1 SEPTEMBER 2018 ISSUE 5 SST IMPLEMENTATION. WHAT YOU SHOULD KNOW. Further to the Royal Assent on 24 August 2018, the long awaited SST Acts and its supporting supplementary orders has been gazetted on 28 August 2018. However, there are still plenty of uncertainties in the market whether I am subject to SST? How do I submit my SST Return? Will that impact my pricing? How should I change my invoice format? If I am not automatically registered under SST, when should I register? Businesses, Entrepreneurs, Professionals and Management has given very little time to implement SST. In addition, with the dynamic changes of SST scope, guides and rules, it is a very challenging task. This update aims to help you gain a very quick understanding as to how the new tax is going to work. What are the scopes and most frequently asked questions. Copyright ANC Hub Consultants – September 2018 ANC TAXLETTER Check out our Facebook Our Latest Videos

Transcript

1 SEPTEMBER 2018 ISSUE 5

SST IMPLEMENTATION. WHAT YOU SHOULD KNOW.

Further to the Royal Assent on 24 August 2018, the long awaited SST Acts and its supporting supplementary orders has been gazetted on 28 August 2018. However, there are still plenty of uncertainties in the market whether I am subject to SST? How do I submit my SST Return? Will that impact my pricing? How should I change my invoice format? If I am not automatically registered under SST, when should I register?

Businesses, Entrepreneurs, Professionals and Management has given very little time to implement SST. In addition, with the dynamic changes of SST scope, guides and rules, it is a very challenging task.

This update aims to help you gain a very quick understanding as to how the new tax is going to work. What are the scopes and most frequently asked questions.

Copyright ANC Hub Consultants – September 2018

ANC TAXLETTER Check out our FacebookOur Latest Videos

Companies registered under GST which were identified and fulfilled the required criteria will be registered automatically as registered service tax provider. But, how do I check? Follow the simple instruction below:-

1. If you are automatically registered as a SST registrant, you shall charge SST commencing 1 September 2018 onwards. However, if you found out that you are not supposed to register under the SST, under various circumstances such as incorrect MSIC code, not exceeding threshold, not supplying taxable goods or services etc, you will need to de-register. The checklist for de-registering is as follows:-

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

2. If you fulfilled the required criteria to be a SST registered person, but not automatically registered, you need to register by 30 September 2018.

QUESTION 2 : ARE YOU SUBJECT TO SALES TAX?

5% or 10% (depending on which taxable goods) is levied on importers and manufacturers. However, such sales tax may be exempted under the circumstances below. Refer illustration and links provided.

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

QUESTION 3 : ARE YOU SUBJECT TO SERVICE TAX?

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

Service Tax is levied on taxable services and those who are not in the list is exempted from service tax. Compared to the old Service Tax 1975, the scope of service tax has been expanded to include provision of IT services, electricity, domestic flights and gaming providers. It is also noteworthy that the Ministry of Finance has recently increased the threshold of Food and Beverage Providers to RM1,500,000 (from the previous RM1,000,000).

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

QUESTION 4 : HOW DO I CALCULATE MY SST THRESHOLD

Unlike GST, SST threshold is calculated based on value of taxable goods and taxable services where the value exceeds RM500,000 or any specified threshold for 12 months’ period. If a company provides both taxable goods and taxable services which exceeded both thresholds, the aforesaid Company will have to register for both.

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

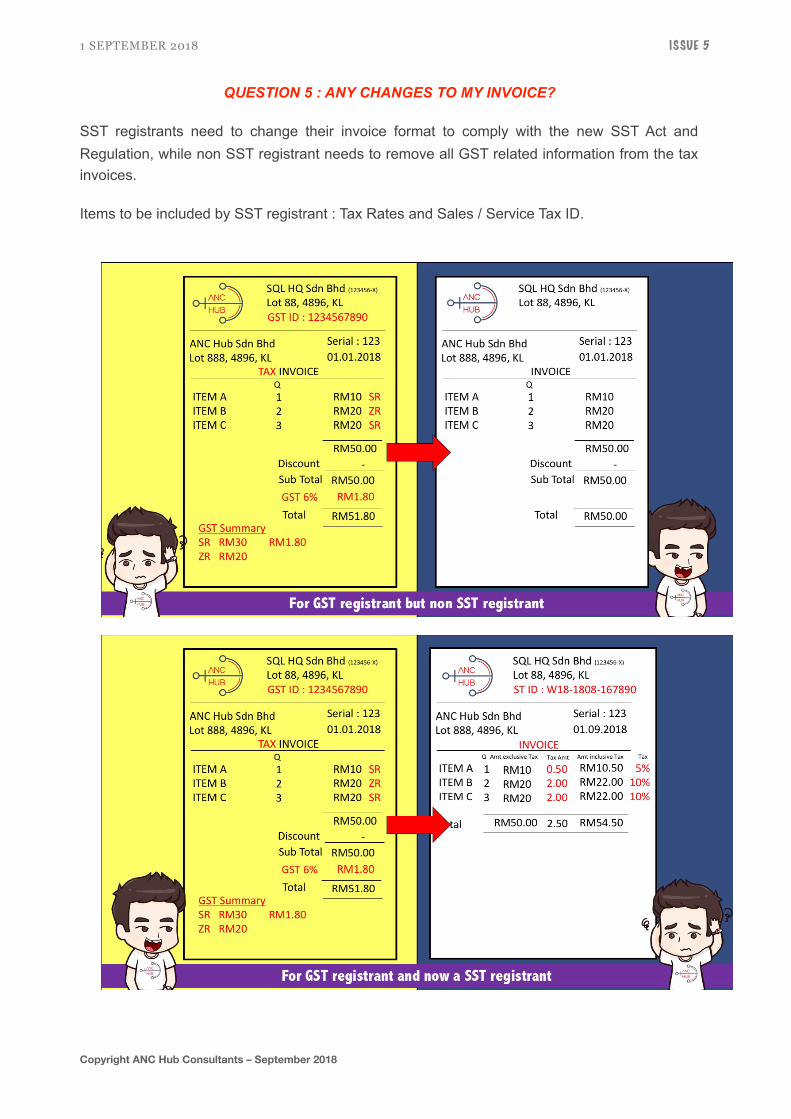

QUESTION 5 : ANY CHANGES TO MY INVOICE?

SST registrants need to change their invoice format to comply with the new SST Act and Regulation, while non SST registrant needs to remove all GST related information from the tax invoices.

Items to be included by SST registrant : Tax Rates and Sales / Service Tax ID.

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

Particulars required under SST Regulations

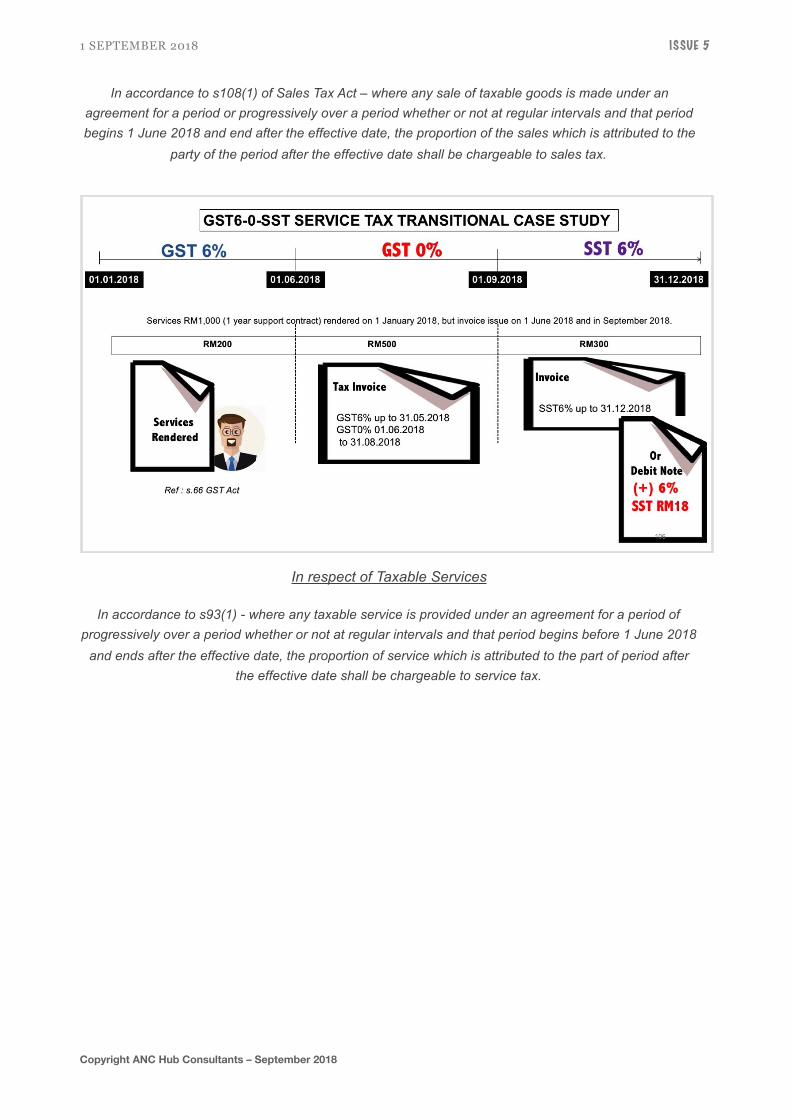

QUESTION 6 : TRANSITIONAL RULES FOR 6-0-SST

In respect of Taxable Goods

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

In accordance to s108(1) of Sales Tax Act – where any sale of taxable goods is made under an agreement for a period or progressively over a period whether or not at regular intervals and that period begins 1 June 2018 and end after the effective date, the proportion of the sales which is attributed to the

party of the period after the effective date shall be chargeable to sales tax.

In respect of Taxable Services

In accordance to s93(1) - where any taxable service is provided under an agreement for a period of progressively over a period whether or not at regular intervals and that period begins before 1 June 2018

and ends after the effective date, the proportion of service which is attributed to the part of period after the effective date shall be chargeable to service tax.

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

QUESTION 7 : WHEN IS THE LAST GST RETURN?

Pursuant to s.6 of GST (Repeal) Act 2018, all GST registrants are required to submit their GST-03 Return in the final taxable period and make full payment for the amount of tax payable in connection with the supply, for the last period within 120 days from 01.09.2018. Please refer to the illustrations below:-

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

Copyright ANC Hub Consultants – September 2018

1 SEPTEMBER 2018 ISSUE 5

Copyright ANC Hub Consultants – September 2018

This highlight is provided gratuitously and without liability. It is intended as a general guide only. Readers should seek appropriate professional advice regarding any particular problems they encounter. Accordingly, Anc Hub Consultants PLT assumes no responsibility for any errors or omissions it may contain, whether caused by negligence or otherwise, or any losses, however caused, sustained by any person that relies on it. For further information, clarification or advice on any of the contents stated herein, please feel free to contact our team.

Song Liew CA(M), ACTIM(M), ACCA(UK)

Managing Partner of ANC Hub Consultants MYGCAP Reviewer and Tax Consultant Certified HRDF Trainer