a presence or make certain investments in Canada. OSFI administers a regulatory approval process that is prudentially effective, responsive and transparent. OSFI’s Approvals and Precedents Division is responsible for making recommendations to the Superintendent, and to the Minister of Finance, for those matters requiring regulatory approval.

In 2016-2017, OSFI processed 180 applications, of which 178 were approved and two were withdrawn. Individual applications often contain multiple approval requests. The 178 approved applications involved a total of 421 individual approvals, 268 of which were granted by the Superintendent and 153 by the Minister of Finance. The number of applications decreased slightly from the previous year, when 197 applications were approved. The majority of approved applications for 2016-2017 related to P&C insurers (36%) and banks (37%). (See figure 1)

FIGURE 1Approved Applications by Industry 2016-2017

70

60

50

40

30

20

10

0 Bank T&L/Coop* Life P&C

Num

ber

*Trust and Loan/Cooperative Associations

The most common applications received from deposit-taking institutions related to purchases or redemptions of shares or debentures, continuations, cancellations of representative office registrations, and acquisitions of ownership interests and/or control in entities. Applications received from insurance companies related mainly to reinsurance with related unregistered reinsurers, amendments to orders to commence and carry on business, for the insurance in Canada of risks, changes in ownership, and releases of assets.

18 OSFI ANNUAL REPORT 2016-2017

During 2016-2017, letters patent were granted to incorporate Brookfield Annuity Company as a life insurance company; to continue four entities as domestic banks − Exchange Bank of Canada, Street Capital Bank of Canada, Concentra Bank, and Caisse populaire acadienne ltée, a federal credit union; to continue two entities as federally regulated trust companies − Cidel Trust Company and TMX Equity Transfer and Trust Company (subsequently changing its name to TSX Trust Company); and to continue Toronto Police Widows and Orphans Fund as a federally regulated fraternal benefit society.

Orders for the insurance in Canada of risks were issued to Pacific Life Re Limited, CCR RE, Compañia Española de Seguros y Reaseguros de Crédito y Caución, S.A.U., and Wilton Re (Canada) Limited, establishing them as foreign insurance branches in Canada. An order authorizing the establishment of a foreign bank branch in Canada was issued to Sumitomo Mitsui Banking Corporation.

Upon request, OSFI also provides advance capital confirmations on the eligibility of proposed capital instruments. A total of 23 such opinions and validations were provided in 2016-2017, compared to 47 the previous year.

OSFI has performance standards establishing time frames for processing applications for regulatory approval and for other services, all of which were met during 2016-2017. More information on service performance standards can be found on OSFI’s website.

Guidance and Education

In keeping with the objective of enhancing the transparency of OSFI’s legislative approval process and promoting a better understanding of its interpretation of the federal financial institutions statutes, OSFI develops and publishes legislative guidance, including advisories, rulings, and transaction instructions. In 2016-2017, OSFI issued a guide for the continuance as a federal credit union and a ruling regarding the promotion of a “comprehensive credit insurance” policy by a bank. OSFI also issued revised versions of the guide for the continuance as a federal deposit-taking institution, and of the transaction instructions for assumption reinsurance and substantial investments approvals.

Megan TeeterHuman Resources Assistant, Human Resources Operations,Corporate Services Sector

Sean Walker Senior Manager, Deposit-taking Group – Conglomerates,Deposit-taking Supervision Sector

19 OSFI ANNUAL REPORT 2016-2017

Federally Regulated Private Pension Plans

when compared to the period ending in December 2015. The reason is that the overall solvency ratio at December 2016 was roughly equivalent to the December 2013 value that it replaces in calculating the three-year average.

The estimated solvency ratio (ESR) results suggest that federal defined benefit plans, as a whole, will not experience a significant increase in required contributions in 2017 compared to 2016; however, each plan will experience differences in their funding requirements for various reasons.

The Canadian group annuity market saw another increase, with total sales approaching close to $3.0 billion in 2016. This compares to total sales of $1.1 billion in 2012. In the past, annuity purchases were made mostly from plans that were terminated. But for the past few years, more than half of these group annuity purchases have been from ongoing pension plans. Many expect this trend to continue as employers and administrators continue to look for opportunities to transfer their pension risk.

Pooled Registered Pension Plans (PRPPs)The federal Pooled Registered Pension Plan Act (PRPP Act) and its associated regulations came into force in 2012. OSFI’s responsibilities with respect to this new type of pension plan include licensing PRPP administrators, registering PRPPs and providing ongoing supervision. At the end of 2016, there were four federally registered PRPPs (the same as at the end of 2015), with one reporting that it had entered into contracts with four employers and had enrolled 53 members (the total value of investments was $77,295.)

OSFI supervises federally regulated private pension plans and protects pension plan members and other beneficiaries by developing guidance on risk management

and mitigation, assessing whether private pension plans are meeting their funding requirements and managing risks effectively, and intervening promptly when corrective actions need to be taken. OSFI holds pension plan administrators ultimately responsible for sound and prudent management of their plans.

Approximately 7% of private pension plans in Canada are federally regulated (Statistics Canada data as at January 2016). As at March 31, 2017, 1,230 private pension plans were registered under the Pension Benefits Standards Act, 1985, covering more than 1,119,000 active members and other beneficiaries in federally regulated areas of employment, such as banking, inter-provincial transportation and telecommunications. Between April 1, 2016, and March 31, 2017, federally regulated private pension plan assets increased by 4%, to a value of approximately $206 billion (see figure 2).

Private Pension Plan Environment

The overall solvency position of federally registered pension plans improved slightly from 2015. This improvement reflected the positive effects on plan assets of strong returns on equity investments, dampened somewhat by the impact of lower interest rates, which have the effect of increasing plan liabilities. Federal solvency funding requirements are based on a plan’s three-year average solvency position. Despite the noted small improvement in the overall solvency position in 2016, the three-year average solvency ratio for federal defined benefit pension plans, as a whole, did not change for the period ending in December 2016

20 OSFI ANNUAL REPORT 2016-2017

2014 20152 20162 20172

Total Plans 1,234 1,226 1,233 1,230

Defined Benefit 329 317 306 294

Combination 117 118 124 126

Defined Contribution 788 791 803 810

Total Active Membership 639,000 631,000 631,000 624,000

Defined Benefit 293,000 283,000 251,000 244,000

Combination 222,000 220,000 249,000 250,000

Defined Contribution 124,000 128,000 131,000 130,000

Total Other Beneficiaries 430,000 445,000 479,000 495,000

Defined Benefit 232,000 233,000 238,000 247,000

Combination 183,000 195,000 224,000 230,000

Defined Contribution 15,000 17,000 17,000 18,000

Total Assets $171 billion $189 billion $198 billion $206 billion

Defined Benefit $90 billion $99 billion $99 billion $102 billion

Combination $76 billion $84 billion $92 billion $97 billion

Defined Contribution $5 billion $6 billion $7 billion $7 billion

1 Some defined benefit and combination plans were reclassified in 2016. Figures for prior years are restated for comparison purposes. 2 Does not include Pooled Registered Pension Plans (five in 2015, four in 2016 and in 2017).

FIGURE 2Federally Regulated Private Pension Plans by type as at March 31, 2016 (last 4 years)1

Representatives of the governments of Canada, British Columbia, Nova Scotia, Ontario, Quebec and Saskatchewan have signed a Multilateral Agreement Respecting Pooled Registered Pension Plans and Voluntary Retirement Savings Plans (PRPP Agreement). An earlier version of this agreement was signed by these jurisdictions (except Ontario), effective June 15, 2016. Ontario became a signatory to the PRPP Agreement on March 31, 2017, following the implementation of Ontario’s PRPP legislation.

The PRPP Agreement is intended to streamline the regulation and supervision of PRPPs that are subject to the federal PRPP Act and the PRPP legislation of at least one province participating in the agreement. The PRPP Agreement effectively delegates to OSFI responsibility for licensing, registering and supervising PRPPs whose operations fall within the jurisdiction of both the federal government and the participating provinces. The PRPP Agreement does not give OSFI responsibility with respect to the Quebec Voluntary Retirement Savings Plan (VRSP), but permits authorized VRSP

administrators to act as PRPP administrators under the federal PRPP Act if they register a PRPP federally.

The Assessment of Pension Plans Regulations, made pursuant to the Office of the Superintendent of Financial Institutions Act, were amended, effective October 21, 2016, to provide for the recovery of expenses from PRPPs by way of annual assessments of PRPPs. For purposes of calculating annual assessments, PRPPs are subject to the same assessment formula and basic rate as pension plans subject to the Pension Benefits Standards Act, 1985.

Risk Assessment, Supervision and InterventionIn 2016-2017, OSFI continued to focus on prudent and effective risk management given the ongoing challenging economic environment.

OSFI’s Risk Assessment System for Pensions (RASP) analyses information from pension plan

OSFI ANNUAL REPORT 2016-2017 21

filings, submitted via the Regulatory Reporting System (RRS), and other sources. Key risk indicators are generated for each federally regulated private pension plan registered with OSFI, thereby enabling early identification of issues. In order to ensure a better coordination of information between RASP and RRS, OSFI made significant upgrades to RASP in 2016-2017. OSFI also reviewed many of the procedures and risk assessment tools used during the supervisory process to strengthen our risk-based approach to supervision.

During 2016-2017, OSFI continued to examine how the supervision of plans with defined contribution provisions may be improved. In 2017-2018, OSFI will pay particular attention to pension plans with defined contribution provisions, by way of examinations, to gauge the trends in the default investment accounts and the adequacy of information relating to fee disclosure.

Solvency Testing

OSFI estimates solvency ratios (the ratio of assets over liabilities on a plan termination basis) for the defined benefit pension plans it regulates. At December 31, 2016, the estimated solvency ratio (ESR) for all plans was 0.97, up from 0.95 at year-end 2015 (see figure 3). ESRs calculated by OSFI at year-end 2016 showed that approximately 80% of all defined benefit pension plans supervised by OSFI were under-funded (compared to 79% at year-end 2015), meaning that their estimated liabilities exceeded assets, on a plan termination basis. There has been a decrease in the number of plans that are more significantly under-funded (ESRs below 0.80) from 19% at the end of 2015 to 16% at the end of 2016.

Examinations

As part of its risk-based supervisory approach, OSFI conducts examinations of select federally regulated private pension plans. During 2016-2017, OSFI performed nine examinations. The examinations may be limited to a desk review or could be conducted on the plan administrator’s premises (onsite examinations). During onsite examinations, OSFI reviews more thoroughly the plan administrator’s processes by interviewing those involved in the administration of the pension plan. The objectives of an examination are to gather additional information and to better assess the plan’s quality of risk management.

FIGURE 3Defined Benefit Plans’ Estimated Solvency Ratio (ESR) Distribution (past 10 years)

Estimated Sovency Ration (ESR)

1.10

1.05

0.90

0.80

0.70

The ESR increased from 0.95 to 0.97 since year-end 2015.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Watch List

Pension plans facing higher risk − due to their financial condition, plan management or other reasons − are placed on a watch list and actively monitored. At March 31, 2017, 30 plans were on the watch list (the same as March 31, 2016). Of the 30 plans, 23 were defined benefit plans and seven were defined contribution plans. During 2016-2017, 16 plans were removed from the watch list while 16 new plans were added.

Intervention

OSFI strives to protect members’ benefits through cooperation with plan administrators and employers before exercising its powers to enforce legislative requirements. In 2016-2017, OSFI interventions with respect to high-risk pension plans included issuing a notice of intent to issue a direction of compliance to two employers, which successfully resulted in the remittance of outstanding contributions. In addition, the Superintendent appointed a replacement administrator for one plan.

Rules and Guidance

Proposed amendments to the Pension Benefits Standards Act, 1985, (PBSA) to introduce Target Benefit Plans

On October 19, 2016, the government tabled Bill C-27, which included proposed amendments to the PBSA that

22 OSFI ANNUAL REPORT 2016-2017

establish a legislative framework for the establishment and operation of federally-registered target benefit pension plans. Target benefit pension plans are intended to provide plan members with lifetime pension benefits at a “target” level, based on a pre-determined formula (like a defined benefit pension plan), while providing a degree of flexibility to adjust benefit levels in response to unexpected changes in key factors, such as long-term interest rates, investment returns and longevity. Bill C-27 must receive Royal Assent and regulations will need to be enacted before a target benefit plan framework can be implemented.

Bill C-27 also included proposed amendments to the PBSA to provide that, subject to certain conditions, if a pension plan purchases immediate or deferred annuities to provide payments to former members or survivors equal to what those members would be entitled to receive as pension benefits from the plan, then the pension plan’s obligation to those members is considered to be satisfied. The proposed amendments are intended to support the purchase of annuities by pension plans as an optional means of providing secure retirement income.

The final round of amendments to the Pension Benefits Standards Regulations, 1985, to implement pension reforms announced in 2009, included a number of changes that came into force on July 1, 2016. This final round of changes included expanded requirements on plan administrators to provide information to members and former members, as well as changes to the investment rules for pension funds. Through its website and regular InfoPensions newsletter, OSFI has provided up-to-date information on the status of changes to the federal pension legislation and its regulations.

Guidance

In keeping with the objectives of promoting prudent practices and a transparent regulatory framework, OSFI regularly provides guidance to plan administrators on legislative requirements and OSFI’s expectations.

In October 2016, OSFI issued various guidance aimed at providing Pooled Registered Pension Plan (PRPP) administrators, and those interested in becoming PRPP administrators, with more detailed information on the various processes and approvals required to establish and operate a PRPP. These include a PRPP licensing guide and PRPP registration guide, as well as updated PRPP frequently-asked questions covering a wide range of topics. A Standardized Termination Report for PRPPs was also issued in October 2016, and in March 2017, OSFI posted a PRPP annual information return and accompanying guide to assist with its filing.

OSFI also issued updated guidance to reflect changes that have been made to relevant provisions of the PBSA and the Regulations since the guidance was last issued. The updated guidance issued in 2016-2017 includes disclosure guides for both defined benefit and defined contribution pension plans, and guidance on Amendments to the Related Party Rules in the Regulations. In October 2016, OSFI issued a revised Instruction Guide for the Preparation of Actuarial Reports

Ayoub MachkourActuarial Officer, Public Pensions,Office of the Chief Actuary

Krista McAlister Manager, Private Pension Plans Division, Regulation Sector

OSFI ANNUAL REPORT 2016-2017 23

for Defined Benefit Pension Plans, which sets out the requirements for actuarial reports filed with OSFI for pension plans with defined benefit provisions.

InfoPensions

OSFI published its bi-annual newsletter, InfoPensions, in May and November 2016. The newsletter includes announcements and reminders on issues relevant to administrators of federally regulated private pension plans, pension advisors and other stakeholders. It also includes descriptions of how OSFI applies select provisions of the pension legislation and OSFI guidance. OSFI regularly consults with its stakeholders to ensure that we are communicating effectively and continues to look for ways to ensure that InfoPensions is highly readable, accessible and relevant.

Approvals

Federally regulated private pension plans are required to seek approval from the Superintendent for several types of transactions. These include plan registrations and terminations, asset transfers between registered defined benefit pension plans, refunds of surplus, and reductions of accrued benefits. The number of pension transactions submitted to the Superintendent for approval decreased to 64 in 2016-2017 from 73 in 2015-2016. OSFI processed 64 applications for approval in 2016-2017, compared to 60 applications in 2015-2016. In 2016-2017, 29 new plans were registered by OSFI (10 defined benefit plans and 19 defined contribution plans), while 14 plan termination reports were approved (11 defined benefit plans and three defined contribution plans).

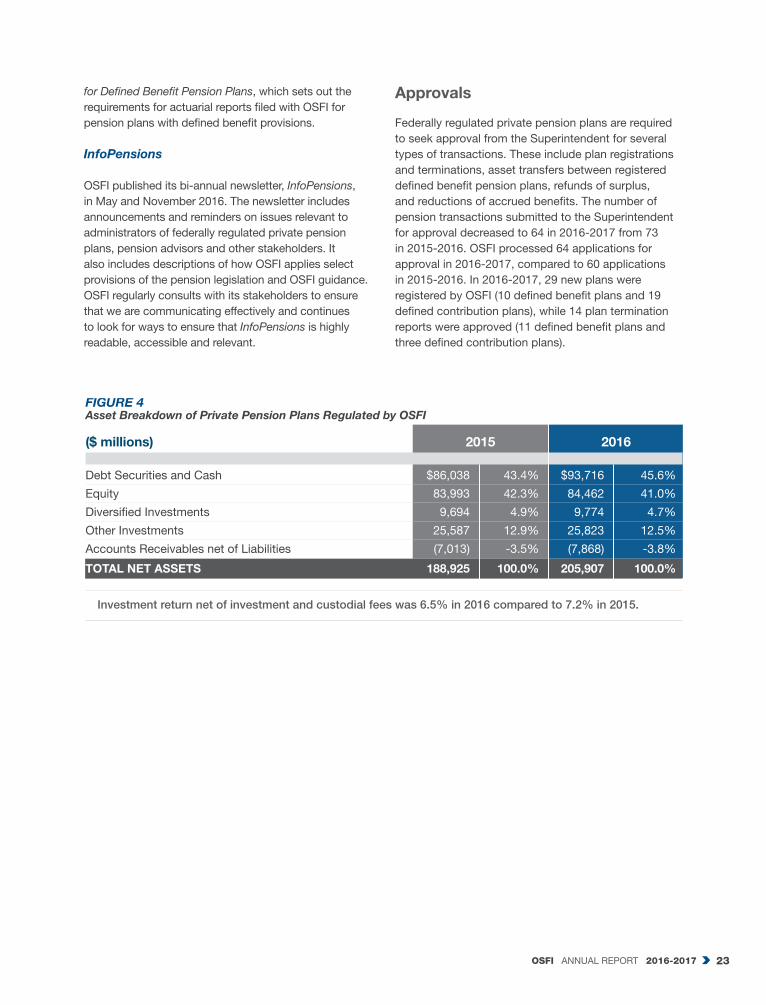

FIGURE 4Asset Breakdown of Private Pension Plans Regulated by OSFI

($ millions) 2015 2016

Debt Securities and Cash $86,038 43.4% $93,716 45.6%

Equity 83,993 42.3% 84,462 41.0%

Diversified Investments 9,694 4.9% 9,774 4.7%

Other Investments 25,587 12.9% 25,823 12.5%

Accounts Receivables net of Liabilities (7,013) -3.5% (7,868) -3.8%

TOTAL NET ASSETS 188,925 100.0% 205,907 100.0%

Investment return net of investment and custodial fees was 6.5% in 2016 compared to 7.2% in 2015.

24 OSFI ANNUAL REPORT 2016-2017

Office of the Chief Actuary

The Office of the Chief Actuary (OCA) contributes to a financially sound and sustainable Canadian public retirement income system through the provision

of expert actuarial valuation and advice to the Government of Canada and to provincial governments that are Canada Pension Plan (CPP) stakeholders.

The OCA provides statutory actuarial valuation and advisory services for the CPP, Old Age Security (OAS) program, the Canada Student Loans program, Employment Insurance program, and pension and benefits plans covering the federal public service, the Canadian Forces, the Royal Canadian Mounted Police, federally appointed judges, and members of Parliament.

The OCA was established within OSFI as an independent unit. The fact that the OCA is hosted by OSFI ensures its independence and impartiality are beyond question. The Chief Actuary reports to the Superintendent; however, the accountability framework of the OCA makes it clear that its staff is solely responsible for actuarial advice provided.

Tabling of the 27th Actuarial Report on the Canada Pension Plan The OCA is required by law to produce an actuarial report on the Canada Pension Plan every three years. The 27th Actuarial Report on the CPP as at 31 December 2015 was tabled before Parliament on September 27, 2016. Prepared by the OCA, this triennial actuarial report on the CPP involves projections of CPP revenues and expenditures over the 75-year projection period, so that the future impact of historical and projected trends on demographic and economic factors can be properly assessed.

Jean-Claude MénardChief Actuary

25 OSFI ANNUAL REPORT 2016-2017

The CPP provides protection to millions of Canadian workers and their families against the loss of income due to retirement, disability and death. In 2016, more than six million Canadians received CPP benefits, with a total value of approximately $41 billion. Canadians want to feel confident that the CPP will be able to meet their needs in future years. The actuarial report provides Canadians with the most recent information on the financial status of the Plan.

The actuarial report finds that under the 9.9% legislated contribution rate, the assets are projected to increase significantly over the near term, reaching $476 billion by the end of 2025. This is because the contribution revenue is expected to exceed expenditures over that period. Assets will continue to grow thereafter until the end of the projection period, but at a slower pace, reaching a level of 7.3 years of annual Plan expenditures by 2050. Thus, despite the projected substantial increase in benefits paid as a result of an aging population, the CPP is expected to be able to meet its obligations throughout the projection period and to remain financially sustainable over the long term.

External Peer Review of the 27th CPP Actuarial ReportThe OCA commissioned an external peer review of the 27th CPP Actuarial Report. First introduced in 1999, the external peer review of actuarial reports by an independent panel of reviewers is intended to ensure that actuarial reports meet high professional standards and are based on reasonable assumptions in order to provide sound actuarial advice to Canadians.

The independent panel’s findings confirm that the work performed by the OCA on the 27th CPP Actuarial Report meets professional standards of practice and statutory requirements, and that the assumptions and methods used are reasonable. The panel also stated that the report fairly communicates the results of the work performed by the Chief Actuary and his staff.

The external peer review of the 27th CPP Actuarial Report is public, as were previous peer reviews of the CPP actuarial reports, and is available on the OSFI website.

Tabling of the 28th Actuarial Report on the Canada Pension Plan On June 20, 2016, the federal and provincial ministers of finance agreed in principle to a CPP enhancement,

with a target replacement rate for additional retirement benefits of 8.33% of the adjusted career-average earnings below the Year’s Maximum Pensionable Earnings (YMPE), and 33.33% on adjusted career-average earnings between the YMPE and 114% of the YMPE. These enhancements are to be financed with the first additional combined employer-employee contribution rate of 2.0% applied on earnings between the Year’s Basic Exemption and the YMPE, and the second additional contribution rate of 8.0% applied on earnings between 100% and 114% of the YMPE.

Bill C-26, formalizing this agreement, was introduced in Parliament in October 2016. In compliance with the Canada Pension Plan, the 28th Actuarial Report Supplementing the Actuarial Report on the Canada Pension Plan as at 31 December 2015 (the 28th CPP Actuarial Report) has been prepared on the basis of the 27th CPP Actuarial Report to show the effect of Bill C-26 on the long-term financial state of the CPP. This report was tabled before Parliament on October 28, 2016.

The 28th CPP Actuarial Report confirms that legislated first and second additional contribution rates result in projected contributions and investment income that are sufficient to fully pay the projected expenditures of the additional Plan over the long term.

The report projects that under the legislated additional contribution rates, assets of the additional CPP are expected to increase rapidly over the first several decades as contributions are projected to exceed expenditures. The additional CPP assets are projected to grow from $1.5 billion at the end of 2019 to $70 billion by 2025, $196 billion by 2030, and $1,330 billion by 2050. As investment income will become the major source of revenues for the additional Plan, the additional contribution rates will become highly sensitive to financial market environments.

Tabling of the 13th Actuarial Report on the Old Age Security ProgramThe legislation following proposals in the 2016 federal budget has restored the age of eligibility for OAS benefits to age 65, and has increased the Guaranteed Income Supplement top-up benefit for the most vulnerable single seniors.

In compliance with Public Pensions Reporting Act, the OCA has prepared the 13th Actuarial Report Supplementing the Actuarial Report on the Old Age

26 OSFI ANNUAL REPORT 2016-2017

Security Program as at 31 December 2012, which was tabled before Parliament on August 17, 2016.

This report has found that the above amendments are projected to increase total OAS program expenditures by $11.6 billion by 2030, which represents an increase of 0.33% of GDP.

Public Sector Insurance and Pension Plans In 2016-2017, the OCA completed three actuarial reports with respect to public sector insurance and pension plans, which were submitted to the President of the Treasury Board for tabling before Parliament: The Actuarial Report on the Pension Plan for the Canadian Forces − Reserve Force, as at 31 March 2015, was tabled on November 25, 2016; the Actuarial Report on the Pension Plan for the Royal Canadian Mounted Police, as at 31 March 2015, was tabled on November 4, 2016; and the Actuarial Report on the Benefit Plan Financed Through the Royal Canadian Mounted Police (Dependants) Pension Fund, as at 31 March 2016, was tabled on January 18, 2017. These reports provide actuarial information to decision makers, parliamentarians and the public, thereby increasing transparency and confidence in Canada’s retirement income system.

Actuarial Report on the Employment Insurance Premium Rate