15

Overview of Autogas market in Europe Samuel Maubanc General Manager AEGPL – European LPG Association [email protected] www.aegpl.be AIGLP Congress Buenos Aires, March 30 th , 2017

Overview of Autogas market in Europe

Samuel Maubanc General Manager

AEGPL – European LPG Association [email protected]

www.aegpl.be

AIGLP Congress Buenos Aires, March 30th, 2017

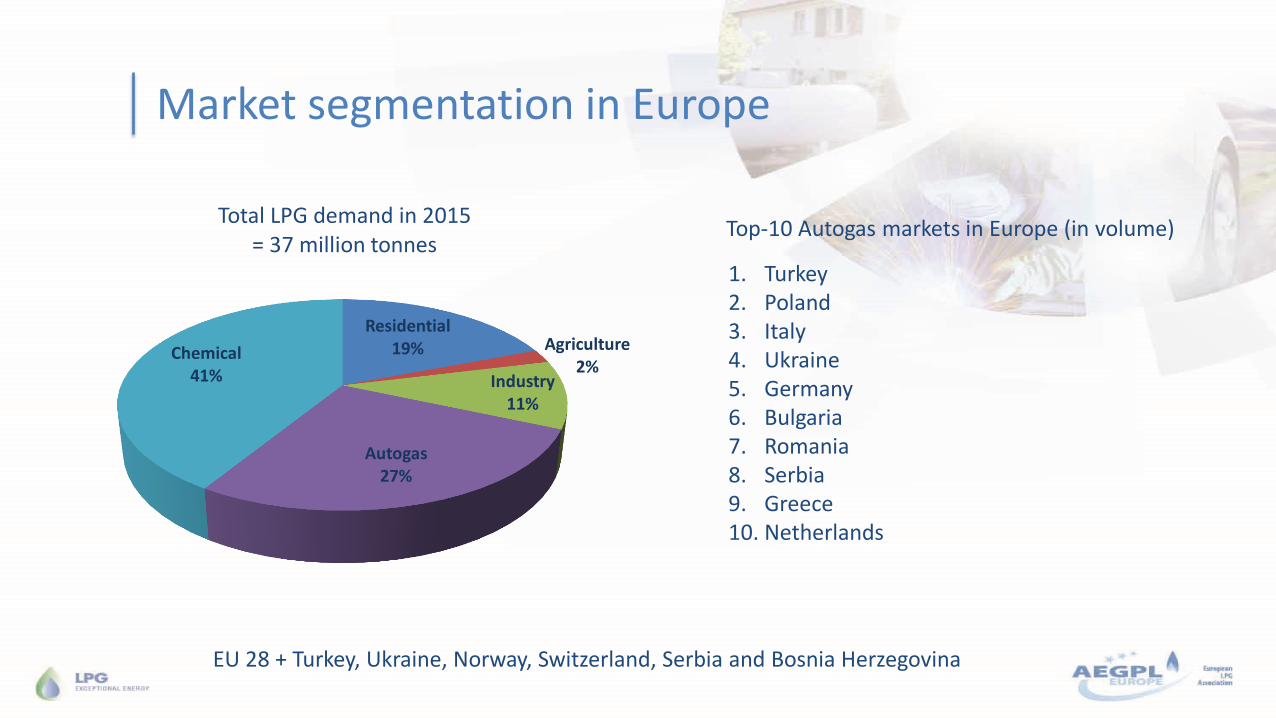

Market segmentation in Europe

Residential 19% Agriculture

2% Industry

11%

Autogas 27%

Chemical 41%

Total LPG demand in 2015 = 37 million tonnes

1. Turkey 2. Poland 3. Italy 4. Ukraine 5. Germany 6. Bulgaria 7. Romania 8. Serbia 9. Greece 10. Netherlands

Top-10 Autogas markets in Europe (in volume)

EU 28 + Turkey, Ukraine, Norway, Switzerland, Serbia and Bosnia Herzegovina

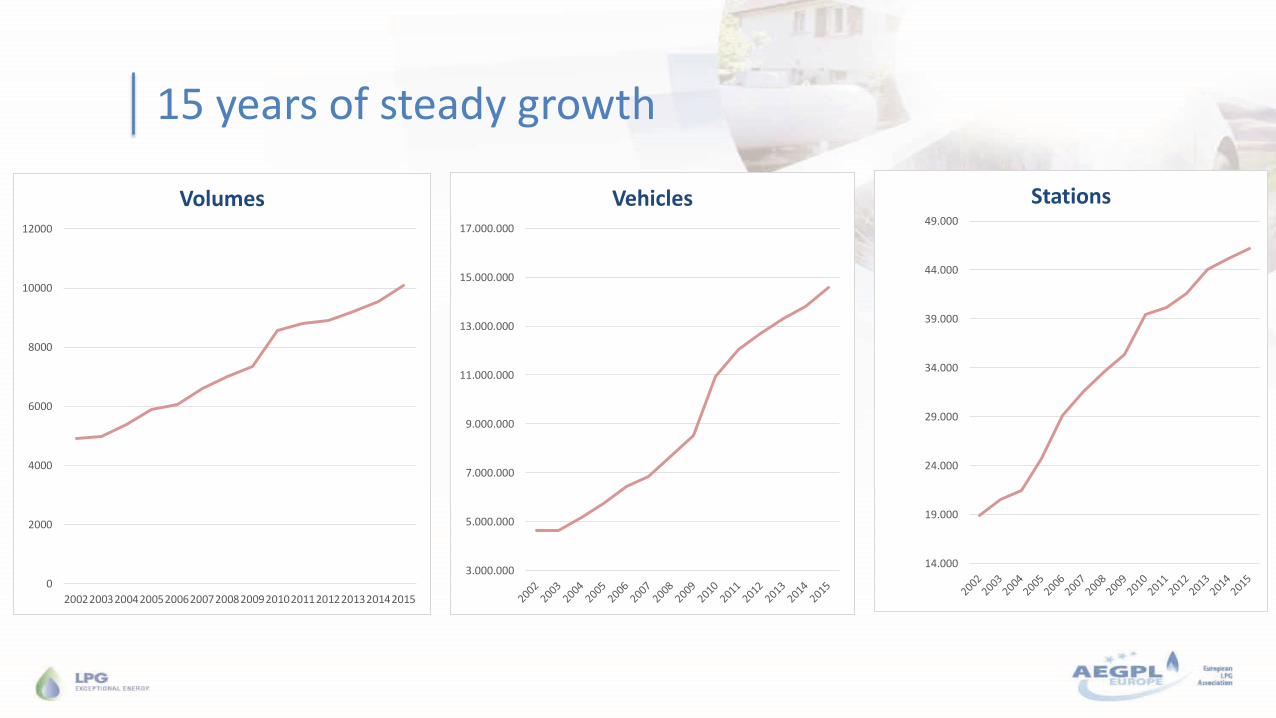

15 years of steady growth

0

2000

4000

6000

8000

10000

12000

20022003200420052006200720082009201020112012201320142015

Volumes

3.000.000

5.000.000

7.000.000

9.000.000

11.000.000

13.000.000

15.000.000

17.000.000

Vehicles

14.000

19.000

24.000

29.000

34.000

39.000

44.000

49.000

Stations

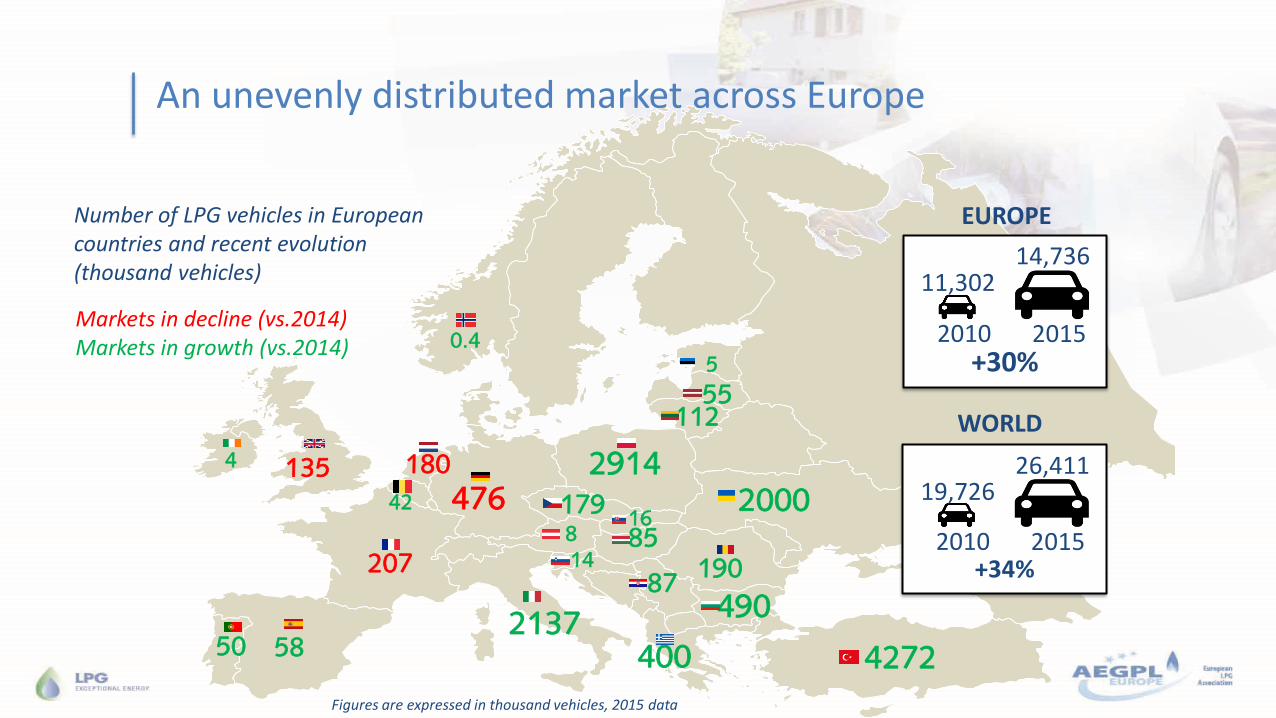

Number of LPG vehicles in European countries and recent evolution (thousand vehicles)

Markets in decline (vs.2014) Markets in growth (vs.2014)

14,736 11,302

2010 2015 +30%

26,411 19,726

2010 2015 +34%

50 58 2137

135 2914

490

400

476

190

180

207

Figures are expressed in thousand vehicles, 2015 data

8

42

87

179

5

85

4

55 112

16

14

0.4

4272

2000

EUROPE

WORLD

An unevenly distributed market across Europe

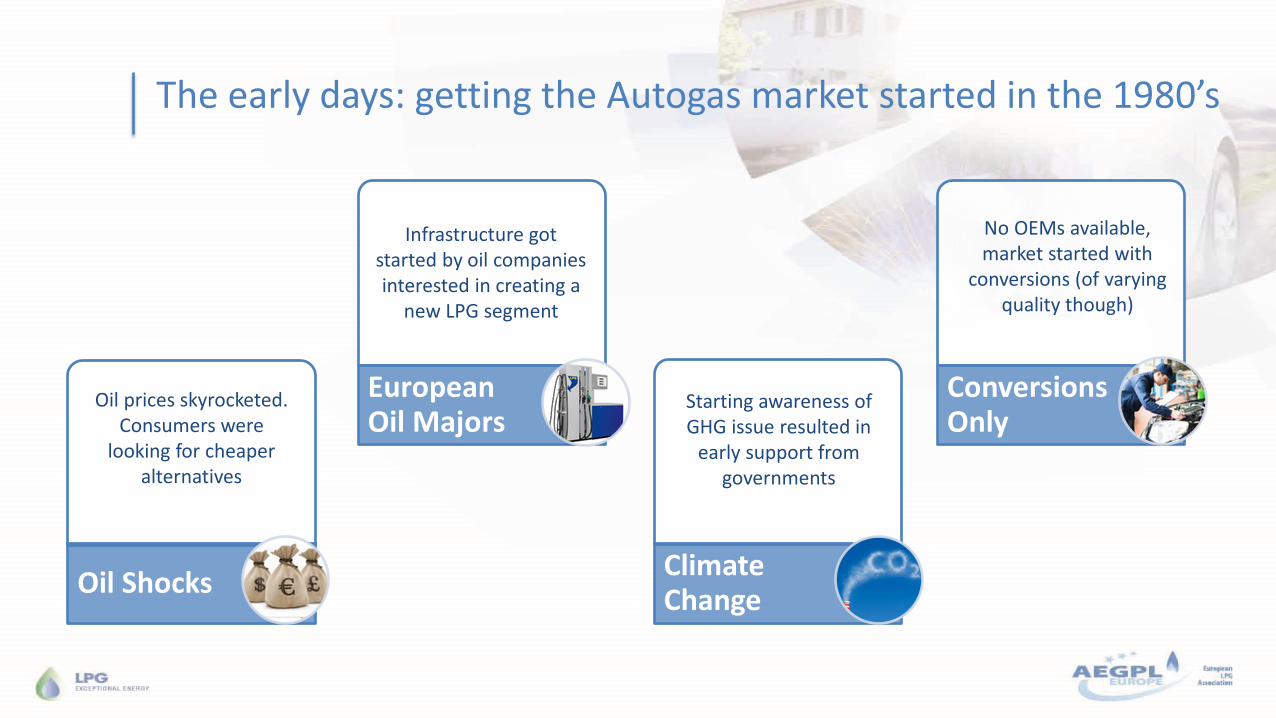

Key factors driving LPG demand in Europe

Oil Shocks

European Oil Majors

Climate Change

Conversions Only

Oil prices skyrocketed. Consumers were

looking for cheaper alternatives

Infrastructure got started by oil companies interested in creating a

new LPG segment

Starting awareness of GHG issue resulted in

early support from governments

No OEMs available, market started with

conversions (of varying quality though)

The early days: getting the Autogas market started in the 1980’s

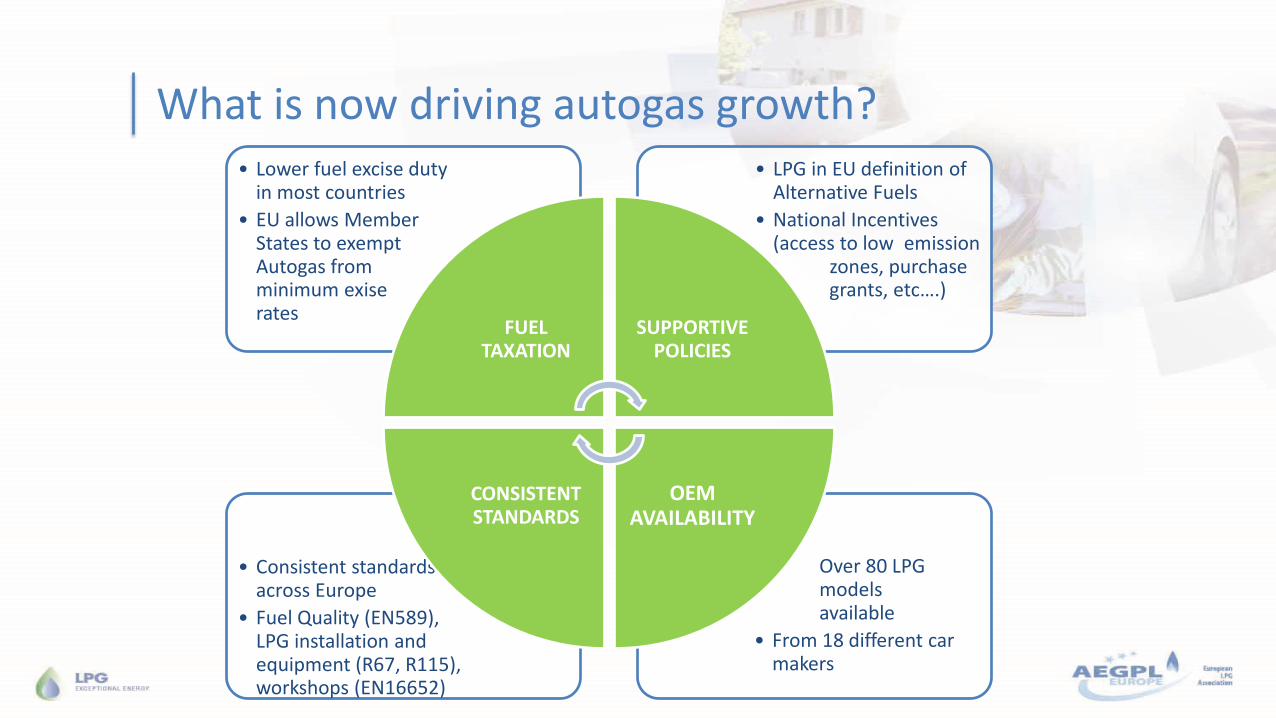

• Over 80 LPG models available

• From 18 different car makers

• Consistent standards across Europe

• Fuel Quality (EN589), LPG installation and equipment (R67, R115), workshops (EN16652)

• LPG in EU definition of Alternative Fuels

• National Incentives (access to low emission zones, purchase grants, etc….)

• Lower fuel excise duty in most countries

• EU allows Member States to exempt Autogas from minimum exise rates

FUEL TAXATION

SUPPORTIVE POLICIES

OEM AVAILABILITY

CONSISTENT STANDARDS

What is now driving autogas growth?

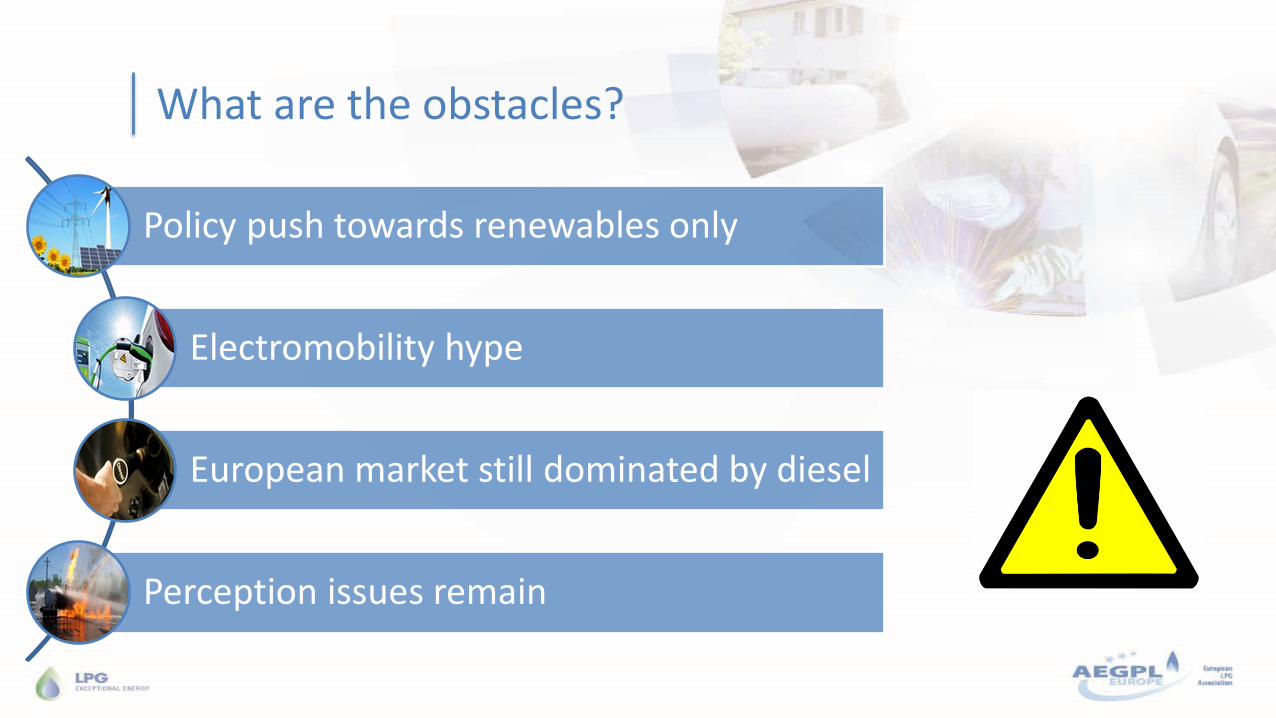

Policy push towards renewables only

Electromobility hype

European market still dominated by diesel

Perception issues remain

What are the obstacles?

What winning cards up our sleeves?

THE GAME CHANGER

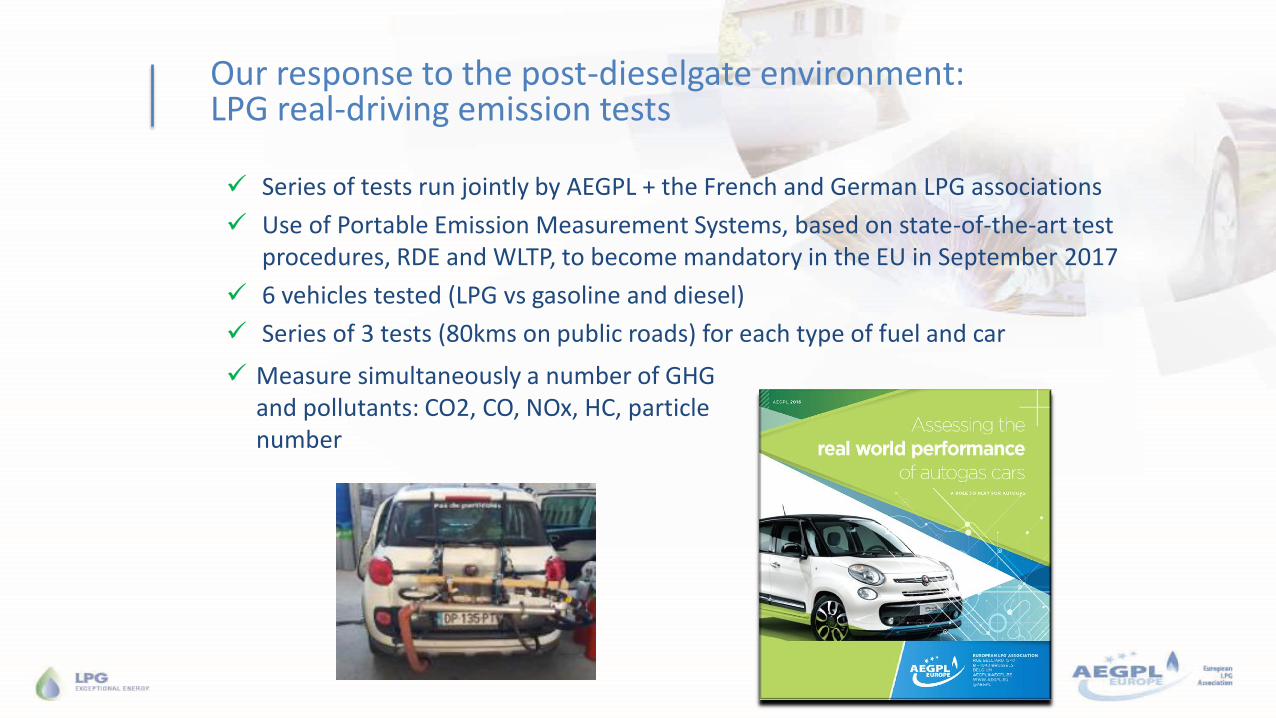

Our response to the post-dieselgate environment: LPG real-driving emission tests

Series of tests run jointly by AEGPL + the French and German LPG associations

Use of Portable Emission Measurement Systems, based on state-of-the-art test procedures, RDE and WLTP, to become mandatory in the EU in September 2017

6 vehicles tested (LPG vs gasoline and diesel)

Series of 3 tests (80kms on public roads) for each type of fuel and car

Measure simultaneously a number of GHG and pollutants: CO2, CO, NOx, HC, particle number

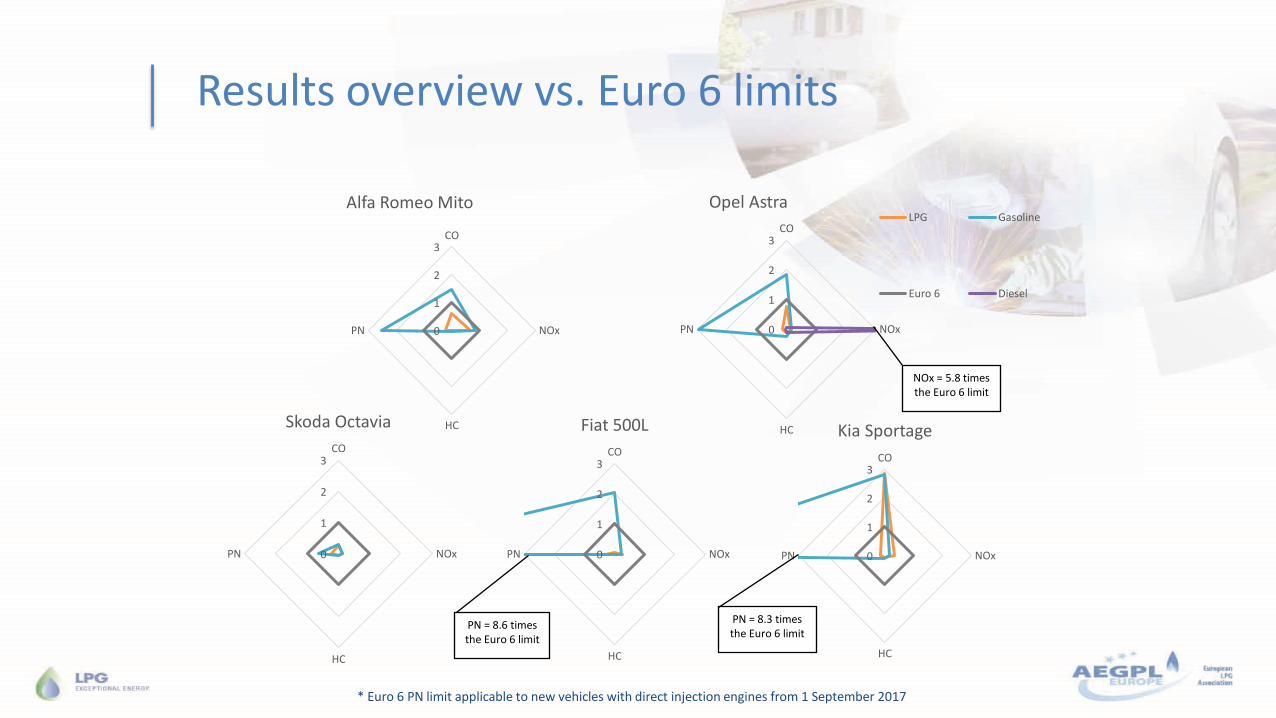

Results overview vs. Euro 6 limits

0

1

2

3CO

NOx

HC

PN

Alfa Romeo Mito

0

1

2

3CO

NOx

HC

PN

Fiat 500L

PN = 8.6 times the Euro 6 limit

0

1

2

3CO

NOx

HC

PN

Skoda Octavia

0

1

2

3CO

NOx

HC

PN

Opel Astra LPG Gasoline

Euro 6 Diesel

0

1

2

3CO

NOx

HC

PN

Kia Sportage

NOx = 5.8 times the Euro 6 limit

PN = 8.3 times the Euro 6 limit

* Euro 6 PN limit applicable to new vehicles with direct injection engines from 1 September 2017

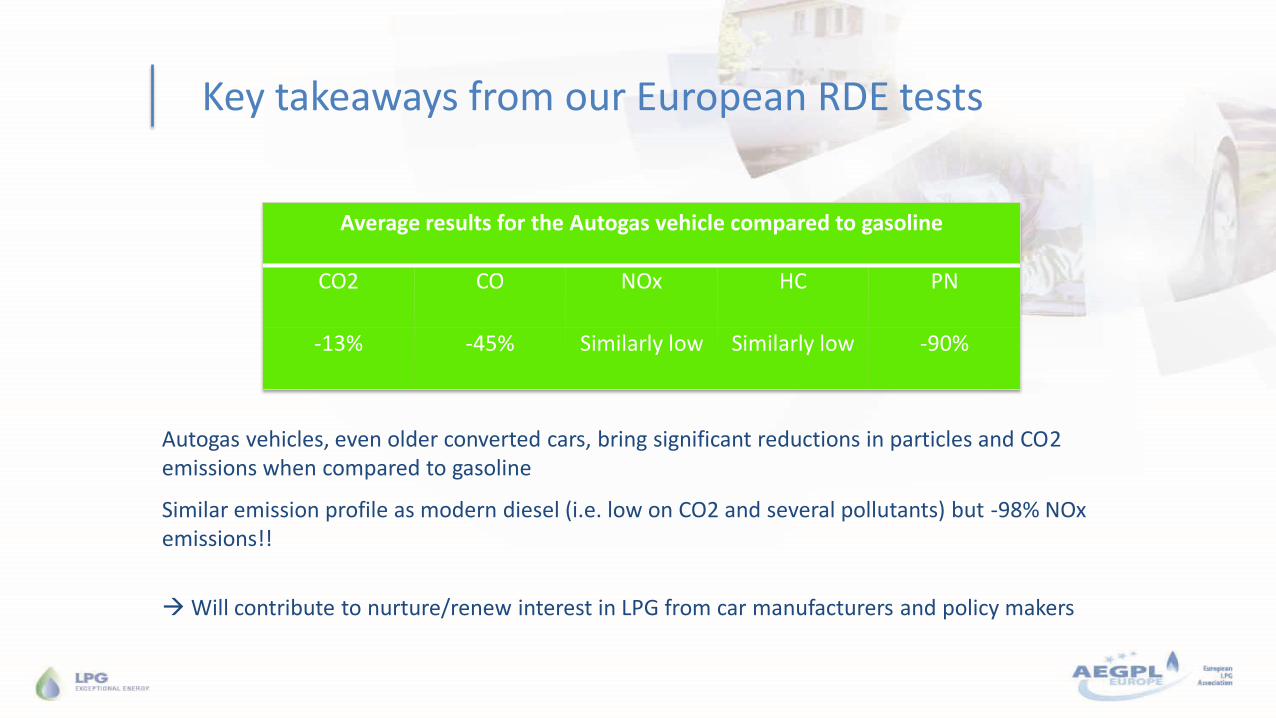

Key takeaways from our European RDE tests

Autogas vehicles, even older converted cars, bring significant reductions in particles and CO2 emissions when compared to gasoline

Average results for the Autogas vehicle compared to gasoline

CO2 CO NOx HC PN

-13% -45% Similarly low Similarly low -90%

Similar emission profile as modern diesel (i.e. low on CO2 and several pollutants) but -98% NOx emissions!!

Will contribute to nurture/renew interest in LPG from car manufacturers and policy makers

Biopropane is becoming a commercial reality in Europe

Several major announcements from the industry in the last months

Critical for maintaining authorities’ interest to support LPG

AEGPL and European industry at large stepping up effort to integrate in our advocacy strategy

See you in Lisbon, Portugal !

www.aegpl2017.com