26

Natural Gas Natural Gas as a Transportation Fuel Overview and Opportunity Sherrie Merrow National Conference of State Legislatures February 2, 2012

Natural GasNatural

Gas as a

Transportation Fuel Overview and Opportunity

Sherrie Merrow National Conference of State Legislatures February 2, 2012

America’s Natural Gas Alliance Members Highlighting the Benefits of Natural Gas

ABUNDANT

Why Natural Gas?

DOMESTIC

CLEAN

JOBS

ABUNDANT

The United States is now the largest producer of natural gas in the world!

Stable Supplies = Stable PricesNew Projections for Natural Gas Price Stability

($ per million BTU)

Source for NG Prices: EIA Annual Energy Outlook 2011Henry Hub Spot prices (actual prices included foryears prior to annual projections)

Source for Fuel Prices: US DOE Alternative Fuels & Advanced

Vehicles Data Center

U.S. Average Retail Fuel Prices

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.004/1/00

7/1/00

10/1/00

1/1/01

4/1/01

7/1/01

10/1/01

1/1/02

4/1/02

7/1/02

10/1/02

1/1/03

4/1/03

7/1/03

10/1/03

1/1/04

4/1/04

7/1/04

10/1/04

1/1/05

4/1/05

7/1/05

10/1/05

1/1/06

4/1/06

7/1/06

10/1/06

1/1/07

4/1/07

7/1/07

10/1/07

1/1/08

4/1/08

7/1/08

10/1/08

1/1/09

4/1/09

7/1/09

10/1/09

1/1/10

4/1/10

7/1/10

10/1/10

1/1/11

4/1/11

7/1/11

Cost per GGE

Propane

E85

B99/B100

B20

Gasoline

Diesel

CNG

U.S. Average Retail Fuel Prices

Natural Gas is consistently the lowest price

< $1.00 in 2000 to about $2.00 in 2011

U.S. Transportation Fuel Portfolio

71.1%

28.7%

0.2%

Gasoline Diesel Alternative Fuel

Source: Energy Information Administration (EIA), 2009, Excludes Oxygenates

U.S. Gasoline – 137.9 B GGE ▪

Diesel – 55.6 B GGE ▪

Alt. Fuels – .4 B GGE

Equivalent to 22.4 Tcf or 61.6 Bcfd

How much foreign oil do we use?

–

4.250 billion barrels imported in 2010

How much does foreign oil cost?

–

$337 billion for imported oil in 2010

–

$1,091 for each person in America

–

In 2009, energy imports made up

nearly 60% of our trade deficit

17.7 Bcfe/d

43.8 Bcfe/d

0.1 Bcfe/d

America currently relies on one primary fuel for transportation –

Petroleum

Taking Action: U.S. Transportation Sector Displacement

Fuel Consumption by Market Segment

0

5

10

15

20

25

30

35

40

45

Light Duty Heavy Duty Medium Duty Marine Rail Upstream

Source: Data and forecast from EIA, Encana, 2010Displacement opportunities exclude Air, International Shipping, Military, Pipeline Fuel

Displaceable Market Volume: 61.6 Bcfe/d69%

18%

5% 5%1%2% (1.3 Bcf/d)

42.4 Bcf/d

10.8 Bcf/d

3.2 Bcf/d 3.2 Bcf/d(0.7 Bcf/d)

Most Commercially

Ready

Industry’s Early

Opportunity

Largest Opportunity

Natural Gas Value Proposition: Four Core Value Propositions

Environmental Benefits Social Benefits

Energy Security BenefitsEconomic Benefits

Reduced CO2 emissions (20-30%)

Reduced associative emissions–

CO, SO2, NOX

Lower engine noise

Lower fuel price than diesel / gasoline

Reduced maintenance costs

Technology is proven and improved

Jurisdiction dependent grants / credits

Domestic energy source–

Economic benefits through value chain

Displaces foreign oil–

63% petroleum is imported

Natural gas production related revenues–

Royalties, taxes, job creation

Natural gas fueling infrastructure revenues–

Job creation, taxes, economic spin-off

Natural Gas FuelsCompressed Natural Gas (CNG)

•

Source: Pipeline

•

Compressed to 3,600 psi

•

Primarily for light and medium duty vehicles

•

Ideal for return‐to base fleets or fleets that

require fast‐filling

•

Time‐fill and fast‐fill capability / stored in

pressurized tanks

Liquefied Natural Gas (LNG)

•

Source: Liquefaction Plant

•

Converted to liquid form for ease of storage and

transport

(Cooled to ‐260 °F and 40 psi)

•

Ideal for medium to heavy duty fleets

•

Fast‐fill / stored in tanks (similar to diesel size)

Vehicle Categories –

Choices Already Exist

Light Duty CNG

Medium to Heavy Duty CNG

Heavy Duty On Road LNG

Heavy Duty Off Road LNG

U.S. Interstate Highway System Linking Green Corridors

ICTC

RMC

TT

I-75 –

Interstate 75 Corridor

TT –

Texas Triangle

RMC –

Rocky Mountain Corridor

ICTC –

Interstate Clean Transportation Corridor

I-75

USA CNG and LNG Stations

0

200

400

600

800

1,000

1,200

1,400

1,600

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Ann

ual F

uel D

ispe

nsed

per

Sta

tion,

GG

ECNG Stations LNG Stations

Source: US DOE Alternative Fuels & Advanced Vehicles Data Center

10% CAGR

As of December 31, 2011 –

975 CNG stations and 46 LNG stations

Top States for NGV Stations

California: 260

New York: 103

Utah: 78

Oklahoma; 63

Texas: 38

OEMs Deliver Light-Duty NGVs

Ford and Westport LD

Announce New Natural Gas

System for Super Duty Pickups Spring 2012

Honda Civic Natural Gas Unveils New Name, New

Features

GM to Launch New CNG Bi-

Fuel Pickup Truck in Late

2012

Dodge to Introduce

CNG-Powered Bi-Fuel Pickup

Trucks in March 2012

Types of NGV Legislation

Source: US DOE Alternative Fuels & Advanced Vehicles Data Center

CNG/LNG Fuel Tax Incentives

Vehicle Purchase/Conversion Funding

Infrastructure/Station Funding

Fleet Purchase Requirements

Other–

Use of HOV lanes

–

Use of carpool parking areas

–

Access to State alternative fueling stations

–

Emissions inspection exemption

–

AFV insurance discounts

–

Airport incentives (preferential taxi lanes)

–

Reduction in license / state fees

NGV Incentive ComparisonsFederal Texas West Virginia Oklahoma Oregon Colorado Louisiana

Natural Gas Vehicle Count 117,446 10,440 22 2,932 1,675 1,197 361

Natural Gas Stations (E/P)

960 / 115 41 / 13 0 62 / 5 12 / 0 29 / 5 8 / 12

Infrastructure/

Home fuel

Texas Clean Transportation

Triangle funds up to $2MM

50% of the construction costs up to $250,000

($312,500 if allows public access)

Expires: 01/01/21

75% of infrastructure

Expires: 01/01/14

25% of the incremental cost

or $750 for residents / 35% for businesses

50% of the cost of constructing an

alternative fueling station

No expiration

Vehicle IncentivesAccelerated

depreciation in 2012

Texas Gas Services offers

$2,000 rebate for the purchase of a NGV / $3,000 for the conversion

Texas Clean Transportation

Triangle funds 60- 90% of cost up to

$8MM

35% of the purchase price or 50% of the

conversion cost up to $7,500 for < 26,000 GVWR and up to

$25,000 for > 26,000 GVWR

Expires: 01/01/21

50% of the incremental cost

Expires: 01/01/14

25% of the incremental cost

or $750 for residents / 35% for businesses

55% of incremental cost

in 2012

Decreases: 35% : 2013 25% : 2014 and 2015

50% of the incremental cost, or 10% of the cost of the motor vehicle or up to

$3,000

No expiration

Fuel Credits Preferential NG Fuel rates

Deregulation of CNG as a Motor Fuel

Mandates/Goals Acquisition Requirements

Acquisition Requirements

Acquisition Requirements

Acquisition Requirements

CNG highway/station

every 100 miles by 2015

Acquisition Requirements

Acquisition Requirements

Acquisition Requirements

Funding Grants / Loans Grants / Loans Grants / Loans Infrastructure Loans Loans Grants Loans

Source: AFDC as of 1/27/2012

NGV MOU

Led by CO, OK, PA and WY,

states are joining together

to use NGVs in state fleets─

Aggregate vehicle purchase

numbers for “Detroit”

–

joint RFP

─

Commit to converting state

fleets (county, municipal, and

other government)

─

ME, UT, NM, WV, KY have joined

CO, OK, PA and WY with other

states in progress

Leading the Way•

NGVs in fleets across America─

16 % of all transit buses in U.S.

─

Airports use NGVs for transit and taxis

─

Waste trucks are fastest‐growing segment

─

Medium and heavy duty trucks used by large

fleets like UPS, AT&T, Comcast, Sysco, Ryder,

and many others

─

First CNG‐powered fire trucks and ambulances

are coming into the market

Completed Picture for Market Growth

FLEETS & CONSUMERS

OEMs & MULTIPLE

PLATFORMSFUELING STATIONS

COMPETITIVE PRICING

MAINTAIN INDUSTRY SAFETY &

COMPLIANCE

North America

HOME FUELING

Additional Information

Source: IANGV, NGVA Europe, Fiat

Natural Gas Vehicle Growth by Continent Great North American Opportunity

Natural Gas Vehicles (Millions)

Natural Gas Vehicles by Continent

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Asia Europe N. America S. America Africa

Italy as an Example

~600,000 NGVs

37% growth since 2007

NGVs have 7% market share of all

new vehicles purchased

Cost of CNG is 50% to 60% less

expensive than gasoline

Government incentives

Imports 89% of natural gas

Fiat Qubo Natural Power

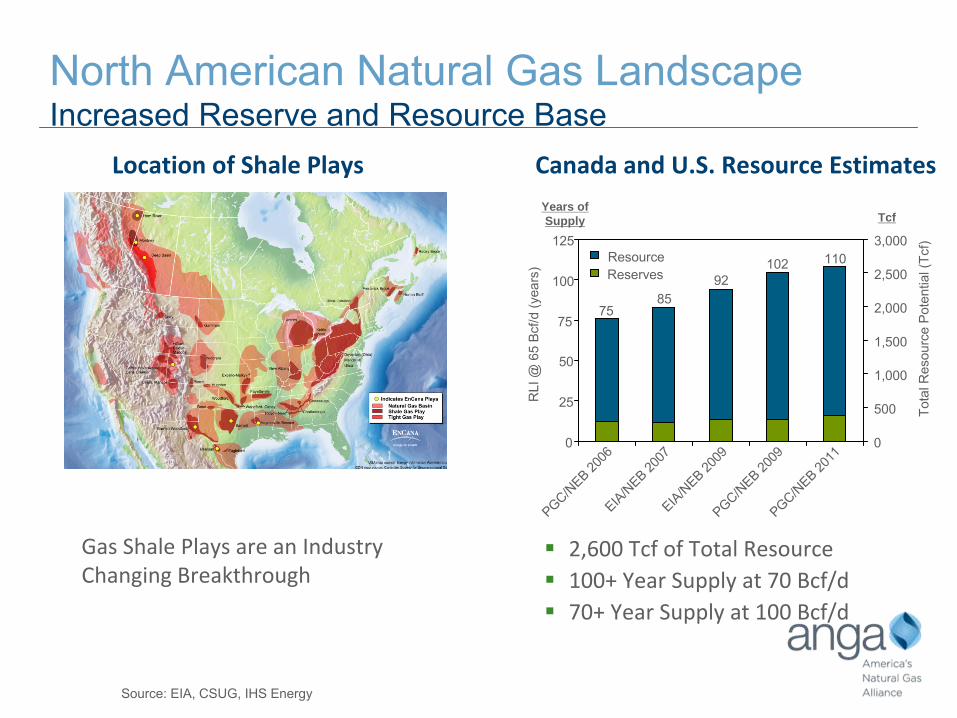

Source: EIA, CSUG, IHS Energy

Gas Shale Plays are an Industry

Changing Breakthrough

North American Natural Gas Landscape Increased Reserve and Resource Base

2,600 Tcf of Total Resource

100+ Year Supply at 70 Bcf/d

70+ Year Supply at 100 Bcf/d

Years of Supply Tcf

Canada and U.S. Resource EstimatesLocation of Shale Plays

92102

7585

0

25

50

75

100

125

PGC/NEB 20

06EIA/N

EB 2007

EIA/NEB 20

09PGC/N

EB 2009

PGC/NEB 20

11

RLI

@ 6

5 Bc

f/d (y

ears

)

0

500

1,000

1,500

2,000

2,500

3,000

Tota

l Res

ourc

e Po

tent

ial (

Tcf)

ResourceReserves

110

Natural Gas Usage by Sector

Source: EIA, Natural Gas Year In Review, 2009

How Natural Gas is Used Today

3% Transportation

14% Commercial

32% Industrial 21% Residential

30% Electric Power

Petroleum Fuel By Vehicle Per YearVehicle # Gallons Per Year Today’s Premium*

Freight Truck 12,000 $60,000

Transit Bus 12,000 $50,000

Garbage Truck 9,000 $52,000

Airport Shuttle 5,800 - 7,200 $30,000

Taxi Cab 5,000 $10,000

Delivery Truck 4,500 - 5,500 $30,000

School Bus 2,200 – 2,800 $36,000

Light Duty Truck 2,000 $10,000

Consumer Vehicle 1,000 $7,000

*Premium is today’s price without subsidies or additional volume

Natural Gas Vehicle Option Examples•

Light Duty Vehicles

─

Honda Civic Natural Gas (NG)

─

Chevrolet –

Impala, Silverado, Tahoe, Malibu, Tahoe

─

Ford – Focus, Fusion, F150, Milan, Transit Connect

─

Dodge – Ram

•

Medium Duty Vehicles

─

Chevrolet –W4500, C4500 / 5500, Express, Savana

─

Ford –

F250, F350, E450, F450, F550, F53 / F59

─

Transit Bus –

Blue Bird, Thomas Built, El Dorado, Foton America, NABI, New Flyer,

Orion, Motor Coach Industries

─

Work Trucks –

Workhorse, Sterling, International, MaxxForce

─

Refuse – American LaFrance, Mack, AutoCar, Crane Carrier, Freightliner,

Kenworth, McNeilus

─

Street Sweeper –

Elgin, Freightliner, Schwarze

•

Heavy Duty Vehicles

─

Short‐Haul –

Freightliner, Kenworth, Peterbilt, Volvo Trucks N.A.

─

Long‐Haul – Kenworth, Peterbilt, Volvo Trucks N.A., International Transtar

•

Heavy Duty Engine Manufacturers

─

Cummins Westport 8.9L ISL G

─

Westport 15L

Grant Funding OptionsFederal GrantsDOT Congestion Mitigation and Air Quality Improvement Program (CMAQ)

Generally limited to projects in non-attainment areas

DOE State Energy Program (SEP) Clean Cities program which supports alternative fuel vehicle and

infrastructure.

EPA Supplemental Environment Project and DERA Grants

–Repower: 75% of cost

–Vehicle replacements: 25% of cost

Diesel Emissions Reduction Program (DERP): EPA program which assists government agencies, school districts and other parties to replace older diesel engines.

Diesel Truck Retrofit and Fleet Modernization Program: EPA program provides grants to states to fund fleet modernization programs, with preference to be given to ports and other major hauling operations.

Clean School Bus Program: EPA program provides grants to school districts and related organizations for the replacement, repower or retrofit of school buses, the purchase of alternative fuels for school buses and alternative fuel infrastructure.

Federal Transit Administration (FTA) Clean Fuels Grants

Funds transit projects such as purchasing or leasing clean fuel buses and/or constructing or leasing clean fuel bus facilities.

Federal Aviation Administration (FAA) Voluntary Airport Low Emissions (VALE) Program

National program to reduce airport ground emissions at commercial service airports located in designated air quality nonattainment and maintenance areas,

Resources•

American Natural Gas Alliance (ANGA)

–

http://www.anga.us/

•

Alternative Fuel Stations and Prices

–

http://www.afdc.energy.gov/afdc/stations/advanced.php/

–

http://www.altfuelprices.com/

–

http://www.cngprices.com/

–

http://www.fueleconomy.gov/

•

Clean Vehicle Foundation

http://www.cleanvehicle.org/index.shtml/

•

Natural Gas Vehicle Institute

–

http://www.ngvi.com/

•

Natural Gas Vehicles for America

–

http://www.ngvc.org/index.html/

•

US DOE Alternative Fuels & Advanced Vehicles Data Center

–

http://www.afdc.energy.gov/afdc/

•

Weld County Smart Energy

–

http://www.weldsmartenergy.org/

–

Abundant–

Affordable

–

Clean–

Reliable

–

Domestic Solution

Natural Gas is…