16

646564 1 Overview of Foreign Bank Supervision in the United States Division of Banking Supervision & Regulation Board of Governors of the Federal Reserve System October, 2006

646564 1

Overview of Foreign Bank Supervision in the United States

Division of Banking Supervision & RegulationBoard of Governors of theFederal Reserve System

October, 2006

2646564

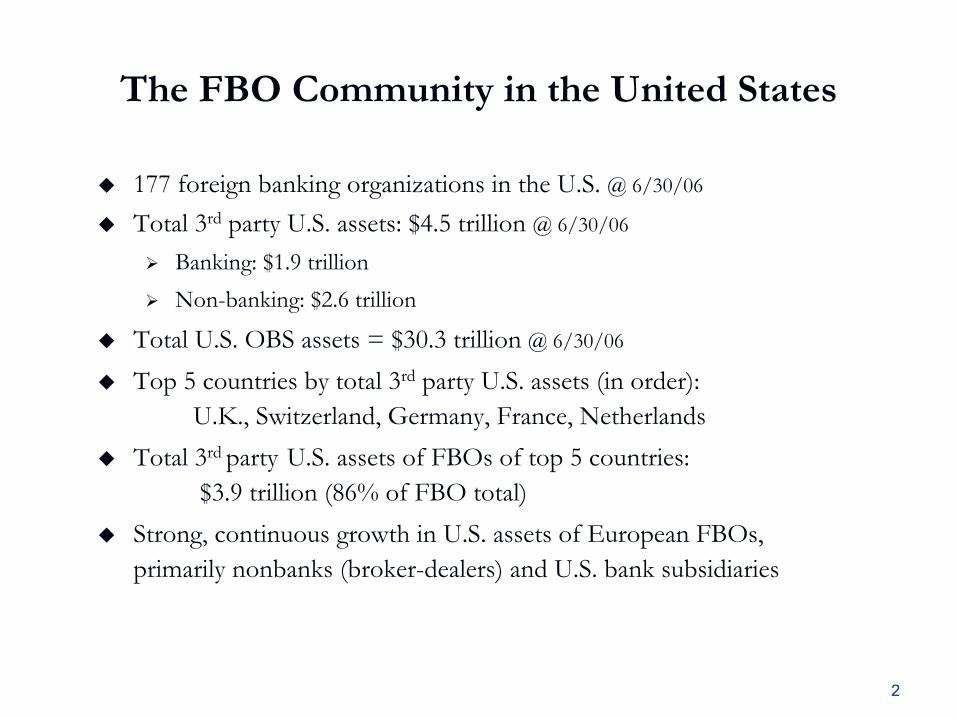

The FBO Community in the United States

177 foreign banking organizations in the U.S. @ 6/30/06

Total 3rd party U.S. assets: $4.5 trillion @ 6/30/06

Banking: $1.9 trillionNon-banking: $2.6 trillion

Total U.S. OBS assets = $30.3 trillion @ 6/30/06

Top 5 countries by total 3rd party U.S. assets (in order):U.K., Switzerland, Germany, France, Netherlands

Total 3rd party U.S. assets of FBOs of top 5 countries:$3.9 trillion (86% of FBO total)

Strong, continuous growth in U.S. assets of European FBOs,primarily nonbanks (broker-dealers) and U.S. bank subsidiaries

3646564

FBOs’ Share of U.S. Third Party Assets Are Concentrated in the Ten Largest FBOs

1995

72%28%

2006

OthersTop 10

39%61%

Top 10Others

4646564

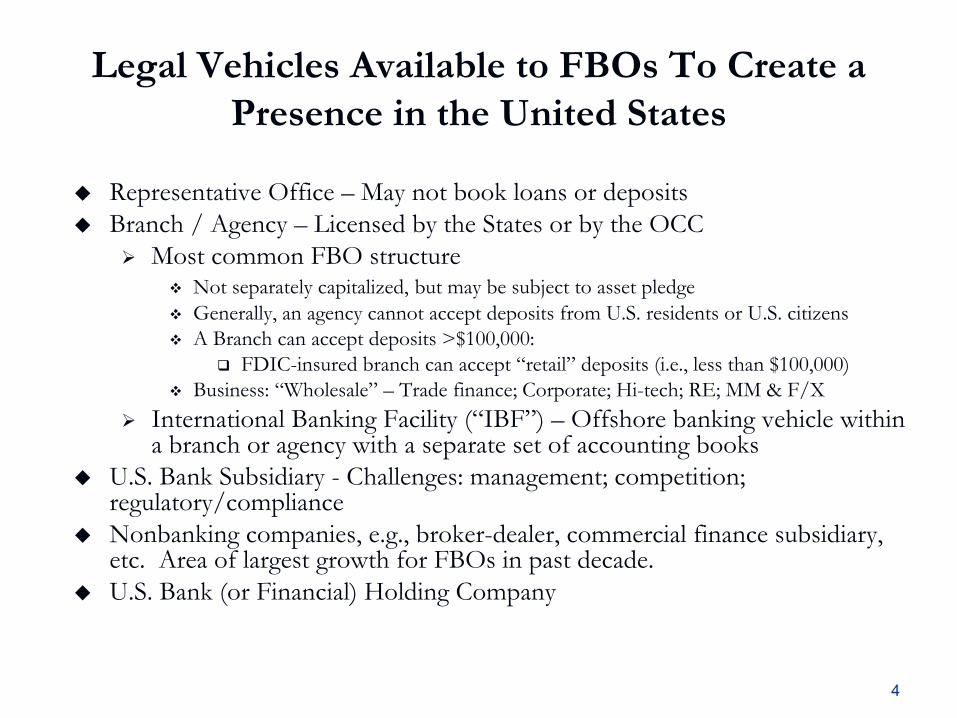

Legal Vehicles Available to FBOs To Create a Presence in the United States

Representative Office – May not book loans or depositsBranch / Agency – Licensed by the States or by the OCC

Most common FBO structureNot separately capitalized, but may be subject to asset pledgeGenerally, an agency cannot accept deposits from U.S. residents or U.S. citizensA Branch can accept deposits >$100,000:

FDIC-insured branch can accept “retail” deposits (i.e., less than $100,000)Business: “Wholesale” – Trade finance; Corporate; Hi-tech; RE; MM & F/X

International Banking Facility (“IBF”) – Offshore banking vehicle within a branch or agency with a separate set of accounting books

U.S. Bank Subsidiary - Challenges: management; competition; regulatory/complianceNonbanking companies, e.g., broker-dealer, commercial finance subsidiary, etc. Area of largest growth for FBOs in past decade.U.S. Bank (or Financial) Holding Company

5646564

U.S. Bank Supervisors:Who Supervises What – Domestic and Foreign

Federal Reserve (“FR”)Financial Holding Companies (“FHC”) and Bank Holding Companies (“BHC”) State member banksState licensed branches and agenciesEdge Act and Agreement CorporationsRepresentative OfficesNon-banks, except for broker-dealers (which SEC supervises)

The FR serves as the “umbrella” supervisor for foreign banking organizations (“FBO”)

StatesState-licensed branches and agenciesState member and nonmember banks

OCCFederally licensed branches and agenciesNational banks

FDICState nonmember banksInsured state licensed branches and agencies

6646564

Risk-Focused Supervisory Process

I. Understand the FBO

II. Assess the FBO’s Risks

III. Plan Supervisory Activities

IV. Determine the Overall Condition of the FBO’s U.S.

Operations

Risk-Focused Banking

Supervision

7646564

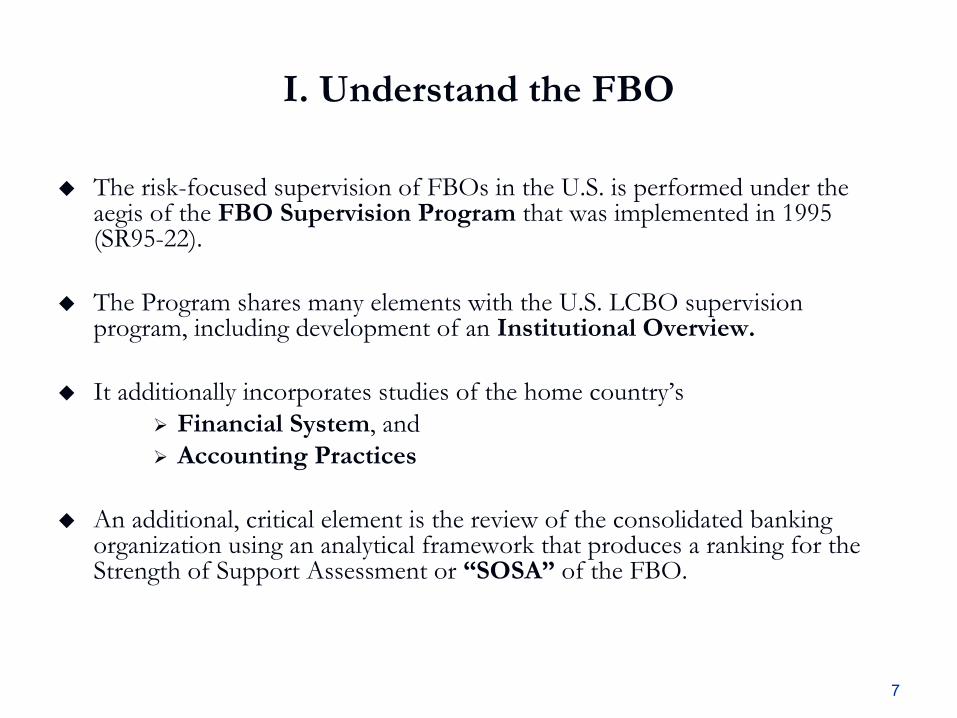

I. Understand the FBO

The risk-focused supervision of FBOs in the U.S. is performed under the aegis of the FBO Supervision Program that was implemented in 1995 (SR95-22).

The Program shares many elements with the U.S. LCBO supervision program, including development of an Institutional Overview.

It additionally incorporates studies of the home country’sFinancial System, andAccounting Practices

An additional, critical element is the review of the consolidated banking organization using an analytical framework that produces a ranking for the Strength of Support Assessment or “SOSA” of the FBO.

8646564

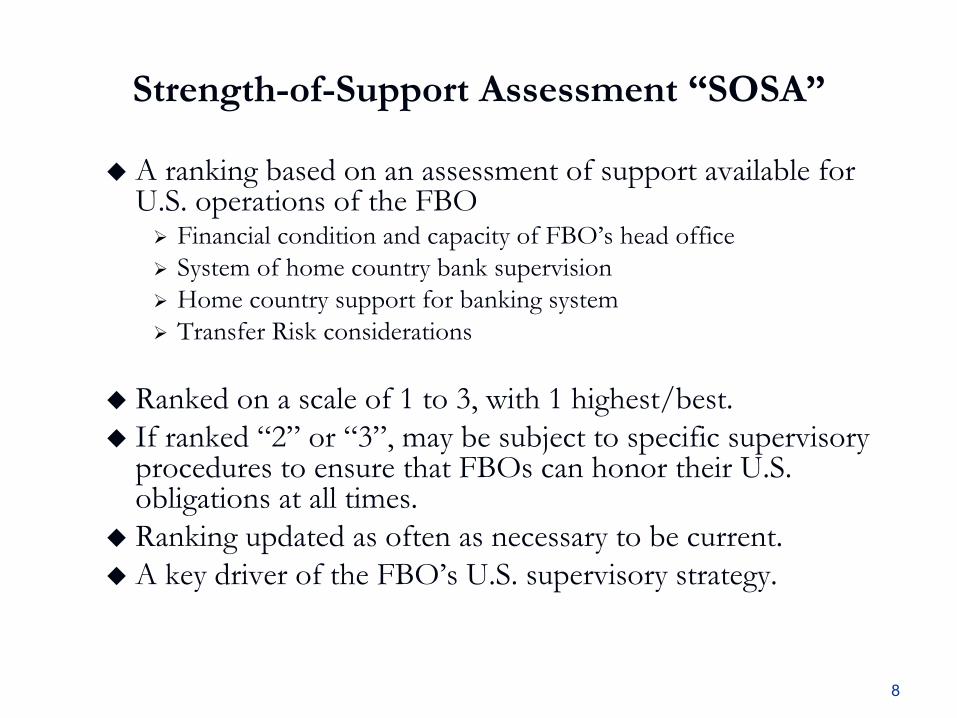

Strength-of-Support Assessment “SOSA”

A ranking based on an assessment of support available for U.S. operations of the FBO

Financial condition and capacity of FBO’s head officeSystem of home country bank supervisionHome country support for banking systemTransfer Risk considerations

Ranked on a scale of 1 to 3, with 1 highest/best.If ranked “2” or “3”, may be subject to specific supervisory procedures to ensure that FBOs can honor their U.S. obligations at all times.Ranking updated as often as necessary to be current.A key driver of the FBO’s U.S. supervisory strategy.

9646564

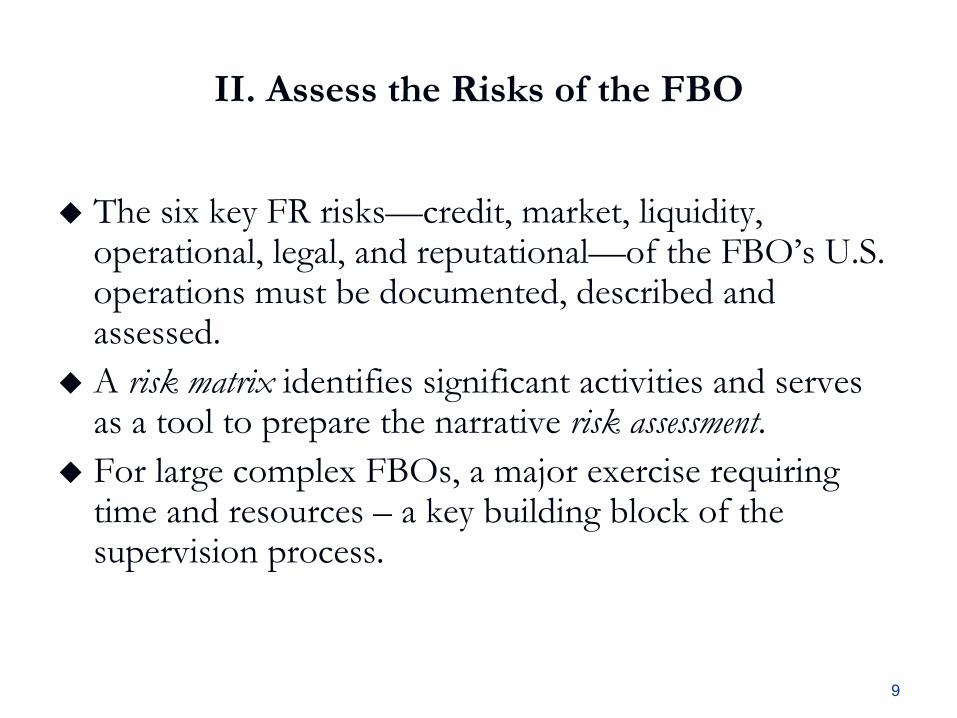

II. Assess the Risks of the FBO

The six key FR risks—credit, market, liquidity, operational, legal, and reputational—of the FBO’s U.S. operations must be documented, described and assessed. A risk matrix identifies significant activities and serves as a tool to prepare the narrative risk assessment.For large complex FBOs, a major exercise requiring time and resources – a key building block of the supervision process.

10646564

III. Plan Supervisory Activities

Risk-focused Approach

SOSA + Risk Assessment + Judgment Supervisory Plan+Examination Program

Prioritize supervisory resources based on riskCoordinate reviews and examinationsStrong focus on risk-management, compliance, and controls

11646564

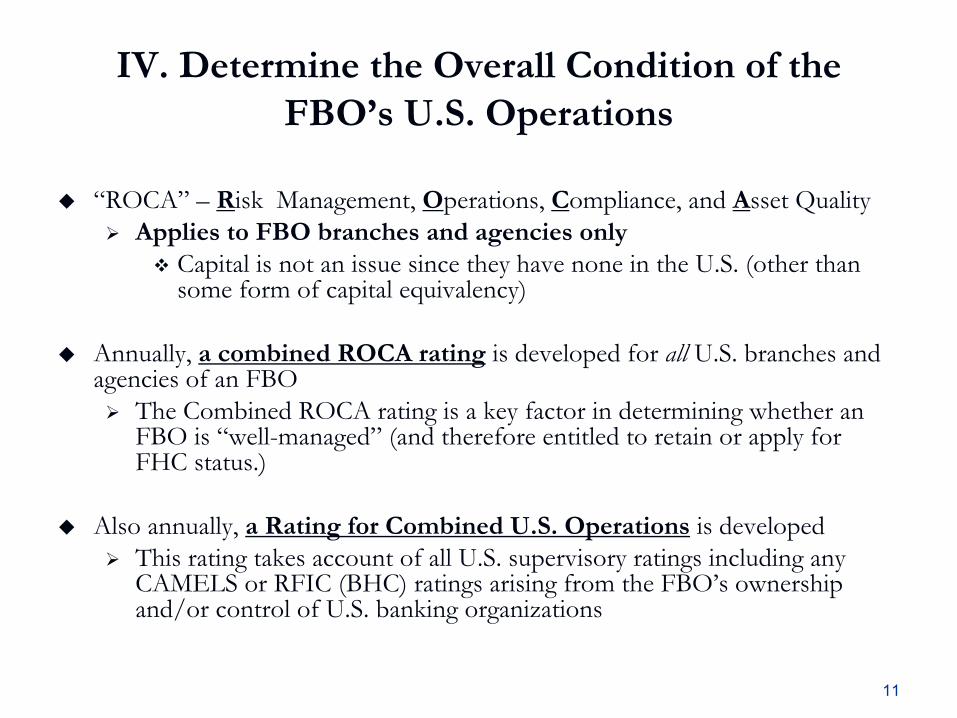

IV. Determine the Overall Condition of the FBO’s U.S. Operations

“ROCA” – Risk Management, Operations, Compliance, and Asset QualityApplies to FBO branches and agencies only

Capital is not an issue since they have none in the U.S. (other than some form of capital equivalency)

Annually, a combined ROCA rating is developed for all U.S. branches and agencies of an FBO

The Combined ROCA rating is a key factor in determining whether an FBO is “well-managed” (and therefore entitled to retain or apply for FHC status.)

Also annually, a Rating for Combined U.S. Operations is developedThis rating takes account of all U.S. supervisory ratings including any CAMELS or RFIC (BHC) ratings arising from the FBO’s ownership and/or control of U.S. banking organizations

12646564

Communicate the Results of the FBO Supervision Process

Annually, the Federal Reserve communicates in writing the results of the FBO supervision process to the:

Head Office Management of the FBOResident U.S. management of the FBOHome Country Supervisor of the FBO

What is communicated?1. A Summary of Condition of U.S. Operations2. Rating for Combined U.S. operations3. Combined ROCA rating4. Any corrective actions taken or to be taken5. The SOSA ranking

13646564

Supervisory Tools for Respondingto SOSA-related Concerns

A range of options…Monitor U.S. operations for areas of concern.Assure that contingent funding and liquidity are in place.Restraints on related party transactions.

Require a net due-to position.Asset maintenance to cover third parties.

SOSA 3

SOSA 1

Some manner of periodic reporting would be required for the above options.

14646564

Bank Secrecy Act/Anti-Money Laundering (1)Had steadily become a significant domestic bank supervisory issue in the U.S. since the mid-1980s

Has become a critical issue for the Federal Reserve and FBOs, especially since 9/11.

The USA Patriot Act (2001) provided many additional tools of enforcement and for intensified supervision over banks in the U.S.

The Federal Reserve expects all foreign banks in the U.S. to have in place a comprehensive BSA/AML program that must include

High-Level commitment and oversight by Directors and ManagementDetailed policies and proceduresEffective internal controlsIndependent testing (by internal or external auditors)Know-Your-Customer (“KYC”) and Customer Identification ProgramsTransaction Monitoring and Suspicious Activity ReportingTraining programs for staff and managementSOSA 3

Some manner of periodic reporting would be required for the above options.

15646564

Bank Secrecy Act/Anti-Money Laundering (2) Since 2001, the FR’s onsite examination process has identified arelatively large number of FBOs with significant BSA/AML deficiencies

Inadequate or no policies and proceduresInadequate or no filings of Suspicious Activity Reports (“SAR”)A lack of enhanced due diligence of higher risk customers and incorrespondent banking operationsPoor internal controls/audit that failed to surface BSA/AML problemsInadequate oversight by the head office and/or US regional managementInsufficient investment/resources in the U.S. compliance function

Many FBOs have been placed under formal and informal supervisoryactions

Some FBOs have been very slow to take action to remedy deficienciesThe timeline for correction is often slow, complex, and costly

BSA/AML manual, FFIEC, June 2005.SOSA 3

Some manner of periodic reporting would be required for the above options.

16646564

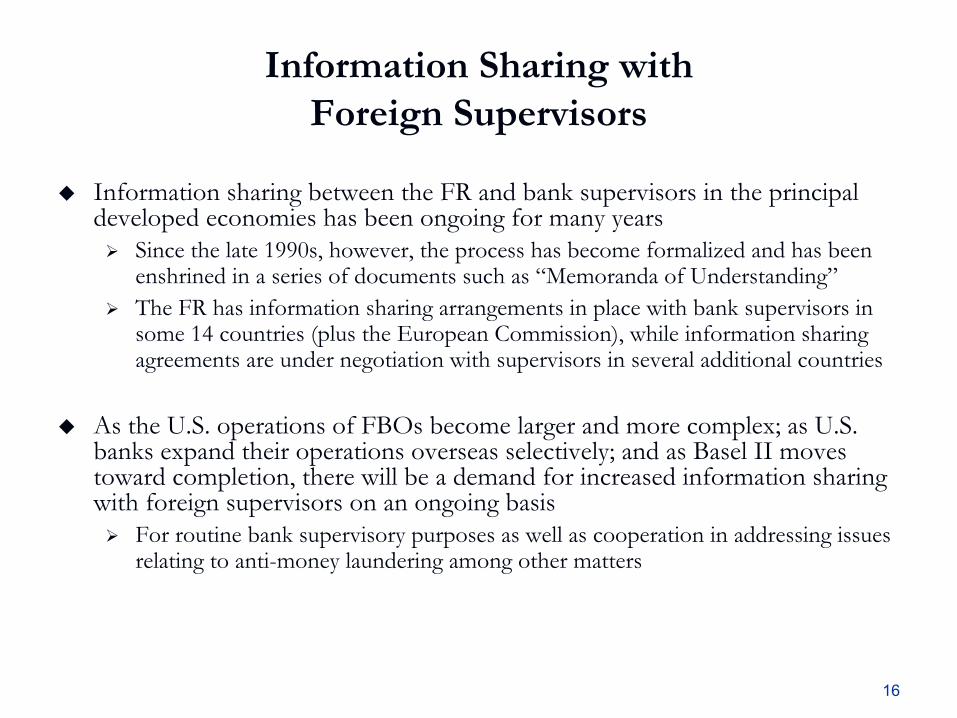

Information Sharing with Foreign Supervisors

Information sharing between the FR and bank supervisors in the principal developed economies has been ongoing for many years

Since the late 1990s, however, the process has become formalized and has been enshrined in a series of documents such as “Memoranda of Understanding”The FR has information sharing arrangements in place with bank supervisors in some 14 countries (plus the European Commission), while information sharing agreements are under negotiation with supervisors in several additional countries

As the U.S. operations of FBOs become larger and more complex; as U.S. banks expand their operations overseas selectively; and as Basel II moves toward completion, there will be a demand for increased information sharing with foreign supervisors on an ongoing basis

For routine bank supervisory purposes as well as cooperation in addressing issues relating to anti-money laundering among other matters

![BSMT378 Supervision - Syllabus - Spring 2017 Franco[1] · Supervision Today! Stephen P. Robbins, David A. DeCenzo ... Supervision Challenges Supervision Challenges Planning and Goal](https://static.documents.pub/doc/80x56/5b2eba097f8b9a594c8d9060/bsmt378-supervision-syllabus-spring-2017-franco1-supervision-today-stephen.jpg)