27

Outreach on the Affordable Care Act to Farm Families in Wisconsin Heidi Johnson Dane County University of Wisconsin- Extension Crops and Soils Agent

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | alexander-white |

| View: | 219 times |

| Download: | 2 times |

Outreach on the Affordable Care Act to

Farm Families in Wisconsin

Heidi JohnsonDane County University of Wisconsin-Extension

Crops and Soils Agent

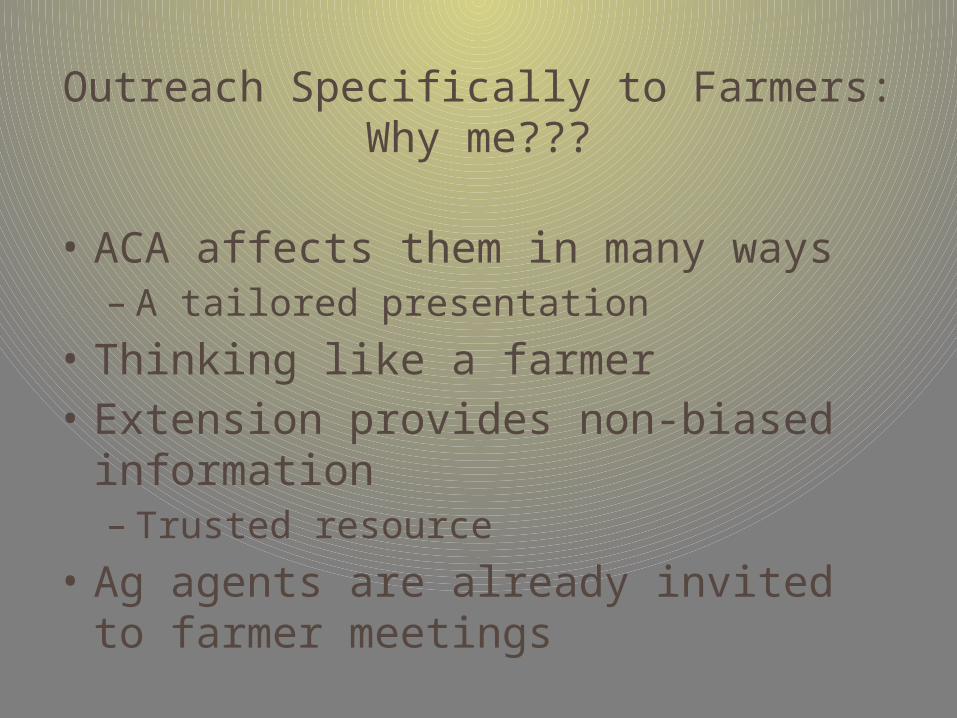

Outreach Specifically to Farmers:Why me???

• ACA affects them in many ways – A tailored presentation

• Thinking like a farmer• Extension provides non-biased

information– Trusted resource

• Ag agents are already invited to farmer meetings

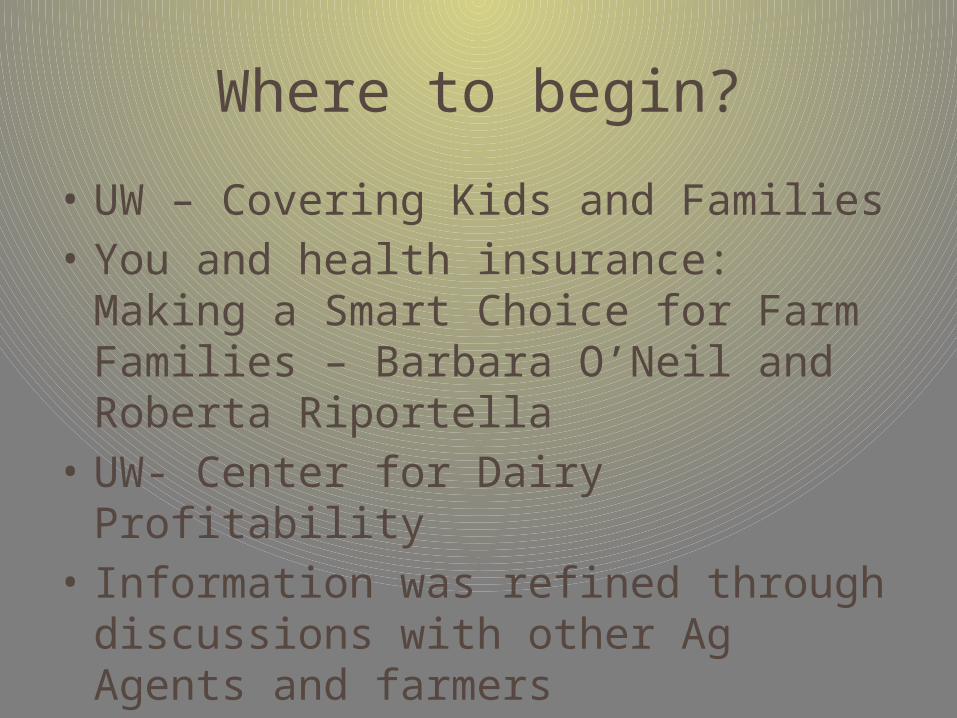

Where to begin?

• UW – Covering Kids and Families• You and health insurance: Making a

Smart Choice for Farm Families – Barbara O’Neil and Roberta Riportella

• UW- Center for Dairy Profitability• Information was refined through

discussions with other Ag Agents and farmers

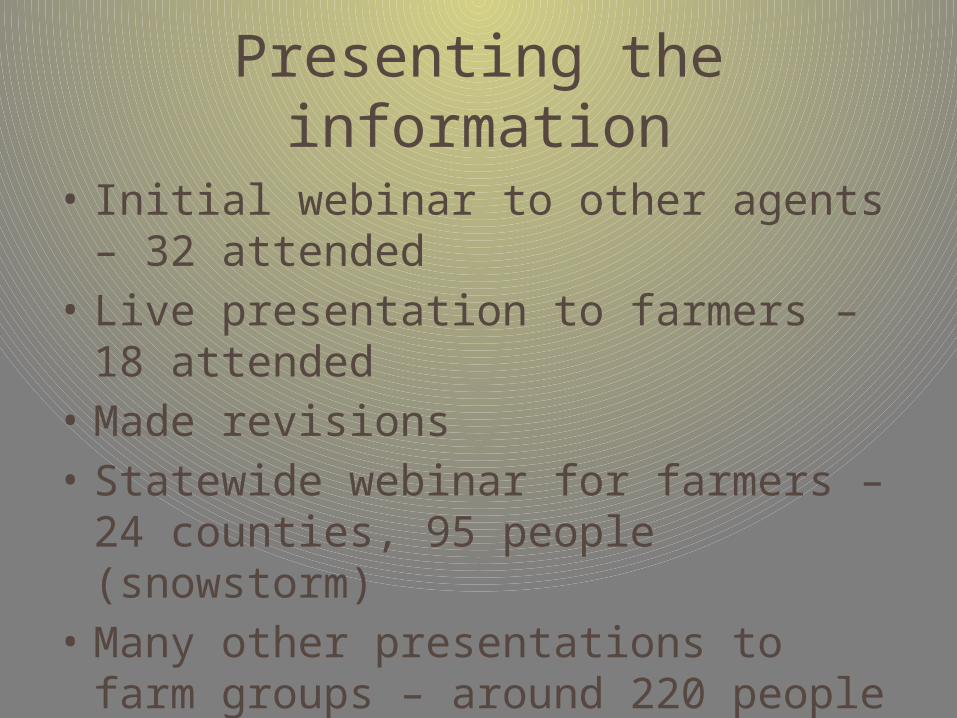

Presenting the information

• Initial webinar to other agents – 32 attended

• Live presentation to farmers – 18 attended

• Made revisions• Statewide webinar for farmers – 24

counties, 95 people (snowstorm)• Many other presentations to farm

groups – around 220 people• 3 major ag papers wrote long

features

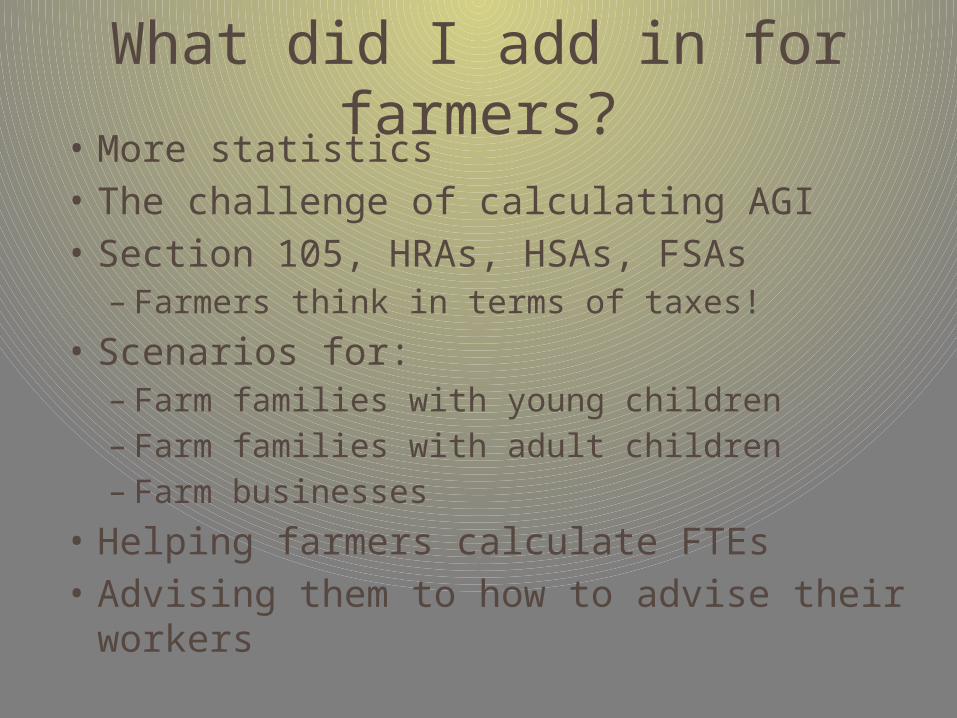

What did I add in for farmers?

• More statistics• The challenge of calculating AGI• Section 105, HRAs, HSAs, FSAs– Farmers think in terms of taxes!

• Scenarios for:– Farm families with young children– Farm families with adult children– Farm businesses

• Helping farmers calculate FTEs• Advising them to how to advise their

workers

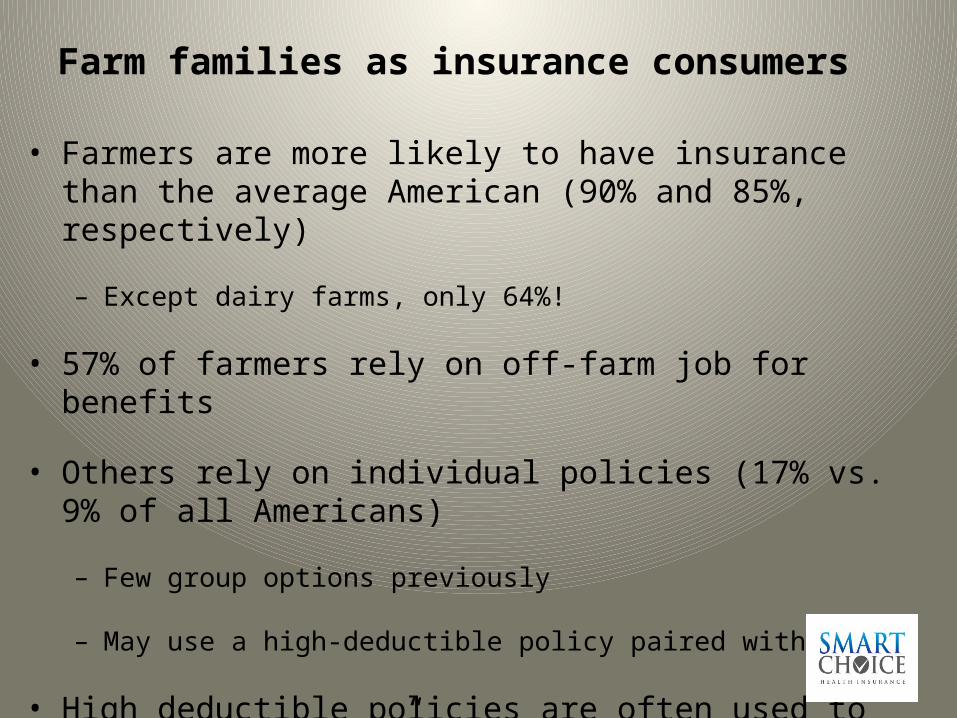

Farm families as insurance consumers

• Farmers are more likely to have insurance than the average American (90% and 85%, respectively)

– Except dairy farms, only 64%!

• 57% of farmers rely on off-farm job for benefits

• Others rely on individual policies (17% vs. 9% of all Americans)

– Few group options previously

– May use a high-deductible policy paired with a HSA

• High deductible policies are often used to “protect the farm”

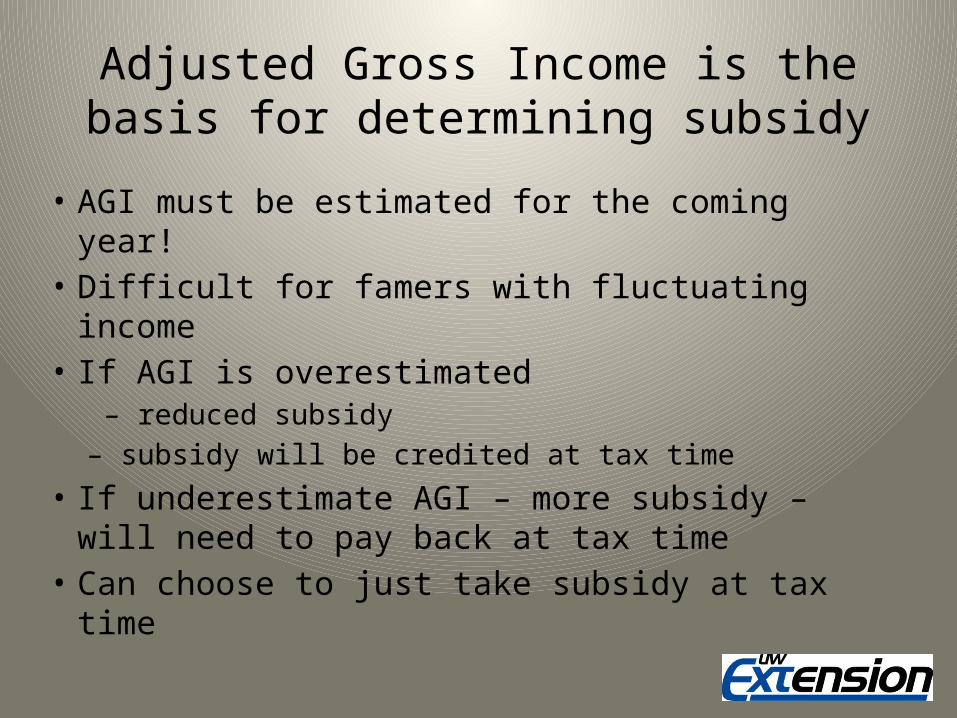

Adjusted Gross Income is the basis for determining subsidy

• AGI must be estimated for the coming year!• Difficult for famers with fluctuating income• If AGI is overestimated

– reduced subsidy – subsidy will be credited at tax time

• If underestimate AGI – more subsidy – will need to pay back at tax time

• Can choose to just take subsidy at tax time

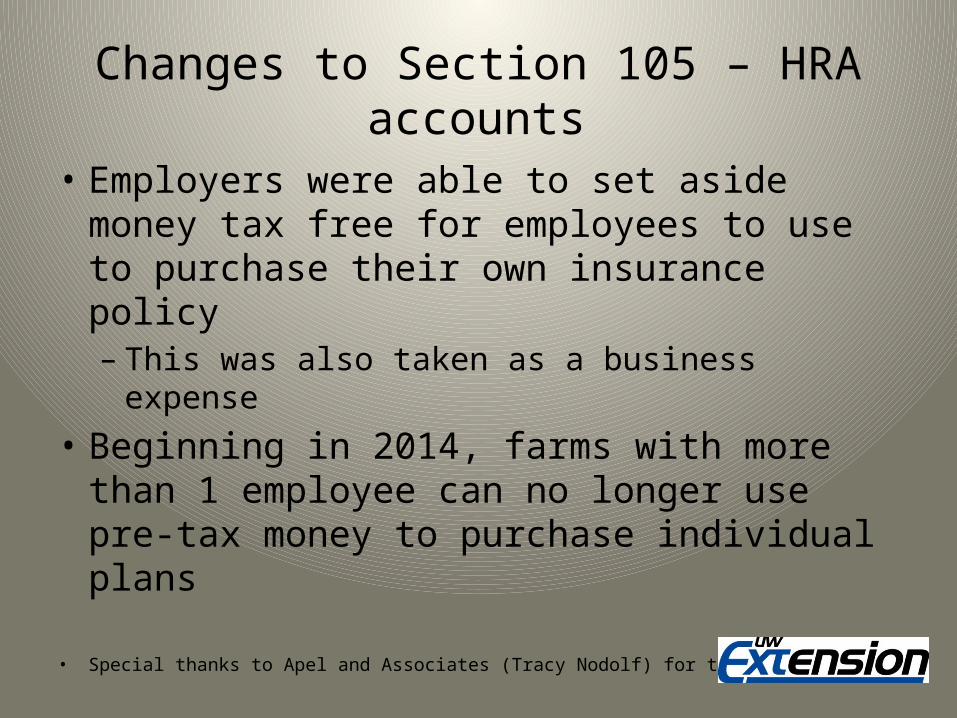

Changes to Section 105 – HRA accounts

• Employers were able to set aside money tax free for employees to use to purchase their own insurance policy– This was also taken as a business expense

• Beginning in 2014, farms with more than 1 employee can no longer use pre-tax money to purchase individual plans

• Special thanks to Apel and Associates (Tracy Nodolf) for this information

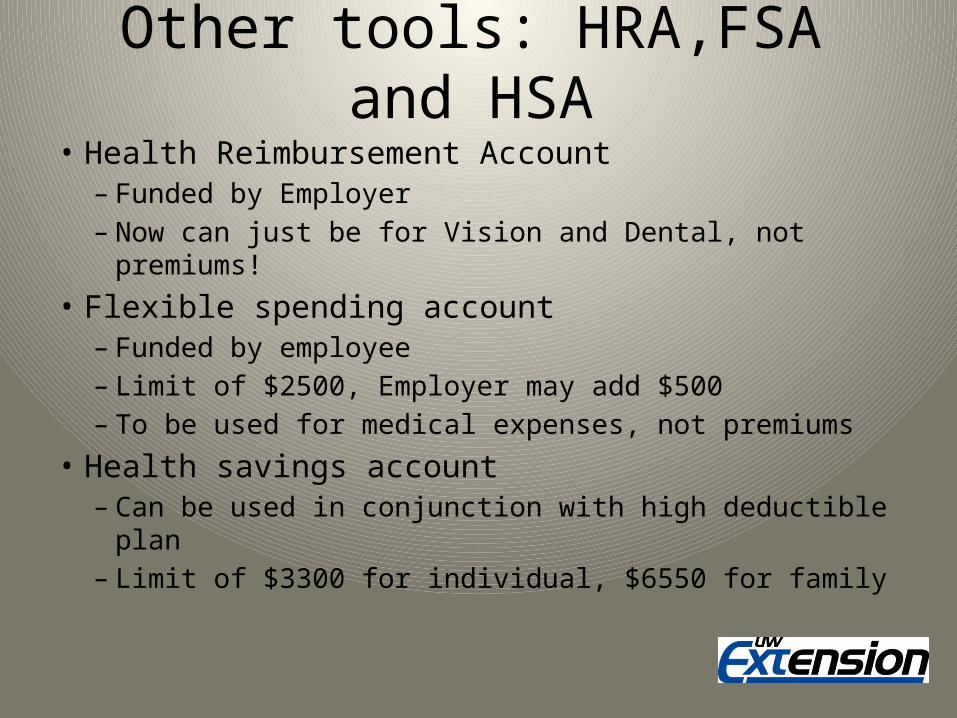

Other tools: HRA,FSA and HSA• Health Reimbursement Account– Funded by Employer– Now can just be for Vision and Dental, not premiums!

• Flexible spending account – Funded by employee– Limit of $2500, Employer may add $500– To be used for medical expenses, not premiums

• Health savings account– Can be used in conjunction with high deductible plan– Limit of $3300 for individual, $6550 for family

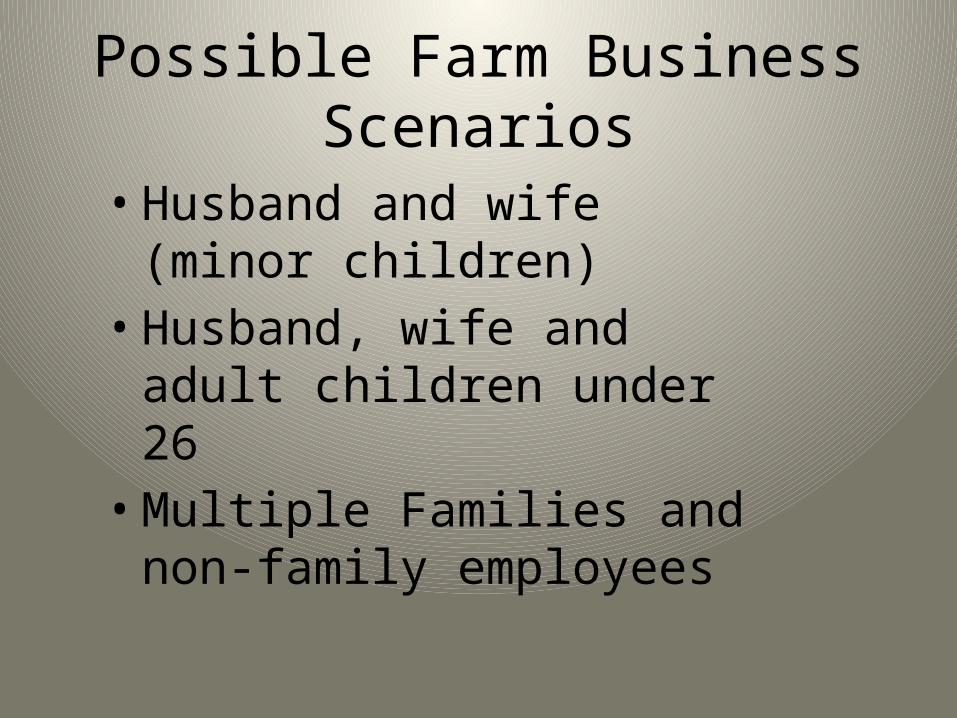

Possible Farm Business Scenarios

• Husband and wife (minor children)

• Husband, wife and adult children under 26

• Multiple Families and non-family employees

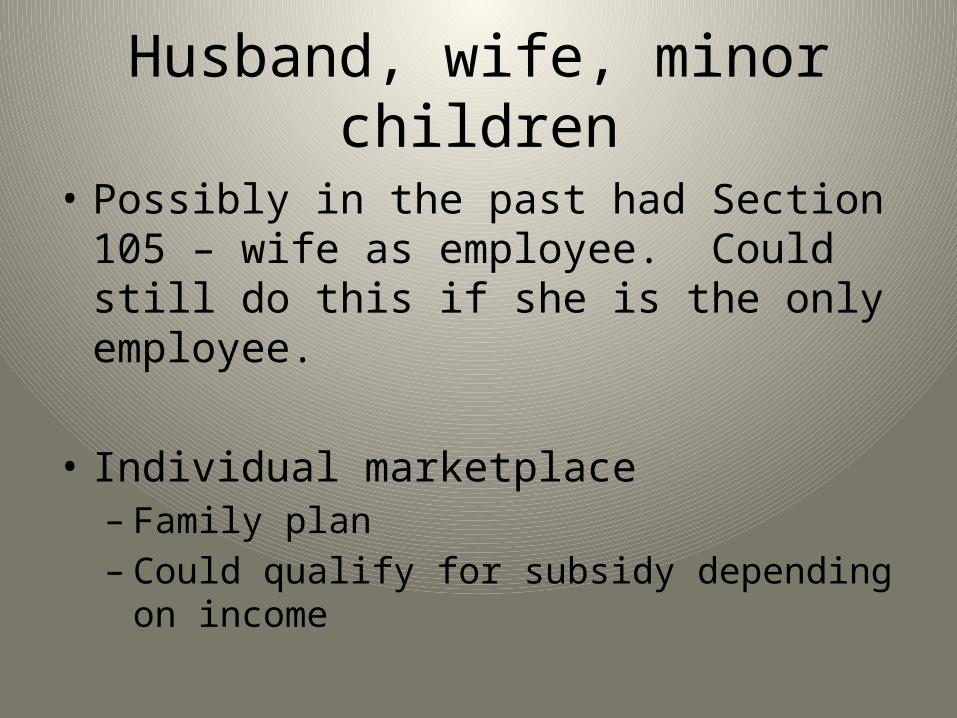

Husband, wife, minor children

• Possibly in the past had Section 105 – wife as employee. Could still do this if she is the only employee.

• Individual marketplace– Family plan– Could qualify for subsidy depending on income

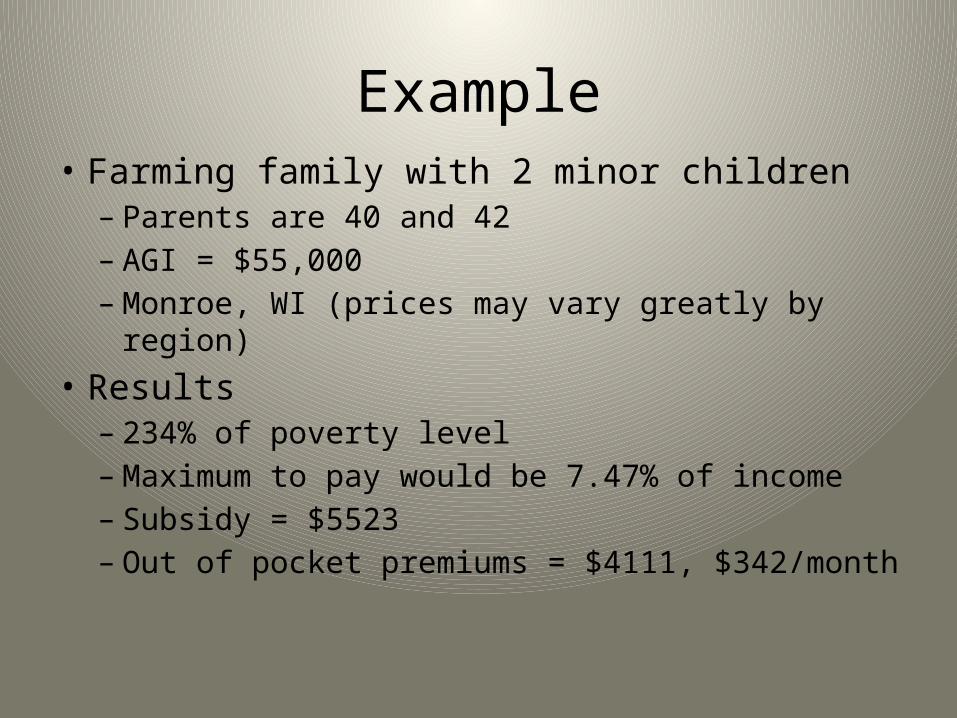

Example• Farming family with 2 minor children– Parents are 40 and 42– AGI = $55,000– Monroe, WI (prices may vary greatly by region)

• Results– 234% of poverty level– Maximum to pay would be 7.47% of income– Subsidy = $5523– Out of pocket premiums = $4111, $342/month

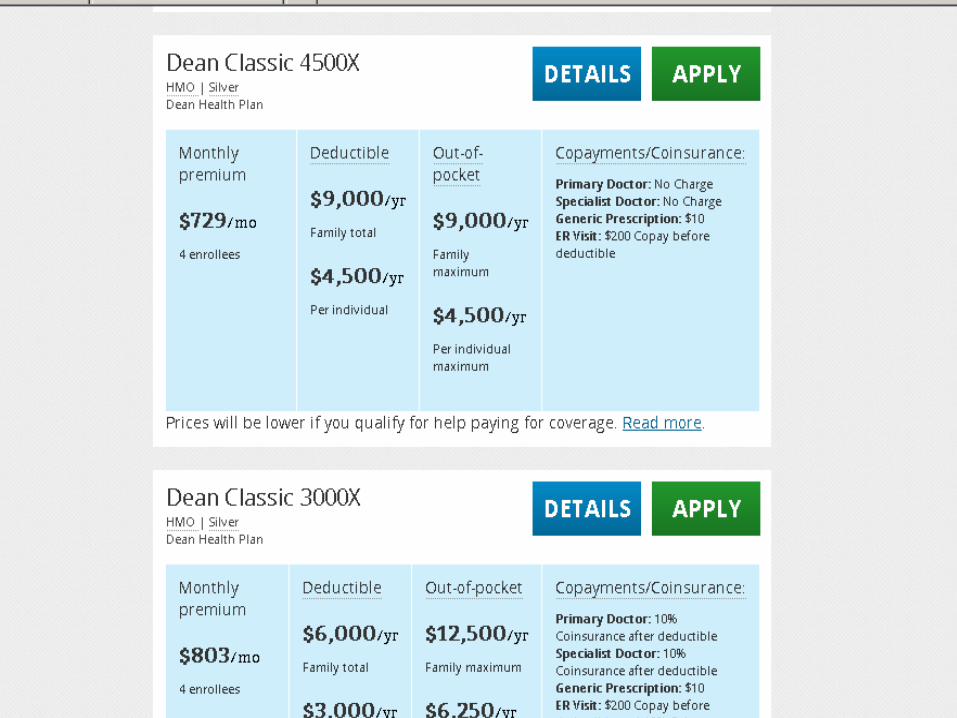

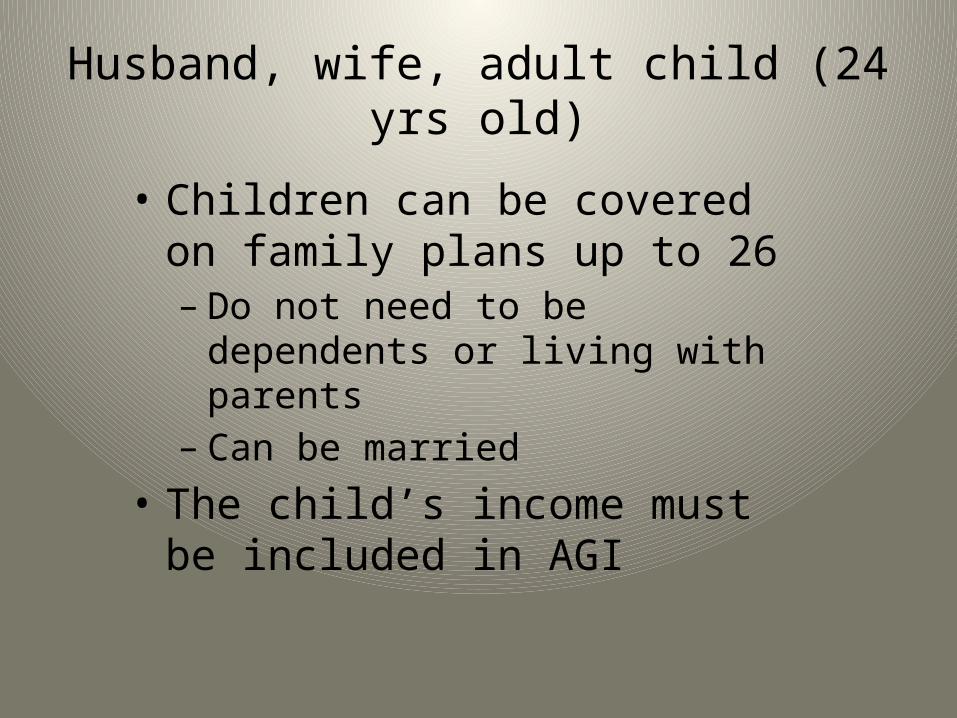

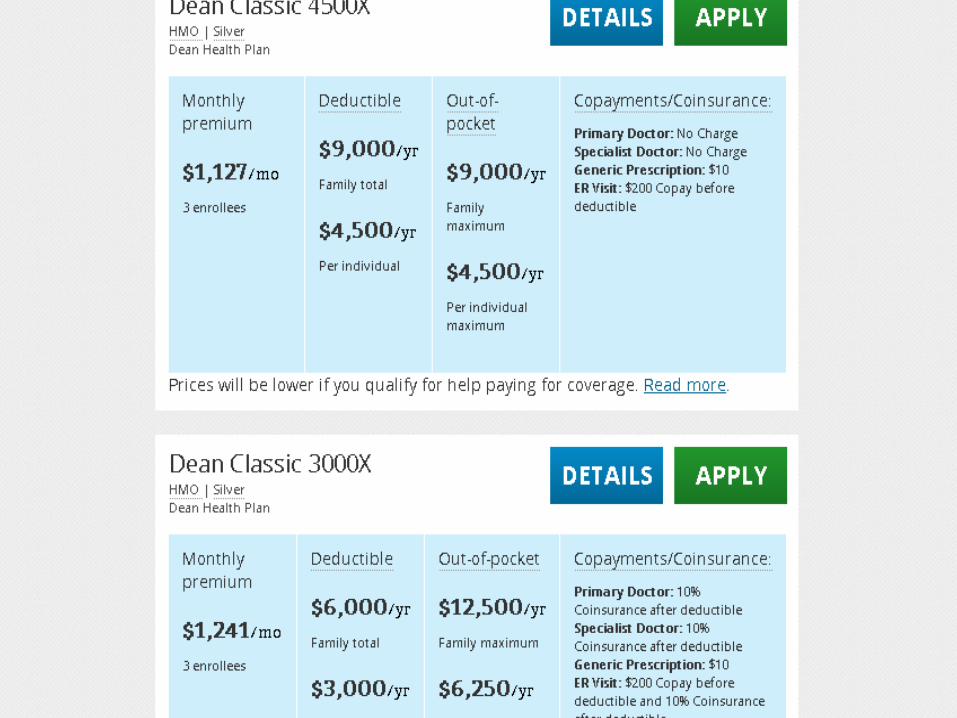

Husband, wife, adult child (24 yrs old)

• Children can be covered on family plans up to 26– Do not need to be dependents or living

with parents– Can be married

• The child’s income must be included in AGI

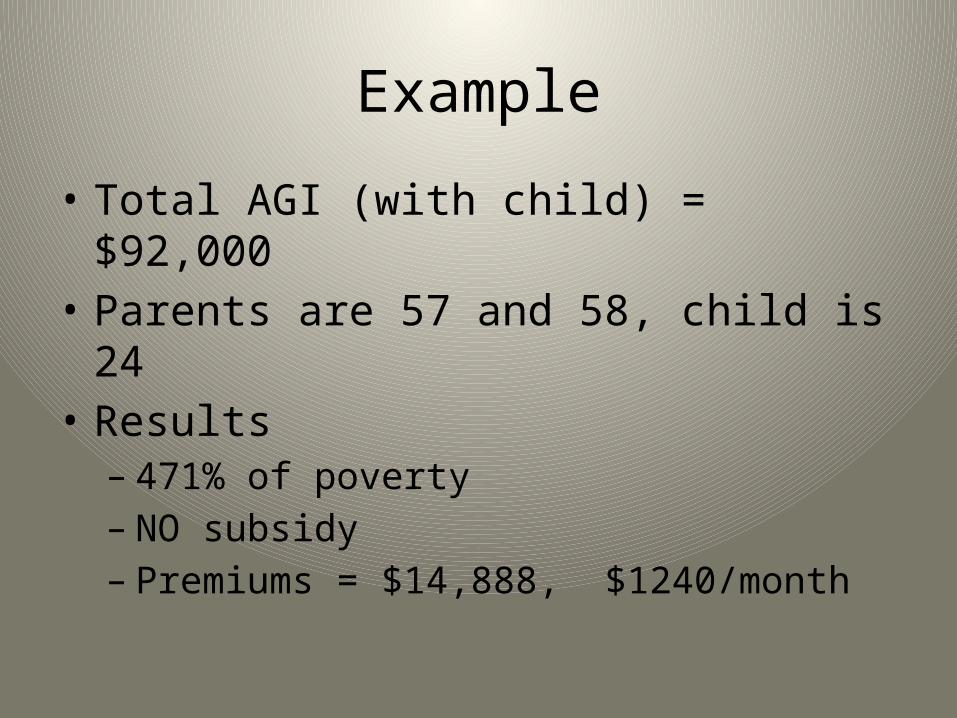

Example

• Total AGI (with child) = $92,000• Parents are 57 and 58, child is 24• Results– 471% of poverty– NO subsidy– Premiums = $14,888, $1240/month

Farm businesses with multiple families and non-family employees

• Group plan through SHOP – Eligible for tax credit if you meet criteria

• Group plan purchased outside of SHOP– Still taken as business expense

• Do not provide group insurance

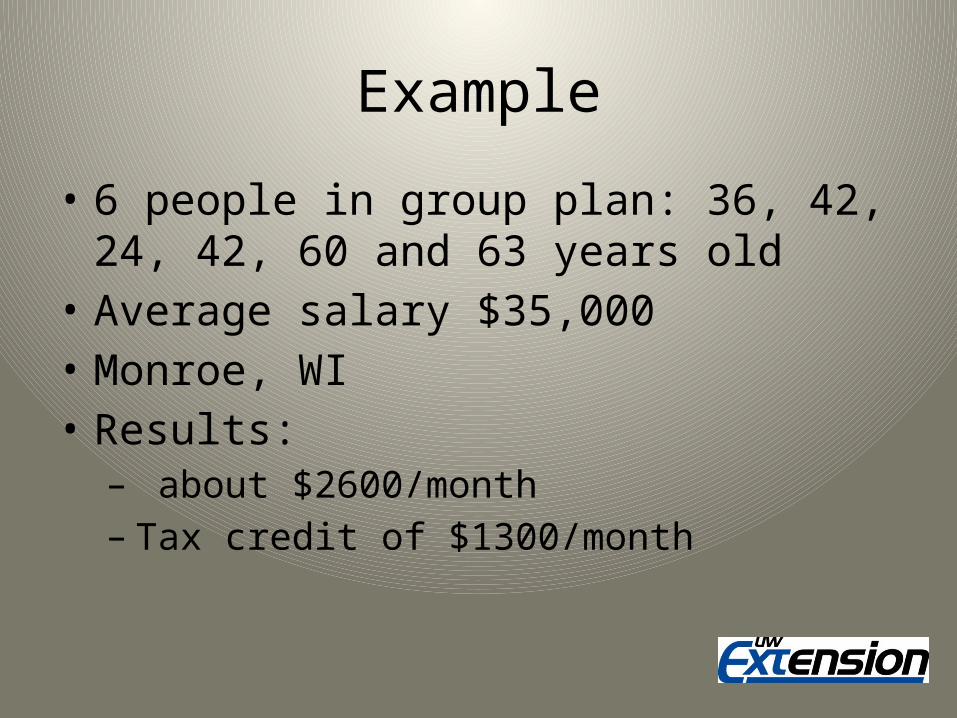

Example

• 6 people in group plan: 36, 42, 24, 42, 60 and 63 years old

• Average salary $35,000• Monroe, WI• Results:– about $2600/month– Tax credit of $1300/month

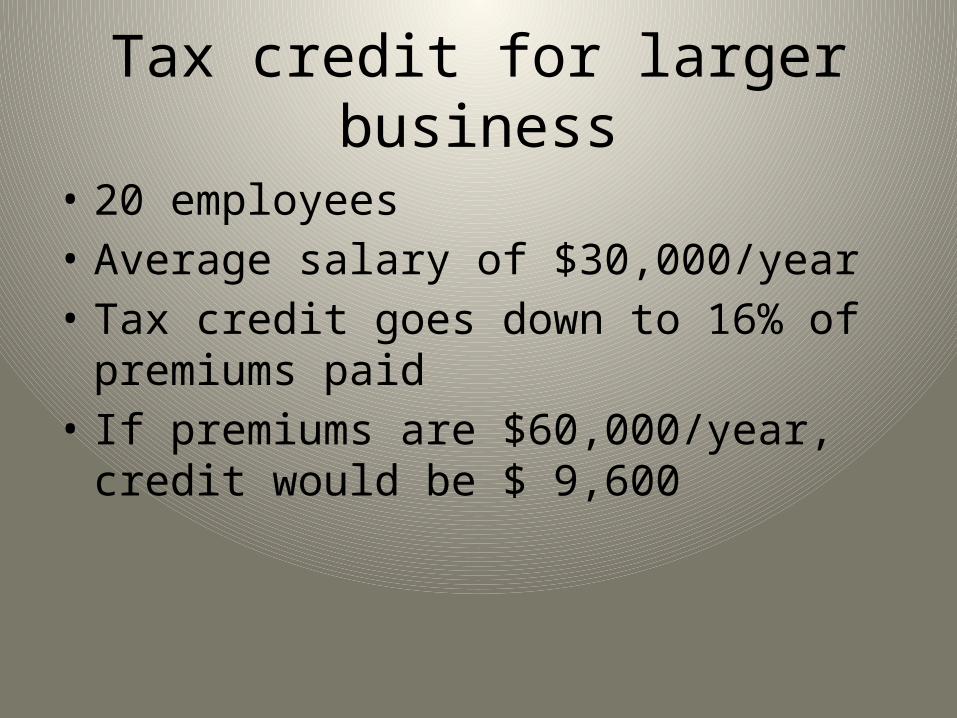

Tax credit for larger business

• 20 employees• Average salary of $30,000/year• Tax credit goes down to 16% of premiums paid• If premiums are $60,000/year, credit would be

$ 9,600

How do you calculate your number of Full Time Equivalents (FTE) Employees?

• For every month – Number of employees that worked >130 hours– Then add up hours of part timers and divide by

120– Add two previous numbers together

• Do this for every month of the year and divide by twelve to get average

• Must be 50 or more, not 49.8

What if you have less than 50?

• Small employers (less than 50 FTEs) are not mandated to offer health insurance to full-time employees

• But small businesses are eligible for a tax credit to offset the cost of providing insurance

• Criteria for credit

– Less than 25 FTE employees, average salary of less than $50,000/year and contribute at least 50% of employees premuims

Requirements for Small Business Credit

• Maximum tax credit is 50% of the premiums paid

– Only receive maximum credit for 10 employees @ $25,000, more employees and higher salary fades out credit!

• SHOP (Small Business Health Option Program) Marketplace must be used

– WEBSITE DELAYED – must use paper application with agent

– https://www.healthcare.gov/marketplace/shop/#state=wisconsin

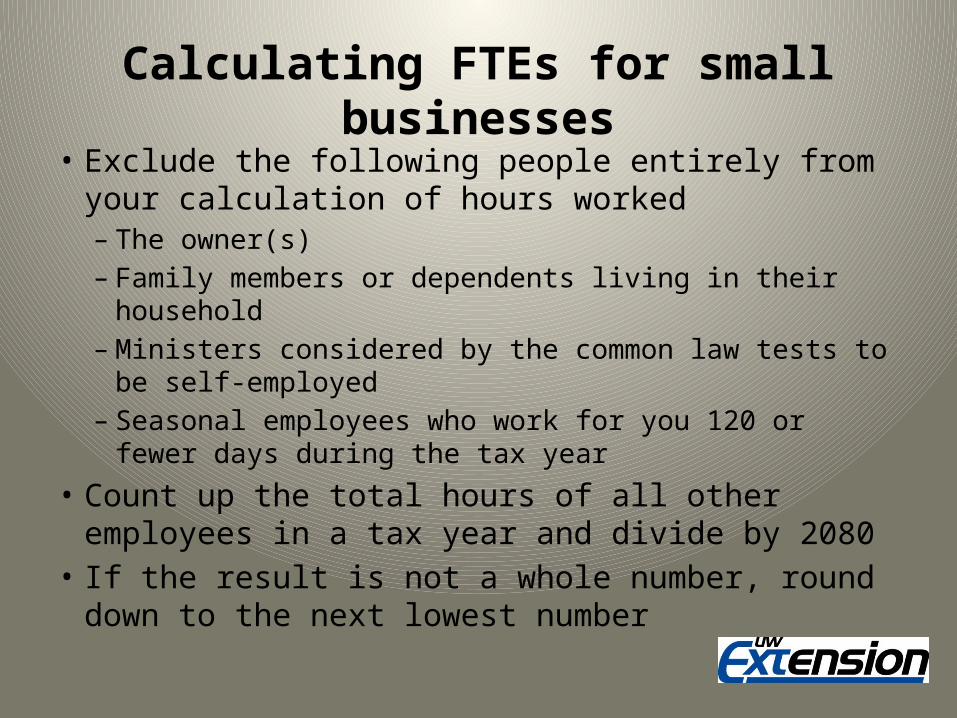

Calculating FTEs for small businesses• Exclude the following people entirely from your

calculation of hours worked– The owner(s) – Family members or dependents living in their household– Ministers considered by the common law tests to be self-

employed– Seasonal employees who work for you 120 or fewer days

during the tax year• Count up the total hours of all other employees in a tax

year and divide by 2080• If the result is not a whole number, round down to the

next lowest number

The Reaction

• Many good questions and interest– Private phone calls and conversations

• Questions often revealed the amount of misinformation out there– Farmers in Wisconsin tend conservative

• It is very difficult for people to get information about how health care choices will impact their taxes

Evaluation• 105 returned evaluations• Increase in knowledge in how the ACA impacts:– Insurance consumers (from 1.8 to 3.6)– Businesses (from 1.5 to 3.6)

• 90% indicated their questions were answered about their personal health insurance

• 88% indicated their questions were answered about their health insurance for their business

• Most said they would use the Smart Choices workbook

• Most said they would use the website links provided

The Future of ACA and Farmer Education

• One more presentation for DATCP Farm Center Volunteers

• We may have only seen the first wave of questions and issues– Next sign-up time – not good for

farmer– Tax time– All of the issue made people walk

away – they may reconsider